Sample Category Title

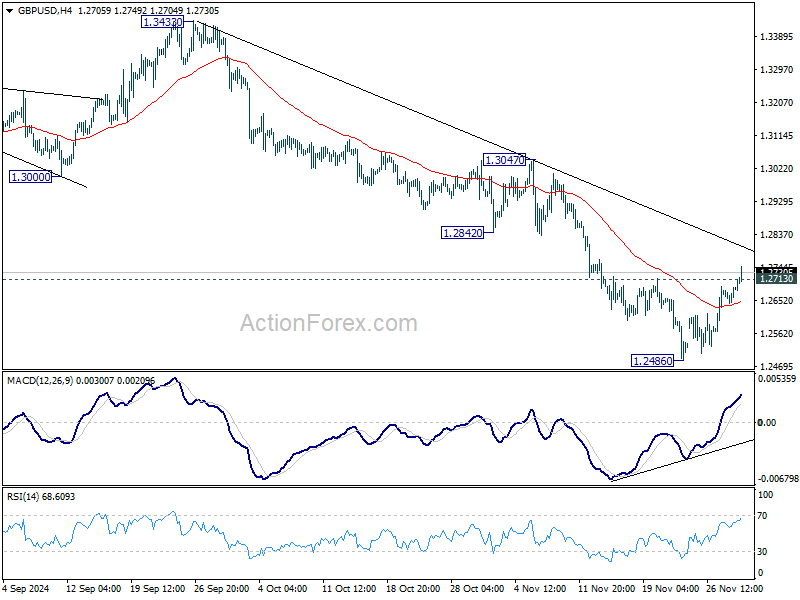

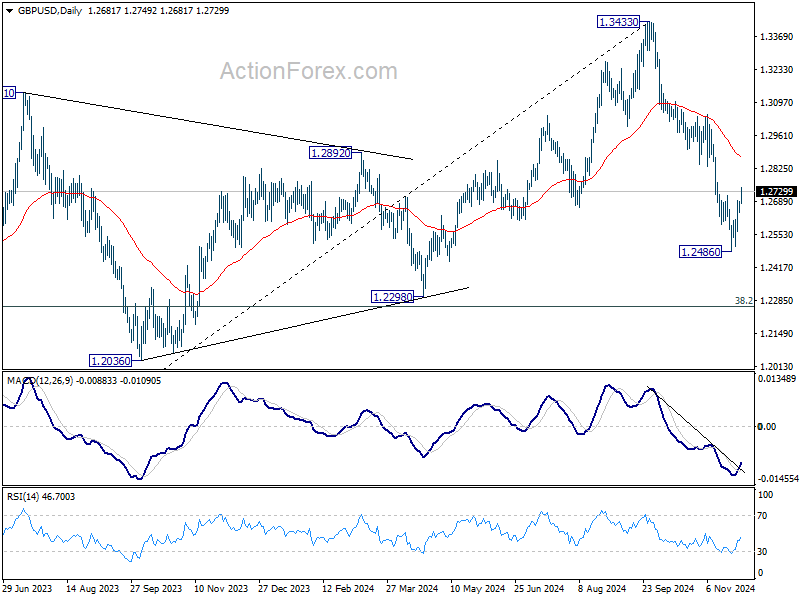

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2656; (P) 1.2676; (R1) 1.2707; More...

GBP/USD's break of 1.2713 resistance indicates short term bottoming at 1.2486, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 55 D EMA (now at 1.2873). For now, risk of another rebound remains as long as 1.2486 holds, in case of retreat.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2873) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

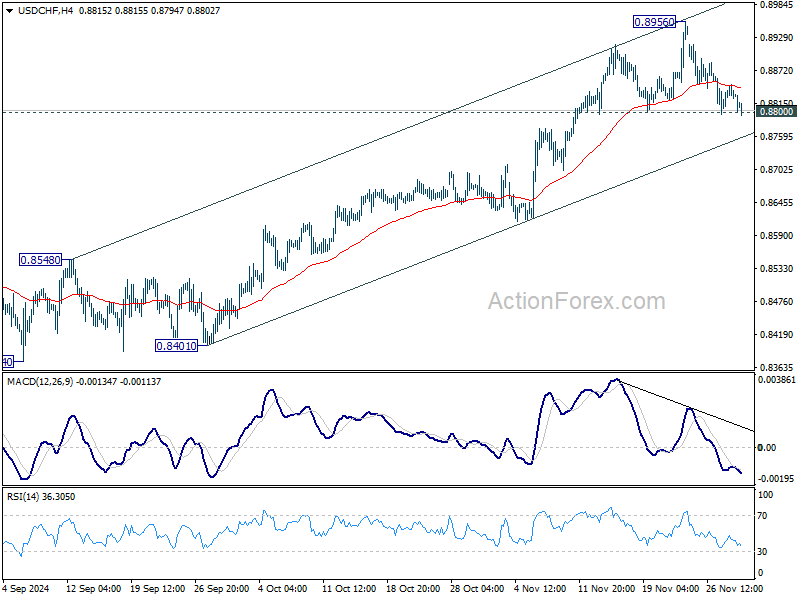

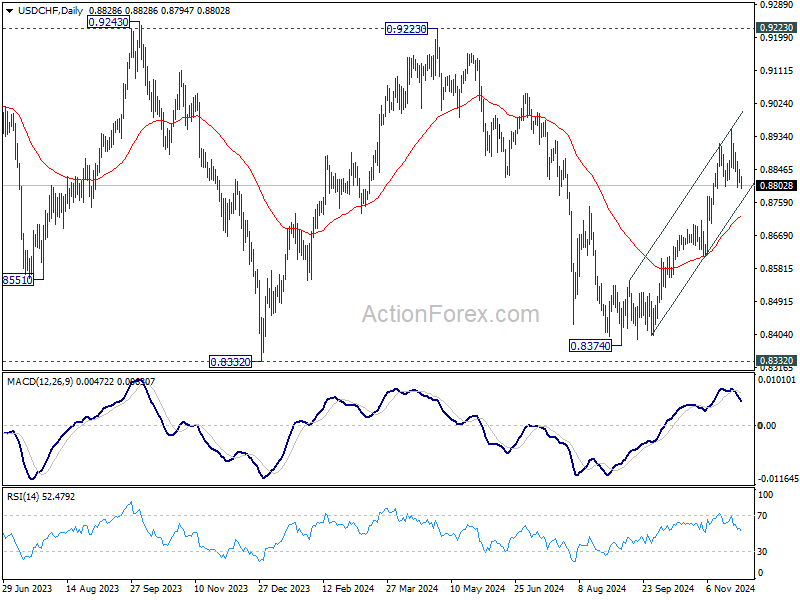

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8809; (P) 0.8828; (R1) 0.8851; More…

Intraday bias in USD/CHF remains neutral for the moment. Further rally is still in favor as long as 0.8800 support holds. On the upside, break of 0.8956 will resume the rally from 0.8374, and target 0.9223 key resistance next. However, firm break of 0.8800 will confirm short term topping and turn bias back to the downside for 55 D EMA (now at 0.8721).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

November Tokyo Inflation Boosts Odds that BOJ Will Conduct Another Hike at December Meeting

Markets

US markets were closed for Thanksgiving yesterday, leaving European markets looking for their own dynamics. National inflation data from Germany (HICP -0.7% M/M and 2.4% Y/Y; unchanged October) and Spain (0% M/M and 2.4% Y/Y from 1.8%, core 2.4% from 2.5%) overall printed on the softer side of expectations, suggesting (modest) downside risks for today’s Flash EMU release. The decline of EMU yields to the incoming CPI data was initially modest/limited. However, in afternoon trading, comments from Banque de France governor Villeroy clearly put other accents on the ECB’s strategy than board member Schnabel on Wednesday. The French governor indicated that the ECB needs full optionality in the current environment on the frequence and the size of rate cuts, including the December one. Inflation reaching the target sooner than expected also is a reason to bring rates to a neutral level and even a decline below neutral might be possible. Especially the latter assessment clearly diverged from Schnabel’s view. The combination of slightly softer than-expected CPI data and the Villeroy comments finally caused EMU yields to follow the path of least resistance, which currently obviously is still south. German yields declined 3.8 bps (5-y) to 1.9 bps (30-y). Money markets see the trough in the EMU easing cycle next year near 1.75%. The Euro this time quite easily withstood the further decline in yields and closed only modestly lower at 1.0552 (from 1.0566). Growing tensions/uncertainty on the French budget didn’t impact the euro. The Eurostoxx 50 even added 0.54%.

US markets rejoin the action today. However with no US data scheduled for release, the focus in the US might be on the shopping malls rather than on Wall Street. Still, US yields this morning continue their recent corrective decline, ceding 3-4 bps across the curve. EMU November CPI data take center stage (headline expected at -0.2% M/M and 2.3% Y/Y from 2%, core expected 2.8% from 2.7%). Even with the French and Italian data still to be released, risks for the outcome are to the downside. Question is how much further markets will/can push expected easing next year, given what is already discounted (1.75% ECB depo rate in H2). For now, there probably is no trigger to row against the existing downtrend in EMU yields, but it might shift into a lower gear. On FX markets, the euro (EUR/USD) enjoys some relief as the correction in US yields and the dollar apparently still has some legs. DXY drops below the 106 handle (105.85). USD/JPY, also pressured by yen strength, is testing the 150 mark this morning. EUR/USD gains a few ticks (EUR/USD 1.0582), but the political/budgetary uncertainty in France probably will continue to prevent dynamic/sustained comeback.

News & Views

November Tokyo inflation numbers boost market odds that the Bank of Japan will conduct another rate hike at its December policy meeting. Prices in the capital region rose by 0.5% M/M on a headline level. That’s the third such increase in the past four months. In annual terms, CPI jumped from 1.8% to 2.6%, matching the YTD high. The BoJ’s preferred ex-fresh food gauge equally rose by 0.5% M/M to be up 2.2% Y/Y (from 1.8%). More details showed goods and services inflation increasing by 0.8% and 0.2% respectively in November. Only household goods (-0.5% M/M) and entertainment (-0.1% M/M) had a dampening impact on the monthly CPI-print. The Japanese yen rallied from USD/JPY 151.50 to 150 in response to the figures with money markets currently discounting a 15 bps increase in the BoJ’s target rate (currently 0.25%).

French finance minister Armand yesterday noon already hinted that it’s better to have a budget that is not exactly the one they want instead of having no budget at all. PM Barnier than later on the day stressed that they will do everything to bring the country’s budget deficit from this year’s 6% of GDP to about 5% next year. He also announced a first major concession for the far-right RN who threatens the government over the budget bill. A previously planned increase for an electricity tax will no longer be included in the budget. From February, electricity taxes will now decrease by 14% instead of by 9%. While obviously welcomed, RN-president Bardella already said that his party won’t stop there and that other red lines remain. The French left opposition still plans to table a motion of no-confidence as soon as next week..

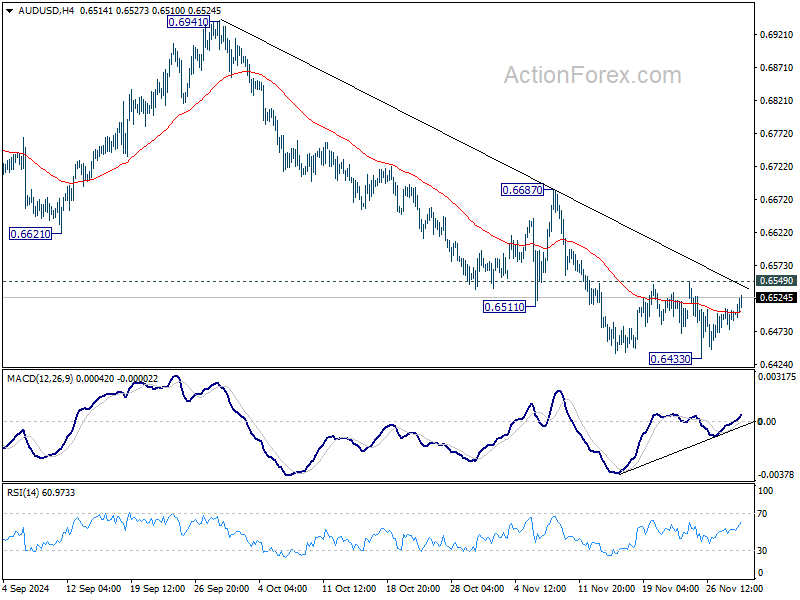

AUD/USD Daily Report

Daily Pivots: (S1) 0.6481; (P) 0.6495; (R1) 0.6513; More...

AUD/USD is still bounded in sideway trading and intraday bias remains neutral. . Further decline is expected as long as 0.6549 resistance holds. On the downside, break of 0.6433 will resume whole decline from 0.6941. However, firm break of 0.6549 will indicate short term bottoming, and bring stronger rebound to 55 D EMA (now at 0.6606).

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

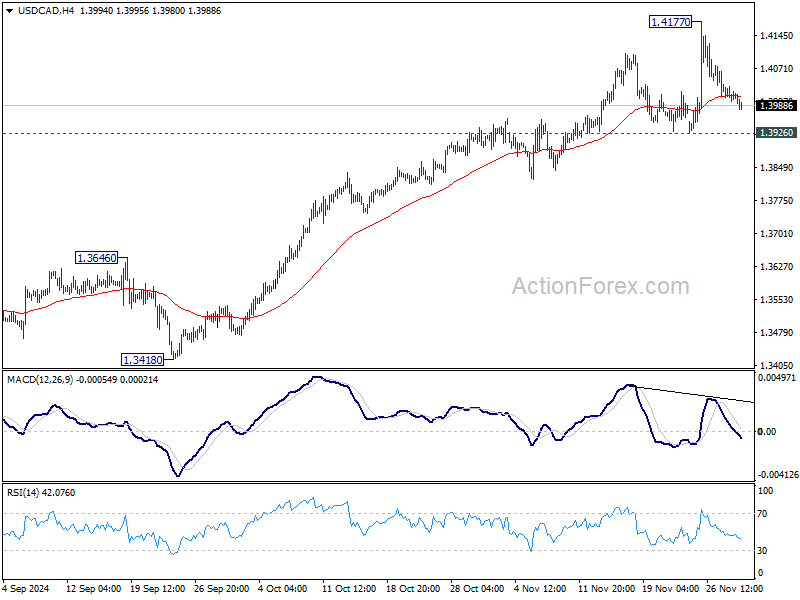

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3995; (P) 1.4019; (R1) 1.4038; More...

USD/CAD is staying in range of 1.3926/4177 and intraday bias remains neutral. Further rally is expected with 1.3930 support intact. On the upside, firm break of 1.4177 will resume larger up trend. However, break of 1.3926 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.3850).

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

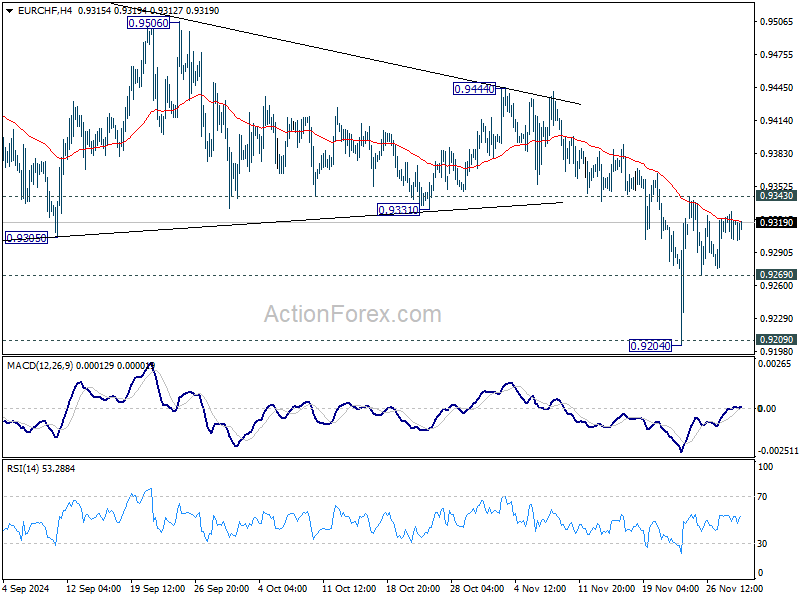

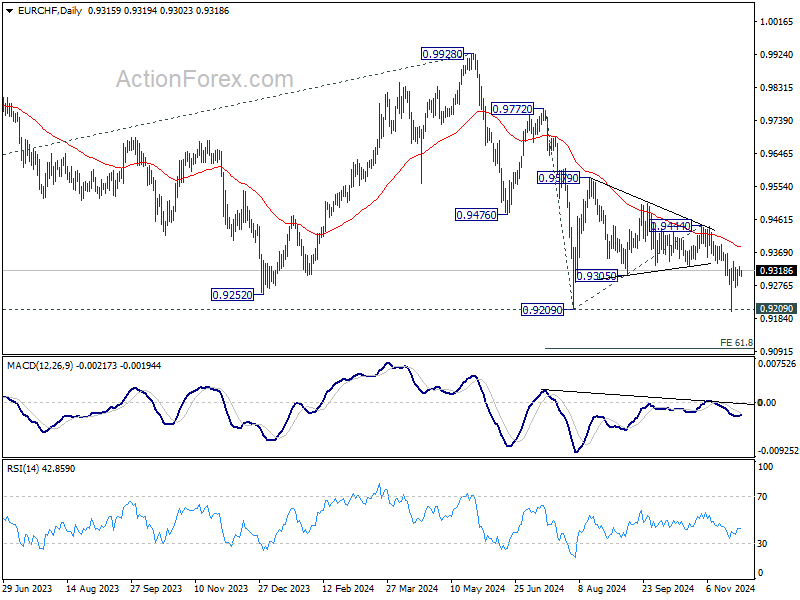

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9307; (P) 0.9318; (R1) 0.9332; More....

Intraday bias in EUR/CHF Remains neutral for the moment. On the downside, below 0.9269 minor support will bring retest of 0.9204/9 support zone. Decisive break there will confirm larger down trend resumption. Nevertheless, firm break of 0.9343 will now be a sign of near term bullish reversal, and target 0.9444 resistance for confirmation.

In the bigger picture, outlook will now stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resumed long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

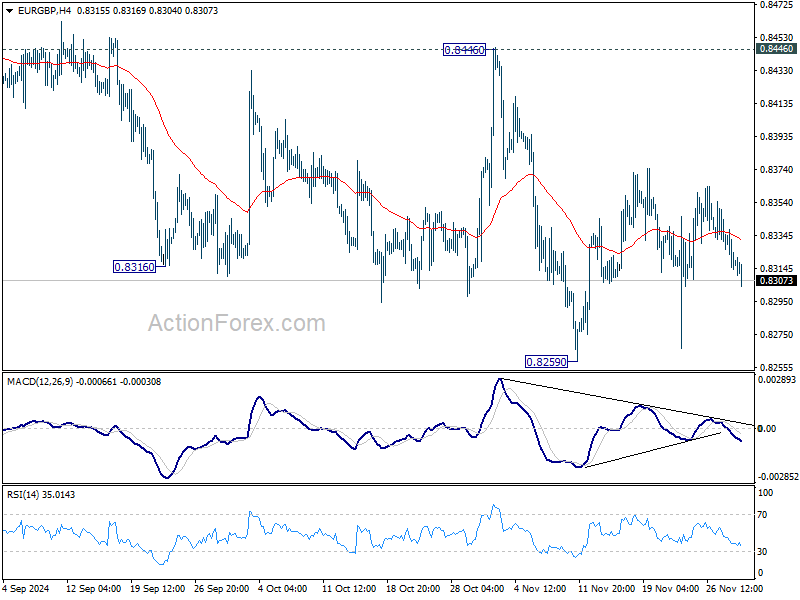

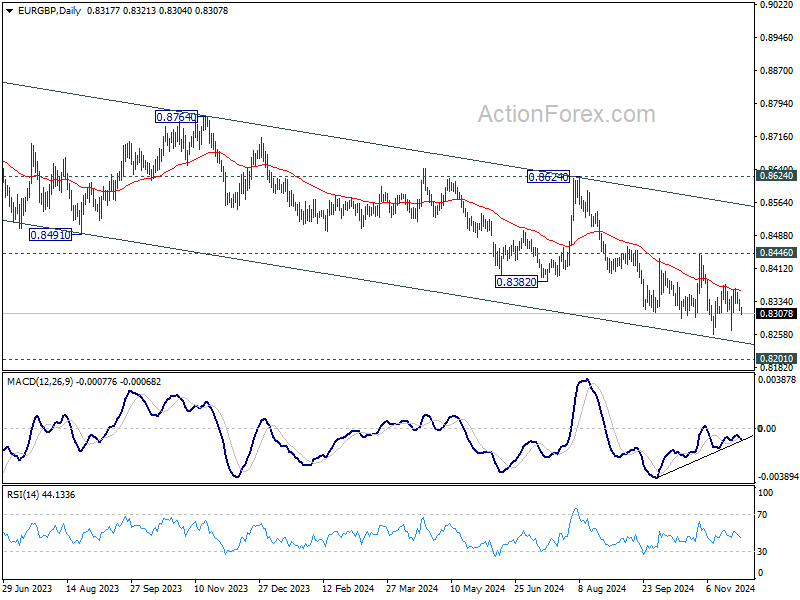

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8310; (P) 0.8324; (R1) 0.8334; More...

Outlook in EUR/GBP remains unchanged as range trading continues. Intraday bias stays neutral and further decline is expected with 0.8446 resistance intact. On the downside, decisive break of 0.8259 will resume larger down trend to 0.8201 key support.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

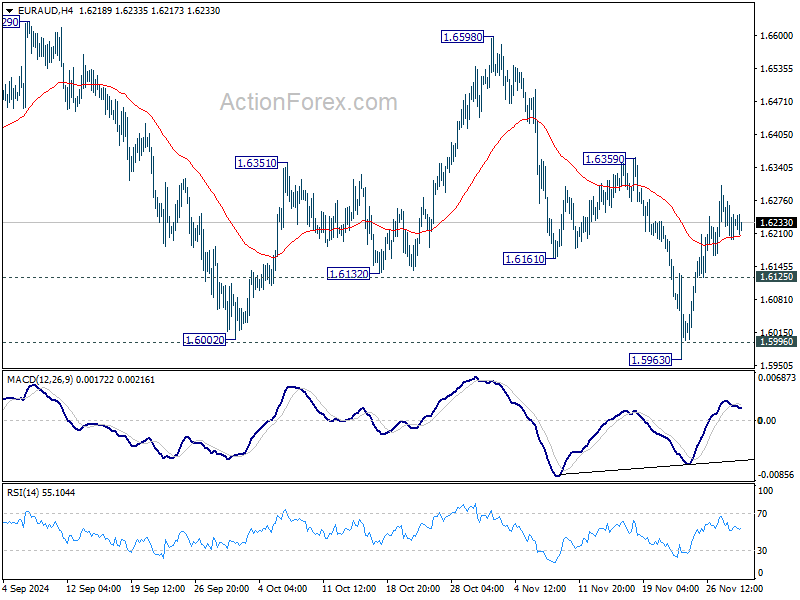

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6198; (P) 1.6241; (R1) 1.6282; More...

Intraday bias in EUR/AUD remains neutral for the moment, and outlook is unchanged. . On the upside, firm break of 1.6359 resistance will be the first sign of bullish reversal and target 1.6598 resistance for confirmation. On the downside, though, below 1.6125 minor support will bring retest of 1.5963 low.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.

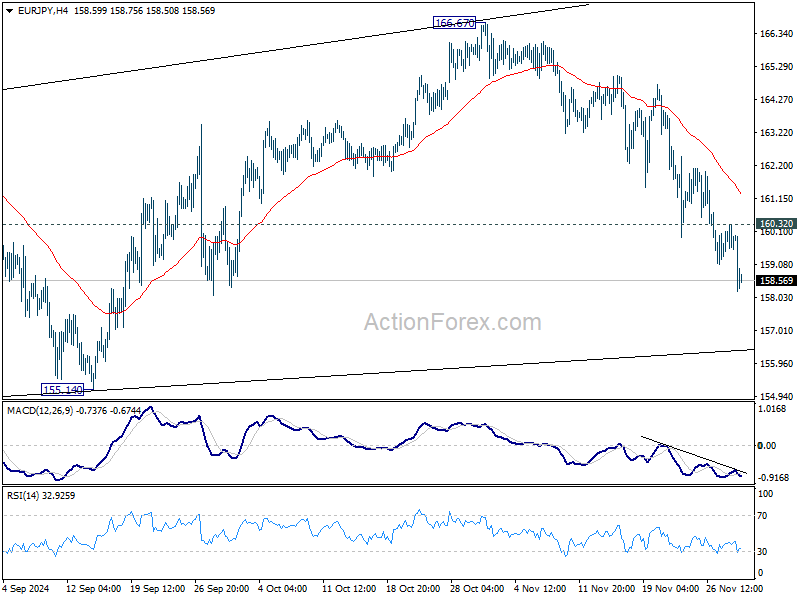

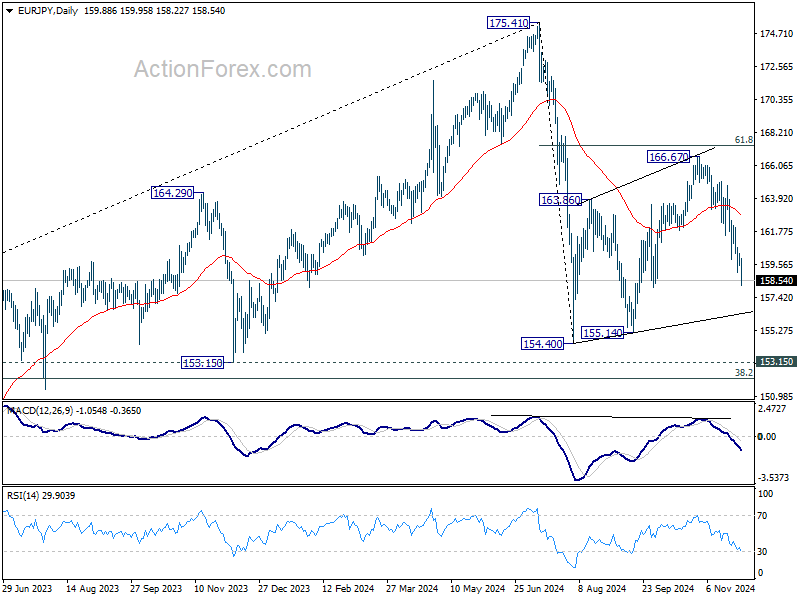

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.49; (P) 159.92; (R1) 160.36; More....

EUR/JPY's fall from 166.67 is in progress today and intraday bias stays on the downside. As noted before, corrective rebound from 154.40 could have completed with three waves up to 166.67. Deeper decline would be seen to 155.14 support next. On the upside, above 160.32 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 55 D EMA (now at 162.78) holds, in case of recovery.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

USD/JPY Tips a Toe Below 150.00 Euro CPI in Focus

The chip makers around the world felt the relief of a rumour suggesting that the sales curb to China could be less severe than previously expected. But the news didn’t necessarily translated in a strong rally. ASML - Europe’s biggest chip equipment maker that predicted a 30% fall to its Chinese revenue next year - closed 0.22% lower yesterday, while Tokyo Electron – which was up by more than 6% yesterday - couldn’t extend gains at today’s session.

With US markets paused for the Thanksgiving break, France was at the heart of the attention yesterday. The political drama, there, only got worst as Michel Barnier gave concessions to Marine Le Pen – who only asked more of them. Barnier dropped plans to increase taxes on electricity, but Le Pen’s party also wants him to drop the plans to reduce drug reimbursement, help small and medium companies compete better and index pensions on inflation starting from January 1st. The demands are nice - and they have the merit to please the French voters who, as everyone else, are dealing with inflation and cost-of-living crisis - but Le Pen’s demands cost money. And the growing French deficit doesn’t allow the French government to spend that money, please or not. The country’s debt-to-GDP stands near 5.5% today, well above the EU’s 3% target. Pushing for spending the money that you don’t have doesn’t always bode well with investors – except if you’re named after the US. Remember, Liz Truss wanted to offer the Brits significant tax cuts two years ago, and all she got was a mini financial crisis. This is what we sense from the market reaction to Le Pen’s threats that she would vote Barnier’s government down if he doesn’t give Le Pen what she wants. The French 10-year yield eased while CAC 40 was in a better mood. But the political uncertainties in France will certainly keep volatility high across French-denominated assets into the year end.

For the euro, we don’t yet see a major impact of French political shenanigans, but the French touch is not necessarily a positive one. The EURUSD swung between gains and losses yesterday, caught between mixed inflation data from Spain and Germany. Inflation in Spain ticked higher – from 1.8% to 2.4% in November, while price pressures in Germany came in softer-than-expected thanks to softer food prices. This divergence in the bloc's largest economies left traders uncertain about the European Central Bank’s (ECB) next moves. Dues this morning, the EZ aggregate inflation data is expected to print an uptick in price pressures. A softer-than-expected read will certainly keep the ECB doves in charge of the market and cap the euro appetite limited into the 1.06 psychological level, while a stronger-than-expected number should encourage the euro bulls to push for a further recovery. But in both cases, the EURUSD will remain in a bearish trend below 1.0672 – the major 38.2% Fibonacci retracement on September to November selloff.

Speaking of inflation, inflation in Tokyo came in stronger than expected in November, industrial production advanced 3%, almost the double of expectations but came in lower than expected, while retail sales grew sensibly softer than expected. But traders focuses on Tokyo inflation that backed the growing expectation that the Bank of Japan (BoJ) would hike rates in the December meeting. As such, the rise of the hawkish BoJ expectations shortly pushed the USDJPY below the 150 mark. I believe that a sustainable move below this level is possible, if the BoJ goes ahead and hikes rates in its December 18-19 meeting.

In energy, there is hesitation about what to do at the current levels. The latest news suggests that OPEC+ will delay its decision time from Sunday to December 5th. It appears that the cartel members need more time to discuss about what to do about their plans to restore production. It is clear that extending production cuts deep into next year is the only option to prevent boosting the supply gut in global markets – and keep the downside in prices limited at a time of easing geopolitical tensions in the Middle East.