Sample Category Title

D-Day for NFP

Friday March 10: Five things the markets are talking about

An upbeat payrolls report will add to expectations that the Fed will raise rates next week (Mar 14-15).

Today's headline print is expected to be high (+197k and +4.7%) given the extremely high ADP employment figures we have seen this week. Any serious deviation to the downside and the U.S bond market will be aggressively unwinding the almost 'slam dunk' expectation that fixed income dealers have already priced into the short-end of their treasury curve.

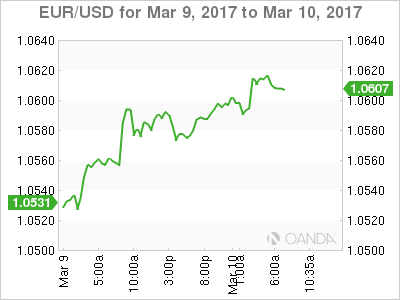

Yesterday, ECB President Draghi sent some confusing signals in his rate announcement press conference. While the main message is that the ECB is inching toward a policy exit, he undermined the forward guidance by reading out a year-old statement stating that the ECB does "not expect a further rate cut," and also said that the ECB's forecast on wages, productivity and core inflation "looks ambitious."

Despite the 'no rate change' decision, the somewhat less 'dovish' press conference has given the EUR (€1.0611) some stamina for now.

A tighter U.S labor market, stock market boom and rising global inflation supports the Fed increasing interest rates, but how many for this year?

Canada will also be releasing its job numbers at 08:30am. Will the headline print (-4k exp.) again sideswipe the market?

Note: Daylight savings time in North America begins on Mar 12

1. Global stocks get the green light

In Japan, the Nikkei closed at a 15-month high on a weaker yen (¥115.41) benefiting exporters. The index added +1.5% Friday, its highest closing level since Dec. 7, 2015. For the week, the benchmark index has climbed +0.7%. The broader Topix was up +1.2%.

In Hong Kong, its main index ends up despite oil prices dropping. The Hang Seng index gained +0.3%, while the Hong Kong China Enterprises Index shed -0.3%, dragged by Chinese energy giants. For the week, the market was roughly flat.

In China, stocks ended flat overnight, as investor excitement towards the country's annual parliamentary meeting petered out. The Shanghai Composite Index was down -0.1%.

In Europe, equity indices are trading sharply higher after ECB President Draghi's comments yesterday continue to add support. Financial stocks across Europe are trading notably higher on the Eurostoxx, while energy names are supporting the FTSE 100.

U.S equities are set to open in the black (+0.3%).

Indices: Stoxx50 +0.7% at 3,434, FTSE +0.4% at 7,344, DAX +0.5% at 12,044, CAC-40 +0.5% at 5,008, IBEX-35 +0.7% at 10,069, FTSE MIB +0.8% at 19,727, SMI +0.2% at 8,654, S&P 500 Futures +0.3%

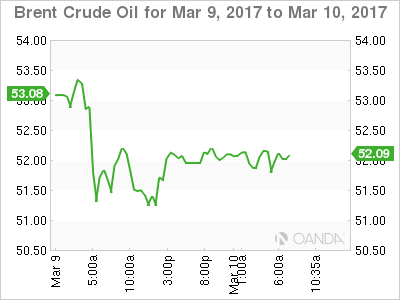

2. Oil edges off three-month low but glut worries persist

Oil prices have recovered a tad overnight after dropping to their lowest in more than three months yesterday, pressured by heavy oversupply despite OPEC's production cuts.

Brent crude is up +35c at +$52.54 a barrel, after falling -1.7% yesterday and -5% Wednesday in its biggest percentage decline in 12-months. U.S light crude (WTI) is up +40c at +$49.68 a barrel. It fell below -$50 on Thursday for the first time in three-months and is on track for a drop of more than -7% this week.

Market confidence is low after another big rise in U.S crude inventories this week - EIA data mid-week shows crude oil inventories swelled by +8.2m barrels last week to a record +528.4m barrels.

Also providing pressure is U.S oil and gas drilling has also picked up, with producers planning to expand crude production in North Dakota, Oklahoma and other shale regions.

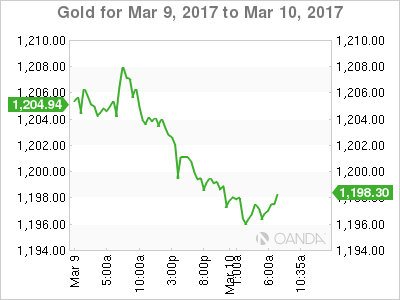

Metals prices are also under pressure, weighed by expectations of a Fed hike next week. Gold for April delivery was recently down -0.4% at +$1,204.20 a troy ounce and remains on track for its longest losing streak in nearly 12-months.

Elsewhere, Copper for May delivery is down -1% at +$2.5750 a pound, trading at a two-month low.

<

p>3. Bond rout eases

The nine-day slide in U.S debt prices has eased ahead of this morning's job's report. The yield on U.S 10's has backed up +1bps to +2.61%. Yesterday, it climbed +5bps to exceed the +2.60% watermark that many dealers believe signals the start of a 'bear' market, should it hold on a weekly basis.

In Europe, the ECB did not signal cuts in asset buying yesterday, but after its optimistic comments on the economy, money markets is pricing in an ECB rate hike by March 2018. Current futures price suggest there is a +80% chance of a +10bps by the meeting on Jan. 25, 2018 and a +60% chance by Dec. 2017.

Elsewhere, the yield on Aussie 10-year bonds has backed up +5bps to +2.97%. The yield on similar-dated debt in Japan was down -0.5% bps at +0.085%.

4. The dollar waits for NFP

Dollar bulls will be looking to today's average hourly earnings for support rather than the NFP headline print. Any signs to support inflation expectations will go a long way in pricing in the number of Fed rate hikes in 2017 - currently seen at three hike.

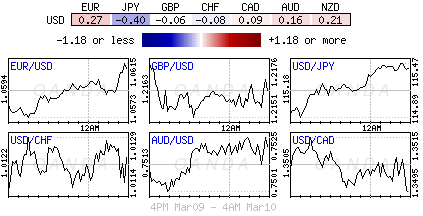

In Europe, with dealers perceiving a "hawkish" tilt from Draghi yesterday has instigated a sell-off in bunds and a higher EUR - currently testing above the psychological €1.0600 handle. German yields, which are set for biggest 14-day rise in nearly two-years has FX traders reconsidering paring current 'short' positions. The JPY has managed to drop to a seven-week low outright (¥115.43) on rate differentials. The pound (£1.2158) is little changed despite a plethora of mixed economic data for January (see below).

Elsewhere, EUR/NOK cross is higher (€9.1355) after Norway's Feb CPI data came in below expectations. The Norges Bank will have a tricky balancing act to pull off at its meeting next week.

5. U.K manufacturing has a weak start to 2017

Data this morning shows that U.K. industrial production declined in January, falling -0.4% m/m. A fall in manufacturing output mostly drove the slowdown, concentrated largely in the volatile pharmaceuticals sector.

Other data also shows the U.K's trade deficit (-£10.8B vs. -£11.1B) narrowed in January, while construction output declined.

Overall, the data paints a mixed picture of activity for the U.K at the start of the year and any squeeze on consumer spending from quickening inflation is also expected to weigh on growth later in the year.

GBP/USD: Starting A New Consolidation Phase

EUR/USD Ready for another leg lower.

EUR/USD has consolidated higher but the demand seems to weaken. Hourly resistance is given at 1.0679 (16/02/2017 high) while hourly support at 1.0493 (22/02/2017 low). The technical structure suggests deeper consolidation towards 1.0500. • In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Starting a new consolidation phase.

GBP/USD continues to edge lower since the pair has broken support given at 1.2254 (19/01/2017 low). The road is wide-open for further decline. Hourly resistance is now given at 1.2214 (09/03/2017 high).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Renewed buying pressures.

USD/JPY is pushing higher towards key resistance given at 115.62 (19/01/2016 high). Hourly support can be found at 113.56 (06/03/2017 low).

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CAD: Wide-Open Toward Resistance At 1.3599

USD/CHF Consolidating above 1.0100.

USD/CHF continues to improves. Hourly resistance is implied by upper bound of the uptrend channel. Key resistance is given at a distance at 1.0344 (15/12/2016 high). Expected to see further strengthening.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

USD/CAD Wide-open toward resistance at 1.3599.

USD/CAD's bullish pressures are definitely on after breaking key resistance at 1.3353 (20/01/2017 high). Yet, as long as this resistance was not broken (20/01/2017 high), bullishness was limited. Expected to see further upside potential for the pair.

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Wide-open for further weakness.

AUD/USD keeps on declining since its exit from uptrend channel. The road is wide-open for further weakness. Key resistance is given at 0.7778 (08/11/2016 high).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

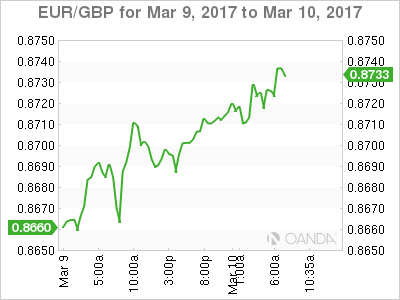

EUR/GBP: Breaking Resistance At 0.8707

EUR/CHF Holding above 1.0700.

EUR/CHF's bullish pressures have increased sharply. Strong resistance given at 1.0762 (27/12/2016 high) seems nonetheless far. Anyway, the medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Temporary surges seem the new normal for the CHF.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low)

EUR/JPY Strong bullish pressures.

EUR/JPY's demand has rejuvenated . Hourly resistance at 121.34 (10/02/2017 high) has been broken. Strong resistance is given at a distance at 123.31 (27/01/2017 high). Expected to show further consolidation. • In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Breaking resistance at 0.8707.

EUR/GBP has pushed higher towards strong resistance at 0.8707 (18/01/2017 high) which has been broken. We rule out further weakness towards supports given at 0.8450 (03/01/2016 low) and at 0.8304 (05/12/2016). Expected to pause below resistance at 0.8707.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level

Gold: Strong Weakness

GOLD (in USD) Strong weakness.

Gold is showing no signs of reversing bearish course after recent pullbacks. The positive midterm trend has been broken. It is unlikely that the metal will test again 1263 (27/02/2017 high). Expected to reach strong support at 1177 (11/01/2017 low).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER (in USD) Collapsing.

Silver's selling pressures are growing since the pair exited uptrend channel. Hourly support at 17.75 (14/02/2017 low) has been broken, Next one lies at 16.63 (27/01/2017 low). Expected to see continued bearish pressures below 17.00.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude Oil (in USD) Continued weakness.

Crude oil's bearish pressures continues. The commodity has been unable to mount a serious challenge to 55.24 (03/01/2017 high) resistance. Strong support given at 49.61 (08/12/2016) has been broken. Expected to see deeper selling pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

WTI Dips Below $50, NFPs In Focus

News and Events:

Oil caps worst week since November

The West Texas Intermediate is about to post its largest weekly decline since the first week of November when it dropped 9.50% to below $45 a barrel. This week, the WTI slid almost 7% as it dipped below $50 a barrel for the first time since the November OPEC 'supply cut' deal. The move was initiated on Wednesday after the EIA reported that US stockpiles had surged by 8.2 million barrels in the previous week, more than four times what the market was expecting, pushing US inventories (excluding strategic reserve) to an all-time high of 528 million barrels.

The market has begun to consider the possibility that OPEC and certain non-OPEC members such as Russia, who initially agreed to curb production back in November, may now be backtracking on their promise. Indeed, the US shale industry was the primary beneficiary of this 'supply cut' as shown by the massive rise in rig count (+38% or 168 new wells since November last year). In this fight, the US has been continuously increasing their market share on the back of those who agreed to cut production.

On the top of this, the market positioning on the NYMEX had reached extreme levels recently as the total net position reached 387k contracts. Even back in June 2014, the market wasn’t that bullish (348k net long). Therefore, we believe that there is room for further downside move in crude oil prices. Investors were betting that the recovery in prices would be proven sustainable as the main oil producers seemed to have found an agreement. We would not be surprised to see OPEC and Russia back-pedalling on the 'supply cut' deal as it is clearly to the advantage of the US right now. We expect further weakness of crude prices as traders unwind their long positions, with $45 a barrel as the next target.

Tread cautiously in EM

Markets are currently repricing in three Fed rate hikes (four in 2018), which is forcing the US yield curve higher. The complacency in the market to price in faster rate hikes looks to have diminished. While the USD has gained versus the G10 (especially commodity-linked currencies NOK and NZD), widening interest rate differentials and softer commodity prices have not supported broad-based EM selling. In fact, EM currencies have widely improved against the dollar. Part of the rationale of the lagging behavior is due to signs of reflation, which should push policymakers to manage accommodating policy correctly. In addition, the delay in the US trade policy has provided EM with a bit of macro-head winds respite. Yet, with 8 trillion sitting in negative yielding sovereign paper, the probability that higher US rates will attract flows driving USD higher has significantly increased. Further, EM volumes seem to be completely mispricing the risk relating to Fed tightening and global protectionism. As markets price in a quicker rate of Fed hikes, low yielding EM currencies, already behind the curve, will come under selling pressure.

NFP report irrelevant as Fed hike is a done deal

After the massive ADPs on Wednesday, which came in slightly below 300k, financial markets are now awaiting confirmation from the NFPs, which are expected to come in for February lower than the January print, 200k vs 227k. From our standpoint, this read is irrelevant as it will have little impact on the US central bank’s decision concerning the raising of rates.

Despite the occasional spectacular miss from the ADP, we would not expect a low NFP read. A weak read could drive the dollar lower, knowing that there is room for disappointment as a rate hike is now priced in by the financial markets.

Moreover, there is the increasing probability of rate hikes at the next meetings. We reaffirm our belief that the Fed will not raise rates above 2% for the next two years as it could trigger a much deeper crisis.

The dollar should remain strong and while today’s NFPs are likely to be a non-event, one should not forget Trump’s stance that the dollar is too high. For the time being, European uncertainties are definitely sending the greenback higher.

Today's Key Issues (time in GMT):

- Feb CPI MoM, exp 0,90%, last 0,00% DKK / 08:00

- Feb CPI YoY, exp 1,10%, last 0,90% DKK / 08:00

- Feb CPI EU Harmonized MoM, exp 0,80%, last -0,10% DKK / 08:00

- Feb CPI EU Harmonized YoY, exp 1,00%, last 0,70% DKK / 08:00

- mars.03 Money Supply Narrow Def, last 8.85t RUB / 08:00

- Jan Retail Sales YoY, last 0,90% EUR / 08:00

- Jan Retail Sales SA YoY, exp 2,50%, last 2,90%, rev 2,10% EUR / 08:00

- mars.07 FIPE CPI - Weekly, exp -0,03%, last -0,05% BRL / 08:00

- 4Q Unemployment Rate Quarterly, exp 11,70%, last 11,60% EUR / 09:00

- Jan Industrial Production MoM, exp -0,50%, last 1,10%, rev 0,90% GBP / 09:30

- Jan Industrial Production YoY, exp 3,20%, last 4,30% GBP / 09:30

- Jan Manufacturing Production MoM, exp -0,70%, last 2,10%, rev 2,20% GBP / 09:30

- Jan Manufacturing Production YoY, exp 2,90%, last 4,00%, rev 4,20% GBP / 09:30

- Jan Construction Output SA MoM, exp -0,20%, last 1,80% GBP / 09:30

- Jan Construction Output SA YoY, exp 0,30%, last 0,60%, rev 2,60% GBP / 09:30

- Jan Visible Trade Balance GBP/Mn, exp -£11100, last -£10890, rev -£10915 GBP / 09:30

- Jan Trade Balance Non EU GBP/Mn, exp -£2425, last -£2114, rev -£2527 GBP / 09:30

- Jan Trade Balance, exp -£3100, last -£3304, rev -£2026 GBP / 09:30

- Feb BoE/TNS Inflation Next 12 Mths, last 2,80% GBP / 09:30

- Feb IBGE Inflation IPCA MoM, exp 0,43%, last 0,38% BRL / 12:00

- Feb IBGE Inflation IPCA YoY, exp 4,86%, last 5,35% BRL / 12:00

- Jan Industrial Production YoY, exp 0,50%, last -0,40% INR / 12:00

- Feb Unemployment Rate, exp 6,80%, last 6,80% CAD / 13:30

- Feb Change in Nonfarm Payrolls, exp 200k, last 227k USD / 13:30

- Feb Net Change in Employment, exp -5.0k, last 48.3k CAD / 13:30

- Feb Two-Month Payroll Net Revision USD / 13:30

- Feb Full Time Employment Change, last 15,8 CAD / 13:30

- Feb Change in Private Payrolls, exp 215k, last 237k USD / 13:30

- Feb Part Time Employment Change, last 32,4 CAD / 13:30

- Feb Change in Manufact. Payrolls, exp 10k, last 5k USD / 13:30

- Feb Participation Rate, last 65,9 CAD / 13:30

- Feb Unemployment Rate, exp 4,70%, last 4,80% USD / 13:30

- Feb Average Hourly Earnings MoM, exp 0,30%, last 0,10% USD / 13:30

- Feb Average Hourly Earnings YoY, exp 2,80%, last 2,50% USD / 13:30

- Feb Average Weekly Hours All Employees, exp 34,4, last 34,4 USD / 13:30

- Feb Labor Force Participation Rate, last 62,90% USD / 13:30

- Feb Underemployment Rate, last 9,40% USD / 13:30

- Feb NIESR GDP Estimate, exp 0,60%, last 0,70% GBP / 15:00

- Feb Monthly Budget Statement, exp -$190.0b, last $51.3b USD / 19:00

- Feb Foreign Direct Investment YoY CNY, exp -4,20%, last -9,20% CNY / 23:00

The Risk Today:

EUR/USD has consolidated higher but the demand seems to weaken. Hourly resistance is given at 1.0679 (16/02/2017 high) while hourly support at 1.0493 (22/02/2017 low). The technical structure suggests deeper consolidation towards 1.0500. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD continues to edge lower since the pair has broken support given at 1.2254 (19/01/2017 low). The road is wide-open for further decline. Hourly resistance is now given at 1.2214 (09/03/2017 high). The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY is pushing higher towards key resistance given at 115.62 (19/01/2016 high). Hourly support can be found at 113.56 (06/03/2017 low). We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF continues to improves. Hourly resistance is implied by upper bound of the uptrend channel. Key resistance is given at a distance at 1.0344 (15/12/2016 high). Expected to see further strengthening. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3445 | 1.1731 | 121.69 |

| 1.0954 | 1.3121 | 1.0652 | 118.66 |

| 1.0874 | 1.2771 | 1.0344 | 115.62 |

| 1.0610 | 1.2169 | 1.0120 | 115.38 |

| 1.0454 | 1.1986 | 0.9967 | 111.36 |

| 1.0341 | 1.1841 | 0.9862 | 106.04 |

| 1.0000 | 1.0520 | 0.9550 | 101.20 |

EC Leaves Interest Rates And QE Programme Unchanged

'There was a sentence that has been removed from my introductory statement that used to say 'if warranted to achieve its objective, the Governing Council will act using all the instruments available within its mandate'. - Mario Draghi, ECB

As markets expected, the European Central Bank left its monetary policy unchanged at its meeting on Thursday, saying it would continue monitoring inflation. Regarding non-standard monetary policy measures, the Governing Council confirmed that the monthly asset purchases of 80 billion euros would be reduced to 60 billion euros starting from next month. Policymakers also voted to keep the main refinancing rate at 0% and the overnight deposit rate at -0.4%. The ECB said that its key interest rates would likely remain at present or lower levels for an extended period of time, and well past the horizon of our net asset purchases. After two years of the ECB's QE programme inflation accelerated well above the Bank's initial goal, signaling that the monetary stimulus should be reduced. However, the ECB President Mario Draghi pointed out that the recent acceleration in prices was mainly driven by a rebound in energy prices. Draghi also highlighted that risks related to the upcoming European elections had the potential of slowing the economic recovery in the region. Nevertheless, the ECB raised its 2017 inflation projection to 1.7% from 1.3% in December, adding that the expected pick-up would probably be temporary. Meanwhile, GDP growth projections were revised up to 1.8% from 1.7% in December.

Initial Jobless Claims Rise Above Market Forecasts

'There is no evidence of a pickup in involuntary employment separations. We view this as evidence of a tight labor market.' - John Ryding, RDQ Economics

The number of Americans filing for unemployment benefits rose more than expected last week, official figures showed on Thursday. The US Department of Labour reported initial jobless claims rose to 243,000 in the week ended March 3, up from the preceding week's record low of 223,000. Meanwhile, market analysts expected claims would climb to 239,000 claims during the reported week. Last week marked the 105th consecutive week of claims below the benchmark 300,000 level. Analysts state that the US economy is at or near full employment, with companies struggling to find qualified candidates for job openings. The strong performance of the labour market and rising inflation would probably force the Federal Reserve to raise rates at its next meeting on March 15. The Labour Department said there were no special factors influencing claims data. The four-week moving average of initial claims, considered a better measure of the labour market trends, advanced 2,250 to 236,500 last week. Thursday's report also showed continuous jobless claims dropped 6,000 to 2.06 million in the week ending February 25, while their four-week moving average fell 5,250 to 2.07 million. The US Dollar traded little changed after the release, as investors awaited Friday's NFP report.

EUR/USD – Euro Hugging 1.06 Ahead Of US Nonfarm Payrolls Next

EUR/USD has posted slight gains in the Friday session. Currently, the pair is trading just above the 1.06 line. On the release front, German numbers were mixed. The trade surplus was almost unchanged at EUR 18.5 billion, short of the estimate of 19.2 billion. There was better news on the inflation front, as German WPI posted a gain of 0.5%, beating the forecast of 0.3%. In the US, employment numbers will be on center stage, with the release of three key indicators – Nonfarm Payrolls, Average Hourly Earnings and the unemployment rate. The Nonfarm payrolls report is expected to drop to 200 thousand, while wages are forecast to improve to 0.3%. Traders should be prepared for some volatility in the currency markets during the North American session.

As expected, the ECB held course and maintained interest rates at a flat 0.00% on Thursday. ECB President Mark Draghi focused on nuances, noting that the central bank removed one phrase from its standard introductory statement – 'using all the instruments available within its mandate'. Draghi added that the removal of this phrase means that the ECB 'no longer has a sense of urgency in taking further actions …. prompted by the risk of deflation'. With growth and inflation showing signs of improvement, the ECB has been under pressure to tighten policy and reduce its asset-purchase program. Germany, in particular, is unhappy with the ECB’s ultra-loose policy and on Thursday, German Finance Minister Wolfgang Schaeuble bluntly stated that he wanted to see a 'timely start to the exit' from the ECB’s asset-purchase scheme. For his part, Mario Draghi must balance the improved economy with upcoming elections in France, Germany and the Netherlands. Euro-skeptics are a strong force throughout Europe and Draghi is reluctant to make any moves which could be seized on by politicians. The ECB’s asset-purchase program is slated to end in December, but economic and political circumstances could trigger an earlier end to the program.

The Federal Reserve waited an entire year to raise rates in December, but appears ready to make a March move. The odds of a March hike continue to climb, and are currently at 88% percent, according to the CME Group. Fed policymakers have been dropping hints of a March move, and a red-hot labor market and higher inflation levels present further arguments in favor of higher rates. Earlier in the year, the Fed had said that it wanted to wait until it had a clearer idea of President Trump’s economic policy before it tightened monetary policy. However, Trump has not backed up his promises to reform the tax code and increase fiscal spending with any details. Some Fed policymakers wanted to raise rates earlier this year, so Fed Chair Yellen is under pressure to make a move, and it appears virtually certain that the Fed will raise rates by a quarter-point on March 15.

US Jobs Data Largely Irrelevant To Next Weeks Fed Meeting

- Jobs data the final piece of the puzzle but not necessarily essential for a hike;

- ADP number suggests we're heading for another stellar report;

- Earnings and participation arguably the most important parts of the report;

- Oil paring losses but recent declines a concern with output deal extension not guaranteed.

US equity markets have spent the last week in correction mode following a fantastic run throughout February, but futures suggest they could open higher on Friday in a sign that traders may be expecting some good numbers from the US jobs data today.

The February jobs report could be the final piece of the puzzle as the Federal Reserve prepares to meet next week to discuss whether to raise interest rates for the first time this year. The coordinated comments from Fed policy makers is recent weeks has been like interest rate hike roadshow, with officials clearly determined to sell the idea to the markets ahead of the meeting. Markets until that point had completely written off such a scenario but have since responded to the barrage of hawkish commentary from Fed officials.

Given the recent efforts from policy makers, I think the jobs report today will be largely irrelevant when it comes to the discussion on interest rates next week. The figures today will literally have to be terrible in order for the Fed to consider postponing a hike that has only been made possible because of their determination that it could happen. The possible credibility cost is great enough that the Fed will not want to disappoint unless it feels it absolutely necessary.

What's more, the ADP number on Wednesday would suggest there's nothing to worry about. While this isn't always a great estimate of the NFP number, it does tend to be a decent indicator of market expectations being either way too high or low and coming in more than 100,000 above expectations certainly falls in that bracket. A lot of people will have raised their expectations on the back of the ADP release but even if NFP now fails to live up to them, I very much doubt it will be bad enough to cast doubt on a rate hike next week which should offer support for the US dollar.

Other aspects of the report are arguably more important, such as average hourly earnings which tend to rise when the labour market is as tight as the unemployment number would suggest. Earnings have been steadily rising over the last two years but are still doing so at a slower pace than the Fed would like and expect if inflation is going to rise in line with its expectations. The stubbornly low participation rate may go some way to explaining this along with other structural issues but I think the central bank will be comfortable as long as the direction of travel continues as it has since the start of 2015.

Brent and WTI crude is paring losses today having suffered considerable losses over the last few days. It would appear the substantial long speculative positions have been pared back over the last 48 hours which may bring some stability back to the market but ultimately, what's happened is a worrying sign for oil and more importantly, those countries that have agreed to cut production in order to support prices. An extension beyond the middle of the year appears to be required to prevent oil slipping further but this is far from guaranteed with Saudi Arabia appearing to lose it patience and non-OPEC compliance not seeming to match that of OPEC members.