Sample Category Title

Daily Technical Outlook And Review

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

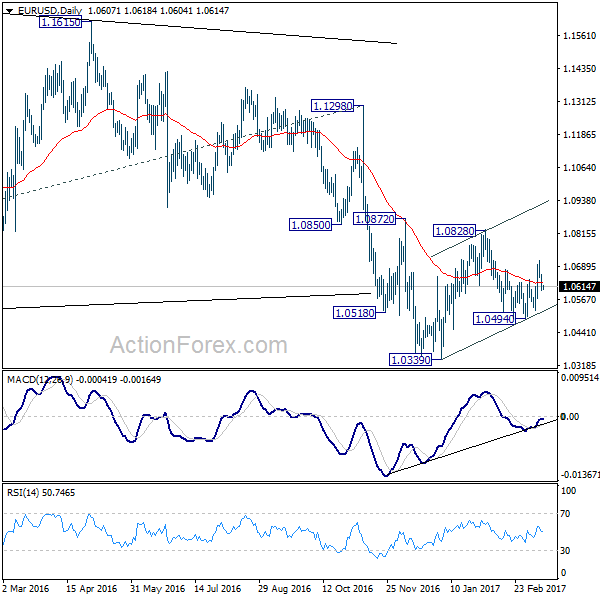

The EUR sustained further losses against its US counterpart during the course of yesterday's sessions, consequently bringing the pair down as far as the 1.06 handle into the closing bell. US PPI data came in hotter than expected, but failed to generate much of a reaction. Although1.06 boasts little higher-timeframe structure; it does merge closely with the 50.0% retracement value at 1.0603. Furthermore, the pair is likely to find some support around 1.06ish region with it having been a strong barrier of resistance on a number of occasions over the past few weeks (see green circle).

Our suggestions: With little higher-timeframe structure seen supporting the 1.06 zone, it's still a risky buy from here, in our opinion. As a result of this, we would strongly recommend waiting for a lower-timeframe confirming buy signal (see the top of this report) to form before considering a position. The first take-profit target is set at the nearby H4 resistance area coming in at 1.0636-1.0628.

In addition to the technicals, the much anticipated FOMC rate decision, economic projections and press conference is finally upon us today. According to the CME's FedWatch tool, there's over a 90% chance that we'll see an increase of 25bps. Therefore, remain alert during this time!

Data points to consider: US CPI report/US retail sales both scheduled for release at 12.30pm, FOMC rate decision, economic projections and press conference at 6-6.30pm GMT.

Levels to watch/live orders:

- Buys: 1.06 neighborhood ([waiting for a lower-timeframe confirming signal to form is advised] stop loss: dependent on where one confirms this level).

- Sells: Flat (stop loss: N/A).

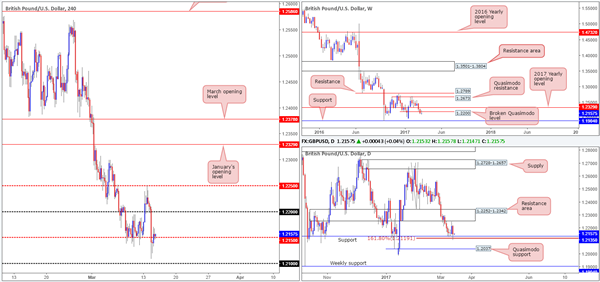

GBP/USD

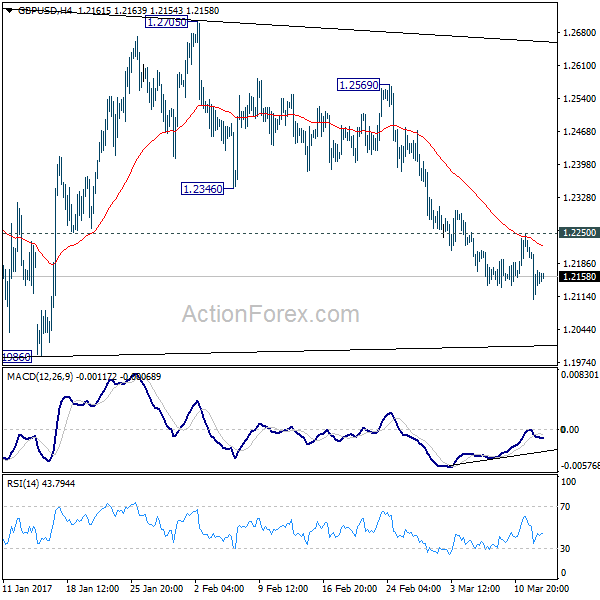

Weekly action is currently seen defending the underside of a recently broken weekly Quasimodo line coming in at 1.22. On the condition that the pair remains bearish beyond this hurdle, then the next port of call on this scale can be seen around weekly support coming in at 1.1904. Looking down to the daily timeframe, yesterday's candle tested daily support drawn from 1.2135/ the daily 161.8% Fib ext. at 1.2119 taken from the high 1.2706, consequently erasing all of Monday's gains!

Over on the H4 candles, we can see that the major plummeted lower going into the early hours of Europe yesterday, taking out both the 1.22 handle and the H4 mid-way support at 1.2150. Nevertheless, during the London morning segment, price did manage to bottom just ahead of the 1.21 handle and break back above the 1.2150 vicinity into the US open.

Our suggestions: Although the market does sport a rather bearish vibe right now, traders are in somewhat of a precarious position according to technical structure. A sell trade looks fantastic from the weekly timeframe, but at the same time, a potentially terrible idea on the daily timeframe. A buy trade on the other hand, appears sound from the daily timeframe, but risky from a weekly perspective.

With the much anticipated FOMC rate decision, economic projections and press conference upon us today, and UK employment data just around the corner, we feel opting to stand on the sidelines may very well be the better path to take. At least until the FOMC have had their way!

Data points to consider: UK employment report at 9.30am. US CPI report/US retail sales both scheduled for release at 12.30pm, FOMC rate decision, economic projections and press conference at 6-6.30pm GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

AUD/USD

After the pair broke beyond the H4 mid-way support hurdle at 0.7550 during the early hours of Monday's segment, price has remained somewhat directionless between 0.7550 and the overhead February opening level at 0.7577. Over on the weekly scale the weekly support area continues to buoy price, which could eventually prompt an approach up to the weekly trendline resistance extended from the high 0.8163. On the other side of the field, however, daily price is seen tickling the underside of a daily supply zone at 0.7632-0.7584. In order for weekly price to advance, this daily zone will have to be taken out. Of particular interest here is the daily supply at 0.7699-0.7656 seen above the current zone, given that it intersects with the aforementioned weekly trendline resistance.

Our suggestions: There is very little telling us to get involved with this market at the moment. While a break above February's opening base would be considered a bullish signal according to the weekly timeframe, we would be wary of buying here owing to the next upside target sitting at 0.76, and also the fact that price would still be trading within daily supply!

Our team feels that in light of the slightly restricted price action currently in view, the best position to take here is no position at all.

Data points to consider: US CPI report/US retail sales both scheduled for release at 12.30pm, FOMC rate decision, economic projections and press conference at 6-6.30pm GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

USD/JPY

During the course of yesterday's sessions the USD/JPY aggressively whipsawed through the 115 handle, tapped the underside of a nearby H4 supply zone at 115.37-115.18, and proceeded to selloff going into the London segment. With the H4 candles now currently finding support just ahead of the H4 mid-way number 114.50, where do we go from here? Well, according to the weekly timeframe, price remains on course to cross swords with a weekly resistance level seen at 116.08. Despite this, the daily candles are persistently holding ground within the walls of a daily resistance area coming in at 115.62-114.60.

Our suggestions: Based on the above notes, our team has their eye on the H4 113.84/114.20 (AB=CD H4 Fib ext. 127.2/161.8%) neighborhood for longs. Granted this does entail entering long just below the current daily resistance area, but what with weekly price suggesting further buying could be on the cards and the confluence (H4 trendline support extended from the high 115.62, 114 handle and H4 AB=CD approach [black arrows]) seen around 113.84/114.20, a bounce north from here is considered high probability, in our opinion. Be that as it may, we would not advise trading this zone around FOMC time today, as volatility is expected to be high.

Data points to consider: US CPI report/US retail sales both scheduled for release at 12.30pm, FOMC rate decision, economic projections and press conference at 6-6.30pm GMT.

Levels to watch/live orders:

- Buys: 113.84/114.20 ([waiting for a lower-timeframe confirming signal to form is advised – this will help avoid a fakeout down to the nearby H4 demand at 113.47-113.70] stop loss: dependent on where one confirms this level).

- Sells: Flat (stop loss: N/A).

USD/CAD

Recent action shows that the USD/CAD extended its bounce from the 1.3419/1.3434 H4 region (November/December/January's opening levels), lifting price up to within striking distance of the 1.35 handle. As you can see, the H4 candles have held ground within a H4 AB=CD Fib ext. 161.8%/127.2% area at 1.3507/1.3488 (taken from the low 1.3420) and is selling off as we write. This was a nice reversal zone. The thing that turned us off, however, was the fact that H4 momentum is still pointing to the upside and daily price had recently bounced from the top edge of a daily demand area chalked in at 1.3371-1.3437. The flipside to this, of course, is the weekly timeframe. The unit managed to marginally close beyond the 2017 yearly opening level at 1.3434. But since the close above this line was relatively minor, and taking into account that there is a nearby weekly double-top formation seen around the 1.3588 region (green circle), we do not consider 1.3434 to be out of the picture as a weekly resistance just yet!

Our suggestions: In view of the conflict seen between the higher-timeframe structures at the moment, we are wary of attempting to try and sell right now, despite the beautiful H4 AB=CD setup in play! And as for buying, this is also something we would not be comfortable taking part in, owing to the weekly structure mentioned above. With this in mind, opting to stand on the sidelines here may very well be the better path to take today.

Data points to consider: US CPI report/US retail sales both scheduled for release at 12.30pm, FOMC rate decision, economic projections and press conference at 6-6.30pm. Crude oil inventories at 2.30pm GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

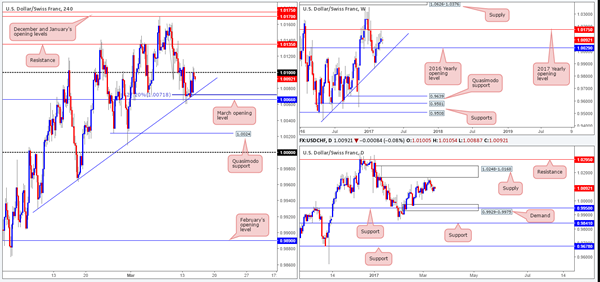

USD/CHF:

Try as it might, the Swissy could not muster enough strength to breach March's opening level at 1.0066. As highlighted in Monday's report, this number is bolstered by a H4 trendline support taken from the low 0.9929 and a H4 127.2% Fib ext. at 1.0071 (taken from the high 1.0160). As we write, nevertheless, the nearby 1.01 handle is providing resistance to this market. Whether or not this will be enough to push the unit back down to the 1.0066 perimeter is difficult to judge, since there is no higher-timeframe structures positioned nearby these levels.

Looking up to the weekly picture, price is seen trading mid-range between the 2017/2016 yearly opening levels at 1.0175/1.0029. By the same token, daily action is also currently seen trading mid-range between daily supply at 1.0248-1.0168 and daily demand pegged at 0.9929-0.9975, which happens to intersect with a daily support level seen at 0.9950.

Our suggestions: A break above 1.01 boasts little room for maneuver with H4 resistance seen at 1.0135. A break below 1.0066 on the other hand may call for price to challenge the H4 Quasimodo support at 1.0024, followed closely by parity (1.0000). To that end, we feel there's a possibility for shorts beyond 1.0066 today if a retest of this number as resistance is seen that's bolstered by a lower-timeframe sell signal (see the top of this report). However, do remain vigilant today since we have the much anticipated FOMC rate decision, economic projections and press conference just around the corner.

Data points to consider: US CPI report/US retail sales both scheduled for release at 12.30pm, FOMC rate decision, economic projections and press conference at 6-6.30pm. CHF PPI data at 8.15am GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for price to engulf 1.0066 and then look to trade any retest seen thereafter (waiting for a lower-timeframe confirming signal to form following the retest is advised] stop loss: dependent on where one confirms the level).

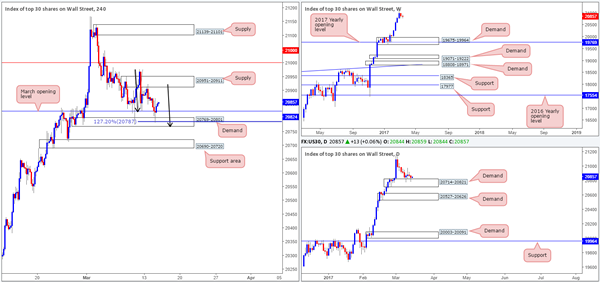

DOW 30

As can be seen from the H4 chart this morning, the DOW momentarily surpassed March's opening level at 20824, bounced off a H4 AB=CD 127.2% Fib ext. at 20787 (seen lodged within a H4 demand at 20769-20801), and ended the day closing at 20844. What this move also accomplished was a relatively nice-looking daily buying tail printed from the top edge of a daily demand zone seen at 20714-20821.

With equities still trading nearby record highs, there's a good chance that this unit could stretch higher today and potentially even break through H4 supply at 20951-20911. Should price retest March's opening base line sometime today, we would consider a long in this market on the condition that a reasonably sized H4 bullish rotation candle is seen. However, do remain vigilant today since we have the much anticipated FOMC rate decision, economic projections and press conference just around the corner.

Our suggestions: Watch for potential longs off the 20824 barrier today. In the event that one manages to pin down a setup from here, we'd look to trail the position up to the aforementioned H4 supply, followed closely by the 21000 mark.

Data points to consider: US CPI report/US retail sales both scheduled for release at 12.30pm, FOMC rate decision, economic projections and press conference at 6-6.30pm GMT.

Levels to watch/live orders:

- Buys: 20824 region ([waiting for a reasonably sized H4 bull candle to form here before pulling the trigger is advised] stop loss: ideally beyond the trigger candle).

- Sells: Flat (stop loss: N/A).

GOLD

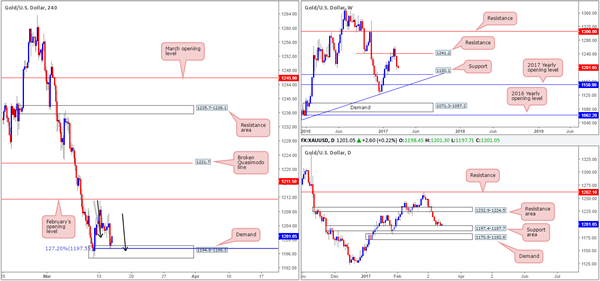

Following the daily bearish selling wick printed on Monday, we saw the yellow metal take a hit during yesterday's trading, bringing price back to the top edge of the daily support area at 1197.4-1187.7. What is also quite notable from a technical perspective is the H4 bullish AB=CD 127.2% pattern that completed within the walls of a H4 demand zone drawn from 1194.8-1198.3. As we can all see, price is rallying from this base. How far price will advance from here is, well, anybody's guess. The reason we say this is simply due to the weekly timeframe indicating that price could potentially continue driving lower until we reach the weekly support level drawn from 1180.1.

Our suggestions: While there is some conflict seen between the higher timeframes at the moment, there's a good chance that H4 flow will reach the 1204.0 region before stalling. Well done to any of our readers who managed to get long from the tip of the H4 AB=CD formation!

Unless the H4 candles retest the current H4 demand sometime today (at this point we would consider entering long from here assuming that we have the backing of a lower-timeframe buy signal [see the top of this report]), we will remain flat until after today's FOMC event.

Levels to watch/live orders:

- Buys: 1194.8-1198.3 ([waiting for a lower-timeframe confirming signal to form is advised prior to pulling the trigger here] stop loss: dependent on where one confirms this area).

- Sells: Flat (stop loss: N/A).

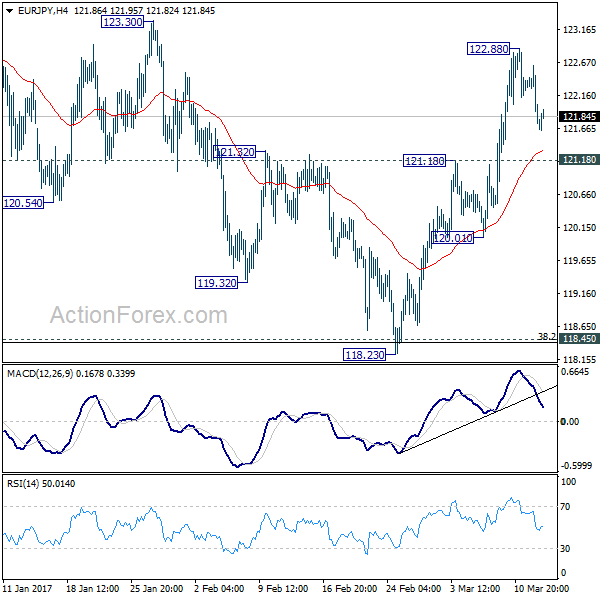

EUR/JPY Daily Outlook

Daily Pivots: (S1) 121.34; (P) 121.98; (R1) 122.31; More...

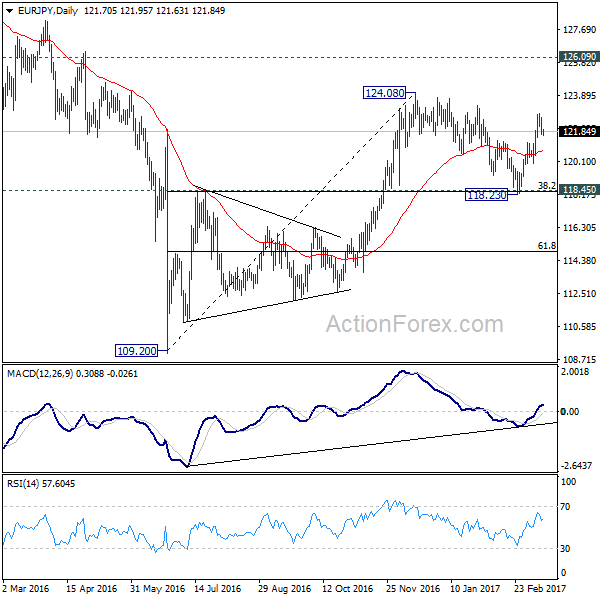

Intraday bias in EUR/JPY remains neutral as consolidation from 122.88 temporary top continues. Deeper retreat cannot be ruled out but downside should be contained by 121.18 resistance turned support and bring another rally. Above 122.88 will target 124.08. Decisive break there will extend larger rise from 109.20 and target 126.09 key resistance next.

In the bigger picture, current development suggests that medium term rise from 109.20 is still in progress. Focus is now on 126.09 key resistance level. Sustained break will confirm completion of the whole decline from 149.76. And rise from 109.20 is of the same degree as the fall from 149.76. In such case, further rally would be seen to 104.04 resistance and possibly above before topping. Meanwhile, rejection from 126.09 will extend the fall from 149.76 through 109.209 low.

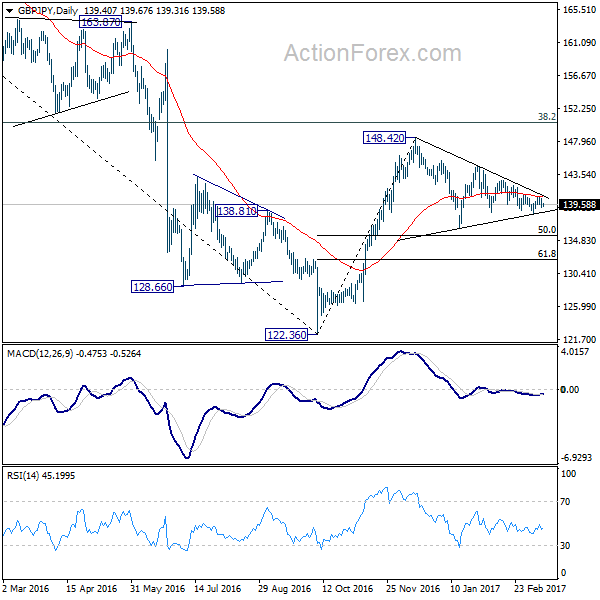

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.91; (P) 139.67; (R1) 140.19; More...

.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern with a test on 122.36 low next. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement at 167.78.

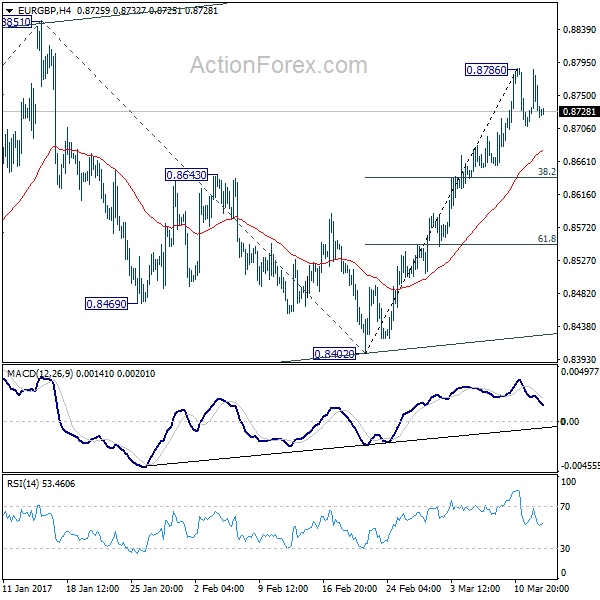

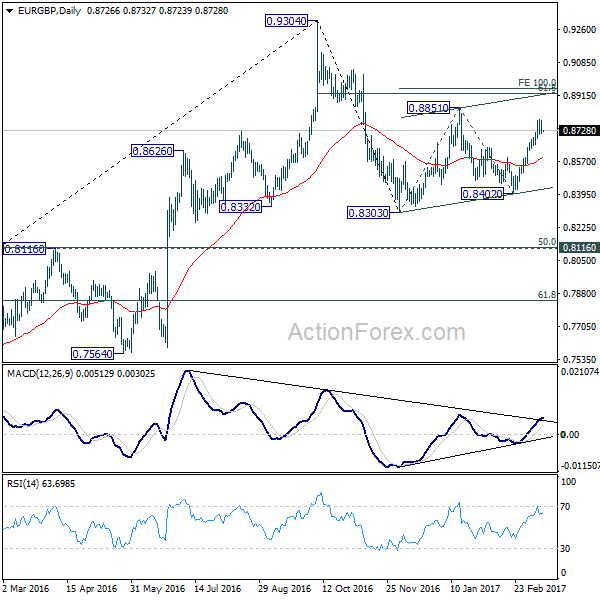

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8697; (P) 0.8741; (R1) 0.8768; More...

EUR/GBP is still bounded in consolidation below 0.8786 and intraday bias remains neutral for the moment. Another fall could be seen as the consolidation extends. But downside should be contained by 38.2% retracement of 0.8402 to 0.8786 at 38.2% retracement of 0.8402 to 0.8786 at 0.8639 and bring another rise. Above 0.8786 will target 0.8851 resistance and above. However, price actions from 0.8303 are seen as the second leg of the corrective pattern from 0.9304. Hence, we'd expect strong resistance from 100% projection of 0.8303 to 0.8851 from 0.8402 at 0.8950 to limit upside.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).

European Open Briefing

Global Markets:

- Asian stock markets: Nikkei down 0.20 %, Shanghai Composite gained 0.05 %, Hang Seng lost 0.30 %, ASX 200 fell 0.35 %

- Commodities: Gold at $1201 (-0.15 %), Silver at $16.95 (+0.15 %), WTI Oil at $48.50 (+1.60 %), Brent Oil at $51.65 (+1.40 %)

- Rates: US 10 year yield at 2.60, UK 10 year yield at 1.23, German 10 year yield at 0.45

News & Data:

- New Zealand Current Account (NZD) (Q4): -2.335bn (est -2.425bn, prev -4.891bn)

- Australia Westpac Consumer Confidence SA (Mar): +0.1% @ 99.7 (prev +2.3% @ 99.6)

- Australia New Motor Vehicle Sales (MoM) (Feb): -2.70% (prev 0.60%)

- Australia New Motor Vehicle Sales (YoY) (Feb): -4.10% (prev -0.90%)

- PBOC sets USD/CNY central rate at 6.9115 (vs. yesterday at 6.9118)

- Asian stocks slip, Fed's decision day makes investors wary – RTRS

- Dollar off recent highs ahead of expected Fed rate hike – RTRS

Markets Update:

The Dollar is bid ahead of the Federal Reserve rate decision tonight. EUR/USD traded as low as 1.0605 yesterday, and price action is looking increasingly bearish. Key intraday support is noted at 1.0570 and 1.0520.

Meanwhile, USD/JPY tested Friday's high at 115.40 yesterday. While it failed to break above it, it remains well supported. In Asia, the pair consolidated in a 114.65-85 range. Should it break above 115.40 resistance, a rally towards 117 seems likely.

The US central bank will very likely increase rates by 25bps, and signal that further rate hikes could follow this year. Much will depend on the new forecasts and the tone of the FOMC though. Should they remain rather cautious overall, the Dollar could come under pressure. Since a rate hike tomorrow is almost 100 % priced in, that alone will not support the Dollar by much.

Upcoming Events:

- 07:45 GMT – French CPI

- 08:15 GMT – Swiss PPI

- 09:30 GMT – UK Unemployment Rate

- 09:30 GMT – UK Claimant Count Change

- 09:30 GMT – UK Average Hourly Earnings

- 10:00 GMT – Italian CPI

- 12:30 GMT – US CPI

- 12:30 GMT – US Retail Sales

- 14:00 GMT – US NAHB Housing Market Index

- 14:30 GMT – US Crude Oil Inventories

- 18:00 GMT – Federal Reserve Rate Decision

- 18:00 GMT – FOMC Statement

- 18:30 GMT – FOMC Press Conference

- 21:45 GMT – New Zealand GDP

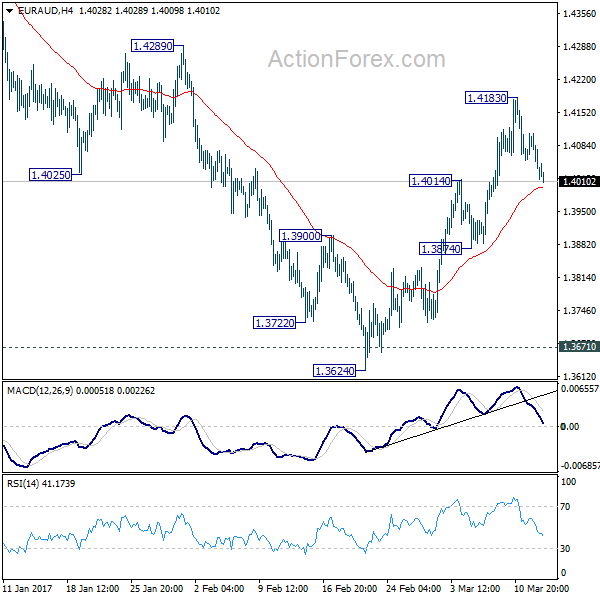

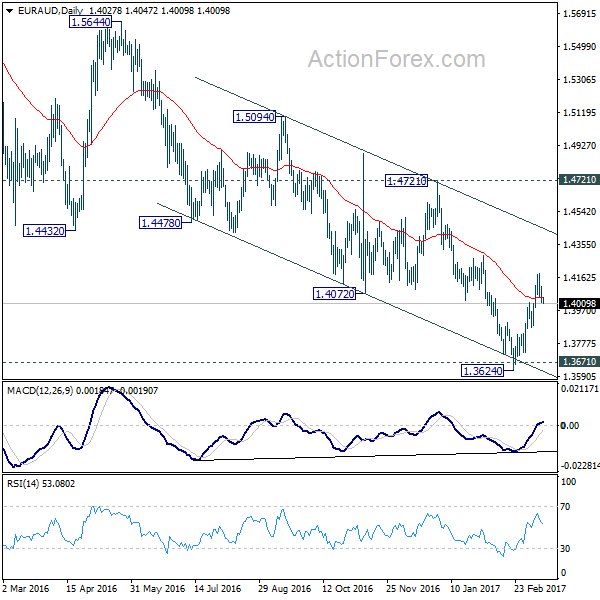

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.3992; (P) 1.4051; (R1) 1.4087; More...

Intraday bias in EUR/AUD remains neutral as the correction from 1.4183 continues. Deeper retreat could be seen but downside should be contained by 1.3874/4014 support zone and bring another rally. As noted before, we're favoring the case of medium term trend reversal defending key support level at 1.3671, on bullish convergence condition in daily MACD Above 1.4183 will turn bias back to the upside for 1.4289 resistance. Sustained break there will affirm our bullish view and target 1.4721 key resistance next. However, break of 1.3874 will dampen our view and turn bias to the downside for 1.3624 low.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. We'd expect strong support from 1.3671 key level to contain downside and bring rebound. Up trend from 1.1602 should not be finished and will resume later. Break of 1.4721 resistance will indicate completion of such correction and turn outlook bullish for retesting 1.6587 high. However, sustained break of 1.3671 will invalidate our bullish view and would turn focus back to 1.1602 long term bottom.

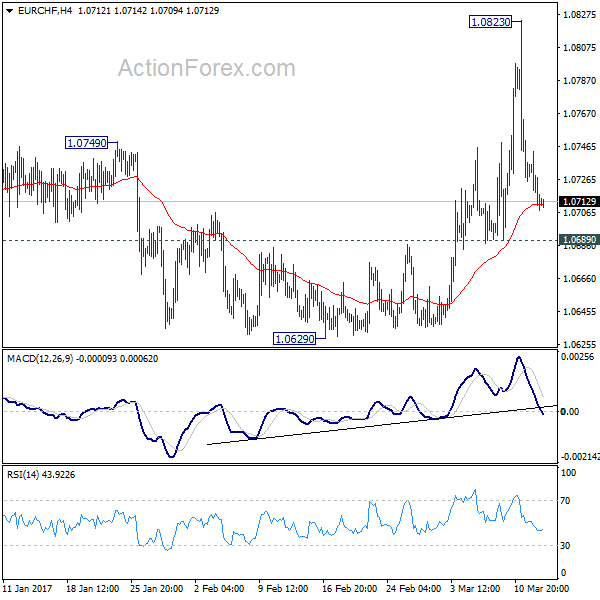

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0700; (P) 1.0722; (R1) 1.0733; More...

Intraday bias in EUR/CHF remains neutral for the moment. With 1.0689 minor support intact, we continue to favor the case of trend reversal, on bullish convergence condition in daily MACD, after defending 1.0620 key support level. That is, correction from 1.1198 could have completed. Above 1.0823 will target 1.0897 resistance next. However, break of 1.0689 support will dampen our view and turn focus back to 1.0629 low again.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Decisive break of 1.0897 resistance should confirm that it's completed. And in that case, larger up trend is resuming for another high above 1.1198. Meanwhile, sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0581; (P) 1.0621 (R1) 1.0644; More.....

Intraday bias in EUR/USD remains mildly on the downside for 1.0494 support. Overall, price actions from 1.0339 are seen as a corrective pattern. Break of 1.0494 will revive that case that such correction is completed. And in such case, deeper decline should be seen to retest 1.0339. Meanwhile, above 1.0713 will turn bias back to the upside for 1.0828 and above to extend the correction from 1.0339.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2100; (P) 1.2161; (R1) 1.2213; More...

Intraday bias in GBP/USD remains on the downside as the fall from 1.2705 is in progress. Deeper decline would be seen to retest 1.1946/86 support zone. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. Break of 1.1946 will confirm our bearish view. On the upside, above 1.2250 minor resistance will turn bias neutral again. But outlook will stay bearish as long as 1.2346 support turned resistance holds.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

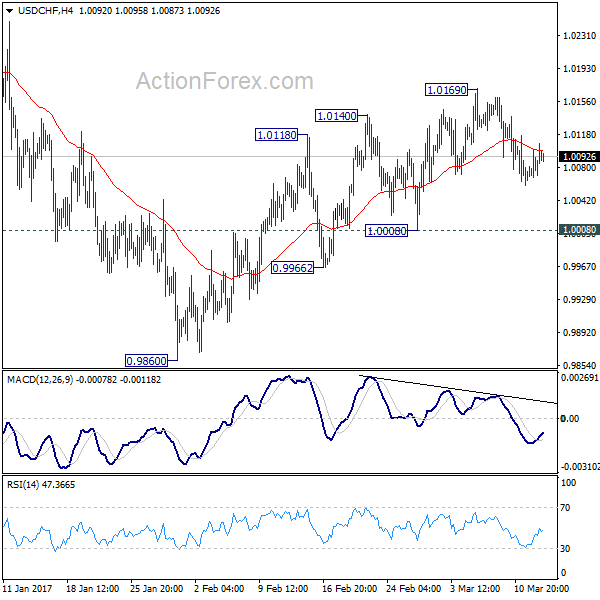

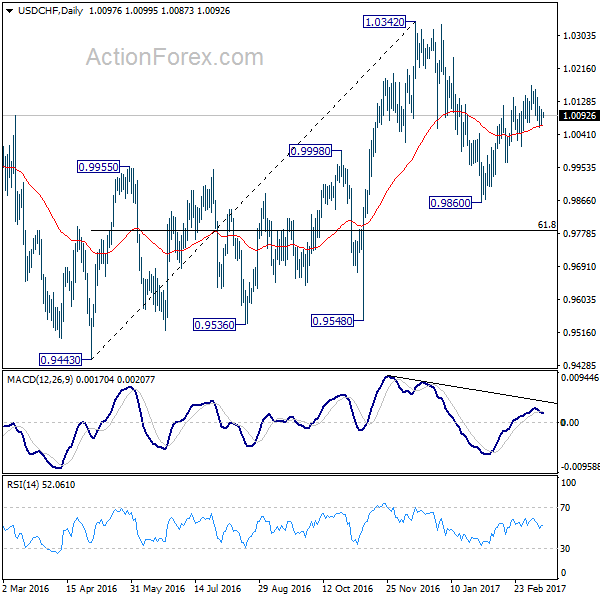

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0076; (P) 1.0092; (R1) 1.0116; More.....

Intraday bias in USD/CHF remains neutral for the moment as the pull back from 1.0169 continues. At this point, with 1.0008 support intact, further rise is mildly in favor. Above 1.0169 will turn bias to the upside and target a test on 1.0342 resistance. Based on neutral medium term outlook, we'd be cautious on topping below 1.0342. On the downside, break of 1.0008, however, will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.