Sample Category Title

NZDUSD Intraday View

On the hourly chart of NZDUSD we can see a nice higher degree impulse in the making, with price currently trading in one of its sub-waves, wave 4. Well, current intraday weakness could suggest a continuation into wave 5, but we believe this could be only a temporary drop, as we still expect price to make a final reversal higher into wave c of 4. That said, price could later then face a turning point lower around the 23.6/50.0 Fibonacci ratio.

NZDUSD, 1H

European Market Update: BOE Dep Gov Nominee Hogg Resigns

BOE Dep Gov nominee Hogg resigns

EU Mid-Market Update: European inflation at multi-year highs; BOE Dep Gov nominee Hogg resigns

Notes/Observations

German Final CPI reading confirms highest annual pace since August 2012 (2.2% v 2.2%e)

Sweden CPIF inflation annual reading at highest level since Dec 2010

BOE Dep Gov nominee Hogg resigns after failing to disclose her brother worked at Barclays

Overnight:

Asia:

China Feb Industrial Production hits a 6-month high (YoY: 6.3% v 6.2%e) while retail sales missed due to slower auto sales (YoY: 9.5% V 10.6%e)

China Stats Bureau (NBS): Fundamentals of real economy were improving, business environment much better than this time last year; PPI might have peaked in Feb

Japan Fin Min Aso: Financial regulations and taxation will be topics at G20; plan to explain Japan's economy and listen to others opinions

Europe:

(UK) Parliament approved PM May to start Brexit process. Brexit bill has now made it through parliament and is set to receive Royal Assent before becoming law. Once the bill became law, PM May would have the authority to trigger the Article 50 exit process.

UK Brexit Min Davis reiterated that govt would trigger A50 by end of month as planned; to deliver an outcome that works in interests of whole UK

UK would need to pass 7 new Bills in key areas to prepare for Brexit; including areas covering immigration, tax, agriculture, trade/customs, fisheries, data protection and sanctions

PM May said to be preparing to reject Scotland 1st Min Sturgeon’s demand for 2nd referendum on Scottish independence

Americas:

Treasury official: G20 needed to abide by existing currency views; affirmed commitments to not target FX rates to gain competitive trade advantage

Energy:

EIA forecasts April total shale regions oil production at 4.962M bpd, +109K bbd m/m

Economic data

(IN) India Feb Wholesale Prices (WPI) Y/Y: 6.6% v 6.1%e

(DE) Germany Feb Final CPI M/M: 0.6% v 0.6%e; Y/Y: 2.2% v 2.2%e (highest annual pace since August 2012)

(DE) Germany Feb Final CPI EU Harmonized M/M: 0.7% v 0.7%e; Y/Y: 2.2% v 2.2%e

(ES) Spain Feb Final CPI M/M: -0.4% v -0.3%e; Y/Y: 3% v 3.0%e

(ES) Spain Feb Final CPI EU Harmonized M/M: -0.3% v -0.3%e; Y/Y: 3.0% v 3.0%e

(SE) Sweden Feb CPI M/M: 0.7% v 0.6%e; Y/Y: 1.8% v 1.7%e

(SE) Sweden Feb CPI CPIF M/M: 0.7% v 0.6%e; Y/Y: 2.0% v 1.9%e

(ES) Bank of Spain (BOS): Feb Spanish Banks ECB borrowings at €145.0B v €144.9B prior

Fixed Income Issuance:

(ID) Indonesia sold total IDR11.35T in 5-year,15-year and 20-year Bonds

(NL) Netherlands Debt Agency (DSTA) sold €2.275B vs. €2.0-3.0B indicated range in 0% 2022 DSL Bonds; Yield: -0.197% v -0.283% prior

(ES) Spain Debt Agency (Tesoro) sold total €3.02B vs. €2.5-3.5B indicated range in 3-month and 9-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 09:40 GMT)

Indices [Stoxx50 -0.4% at 3,404, FTSE +0.1% at 7,375, DAX -0.1% at 11,980, CAC-40 -0.3% at 4,986, IBEX-35 -0.6% at 9,932, FTSE MIB -0.4% at 19,628, SMI -0.1% at 8,672, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes: European equity indices are trading mixed but generally lower after a mixed end to the Asian session overnight; Banking stocks generally lower across the board with the IBEX-35 underperforming, weighed down by the Spanish peripheral lenders; shares of Engie leading the losses in the Eurostoxx after it was reported to be mulling a bid for recently IPO’ed Innogy, shares of Innogy conversely higher; FTSE 100 outperforming, with shares of Prudential leading the gains in the index after releasing its FY16 results.

Upcoming scheduled US earnings (pre-market) include DSW, HD Supply, Radnet, Veritiv, Walter Investment Management, and YY Inc.

Equities (as of 09:35 GMT)

Consumer Discretionary: [Ocado OCDO.UK +4.6% (Q1 sales)]

Energy: [Innogy IGY.DE +5.1% (Engie reportedly mulling a bid, said to be valued at ~$20B), RWE RWE.DE +8.7% (FY16 results)]

Financials: [Amundi AMUN.FR -0.4% (€1.4B rights offering), Prudential PRU.UK +3.0% (FY16 results, raises div)]

Healthcare: [Galenica GALN.CH -2.9% (FY16 results), Stratec Biomedical SBS.DE +9.3% (FY16 results)]

Industrials: [Aker Solutions AKSO.NO +14.2% (Halliburton said to be in advanced talks for acquisition), Antofagasta ANTO.UK +0.1% (FY16 results), Geberit GEBN.CH -1.0% (FY16 results, share buyback, div increase), Huber & Suhner HUBN.CH -0.2% (final FY16 results, div increase), Symrise SY1.DE -0.7% (FY16 results)]

Materials: [SIG Plc SHI.UK +9.5% (FY16 results, rebases div, names new CE), Wacker Chemie WCH.DE -1.5% (FY16 results)]

Utilities: [Engie ENGI.FR -1.7% (Reportedly mulling a bid for Innogy)]

Speakers

Sweden Central Bank (Riksbank) Gov Ingvesstated that it had reversed the trend in inflation but was not out of the woods just yet; needed continuous stimulus to stabilize inflation. Inflation remain low when excluding energy prices. Reiterated that inflation to stabilize around 2% in 2018 and that the exchange rate was important for its development

UK Treasury committee report on Charlotte Hogg expressed concerned that she misled (inadvertently) the committee and thus had concerns over her competence to serve as Dep Gov. They concluded that she fallen short of standards (**Note: she did not declare that brother worked at Barclays back in 2013 when she joined the central bank

BOE's Dep Gov nominee Charlotte Hogg resigned (voluntary)

Italy Government to hold labor legislation referendum on May 28th

Germany 2018 budget draft said to assume economic growth of 1.6% led by domestic demand

France former PM Valls refutes reports that he sought to endorse Macron for President

Bank of Korea (BOK) Feb Minutes saw various members state that CPI rise to be in-line with Jan forecast and no big necessity to adjust interest rates. Steady policy provided policy space if needed

China NDRC to cut fuel prices (gasoline prices by CNY85/ton and diesel prices by CNY85/ton)

Currencies

EUR/USD hovering around the mid-1.06 area. German Final CPI reading confirmed highest annual pace since August 2012 (2.2% v 2.2%e). Despite the pickup in headline inflation in Germany and elsewhere in the eurozone, there may be no change in the European Central Bank's loose monetary policy given that it is volatile energy and food prices which are pushing the inflation rate up

USD/JPY pair held above the 115 level aided by yield differentials. 30-Year Treasury Yield Touches Highest Since July 2015

The GBP/USD was weaker in the session after UK PM May was given the go-ahead to trigger Brexit by her Parliament with no amendment attached. The response was a bit of delay for the currency.Market participants were said to be reluctant to sell the GBP currency during Tokyo trading hours as markets were quiet before the Fed mid-week rate decision.

Fixed Income:

Bund futures trade at 159.10 down 9 ticks having traded as low as 158.73 a contract low, fading some of the move lower as Equities retreat. A move back below lows target 158.26 followed by 158.04. Resistance moves to 159.68 then 159.85 Friday high followed by 160.20.

Gilt futures trade at 125.89 down 15 ticks ahead of the launch of a new 10 year Gilts due later today. Support moves to 125.57 with further weakness eyeing 125.24. Resistance moves to 126.38 then 126.87 followed by 127.35. Short Sterling futures trade flat to down 1bp, in slight steepening trade with Jun17Jun18 spread rising to 17/18bp.

Tuesday liquidity report showed Monday's excess liquidity remained flat at €1.371T. Use of the marginal lending facility rose to €620M from €450M prior.

Corporate issuance saw another strong start to the week with $18.3B coming to market via 8 issuers headlined by Verizon $11B 5 part offering and Citigroup 2 part $2.5B offering, with the Verizon deal just over 2 times covered. Issuance for the week is already at the top end of analysts expectations, with monthly issuance topping $77B.

Political/In the Papers:

US Congressional Budget Office (CBO) scored American Health Care Act (AHCA): 14M more people would be uninsured in 2018 and 24M more by 2026

Looking Ahead

(PT) Bank of Portugal reports Jan ECB financing to Portuguese Banks: No est v €23.0B prior

06:00 (US) Feb NFIB Small Business Optimism: 105.6e v 105.9 prior

06:00 (DE) Germany Mar ZEW Current Situation Survey: 78.0e v 76.4 prior; Expectations Survey: 13.0e v 10.4 prior

06:00 (EU) Euro Zone Mar ZEW Survey Expectations: No est v 17.1 prior

06:00 (EU) Euro Zone Jan Industrial Production M/M: +1.3%e v -1.6% prior; Y/Y: 0.9%e v 2.0% prior

06:00 (EU) Daily Euribor Fixing

06:00 (ZA) South Africa to sell combined ZAR2.35B in 2023, 2035 and 2040 bonds

06:15 (CH) Switzerland to sell 3-month Bills

06.30 (UK) Weekly John Lewis LFL sales data

06:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

06:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

06:30 (UK) DMO to sell £2.25B in new 2927 Gilt

07:00 (ZA) South Africa Jan Manufacturing Production M/: No est v 0.3% prior; Y/Y: +1.6%e v -2.0% prior

07:00 (TR) Turkey to sell Floating 2022 Bonds; Yield: % v 4.87% prior

07:30 OPEC Monthly Report

07:45 (US) Weekly Goldman Economist Chain Store Sales

07:45 (US) Daily Libor Fixing

08:00 (IN) India Feb CPI Y/Y: 3.6%e 3.2% prior

08:00 (IS) Iceland Feb Unemployment Rate: No est v 3.0% prior

08:30 (US) Feb PPI Final Demand M/M: 0.1%e v 0.6% prior; Y/Y: 1.9%e v 1.6% prior

08:30 (US) Feb PPI Ex Food and Energy M/M: 0.2%e v 0.4% prior; Y/Y: 1.5%e v 1.2% prior

08:30 (US) Feb PPI Ex Food, Energy, Trade M/M: 0.2%e v 0.4% prior; Y/Y: No est v 1.6% prior

08:30 (CA) Canada Feb Teranet/National Bank HPI M/M: No est v 0.5% prior; Y/Y: No est v 13.0% prior

08:55 (US) Weekly Redbook Sales

09:00 (RU) Russia announces weekly OFZ bond auction

09:00 (PL) Poland Feb CPI M/M: 0.2%e v 0.4% prior; Y/Y: 2.1%e v 1.8% prior

09:00 (PL) Poland Feb M3 Money Supply M/M: +0.6%e v -1.3% prior; Y/Y: 8.4%e v 8.5% prior

09:00 (RU) Russia Jan Trade Balance: $11.6Be v $11.8B prior; Exports: $24.6Be v $31.1B prior; Imports: $13.5Be v $19.3B prior

09:00 (US) The Federal Open Market Committee (FOMC) begins 2-day policy meeting (decision on Wed)

09:15 (UK) Baltic Dry Bulk Index

10:00 (MX) Mexico Jan Industrial Production M/M: 0.0%e v -0.1% prior; Y/Y: 0.0%e v -0.6% prior; Manufacturing Production Y/Y: 2.5%e v 1.8% prior

10:00 (EU) Weekly ECB Forex Reserves:

10:50 (UK) BoE conducts reverse Gilt auction (over 15 years)

11:30 (US) Treasury to sell 4-Week Bills

12:00 (IS) Iceland Feb International Reserves (ISK): No est v 855B prior

12:00 (UR) Ukraine to sell Bonds

15:00 (CO) Colombia Jan Retail Sales Y/Y: 3.0%e v 6.2% prior

15:00 (CO) Colombia Jan Industrial Production Y/Y: 2.2%e v 2.2% prior

16:30 (US) Weekly API Oil Inventories

Crude Oil: Wide-Open For Further Weakness

GOLD (in USD) Continued weakness.

Gold's weakness is definitely on since the metal reached resistance given at 1263 (27/02/2017 high). Expected to reach support at 1177 (11/01/2017 low).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER (in USD) Heading lower.

Silver's selling pressures are important. Hourly support is given at 16.63 (27/01/2016 low). Expected to see continued bearish pressures.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude Oil (in USD) Wide-open for further weakness.

Crude oil's bearish pressures continues. The commodity has been unable to mount a serious challenge to 55.24 (03/01/2017 high) resistance. Strong support given at 49.61 (08/12/2016) has been broken. Expected to see deeper selling pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EURGBP: Heading Higher

EUR/CHF Renewed bearish pressures.

EUR/CHF's bullish pressures have increased sharply. Resistance given at 1.0762 (27/12/2016 high) has been broken. Anyway, the mediumterm pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Temporary surges seem the new normal for the CHF.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/JPY Targeting resistance at 123.31.

EUR/JPY's demand has rejuvenated . Hourly resistance at 121.34 (10/02/2017 high) has been broken. Strong resistance is given at a distance at 123.31 (27/01/2017 high). Expected to show further increase.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Heading higher.

EUR/GBP is pushing higher. Strong resistance given at 0.8854 (15/01/2017 high) is at stake. We rule out further weakness towards supports given at 0.8450 (03/01/2016 low) and at 0.8304 (05/12/2016). Expected to further strengthen.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

AUDUSD: Ready For Another Leg Lower

USD/CHF is still riding within uptrend channel and is on its way to monitor support implied by lower bound of the uptrend channel. Key resistance is given at a distance at 1.0344 (15/12/2016 high). Expected to consolidate.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

USD/CAD Bearish consolidation.

USD/CAD's bullish pressures are definitely on after breaking key resistance at 1.3353 (20/01/2017 high). Yet, as long as this resistance was not broken (20/01/2017 high), bullishness was limited. Expected to see further upside potential for the pair.

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Ready for another leg lower.

AUD/USD's technical structure is still negative. The road is wide-open for further weakness towards support given at 0.7494 (19/01/2017 low). Key resistance is given at 0.7778 (08/11/2016 high).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

USDJPY: Monitoring Resistance At 115.62

EUR/USD Setting higher lows.

EUR/USD continues to strengthen despite ongoing bearish consolidation. Hourly resistance given at 1.0679 (16/02/2017 high) has been broken while hourly support at 1.0493 (22/02/2017 low). The technical structure suggests deeper increase towards resistance at 1.0874 (08/12/2017 high).

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Weakening.

GBP/USD continues to edge lower despite ongoing consolidation since the pair has broken support given at 1.2254 (19/01/2017 low). The road is wide-open for further decline. Hourly resistance is now given at 1.2300 (05/03/2017 high).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Monitoring resistance at 115.62.

USD/JPY is pushing higher towards key resistance given at 115.62 (19/01/2016 high). Hourly support can be found at 113.56 (06/03/2017 low). Expected to push higher.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

FTSE 100 – Recovery Rally Nears Record High, Bullish Bias Favors Fresh Gains

FTSE remains supported and extended recovery from 7254 correction, ticks ahead of 7382 record high.

Fresh weakness of pound and uncertainty on nearing start of official UK/EU divorce helped the index to almost fully retrace near-term correction and look for fresh upside action.

Rise in mining stocks also helped index's rally.

Ascending 10SMA continues to track recovery and offers immediate support at 7345, ahead of Monday's low at 7331 and daily Tenkan-sen at 7318, which is expected to contain stronger downticks.

Upper targets above 7382 lay at 7441/61 (Fibo 138.2% and 161.8% projections), with extension towards 7511 (200% projection of the upleg from 7254) seen on stronger bullish acceleration.

Res: 7382, 7400, 7431, 7461

Sup: 7356, 7345, 7333, 7318

China Had A Start Start Into The Year, Frexit Is A Live Possibility

News and Events:

Chinese data suggests sustained growth

China's annual NPC (National People's Congress) 2017 economic objectives, which included a deceleration of GDP growth target to 6.5% (below 2016 6.5-7.0% target) grabbed the headlines. Yet rather than an indication of weaker outlook this conservative (and mature) number indicates an emphasis on stability rather than boastfulness through economic acceleration. In addition, February FX reserves point to a reversal of capital outflow, temporarily halting doomsday predictions.

January/February industrial production surprised slightly to the upside, printing at 6.3%y/y versus 6.2% expected and 6.0% previous reading. Fixed asset investment accelerated substantially and surged 8.9%y/y, widely above median forecast of 8.3% and previous reading of 8.1%. The only blot on this otherwise encouraging landscape is the retail sales gauge which decelerated to 9.5% (10.6% expected and 10.4% previous). However, in our opinion, the data provided further evidence that China is building towards a strong Q1. On a side note, the softening of rhetoric by US president Trump suggests that a trade war or nation specific traffic is unlikely (although a less punitive trade policy are highly probability). However, as with all populist leaders, when approval ratings sag they resort back to hardliner issues that got them into power in the first place.

On the FX side, after losing more than 1% against the USD since mid-January the Chinese yuan took breather. This morning the renminbi was trading at around 6.91, while off-shore the yuan was trading at around 6.90. We do not expected the yuan to weakness against the USD, at least not at the same pace as last year.

Moody's estimates growing Frexit risk

The credit rating agency estimates that a victory of Marine Le Pen, even though unlikely is not unconceivable. The National Front President would drive France towards a referendum on the exit of the European Union. Moody's warns that a return to the Franc would push France to default. Government bonds should be converted into Franc and the Franc would very likely be depreciated.

However we believe that the nightmare promised by Moody's seems a bit exaggerated especially when looking towards other European's countries direction such as Greece. This country does not need to exit the Eurozone to be in big trouble. Indeed Greece is living on never-ending austerity policies.

Whatever happens at the French elections, the new president will inherit a country with a ratio debt-to-GDP over than 100%. A Frexit would also push other European countries' bonds' yields and grades higher and weaken the single currency.

Today's Key Issues (time in GMT):

- Feb CPI Core MoM, last -1,50% EUR / 08:00

- Feb CPI Core YoY, exp 1,00%, last 1,10% EUR / 08:00

- Feb F CPI MoM, exp -0,30%, last -0,30% EUR / 08:00

- Feb F CPI YoY, exp 3,00%, last 3,00% EUR / 08:00

- Feb F CPI EU Harmonised MoM, exp -0,30%, last -0,30% EUR / 08:00

- Feb F CPI EU Harmonised YoY, exp 3,00%, last 3,00% EUR / 08:00

- Feb CPI MoM, exp 0,60%, last -0,70% SEK / 08:30

- Feb CPI YoY, exp 1,70%, last 1,40% SEK / 08:30

- Feb CPI CPIF MoM, exp 0,60%, last -0,70% SEK / 08:30

- Feb CPI CPIF YoY, exp 1,90%, last 1,60% SEK / 08:30

- Feb CPI Level, exp 319,54, last 317,5 SEK / 08:30

- Jan Mining Production MoM, last 0,70%, rev -0,30% ZAR / 09:30

- Jan Gold Production YoY, last -7,10%, rev -7,60% ZAR / 09:30

- Jan Platinum Production YoY, last -15,10% ZAR / 09:30

- Jan Mining Production YoY, exp 1,20%, last -1,90%, rev -3,10% ZAR / 09:30

- Jan Industrial Production SA MoM, exp 1,30%, last -1,60% EUR / 10:00

- Jan Industrial Production WDA YoY, exp 0,90%, last 2,00% EUR / 10:00

- Mar ZEW Survey Current Situation, exp 78, last 76,4 EUR / 10:00

- Mar ZEW Survey Expectations, last 17,1 EUR / 10:00

- Mar ZEW Survey Expectations, exp 13, last 10,4 EUR / 10:00

- Feb NFIB Small Business Optimism, exp 105,6, last 105,9 USD / 10:00

- Jan Manufacturing Prod NSA YoY, exp 1,60%, last -2,00% ZAR / 11:00

- Jan Manufacturing Prod SA MoM, exp 1,50%, last 0,30% ZAR / 11:00

- Feb CPI YoY, exp 3,60%, last 3,17% INR / 12:00

- Feb PPI Final Demand MoM, exp 0,10%, last 0,60% USD / 12:30

- Feb PPI Ex Food and Energy MoM, exp 0,20%, last 0,40% USD / 12:30

- Feb PPI Ex Food, Energy, Trade MoM, exp 0,20%, last 0,20% USD / 12:30

- Feb Teranet/National Bank HPI MoM, last 0,50% CAD / 12:30

- Feb PPI Final Demand YoY, exp 1,90%, last 1,60% USD / 12:30

- Feb Teranet/National Bank HP Index, last 200,34 CAD / 12:30

- Feb PPI Ex Food and Energy YoY, exp 1,50%, last 1,20% USD / 12:30

- Feb Teranet/National Bank HPI YoY, last 13,00% CAD / 12:30

- Feb PPI Ex Food, Energy, Trade YoY, last 1,60% USD / 12:30

- Jan Trade Balance, exp 11.6b, last 11.8b RUB / 13:00

- Jan Exports, exp 24.6b, last 31.1b RUB / 13:00

- Jan Imports, exp 13.5b, last 19.3b RUB / 13:00

- 4Q BoP Current Account Balance NZD, exp -2.425b, last -4.891b NZD / 21:45

- 4Q Current Account GDP Ratio YTD, exp -2,70%, last -2,90% NZD / 21:45

- 4Q BoP Current Account Balance, exp -$12.00b, last -$3.40b INR / 22:00

- ECB President Mario Draghi Speaks in Frankfurt EUR / 23:00

- Feb Foreign Direct Investment YoY CNY, exp -4,20%, last -9,20% CNY / 23:00

- Feb Budget Balance YTD, exp -350.0b, last -23.4b RUB / 23:00

- Feb Tax Collections, exp 93663m, last 137392m BRL / 23:00

The Risk Today:

EUR/USD continues to strengthen despite ongoing bearish consolidation. Hourly resistance given at 1.0679 (16/02/2017 high) has been broken while hourly support at 1.0493 (22/02/2017 low). The technical structure suggests deeper increase towards resistance at 1.0874 (08/12/2017 high). In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD continues to edge lower despite ongoing consolidation since the pair has broken support given at 1.2254 (19/01/2017 low). The road is wide-open for further decline. Hourly resistance is now given at 1.2300 (05/03/2017 high). The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY is pushing higher towards key resistance given at 115.62 (19/01/2016 high). Hourly support can be found at 113.56 (06/03/2017 low). Expected to push higher. We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF is still riding within uptrend channel and is on its way to monitor support implied by lower bound of the uptrend channel. Key resistance is given at a distance at 1.0344 (15/12/2016 high). Expected to consolidate. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3445 | 1.1731 | 121.69 |

| 1.0954 | 1.3121 | 1.0652 | 118.66 |

| 1.0874 | 1.2771 | 1.0344 | 115.62 |

| 1.0641 | 1.2136 | 1.0081 | 115.08 |

| 1.0454 | 1.1986 | 0.9967 | 111.36 |

| 1.0341 | 1.1841 | 0.9862 | 106.04 |

| 1.0000 | 1.0520 | 0.9550 | 101.20 |

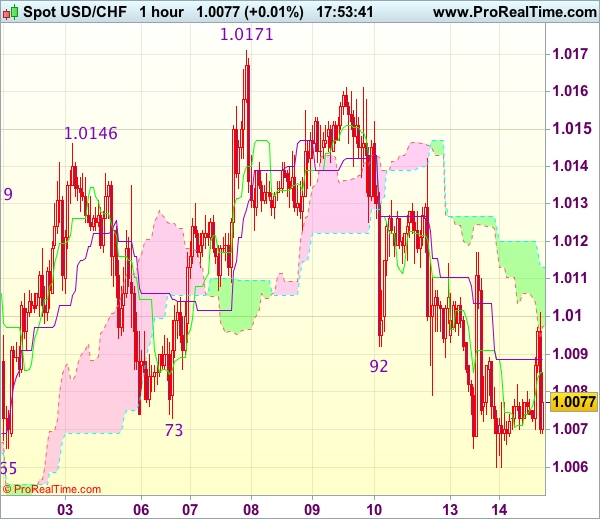

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 1.0083

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s marginal fall to 1.0060, lack of follow through selling on break of previous support at 1.0065 and current rebound suggest further consolidation above yesterday’s low would be seen and gain to 1.0110-20 cannot be ruled out, however, a break of resistance at 1.0142 is needed to signal the retreat from 1.0171 (last week’s high) has ended, bring another rise towards this level later.

On the downside, below said support at 1.0060 would signal the fall from 1.0171 top is still in progress and may bring further fall to 1.0035-40 but support at 1.0009 should remain intact, bring rebound later. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

AUDUSD – Mixed Technicals Show No Clear Direction

The pair eases after two-day recovery was capped by daily Tenkan-sen at 0.7590 yesterday, shifting near-term focus lower again.

Fresh weakness pressures strong support at 0.7531 (55/200 SMA Golden cross), increasing risk of renewed attempt through strong 0.7531/0.7494 support zone (defined by 200 and 100SMA's).

Despite strong bullish signals after pullback from 0.7739 was contained by rising daily cloud, fresh weakness suggests that corrective phase is not over and keeps the downside at risk.

Mixed readings of daily chart studies show no clear direction, with break through pivots at 0.7584/0.7614 (upper) or 0.7531/0.7494 (lower) needed for stronger direction signals.

Fresh strength of the US dollar in anticipation of tomorrow's rate hike, however, keeps near-term bias shifted lower for now.

Res: 0.7590, 0.7614, 0.7643, 0.7700

Sup: 0.7531, 0.7519, 0.7494, 0.7448