Sample Category Title

EUR/GBP Weekly Outlook

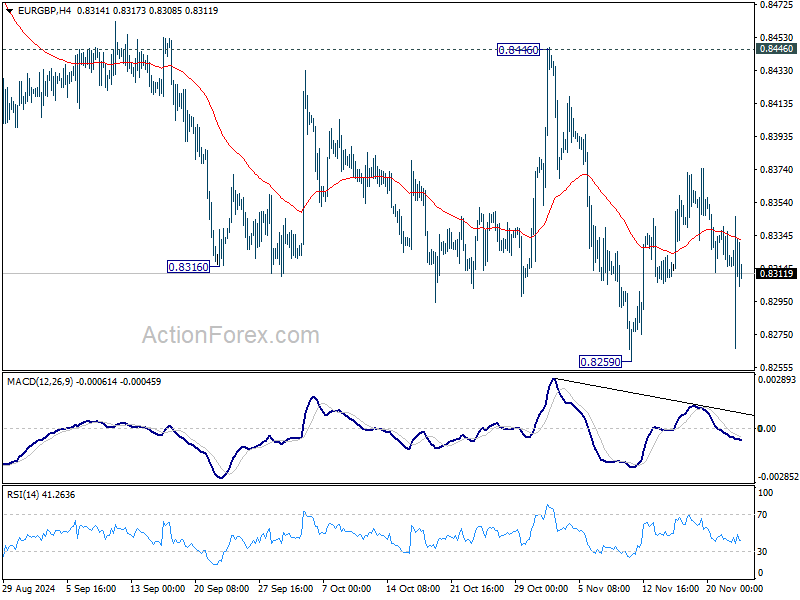

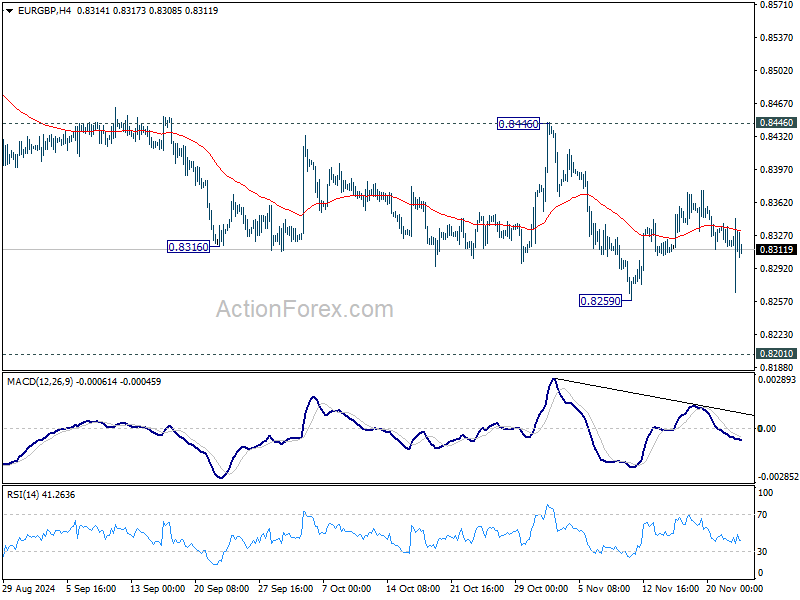

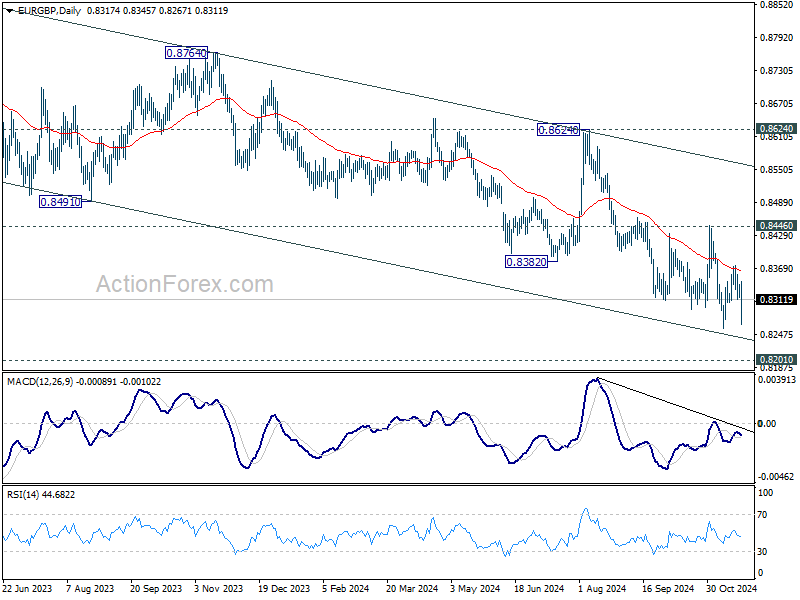

EUR/GBP spiked lower to 0.8267 last week but failed to break through 0.8259 low and recovered. Initial bias remains neutral this week first. Some more range trading could be seen but outlook will stay bearish as long as 0.8446 resistance holds. Decisive break of 0.8259 will resume larger down trend to 0.8201 key support.

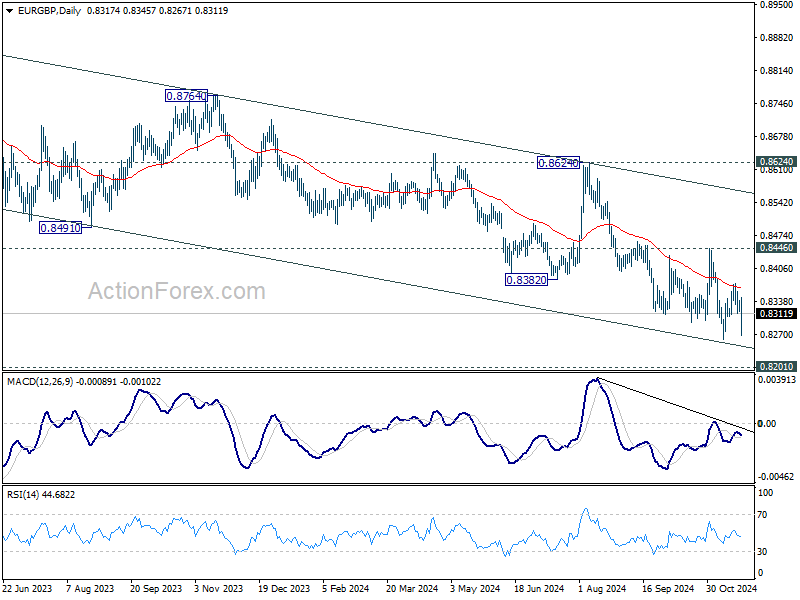

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

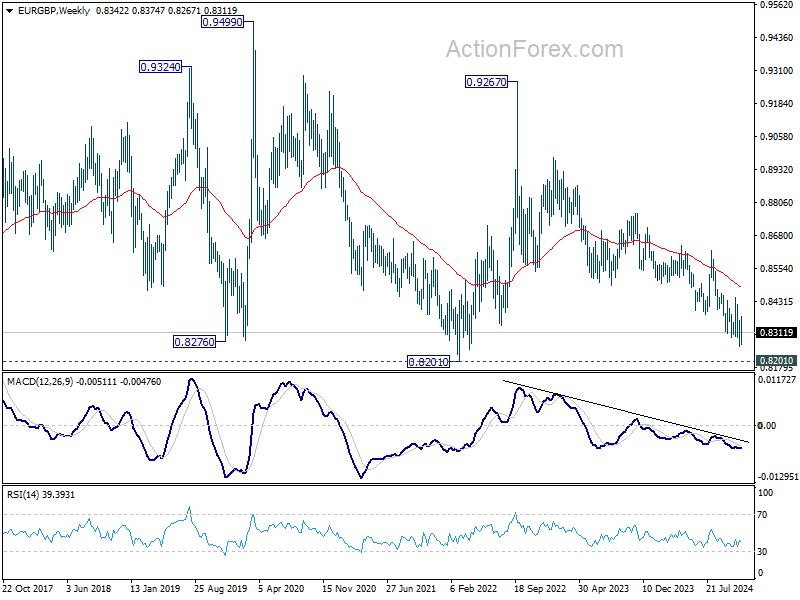

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

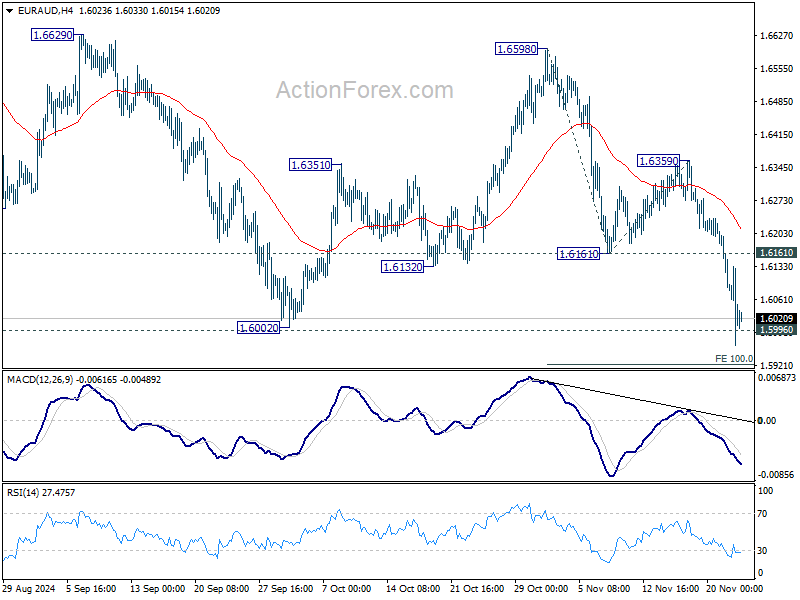

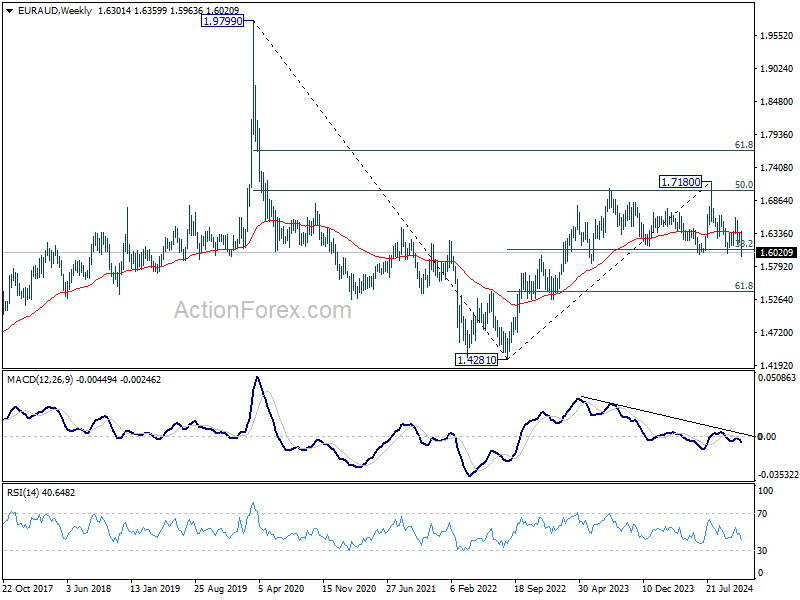

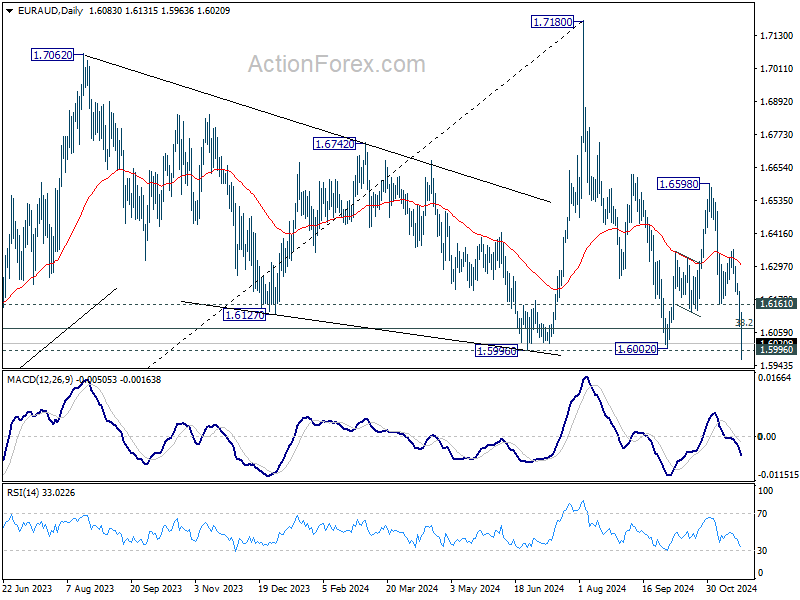

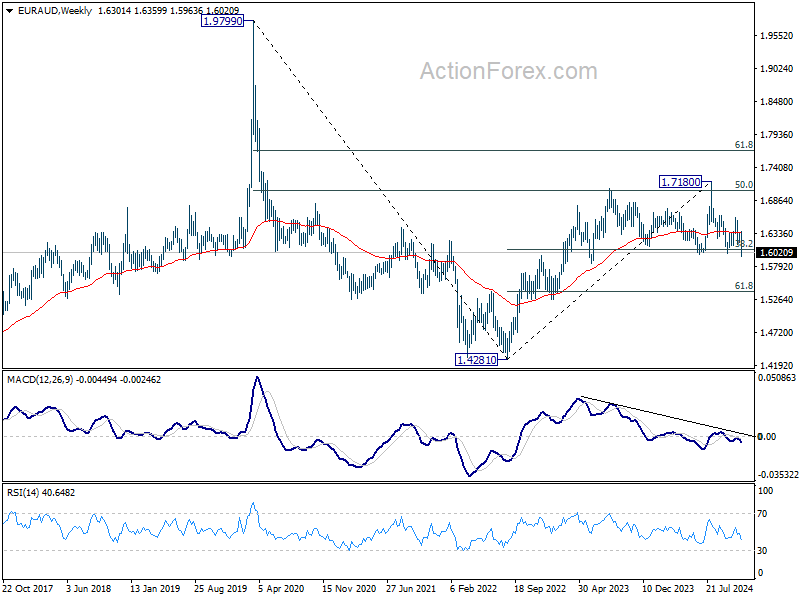

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.6598 resumed last week and hit as low as 1.5963. With no clear sign of bottoming yet, initial bias stays on the downside this week. Decisive break of 1.5996 key support will carry larger bearish implications. Next near term target will be 100% projection of 1.6598 to 1.6161 from 1.6359 at 1.5922, and then 161.8% projection at 1.5652. For now, outlook will stay bearish as long as 1.6161 support turned resistance holds, in case of recovery.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.

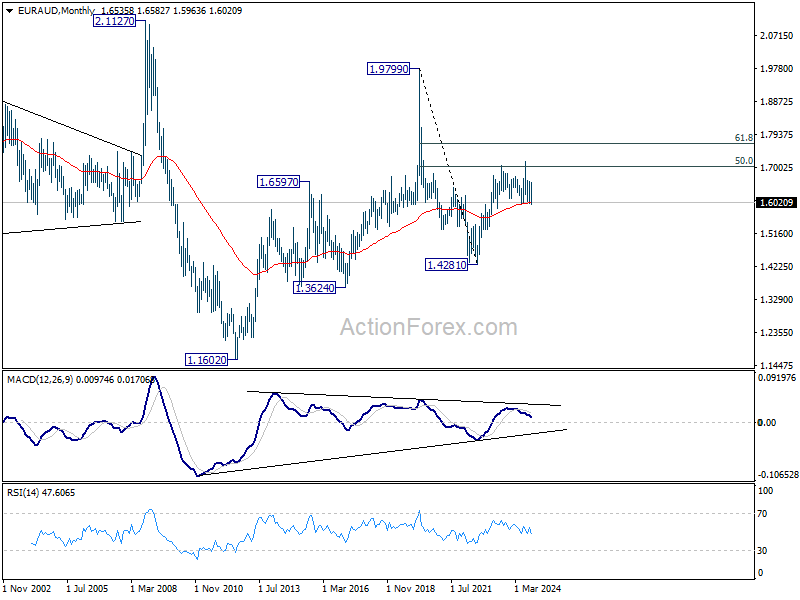

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6022) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

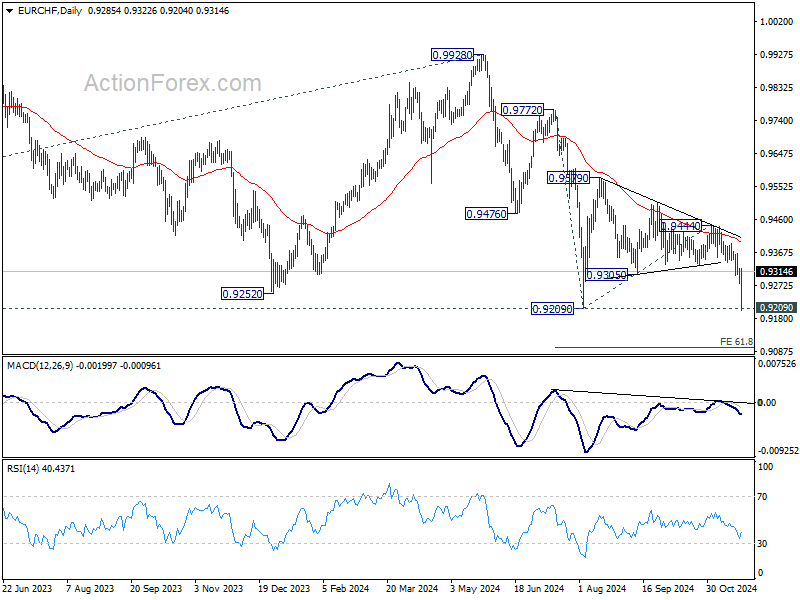

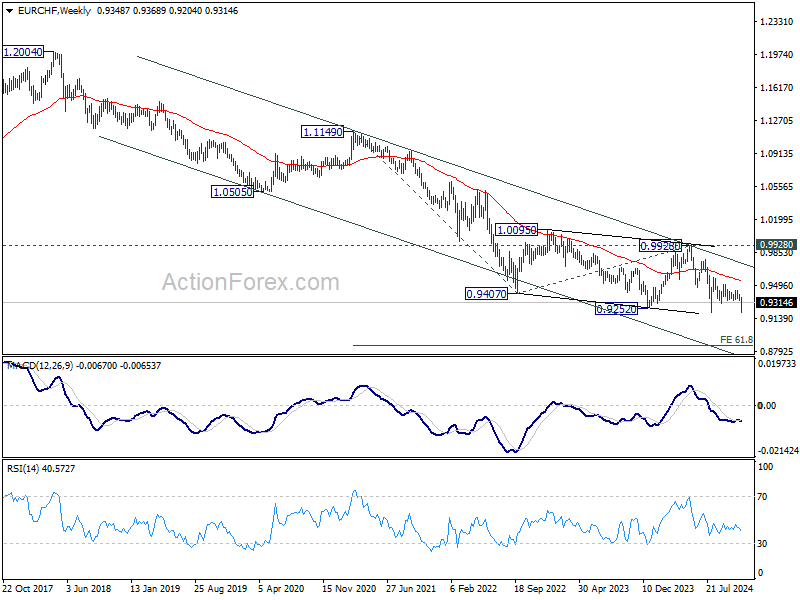

EUR/CHF Weekly Outlook

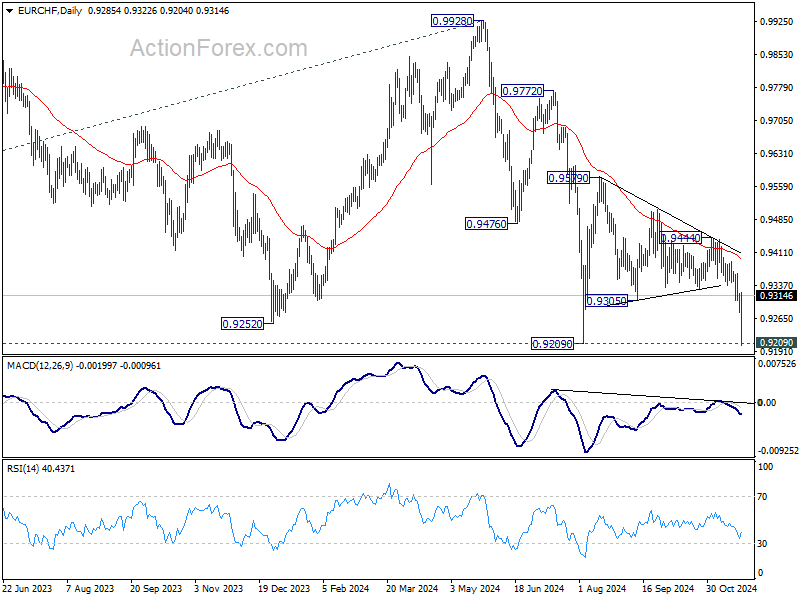

EUR/CHF dived sharply to as low as 0.9204 last week after breaking out of consolidations. But it rebounded strongly after brief breach of 0.9209 low. Initial bias is turned neutral again this week. Some more consolidations would be seen again. Outlook will stay bearish as long as 0.9364 resistance holds. Firm break of 0.9204/9 will indicate larger down trend resumption.

In the bigger picture, outlook will now stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resumed long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

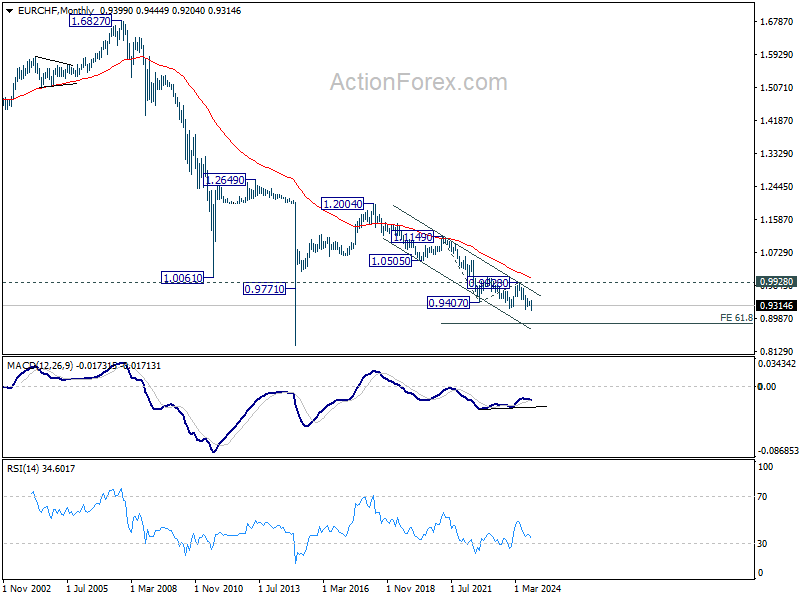

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption to 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Euro Weakens Sharply, Sterling and Swiss Franc Also Under Pressure

Euro stole the limelight last week with a steep selloff triggered by poor activity data. This downturn has intensified the pressing need for the ECB to ease monetary policy swiftly back to neutral levels. While Euro's decline was pronounced, Sterling and the Swiss Franc are not far behind, each facing their own set of challenges. Although these European majors are clearly bearish against most other major currencies, their relative outlook is less clear due to their intertwined relationship.

Conversely, Canadian Dollar and Australian Dollar emerged as the strongest performers, partly supported by renewed risk-on sentiment in the US markets. This positive mood has bolstered commodity-linked currencies as investors seek higher-yielding assets. Dollar holds the position of the third strongest currency; however, its upward momentum is somewhat capped by risk-on sentiment and sluggishness in treasury yields. Nevertheless, the greenback could merely be consolidating against commodity currencies and Yen, with buyers ready to come in again any time.

European Majors Falter on Intertwined Economic and Political Challenges

European major currencies posted significant declines last week, with Euro leading the way as market participants increased bets on more aggressive monetary easing by ECB. The catalyst for the sell-off was disappointing Eurozone PMI data, which revealed contractions in both the services and manufacturing sectors. The manufacturing sector's prolonged recession is deepening, and the services sector has now joined in contraction. The deteriorating conditions in the Eurozone's largest economies, Germany and France, have intensified concerns about the region's economic prospects.

Adding to the economic woes are mounting political challenges. France's government remains unstable following this year's snap election, and Germany is preparing for early elections, contributing to domestic uncertainty. Externally, the recent escalation in the conflict between Ukraine and Russia is casting a long shadow over the region. Furthermore, the risks of renewed trade tensions with the US looming, as a new administration under Donald Trump is set to take office next year. These factors are collectively dampening business optimism across Europe.

Economists are increasingly highlighting the urgent need for lower interest rates to support the faltering economies. The markets are currently pricing in a 50% probability of a 50 bps rate cut by ECB in December, a significant shift from previous expectations. More importantly, there is growing speculation that ECB would need to expedite the reduction of rates from the current 3.25% to the estimated neutral rate of 2%. Some ECB policymakers, particularly the more dovish members, are even discussing the possibility that rates may need to fall below the neutral level in this cycle to stimulate the economy effectively and prevent inflation undershooting.

The situation in the UK is somewhat more complex. On one side, recent data showed an unexpected contraction in retail sales and the first contraction in the private sector in 13 months, as indicated by PMI readings, with the services sector stagnating. On the other side, inflation figures surprised to the upside, with the CPI rising more than expected to 2.3%, and services inflation ticking up to 5%. These inflationary pressures, combined with uncertainty surrounding the impact of the Labour government's budget, complicate BoE's ability to accelerate monetary easing.

Moreover, according to S&P Global, business optimism in the UK has been in a sharp and persistent decline since the general elections in July. Companies are expressing a clear "thumbs down" to the recent budget policies, suggesting that sentiment may deteriorate further before reaching a bottom. This negative trend in business confidence could pressure the BoE to act more swiftly in the early part of next year to support the economy.

Swiss Franc is also facing its own set of challenges. Deflationary pressures are mounting, with Swiss CPI falling consistently from 1.4% in mid-year to just 0.6% in October. With geopolitical risks sustaining demand for the safe-haven Franc, its appreciation exacerbates further deflationary trends. Also, aggressive easing by ECB could further strengthen the Franc, potentially forcing SNB to intervene more forcefully to prevent excessive appreciation. With the policy rate already low at 1.00%, SNB has limited ammunitions before considering a return to negative interest rates.

Lack of Conviction in European Crosses, While Commodity Currencies Show Strength

Technically, while Euro displayed weakness against both the Sterling and Swiss Franc, the selling pressure lacked clear conviction, leaving the movements in EUR/CHF, EUR/GBP, and to a lesser extent GBP/CHF indecisive. This lack of clarity suggests that market participants are still hesitant to fully commit to a clear trend for these pairs.

In contrast, the outlook for European crosses with commodity currencies appears more defined. This is likely driven by renewed sense of risk appetite, particularly stemming from the strength seen in US markets.

EUR/GBP spiked lower on Friday but quickly recovered ahead of 0.8259 support, without a breakout. On the one hand, near term outlook stays bearish with 0.8446 resistance intact, and further decline is in favor. On the other hand, EUR/GBP would be facing an important level at 0.8201 (2022 low) on next fall, which could provide strong support for a sustainable rebound. It might still take some more time for the outlook to clear out itself.

EUR/CHF dived even more sharply to 0.9204 on Friday, but rebounded equally strongly after a brief breach of 0.9209 low. The long term down trend remains intact, but EUR/CHF would likely have more consolidations above 0.9204/9 first before making a more decisive down move.

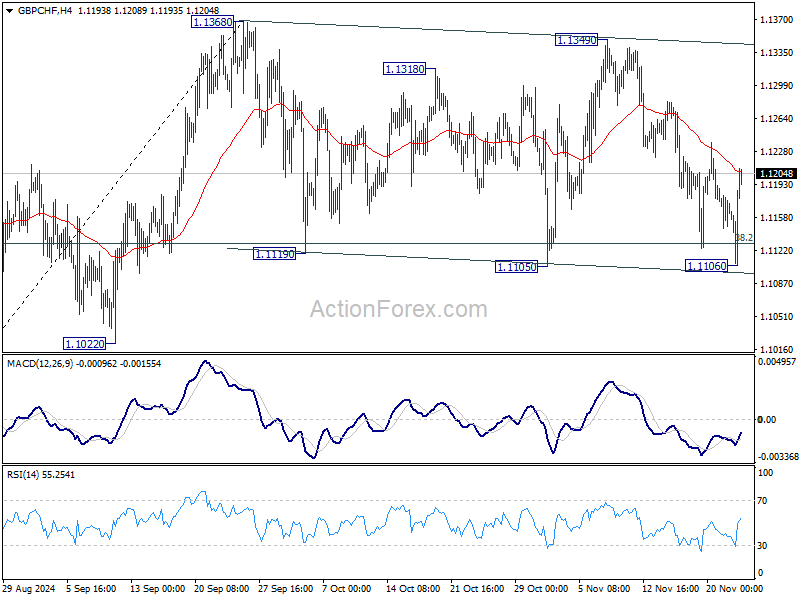

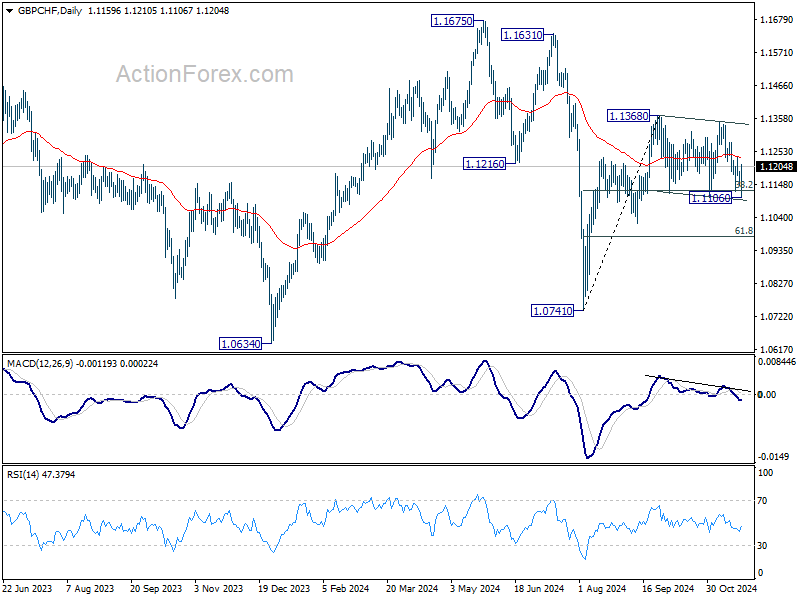

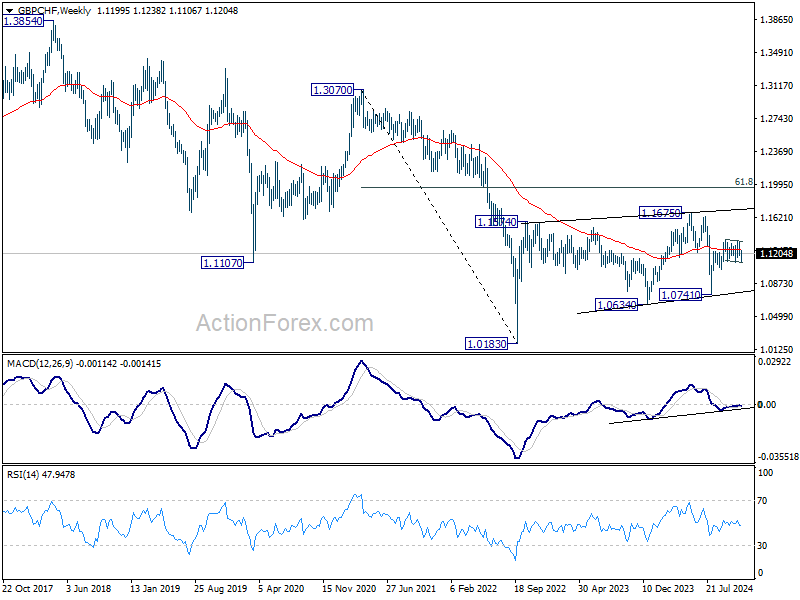

GBP/CHF drew notable support again from 38.2% retracement of 1.0741 to 1.1368 at 1.1128 again last week. The development keeps price action from 1.1368 as a sideway consolidation pattern. That means, rise from 1.0741 is still in favor to resume at a later stage. Yet, firstly, the bullish outlook is not totally cleared with GBP/CHF still struggling around flat 55 W EMA. Secondly, it's unsure how long the consolidation will extend further.

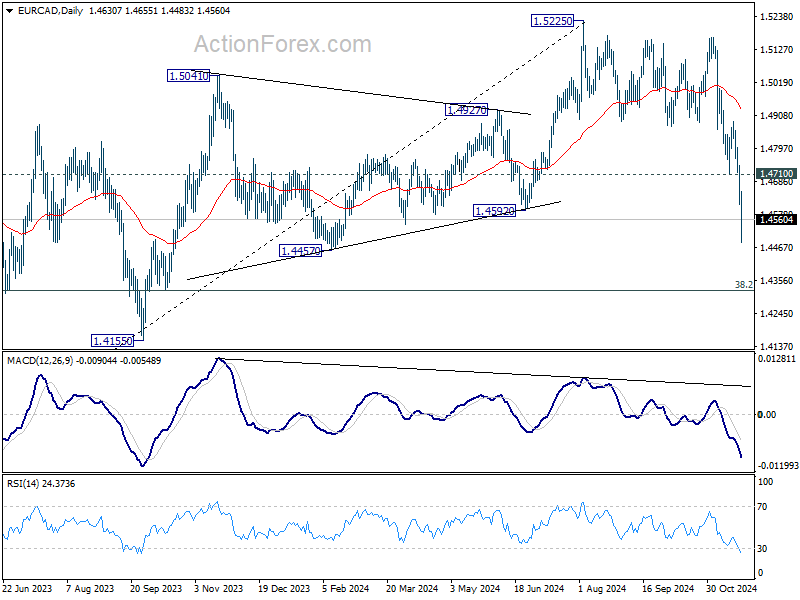

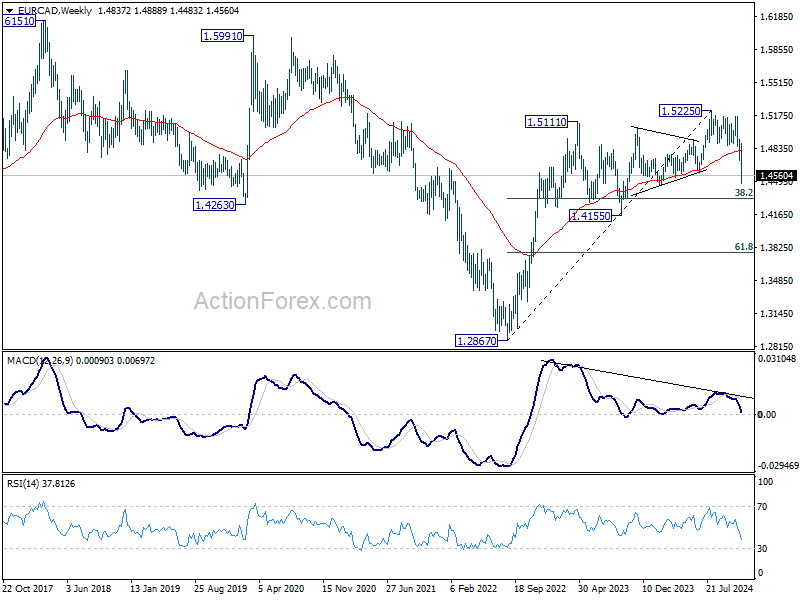

EUR/CAD's fall from 1.5225 accelerated lower last week and broke through 1.4592 support decisively. Considering bearish divergence condition in W MACD, 1.5225 is at least a medium term top. Further decline is expected as long as 1.4710 support turned resistance holds. Next target is 38.2% retracement of 1.2867 (2022 low) to 1.5225 at 1.4324. Sustained break there will indicate medium term bearish reversal and target 61.8% retracement at 1.3768 next.

EUR/AUD's decline from 1.7180 tried to resume through 1.5996/6002 support zone last week. Further fall is expected as long as 1.6161 support turned resistance holds. Considering bearish divergence condition in W MACD, sustained break of 1.5996 will argue that the trend from 1.4281 (2022 low) is reversal. Deeper fall would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388 next.

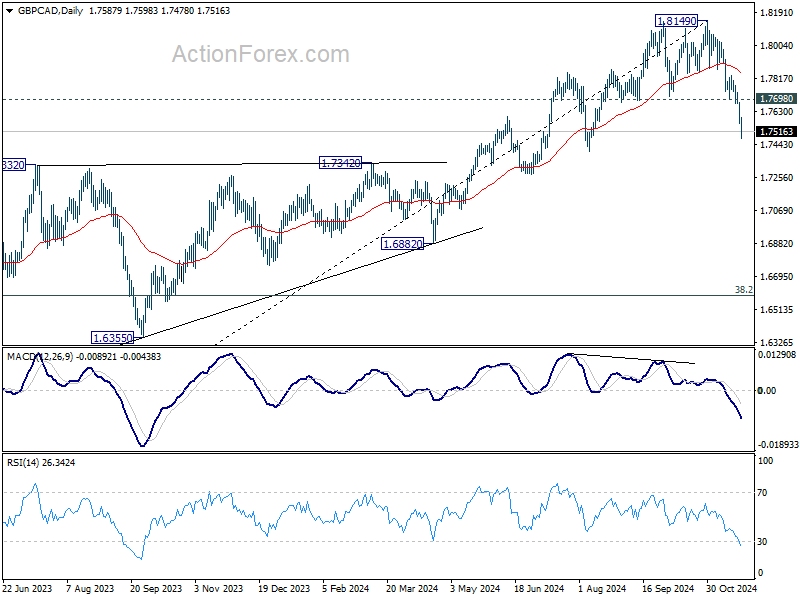

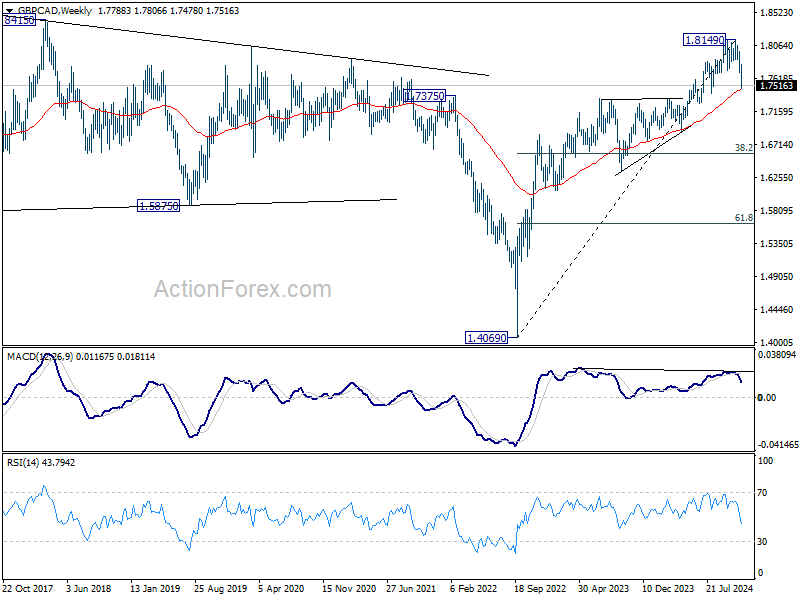

A medium term top should be in place at 1.8149 in GBP/CAD considering bearish divergence condition in D MACD. But it's still early to conclude if the up trend from 1.4069 (2022 low) is reversing. Nonetheless, further decline is expected as long as 1.7698 support turned resistance holds. Sustained trading below 55 W EMA (now at 1.7454) will pave the way to 38.2% retracement of 1.4069 to 1.8149 at 1.6590.

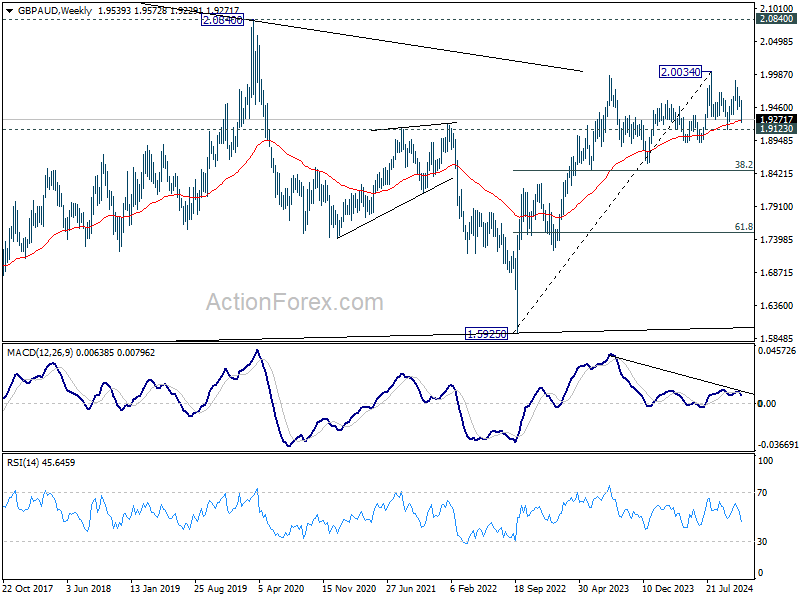

GBP/AUD's outlook is less clear. Bearish divergence in W MACD suggests medium term topping at 2.0045. But firm break below 1.9123 support is needed to confirm. In this case, deeper fall would be seen to 38.2% retracement of 1.5925 to 2.0034 at 1.8464 as a correction. Nevertheless, strong rebound from 1.9123 will keep outlook bullish for another rise through 2.0034 at a later stage.

Resilient US Economy Propels Equities, Dollar Index Surges on Weak Euro

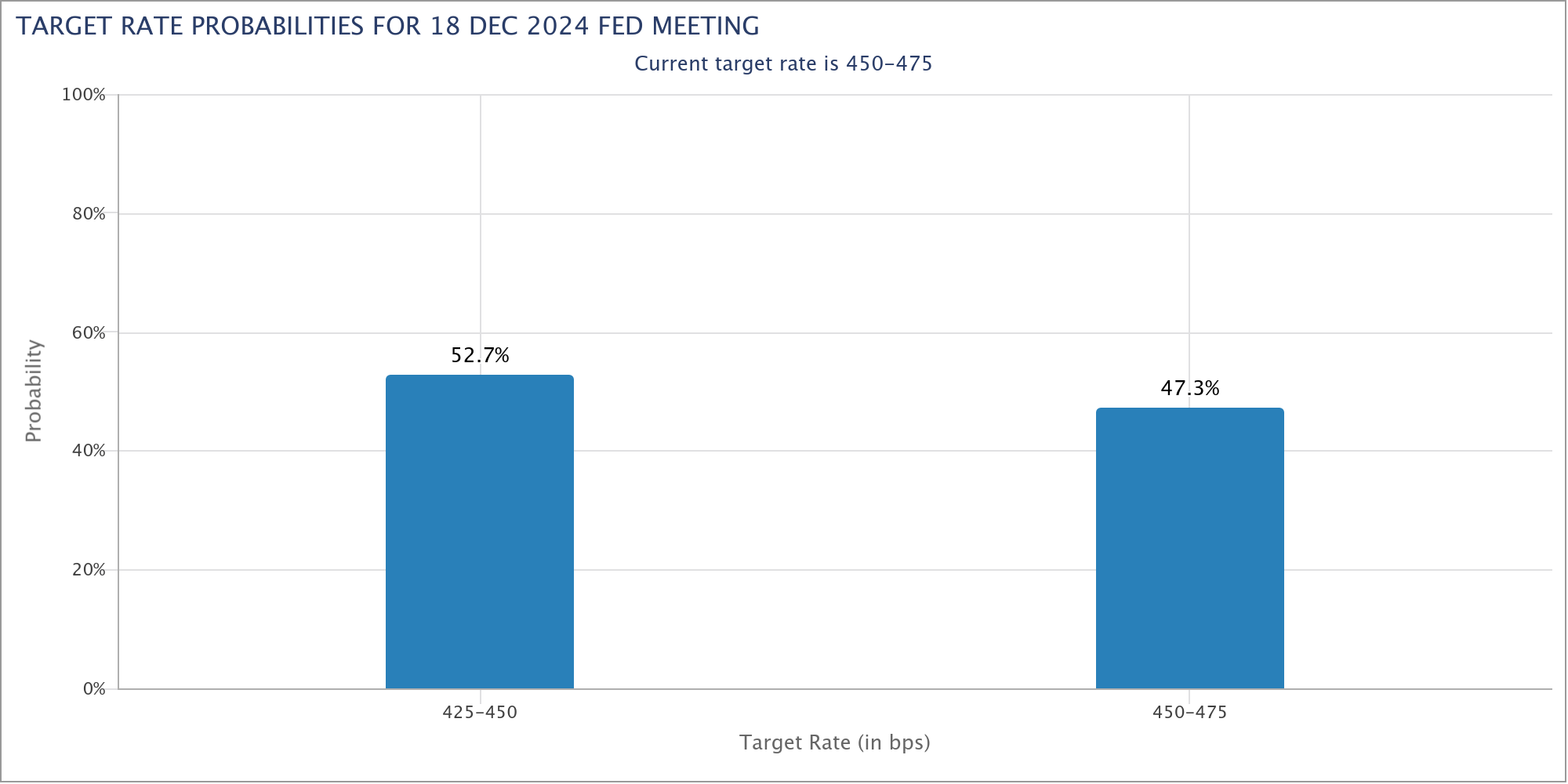

In the US markets, investors displayed renewed optimism as they cheered robust economic indicators, particularly the encouraging PMI data with services sector stood out with a significant performance boost. Market participants seemed unfazed with diminishing likelihood of aggressive Fed rate cuts. Fed funds futures now indicate only a 52.7% probability of a rate cut in December, suggesting that traders believe Fed might even consider pausing rate adjustments. The upcoming US employment data, set to be released in two weeks, will be crucial.

Technically, DOW's strong rebound last week suggests that pull back from 44486.70 has completed at 42938.70 already. Break of 44486.70 will resume larger up trend to 100% projection of 32327.20 to 39889.05 from 38000.96 at 45562.81 next.

10 year yield continued to struggle around 4.45 mark, facing strong resistance from medium term falling trend line, as well as 61.8% retracement of 4.997 to 3.603 at 4.464. However, there is no clear sign of a reversal for now. Further rise is in favor as long as 4.264 support holds. Sustained break of 4.464 will strengthen the bullish case that whole correction from 4.997 has completed with three waves down to 3.603. Further rally should then be seen to 4.737 and then 4.997.

Dollar Index surged further to 108.07 last week and breached 100% projection of 99.57 to 107.34 from 100.15 at 107.92 before closing slightly lower at 107.55. Surprisingly, that was neither driven by risk-off sentiment nor rally in US yields, but the deep selloff in Euro.

Immediate focus in now on whether Dollar Index could sustain above 107.92 with conviction. In this case, that would strengthen the case that pullback from 114.77 (2022 high) as completed after getting strong support from 55 M EMA. Further rally should then be seen to 161.8% projection at 112.72 next.

Nevertheless, rejection by 107.92, followed by break of 106.11 support, will keep medium term outlook neutral first.

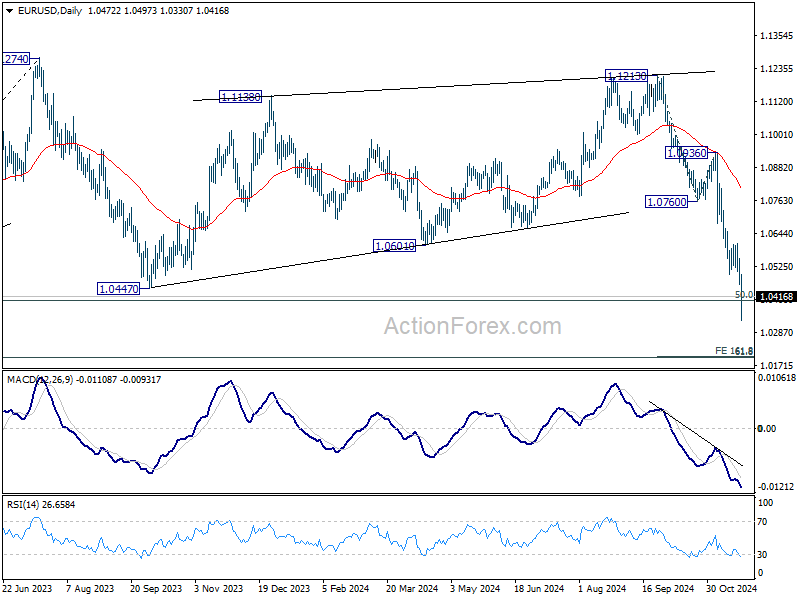

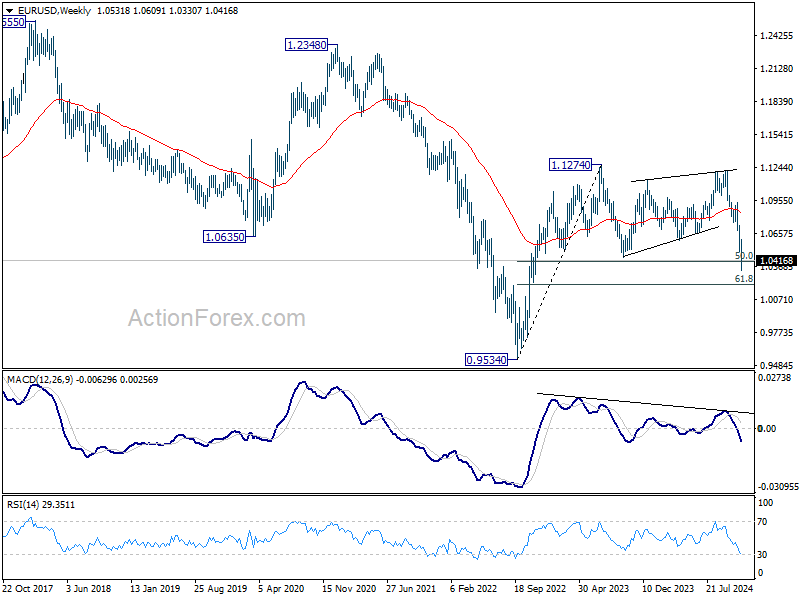

EUR/USD Weekly Outlook

EUR/USD's decline from 1.1213 continued last week and accelerated to as low as 1.0330. There is no sign of bottoming yet and initial bias stays on the downside this week. Sustained trading below 1.0404 key fibonacci level will carry larger bearish implication and target next level at 161.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0203. Nevertheless, strong rebound from current level, followed by break of 1.0609 resistance, will indicate short term bottoming.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0991). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds. downside breakout would be mildly in favor.

Summary 11/25 – 11/29

Monday, Nov 25, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q3 | -0.50% | -1.20% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | -0.30% | -1.00% |

| 21:45 | NZD | Trade Balance (NZD) Oct | -1760M | -2108M |

| 09:00 | EUR | Germany IFO Business Climate Nov | 86 | 86.5 |

| 09:00 | EUR | Germany IFO Current Assessment Nov | 85.5 | 85.7 |

| 09:00 | EUR | Germany IFO Expectations Nov | 87.3 | 87.3 |

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 2.50% | 2.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q3 | |

| Forecast: -0.50% | Previous: -1.20% | ||

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | |

| Forecast: -0.30% | Previous: -1.00% | ||

| 21:45 | NZD | Trade Balance (NZD) Oct | |

| Forecast: -1760M | Previous: -2108M | ||

| 09:00 | EUR | Germany IFO Business Climate Nov | |

| Forecast: 86 | Previous: 86.5 | ||

| 09:00 | EUR | Germany IFO Current Assessment Nov | |

| Forecast: 85.5 | Previous: 85.7 | ||

| 09:00 | EUR | Germany IFO Expectations Nov | |

| Forecast: 87.3 | Previous: 87.3 | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | |

| Forecast: 2.50% | Previous: 2.60% | ||

Tuesday, Nov 26, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Sep | 5.10% | 5.20% |

| 14:00 | USD | Housing Price Index M/M Sep | 0.30% | 0.30% |

| 15:00 | USD | Consumer Confidence Nov | 112 | 108.7 |

| 15:00 | USD | New Home Sales Oct | 724K | 738K |

| GMT | Ccy | Events | |

|---|---|---|---|

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Sep | |

| Forecast: 5.10% | Previous: 5.20% | ||

| 14:00 | USD | Housing Price Index M/M Sep | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 15:00 | USD | Consumer Confidence Nov | |

| Forecast: 112 | Previous: 108.7 | ||

| 15:00 | USD | New Home Sales Oct | |

| Forecast: 724K | Previous: 738K | ||

Wednesday, Nov 27 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Oct | 2.50% | 2.10% |

| 01:00 | NZD | RBNZ Rate Decision | 4.25% | 4.75% |

| 02:00 | NZD | RBNZ Press Conference | ||

| 07:00 | EUR | Germany GfK Consumer Confidence Dec | -18.8 | -18.3 |

| 09:00 | CHF | UBS Economic Expectations Nov | -7.7 | |

| 13:30 | USD | GDP Annualized Q3 P | 2.80% | 2.80% |

| 13:30 | USD | GDP Price Index Q3 P | 1.80% | 1.80% |

| 13:30 | USD | Initial Jobless Claims (Nov 22) | 220K | 213K |

| 13:30 | USD | Goods Trade Balance (USD) Oct P | -101.6B | -108.2B |

| 13:30 | USD | Wholesale Inventories Oct P | -0.10% | -0.20% |

| 13:30 | USD | Durable Goods Orders Oct | 0.40% | -0.70% |

| 13:30 | USD | Durable Goods Orders ex Transport Oct | 0.20% | 0.50% |

| 13:30 | USD | Personal Income M/M Oct | 0.30% | 0.30% |

| 13:30 | USD | Personal Spending Oct | 0.40% | 0.50% |

| 13:30 | USD | PCE Price Index M/M Oct | 0.20% | 0.20% |

| 13:30 | USD | PCE Price Index Y/Y Oct | 2.10% | |

| 13:30 | USD | Core PCE Price Index M/M Oct | 0.30% | 0.30% |

| 13:30 | USD | Core PCE Price Index Y/Y Oct | 2.70% | |

| 14:45 | USD | Chicago PMI Nov | 44.9 | 41.6 |

| 15:00 | USD | Pending Home Sales M/M Oct | -1.70% | 7.40% |

| 15:30 | USD | Crude Oil Inventories | 0.5M | |

| 17:00 | USD | Natural Gas Storage | -3B | |

| 19:00 | USD | FOMC Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Oct | |

| Forecast: 2.50% | Previous: 2.10% | ||

| 01:00 | NZD | RBNZ Rate Decision | |

| Forecast: 4.25% | Previous: 4.75% | ||

| 02:00 | NZD | RBNZ Press Conference | |

| Forecast: | Previous: | ||

| 07:00 | EUR | Germany GfK Consumer Confidence Dec | |

| Forecast: -18.8 | Previous: -18.3 | ||

| 09:00 | CHF | UBS Economic Expectations Nov | |

| Forecast: | Previous: -7.7 | ||

| 13:30 | USD | GDP Annualized Q3 P | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 13:30 | USD | GDP Price Index Q3 P | |

| Forecast: 1.80% | Previous: 1.80% | ||

| 13:30 | USD | Initial Jobless Claims (Nov 22) | |

| Forecast: 220K | Previous: 213K | ||

| 13:30 | USD | Goods Trade Balance (USD) Oct P | |

| Forecast: -101.6B | Previous: -108.2B | ||

| 13:30 | USD | Wholesale Inventories Oct P | |

| Forecast: -0.10% | Previous: -0.20% | ||

| 13:30 | USD | Durable Goods Orders Oct | |

| Forecast: 0.40% | Previous: -0.70% | ||

| 13:30 | USD | Durable Goods Orders ex Transport Oct | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 13:30 | USD | Personal Income M/M Oct | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | Personal Spending Oct | |

| Forecast: 0.40% | Previous: 0.50% | ||

| 13:30 | USD | PCE Price Index M/M Oct | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:30 | USD | PCE Price Index Y/Y Oct | |

| Forecast: | Previous: 2.10% | ||

| 13:30 | USD | Core PCE Price Index M/M Oct | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Oct | |

| Forecast: | Previous: 2.70% | ||

| 14:45 | USD | Chicago PMI Nov | |

| Forecast: 44.9 | Previous: 41.6 | ||

| 15:00 | USD | Pending Home Sales M/M Oct | |

| Forecast: -1.70% | Previous: 7.40% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 0.5M | ||

| 17:00 | USD | Natural Gas Storage | |

| Forecast: | Previous: -3B | ||

| 19:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

Thursday, Nov 28, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Nov | 65.7 | |

| 00:30 | AUD | Private Capital Expenditure Q3 | 1.10% | -2.20% |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | 3.30% | 3.20% |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Nov | 95.6 | |

| 10:00 | EUR | Eurozone Industrial Confidence Nov | -13 | |

| 10:00 | EUR | Eurozone Services Sentiment Nov | 7.1 | |

| 13:00 | EUR | Germany CPI M/M Nov P | -0.20% | 0.40% |

| 13:00 | EUR | Germany CPI Y/Y Nov P | 2% | |

| 13:30 | CAD | Current Account (CAD) Q3 | -8.6B | -8.5B |

| 23:30 | JPY | Tokyo CPI Y/Y Nov | 1.80% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | 2.10% | 1.80% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Nov | 1.80% | |

| 23:50 | JPY | Industrial Production M/M Oct P | 3.90% | 1.60% |

| 23:50 | JPY | Retail Trade Y/Y Oct | 2.10% | 0.70% |

| 23:30 | JPY | Unemployment Rate Oct | 2.50% | 2.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Nov | |

| Forecast: | Previous: 65.7 | ||

| 00:30 | AUD | Private Capital Expenditure Q3 | |

| Forecast: 1.10% | Previous: -2.20% | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | |

| Forecast: 3.30% | Previous: 3.20% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Nov | |

| Forecast: | Previous: 95.6 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Nov | |

| Forecast: | Previous: -13 | ||

| 10:00 | EUR | Eurozone Services Sentiment Nov | |

| Forecast: | Previous: 7.1 | ||

| 13:00 | EUR | Germany CPI M/M Nov P | |

| Forecast: -0.20% | Previous: 0.40% | ||

| 13:00 | EUR | Germany CPI Y/Y Nov P | |

| Forecast: | Previous: 2% | ||

| 13:30 | CAD | Current Account (CAD) Q3 | |

| Forecast: -8.6B | Previous: -8.5B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Nov | |

| Forecast: | Previous: 1.80% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | |

| Forecast: 2.10% | Previous: 1.80% | ||

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Nov | |

| Forecast: | Previous: 1.80% | ||

| 23:50 | JPY | Industrial Production M/M Oct P | |

| Forecast: 3.90% | Previous: 1.60% | ||

| 23:50 | JPY | Retail Trade Y/Y Oct | |

| Forecast: 2.10% | Previous: 0.70% | ||

| 23:30 | JPY | Unemployment Rate Oct | |

| Forecast: 2.50% | Previous: 2.40% | ||

Friday, Nov 29, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Private Sector Credit M/M Oct | 0.50% | 0.50% |

| 05:00 | JPY | Housing Starts Y/Y Oct | -2.00% | -0.60% |

| 05:00 | JPY | Consumer Confidence Nov | 36.4 | 36.2 |

| 07:00 | EUR | Germany Import Price Index M/M Oct | 0.20% | -0.40% |

| 07:00 | EUR | Germany Retail Sales M/M Oct | -0.50% | 1.20% |

| 07:45 | EUR | France GDP Q/Q Q3 | 0.40% | 0.40% |

| 08:00 | CHF | GDP Q/Q Q3 | 0.40% | 0.70% |

| 08:55 | EUR | Germany Unemployment Rate Nov | 6.10% | |

| 08:55 | EUR | Germany Unemployment Change Nov | 27K | |

| 09:30 | GBP | Mortgage Approvals Oct | 65K | 66K |

| 09:30 | GBP | M4 Money Supply M/M Oct | 0.40% | 0.60% |

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | 2.30% | 2.00% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov P | 2.80% | 2.70% |

| 13:30 | CAD | GDP M/M Sep | 0.30% | 0.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Private Sector Credit M/M Oct | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 05:00 | JPY | Housing Starts Y/Y Oct | |

| Forecast: -2.00% | Previous: -0.60% | ||

| 05:00 | JPY | Consumer Confidence Nov | |

| Forecast: 36.4 | Previous: 36.2 | ||

| 07:00 | EUR | Germany Import Price Index M/M Oct | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 07:00 | EUR | Germany Retail Sales M/M Oct | |

| Forecast: -0.50% | Previous: 1.20% | ||

| 07:45 | EUR | France GDP Q/Q Q3 | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 08:00 | CHF | GDP Q/Q Q3 | |

| Forecast: 0.40% | Previous: 0.70% | ||

| 08:55 | EUR | Germany Unemployment Rate Nov | |

| Forecast: | Previous: 6.10% | ||

| 08:55 | EUR | Germany Unemployment Change Nov | |

| Forecast: | Previous: 27K | ||

| 09:30 | GBP | Mortgage Approvals Oct | |

| Forecast: 65K | Previous: 66K | ||

| 09:30 | GBP | M4 Money Supply M/M Oct | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | |

| Forecast: 2.30% | Previous: 2.00% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov P | |

| Forecast: 2.80% | Previous: 2.70% | ||

| 13:30 | CAD | GDP M/M Sep | |

| Forecast: 0.30% | Previous: 0.00% | ||

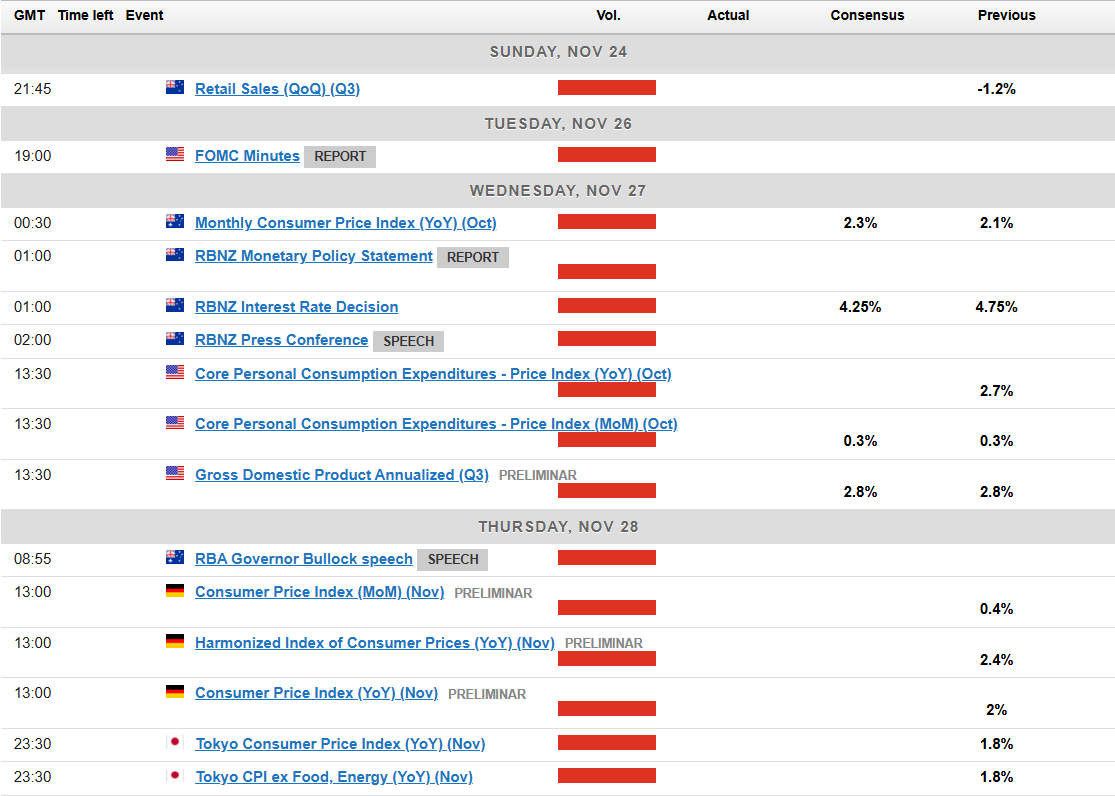

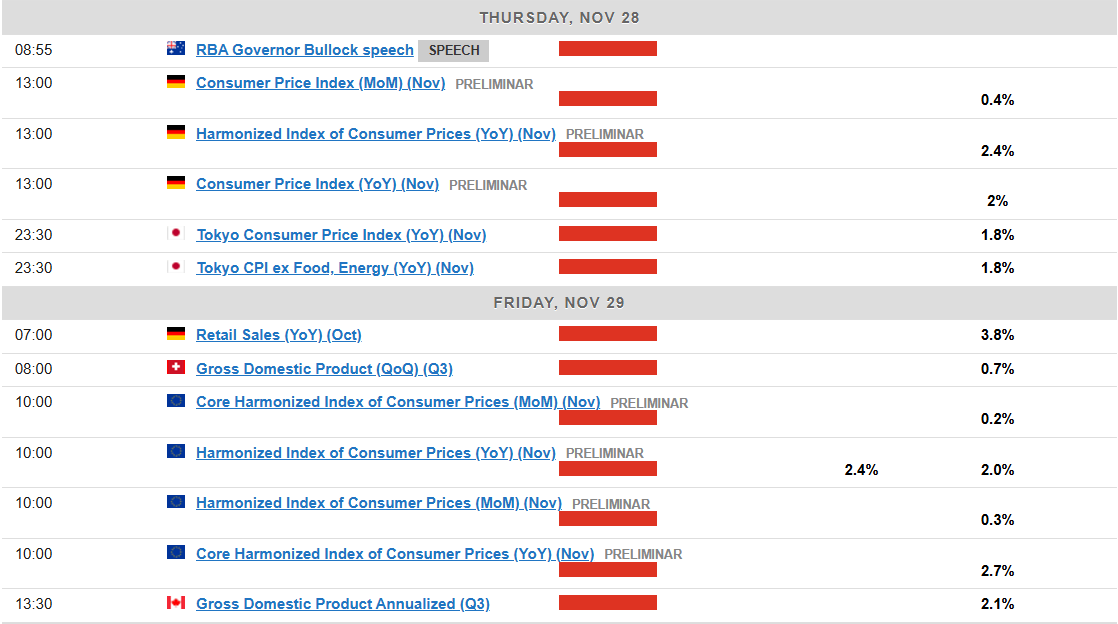

Markets Weekly Outlook – Inflation Data & Geopolitics to Dominate

- Weak PMI data from Europe and the UK raise concerns about global economic outlook and sent the EUR and GBP tumbling.

- Escalating tensions in Russia-Ukraine and the Middle East add to market uncertainty.

- Upcoming PCE inflation data will influence Fed policy and market sentiment.

Week in Review: DXY Continues Advance, as EU and UK Growth Struggles Continue

Europe and the UK are the biggest losers this week both from a geopolitical risk and economic data perspective. Poor PMI data across the Euro Area and more importantly its major industrial hub Germany, have left the Euro reeling against G7 counterparts.

The UK is starting to face a similar change as stagnant growth, stubborn services inflation and a host of budgetary concerns have left the British Pound in a spot of bother. The data this week has seen market participants increase their rate cut expectation over the next 12 months. GBP/USD is trading at six month lows with more losses possible if markets continue pricing in more aggressive rate cuts moving forward.

Gold (XAU/USD) has been on a tear this week and is on course for its best week in twelve months. The rally largely driven by rising geopolitical risk looks set to continue and follows an investment note by Goldman Sachs, in which analysts predicted the precious metal will set a new record by the end of 2025.

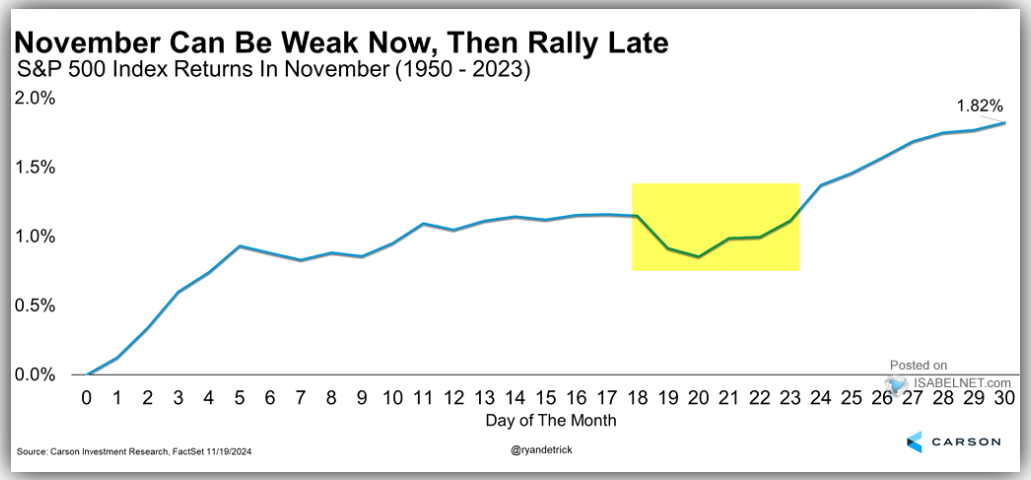

US Indices recovered with a modicum of caution this week with the blockbuster release of NVIDIA earnings now out of the way. The market reaction was rather mixed to NVIDIAS (NVDA) earnings with the share enjoying some whipsaw price action since the earnings release. This concludes the earnings release from the ‘magnificent 7’ with attention now shifting to other areas as the festive season approaches.

The S&P 500 and Nasdaq 100 rose 1.4% and 1.6% respectively. Now, there is something that caught my eyes recently and it was the historical performance of US stocks in the month of November. Historically US stocks experience a strong month of November with the last week of the month experiencing a significant rise. This usually carries on in December in what is affectionately called the ‘santa rally’. WIll history repeat itself?

Source: Isabelnet, Carson Research (click to enlarge)

Geopolitical risk is back in focus and is likely to remain so reading into the end of the year. Keep an eye on the evolving situations in both the Middle East and Russia-Ukraine. Any escalation is likely to lead to some wild price swings in the weeks ahead.

The Week Ahead: Muted Week in APAC, PMI Data Rules

Asia Pacific Markets

The week ahead in the Asia Pacific region sees an uptick in economic data releases.

In China, a quiet week is expected with the main event on the docket being the medium-term lending rate. The People’s Bank of China (PBoC) is expected to keep the medium-term lending rate steady at 2.0% when it announces its decision on Monday. On Wednesday, attention will shift to industrial profits data, as investors look for signs of improvement after two months of steep declines compared to last year.

In Japan, labor market data will be in focus this week. The job market is still strong, so the unemployment rate is likely to stay about the same as last month. Production and retail sales are expected to do well, as issues like earthquake warnings and safety scandals are no longer affecting activity.

In Australia, markets focus will shift to the inflation data. Australia’s economy is expected to grow slightly in October. The job market remains strong, and prices for services are still rising. However, overall inflation is likely to stay within the 2-3% target range.

Europe + UK + US

In developed markets, inflation data takes center stage next week coupled with geopolitical risks as the Russia Ukraine conflict heats up.

In the Euro Area, inflation data will be released on Friday and will be a key release after the poor PMI data released this past week. Inflation is expected to rise further, mainly due to comparisons with low figures from last year.

Market participants began to see some hope for the Euro Area in recent weeks but the PMI data release and geopolitical cloud will no doubt have serious repercussions moving forward. At the October press conference, Christine Lagarde gave a gloomy economic outlook which may have been seen as pessimistic at the time. I still expect inflation to drop in the coming months which should help but if growth remains subdued the ECB may have to be more aggressive with rate cuts moving forward.

Another key release next week will be the release of the Euro Areas economic sentiment survey, which will provide more details on how businesses feel about the current economy, their pricing strategies, and hiring plans.

In the UK, there is a pause on high impact economic data releases. The PMI data from the UK sent the Pound tumbling last Friday. For now, rate cut expectations have increased from 72 bps to 77 bps of cuts through December 2025.

The US awaits the Feds Preferred inflation gauge next week with the PCE release as market participants are expecting an uptick in inflationary pressure in the coming months. Following a hot CPI and PPI print this month, the PCE release will be even more intriguing.

The PCE measure combines data from both the CPI and PPI reports, and current data suggests a 0.3% month-on-month increase. For inflation to settle at the Fed’s 2% annual target, monthly increases need to average around 0.17%, so 0.3% is still too high for the Fed to feel fully comfortable.

However jobs data still is the key at the moment. When it comes to the Federal Reserve December meeting, the jobs data on December 6 is likely to still hold the key.

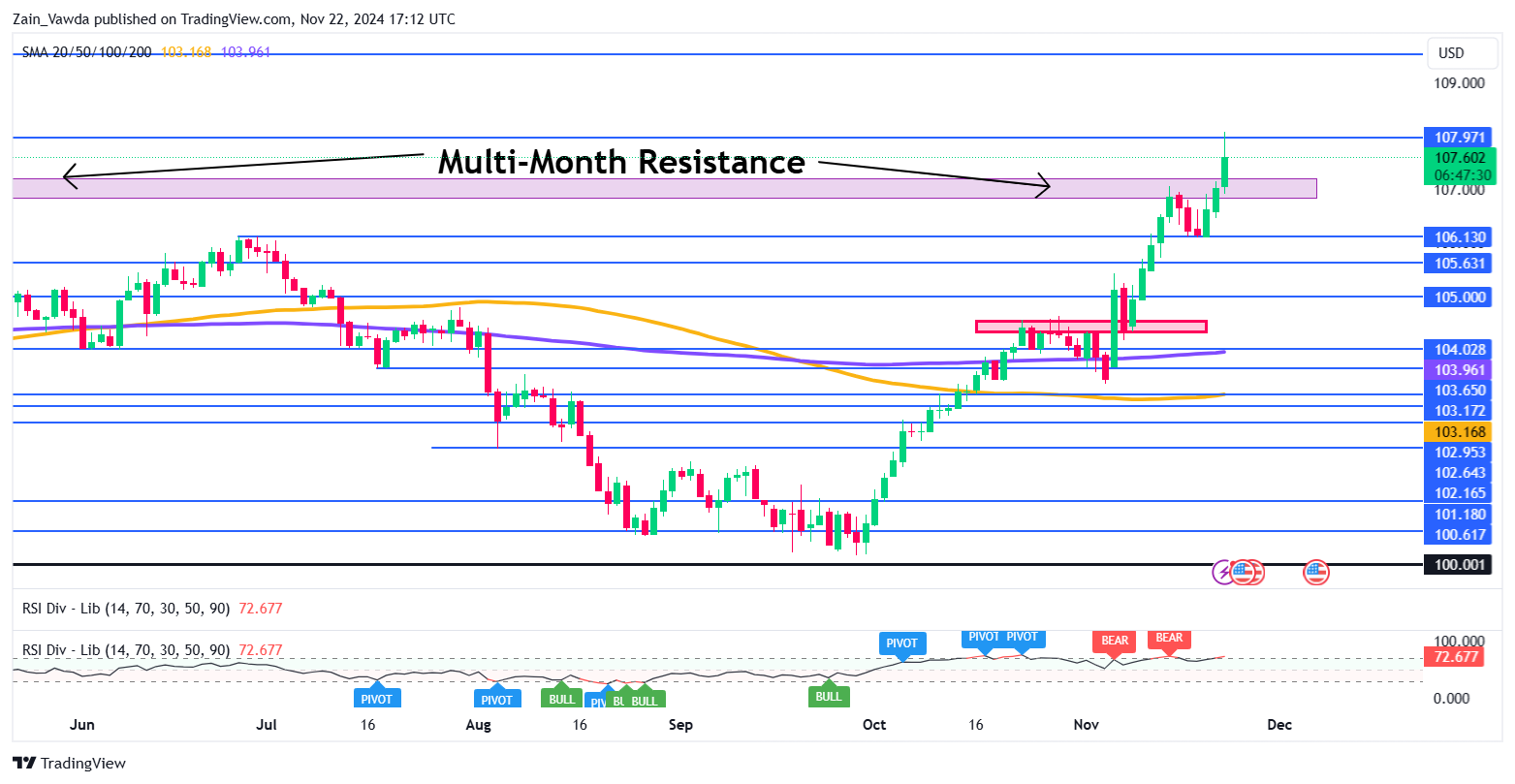

Chart of the Week

This week’s focus remains the US Dollar Index (DXY), which has taken out a key multi-month resistance level at the 107.00 handle rising to a high of around 108.00 before a pullback.

The DXY rally seems unstoppable at present with rising geopolitical risk also underpinning the greenback. The DXY is back in overbought territory on the daily chart below based on the 14 period RSI. However this is of course no guarantee that a drop will materialize but it is worth paying attention to.

Given the geopolitical dynamics at play and the optimism around a Trump return to the White House the potential for a drop in the DXY remains slim. Any pullbacks are likely to be met with buying pressure and thus capping the downside potential. A significantly lower PCE print than expected may help weaken the DXY, but whether such a move would be a sustainable remains up to debate.

Looking at immediate support and the purple block on the chart below around the 107.00 handle is key if bulls are to continue the recent rally. Below the 107.00 handle support rests at 106.130 and 105.63.

Looking at the upside and immediate resistance rests at the 108.00 handle with 109.00 and the 110.00 psychological level next in line.

US Dollar Index Daily Chart – November 21, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 105.63

- 105.00

- 104.50

Resistance

- 107.00

- 107.97

- 109.52

The Weekly Bottom Line: Inflation Can’t ‘Shake it Off’

Canadian Highlights

- Canadian inflation made headlines this week, with both overall and core inflation pushing higher in October.

- The Canadian consumer was also in the spotlight as retail sales surged and the Federal government announced big stimulus measures to further support spending.

- Rising inflation and stronger consumer spending have raised odds that the BoC will revert to a 25 bp cut when it meets in December.

U.S. Highlights

- A quiet week for data with the housing market showing healthy sales activity and Fed speakers recommitting to a data-dependent approach to policy.

- The focus will be on housing inflation in next week’s Personal Income and Outlays report for October.

- Productivity growth has allowed inflation to cool without sacrificing much growth. Whether that continues through the end of 2024 and into 2025 will be material for Fed policy.

Canada – Inflation Can’t ‘Shake it Off’

Taylor Swift may still be in Toronto, but it was the steady stream of economic data that dominated headlines this week. Canadian Consumer Price Index (CPI) inflation was supposed to be the star with a big upwards move in October (Chart 1), but the Federal government’s large pre-election stimulus to support consumer spending took center stage. Retail sales data for September also came in hot, showing that Canadian consumers may have entered a new ‘Era’ of elevated spending. Housing starts data also showed strength in October, likely reacting to the revival happening in the resale market. Financial markets responded by pricing a greater likelihood that the Bank of Canada (BoC) will revert to cutting by 25 bps at its December meeting.

A more gradual pace of interest rate cuts is consistent with October’s inflation data, which was a bit hotter than expected, bouncing back to target after a soft reading in September. And it wasn’t just higher gasoline prices behind the increase. The BoC’s core inflation measures also rose two tenths to 2.6% y/y on average, above the 2.5% mark the Bank had flagged in the past as behind the reason they were comfortable making a larger 50 basis point cut. This reminded markets that the BoC is not ‘Out of the Woods’ when it comes to controlling inflation.

Stronger consumer demand may be the source of rising inflation. After a long period of cautious spending, consumers are feeling ‘22’ again. It looks like the effect of lower rates is finally starting to raise sentiment. Retail sales data released Friday confirmed this, with a near 1% monthly jump in September and the advanced estimate for October showing more of the same. And this isn’t even including the rampant spending seen in Toronto over the last two weeks, where a flood of Swifties descended on the city to scoop up $100 shirts and T-Swift themed cocktails at local bars. The Federal government’s huge pre-election stimulus is likely to extend this spending spree through the first half of 2025, as the HST break and a round of $250 cheques will pull spending forward and boost overall GDP growth.

A stronger Canadian consumer also means that housing is back in ‘Style’. Lower rates have sparked the housing market, with resale activity and prices showing renewed strength ever since the BoC cut by 50 bps in October. This has parleyed into improved builder confidence, as housing starts data showed an impressive 8% monthly increase in October. This implies that residential investment should start being a positive contributor to Canadian GDP growth following three years of this sector dragging down growth.

If there was one T-Swift song that would characterize what the BoC should do, it’s: ‘You Need to Calm Down’ - with the pace of rate cuts that is. Everyone remembers the central bank electing to cut by an oversized 50 bps back in October. At the time, we made our own headlines by saying how this wasn’t needed and that it risked sparking the real estate market. This was the right advice, as the bank is looking increasingly likely to revert to its prior pace of 25 bps cuts. This may make it the ‘Anti-hero’ for those hoping for a Swifter pace of cuts, but it is likely the best course of action given the state of the economy.

U.S. – Looking Ahead After a Quiet Week

A brief rally in Treasuries fizzled out this week and, at the time of writing, Treasury yields are roughly back to where they were at Monday’s open. Ultimately, a pair of housing reports coming in roughly in line with expectations and two Fed speakers emphasizing data dependence, leave us looking to next week’s Personal Income and Outlays report as the next sign-post to gauge where the Fed’s rate cutting campaign is headed.

Two Fed Board Members took the stage this week – Governor’s Bowman and Cook. Though they offered slightly different interpretations of the state of the economy both recommitted to a data-dependent approach to rate setting. Governor Cook presented her view of the outlook, with an emphasis that the disinflation process is well on its way “even if the path is occasionally bumpy”. Governor Bowman was more pessimistic noting that, “progress on inflation seems to have stalled”. Markets now expect the Fed’s preferred inflation gauge (the personal consumption expenditure index excluding food and energy) to show another strong advanced in October of 0.3% month-on-month (m/m, 3.7% annualized) – well ahead of the Fed’s 2.0% target. Whether it’s a bump or another sign of stalling will come down to the details of the report.

The good news is that the growth in most goods and services prices has moderated significantly (Chart 1). Goods price trends have been a key part of the recent cooling with prices in both durables and nondurables in deflation over the past several months. There is some worry this benefit could be coming to an end as there was a notable uptick in durable goods prices last month (+0.3% m/m). With retail sales demand still healthy, another price gain can’t be ruled out. Adding to the concern is the prospect that tariffs are around the corner. For policymakers, the end of the downdraft from durable goods prices would come at an inopportune time as it has provided a meaningful deflationary offset to a still-hot housing sector.

This puts more focus on what kind of print we can expect in the coming months from the housing market. Sales activity clocked in a healthy gain last month amid lower mortgage rates in late summer. However, this is likely to be a temporary burst as affordability is still stretched, and the recent backup in borrowing costs should dent demand (Chart 2). With inventory levels near balanced territory, this should help temper further price gains.

To date, U.S. consumers have benefited from a productivity boom that has allowed inflation to cool without sacrificing much growth. The key concern now is whether this pace of productivity growth can extend into next year. This means looking at the details in the data for signs that demand growth is yet again outpacing supply. Markets currently judge the odds of a Fed cut in December at a coin toss. An upside surprise next week could make it a long-shot.

Weekly Economic & Financial Commentary: How Much Will the Fed Cut Rates?

United States: Back-up in Mortgage Rates a Setback for Housing

- The residential sector was in focus this week. The late summer dip in mortgage rates led to an upside surprise in existing home sales. Recent hurricanes weighed on housing starts in October. An upturn in the NAHB HMI shows builders are not put off by the rebound in financing costs and generally are encouraged by the election results.

- Next week: Durable Goods (Wed.), Personal Income & Spending (Wed.)

International: European Sentiment Slumps While Global Inflation Pressures Linger

- Sentiment surveys worsened in both the Eurozone and United Kingdom in November, supporting the view that the 2025 growth prospects for Europe could be more challenging in the wake of the U.S. presidential election. Against that backdrop we expect continued monetary easing from foreign central banks next year, though this week's price and wage data from the U.K., Canada and the Eurozone suggest a steady rather than accelerated pace of rate cuts.

- Next week: RBNZ Policy Rate (Wed.), Eurozone CPI (Fri.), Canada GDP (Fri.)

Interest Rate Watch: How Much Will the Fed Cut Rates?

- Strong economic data, recent comments by Fed officials and the potential of higher inflation in 2025 due to tariff increases have led market participants to dial back their expectations of Fed rate cuts in coming months.

Topic of the Week: Aye, There's the (Turkey) Rub

- Price growth at grocery stores has eased considerably since spiking at over 13% in the summer of 2022. Thanksgiving of that year, many families faced inflation for Turkey Day staples well into double digits with the price for the star of the meal—the turkey—up 16.9% from a year prior. Still, even amid dramatic declines in the rate of price growth, it is difficult to imagine swaths of Americans declaring “This year, I’m grateful for food disinflation” around their tables next Thursday.

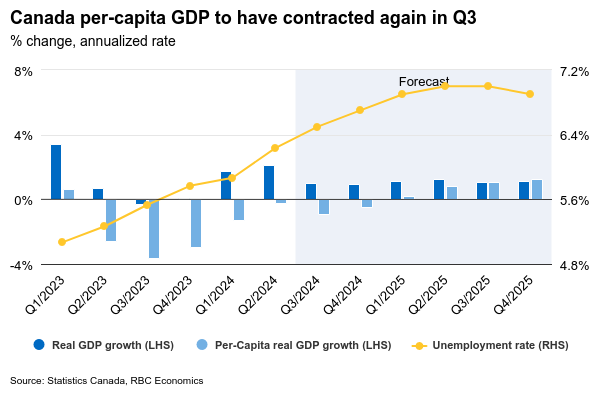

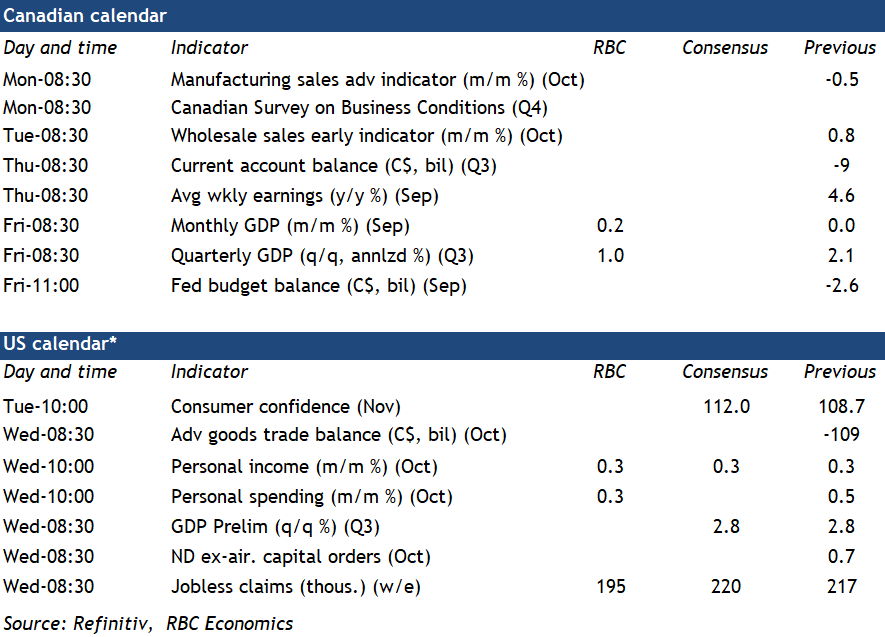

September data to show Canadian GDP growth halved in Q3

We look for gross domestic product growth in Canada to have picked up slightly to 0.2% in September on Friday after holding steady in August. That should leave the Q3 reading in line with our projection for a 1% annualized increase—slightly below the Bank of Canada’s 1.5% forecast and less than half the 2.1% rise in Q2.

Consumer spending likely increased in Q3 given a 5% (annualized rate) rise in retail sales, but a pullback in equipment imports is flagging a drop in business investment after a surprisingly large Q2 increase. A small pick-up in home resales in August and September likely drove residential investment higher in Q3, the first increase in four quarters.

The 0.2% increase we expect in September GDP is lower than Statistics Canada’s 0.3% advance estimate, with the rise partly due to the rail transportation bounce-back after disruptions in August. Wholesale and retail sale volumes rose in September, but manufacturing output likely contracted again, while hours worked fell 0.4% in September.

More importantly, the increase in Q3 GDP won’t prevent another contraction in real per-person activity, extending that downward trend for a sixth consecutive quarter. The soft growth backdrop and broadly easing inflation pressures are the main reasons our own base-case projections look for another 50 basis point rate cut from the Bank of Canada in December.

September’s GDP report will also include annual benchmark revisions with early estimates already suggesting that the level of GDP in 2023 was 1.3% higher than previously estimated. However, that is unlikely to change the broader trajectory for per-capita output, which has been persistently lower and consistent with a rising unemployment rate and slowing inflation pressures.

Week ahead data watch

We expect U.S. personal spending to grow by 0.3% in October, down from the 0.5% in the prior month. Retail sales came in at 0.4% during that month, also grew at a slower pace than in September.

U.S. Personal income likely rose 0.3% in October. Disruptions from hurricanes and a large strike in the manufacturing sector paused job growth in October (+12k), but wages rose.

Job openings in the Canadian September SEPH data will be watched closely for signs of further softening in the labour market. Job openings have been declining, and we continue to expect wage growth to slow.

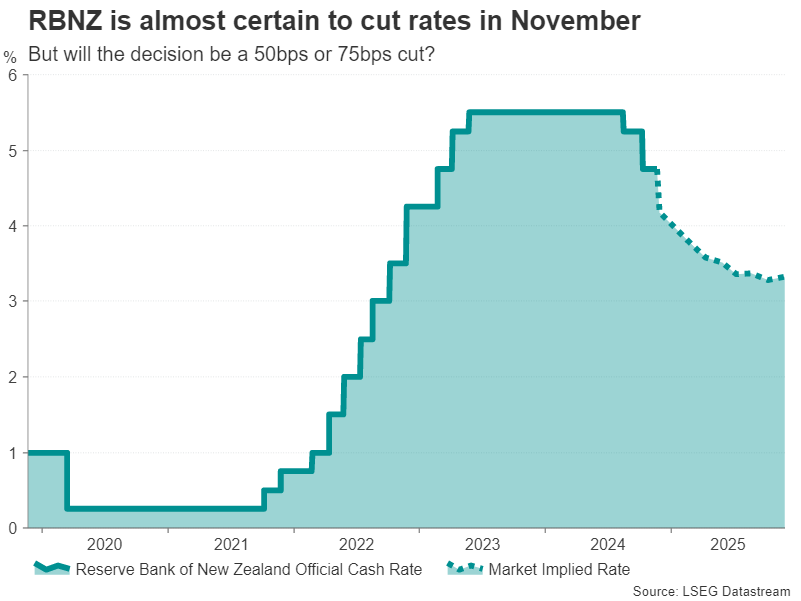

Week Ahead – RBNZ to Slash Rates Ahead of US and Eurozone Inflation Data

- RBNZ is expected to cut rates by 50 bps at its last policy meeting of 2024

- But will PCE inflation data give the green light for a Fed cut?

- Eurozone flash CPI also critical for ECB’s December decision

RBNZ set for third rate cut

The Reserve Bank of New Zealand will kick-start the end of year policy meetings of the major central banks when it announces its decision on Wednesday. Having stood out as being ultra-hawkish during the global tightening cycle, the RBNZ performed a major policy reversal over the summer by embarking on a loosening campaign even before the Fed had started its own.

With the annual rate of CPI falling within its 1-3% target band, inflation expectations settling around 2.0% and GDP growth remaining sluggish, policymakers have little reason to be cautious and a back-to-back 50-basis point cut is fully priced in. There is even speculation that the RBNZ might opt for a triple reduction of 75 basis points, which can be justified by the fact that, after November, policymakers won’t meet again until February.

Should the RBNZ surprise with a hefty cut, it will be difficult for the New Zealand dollar to regain its footing against the US dollar, and it could tumble to fresh 2024 lows.

Storm of US data before Thanksgiving break

The US economic agenda will get back into full gear next week as a flurry of releases are on the way before traders abandon their desks for the Thanksgiving holiday. Politics briefly eclipsed monetary policy after Donald Trump’s shock election win. But the focus is primarily back on the Fed now amid growing doubts about how many times the US central bank will be able to cut rates even before the incoming administration’s inflationary policies have seen the light of day.

Expectations of a 25-bps reduction in December currently stand at between 60% and 55% as Fed officials have turned more hawkish after a string of upbeat indicators on the economy, but more importantly, after the decline in underlying inflation stalled again.

Fed Char Powell has joined the FOMC’s hawkish camp, flagging the possibility of a pause. Hence, the likelihood of a cut will depend on how strong or weak the next inflation and jobs reports are before the December meeting.

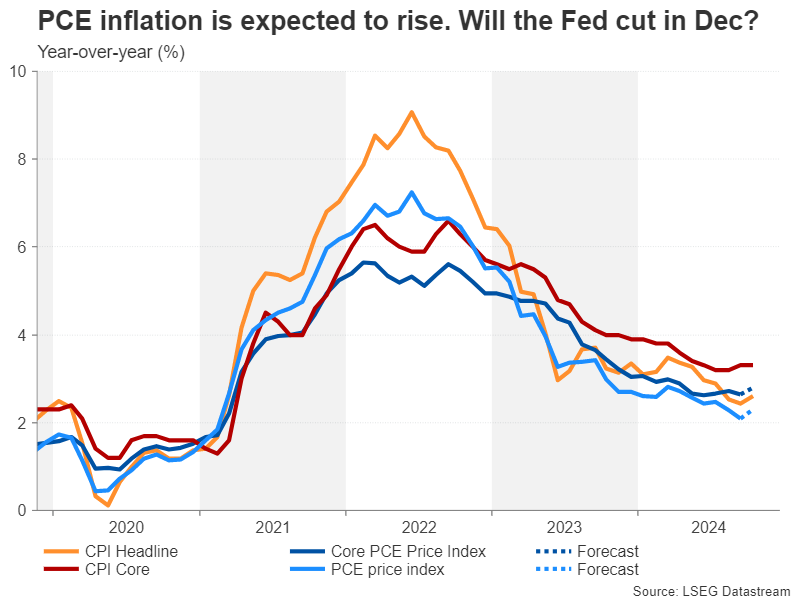

The PCE inflation report, out on Wednesday, is up first on the schedule. Powell recently said he sees core PCE edging up from 2.7% to 2.8% in October, which would mark a setback for the Fed. The projection for headline PCE is a pickup from 2.1% to 2.3%.

Both the headline measures of PCE and CPI inflation have maintained a clearer downward path than the core readings, and if the incoming numbers do not throw this trend into question, the Fed might still have some manoeuvrability to trim rates in December.

Fed minutes also in the spotlight

Should the PCE price indices fail to shed any light on the Fed’s next move, investors will look to the minutes of the Fed’s November policy meeting due the same day for fresh policy insight. There will also be plenty of other data to sift through on Wednesday. Personal income and consumption will be quite important, followed by durable goods orders for October and the second estimate of Q3 GDP growth.

A day earlier, new home sales and the Conference Board’s consumer confidence gauge are likely to attract some attention too. US markets will be shut on Thursday for Thanksgiving Day and the stock market will close early on Friday, which means there will only be light trading. Nevertheless, those choosing not to make a weekend of it will have the Chicago PMI to keep them entertained.

The US dollar has been extending its post-election rally over the past week. But its gains are now looking overstretched. Any disappointing data therefore risks triggering a sharp correction.

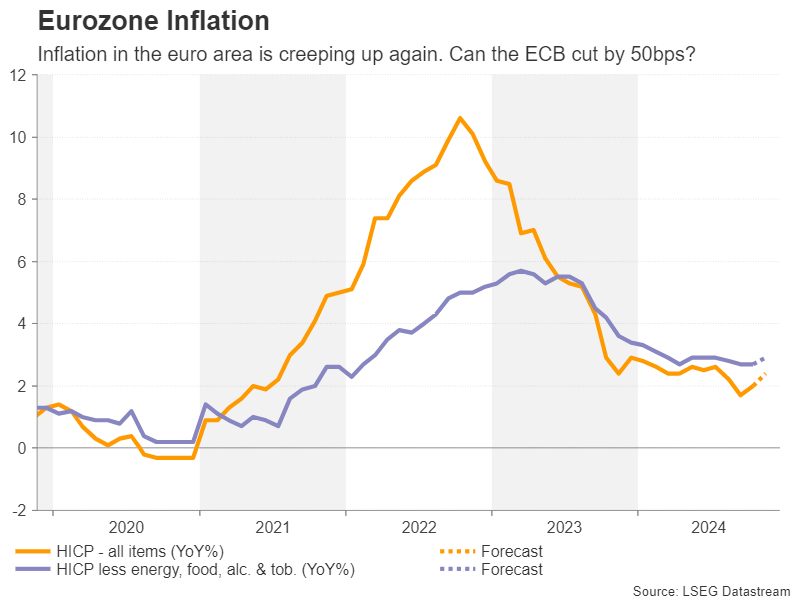

Eurozone CPI eyed for ECB clues

Despite rising pessimism about the European growth outlook, ECB policymakers have been pushing back on investor expectations of a 50-bps rate cut in December. The recent jump in negotiated wages – a key metric for the ECB – and services inflation continuing to hover around 4% underline policymakers’ concerns about cutting too fast.

Markets have assigned about a 25% probability for a 50-bps move in December, which may be overstating the true odds if the latest ECB rhetoric is to be believed. This implies there’s quite a mountain to climb to push the chances for a 50-bps cut substantially higher.

Nevertheless, Friday’s flash CPI figures will be watched closely. In October, headline CPI accelerated from 1.7% to 2.0%. A further increase to 2.4% is forecast for November, which could dash hopes for a larger cut even more, potentially helping the euro to stop the recent bleeding against the greenback.

Ahead of the CPI numbers, Monday’s Ifo business survey out of Germany will be on investors’ radar amid worries about how the political uncertainty in the country is affecting business confidence.

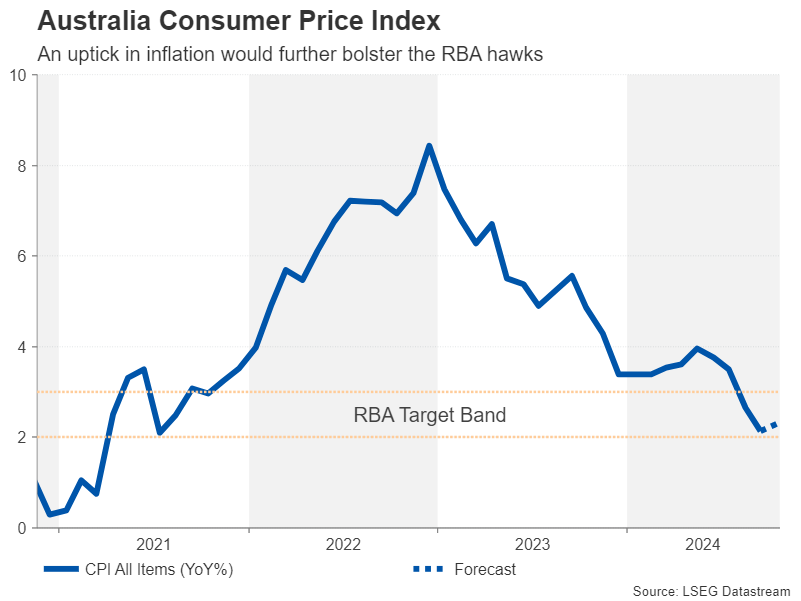

Will CPI data worsen the aussie’s pain?

In Australia, the latest CPI stats will also be doing the rounds. The monthly readings for October are due on Wednesday, while on Thursday, Q3 capital expenditure data will be monitored. Annual inflation fell to 2.1% in September, which is at the lower end of the RBA’s 2-3% target band. Yet, the RBA is not ready to start taking its foot off the brake, and investors don’t foresee a rate cut before May 2025 at the earliest.

If CPI edges up to 2.3% in October as expected, there might be some support for the Australian dollar versus its stronger US counterpart.

Loonie turns attention to Canadian GDP

Another currency struggling to keep its head above water is the Canadian dollar. The Bank of Canada has been more aggressive than other central banks in slashing rates, and this explains why the loonie is the third worst performing major currency this year.

A fifth consecutive rate cut is likely in December but bets for a second 50-bps cut faded after the recent hotter-than-expected CPI report. Friday’s Q3 GDP print will probably not be a game changer for the BoC, but there could still be a sizeable reaction in the loonie from any big surprises.

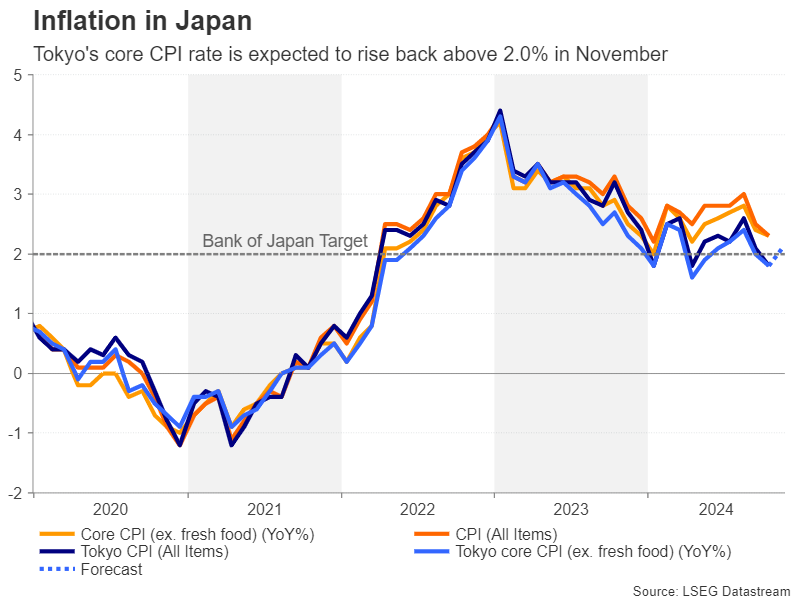

Tokyo inflation on tap

Adding to Friday’s data barrage are the Tokyo CPI figures for November. Inflation in Tokyo fell below the Bank of Japan’s 2.0% target in October, but this hasn’t dissuaded policymakers from wanting to raise interest rates further. The question now is more about the timing. With investors split 50-50 about the possibility of a rate increase in December, stronger-than-forecast numbers could bolster bets for a year-end hike, lifting the yen.