Sample Category Title

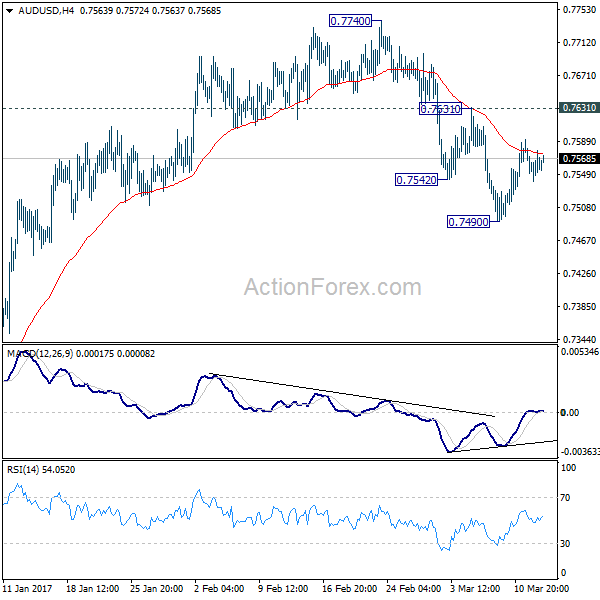

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7539; (P) 0.7559; (R1) 0.7578; More...

AUD/USD's correction from 0.7490 is still in progress and intraday bias stays neutral first. We'd continue to expect recovery to be limited by 0.7631 resistance and bring fall resumption. As noted before, rise from 0.7150 has completed at 0.7740 already. Below 0.7490 will turn bias back to the downside and target 0.7144/7158 support zone. However, break of 0.7631 resistance will dampen our bearish view and turn bias back to the upside for 0.7740 instead.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8185) and above.

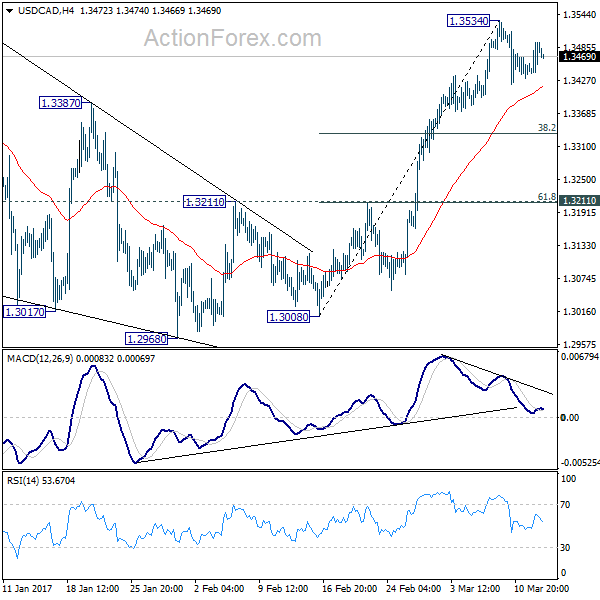

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3446; (P) 1.3470; (R1) 1.3503; More...

USD/CAD is still bounded in consolidation below 1.3534 and intraday bias remains neutral for the moment. Another fall cannot be ruled out as the consolidation extends. But downside should be contained by 38.2% retracement of 1.3008 to 1.3534 at 1.3333 and bring another rally. Above 1.3534 will turn bias to the upside for retesting 1.3598 high next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg, started from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Markets Holding Breath ahead of FOMC, Fed Projections is the Key

Markets are holding their breath as the highly anticipated FOMC meeting awaited. DJIA's recovery lost steam and closed down -44.11 pts, or -0.21%, at 20837.37 after breaching 20800 briefly. S&P 500 also lost -8.02 pts, or -0.34%, to close at 2365.45. Both indices are holding above last week's low at 20777.16 and 2354.54 so far. 10 year yield stayed in tight range below recent resistance at 2.621 and closed down -0.013 at 2.595. Gold continued to engage in range trading around 1200. WTI crude oil dived sharply to as low as 47.09 but recovered to 48.50 for the moment.

Dollar index trading mildly higher to 101.70 at the time of writing, holding above 100.66 near term support. In the currency market, despite some volatility, major pairs and crosses are generally stuck in last week's range, except GBP/CHF. General weakness is seen in Euro for the week as the common currency pared back post ECB gains. Yen follows as the second weakest as its rebound attempt quickly falters.

Fed to upgrade economic projections

Fed is widely expected to hike federal funds rate by 25bps to 0.75-1.00%. The rate hike itself is well priced in. Thus the focus will be largely on three things, the FOMC statement, new economic projection, and Fed chair Janet Yellen's press conference. Markets are looking through today's hike and are eager to get the hints on what Fed would do next. The table below showed FOMC's median projections back in December.

Federal funds rate are projected to be at 1.4% by the end of 2017, 2.1% by the end of 2018. They equivalent to 3 rate hikes in total for this year and 2-3 hikes next year. Any upward revision to the numbers will imply a faster path. In particular, some analysts are anticipating a meaningful revision to 2018's projections to reflect a firmer chance of 3 hikes. Meanwhile, the markets will also look closely to the revisions to economic projections, with focuses on the core PCE number for this year and next.

More on FOMC:

- Upcoming Rate Hikes And 2018 Median Dot Plot In Focus

- FOMC Preview - It's All in the Dots

- Fed Expected to Raise US Interest Rates

- FOMC Preview: Fed to Maintain Signal of Three Hikes this Year

UK employment, US CPI and retail sales featured

Elsewhere, New Zealand current account deficit narrowed to NZD 2.3b in Q4. Australia Westpac consumer confidence rose 0.1% in March. UK employment data will be a main focus in European session. Swiss will release PPI and Eurozone will release employment. US will release Empire state manufacturing, CPI, retail sales and NAHB housing market index.

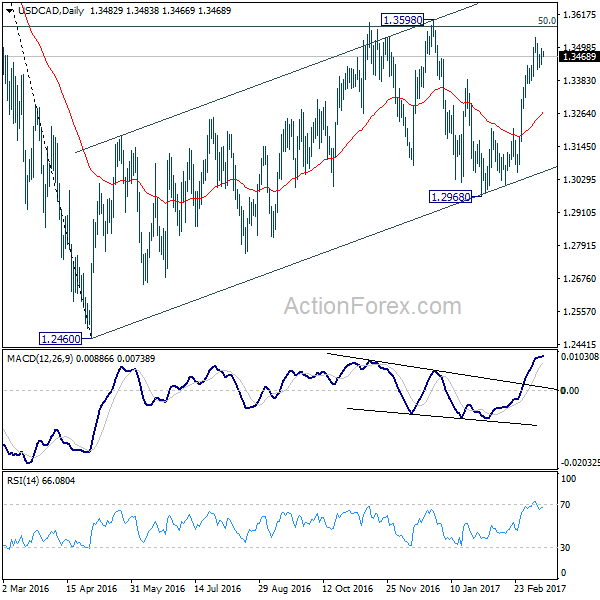

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3446; (P) 1.3470; (R1) 1.3503; More...

USD/CAD is still bounded in consolidation below 1.3534 and intraday bias remains neutral for the moment. Another fall cannot be ruled out as the consolidation extends. But downside should be contained by 38.2% retracement of 1.3008 to 1.3534 at 1.3333 and bring another rally. Above 1.3534 will turn bias to the upside for retesting 1.3598 high next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg, started from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account Balance (NZD) Q4 | -2.3B | -2.43B | -4.89B | -5.03B |

| 23:30 | AUD | Westpac Consumer Confidence Mar | 0.10% | 2.30% | ||

| 04:30 | JPY | Industrial Production M/M Jan F | -0.80% | -0.80% | ||

| 08:15 | CHF | Producer & Import Prices M/M Feb | 0.40% | 0.40% | ||

| 08:15 | CHF | Producer & Import Prices Y/Y Feb | 0.80% | |||

| 09:30 | GBP | Jobless Claims Change Feb | 3.2K | -42.4K | ||

| 09:30 | GBP | Claimant Count Rate Feb | 2.10% | |||

| 09:30 | GBP | ILO Unemployment Rate (3M) Jan | 4.80% | 4.80% | ||

| 09:30 | GBP | Average Weekly Earnings 3M/Y Jan | 2.40% | 2.60% | ||

| 10:00 | EUR | Eurozone Employment Q/Q Q4 | 0.20% | 0.20% | ||

| 12:30 | USD | Empire State Manufacturing Index Mar | 15 | 18.7 | ||

| 12:30 | USD | CPI M/M Feb | 0.00% | 0.60% | ||

| 12:30 | USD | CPI Y/Y Feb | 2.60% | 2.50% | ||

| 12:30 | USD | CPI Core M/M Feb | 0.20% | 0.30% | ||

| 12:30 | USD | CPI Core Y/Y Feb | 2.30% | |||

| 12:30 | USD | Advance Retail Sales Feb | -0.10% | 0.40% | ||

| 12:30 | USD | Retail Sales Less Autos Feb | -0.10% | 0.80% | ||

| 14:00 | USD | NAHB Housing Market Index Mar | 65 | |||

| 14:00 | USD | Business Inventories Jan | 0.30% | 0.40% | ||

| 14:30 | USD | Crude Oil Inventories | 8.2M | |||

| 18:00 | USD | FOMC Rate Decision | 1.00% | 0.75% |

Foreign Exchange Market Commentary

EUR/USD

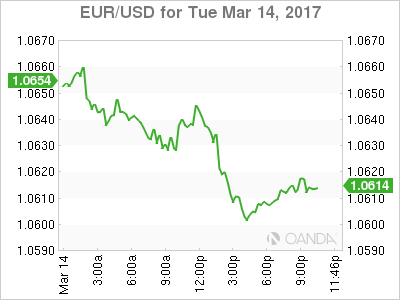

The EUR/USD pair closed the day at the lower end of its daily range, with the American dollar closing the day mixed, but up against its European rivals. The common currency's retracement was due to technical factors, as the pair was rejected from a major resistance area around 1.0710 tested earlier this week, although soft data coming from the EU also weighed. Industrial Production in the EU rose by less than expected in January, posting a modest 0.9% advance monthly basis, against expectations of a 2.0% advance, edging up 0.6% when compared to a year earlier. The German ZEW survey showed that the economic sentiment improved slightly, up to 12.8 from previous 10.4, while for the EU sentiment saw a largest improvement up to 5.6 from previous 17.1. In the US, however, things were a bit better, as the Producer Price Index for final demand increased 0.3% in February, seasonally adjusted, while on an unadjusted basis, it rose by 2.2% in the 12 months to February, the largest advance in almost five years.

Market is now focused on whatever the FED will offer this Wednesday, as the US Central Bank is largely expected to announce a 25bps rate hike, which is fully priced in at this point. Investors will therefore be looking for hints of what's next on monetary policy whether to buy or sell the greenback.

Technically, the 4 hours chart presents an increasing bearish potential, as the price has pulled below a bullish 20 SMA, while now extending below a horizontal 200 SMA, whilst technical indicators head sharply lower, entering negative territory ahead of the Asian opening. The pair however, holds around 1.0630, and much of the upcoming direction will depend solely on market's reaction to the Fed, with either a break below 1.0565, or above 1.0720 setting the tone for the rest of the week. Still, political uncertainty will likely kick in after the market settles, preventing the pair from advancing much in either direction, situation that will likely persist until the end of the summer.

Support levels: 1.0600 1.0565 1.0520

Resistance levels: 1.0660 1.0710 1.0755

USD/JPY

The USD/JPY pair closed the day marginally lower, still confined to a tight range ahead of the Fed's monetary policy decision this Wednesday. The pair peaked at 115.19 early London, but quickly retreated, undermined by falling stocks and a modest retracement from 2017 highs in US Treasury yields. The 10-year note benchmark settled at 2.58% after flirting with 2.62% earlier this week. The Bank of Japan will also have its monetary policy meeting these days, early Thursday, but the pair's direction will depend on the US Central Bank. From a technical point of view, the pair has been quite reluctant to advance, despite positive US data and central bankers' promises, with the pair unable to settle above 115.00 for over a month. A spike up to 115.50 on Friday settled a critical resistance, as it would take a break above it to confirm a more sustainable recovery for the following sessions. In the 4 hours chart, the pair is pretty much neutral, as the price has bounced modestly from the 23.6% retracement of the latest bullish run, around 114.50, whilst technical indicators have gyrated higher, but remain below their mid-lines. A disappointing Fed could see the pair breaking through 114.00, opening doors for a slide down to 112.60.

Support levels: 114.50 114.15 113.70

Resistance levels: 115.10 115.50 115.85

GBP/USD

The GBP/USD pair fell to 1.2108, its lowest since early January when PM Theresa May announced the government's decision to go for a "hard-Brexit," with the Pound undermined by the imminent launch of the Art. 50 of the Lisbon Treaty. In a short session late Monday, the House of Common cleared PM May´s way towards the Brexit, reverting the amendments voted in the House of Lords. Much of this decline is due to the fact that once the UK begins negotiations, things will be out of the UK control, and any benefit the kingdom could obtain from this divorce will depend mostly on the good will of the EU. In the data front, the Conference Board Leading Economic Index for the UK increased 0.4% in January 2017 to 113.5, but more relevant the UK will release its latest employment figures this Wednesday, with upward wage pressure expected to ease some, and the unemployment rate expected to remain unchanged at 4.8%. Technical readings in the 4 hour chart favor additional declines, as the intraday recovery was contained by selling interest around 1.2165 and a horizontal 20 SMA, whilst technical indicators have quickly turned south after a modest advance, with the RSI currently at 43, anticipating some further slides on a break below 1.2110.

Support levels: 1.2110 1.2070 1.2035

Resistance levels: 1.2165 1.2200 1.2245

GOLD

Gold prices attempted to advance this Tuesday, but were unable to sustain tepid intraday gains, with spot ending the day pretty much unchanged at $1,202.80 a troy ounce. The bright metal held steady as investors wait for the Fed's monetary policy meeting outcome, currently trapped between in a rock and a hard place, as opposing to Fed's decision to raise rates, which should result in the metal plunging, is the underlying political risk surrounding Europe and the US, something that usually benefits gold. Physical demand in India remains subdued, with prices down for fifth consecutive day in the country amid sluggish industrial demand. From a technical point of view, the risk is towards the downside, as the commodity posted a lower low and a lower high daily basis, whilst the 20 DMA keeps gaining bearish strength far above the current level and technical indicators in the daily chart remain near oversold readings, although lacking directional strength. In the 4 hours chart, the price kept hovering around a horizontal 20 SMA, whilst technical indicators have turned sharply lower after entering positive territory, with the RSI anticipating some further declines as the indicator stands at 41. The immediate support is the 50% retracement of the latest daily bullish run at 1,193.00, the level to break to confirm additional slides during the upcoming sessions.

Support levels: 1,197.10 1,188.20 1,180.50

Resistance levels: 1,210.00 1,218.50 1,226.70

WTI CRUDE

West Texas Intermediate crude oil futures fell to a fresh 2017 low of $47.08 a barrel, resuming its decline after Monday's consolidation, undermined by news coming from the US, as the EIA drilling productivity report released late Monday points for further increases in shale production next April. Also, the OPEC´s monthly report said oil stocks rose in January some 280 million barrels above the five-year average, making it tough for the organization to curb prices and clear the worldwide glut that affected the market for over two years already. WTI finished the day around 47.70, and despite the oversold conditions seen in technical readings in the daily chart, with the RSI indicator still heading south around 21, the risk remains towards the downside, as in the same chart, an early advance was contained below the 200 SMA broken late last week. In the 4 hours chart, a bearish 20 SMA capped the upside, currently at 48.40, while technical indicators have lost their downward strength, but remain within negative territory, with the RSI currently at 24.

Support levels: 48.00 47.30 46.65

Resistance levels: 48.40 49.10 49.75

DJIA

Wall Street closed in the red, with the Dow Jones Industrial average shedding 44 points, to end at 20,837.37, its lowest settlement since March 1st. The Nasdaq Composite ended 19 points lower at 5,856.82 while the S&P closed at 2,365.45, down by 0.34%. Weakening oil prices weighed on stocks, while a cautious stance persisted ahead of the upcoming Fed´s meeting. Within the Dow, Nike led advancers, adding 1.26%, followed by Wal-Mart that closed 1.20%. Decliners were led by Chevron that closed 1.59% and El du Pont that shed 1.09%. The DJIA has been retreating ever since toping at all-time highs early March, now trading some 300 points below such high, barely a correction considering the 3,600 points rally that followed Trump's victory. And while the upward momentum keeps fading, technical readings are far from confirming an interim top and further declines ahead, rather looking as a consolidative stage ahead of the next big catalyst. In the daily chart, technical indicators keep heading south, with the Momentum nearing its 100 level but the RSI still at 60, and the benchmark hovering around a bullish 20 DMA for a second consecutive day. In the shorter term, and according to the 4 hours chart, the risk is towards the downside, as the index kept developing below its 20 and 100 SMAs, both now converging around 20,880, the Momentum indicator retreating from its mid-line, and the RSI indicator hovering around 42.

Support levels: 20,852 20,817 20,777

Resistance levels: 20,880 20,922 20,978

FTSE 100

The FTSE 100 lost 9 points or 0.13% to close the day at 7,357.85, with banking and retail shares dragging the benchmark lower following news that the Brexit will be triggered this March. A weaker Pound was not enough to lift investors' mood that rushed to take profits out of the table as the index holds near record highs. Prudential was the best performer, adding 3.03% after the company reported that its Asian business helped the group´s operating profits to rise 7% to £4.3bn. Pearson was the worst performer, down 2.90%, followed by financial equities, with Royal Bank of Scotland ending the day 2.53% and Barclays shedding 1.59%. The daily chart for the Footsie shows that it managed to hold above its 20 SMA that is losing its upward strength, and currently offering a dynamic support at 7,322, whilst technical indicators hold within positive territory, although with no directional strength. In the 4 hours chart, technical readings support an upward extension for this Wednesday, as the index bounced from a modestly bullish 20 SMA on an early slide, whilst technical indicators have regained their upward strength after a modest correction within positive territory.

Support levels: 7,322 7,306 7,262

Resistance levels: 7,397 7,420 7,450

DAX

The German DAX closed the day flat, down 1 point to 11,988.79, with most major European indexes closing the day marginally lower, tracking losses from their Asian counterparts. The Dutch election taking place this Wednesday, could be the less relevant within the region, but took its toll over local shares, as the anti-immigration Freedom Party is quite close in polls to the ruling conservative party. A surprise victory from populist Wilders could weigh on markets' mood ahead of the FED and send European benchmarks lower this Wednesday. Most components closed down, although RWE AG added 4.30&, leading the advance. Adidas was the worst performer, down 2.47%, followed by Volkswagen that shed 1.58%. Banks closed in the red with Commerzbank and Deutsche Bank losing over 1% each. The index is technically neutral-to-bullish, as in the daily chart, an intraday decline was quickly reverted after it tested a bullish 20 SMA, whilst technical indicators have turned flat, with the Momentum around its 100 level and the RSI indicator at 59. In the 4 hours chart, the index is hovering around a horizontal 20 SMA, whilst technical indicators lack directional strength around their mid-lines, presenting a short term neutral stance.

Support levels: 11,961 11,909 11,857

Resistance levels: 12,018 12,067 12,100

Market Morning Briefing

STOCKS

Dow and Dax are almost stable and could consolidate for some more sessions. Nikkei and Shanghai could come down in the near term while Nifty looks bullish.

Dow (20837.37, -0.21%) could remain stable near current levels for another 1-2 sessions before moving up above 21000. Crucial resistance is seen near 21200.

Dax (11988.79, -0.01%) has been stable for the last few sessions and is stuck in the 12090-11930 region. Resistance is visible near 12200 levels and if that holds, there could be a fall towards 11900-11800 in the near term. Sideways consolidation may continue for the rest of the sessions this week.

Nikkei (19551.72, -0.29%) came off from immediate resistance near 19620 as expected. Narrow range of 19620-19400 and a broader range of 19620-19200 can be expected in the near term. Clear contraction in price action is visible just now.

Shanghai (3233.50, -0.16%) is holding well below the 3250 resistance and while that holds, we could expect trade within the 3175-3250 region in the coming sessions.

Nifty (9087, +1.71%) opened with a gap up but was ranged within the 9122-9060 region yesterday. Note that although the target of 9280 remains open on the upside, there is a decent resistance near 9130. A sharp break above 9130 could confirm higher levels of 9280 in the near term.

COMMODITIES

Gold (1200) is trading within the range of 1180-1220. Until it will manage to close above 1220, it will be difficult for gold to move higher. We will remain bearish while it is trading below 1240.The downward channel in Gold-WTI ratio(24.5) since Aug 16, has been broken and the same could move towards 26-27 levels. We have US Fed Funds rate announcement at 11.30 pm IST, which may add some more clarity through Dollar Index (101.30).

Silver (16.92) is trading slightly higher from its immediate support at 16.65-72 levels. The bias will remain bearish while it is trading below 17.45-50 levels.

Copper (2.64) was unable to close above its pivot at 2.72 of its recent trading range of 2.55-83. We have US CPI and Retail sales data at 6:00 p.m IST, which could influence the price of copper and silver.

Brent (51.60) and WTI (48.43) both are trading within their narrow ranges of 50-52 and 46-50 with a bearish bias. We have US crude oil inventory data at 8.00 pm IST. Only a surplus beyond expectation (3.3M) in US weekly crude oil inventory could affect the price negatively and open up further lower levels for both Brent (47.50) and WTI (45) respectively. Otherwise we may see short term bounce back towards the upper band of the recent ranges.

FOREX

The FOMC decision will be out today and a rate hike looks certain but the markets are more interested about the interest path the Fed indicates.

Dollar Index (101.69) is well on its way towards 102.00-30 as expected, unless the Fed produces any negative surprise tonight. Major support unchanged at 101.00.

Euro (1.0614) is weak and has already tested 1.06 levels in line with expectations. The lower targets of 1.0550-00 may be achieved by the end of the week.

Dollar-Yen (114.81) is stuck in the narrow range of 114.50-115.50 for the 5th consecutive session with a bullish bias. A breakout in the US-Japan 10Yr above 2.55% may help Dollar Yen to rise to 116.00 and 117.50 but till then, more sideways action looks likely.

Pound (1.2158) continues to struggle at the lower levels and the price action may be contained in the range of 1.20-1.23 for the next 5-10 days. Repeat - it remains to be seen if any bottoming price action may take place around the current levels or not.

Aussie (0.7569) keeps trading in the range of 0.75-0.76 with the trend neutral at this point. As discussed yesterday, only a firm break from this range can give directional clue in the near term.

Dollar-Rupee (65.81) has broken below 66.00 in the near term but as it nears oversold condition with the FOMC coming tonight, both these combined may help the pair find near term support today close to 65.70-50, may be even a bounce of 20-30 paisa can be seen. Immediate resistance comes at 66.25-35.

INTEREST RATES

The US yields are testing resistance near current levels and while that holds, we could possibly see some fall in the near term. The 5Yr (2.13%), 10Yr (2.60%) and the 30Yr (3.17%) are slightly down from previous levels of 2.14%, 2.62% and 3.20% respectively.

The German yields have started to come off and looks bearish in the near term. The yield differentials are also headed downwards and could fall in the coming sessions.

The UK 5Yr yield has risen faster than the longer term yields and have paused near current levels for now. There is some more potential on the upside for the near term.

Daily Technical Analysis

EURUSD

The EURUSD had a bearish momentum yesterday bottomed at 1.0599. Price closed a little bit below the H4 EMA 200 suggests a potential bearish outlook especially if price able to make a clear break below 1.0600 testing 1.0500 – 1.0450 area which is a good place to buy with a tight stop loss. Immediate resistance is seen around 1.0650. A clear break above that area could lead price to neutral zone in nearest term testing 1.0700 – 1.0750 region. Overall I remain neutral.

GBPUSD

The GBPUSD had a bearish momentum yesterday slipped below 1.2135 but still unable to closed below that support area so far. The bias is bearish in nearest term especially if price able to make a clear break below 1.2135/00 support area but note that any movement near 1.2000 psychological level should be seen as a good opportunity to buy with a tight stop loss below 1.2000. Immediate resistance is seen around 1.2175. A clear break above that area could lead price to neutral zone in nearest term testing 1.2215 or higher. Overall I remain neutral.

USDJPY

The USDJPY had another indecisive movement yesterday. The bias remains neutral in nearest term probably with a little bearish bias testing 114.35/00 area. Immediate resistance is seen around 115.20 followed by 115.60 which remains a good place to sell with a tight stop loss as a clear break and daily close above 115.60 would expose 117.00 – 118.60 region.

USDCHF

The USDCHF failed to continue its bearish momentum yesterday topped at 1.0107 after unable to break below the H4 EMA 200. I have made some adjustments to the bullish channel on my H4 chart below. The bias is neutral in nearest term probably with a little bullish bias testing 1.0150 – 1.0200 area. Immediate support is seen around 1.0070. A clear break and daily close below that area would expose 1.0000 region. Overall I remain neutral.

Confluence of Resistance on EUR/JPY

After a day off from the blog yesterday, we're back onto the forex currency crosses today with a nice level of confluence in EUR/JPY.

EUR/JPY Daily:

Here you can see the higher time frame confluence of resistance that I'm talking about on the daily chart. Price has not only hit the pretty obvious trend line resistance, but also the horizontal resistance zone.

Both are pretty obvious levels, with the trend line resistance speaking for itself and the horizontal zone formed by a retest of previous swing lows.

EUR/JPY 15 Minute:

Once we zoom into the 15 minute chart, we can look for levels to possibly get short.

I try to usually wait for the higher time frame resistance zone to clear, just to make sure that the level has in fact held, and it is shorts that we should be looking to trade.

As you can see marked in green on the intraday chart above, the level has cleared and we were presented with this little short term retest to manage our risk around and possibly get short off of.

Open an account and take advantage of market opportunity presented to you daily!

NZDUSD – Can Double Bottom Signal a Correction?

The NZD has been on a torrid run against its US counterpart so far this month, falling more than 4% in a little over a week before finding some stability around December's lows.

Since then the pair has run into resistance around 0.6950, an area than had been key support between June and November last year before retesting the lows again.

Once again, the pair found support just below 0.69, potentially suggesting that the strongly bearish sentiment has subsided, allowing for a possible correction in the near term.

With the pair having found a clear floor for now, the test becomes whether it will break above 0.6950 - the double bottom neckline - or through what has become a pretty sturdy support first, just below 0.69.

A break above 0.6950 would suggest we're heading for a correction in the near term rather than a resumption of the aggressive downtrend. While it doesn't tell us how big the correction will be, it would suggest we may at least see a move back towards 0.70. One of the benefits of double bottom setups is that they give us possible price projection levels, based on the size of the double bottom (0.69-0.6950) projected above the neckline.

A break through 0.70 could signal a broader correction, at which point the Fibonacci retracement levels - 7 February highs to 9 March lows - stand out for me, with 38.2% falling around 0.7075, 50% falling around 0.7132 and 61.8% around 0.7190.

A break through the lows of the last week would suggest the sellers are back on board, although one important test remains around 0.6862 - 23 December low - with the next major support below here arguably coming around 0.6675.

Fed Expected to Raise US Interest Rates

Economic projections to give insight on Fed's next steps

The USD is higher across the board awaiting the release of the Federal Open Market Committee (FOMC) rate statement on Wednesday, March 15, at 2:00 pm EDT (6pm GMT). Fed speakers went out of their way in making sure they telegraphed the central banks' decision as the market expected a more patient Fed given the Trump administration has not launched its tax stimulus and infrastructure spending policies.

The CME FedWatch tool based on Fed fund rate futures shows the market has listened to Fed member comments and the probability of a rate hike in March is 93 percent. The Fed will also update its economic projections with investors eager to see what path of tighter monetary policy the Fed is anticipating. Chair Yellen's press conference before the financial press will be closely followed given the willingness to offer more transparent communication from the central bank. Yellen's press conference is scheduled to start at 2:20 pm EDT (6:30 pm GMT).

The Fed is expected to raise the benchmark interest rate in March, making it the third time since the economic crisis. The American central bank would be proactive in 2017 after exercising a patient stance in the past two years which brought about one rate hike a year. The Fed appears optimistic about the growth of the U.S. economy and Yellen will be asked to address Trump pro-growth policies still to be enacted.

The EUR/USD lost 0.258 percent in the last 24 hours. The single currency is trading at 1.0634 ahead of the Fed's FOMC statement where a rate hike by the U.S. central bank is highly anticipated. The USD rally lost steam at the beginning of the year as the Trump administration has not shown the same commitment to pro-growth policies as it did right after the elections.

The EUR got a boost from the comments from European Central Bank (ECB) President Mario Draghi that saw the worst outcome for the currency was still highly unlikely. As voters prepare to cast their ballot in the Dutch elections investor anxiety is on the rise. A win by the PVV Party could trigger the Netherland leaving the Union. Lack of cooperation from other parties make the PVV win less probable, but given the loss of confidence in pollsters after the Brexit and Trump wins the market won't get ahead of the result.

French elections in April and May could prove to be end of the EUR if Marine LePen wins in the second round. The Far-right candidate has campaigned under a flag of nationalism with calls of reintroducing the franc. A Frexit would not be up to LePen alone unless in the improbable scenario where she wins a majority in the house.

The price of oil fell 1.844 percent today. West Texas is trading at $47.32 ahead of the release of the U.S. weekly inventories on Wednesday. Crude has hit three month lows as the momentum gained from the Organization of the Petroleum Exporting Countries (OPEC) production cut agreement has been offset by other factors. Shale producers in the U.S. used the higher prices to increase their output as evidenced by American inventories that have shown consistent buildups in the last nine weeks. The OPEC has not confirmed if it intends to extend the production cut agreement beyond the current six month period.

The GBP/USD lost 0.544 percent in the trading session. The currency is trading at 1.2164 as the road clears for the legal proceedings to trigger Brexit. Invoking article 50 will begin a two year negotiation process that will result in the United Kingdom leaving the European Union. There have not been many fruitful meetings between the two sides on what the future trade relationship will look like. The U.K. has the most to lose, and this has been reflected in the pound. The USD has risen given the expectations of a rate hike in March putting further downward pressure on the GBP.

Scotland added to the political uncertainty in the U.K. after its First Minister Nicola Sturgeon said the is seeking a second Scottish Independence referendum within the next two years. The FX market so far has been the best gauge of investors losing confidence in Theresa May reaching an acceptable agreement despite the limited effect Brexit proceedings have had on the economy. The true impact of leaving the E.U. has not been felt as article 50 has not triggered Brexit.

The eyes of the market will be focused on the words out of Washington as the Fed finished its two day meeting with the publication of the U.S. benchmark interest rate, economic projections and press conference by Fed Chair Janet Yellen.

Market events to watch this week:

Wednesday, March 15

- 8:30am USD CPI m/m

- 8:30am USD Core CPI m/m

- 8:30am USD Core Retail Sales m/m

- 8:30am USD Retail Sales m/m

- 10:30am USD Crude Oil Inventories

- 2:00pm USD FOMC Economic Projections

- 2:00pm USD FOMC Statement

- 2:00pm USD Federal Funds Rate

- 2:30pm USD FOMC Press Conference

- 5:45pm NZD GDP q/q

- 8:30pm AUD Employment Change

- 8:30pm AUD Unemployment Rate

- Tentative JPY BOJ Policy Rate

- Tentative JPY Monetary Policy Statement

Thursday, March 16

- 2:30am JPY BOJ Press Conference

- 4:30am CHF Libor Rate

- 4:30am CHF SNB Monetary Policy Assessment

- 8:00am GBP MPC Official Bank Rate Votes

- 8:00am GBP Monetary Policy Summary

- 8:00am GBP Official Bank Rate

- 8:30am USD Building Permits

- 8:30am USD Philly Fed Manufacturing Index

- 8:30am USD Unemployment Claims

Friday, March 17

- 8:30am CAD Manufacturing Sales m/m

- 10:00am USD Prelim UoM Consumer Sentiment

*All times EST

NY Survived Stella but Will the Markets Survive Janet?

While my colleagues in New York managed much better than expected, as the city sidestepped the worst of the winter storm Stella, but there was little inspiration during Tuesday's North American session. Currency markets were constrained due to little more than position square dancing, ahead of a potentially wicked Wednesday (in NY). Traders eyes are peeled on the Fed Dot Plots while remaining attuned for any political noise, which there certainly is no shortage of these days.

The collapse in oil prices was the big story overnight when the WTI dropped from $48.80 level towards $47 zone. The catalyst was the release of the OPEC monthly report, as Traders focused on headlines that Saudi Arabia increased their production in February by 263.3k barrels a day, to 10.011mn per day, as reported. However, given it's still below 10.06mn agreed to in the production deal, the move looks to be little more than a momentum fast money reaction. After cooler heads had prevailed, the market had all but filled the headline gap, aided by the Weekly API inventories, which reported its first draw in 3 weeks coming in at -.5M vs. +11.6 M prior. Oil patch traders should take no solace as we are far from an endgame in this shale vs. production cut debate.

The slide in oil prices yanked down shares across the energy sector, but broader commodity weakness has also weighed on stocks. While other areas of the markets saw moderate losses as investors taper positions while in wait and hear mode ahead of the Federal Reserve, which has begun its two-day policy meeting on interest rates.

Australian Dollar

The AUD fell under moderate pressure after the NAB business conditions indicated signs of weakness, which seems to confirm the recent underwhelming string of economic data all the while the RBA continues to paint a rosy picture.

Commodity prices continued to sag, despite stronger-than-expected activity data in China which offered little support to the currency.

Headlines have materialised that the RBA assistant governor Bullock has announced there will be further macro-prudential measures to compensate for the rising housing market – while these tightening measures could imply the RBA has wiggle room to cut rates, I suspect Governor Low will opt for a lower for longer stance than a more drastic cut.

While the Aussie dollar has hardly budged from yesterday's APAC levels, with concerns, the commodity complex outlook remains fragile. One could expect the AUD at some point to play catch up with the other commodity high betas that have been experiencing a broader correction lower. The longer we float in this mid-7500 no man's land, the more likely USD support from US$ yields will kick in, and if commodity prices are to roll over, it could make a compelling argument for a full correction lower on the AUD.

On the domestic data front, the Australia March Westpac consumer confidence index printed 99.7%, a four-month high vs. 99.6% prior, on a month to month basis 0.1% and the third consecutive increase. While AUD is off the interday lows, it will struggle to gain traction ahead of the deluge of central bank cacophony ahead.

Japanese Yen

There has been see-sawing between the US yield play and the minor risk reversal in equity markets due to falling oil prices.But I suspect the USDJPY remains the favourite trade if we get any glimmering hope from the Fed of a more hefty path of US interest rates through 2017, but the 115.60-75 level will be the first tricky area for the dollar bulls to challenge if Dr Yellen signals a robust interest rate trajectory

Euro

The Euro is pulling back, as EUR traders adopt a bit of risk aversion temperament, which is justifiable with the Dutch election looming. Some near term stops reported below 1.06 will likely come in play as the dealers play position chess with one another ahead of the FOMC.

EM Asia

USDAsia retraced in a big way yesterday with the market trading US dollar offered throughout the session, as dealers eagerly awaited the USDINR fix (open) which then turned into an INR feeding frenzy after stops were triggers below 66. While the market remains very bullish INR, dealers will sit tight and await better clarity on the Fed trajectory before doubling down on the post-election euphoria. While much of the move was driven onshore, offshore investors will take note of the record NSE index highs so there could be another wave

As for the rest of Asia, we could be witnessing little more than the calm before the storm as USD selling across the region yesterday was supported on the back of adamant equity inflows.

Overnight the NY NDF market, USDKRW traded 1148.5-1150.5 and closed at 1149.0-1150.0. USDKRW has opened a touch 1148.0, but I suspect we will continue to drift in range. The technical edges of support and resistance will not come into play until further clarity on the Feds offered later tonight