Sample Category Title

U.S. Payroll Employment Up Solidly in February

- Employment rose 235k following a revised 238k (was 227k) increase in January. Private-sector jobs rose 227k (up from 221k in January) with government jobs up 8k following a 17k January gain.

- The unemployment rate declined to 4.7% from 4.8% in January

The February employment gain was boosted by a 95k surge in private sector goods-producing jobs (the largest monthly gain since March 2000) with construction employment up 58k (to build on a 40k jump in January) and manufacturing sector headcount up 28k to mark a third consecutive solid monthly gain. Private service-sector job growth slowed to 132k from 167k in January. Employment in the retail sector declined 26k after a 40k jump in January.

The dip in the unemployment rate (calculated from the separate household survey) occurred despite a tick higher in the participation rate to 63.0% from 62.9% in January.

Hours worked inched up 0.2% in February and 1.4% from a year ago. Hourly wages also rose 0.2% from January and the year-over-year rate ticked up to 2.8% to retrace most of a dip to 2.6% in January from (a cycle high) 2.9% in December.

Our Take:

Given comments from Fed officials, including Chair Yellen, in recent weeks, it would likely have taken a significant downside surprise to derail market expectations that were already pricing in about 90% odds of a 25 basis point hike to the fed funds target range following next week's FOMC meeting before the release of today's numbers. Although the earlier-reported 299k surge in private employment in the ADP report earlier this week may have boosted some expectations for today's job growth numbers to unrealistic levels, solid employment growth (well-above the underlying 'trend' rate), a dip in the unemployment rate, and a tick higher in wage growth should all provide reassurance that labour markets continue to tighten. We continue to expect a 25 basis point rate hike from the Fed next Wednesday. With an increase in rates, barring some unexpected shock, appearing very likely, attention is likely to shift to the expected pace of future hikes (Previous Fed projections suggested three hikes were felt to be appropriate this year) with a stronger economy arguing higher rates are needed but with considerable uncertainty remaining in the outlook, particularly around the future of U.S. government policy.

Canada’s Job Market Keeps Rolling

- 15K jobs created in February while labour force dipped by 19.6K pushing unemployment rate to 6.6%

- Today's labour market report went some distance to allay concerns about the mix of part-time and full-time job creation with 105K full-time positions created and 89K part-time jobs lost. In the first two months of the year, full-time employment grew 121K.

- Service sector employment rose 30K while goods producers cut 15K positions

- The unemployment rate fell 0.2 ppt to stand at the lowest level since November 2008

- Participation in the labour market fell in February however 175K more people were in the labour force than a year earlier

- Hours worked rose 0.2% from January; pace of decline from a year ago eased to -0.3% from -0.8%

- Wage growth remains tepid, earnings for permanent workers rose 1.1% from February 2016

Our Take:

Another, albeit more modest, rise in employment in February kept the string of gains running that started last summer just as the economy shifted into higher gear. The stronger growth generated increased demand for labour and a rise in capacity usage with the utilization rate touching a two-year high in late 2016. These reports may give the Bank fodder to reassess the degree of "persistent economic slack in Canada". The wage numbers however have been surprisingly weak and appear out of whack with strong employment gains with the six-month run rate at 36K. Given the lag between job creation and higher wage demands, a recovery in wage growth is likely to materialize later this year. Additionally, the rebound in commodity prices and stronger growth are fueling expectations that inflation will move higher, not lower as was the concern early last year. In its March statement, the Bank also went out of its way to contrast conditions at home with those in the US delivering a clear message that even if the Fed ramps up the pace of rate increases, hikes in Canada are a long way off.

Jobs Data Does Rate Hike Chances No Harm at All

It may not have been the knockout NFP that the ADP release on Wednesday indicated it could be, but today's US jobs report was more than adequate to justify a rate hike next week, assuming of course that the markets have correctly interpreted the Fed's very deliberate hawkish delivery over the last few weeks.

It's difficult to find anything to be down about in the jobs report, with job creation being well above the 12 month average and far exceeding what the Fed deems to be good enough. Unemployment fell even as participation rose to 63% - only the second time it's reached that level since April 2014 - while average hourly earnings rose to 2.8% year on year, not quite good enough yet but heading in the right direction.

All things considered, if the Fed was keen to raise interest rates next week, as it indicated it is, then today's report will only have aided the decision. The dollar may well have weakened following the release but this is probably due to the NFP number falling short of the ADP reading which raised people's expectations. The only thing standing in the way of a rate hike now is the Fed itself but after its efforts over the last few weeks, surely even it won't bottle it now.

The drop off in the US dollar has triggered some interesting moves, for example in EURUSD, where the pair has broken above the range it has been contained within for almost three weeks. As of yet, the breakout has not triggered a substantial move to the upside, which could be expected if a large number of stops had been triggered. Perhaps this suggests we're seeing a false breakout and the pair will once again settle back inside the range. Alternatively, another move above today's highs could break down what's left of the resistance, with the next notable level coming around 1.0680.

The commodity currencies have been particularly battered as of late, with dollar strength and its impact, among others, on dollar-denominated commodities delivering a double blow to them. The AUDUSD is getting some relief following the jobs data, just as a very important support, around 0.75 was coming under significant pressure. With 0.7550 currently proving to be a strong resistance level to the upside - prior support - the relief may not last very long but as long as the pair doesn't break above 0.7633 - this week's high - then 0.75 may not be out of the woods quite yet.

US: Hiring Spree Continues in February, Solidifying Case for Rate Hike Next Week

Non-farm payrolls increased by 235k in February, or well ahead of the 200k expected by the street. Revisions to the previous two months' of payrolls added 9k positions with January hiring now reported as 238k.

Private payrolls rose by 227k, some 12k above the consensus expectations for 215k. Private services hiring was led by health care & education (+62k), business services (+37k), leisure & hospitality (+26k) and transport (+16k). Goods hiring was nothing short of phenomenal, with construction (+58k) and manufacturing (+28k) both having great months, with mining & logging (+9k) even adding to the mix. Government hiring (+8k) was modest, with federal level hiring (+2k) up despite a hiring freeze put in by the new administration.

The unemployment rate ticked down by 0.1 percentage points to 4.7% as the huge gain in employment was more than enough to offset the number of people re-entering the labor force. The additional influx has lifted the participation rate up by 0.1pp to 63.0% on the month - the highest level in nearly a year. Other underemployment measures were also lower, with the broadest measure (U-6) down 0.2pp to 9.2% - matching its level of April 2008.

Average hourly earnings rose by 0.2% during the month, slightly disappointing expectations for a 0.3% m/m print, but this came atop of upward revisions to the previous months. On the whole, the year-over-year wage growth accelerated from 2.6% to 2.8% in February.

Average weekly hours were unchanged at 34.4.

Key Implications

This was a solid employment report any way you slice it. The headline blew past expectations, already elevated given the outsized ADP print mid-week. Moreover, the hiring was very broad, with the number of industries showing increases at its highest level since December 2015 - with all but retail and utilities adding jobs on the month. The same was true for manufacturing industries, with the diffusion index at its highest level in more than two years. Mining too, showed resilience, adding jobs for the fourth consecutive month - underscoring the notion that the worst is behind the sector.

The one note of caution has perhaps to do with some of the seasonality that could have crept into the data, particularly in weather-affected sectors. A mild Northeastern winter could have brought forward many construction projects and hiring, something that was apparently not offset by the heavy-rains in California. This suggests that some caution may be warranted as far as hiring across these sectors in the coming months.

Interestingly, the wage print, while decent at 0.2% m/m in both February as well as in the month prior, did not show as much strength as was anticipated, particularly given the implementation of minimum wage legislation across 19 states in January. Having said that, at 2.8% on a year over year basis, and with broad improvement in underutilization measures, we think this report all but solidifies a rate hike from the Fed next Wednesday, with two more likely to come later this year.

Canadian Jobs Kept on Coming in February

The Canadian economy continued to produce jobs in February, adding 15.3k positions on net. Labour market participation fell slightly, resulting in a 0.2 percentage point drop in the unemployment rate to 6.6.

The high level details of the report were strong, with 105.1k net new full-time positions added – the strongest gain since May of 2006. Offsetting this was a 89.1k drop in part-time jobs. The advance was driven by employees (+10k), with a smaller net gain in self-employment (+5k)

By broad sector, it was the private sector (+16.7k) that drove the increase, as the public sector shed jobs on net in February (-6.8k).

Gains were led by the service side of the economy (+30.1k), as employment among goods-producers pulled back (-14.8k). On the positive side of the ledger were trade (+19.1k), public administration (+11.9k), and transportation (+8.8k). The largest net job declines were seen in construction (-8.5k), manufacturing (-5.2k), and professional services (-4.5k).

The overall gain in net employment masked a divergent regional performance: British Columbia (+19.4k) and Saskatchewan (+8.0k) saw healthy net gains, while Quebec (-11.1k) and Nova Scotia (-6.8k) were among those reporting declines.

In spite of the strong gains in full-time work, hour worked fell by 0.3% year-on-year in February – their third consecutive decline. Similarly, hourly earnings grew just 1.1% year-on-year, continuing the trend of weakness that has emerged since the summer of last year.

Key Implications

Wow. Another month of jobs data, and another strong print that confounded market expectations. While this data series can be quite noisy, a robust trend in hiring has begun to emerge, reinforced by gains in full-time work, and suggesting the narrative that the Canadian economy has started to shake off many of the setbacks it faced in the past few years.

If there is a fly in the ointment, it has to be the ongoing declines in hours worked. This suggests that even with strong gains in full-time work, the jobs being created may be at the lower end of the hours scale –perhaps pointing to a change in the quality of work on offer (Statistics Canada defines full-time as working 30 or more hours per week). Further evidence regarding quality comes from the hourly earnings figures, which have been quite weak as of late. On this point, however, we note that other, less timely employment surveys point to still healthy wage growth.

For the Bank of Canada, February's figures will undoubtedly be welcome. That said, the Bank of Canada doesn't target employment, and from an inflation perspective there is little here to move the needle in the near term in light of weakness in reported wage growth. That said, today's report does to the mounting evidence that the Canadian economy is seeing a return to sustained healthy growth, which should absorb remaining slack and lead to eventual inflationary pressures. This process will take time, however, and the Bank of Canada will want to continue supporting it and will likely be reluctant to raise rates until well into next year.

Trade Idea: EUR/GBP – Buy at 0.8660

EUR/GBP - 0.8737

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Buy at 0.8600, Target: 0.8700, Stop: 0.8560

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8660, Target: 0.8760, Stop: 0.8620

Position : -

Target : -

Stop : -

As the single currency has continued moving higher after breaking above resistance at 0.8646, adding credence to our view that the fall from 0.8857 has ended at 0.8403 and upside bias remains for the rally from there to extend further gain to 0.8750, then 0.8770, however, loss of near term upward momentum should prevent sharp move beyond latter level and price should falter well below 0.8800, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as 0.8600 should limit downside. Below support at 0.8547 would suggest first leg of rebound from 0.8403 has ended, bring weakness to 0.8520-25 but support at 0.8509 should contain downside and bring another rise later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Buy at 1.3350

USD/CAD - 1.3449

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3400, Target: 1.3570, Stop: 1.3340

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3350, Target: 1.3550, Stop: 1.3290

Position: -

Target: -

Stop:-

The greenback has retreated after rising to 1.3535, suggesting consolidation below this level would be seen and initial downside risk is for pullback to 1.3400, however, reckon downside would be limited to 1.3370-75 support and renewed buying interest should emerge around 1.3350-55 (38.2% Fibonacci retracement of 1.3056-1.3535) and bring another rise later, above said resistance at 1.3535 would extend recent upmove for further gain to 1.3570-75 and possibly towards 1.3600 but near term overbought condition should prevent sharp move beyond 1.3640-50, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy on further pullback as 1.3350 should limit downside. Only below 1.3295-00 (50% Fibonacci retracement of 1.3056-1.3535) would signal top is formed, risk correction to 1.3250-60 but price should stay well above indicated previous resistance at 1.3212 (now support), bring another rise later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

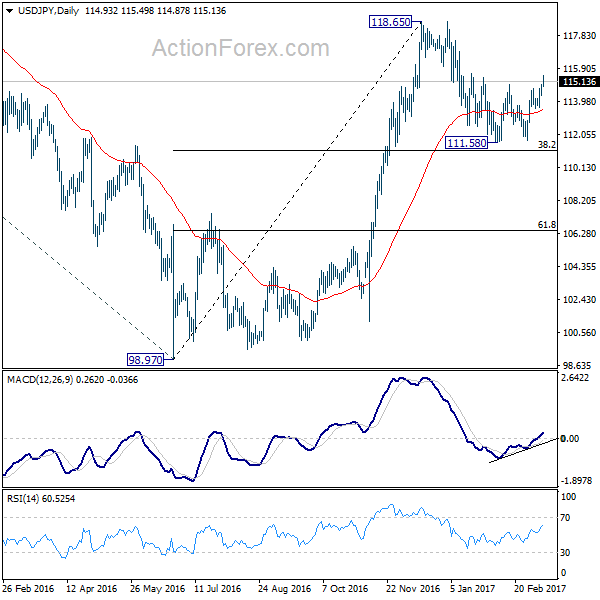

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 114.47; (P) 114.74; (R1) 115.19; More...

USD/JPY retreats mildly in early US session but at this point, intraday bias remains on the upside. Current development indicates near term reversal on double bottom pattern (111.58, 111.68). That's whole correction from 118.65 is completed at 111.58. Further rally would be seen to retest 118.65 resistance. Break will resume whole rally from 98.97 and target 125.85 high next. On the downside, break of 113.60 support is now needed to indicate completion of the current rise. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

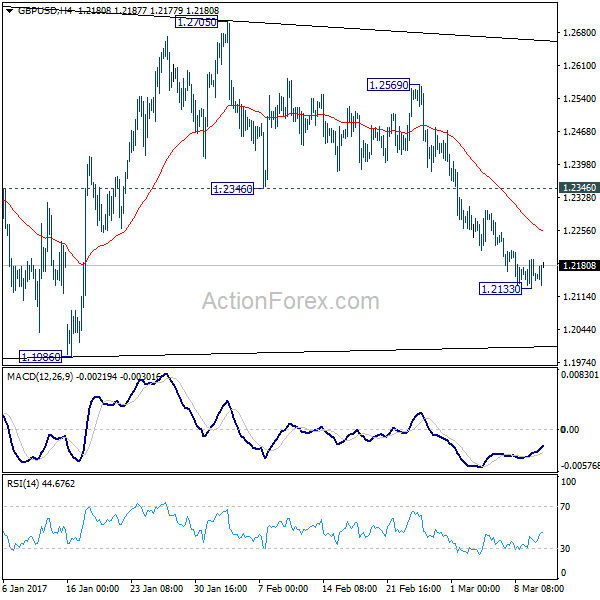

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2131; (P) 1.2163; (R1) 1.2193; More...

A temporary low should be in place at 1.2133 in GBP/USD and intraday bias is turned neutral first. Upside of recovery should be limited by 1.2346 support turned resistance and bring another decline. As noted before, consolidation pattern from 1.1946 should have completed with three waves to 1.2705 already. Below 1.2133 will target 1.1946/86 support zone. Break of 1.1946 will confirm our bearish view and resume the larger down trend.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

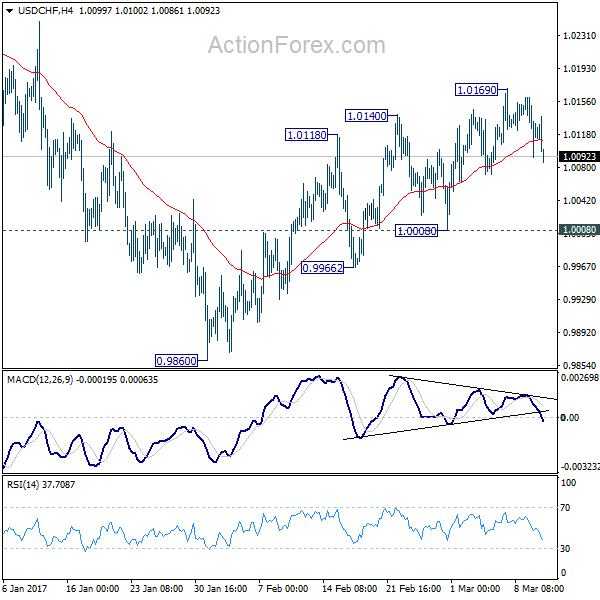

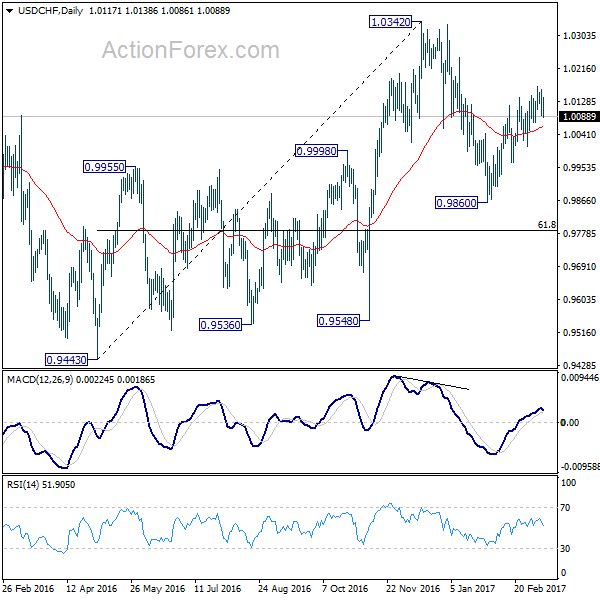

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0087; (P) 1.0124; (R1) 1.0156; More.....

USD/CHF's pull back from 1.0169 extends lower today but it's staying well above 1.0008 support so far. Intraday bias remains neutral for the moment. Further rise cannot be ruled out with 1.0008 support intact. However, based on neutral medium term outlook, we'd be cautious on topping at around 1.0342. This is supported by the corrective structure of the rise from 0.9860 so far. On the downside, break of 1.0008, however, will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.