Sample Category Title

Trump Trade in Full Swing

We’re on the cusp of the US election results. They’re starting to trickle in, pointing toward a more favourable outcome for the Republicans and Donald Trump. As a result, the so-called ‘Trump trade’ is in full swing this morning.

The US yields are pushing higher on expectation of further debt ballooning under a Donald Trump presidency. Bitcoin hit a fresh record. In the traditional currency markets, the US dollar is rallying against most majors this morning. The euro – which is one of the most vulnerable major currencies to Trump presidency due to the tariff threat – tanked to 1.0718 against the greenback. Mexican peso – which is another currency highly vulnerable to a Trump win – is down by 3%. The Chinese yuan is weaker. Cable slipped below 1.29, the USDJPY extended gains to the highest levels since summer and even the safe-haven assets like Swiss franc and gold are weaker this morning against a broadly stronger US dollar.

In equities, the divergence is clear. The major US index futures are in the positive territory, with the Dow Jones futures leading gains. FTSE futures are flat, whereas the DAX and Eurostoxx futures are clearly not smiling. Bloomberg Economics tried to put numbers on the damage that Trump tariffs would cause to the world and the numbers are scary. China’s exports to the US could melt by more than 80%, according to them, assuming a 60% tariffs relative to the baseline of no new tariffs. Australian exports to the US could melt by more than 50%, the British and EU exports could tank by more than 40%. And these numbers would be worse if the trade partners decide to retaliate.

Elsewhere

Yesterday’s data showed that the French industrial production fell more sharply than expected in September, while activity in Britain expanded stronger-than-expected, but that the 10-yer gilt auction didn’t go well. The 10-year gilt yield extended its advance to the highest levels in a year, as a rising warning that the British government’s plans to boost growth by boosting spending won’t come cheap. Deterioration in Britain’s growth outlook is negative for sterling. But the fact that the Bank of England (BoE) will remain careful when easing policy could limit sterling’s downside potential – if the growth prospects don’t worsen significantly.

Chips under Trump

Palantir rallied more than 23% to an ATH yesterday, after the company announced a record profit on AI demand and raised its earnings forecast. Nvidia jumped 3% on AI-positive news, and Invesco’s semiconductor ETF gained 2.80%.

One relevant question is: what will happen to semiconductors under Trump?

The Chips Act that has been brought on the table during the Biden administration is a bipartisan act. Therefore, the present incentives should remain unchanged under Trump. Tax cuts and increased defense spending could be additional positive factors for the US chipmakers. But on the other hand, worsening trade relations and escalation of chip war with China could dampen the chipmakers’ sales and profits.

Earnings and Oil

Saudi’s Aramco is the last oil giant reporting weak earnings last quarter. Aramco’s profit shrank by 15% in Q3 compared to a year ago - due to weak oil prices – but the company kept its monstruous dividend of $31 billion unchanged, because the Saudi government owns nearly all Aramco and needs this money to fund its projects. As such, Aramco has to borrow money to pay dividends to the Saudi government at the moment.

You see where I am going, right?

Oil prices have been on a falling trend since a while now. The weak global economy and sluggish Chinese demand, combined with the green transition have taken a toll on global oil demand prospects, while OPEC’s production cuts have been countered by increased production elsewhere. The US for example is pumping like there is no tomorrow (and Trump vows to keep it that way). Under these circumstances, Saudi, which is the backbone of the OPEC policy, will be incresingly tempted to give up on the production cut strategy and adopt a market share focus to increase its revenue by selling more oil with cheap prices. That, to me, could weaken the OPEC-encouraged oil bulls’ hands in the medium run. The barrel of US crude is back below the 50-DMA and preparing to test the $70pb support to the downside, yet again.

Trump in the Lead – House Control Still Up in the Air

In focus today

Today, the US election dominates the spotlight as investors eagerly anticipate the final outcomes. At the time of writing, Trump has secured a victory in North Carolina and Georgia, with attention fixed on the remaining five swing states. Republicans have been called majority winners in Senate, and the sweep now largely depends on the House elections.

This morning, we are hosting two conference calls where we present our instant views on the election results and implications for markets and the economy: Conference call on the implications of the US election for Global and Scandi markets at 8:40 - 9:10 CET and US elections morning call - Macro need-to-knows at 9:15 - 9:30 CET.

In the euro area, the final PMIs for October are released. Additionally in Germany, we will receive data on factory orders for September, providing a hint of what the industrial production data will show on Thursday.

In Sweden, the monthly Swedish inflation expectations survey is published. We do not expect any surprises, but rather confirmation that the more important 5-year horizon remains stable around 2%.

Economic and market news

What happened overnight

In the US, swing state North Carolina and Georgia were called for Trump, boosting his electoral vote tally to 246. Onlookers are closely watching, as the results from the remaining six swing states continue to unfold. At the time of writing, initial tallies show Trump leading in all five, with Harris closely trailing.

Current sentiment (stronger USD, higher yields) is likely to extend into European morning after Trump is expected to win Georgia and North Carolina with larger than anticipated margins. He is also in the lead in Pennsylvania, which is extremely important for both candidates, but finalizing the state's count might take until Wednesday afternoon (European time). Harris still has a path to victory, but she needs to have performed better-than-expected in the election day voting in Pennsylvania, Michigan and Wisconsin. Senate is likely to flip to Republican majority (as expected), but House race remains very uncertain as none of the most competitive seats have been called.

In crypto markets, Bitcoin soared to a new record high just shy of the USD 75,000 mark as Trump draws ahead in the US presidential election. Crypto investors anticipate less regulation and potentially public financial backing in the event of a Trump win.

What happened yesterday

In the US, the presidential election began as voters amassed at the polls to cast their votes in the race split 50-50 between Trump and Harris. The battleground states, Michigan, Wisconsin and Pennsylvania are the most likely tipping points of the election. We think a Republican sweep would provide support for broad USD and lift yields at both short and long ends of the USD curve on the back of rising inflation and debt sustainability concerns. A Harris win and/or a divided Congress could have the opposite effect if fiscal policy stance remains closer to status quo. Trump could hike tariffs even as a 'lame duck', complicating the outlook especially for USD FX.

Coinciding with the election, US stocks climbed as the ISM report on US non-manufacturing sector showed PMI 56.9 in October (cons: 53.8, prior: 54.9). The headline index was driven higher by the employment index recovering sharply, while prices and new orders weakened. Overall, both PMIs and ISM showed gradually moderating business activity and inflation in services sector in October, which should allow the Fed to continue cutting rates a gradual pace over coming meetings.

Equities: US futures are higher, led by small caps. The three major indices in the US, Dow, S&P500, and Nasdaq, are higher by approximately 1%. Please note, these are not outsized moves. The Russell 2000 is up 2.6%. Listening to commentators, the small cap outperformance is surprising given yields on the long end rising by 12bp. However, this aligns with our observations of small caps performing well as Trump gained in polls and yields increased; thus, this should not come as a surprise.

European futures are intriguing; the EURO STOXX 50 is down by approximately 0.5%, while earlier this morning it was marginally higher. The FTSE 100 future is marginally higher. This European underperformance, particularly in common currency, is likely due to heightened concerns about trade wars and tariffs. However, the movements are not outsized, suggesting that reactions to the election outcomes should be measured. Japanese stocks are significantly higher this morning as the yen weakens, with USDJPY at 153, entering what we call intervention territory. Japanese banks are performing exceptionally well, with the Topix bank index up almost 5% at the time of writing.

FI: US Treasury yields rose significantly as the markets expect a Trump victory and a possible Republican sweep as the Republicans have won the Senate. Hence, 10Y Treasury yields are up some 12-13bp this morning: However, several of the key swing states are yet to publish results at the time of writing, but it looks like a Trump victory. The US curve is steepening from the long end.

FX: On this election morning the USD has been the clear outperformer amid the outlook for a new Trump presidency and by extension tariffs and US-first policy. EUR/USD fell sharply below 1.08 but has rebounded over the last hour amid the potential for less expansionary fiscal policy should the Congress end up split. TRY stands out as a clear winner with markets pricing in a more Erdogan-friendly outlook while CAD and to some extent CHF and GBP are among the overperformers in G10 space. At this stage the CNY has kept up remarkably well. Unsurprisingly, the JPY has been a clear underperformer with the rise in yields sending USD/JPY above 153.50 whilst MXN has also come under pressure. Price action in the Scandies has so far been very muted which to some extent likely reflects poor overnight liquidity and bears watching when markets open.

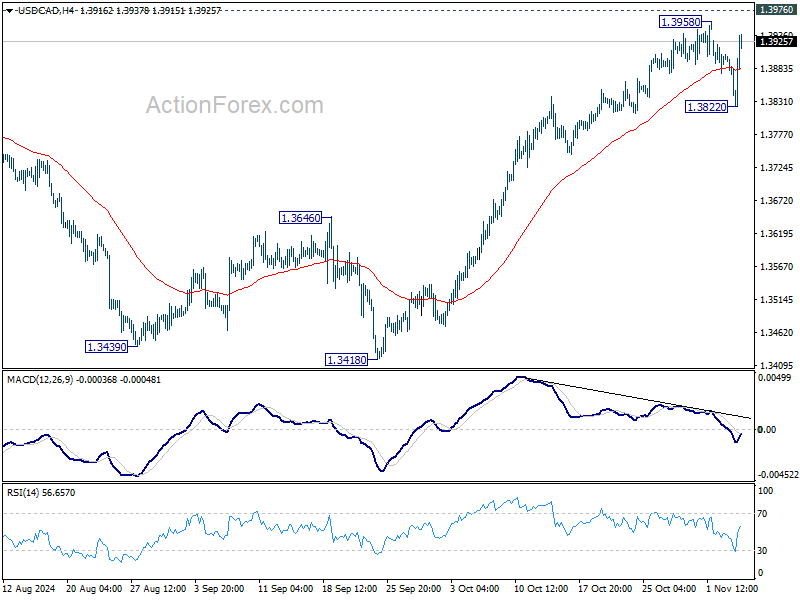

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3796; (P) 1.3851; (R1) 1.3880; More...

USD/CAD rebounded stronger after dipping to 1.3822, but stays below 1.3958. Intraday bias remains neutral first. In case of another fall as consolidation from 1.3958 extends, downside should be contained by 55 D EMA (now at 1.3723). On the upside, decisive break of 1.3976 will resume larger up trend.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

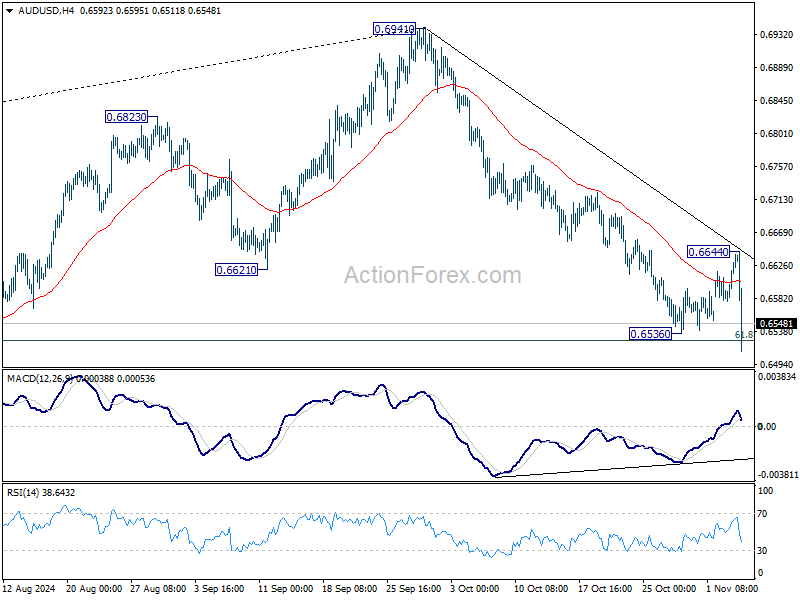

AUD/USD Daily Report

Daily Pivots: (S1) 0.6597; (P) 0.6620; (R1) 0.6660; More...

Intraday in AUD/USD is back on the downside with breach of 0.6536 support. Fall from 0.6941 is resuming and sustained trading below 61.8% retracement of 0.6269 to 0.6941 at 0.6526 will target 0.6348 support next. For now, outlook will stay bearish as long as 0.6644 resistance holds, in case of recovery.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

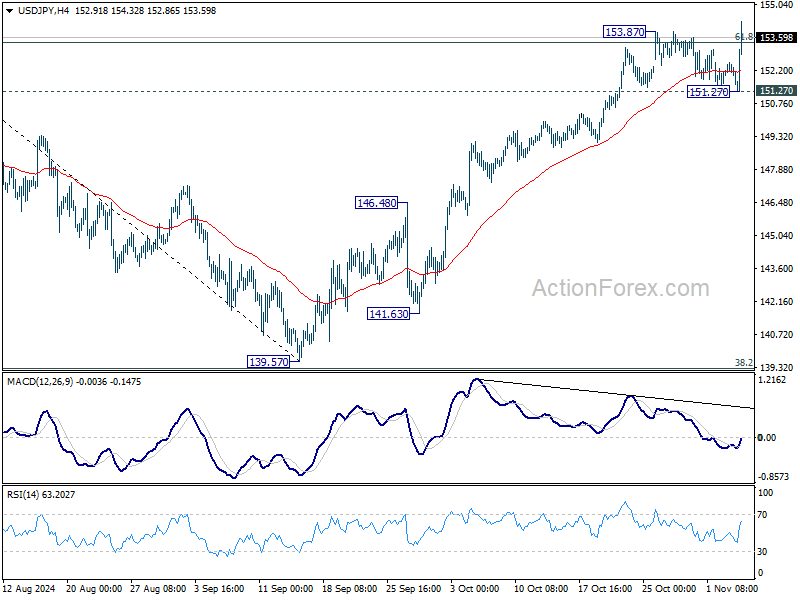

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.12; (P) 151.83; (R1) 152.32; More...

USD/JPY's rally from 139.57 resumed by breaking 153.87 resistance and intraday bias is back on the upside. Sustained trading above of 61.8% retracement of 161.94 to 139.57 at 153.39 will pave the way to retest 161.94 high. For now, outlook will stay bullish as long as 151.27 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

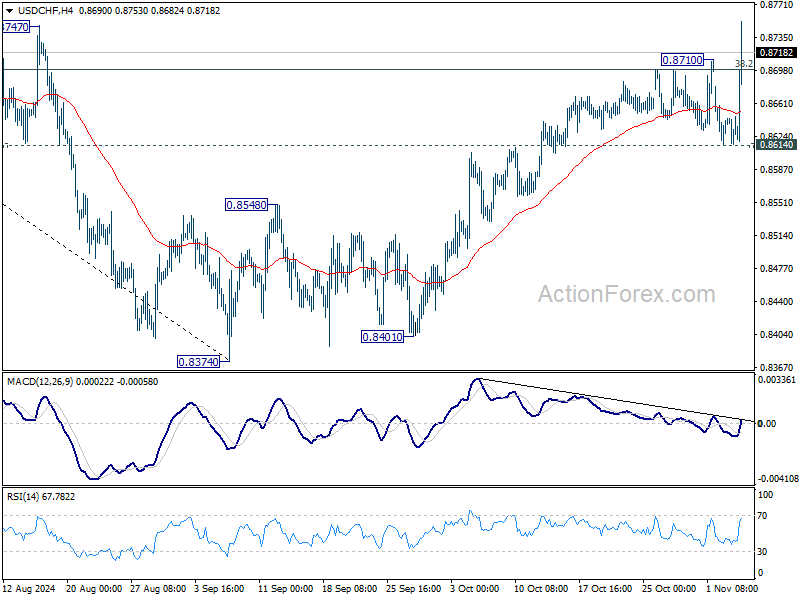

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8616; (P) 0.8632; (R1) 0.8649; More…

USD/CHF's rise from 0.8374 resumed by breaking through 0.8710 and intraday bias is back on the upside. Sustained trading above 0.8710 will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next. For now, near term outlook will stay bullish as long as 0.8614 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

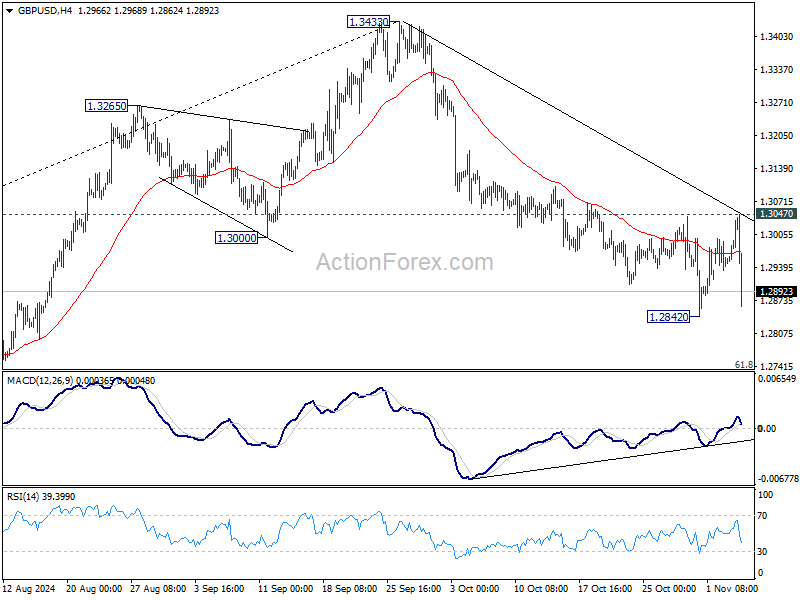

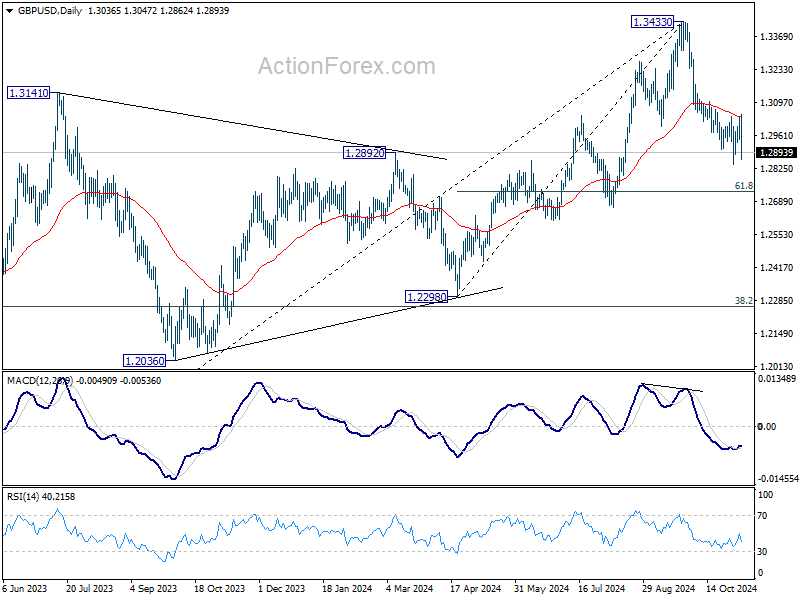

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2979; (P) 1.3011; (R1) 1.3074; More...

GBP/USD falls notably today but stays above 1.2842 temporary low. Intraday bias remains neutral at this point. Further decline is expected as long as 1.3047 resistance holds. Below 1.2842 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bullish convergence condition in 4H MACD, firm break of 1.3047 will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

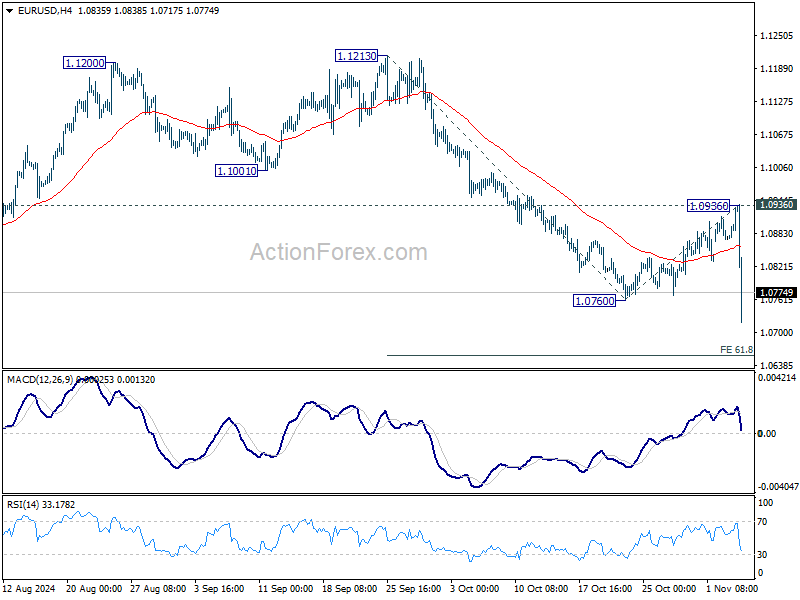

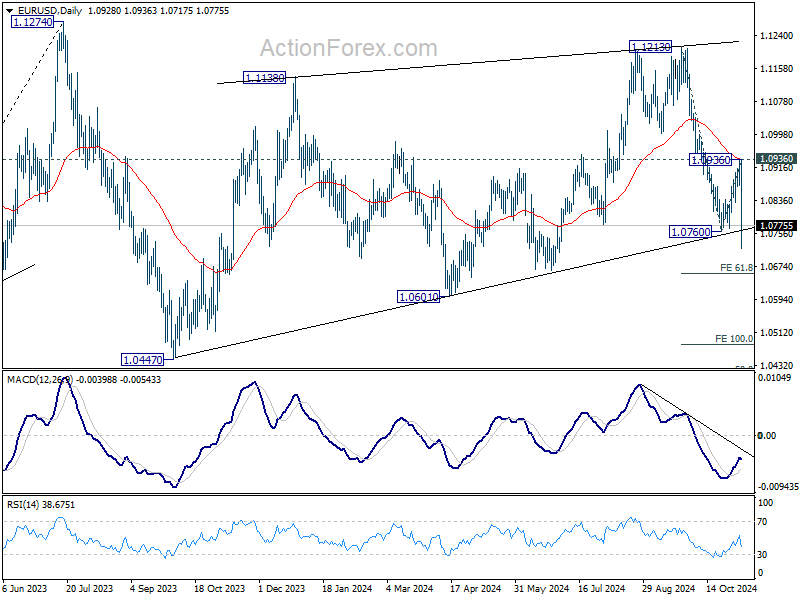

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0890; (P) 1.0913; (R1) 1.0954; More...

EUR/USD's breach of 1.0760 indicates that corrective recovery from there has completed after rejection by 55 D EMA (now at 1.0939), and fall from 1.1213 is resuming. Intraday bias is back on the downside for 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656. Firm break there will pave the way to 100% projection at 1.0483. For now, near term outlook will stay bearish as long as 1.0936 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

Trump’s North Carolina Victory Boosts Dollar and Yields, Bitcoin Hits New High

Dollar rallied sharply today after news broke that Republican candidate Donald Trump defeated Democrat Kamala Harris in North Carolina, a crucial battleground state. This win is considered a pivotal move toward Trump’s return to office, sparking significant moves across financial markets. US stock futures responded with enthusiasm, with DOW futures climbing over 500 points. Meanwhile, 10-year Treasury yield surged above 4.4%, reinforcing the sentiment around Trump’s impact on fiscal policy. Despite this initial surge, traders remain on edge, waiting for further confirmation from key states before taking on new positions.

Asian stock markets offered a mixed picture in response to the news. Japan's Nikkei soared over 2%, driven by positive sentiment linked to a possible Trump victory, as markets see his economic policies as supportive of growth and deregulation. On the other hand, Hong Kong stocks suffered, dropping by more than -2.5% amid concerns over Trump's stance on China, which could bring intensified tensions. In contrast, markets in China and Singapore traded in a narrow range, reflecting uncertainty and caution.

In currency markets, the Australian Dollar is currently the weakest performer, followed by Euro and Yen, pressured by Dollar’s strength. Meanwhile, Canadian Dollar joins Dollar as one of the stronger performers, with Swiss Franc also displaying resilience. New Zealand’s Kiwi is holding steady, seemingly unaffected by recent Q3 employment data, trading alongside the British Pound in mid-range.

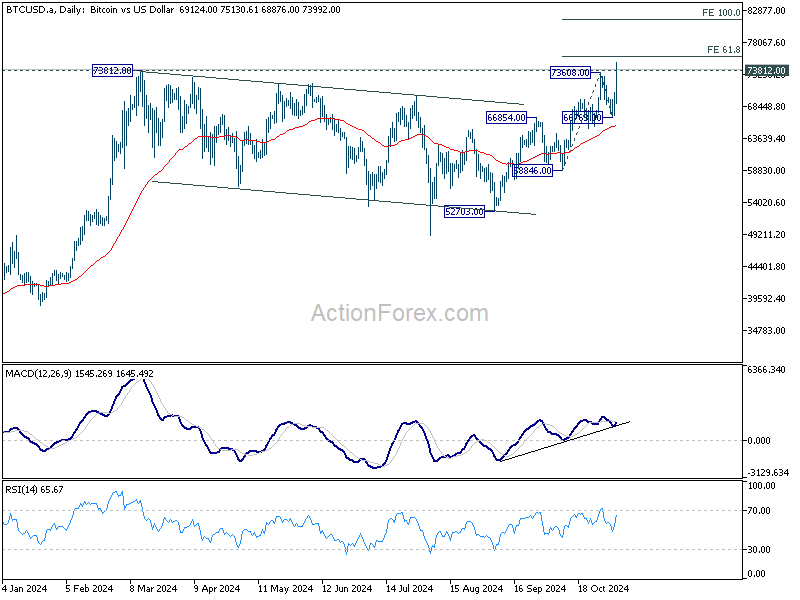

Technically, Bitcoin hits new record high by breaking through 73812 resistance today. Immediate focus is now on 61.8% projection of 58846 to 73608 from 66763 at 75885. Decisive break there could prompt upside acceleration to 100% projection at 81525 rather quickly.

In Asia, at the time of writing, Nikkei is up 2.24%. Hong Kong HSI is down -2.61%. China Shanghai SSE is up 0.16%. Singapore Strait Times is down -0.04%. Japan 10-year JGB yield is up 0.0421 at 0.971. Overnight, DOW rose 1.02%. S&P 500 rose 1.23% .NASDAQ rose 1.43%. 10-year yield fell -0.020 to 4.289.

BoC minutes reveals strong consensus for aggressive rate cut

Summary of BoC Governing Council’s October 23 meeting highlights a decisive stance among members to prioritize growth through an aggressive 50bps rate cut. While members initially discussed the possibility of a modest 25bps cut, a "strong consensus" emerged in favor of a larger reduction to counter economic headwinds.

The Governing Council members expressed "increasingly confident" that inflationary pressures are expected to ease, reducing the need for a restrictive policy stance. Some members voiced concern that an unusual 50bps cut might be perceived as a signal of “economic trouble.” Despite this, they agreed that a more substantial cut was justified, given the "ongoing softness" in the labor market and the need to bolster growth to "absorb excess supply" in the economy.

BoJ minutes: Yen stabilization gives time to monitor global economic risks

Minutes from BoJ's September meeting reveal a careful stance on monetary policy amid global economic uncertainties. At the meeting, BoJ kept its interest rate steady at 0.25%.

Regarding future direction of monetary policy, members broadly agreed that if Japan's economic and inflation outlook aligns with their projections, the Bank would "continue to raise the policy interest rate" and gradually adjust its level of monetary accommodation.

The minutes also underscore the need for "high vigilance" given uncertainties in overseas economies, particularly in the US, and ongoing volatility in global financial markets.

Some members pointed out that recent retracements in Yen’s depreciation have moderated upside risk to inflation from import prices. Given this development, they noted that the Bank has "enough time" to evaluate the effects of global economic shifts and recent policy rate hikes before deciding on further moves.

Japan's PMI services finalized at 49.7, first contraction since Jun

Japan's services sector slipped into contraction in October, with PMI Services index finalized at 49.7, down from September’s 53.1 and marking its first contraction since June. PMI Composite also declined to 49.6 from 52.0, signaling a contraction in private sector activity for the first time in four months and the lowest reading since November 2023.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, the services sector’s performance “came to an abrupt halt” at the start of Q4. While the decline was modest, it was driven by a notable slowdown in new business inflows, particularly in export orders. Despite the dip, businesses maintained a positive outlook, though optimism weakened to its lowest in over two-and-a-half years, with companies citing concerns over labor shortages as a key factor.

The services sector slowdown, combined with a continuing contraction in manufacturing, contributed to the steepest private sector contraction in nearly a year. New order inflows stagnated, particularly impacted by weakened demand in manufacturing order books. Business sentiment, overall, has also softened, with optimism now at its lowest since January 2021.

NZ employment falls -0.5% in Q3, unemployment rate rises to 4.8%

New Zealand’s labor market showed signs of cooling in Q3, with employment falling by -0.5% qoq, in line with expectations. Unemployment rate rose from 4.6 to 4.8%, slightly better than the anticipated 5.0%, but still indicative of softening labor conditions.

Labor force participation rate also declined, dropping from 71.7% to 71.2%, while the employment rate slipped from 68.4% to 67.8%, reflecting fewer people actively engaged in the workforce.

On the wage front, growth showed deceleration. The labor cost index, which includes salary and wage rates with overtime, rose by 3.8% yoy, down from the previous quarter’s 4.3% yoy increase.

The slowdown in wage growth suggests some relief in wage-driven inflation pressures, which could factor into RBNZ's upcoming rate cut.

Looking ahead

Germany factory orders, Eurozone PMI services final and PPI, UK PMI construction will be released in European session. Later in the day, Canada will release Ivey PMI.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0890; (P) 1.0913; (R1) 1.0954; More...

EUR/USD's breach of 1.0760 indicates that corrective recovery from there has completed after rejection by 55 D EMA (now at 1.0939), and fall from 1.1213 is resuming. Intraday bias is back on the downside for 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656. Firm break there will pave the way to 100% projection at 1.0483. For now, near term outlook will stay bearish as long as 1.0936 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

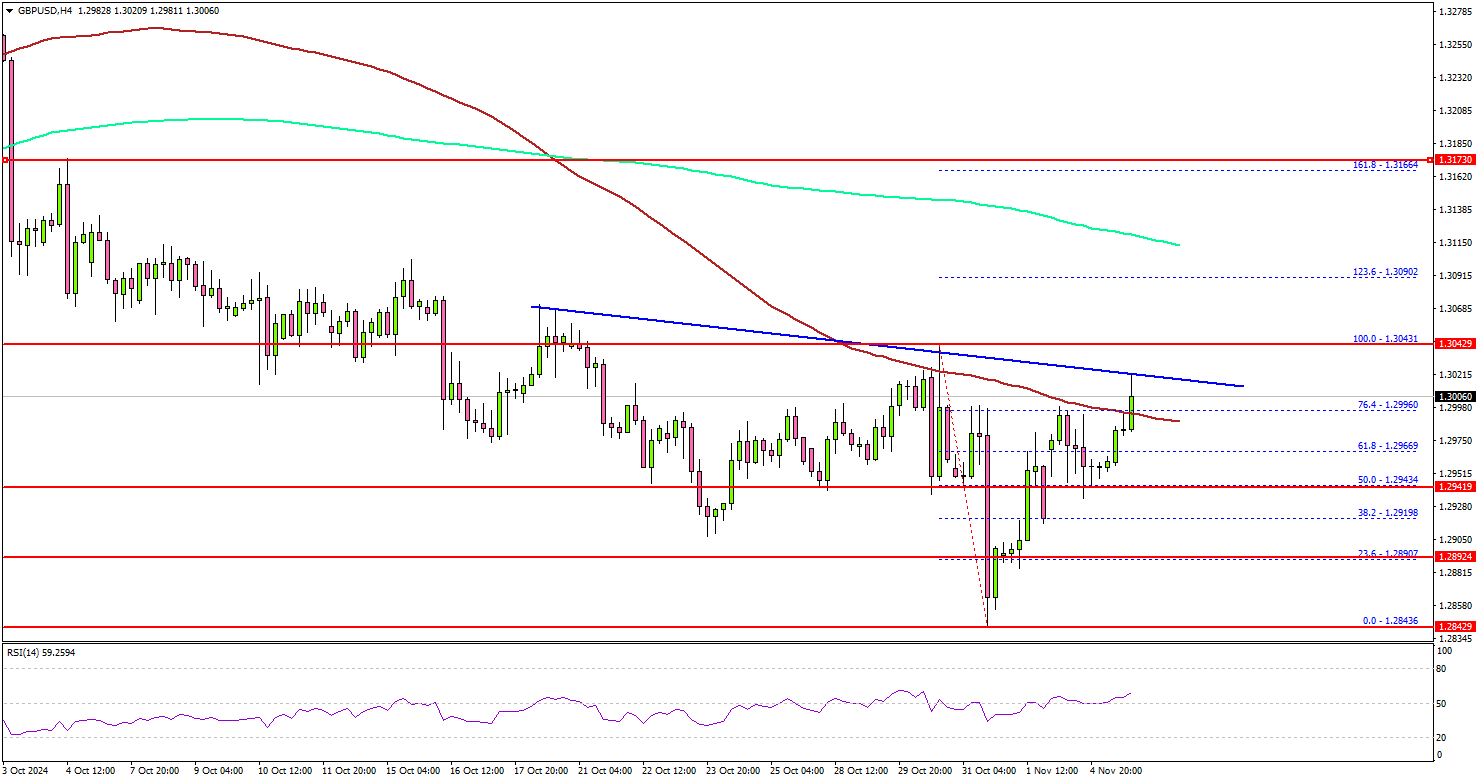

GBP/USD Recovery Potential: Can The Pound Rebound?

Key Highlights

- GBP/USD is attempting to recover from the 1.2840 support zone.

- A connecting bearish trend line is forming with resistance at 1.3020 on the 4-hour chart.

- EUR/USD could gain bullish pace if it clears the 1.0920 resistance.

- Bitcoin bulls aim for a fresh move above the $70,000 resistance.

GBP/USD Technical Analysis

The British Pound started an upside correction from the 1.2840 zone against the US Dollar. GBP/USD climbed above the 1.2880 and 1.2950 resistance levels.

Looking at the 4-hour chart, the pair traded above the 50% Fib retracement level of the downward move from the 1.3043 swing high to the 1.2843 low. However, the pair struggled to settle above the 100 simple moving average (red, 4-hour) and remained well below the 200 simple moving average (green, 4-hour).

On the downside, immediate support sits near the 1.2940 level. The next key support sits near the 1.2890 level. Any more losses could send the pair toward the 1.2840 level.

On the upside, the pair could face resistance near the 1.3020 level. There is also a connecting bearish trend line forming with resistance at 1.3020 on the same chart. The first key resistance is near the 1.3050 level.

A close above the 1.3050 level could set the tone for another increase. The next major resistance could be 1.3120, above which the price could accelerate higher toward the 1.3200 resistance.

Looking at EUR/USD, the pair started a recovery wave and the bulls now aim for a move above the 1.0920 resistance.

Upcoming Economic Events:

- Euro Zone Services PMI for Oct 2024 – Forecast 51.2, versus 51.2 previous.

- UK Services PMI for Oct 2024 – Forecast 56.0, versus 57.2 previous.