Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0548; (P) 1.0572; (R1) 1.0603; More...

EUR/USD dips mildly ahead of 1.0609 resistance, but stays well above 1.0330 support. Intraday bias remains neutral first. For now, further decline is still in favor with 1.0609 resistance intact. On the downside, break of 1.0330 will resume the fall from 1.1213. Also, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication. Nevertheless, firm break of 1.0609 will confirm short term bottoming, and turn bias back to the upside for 1.0760 support turned resistance first.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

Dollar Strengthens Amid Trump’s Currency Warning and Biden’s Last Semiconductor Crackdown on China

Dollar started the week on strong footing, buoyed by a combination of technical factors and geopolitical developments. Technically, the greenback bounced after failing to break through near-term support level against Euro last week. Escalating political and trade tensions is giving further fuel to Dollar's rise.

Over the weekend, US President-elect Donald Trump stirred market attention with a direct demand to BRICS nations, calling for a halt to any plans for a new currency alternative to Dollar. Trump warned on social media that such moves would trigger "100% tariffs" and potentially end these nations’ ability to sell into the "wonderful US economy", underscoring his intent to preserve the "mighty US dollar" as the dominant global currency.

Adding to Dollar's momentum, reports indicate that the US is launching Biden administration's final large-scale efforts on China's semiconductor industry. According to sources cited by Reuters, the new measures include restricting exports to 140 Chinese companies, imposing curbs on shipments of high-bandwidth memory chips critical for AI training, and limiting advanced chipmaking tools and software. The initiative, targeting sectors critical to artificial intelligence and military advancements, underscores ongoing US-China trade tensions, which persist across multiple administrations.

In terms of currency performance, Dollar is currently the strongest, followed by Australian Dollar and Canadian Dollar. Japanese Yen is the weakest performer, trailed by Euro and Swiss Franc, while British Pound and New Zealand Dollar are holding middle positions. Global financial markets are bracing for significant volatility this week, with top-tier US economic data releases on the horizon, including ISM manufacturing and services indexes and non-farm payroll report.

Technically, USD/CNH jumped notably today as near term rally from 6.9709 resumed through 7.7276. This development aligns with the view that medium term correction from 7.3679 (2023 high) has completed with three waves down to 6.9709. Further rise is expected as long as 7.2279 support holds. Break of 7.3111 resistance will pave the way to 7.3679 or further to 7.3745 (2022 high). A key to watch is whether the next decline in Yuan's exchange rate would prompt the Chinese government for some form of intervention.

In Asia, at the time of writing, Nikkei is up 0.66%. Hong Kong HSI is up 0.20%. China Shanghai SSE is up 0.93%. Singapore Strait Times is up 0.29%. Japan 10-year JGB yield is up 0.0264 at 1.079.

Japan's PMI manufacturing finalized at lowest since March, but optimism grows for 2025 recovery

Japan’s Manufacturing PMI was finalized at 49.0 in November, down from October’s 49.2, marking its lowest reading since March. The decline reflects ongoing challenges, with weaker demand leading to sustained declines in new orders and production levels.

S&P Global Market Intelligence’s Usamah Bhatti described the sector’s performance as "downbeat," noting subdued capacity pressures and firms reducing employment for the first time in nine months due to the lack of demand-driven growth.

Cost inflation remained elevated in November, prompting manufacturers to increase selling prices at a stronger rate to protect margins.

However, firms remain optimistic about the future, with confidence reaching its highest level since August. Optimism is supported by expectations of domestic and global economic recovery, alongside planned new product launches that could drive future sales.

Separately, capital spending rose 8.1% yoy in Q3, exceeding expectations of 6.7% yoy and accelerating from Q2’s 7.4% yoy growth. This marks the fastest annual growth in investment since Q4 last year, providing a silver lining amid subdued manufacturing activity.

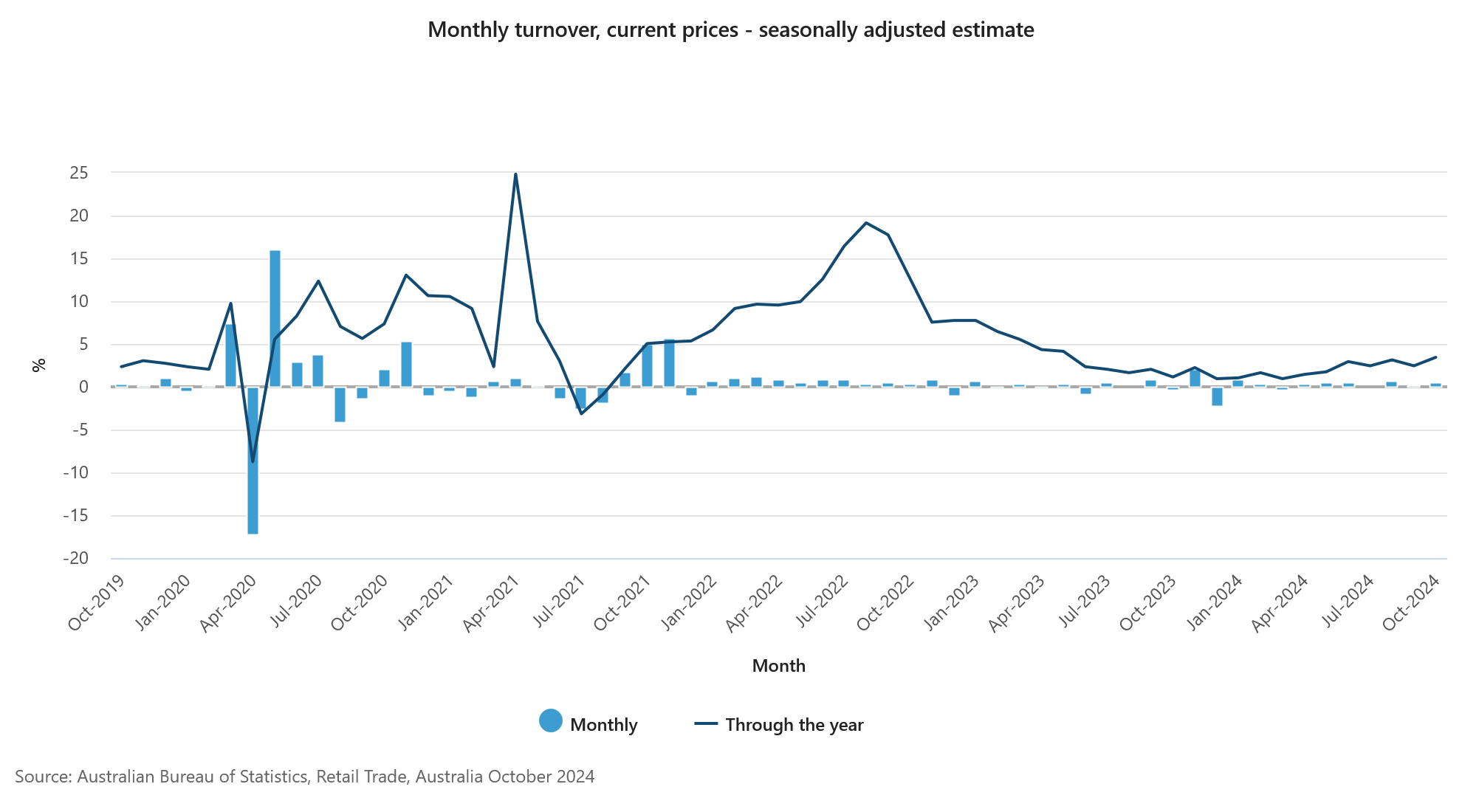

Australia’s retail sales beat expectations with 0.6% mom growth in Nov

Australia’s retail sales increased by 0.6% month-on-month to AUD 36.7B in November, surpassing the forecasted 0.4% mom rise. On a year-on-year basis, sales grew 3.4% yoy, supported by early Black Friday promotions.

Strong gains were seen in non-food categories, with other retailing up 1.6% and household goods retailing rising 1.4%, driven by demand for electronics like televisions. However, declines were noted in clothing, footwear, and personal accessories (-0.6%) and department stores (-0.3%).

Food-related sectors also performed well, with cafes, restaurants, and takeaway services rising 0.3% for the third consecutive month. Food retailing rebounded 0.3%, led by a 1.7% jump in liquor sales, returning turnover to July 2024 levels.

China’s Caixin PMI manufacturing rises to 51.5, confidence grows but challenges in jobs persist

China’s Caixin Manufacturing PMI climbed to 51.5 in November, up from 50.3 in October and surpassing expectations of 50.5. This marks the fastest pace of growth since June, driven by a rebound in new orders, which rose at their quickest pace since February 2023, alongside renewed export growth. Output price inflation reached a 13-month high, and business confidence strengthened to its highest level in eight months.

Wang Zhe, Senior Economist at Caixin Insight Group, highlighted that manufacturers increased supply to meet expanded demand, with businesses purchasing more to build inventories. Input costs and output prices also rose, while supply chains remained stable.

However, employment continued to contract, underscoring lingering challenges. Wang noted that the economy faces "prominent downward pressure," with the government's stimulus measures yet to significantly impact the labor market and workforce expansion.

Markets Focus on U.S. Payrolls, Global Data as Central Banks Weigh Next Moves

As Fed's final rate decision of the year looms, markets are gearing up for a pivotal week of economic data. Among the highlights is the US non-farm payrolls report, which will heavily influence the Fed’s next move. Currently, fed fund futures suggest a 66% chance of a 25bps rate cut to 4.25-4.50%, but these expectations could shift sharply after the NFP release. October’s lackluster job growth of just 12k was widely attributed to disruptions from hurricanes and strikes, making November’s data critical in determining whether the labor market’s underlying strength persists. Additionally, ISM manufacturing and services indexes are also on the radar

Globally, attention turns to Swiss CPI, Australian GDP, and Canadian employment figures, each of which could drive significant policy and market reactions.

In Switzerland, deflation risks persist due to strong Franc and weak demand from the EU. SNB President Martin Schlegel recently remarked, “When Germany has a cold, Switzerland has the flu,” underscoring Switzerland’s reliance on its largest EU trading partner. With these pressures, another SNB rate cut in December is expected. The key question is whether the adjustment will be more aggressive.

In Australia, RBA remains steadfast in its restrictive stance, as reinforced by its recent minutes. RBA emphasized that significant cooling in the labor market is needed to balance demand and supply, which would also temper wage growth. While this could slow economic expansion, inflation concerns keep rate cuts off the table for now.

Meanwhile, in Canada, BoC is likely to remain on its fast track toward neutral interest rates, with another 50bps rate cut expected next week. Continued soft employment data, particularly a rising unemployment rate, would solidify this expectation.

Here are some highlights for the week:

- Monday: New Zealand building permits; Japan capital spending, PMI manufacturing final Australia retail sales, building approvals; Swiss retail sales, PMI manufacturing; Eurozone PMI manufacturing final, unemployment rate; UK PMI manufacturing final; US ISM manufacturing.

- Tuesday: New Zealand terms of trade; Japan monetary base; Australia current account; Swiss CPI.

- Wednesday: Australia GDP; China Caixin PMI services; Eurozone PMI services final, PPI; UK PMI services final; US ADP employment, ISM services, factor orders, Fed's Beige Book report.

- Thursday: Australia trade balance; Swiss unemployment rate; Germany factory orders; France industrial production; UK PMI construction; Eurozone retail sales; Canada trade balance, Ivey PMI; US Challenger job cuts, trade balance, jobless claims.

- Friday: Japan labor cash earnings, household spending, leading indicators; Germany industrial production, trade balance; Swiss foreign currency reserves; Eurozone GDP revision; Canada employment; US non-farm payrolls, U of Michigan consumer sentiment.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0548; (P) 1.0572; (R1) 1.0603; More...

EUR/USD dips mildly ahead of 1.0609 resistance, but stays well above 1.0330 support. Intraday bias remains neutral first. For now, further decline is still in favor with 1.0609 resistance intact. On the downside, break of 1.0330 will resume the fall from 1.1213. Also, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication. Nevertheless, firm break of 1.0609 will confirm short term bottoming, and turn bias back to the upside for 1.0760 support turned resistance first.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

Australia’s retail sales beat expectations with 0.6% mom growth in Nov

Australia’s retail sales increased by 0.6% month-on-month to AUD 36.7B in November, surpassing the forecasted 0.4% mom rise. On a year-on-year basis, sales grew 3.4% yoy, supported by early Black Friday promotions.

Strong gains were seen in non-food categories, with other retailing up 1.6% and household goods retailing rising 1.4%, driven by demand for electronics like televisions. However, declines were noted in clothing, footwear, and personal accessories (-0.6%) and department stores (-0.3%).

Food-related sectors also performed well, with cafes, restaurants, and takeaway services rising 0.3% for the third consecutive month. Food retailing rebounded 0.3%, led by a 1.7% jump in liquor sales, returning turnover to July 2024 levels.

China’s Caixin PMI manufacturing rises to 51.5, confidence grows but challenges in jobs persist

China’s Caixin Manufacturing PMI climbed to 51.5 in November, up from 50.3 in October and surpassing expectations of 50.5. This marks the fastest pace of growth since June, driven by a rebound in new orders, which rose at their quickest pace since February 2023, alongside renewed export growth. Output price inflation reached a 13-month high, and business confidence strengthened to its highest level in eight months.

Wang Zhe, Senior Economist at Caixin Insight Group, highlighted that manufacturers increased supply to meet expanded demand, with businesses purchasing more to build inventories. Input costs and output prices also rose, while supply chains remained stable.

However, employment continued to contract, underscoring lingering challenges. Wang noted that the economy faces "prominent downward pressure," with the government's stimulus measures yet to significantly impact the labor market and workforce expansion.

Japan’s PMI manufacturing finalized at lowest since March, but optimism grows for 2025 recovery

Japan’s Manufacturing PMI was finalized at 49.0 in November, down from October’s 49.2, marking its lowest reading since March. The decline reflects ongoing challenges, with weaker demand leading to sustained declines in new orders and production levels.

S&P Global Market Intelligence’s Usamah Bhatti described the sector’s performance as "downbeat," noting subdued capacity pressures and firms reducing employment for the first time in nine months due to the lack of demand-driven growth.

Cost inflation remained elevated in November, prompting manufacturers to increase selling prices at a stronger rate to protect margins.

However, firms remain optimistic about the future, with confidence reaching its highest level since August. Optimism is supported by expectations of domestic and global economic recovery, alongside planned new product launches that could drive future sales.

Separately, capital spending rose 8.1% yoy in Q3, exceeding expectations of 6.7% yoy and accelerating from Q2’s 7.4% yoy growth. This marks the fastest annual growth in investment since Q4 last year, providing a silver lining amid subdued manufacturing activity.

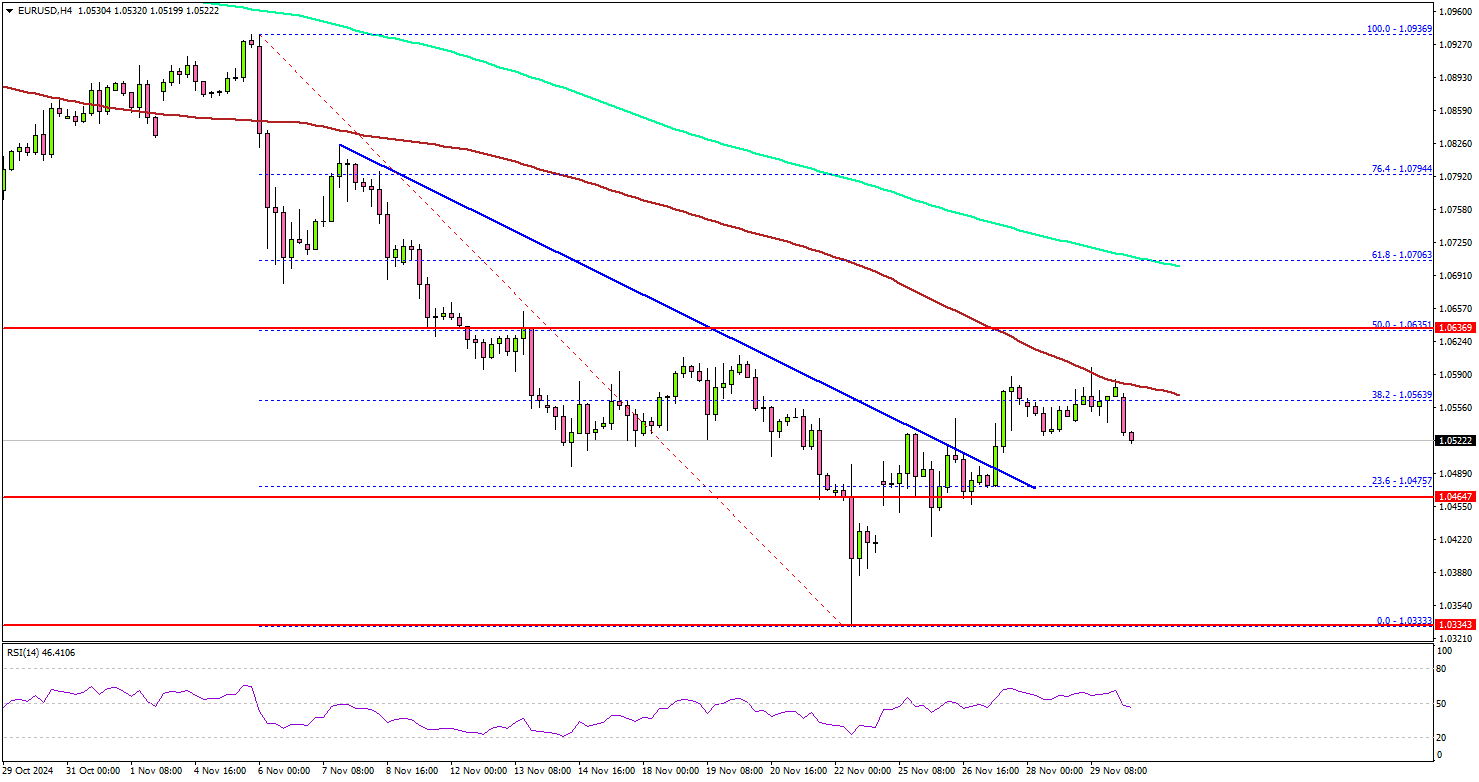

EUR/USD Turning Point: Will 1.0650 Unleash The Bulls?

Key Highlights

- EUR/USD started an upside correction from the 1.0335 zone.

- It cleared a connecting bearish trend line with resistance at 1.0520 on the 4-hour chart.

- USD/JPY is struggling and might drop below the 148.80 support.

- The US ISM Manufacturing Index could increase from 46.5 to 47.5 in Nov 2024.

EUR/USD Technical Analysis

The Euro formed a base above 1.0350 and started a recovery wave against the US Dollar. EUR/USD cleared the 1.0450 and 1.0500 levels to move into a positive zone.

Looking at the 4-hour chart, the pair surpassed a connecting bearish trend line with resistance at 1.0520 on the same chart. There was a move above the 38.2% Fib retracement level of the downward move from the 1.0936 swing high to the 1.0333 low.

The pair even tested the 100 simple moving average (red, 4-hour). On the upside, the pair could face resistance near the 1.0635 level.

The 50% Fib retracement level of the downward move from the 1.0936 swing high to the 1.0333 low is also near 1.0635. The first major resistance is near the 1.0650 level. A close above the 1.0650 level could set the tone for another increase.

The next major resistance could be the 200 simple moving average (green, 4-hour) at 1.0705, above which the price could climb higher toward the 1.080 resistance.

On the downside, immediate support sits near the 1.0500 level. The next key support sits near the 1.0450 level. Any more losses could send the pair toward the 1.0380 level.

Looking at USD/JPY, the pair remains in a bearish zone and there are chances of more downsides below the 148.80 support.

Upcoming Economic Events:

- Euro Zone Manufacturing PMI for Nov 2024 – Forecast 45.2, versus 45.2 previous.

- UK Manufacturing PMI for Nov 2024 – Forecast 48.6, versus 48.6 previous.

- US Manufacturing PMI for Nov 2024 – Forecast 48.8, versus 48.8 previous.

- US ISM Manufacturing Index for Nov 2024 – Forecast 47.5, versus 46.5 previous.

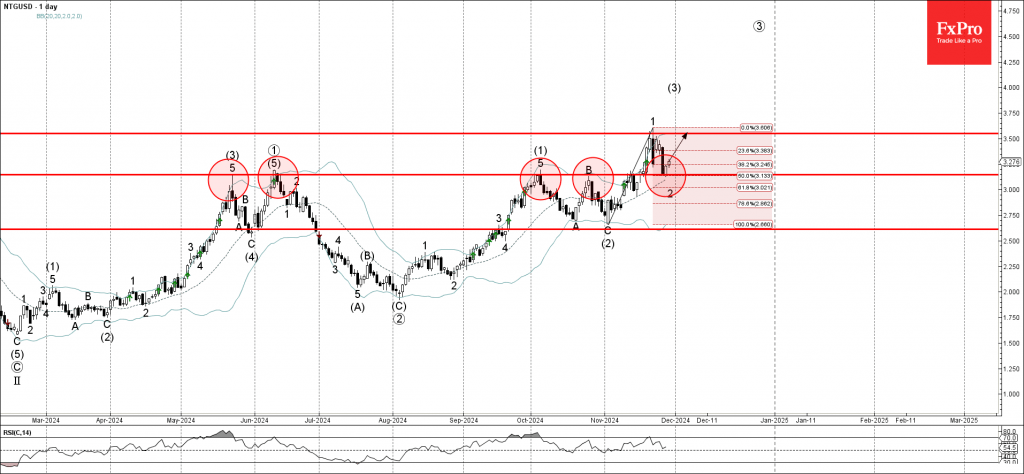

Natural Gas Wave Analysis

- Natural gas reversed from support zone

- Likely to rise to resistance level 3.550

Natural gas recently reversed up from the support zone located between the support level 3.150 (former multi-month high from May, June and October), 20-day moving average and the 50% Fibonacci correction of the upward impulse 1 from the start of November.

The upward reversal from the support level 3.150 stopped the previous minor correction 2 – which belongs to wave (3) from the start of November.

Given the clear daily uptrend, Natural gas can be expected to rise to the next resistance level 3.550 (which stopped the previous sharp impulse wave 1 earlier this month).

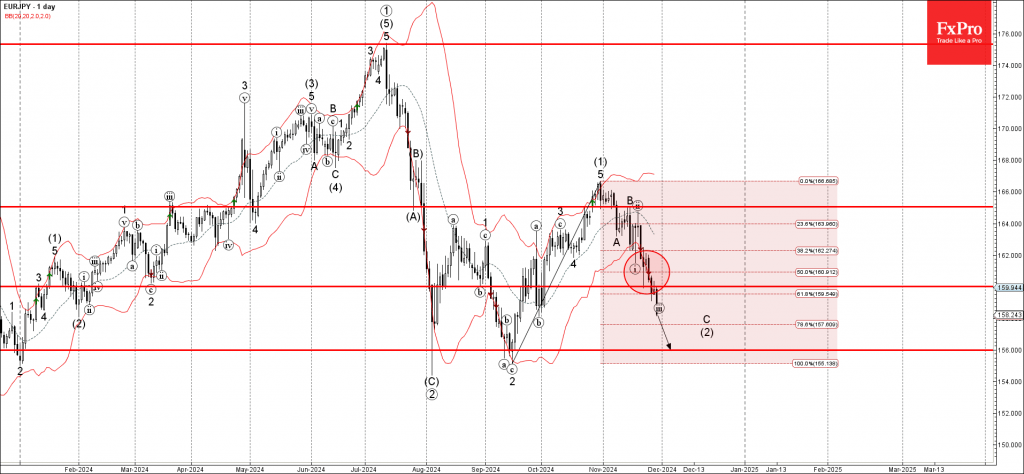

EURJPY Wave Analysis

- EURJPY broke support zone

- Likely to fall to support level 156.00

EURJPY currency pair recently broke the support zone located between the support level 160.00 and the 61.8% Fibonacci correction of the upward impulse from September.

The breakout of the support level 160.00 accelerated the C-wave of the active ABC correction (2) from the end of October.

Given the clear daily downtrend, EURJPY currency pair can be expected to fall to the next support level 156.00 (which reversed the price sharply in August and September).

Markets Weekly Outlook – US Dollar’s Fate Hinges on NFP as Fed Rate Cut Looms

- US equities finished strong, driven by tech and retail stocks, with the S&P 500 reaching record highs.

- The US dollar weakened due to increased expectations of a December rate cut by the Federal Reserve.

- The upcoming week’s focus is on US jobs data, which could impact the Fed’s decision and the US dollar’s performance.

Week in Review: Geopolitics Drives Market Sentiment

A week largely dominated by geopolitical developments as the US celebrated the Thanksgiving Holidays ended with somewhat of a whimper. The lack of liquidity was evident on Thursday and Friday as markets looked to make sense of broad development along the geopolitical sphere.

Donald Trump kicked off the week with the threat of tariffs, his main targets being Mexico, Canada and of course China. Mexican President Claudia Sheinbaum did not take it lying down as she floated the idea of retaliatory tariffs. Brave of the incoming President but still a concern for market participants which also had an effect on currencies like Australian Dollar due to the country’s ‘commodity currency’ status and trade relationship with China.

Technically, Trump could use an executive order to implement tariffs on his first day in office. However, in reality, the timing is unclear. It’s likely the tariffs will be tied to his proposed tax cuts, and such a detailed plan would take time to get approval from Congress. Let’s see how this develops.

Israel and Hezbollah agreed to a ceasefire that began on Wednesday. Israel views its mission in Lebanon as a success, having eliminated much of Hezbollah’s leadership and destroyed many of its weapons. Hezbollah meanwhile views it as a success that Israel gained no ground in Southern Lebanon. A stalemate resembling the 2006 battle between the two. While the ceasefire offers hope in a conflict-filled region, achieving lasting peace will still take time.

The impact saw Oil prices face challenges as the geopolitical risk premium has for now at least disappeared. The only positive being that since an initial selloff on Monday Brent Crude prices remained rather steady for the rest of the week with a lot of choppy price action. Brent remains on course to finish the week around 3.1% down.

US equities enjoyed a surprisingly strong finish to the week with the S&P printing fresh record highs thanks to tech and retail stocks. Technology stocks, including Nvidia, helped raise the S&P 500, while industrial and financial stocks boosted the Dow. Nvidia’s stock went up by 2.4%.

Meanwhile, investors watched how shoppers reacted to big Black Friday discounts. Adobe Analytics predicted online spending would hit a record $10.8 billion, a 9.9% increase compared to last year’s Black Friday.

The S&P is on course for its biggest one-month rise since November 2023. The Russell 2000 index hit a record high earlier in the week, on pace for its steepest monthly rise so far this year.

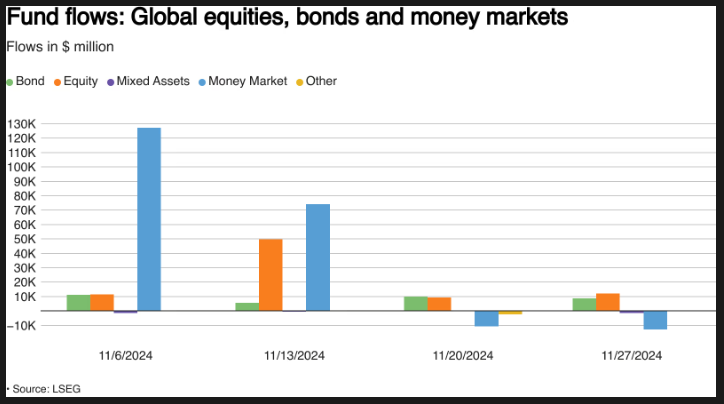

The performance of Wall Street Indexes is reflected in fund flow data with investors pumping a substantial $12.19 billion into global equity funds, a jump of 32% compared with about $9.24 billion worth of net acquisitions in the week before, LSEG Lipper data showed. It marked the ninth consecutive weekly inflow.

Source: LSEG Data

The DXY struggled this week as the probability of a December rate cut from the Federal Reserve increased around 10%. A lot of this came down to the Fed meeting minutes release as well as robust jobs data.

Despite this USD weakness EUR/USD failed to break above the 1.0600 handle with Cable gaining some ground to trade back above the 1.2700 handle. Gold (XAU/USD) experienced a massive selloff to start the week but held above the $2600/oz handle before making its way back above the $2650/oz handle.

The precious metal will still finish the week down around 2% having traded at a peak of around $2720/oz in the early hours of Monday morning.

The Week Ahead: US Jobs Data to Dominate

Asia Pacific Markets

The week ahead in the Asia Pacific region sees an uptick in economic data releases.

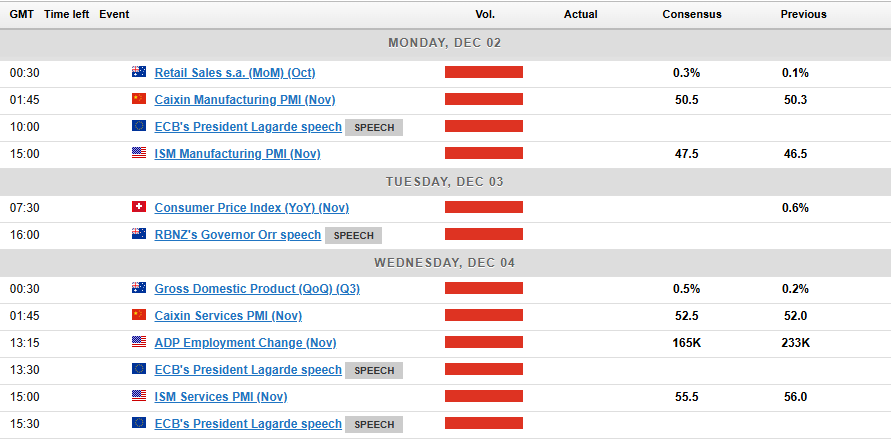

In China, PMI data will be important this week. On Saturday morning, the National Bureau of Statistics (NBS) will release the official manufacturing and non-manufacturing PMI. There is an expectation that the manufacturing PMI will rise slightly to 50.3 from 50.1, showing signs of steady growth. The Caixin manufacturing PMI will be out on Monday.

In Japan, real cash earnings might see a small growth of 0.1% year-on-year in October. With strong labor earnings, the Bank of Japan could raise interest rates in December.

In Australia, markets have quite a bit of high impact data to deal with. Having had a bumper week in lieu of tariff threats against China which sent the Aussie through some volatility the week ahead may prove similar.

Retail sales kicks things off on Monday before we get some GDP data on Wednesday and to round the week off, trade balance data will be released on Thursday.

Europe + UK + US

In developed markets, the focus moves back to the US and jobs date with the NFP due out for release on Friday.

Last month, non-farm payrolls only increased by 12,000, much lower than expected. Hurricane Milton caused big job losses in Florida, where employment dropped by 38,000 compared to its usual growth of 13,000.

This suggests that Hurricane Milton has had a significant impact on payroll data, now with those issues out of the way there is a chance the number could be higher this week. A print around the 220k mark is very much a possibility with the unemployment rate also key to help the Fed ahead of the December meeting.

If unemployment rises to 4.2% and jobs growth comes in around the 220k mark there is a greater chance of a Fed rate cut in December and this could lead to US Dollar weakness.

In Europe and the UK there is a lack of high impact data releases. However we do have a speech by ECB President Christine Lagarde on Wednesday which could provide some insight into where the ECB is leaning regarding December rate cuts.

The slight improvement in Eurostat sentiment as well as the uptick in German inflation which rose to 2.2% year-on-year, up from 2.0% YoY in October will likely rule out a 50 bps cut. Any sign from Lagarde in her speech could stoke some short-term volatility for the Euro.

Chart of the Week

This week’s focus could have been either USD/JPY that has a broken a key medium-term ascending trendline or the chart i have chosen which is GBP/USD.

Cable has benefited from rising expectations that the Bank of England (BoE) will hold rates steady at the December meeting while the Fed are now projected to cut by 25 bps. The impact of this repricing has seen GBP/USD push away from support at the 1.2500 key level to trade just shy of resistance at 1.27500.

As things stand GBP/USD is at intriguing area heading into next week. Price is currently just below resistance at 1.2750 with a key confluence area around the 1,2800 handle where you have the descending trendline and the 200-day MA at 1.2819.

This as the RSI period 14 approaches the 50 neutral level with a break above likely signaling a shift in momentum. If this coincides with a trendline break bulls may be emboldened and this could push GBP/USD toward the 1.3000 psychological level once more. A lot of this will hing on the DXY as well and how the US Dollar performs next week.

A trendline rejection could lead to a retest of the 1.2750 and 1/2618 support areas. A break of these areas could see sellers return and push price beyond the previous lows of around 1.2480. An interesting week ahead indeed.Equity

GBP/USD Daily Chart – November 29, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 1.2618

- 1.2500

- 1.2480

Resistance

- 1.2750

- 1.2800

- 1.2942