Sample Category Title

ECB’s Kazaks calls for further rate cut as inflation problem will soon end

Latvia’s ECB Governing Council member Martins Kazaks indicated his support for an interest rate cut at next week’s ECB meeting, citing the belief that inflation problem "will soon end."

However, Kazaks acknowledged the high level of uncertainty following the widely expected rate cut. He pointed to risks tied to US President-elect Donald Trump’s upcoming administration, noting that new tariffs could further weigh on Europe’s economy.

Despite these concerns, Kazaks maintained a cautiously optimistic view, stating that "Europe’s economy is going from its lowest point upwards."

ECB’s Lane signals shift to forward-looking policy approach ahead

In an interview with the Financial Times, ECB Chief Economist Philip Lane indicated that the central is preparing to adjust its monetary policy approach as inflation moves closer to the 2% target.

While acknowledging that inflation has fallen near the desired level, Lane noted that "there is a little bit of distance to go," especially with services inflation needing further reduction.

However, Lane emphasized that once the disinflation process is complete, monetary policy decisions will need to become "essentially forward-looking," focusing on upcoming risks rather than relying on past data. He highlighted the importance of scanning the horizon for "new shocks" that could impact inflation pressures.

Over the course of next year, Lane expects a "transition to a more sustainable neighborhood of 2%," signifying a shift from combating high inflation to maintaining price stability on a sustainable basis.

The French Theme Will Keep Yields and Euro in a Tight Spot

Markets

The front end of the European yield curve outperformed going into the weekend. Rates dropped almost 5 bps in the 2-yr German tenor, enough to lose the symbolical 2% barrier to close at a 2-year low. It followed European inflation numbers coming in at the expected 2.3% headline, which prompted ECB’s de Guindos and Villeroy but also Nagel downplaying the acceleration above 2%. Core inflation missed the bar slightly with an October-matching 2.7% instead of 2.8% expected. The ECB’s chief economist Lane in a podcast with the Financial Times talked about the matter and the implications for monetary policy. In comments recorded prior to the CPI release Lane said once inflation was sure to return to 2%, the ECB needs “to be driven by upcoming risks rather than being backward-looking”. He refrained from giving time specifics but it suggests the central bank may already change some of its wording in the December policy statement so that “data dependence falls down in priority”. US yields were headed south as well. Net daily changes varied between 7.6 and 9.4 bps but we wouldn’t read too much into it. The US trading session was a shortened one due to Black Friday. The traditional start of the holiday shopping season was a strong one with sales growing at a faster pace this year. Joe Sixpack to the economy is a gift that keeps on giving. The dollar underperformed in currency markets, a product of falling yields and stock optimism. JPY was able to make the most out of it, thanks to consensus-beating Tokyo inflation numbers. USD/JPY dropped below 150. EUR/USD stranded just shy of 1.06 before going in reverse again this morning towards 1.052. French politics are once again cause of concern. Le Pen over the weekend said PM Barnier needs to amend the budget to some of the RN’s demands by today or have her Rassemblement National supporting a no-confidence motion. The finance minister Armand responded in a Bloomberg interview in early Asian trading by saying they won’t be blackmailed and don’t take ultimatums. French OAT futures currently tank, yields prepare for a sharply higher open. Spreads vs swap and German Bund are bound to rise. Watch out for French yields to surpass those in Greece. Last week was a dress rehearsal. The French theme will keep yields and the especially the euro in a tight spot at the very minimum in a daily perspective but more likely for the next two weeks going into December 12, when parliament gets to vote on the budget for a last time. In the US the monthly economic update kicks off with the manufacturing ISM today, followed by the services gauge and ADP job report on Wednesday and the official payrolls report on Friday. Fed’s Waller speech at "Building a Better Fed Framework: The AIER Monetary Conference" tonight is worth mentioning.

News & Views

Rating agency Moody’s on Friday changed Hungary’s credit rating outlook to negative from stable. The rating was maintained at Baa2. It reflects the agency’s assessment related to risks related to the quality of Hungary’s institutions and governance. The country may ultimately lose out on a substantial amount of EU funds because it doesn’t meet the conditions for the release. Moody’s thinks this could also lower trend GDP growth and weaken fiscal and debt metrics. As this happens in a context of weak growth in Germany, an important trading partner, this could amplify the negative pressure on the economy. Moody’s mentions a potential sharp increase in government spending ahead of the 2026 parliamentary elections. The rating agency still sees a partial reversal in 2025 of the weakening in debt affordability from the past two years. At the same it mentions institutional weakness weighing on the debt profile, including in adherence to the rule of law, interference in civil society and concerns over central bank independence and monetary policy. The agency sees growth returning to an average of 3.0% in the 2026-28 period.

GDP growth in India slowed to 5.4% Y/Y from 6.7% Y/Y in Q3. Expectations were for a 6.5% Y/Y growth. Growth in the agricultural sector held up fairly well (3.5% Y/Y from 2.0%) but mining contracted 0.1%. Manufacturing slowed from 7.0% to 2.2% and growth in the sectors of electricity, gas and water (3.3%), construction (7.7% from 10.5%) and financial services/real estate (6.7%) were lower than Q2. On the demand side, private consumption growth slowed from 7.4% Y/Y to 6.0%, as did growth capital formation (5.4% from 7.5%). The disappointing growth performance might pressure the RBI of India not to wait too long with its easing cycle. The bank has kept its policy rate unchanged at 6.50% since February 2023. The rupee is setting new all-time lows against the dollar this morning (USD/INR 84.68).

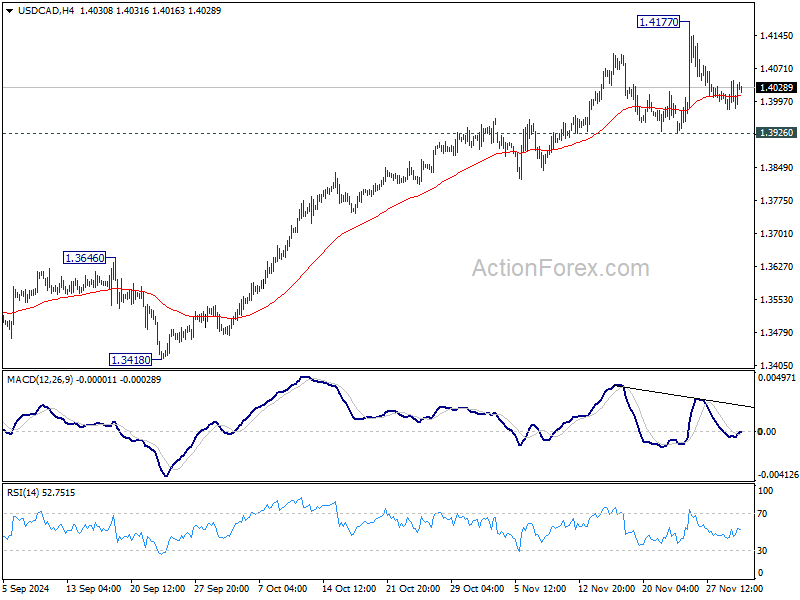

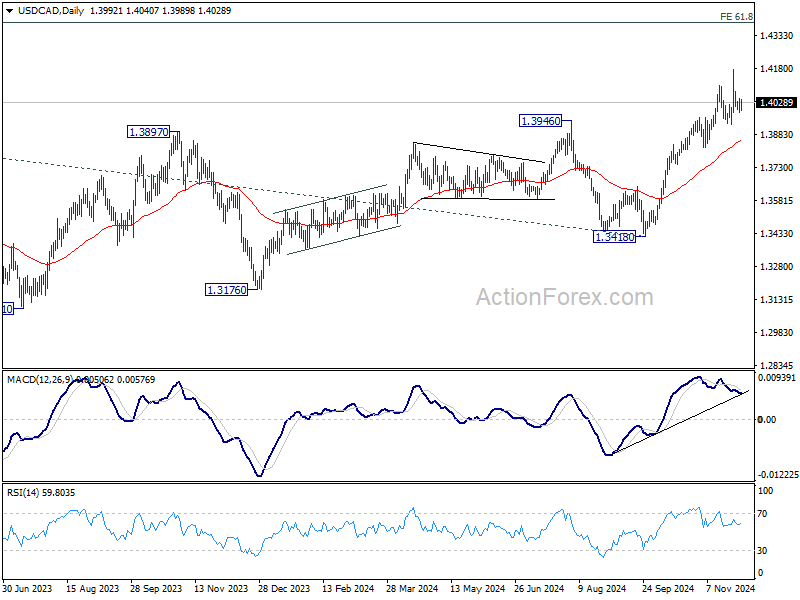

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3973; (P) 1.4010; (R1) 1.4038; More...

Intraday bias in USD/CAD remains neutral as range trading continues. Further rally is expected with 1.3930 support intact. On the upside, firm break of 1.4177 will resume larger up trend towards 1.4391 projection level. However, break of 1.3926 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.3857).

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

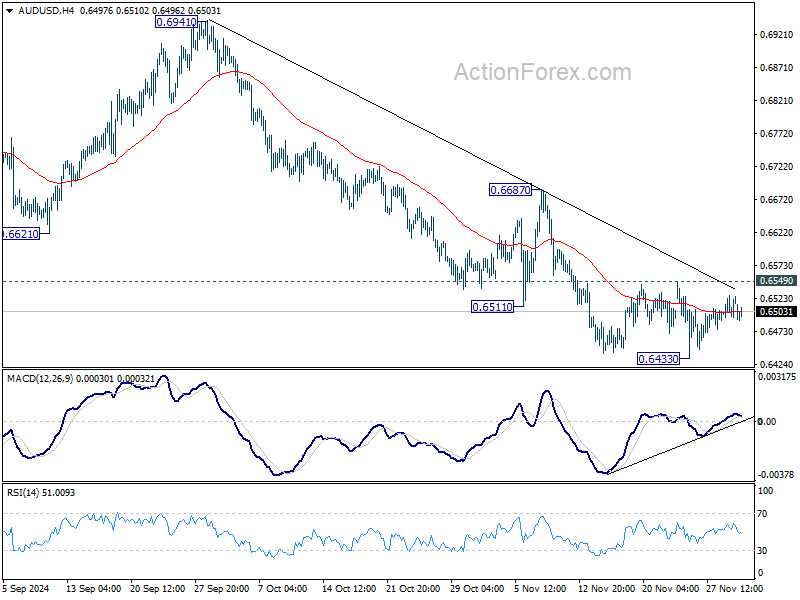

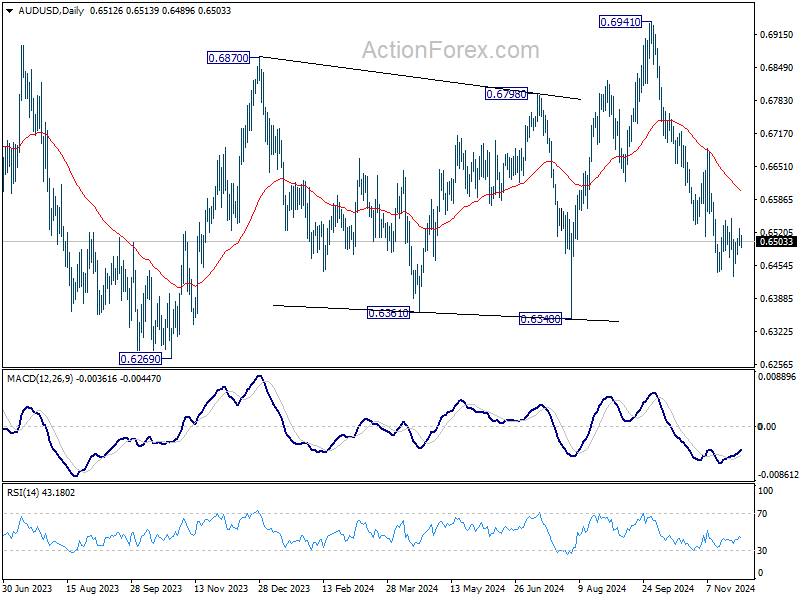

AUD/USD Daily Report

Daily Pivots: (S1) 0.6485; (P) 0.6506; (R1) 0.6533; More...

Range trading continues in AUD/USD and outlook is unchanged. Intraday bias remains neutral first and with 0.6549 resistance intact, further decline is expected. On the downside, break of 0.6433 will resume whole decline from 0.6941, and target 0.6348 support next. However, firm break of 0.6549 will indicate short term bottoming, and bring stronger rebound to 55 D EMA (now at 0.6602).

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

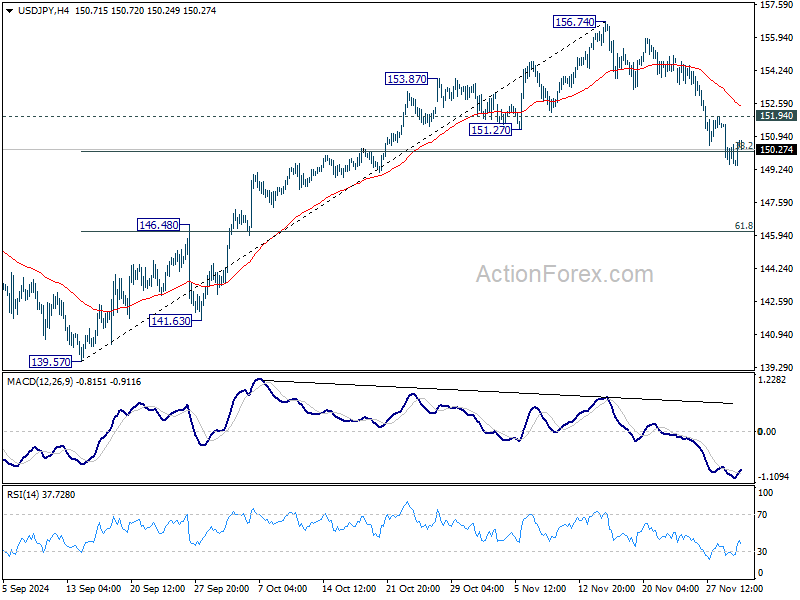

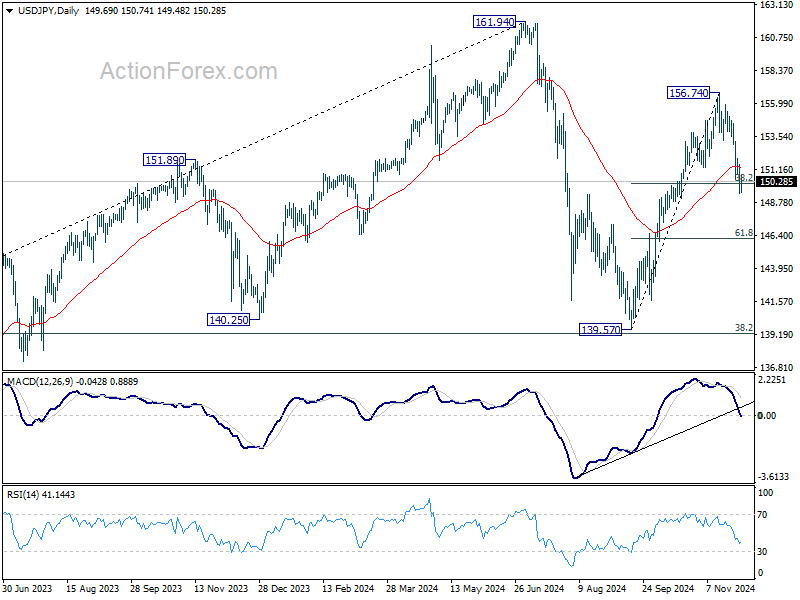

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.89; (P) 150.30; (R1) 151.13; More...

Intraday bias in USD/JPY stays on the downside at this point. Sustained trading below 38.2% retracement of 139.57 to 156.74 at 150.18 will argue that whole rise from 139.57 could have completed. Deeper fall should then be seen to 61.8% retracement at 146.12 next. On the upside, break of 151.94 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

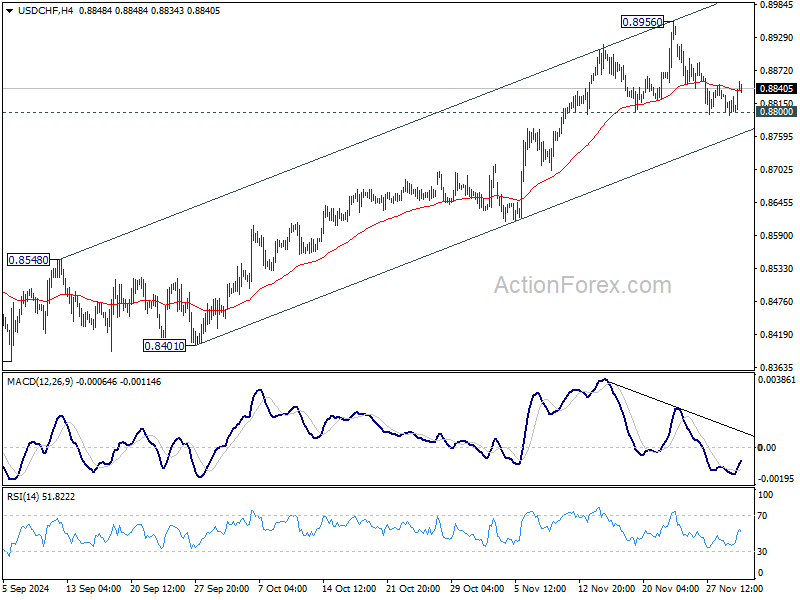

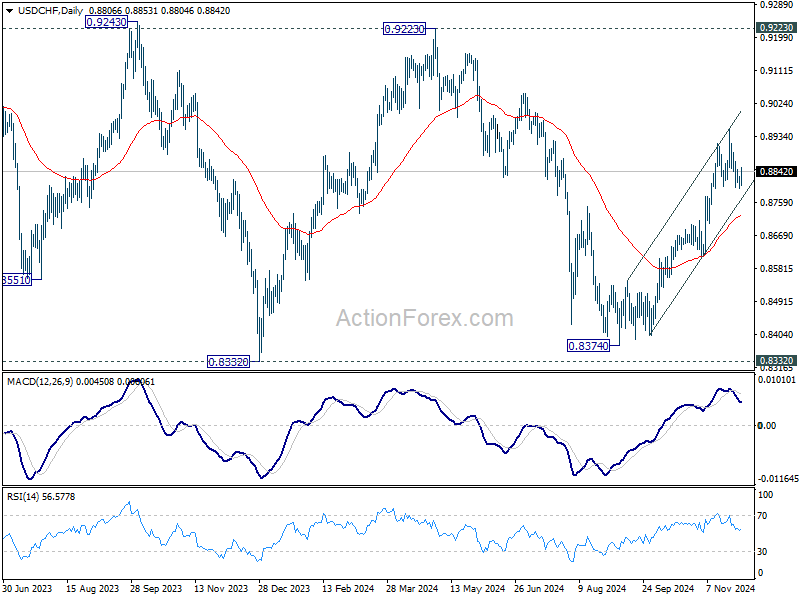

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8792; (P) 0.8815; (R1) 0.8834; More…

Intraday bias in USD/CHF remains neutral and outlook is unchanged. With 0.8800 support intact, further rally remains in favor. On the upside, break of 0.8956 will resume the rally from 0.8374, and target 0.9223 key resistance next. However, firm break of 0.8800 will confirm short term topping and turn bias back to the downside for 55 D EMA (now at 0.8725).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

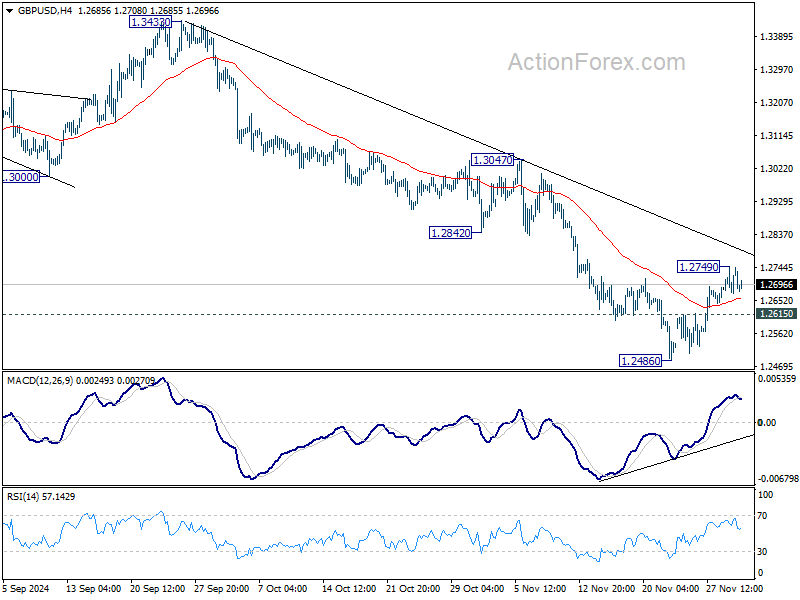

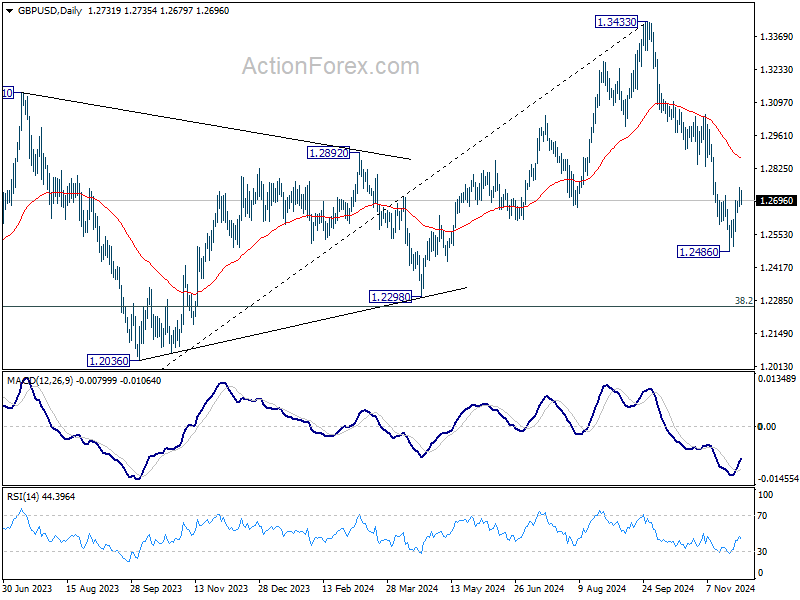

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2687; (P) 1.2719; (R1) 1.2765; More...

Intraday bias in GBP/USD is turned neutral first with recovery from 1.2486 losing momentum. While another rise cannot be ruled out, outlook will stay bearish as long as 55 D EMA (now at 1.2867) holds. Below 1.2615 minor support will turn intraday bias back to the downside for retesting 1.2486. Break there will resume whole fall from 1.3433.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2867) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

European Doom and Gloom

December doesn’t arrive with chocolate and flowers to Europe. First, Stellantis CEO resigns on weaker sales and tumbling profits. Second, VW workers are expected to walk out as early as today, because their labour leaders couldn’t reach an agreement on how to reduce costs to prevent factory closures. Sadly for VW, the worker walkouts may only get the matters worse when there is no money flowing in to make everyone happy. And finally, the French political scene remains messy with the far-right party Marine Le Pen threatening to team up with the leftist and take down Michel Barnier’s government by Wednesday if he doesn’t come up with a less strict budget plan. The problem is that no plan will be good enough to satisfy Le Pen and reduce France’s budget deficit.

As a result, the European futures are in the red at the time of writing, the French yields will probably retrace last Thursday, Friday’s decline, the spread between the German and French yield could shoot above 100bp and the euro is under pressure. The EURGBP starts the new week with a move below the 0.83 level and the EURUSD has potential to break below the 1.05 support on the back of an unsupportive political and economic setup.

One good news for France, though: S&P reaffirmed its AA- debt rating.

In Japan, the news are not brighter. Nissan’s CFO decided to step down as the company now expects its operating income for this fiscal year to be 70% lower than its previous forecast. Beyond Nissan, the Japanese manufacturing PMI fell to the lowest level since March, marking the 5th consecutive month of contraction on sustainably low new orders and weak domestic and international demand. The news gives the USDJPY a good reason to rebound back above the 150 level this morning, retracing a part of last week gains triggered by rising bets that the Bank of Japan (BoJ) would hike the interest rates one more time before the year ends.

The downside pressure on euro and the yen is giving a boost to the US dollar early this week. The US dollar index is up and above the 106 this morning after retracing a part of its recent gains last week. Data-wise, last week printed a relatively strong 2.8% growth for Q3, with strong 3% growth in sales. The data showed that the price pressures last quarter declined, but the core PCE index in October ticked higher from 2.7% to 2.8% - happily, that was already priced in. Consequently, the picture painted by the latest economic data doesn’t necessarily call for another 25bp in December, but this is what the markets are pricing in right now. The US 2-year yield spent last week sliding, while activity on Fed funds futures gives around 68% probability for another 25bp in December. Note, however, that the latter expectation could change with a set of stronger-than-expected jobs and CPI data before the last FOMC decision of the year.

This week, the US will reveal the November jobs data and the expectations are mixed. The US economy is expected to have added 200K new nonfarm jobs last month, after the meagre 12K printed a month earlier due to hurricanes. The unemployment rate on the other hand is expected to have deteriorated to 4.2%, from 4.1% printed a month earlier, and the wages growth may have slightly eased from 0.4% to 0.3% on a monthly basis. Given the hurricane disruption, the unemployment rate and the wages growth will give us a more reliable information on the medium term trend than the NFP number itself. Strong data will certainly revive the rate-cut-or-not discussions, while soft numbers will boost appetite for another 25bp cut from the Fed and could limit the dollar’s upside potential.

In equities, last week, and last month, ended on a positive note for the major US indices. The S&P500 and the Dow Jones hit a fresh record on Friday, Nasdaq also gained 0.90%. The small and mid-caps consolidated near ATH as well. The European Stoxx 600 attempted a recovery on expectation that the European Central Bank (ECB) will cut thoroughly to give support to the struggling European economies, and to counter the US tariff threats, yet claiming fresh record highs with such a long list of unfavourable factors sounds unreasonable. Even less so as the ECB rate cut bets are pressured by the recent uptick in European inflation – and the USD’s recent strength is not promising. Note however that some investors like the growing valuation gap between the American and the European stocks and bet that the things can only get better for the Europeans.

In energy, crude is supported by a better-than-expected Caixin manufacturing number, and hope that OPEC+ will announce - or maybe scrap - its plans to restore production next year to avoid adding to the global glut and pressuring prices lower. The barrel of US crude finds buyers below $69pb, while Brent is bid below the $72pb. OPEC could give a positive spin to oil prices this week, therefore, the short-term risks remain tilted to the upside until the December 5th announcement, but OPEC alone will hardly reverse the medium-term bearish pressures if the demand side of the equation doesn’t improve. Therefore, any price rallies in oil could be interesting top selling opportunities for medium-term bears.

French Politics Hangs in the Balance

In focus today

Attention shifts to French politics as the minority government faces a crucial test in passing a social security bill, which could trigger a no-confidence vote against the government. Previously reliant on tacit support from the National Rally, tensions have risen since Thursday last week, where they called the current proposal "unacceptable". Hence, uncertainty remains in French politics, and it remains unclear if the concessions from Barnier will be enough to satisfy the National Rally. For an in-depth analysis, refer to our recent article, Weekly Focus - Political risks rise again in France, 29 November.

In Sweden, we get manufacturing PMI for November at 08:30. Compared to the major euro economies where PMIs are well below 50, the Swedish manufacturing sector has held up relatively well (October at 53.1). Last week, NIER's manufacturing index bounced higher, though it remains in contraction territory. The weak krona and a solid US market are tailwinds, while the bleak outlook for Europe is a headwind.

This afternoon, the US ISM Manufacturing index is due for release. Flash PMIs for November was below 50, although they showed slight improvement.

The week ahead will be dominated by US data releases, including JOLTs, ADP and ISM services. On Friday consensus expects the US jobs report to show a rebound in the employment growth of 200k, while we call for 165k. The FOMC's blackout period before the December meeting begins on Saturday, yet prior to that, a long list of public remarks is scheduled for the week.

In the euro area, unemployment figures are released on Tuesday, while we receive retail sales data on Thursday. We will also have revisited Q3 GDP figures on Friday, which will include details on the growth composition.

Economic and market news

What happened over the weekend

In the US, president-elect Donald Trump threatened the BRICS countries with tariffs of 100%, if the group continues to work on a global alternative to the US dollar. Trump requires a commitment from the countries to neither create a new currency, nor back any other currency to replace 'the mighty US dollar'. The threats aimed at the BRICS follow similar warnings of steep tariff increases on China, Mexico and Canada earlier last week.

In the euro area, HICP inflation rose to 2.3% y/y in November as expected (cons: 2.3%, prior: 2.0%). The increase in headline inflation was mainly due to base effects on energy inflation. Core inflation rose less than expected to 2.7% y/y (cons: 2.8%, prior: 2.7%). Most importantly, service prices increased only around 0.10% m/m seasonally adjusted in a positive sign for the ECB. Our 3m/3m SAAR measure of momentum declined to 2.7% in November from 3.4%. Hence, the trend lower in momentum of underlying inflation continued in November, which supports further rate cuts by the ECB.

In Sweden, Friday's Q3 GDP surprised upside at 0.3% q/q and 0.7% y/y (cons: -0.1%, 0.1%, prior: -0.1%, -0,1%). The strong reading corroborates the positive NIER confidence data from last Thursday, hinting that the October decline in the NIER survey might have been an anomaly. Additionally, October's retail sales data also came in positive at 0.4% m/m and 0.9% y/y (prior: 0%, 2.1%), suggesting a recovering retail sector on the back of improving sentiment among households and in the retail trade sector continued to improve in yesterday's NIER survey.

In China, both measures of PMIs came out marginally better than expected in November. The official PMIs showed a marginal uptick in the manufacturing index, which printed at 50.3 (cons: 50.2, prior: 50.1), while the non-manufacturing index dropped to 50 (prior: 50.2) and finally composite at 50.8 (prior: 50.8). Additionally, the Caixin manufacturing PMIs surpassed expectations at 51.5 (cons: 50.5, prior: 50.3), with both new orders and employment rising. The positive readings follow the efforts from the government to support growth through the recent round of stimulus, which appears to be starting to take effect.

In the Middle East, rebels captured much of the Syrian capital Aleppo over the weekend, sparking renewed tensions in the region. President al-Assad has promised to restore order 'with the help of friends and allies', which suggests that the regime is awaiting support from Russia, Iran and Hezbollah to regain control. According to Bloomberg, the rebel alliance consists of Hayat Tahrir al-Sham, once linked to Al Queda, and several Turkish-backed groups.

Equities: Global equities were higher on Friday, with gains across most regions and all sectors. With last week's stellar performance, we saw several indices setting new all-time highs, with November performance particularly driven out of the US. Although the US elections now seem distant, we must recall that just a month ago the VIX was above 20, accompanied by a considerable amount of uncertainty. Following last week's drop, the VIX ended close to 13, and investors are now considerably more confident and feel much less uncertain, which largely explains the substantial equity returns harvested in November. It is also worth noting that November's performance was not just driven by the MAG 7; the best performing sector was financials, and the best performing style was small caps. In the US on Friday, the Dow was up by 0.4%, the S&P 500 by 0.6%, Nasdaq by 0.8%, and the Russell 2000 by 0.4%. This morning, most Asian markets are higher, led by Taiwan. US futures are marginally lower, while European futures are starting the week almost 1% lower.

FI: Friday last week, European rates continued the almost uninterrupted streak of decline through November. The entire German curve has essentially shifted 30bp down across all tenors with the 10y Bund yield ending at 2.08%. We have another busy week ahead of us with tap auctions from Germany, France and Spain. Reading the Markets EUR - Look out for funding statements in December, 29 November. In France, tensions are building with Le Pen intensifying the language and potentially going for a no-confidence vote, following intense disagreement on the budget. The French-German spread has tightened some 5-6bp since the midle of last week, but still stands at a wide 80bp spread. We do not expect a material tightening from here.

FX: EUR/USD traded about one figure higher last week, fluctuating within the 1.05-1.06 range, as the broad USD had its largest weekly drop in three months. This week, a packed US calendar is set to prove pivotal for the Fed's December meeting and by extension for EUR/USD. USD/JPY slid down towards the 149-mark in a week when the JPY saw broad gains as market expectations for a BoJ rate hike in December gained traction. Friday's set of data releases out of Norway failed to deliver any significant news to our macro- or FX-narrative for Norway: private goods consumption remaining weak, unemployment grinding modestly higher and an unchanged pace of Norges Bank fiscal FX transaction purchase into December. We remain strategically bearish on the NOK.