Sample Category Title

Trade Idea Update: GBP/USD – Stand aside

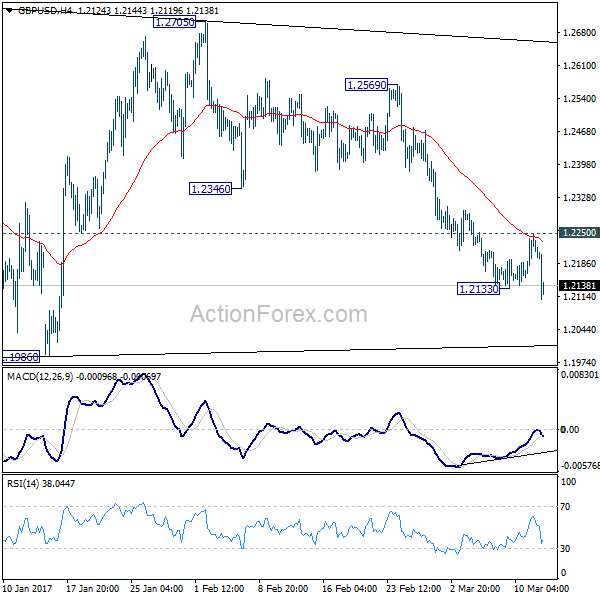

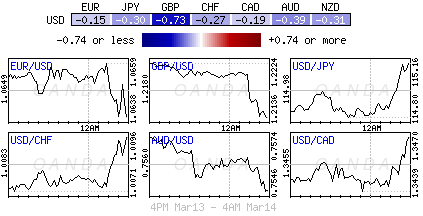

GBP/USD - 1.2140

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Current selloff dampened our near term bullishness and signals recent decline has resumed, hence downside risk remains for further fall to 1.2100, however, loss of downward momentum should prevent sharp fall below 1.2070 and reckon 1.2040-50 would hold from here, sterling may stage another rebound from there later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above the Kijun-Sen (now at 1.2188) would suggest an intra-day low is formed instead, risk rebound to 1.2215 but break there is needed to confirm and bring a stronger rebound towards resistance at 1.2251.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2159; (P) 1.2205; (R1) 1.2263; More...

GBP/USD's break of 1.2133 temporary low suggests that fall from 1.2705 has resumed. Intraday bias is back on the downside for retesting 1.1946/86 support zone. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. Break of 1.1946 will confirm our bearish view. On the upside, above 1.2250 minor resistance will turn bias neutral again. But outlook will stay bearish as long as 1.2346 support turned resistance holds.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Trade Idea Update: EUR/USD – Hold long entered at 1.0640

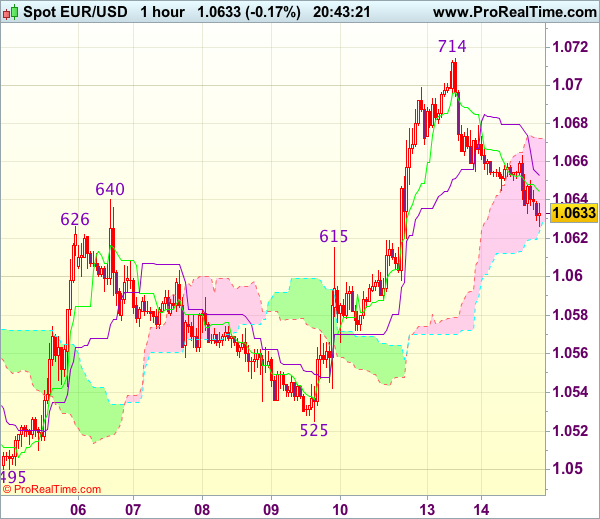

EUR/USD - 1.0629

Original strategy :

Bought at 1.0640, Target: 1.0740, Stop: 1.0610

Position : - Long at 1.0640

Target : - 1.0740

Stop : - 1.0610

New strategy :

Hold long entered at 1.0640, Target: 1.0740, Stop: 1.0610

Position : - Long at 1.0640

Target : - 1.0740

Stop : - 1.0610

Although the single currency has slipped again today and marginal weakness from here cannot be ruled out, reckon downside would be limited and as long as previous resistance at 1.0615 (now support) holds, mild upside bias remains for another rise, above 1.0680 would suggest the retreat from 1.06714 has ended, bring retest of this level, break there would extend the erratic rise from 1.0493 low to 1.0740-45 (1.5 times projection of 1.0495-1.0640 measuring from 1.0525) but loss of upward momentum should prevent sharp move beyond 1.0760 (1.618 times projection of 1.0495-1.0640 measuring from 1.0525).

In view of this, we are holding on to our long position entered at 1.0640. Below previous resistance at 1.0615 would abort and signal top has been formed, risk further fall to 1.0575-80 first.

Dollar Rebounds, Maintain Gains as PPI Beat Expectation

Dollar rebounds broadly today and maintain gains after stronger than expected inflation data. Headline PPI rose 0.3% mom and 2.2% yoy in February, comparing to prior month's 0.6% mom and 1.6% yoy, above consensus of 0.1% mom and 2.0% yoy. Core CPI rose 0.3% mom, 1.5% yoy, up from 0.4% mom and 1.2% yoy, versus consensus of 0.2% mom, 1.5% yoy. In particular, GBP/USD drops through 1.2133 support as Sterling is sold off broadly on news on Brexit and revival of Scexit. Meanwhile, Yen is trading as the strongest major currency with buying interest seen ahead of BoJ meeting.

FOMC to meeting despite snow storm

Markets are keenly awaiting FOMC rate decision tomorrow. In spite of snow storm hobbling much of northeast, Fed will l start it's two-day meeting today as scheduled. Fed will announce decision at 1800 GMT tomorrow together with new economist projections. Fed chair Janet Yellen will hold a press conference at 1830 GMT. It's widely expected that Fed will hike interest rate by 25bps. And it's likely that Fed will sound more upbeat in the statement and the press conference. The point of interests will be on economic projections and in particular the median "dot plot" rate path. Back in December, Fed projected interest rate to hit 1.4% by the end of 2017 and 2.1% by end of 2018. Upward revision in these two figures would fuel rally in Dollar.

Germany economic sentiment improved in March.

German ZEW economic sentiment rose to 12.8 in March, up from 10.4 and beat expectation of 12.0. Current situation gauge rose to 77.3, up fro 76.4, but missed expectation of 78.0. Eurozone ZEW economic sentiment also rose to 25.6, up from 17.1, and beat expectation of 19.3. ZEW President Achim Wambach said that "the fact that the ZEW indicator of economic sentiment only shows a slight upward movement is a reflection of the current uncertainty surrounding future economic development. Meanwhile, "with regard to the economic situation in Germany, no clear conclusion can be drawn from the most recent economic signals."

Also from Eurozone, German CPI was finalized at 0.6% mom, 2.2% yoy in February. Eurozone industrial production rose 0.9% mom in January.

Sterling pressured by news of double divorce

In UK, the Parliament passed the bill allowing Prime Minister Theresa May to trigger Article 50 for Brexit negotiation." May will address the House of Commons today. Some expect May to wait until the end of the month to trigger Brexit. But there are speculations that May could announce it this week. Scottish First Minister Nicola Sturgeon confirmed that she would ask for permission to hold a second independence referendum.

China data beat expectations, except retail sales

China has released just now that industrial production expanded 6.3% yoy in the first two months of the year, up from consensus of 6.1% and December's 6%. Urban fixed asset investment (FAI) grew 8.9% yoy during the period, beating consensus of 8.3% and 8.1% previously. However, the growth of retail sales moderated to 9.5% yoy, from 10.4% in December. The market had anticipated stronger growth of 10.6%.

Retail drags down Australia business confidence

Australia NAB business confidence dropped to 7 in February, down from 10. Meanwhile, business conditions dropped to 9, down from 16. NAB chief economist Alan Oster noted that "big service industries drive the moderation in business conditions this month, but even after pulling-back a little, these industries continue to lead the non-mining recovery." Meanwhile, "it is hard to look past the disappointing results from retail, especially given the importance of consumption to the growth outlook."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2159; (P) 1.2205; (R1) 1.2263; More...

GBP/USD's break of 1.2133 temporary low suggests that fall from 1.2705 has resumed. Intraday bias is back on the downside for retesting 1.1946/86 support zone. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. Break of 1.1946 will confirm our bearish view. On the upside, above 1.2250 minor resistance will turn bias neutral again. But outlook will stay bearish as long as 1.2346 support turned resistance holds.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Feb | 7 | 10 | ||

| 02:00 | CNY | Industrial Production YTD Y/Y Feb | 6.30% | 6.10% | 6.00% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Feb | 8.90% | 8.30% | 8.10% | |

| 02:00 | CNY | Retail Sales YTD Y/Y Feb | 9.50% | 10.60% | 10.40% | |

| 07:00 | EUR | German CPI M/M Feb F | 0.60% | 0.60% | 0.60% | |

| 07:00 | EUR | German CPI Y/Y Feb F | 2.20% | 2.20% | 2.20% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | 0.90% | 1.20% | -1.60% | -1.20% |

| 10:00 | EUR | German ZEW (Economic Sentiment) Mar | 12.8 | 12 | 10.4 | |

| 10:00 | EUR | German ZEW (Current Situation) Mar | 77.3 | 78 | 76.4 | |

| 10:00 | EUR | Eurozone ZEW (Economic Sentiment) Mar | 25.6 | 19.3 | 17.1 | |

| 12:30 | USD | PPI M/M Feb | 0.30% | 0.10% | 0.60% | |

| 12:30 | USD | PPI Y/Y Feb | 2.20% | 2.00% | 1.60% | |

| 12:30 | USD | PPI Core M/M Feb | 0.30% | 0.20% | 0.40% | |

| 12:30 | USD | PPI Core Y/Y Feb | 1.50% | 1.50% | 1.20% |

Trade Idea Update: USD/JPY – Stand aside

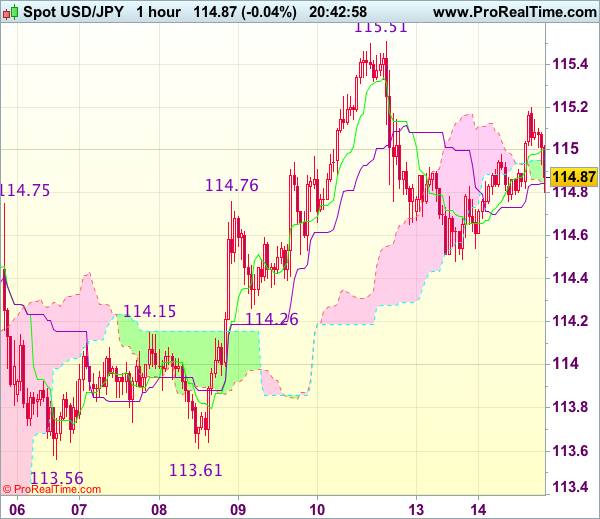

USD/JPY - 114.88

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback recovered after falling to 114.48 yesterday and minor consolidation is in store, reckon upside would be limited to 115.15-20 and near term downside risk remains for the fall from 115.51 top (last week’s high) to bring at least a retracement of recent upmove to 114.26 support but downside should be limited to 114.00-05 (38.2% Fibonacci retracement of 111.69-115.51) and price should stay well above strong support at 113.56-61), bring rebound later.

In view of this, would be prudent to stand aside for now. A firm break above 115.15-20 would suggest an intra-day low is formed, bring a stronger rebound but still reckon said resistance at 115.51 would cap upside. Only break there would revive bullishness and extend recent upmove to previous resistance at 115.62, then towards 115.90-00.

Investors Wait on Fed, GBP Slides on Brexit Vote

We remain in wait and see mode in the markets on Tuesday, with US futures closely tracking moves in Europe where indices are marginally lower as investors perch themselves on the fence ahead of tomorrow's Fed decision.

With markets having almost entirely priced in a rate hike tomorrow, there appears to be little appetite to pre-empt the decision, especially as how investors respond will likely largely be driven by future rate hike expectations as opposed to the hike itself. Should the Fed renege on a rate hike that policy makers have strongly hinted at then the potential downside could be quite substantial. It's always a little concerning when markets are so certain that an event is going to happen and we've seen plenty of examples of this backfiring in 2016 alone.

That said, given the effort that the Fed went to just to get to this point, it would come as quite a shock if it didn't deliver. With the markets now so onside, the most important thing should be the projections and Janet Yellen's expectations going forward. Should the Fed signal a possible fourth hike this year then further upside could be in store for the dollar and Treasury yields, while an indication that expectations are unchanged could trigger some profit taking given investors current positioning.

With so many major events in store this week including the Fed, BoE, BoJ and Dutch elections, today is likely to be another relatively calm session. US PPI and API weekly crude oil stocks are the only notable data releases, with the latter being of particular interest as oil continues to pare its losses today having fallen off a cliff over the last week.

The UK is doing its best to fill the void at the start of the week with the House of Lords late last night passing the Brexit bill in its original form after parliament rejected its two previous amendments. Theresa May is now free to legally trigger article 50 as and when she chooses, which will likely out of respect be later in the month after the Dutch election this week and the sixtieth anniversary celebration of the signing of the Treaty of Rome on 25 March. The pound has taken another hit today after the events of Monday evening, with the loss of the vote on the final deal in parliament possibly being seen as increasing the possibility of a hard Brexit. In reality, the pound had been on the way down prior to its slight bounce on Monday and the vote last night has possibly just been the capitalised on by those looking for an excuse to short. 1.20 remains a key level for EURUSD.

Canadian Dollar Dips Ahead of Expected Fed Hike

USD/CAD has move higher in the Tuesday session. In North American trade, the pair is trading slightly below the 1.35 line. On the release front, US PPI dipped to 0.3%, above the estimate of 0.1%. There are no Canadian releases until Thursday. Wednesday promises to be busy, with the US releasing CPI and retail sales reports. As well, the Federal Reserve is widely expected to raise the benchmark rate to 0.75 percent.

Canada continues to create jobs at an impressive clip, as the Canadian economy has taken advantage of a strong recovery south of the border. On Friday, Employment Change came in at 15.3 thousand. This was lower than the previous two readings, but easily beat the forecast of 0.6 thousand. The economy has created jobs for seven straight months, as the labor market continues to recover. The unemployment rate also improved, dropping from 6.8% to 6.6%. Still, these strong figures only tell part of the story. Wage growth remains soft and many of the recent job gains have been part-time positions. The Canadian dollar posted only modest gains on Friday, as upward movement was limited by a very strong Nonfarm Payrolls report in the US.

More job numbers out of the US, more good news for the economy. Nonfarm payrolls sparkled in February, as the indicator jumped to 235 thousand, easily beating the estimate of 196 thousand. Wage growth climbed 2.6% compared to February 2016, while the participation rate edged up to 63.0%, up from 62.9%. These numbers make it a virtual certainty that the Fed will raise rates by a quarter-point on Wednesday. Although a rate hike has been priced in by the markets at 93%, there have been disappointments in the past, so a rate move will likely give the dollar a boost against its major rivals, such as the euro. The solid job numbers also give President Trump a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room with the economy performing well.

DAX Hugging 12,000 as Germany Posts Solid Data

The DAX Index is steady on Tuesday, trading at 11,995.50 in the European session. In economic news, German Final CPI improved to 0.6%, matching the forecast. German ZEW Economic Sentiment improved to 12.8 points, short of the estimate of 13.2 points. The Eurozone ZEW Economic Sentiment jumped to 25.6, beating the forecast of 19.3 points. On Wednesday, the Federal Reserve is widely expected to raise the benchmark rate to 0.75 percent.

At last week's ECB policy meeting, several policymakers raised the possibility of higher interest rates. With growth and inflation showing signs of improvement, the ECB has been under pressure to tighten policy and reduce its asset-purchase program. Germany, in particular, is unhappy with the ECB's ultra-loose policy and on Thursday, German Finance Minister Wolfgang Schaeuble bluntly stated that he wanted to see a "timely start to the exit" from the ECB's asset-purchase scheme. For his part, Mario Draghi must balance the improved economy with upcoming elections in the Netherlands and France. Euro-skeptics are a strong force throughout Europe and Draghi is reluctant to make any major moves in the middle of heated political campaigns.

More job numbers out of the US, more good news for the economy. Nonfarm payrolls sparkled in February, as the indicator jumped to 235 thousand, easily beating the estimate of 196 thousand. The excellent NFP report make it a virtual certainty that the Fed will raise rates by a quarter-point on Wednesday. Although a rate hike has been priced in by the markets at 93%, there have been disappointments in the past, so a rate move will likely give the dollar a boost against its major rivals, such as the euro. The solid job numbers also give President Trump a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room with the economy performing well.

Sterling to Suffer with Two Divorces

Tuesday March 14: Five things the markets are talking about

With a Fed rate hike almost fully priced in by the markets for tomorrow, expect investors to be fully focused on Ms. Yellen's press conference and the central bank's so-called 'dot plots' for clues about future moves on monetary policy.

In the U.K, the upper house has removed the final hurdle to PM May's plan to commence talks on Britain leaving the E.U - no date on when the PM would trigger talks, but signs still point to the end of the month. However, the threat of another Constitutional crisis with referenda in Scotland and possibly Northern Ireland has the pound again under pressure (£1.2120). Has the market priced-in enough political and economic risk for sterling?

Elsewhere, Dutch voters are heading to the polls tomorrow, in a highly anticipated general election seen as a bellwether for how populist opinion will fare next month in France.

1. Global Stocks mixed reactions

Global stocks sit atop record high as the market increase their expectations for the Fed to raise interest rates at a faster pace.

In Japan, stocks edged down overnight. The Nikkei share average shed -0.1% in quiet trading, while the broader Topix dropped -0.2%. In Hong Kong, the Hang Send was unchanged as investors stayed on the sidelines ahead this week's global risk events (FOMC, BoE, BoJ, OPEC, Dutch elections).

India's Nifty 50 surged +1.8% overnight as the market reopened after a public holiday.

Note: PM Modi's Party won 312 seats in the 403-member assembly of Uttar Pradesh, according to the Election Commission of India, up from 47 in 2012.

Chinese shares traded in Hong Kong climbed +0.6% after surging +1.9% on Monday for the biggest gain in four-months. On the back of stronger industrial data and retail sales (see below)

In Europe, equity indices are trading mixed. Banking stocks are leading the losses in the Eurostoxx while the FTSE 100 is outperforming on the back of commodity and energy names.

U.S equities are set to open in the red (-0.2%).

Indices: Stoxx50 -0.4% at 3,404, FTSE +0.1% at 7,375, DAX -0.1% at 11,980, CAC-40 -0.3% at 4,986, IBEX-35 -0.6% at 9,932, FTSE MIB -0.4% at 19,628, SMI -0.1% at 8,672, S&P 500 Futures -0.2%

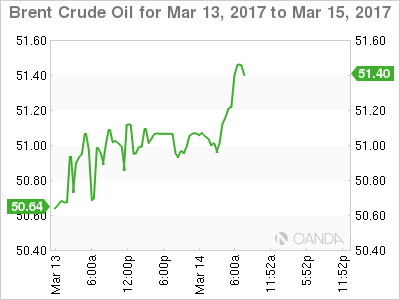

2. Oil hovers near three-month lows as markets await data

Crude oil prices trade atop of their multi-month lows ahead of the U.S open, as dealers wait for key reports that are expected shed light on a supply overhang in the market.

Brent crude futures are up +3c to +$51.32 a barrel, having settled down -2c yesterday. West Texas Intermediate crude (WTI) is down -7c at +$48.33 a barrel. The contract ended down -9c Monday.

Prices fell sharply last week as investors worried that swelling U.S. crude supplies would hinder OPEC's efforts to restrict output and reduce a global glut.

Note: OPEC releases its monthly oil market report later today along with the API's stockpiles, while the IEA releases its closely watched monthly report tomorrow.

Any signs of another big crude inventory build and the market "bears" will be expected to take price control for the short term.

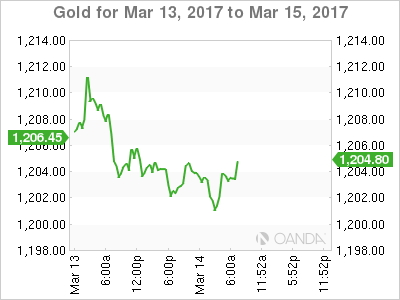

Gold prices are steady (-0.1% to +$1,202.36) as the market waits for the start of the Fed's two-day meeting today that is expected to end with the bank raising interest rates for the second time in three-months.

Gold dealers will also be focusing on tomorrow's Dutch elections - the fears of a Eurosceptic party coming to power is seen as small, however, a strong showing could fuel speculation of a surprise result in next month's French Presidential election.

Note: Holdings of the world's largest gold-backed exchange-traded fund (SPDR) rose +0.83% yesterday after four sessions of outflows.

3. Central bank decisions dominate yield curve shape

Fixed income dealers view a +25bps Fed hike this week as a virtual certainty after last Friday's non-farm payroll (NFP) print (+235k and +4.7% unemployment rate). Dealers will be watching the policy decision for signals on what will come next - another two hikes or maybe three?

Overnight, the yield on U.S 10's fell -1bps to +2.62% - trading above the psychological +2.60% benchmark that many dealers consider the beginning of a bear market if it holds for a week. Down-under, 10-year Aussie bonds fell -1bps to +2.92%.

Elsewhere, the Bank of Japan (BoJ) is expected to keep its rates and yield-curve policy unchanged in its policy decision on Thursday, while the Bank of England (BoE) and the Swiss National Bank (SNB) are also expected to stand pat with their own policy decisions.

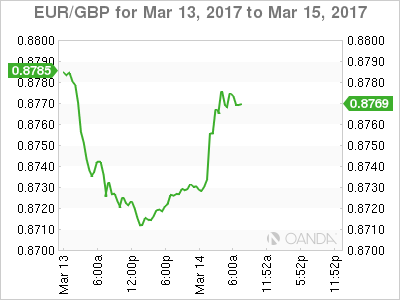

4. Sterling drops to multi week low vs. EUR and Dollar

Concerns about Brexit and calls for a Scottish independence referendum has pushed the pound to a two-month low against the dollar (£1.2109) and a seven-and-a-half week low against the EUR (€0.8789) ahead of the U.S open.

Yesterday, the U.K. parliament cleared the way for PM Theresa May to start Brexit by triggering Article 50, while Scottish First Minister Nicola Sturgeon pledged to push for a second independence vote.

If U.K. data continue to surprise to the downside, fixed income dealers are likely to react by moving to remove the implied increase in interest rates currently priced into U.K rates - this will only aid the pound downfall further.

The EUR is hovering around the mid-€1.06 area. Earlier this morning, German Final CPI reading confirmed highest annual pace since August 2012 (+2.2% vs. +2.2%e).

Note: Despite the pickup in headline inflation in the Eurozone there may be no change in the ECB's "loose" monetary policy given that it is volatile energy and food prices that are pushing the inflation rate up.

USD/JPY is holding above the psychological ¥115 level aided by yield differentials.

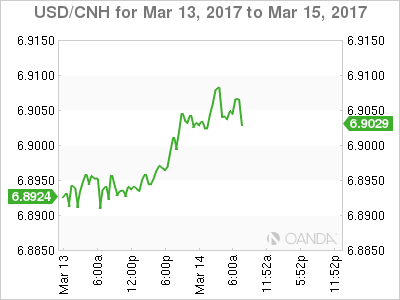

5. China Sales disappoint, industrial production improves

China's retail sales missed estimates to fall below the psychological +10% for the first time since 2003, while fixed-asset investment and industrial output improved.

Retail sales growth disappointed with a multi-year low of +9.5%, despite recent comments from Beijing that the economy is making progress in transition to consumption-driven growth.

Other data showed that industrial output improved, hitting a six-month high with +6.3% increase in power generation, +5.8% rise in crude steel production, and -8% decline in crude oil output. Fixed Asset investment printed an eight-month high rate of growth, driven by +8.9% rise in property investment amid +26% increase in property sales value.

Note: China's Stats bureau also noted that consumption is expected to remain stable this year and that the CPI will rebound after last month's surprise decline.

EUR/USD – Euro Steady As German ZEW Economic Sentiment Improves

EUR/USD has edged lower in the Tuesday session. Currently, the pair is trading at 1.0640. On the release front, German Final CPI improved to 0.6%, matching the forecast. German ZEW Economic Sentiment improved to 12.8 points, short of the estimate of 13.2 points. The Eurozone ZEW Economic Sentiment jumped to 25.6, beating the forecast of 19.3 points. In the US, we’ll get a look at PPI, with the index expected to post a small gain of 0.1%. Wednesday promises to be very busy, with the US releasing CPI and retail sales reports. As well, the Federal Reserve is widely expected to raise the benchmark rate to 0.75 percent.

German data was in the spotlight on Tuesday. There was further indication that inflation continues to improve, as Final CPI rebounded with a gain of 0.6%, compared to a 0.6% decline a month earlier. The well-respected ZEW Economic Sentiment report improved to 1.28, although the markets had expected a stronger reading. Eurozone ZEW Economic Sentiment climbed to 25.6, its strongest gain since December 2015.

The euro posted considerable gains on Friday, as some ECB policymakers raised the possibility of higher interest rates at last week’s policy meeting. At the meeting, the ECB held course and maintained interest rates at a flat 0.00%. The markets were left to pick up on nuances, as ECB President Mario Draghi noted that the central bank removed one phrase from its standard introductory statement – 'using all the instruments available within its mandate'. Draghi stated that the removal of this phrase means that the ECB 'no longer has a sense of urgency in taking further actions …. prompted by the risk of deflation'. With growth and inflation showing signs of improvement, the ECB has been under pressure to tighten policy and reduce its asset-purchase program. Germany, in particular, is unhappy with the ECB’s ultra-loose policy and on Thursday, German Finance Minister Wolfgang Schaeuble bluntly stated that he wanted to see a 'timely start to the exit' from the ECB’s asset-purchase scheme. For his part, Mario Draghi must balance the improved economy with upcoming elections in the Netherlands and France. Euro-skeptics are a strong force throughout Europe and Draghi is reluctant to make any major moves in the middle of heated political campaigns.

More job numbers out of the US, more good news for the economy. Nonfarm payrolls sparkled in February, as the indicator jumped to 235 thousand, easily beating the estimate of 196 thousand. Wage growth climbed 2.6% compared to February 2016, while the participation rate edged up to 63.0%, up from 62.9%. These numbers make it a virtual certainty that the Fed will raise rates by a quarter-point on Wednesday. Although a rate hike has been priced in by the markets, there have been disappointments in the past, so a rate move will likely give the dollar a boost against its major rivals, such as the euro. The solid job numbers also give President Trump a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won’t mind giving him some additional breathing room with the economy performing well.