Sample Category Title

European Market Update: Market Expectations Are For A Strong February Employment Print

Market expectations are for a strong February employment print

Notes/Observations

Market expectations are for a strong February employment print today following ADP on Wednesday

BOE 12-month inflation expectation hits a 3-year high (2.9% v 2.8% prior)

Overnight:

Asia:

South Korea Court Justices presents its impeachment ruling on President Park Geun-hye: Unanimously upholds impeachment decision

PBoC Gov Zhou Xiaochuan reiterated that monetary policy was prudent and neutral; to fine-tune policy based on situation; had many tools for monetary policy and would not overreact to drop in FX reserves

PBoC Dep Gov Yi Gang reiterated govt to stick to current FX framework to keep yuan basically stable. Reiterated view that China will not devalue Yuan to stimulate exports and definitely not engage in a currency war

Europe:

German Chancellor Merkel on EU Leader Summit: ECB chief Draghi reiterated view to leaders that they can't rely on ECB stimulus measures indefinitely (need to implement structural reforms

France President Hollande: UK PM May did not give any hints about Brexit strategy at the EU leaders summit

IMF's Lagarde: French Euro exit would make France poorer and would lead to a period of grave uncertainty

Americas:

Treasury Sec Mnuchin: Congress should raise debt limit at first opportunity. Treasury will take other extraordinary measures to prevent US default

Energy:

Repsol [REP.ES] said to make the biggest US Onshore oil discovery of about 1.2B barrels in Alaska; production to start in 2021

Economic data

(DE) Germany Feb Wholesale Price Index M/M: 0.5% v 0.8% prior; Y/Y: 5.0% v 4.0% prior

(DE) Germany Jan Current Account: €12.8B v €15.5Be; Trade Balance: €14.8B v €18.0Be; Exports M/M: +2.7% v +2.0%e; Imports M/M: +3.0% v +0.5%e

(DE) Germany Q4 Labor Costs Q/Q: 1.5 v 0.6% prior; Y/Y: 3.0 v 2.3% prior

(NO) Norway Feb CPI (miss) M/M: 0.4% v 0.8%e; Y/Y: 2.5% v 2.9%e

(NO) Norway Feb CPI Underlying M/M: 0.5% v 0.8%e; Y/Y: 1.6% v 2.0%e

(RO) Romania Feb CPI M/M: -0.1% v -0.1%e; Y/Y: 0.2% v 0.2%e

(FR) France Jan Industrial Production (miss) M/M: -0.3% v +0.5%e; Y/Y: -0.4% v 0.4%e

(FR) France Jan Manufacturing Production M/M: -1.0% v +0.5%; Y/Y: -1.3% v +0.3%e

(IT) Italy Q4 Unemployment Rate: 11.9% v 11.7%e

(UK) Jan Visible Trade Balance: -£10.8B v -£11.1Be, Total Trade Balance: -£2.0B v -£3.1Be, Trade Balance Non EU: 2.5B v -£2.4Be

(UK) Jan Industrial Production M/M: -0.4% v -0.5%e; Y/Y: 3.2% v 3.2%e

(UK) Jan Manufacturing Production M/M: -0.9% v -0.7%e; Y/Y: 2.7% v 2.9%e

(UK) BoE/TNS Feb Quarterly Inflation expectations Survey (next 12-months): 2.9% v 2.8% prior

Fixed Income Issuance:

(IT) Italy Debt Agency (Tesoro) sold €6.5B vs. €6.5B indicated in 12-month Bills; Avg Yield: -0.226% v -0.247% prior; Bid-to-cover: 1.58x v 1.68x prior

(ZA) South Africa sold total ZAR1.29B in I/L 2029, 2033 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 +0.7% at 3,434, FTSE +0.4% at 7,344, DAX +0.5% at 12,044, CAC-40 +0.5% at 5,008, IBEX-35 +0.7% at 10,069, FTSE MIB +0.8% at 19,727, SMI +0.2% at 8,654, S&P 500 Futures +0.3%]

Market Focal Points/Key Themes: European equity indices are trading sharply higher after ECB President Draghi's comments yesterday continue to add support, and as market participants await the US non-farm payrolls scheduled later today; Banking stocks across Europe trading notably higher with the Eurostoxx led by shares of Deutsche Bank, ING and SocGen; Italian FTSE MIB outperforming as the heavily weighted peripheral lenders in the index trade sharply higher; Energy, commodity and mining stocks also trading higher as oil and copper pare back some recent losses.

Upcoming scheduled US earnings (pre-market) include Buckle, Genesco, Hibbett Sporting Goods, Kirklands, Ply Gem, Sprague Resources, and Vail Resorts.

Equities (as of 09:50 GMT)

Consumer Discretionary: [JD Wetherspoon JDW.UK -3.1% (H1 results)]

Energy: [Repsol REP.ES +2.6% (major oil discovery in Alaska), Spie SPIE.FR -0.6% (FY16 results)]

Financials: [Compagnie Financiere Tradition CFT.CH +7.0% (FY16 results), JRP Group JRP.UK +6.3% (FY16 results), Segro SGRO.UK -4.0% (rights issue, acquires 50% stake in APP JV)]

Healthcare: [Synairgen SNG.UK +11.2% (LOXL2 positive data)]

Industrials: [Semperit SEW.DE -0.6% (FY16 results), SFS Group SFSN.CH -1.2% (FY16 results)]

Materials: [Akzo Nobel AKZA.NL +4.2% (PPG reportedly planning second bid)]

Telecom: [BT Group BT.UK +4.6% (BT and Ofcom reach Openreach governance agreement)]

Speakers

ECB's Vasiliauskas (Lithuania): Euro Area economy is recovering

Foreign Sec Boris Johnson: Would not be reasonable for EU to expect Britain to accept a vast bill to settle its liabilities after Brexit; government would fight any demand for payment.

South Korea Fin Min Yoo commented following Court formal impeachment ruling that the domestic economic policy would be managed as usual

S&P on South Korea: Impeachment ruling had no immediate impact on sovereign rating

China Foreign Ministry reiterated urging of stability on Korean peninsula

Currencies

Focus on US payroll data in session. Market expectations are for a strong February employment print today following ADP on Wednesday but analysts noted that the average hourly earnings would be more important for the USD price action as it would suggest higher domestic inflationary pressures. The key factor would be any change in market expectations for the number of Fed rate hikes in 2017 (currently seen at 3).

Dealers perceived a hawkish tilt from Draghi during Thursday's press conference which saw a sell-off in bunds and EURUSD higher to test above the 1.06 level. German yields were set for biggest fortnightly rise in nearly two years as a result.

Japanese yen dropped to a seven-week low amid speculation a stronger reading in US payroll data could support three rate hikes by Federal Reserve this year. USD/JPY pair probing the mid-115 area ahead of the jobs report.

The GBP/USD was little changed despite a plethora of mixed economic data for January. A quarterly BOE inflation expectation survey saw the 12-month outlook hot a three year high of 2.9%. The central bank had previously cautioned that a rise in inflation could likely to strain the spending power of households who had been driving the recovery in the economy since the financial crisis

EUR/NOK cross was higher after Norway Feb CPI data came in below expectations. The cross tested the 9.12 level for fresh 2017 highs.

Fixed Income:Bund futures trade at 159.67 down 32 ticks on risk on trade following on from a mildly hawkish Draghi in yesterdays ECB press conference. Yields continue to move higher recording the largest fortnightly gain in two years. Support moves to 159.44 low followed by 159.17. Resistance moves to 160.20 followed by 160.66 then 161.06.

Gilt futures trade at 126.00 down 45 ticks aided by slightly stronger Industrial and Manufacturing data out of the UK. Support moves to 125.57 followed by 125.24. Resistance remains at 126.87 followed by 127.35. Short Sterling futures trade flat to down 2bp, in steepening trade with Jun17Jun18 spread widening to 17/18bp.

Friday liquidity report showed Thursday's excess liquidity rose to €1.365T up €9B from €1.356T prior. Use of the marginal lending facility rose to €136M from €111M prior.

Corporate issuance saw $5.5B come to market via 6 issuers as weekly issuance topped $40B. Issuance was led by Delta Airlines $2.0B 2 part offering and Cintas Corp $1.7B 3 part offering. For the week ending March 8th Lipper US Fund lows reported IG funds net inflows of $3.48B bringing YTD Net inflows to $29.43B. High Yield funds reported net outflows of $2.12B bringing YTD outflows to $743M.

Looking Ahead

(PE) Peru Jan Trade Balance: $0.2Be v $1.0B prior

(MX) Mexico Feb Nominal Wages Y/Y: No est v 4.1% prior

06:00 (PT) Portugal Feb CPI M/M: No est v -0.6% prior; Y/Y: No est v 1.3% prior

06:00 (PT) Portugal Feb CPI EU Harmonized M/M: No est v -0.7% prior; Y/Y: 1.5%e v 1.3% prior

06:00 (IE) Ireland Jan Industrial Production M/M: No est v -11.7% prior; Y/Y: No est v -1.3% prior

06:00 (IE) Ireland Jan Property Prices M/M: No est v -0.4% prior; Y/Y: No est v 8.1% prior

06:00 (UK) DMO to sell combined £2.0B in 1-month, 3-month and 6-month bills (£0.5B, £0.5B and £1.0B respectively)

06:30 (CL) Chile Central Bank Economist Survey

06:30 (IN) India Weekly Forex Reserves

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Feb IBGE Inflation IPCA M/M: 0.4%e v 0.4% prior; Y/Y: 4.9%e v 5.4% prior

07:00 (IN) India Jan Industrial Production Y/Y: +0.5%e v -0.4% prior

08:00 Spain Debt Agency (Tesoro) announces upcoming bond issuance

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Feb Change in Nonfarm Payrolls: +200Ke v +227K prior, Change in Private Payrolls: +215Ke v +237K prior, Change in Manufacturing Payrolls: +10Ke v +5K prior

08:30 (US) Feb Unemployment Rate: 4.7%e v 4.8% prior, Underemployment Rate: No est v 9.4% prior, Change in Household Employment (civilian labor force): No est v +159.7K prior, Civilian Labor Force Participation Rate: No est v 62.9 prior

08:30 (US) Feb Average Hourly Earnings M/M: 0.3%e v 0.1% prior; Y/Y: 2.8%e v 2.5% prior; Average Weekly Hours: 34.4e v 34.4 prior

08:30 (CA) Canada Feb Net Change in Employment: -5.0Ke v +48.3K prior; Unemployment Rate: 6.8%e v 6.8% prior

10:00 (UK) Feb NIESR GDP Estimate: 0.6%e v 0.7% prior

11:00 (EU) Potential sovereign ratings after European close: Germany Sovereign Debt to be rated by Fitch

13:00 (US) Weekly Baker Hughes Rig Count data

13:00 (CO) Colombia Central Bank Feb Minutes

14:00 (US) Feb Monthly Budget Statement: -$190.0Be v +$51.3B prior

Bears Continue to Open Short Positions on GBPUSD

Janet Yellen announced a possible increase of the interest rates at the meeting on Friday, March 3. The stable growth of the US economy is main condition for that increase. FedWatch Tool is at the level 84.1% level currently.

FedWatch Tool

Source: cmegroup.com

Our attention is glued to the labor market of the United Stated. Many experts think that the growth of the Nonfarm Payrolls will lower by 16.3% to 190,000. They also anticipate the decrease of the unemployment rate from 4.8% to 4.7%. But the average hourly earnings are likely to increase to 0.3% according to the experts' expectations.

Source: investing.com

We will wait for an optimistic report as the last statistics from the US was at a high level. The demand for USD should grow.

The technical analysis of the GBP/USD currency pair

The key levels:

support: 1.2175, 1.2050

resistance: 1,2300, 1.2400, 1.2550

GBP may weaken against USD. The technical indicators tell us about the sellers' strength. 50 MA is below 200 MA, while MACD has moved to the negative zone. This histogram continues to decline at the moment.

I recommend traders to open short positions, if the price reaches the 1.2175 support level and fixes there. The pair may move to 1.2050. I advise to use a trailing stop while trading this currency pair.

NFP Preview: EUR/USD Trapped Within The Rectangle Consolidation

Total Payrolls showed 227k increase in January that was much higher than the consensus of 190k. The NFP data was the largest in couple of months, reassuring strong US labor market. Additionally we saw unemployment edging up to 4.8 % and the only decrease was in the average hourly earnings annual rate. My expectations from today's US data are that NFP will come better than expected (210k-215k vs 190k expected) while Unemployment Rate and Average Hourly Earnings will roughly stay the same. But you can never be 100 % sure of data so we need to wait and see.

Technically the rallies on EUR/USD are still sold into and depending on NFP we might see a fade on rallies close to 1.0675. Currently the pair is trapped within the rectangle range and we can clearly see 3 trend lines that have formed Xcross ™ at important levels. Today's NFP levels to watch for are: 1.0675 (H5, ATR overshot), 1.0642 (ATR top ), 1.0600 (H3, Xcross ™), 1.0572 (ATR, DPP, Xcross ™) and 1.0525 (L4, Xcross ™).

Gold Could Extend Weakness To $1191 After Break Below $1200 Pivot

Spot Gold is in steep descend that broke below psychological $1200 support today and signals further weakness. Recent strong bearish acceleration through some important supports ($1212, $1207, $1200) generated strong bearish signals for extension of two-legged pullback from $1263 (27 Feb peak). US dollar's strong bullish sentiment on rate hike expectations keeps the yellow metal under pressure. Also, firmly bearish technical studies support the notion. After taking out $1200 pivot, bears are eyeing daily Ichimoku cloud top at $1191, break of which would spark further weakness for full retracement of $1180/$1263 rally ($1180 – 27 Jan trough/daily cloud base). Broken 55 and 100SMA's now act as solid barriers at 1207/10, ahead of broken Fibo 61.8% at $1212. US NFP data are in focus.

Res: 1200, 1207, 1210, 1216

Sup: 1195, 1191, 1188, 1180

AUDUSD – Close Below 200SMA And Penetration Into Daily Cloud Generated Strong Bearish Signal

Extended pullback from 0.7739 high closed below 200SMA and penetrated daily cloud (cloud top lies at 0.7515), generating another strong bearish signal.

The pair came under increased pressure that signals further extension of corrective phase of 0.7158/0.7739 rally that already broke below its 38.2% retracement level at 0.7517.

Meantime, corrective upticks, signaled by oversold slow stochastic, should remain capped under daily Tenkan-sen (currently at 0.7593).

US jobs data are expected to give more clues about near-term action.

Res: 0.7529, 0.7568, 0.7587, 0.7593

Sup: 0.7515, 0.7489, 0.7448, 0.7426

USDJPY – Break Above 115.00 Barrier To Trigger Further Upside, Daily Cloud Underpins

Strong bullish acceleration extends into third day and the price is establishing above 115.00 handle after meeting targets at 115.08/36.

Thickening daily cloud is continuing to underpin, along with daily studies that are now in full bullish setup.

Bulls are eyeing next target at 115.60 (19 Jan high), with extension through pivot at 115.91 (Fibo 61.8% of 118.59/111.57) to be attracted on solid NFP numbers.

Daily Ichimoku cloud (spanned between 114.51/74) and broken 55 SMA (114.30) should contain dips.

The pair is on track for repeated weekly bullish close that confirms strong bullish stance.

Res: 115.60, 115.91, 116.62, 116.91

Sup: 115.13, 114.74, 114.51, 114.30

GBPUSD Is Consolidating Around Fibo Support At 1.2155 Ahead Of US Data, Overall Structure Remains Bearish

Yesterday's Doji signals indecision at 1.2155 support (Fibo 76.4% of 1.1986/1.2704 rally) that was dented but is still acting as valid support, following repeated rejection to close below it.

Overall strong bearish tone keeps downside in focus with firm break below 1.2155 expected to open way towards 1.1986, January's year-to-date low.

Meantime, the pair is expected to consolidate recent fall. Initial barrier at 1.2200 zone is holding for now and keeping intact next pivot at 1.2260 (falling 10 SMA).

Signals of reversal require break above 1.2300 lower platform (reinforced by daily Tenkan-sen).

Res: 1.2171, 1.2212, 1.2260, 1.2300

Sup: 1.2155, 1.2133, 1.2100, 1.2035

EURUSD – Daily Cloud Is Key

The Euro is maintaining positive near-term tone and attempting again into daily cloud (spanned between 1.0605/1.0653). Yesterday's rally turned near-term focus higher but close well below cloud base, kept overall bearish bias intact. Current rally could be seen as positioning ahead of fresh weakness, as thickening daily cloud continues to weigh. Selling upticks scenario is still favored, with good barriers at 1.0620/26 (Fibo 38.2% of 1.0827/1.0492/30 SMA) seen ideally capping extended upticks. Alternative scenario requires firm break above daily cloud top (1.0653), reinforced by falling 100SMA to bring bulls fully in play. NFP data are eyed for stronger signals.

Res: 1.0626, 1.0638, 1.0653, 1.0700

Sup: 1.0586, 1.0570, 1.0541, 1.0524

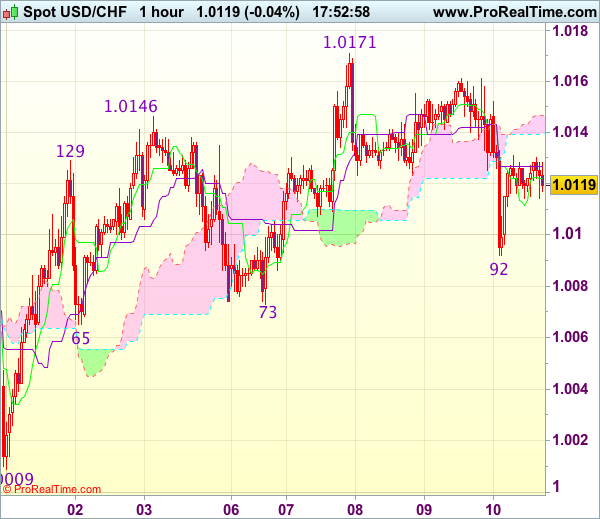

Trade Idea Update: USD/CHF – Buy at 1.0100

USD/CHF - 1.0120

Original strategy :

Buy at 1.0100, Target: 1.0200, Stop: 1.0070

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0100, Target: 1.0200, Stop: 1.0070

Position : -

Target : -

Stop : -

As the greenback found good support at 1.0092 and has staged a strong rebound, suggesting low is possibly formed there and consolidation with mild upside bias is seen for gain to 1.0145-50, however, break of resistance at 1.0171 is needed to signal recent erratic rise from 0.9861 low has resumed and extend further gain to 1.0200-10 but near term overbought condition should limit upside to 1.0220-25 and price should falter below previous chart resistance at 1.0248.

In view of this, we are looking to buy dollar on dips as 1.0100 should limit downside and bring such rise. Below support at 1.0073 would abort and signal top has been formed instead, risk weakness to 1.0040-45 but reckon support at 1.0009 would remain intact.

Trade Idea Update: GBP/USD – Stand aside

GBP/USD - 1.2175

Original strategy :

Sell at 1.2215, Target: 1.2115, Stop: 1.2250

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has recovered after holding above support at 1.2135, suggesting consolidation above this level would be seen and corrective bounce to 1.2210-15 is likely, however, reckon upside would be limited to 1.2245-55 but price should falter well below resistance at 1.2301, bring another decline later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Below said support at 1.2135 would signal recent decline has once again resumed and extend weakness to 1.2100, however, loss of near term downward momentum should prevent sharp fall below 1.2070-75 and price should stay above 1.2050, risk from there is seen for a rebound later.