Sample Category Title

Weak German PPI Send the Euro Back Down

Market picture

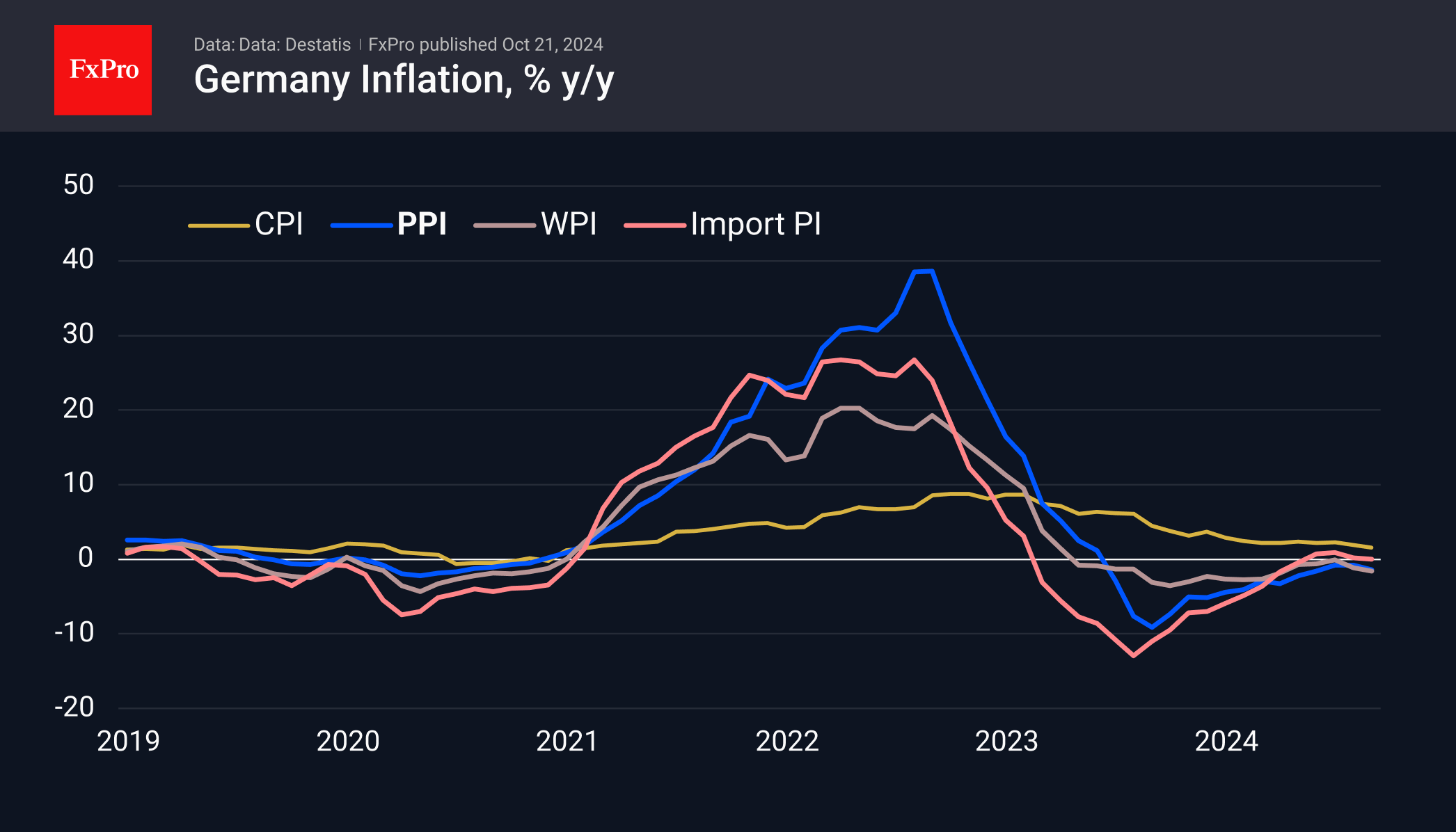

The German Producer Price Index fell more than expected, preventing the EURUSD from extending the rebound seen at the end of last week.

Producer prices in Europe’s largest economy fell 0.5% in September (-0.2% expected), accelerating the annual decline to 1.4% (-0.8% expected) from 0.8% in the previous month. The negative annual growth rate has persisted for the past 15 months, pulling the nominal index back to levels last seen in May 2022.

The weakness in German producer prices puts further active monetary easing in the eurozone back on the agenda. Last week, the ECB cut its key interest rate for the third time this cycle. Soft comments from the bank’s president, Christine Lagarde, sent EURUSD towards 1.08, but a corrective dollar pullback brought the pair back to 1.0870 by early Monday afternoon.

Technical picture

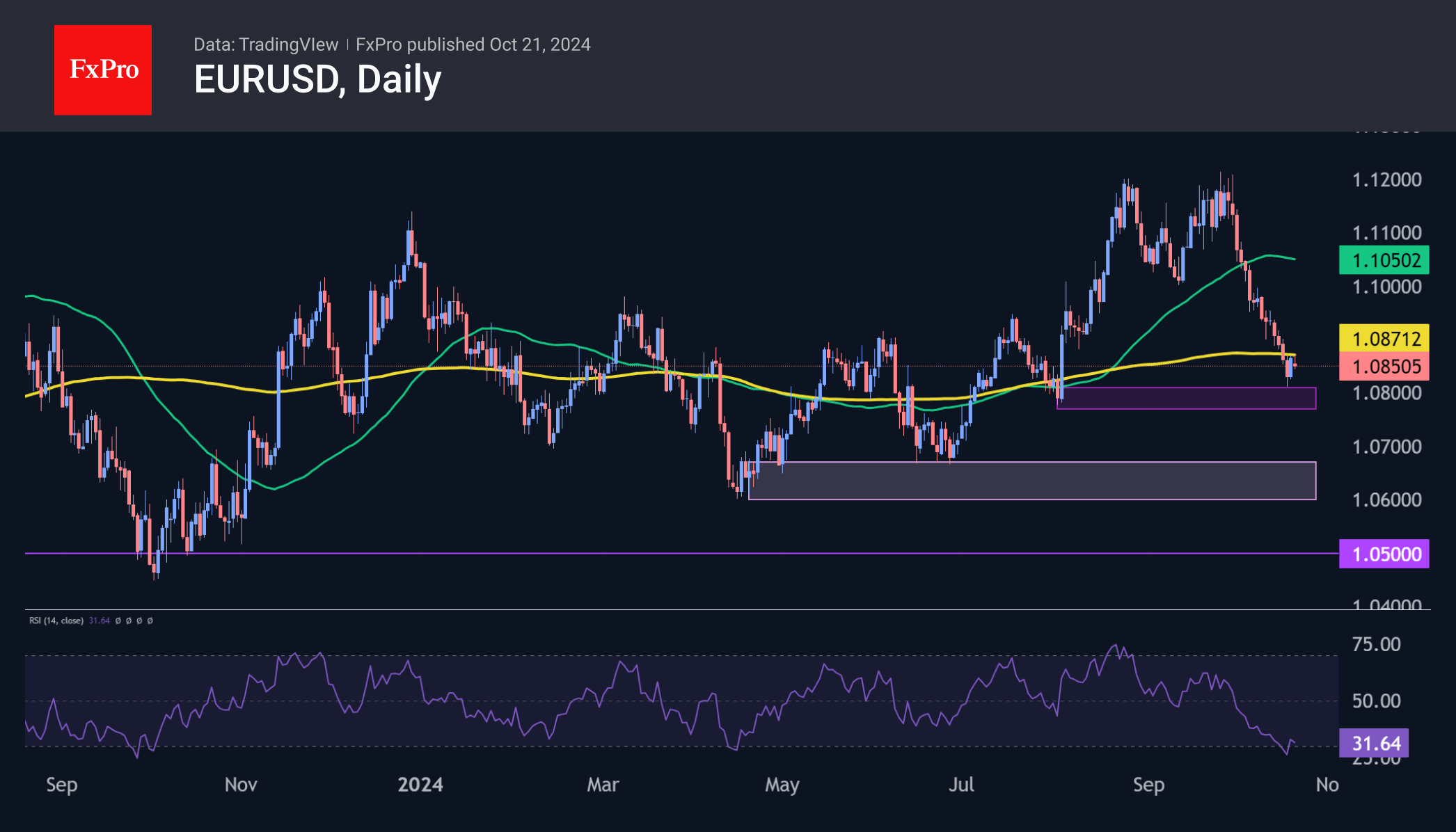

The rally at the end of last week looks like a corrective bounce after the pair had fallen 3.5% from its late September highs. This bounce lost momentum as it ran into the 200-day moving average and unwound what appeared to be overheated selling. The decline at the start of the new week suggests that bearish sentiment is clearly prevailing.

A break below the 1.0770-1.0810 support area would open a direct path to 1.0600-1.0670. If the fundamental background does not change by then, a break to the more fundamental support area—the 1.05 area—is possible.

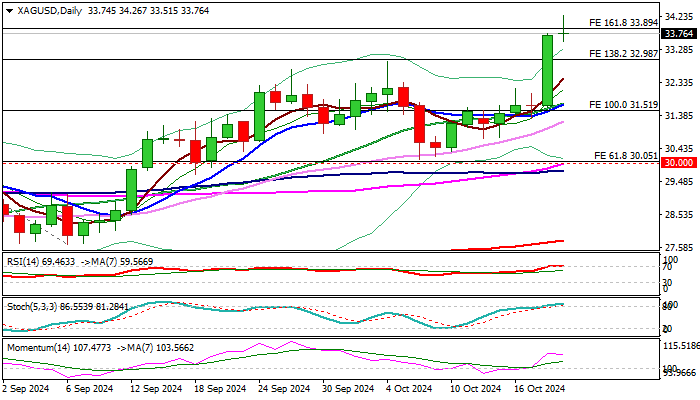

Silver Rises to 12-Year High

Silver price hit new highest since November 2012 on Monday, in extension of last Friday’s record daily rally of 6.4%, with psychological $34.00 barrier being cracked.

Increased safe haven demand dragged silver price, as geopolitical situation is overheated and markets pricing around 90% chance of Fed rate cut in November FOMC policy meeting.

Strong bullish signal has been generated on monthly chart after bulls eventually broke above key barriers at $30.00/50 (psychological / 50% retracement of $49.78/$11.23, 2011/2020 downtrend) which where the price was stuck for four months.

Firmly bullish daily studies continue to contribute to positive structure, underpinned by favorable fundamentals.

The price is currently riding on extended fifth wave of five wave sequence from $26.39 (Aug 8 low) with FE 161.8% (33.89) being cracked.

Close above this level to verify fresh signal and open way for attack at next targets at $35.00/05 (psychological / Fibo 61.8% of $49.78/$11.23) and $35.369 (FE 200%).

Meanwhile, bulls may take a breather under these barriers as daily studies are overbought, with limited dips to be ideally contained above $32.20 zone and to offer better buying opportunities.

Res: 33.89; 34.26; 35.00; 35.36

Sup: 33.51; 32.95; 32.23; 32.00

USD/CHF Technical Outlook: Pullback Before Continuation?

- USD/CHF is showing potential for bullish continuation.

- The Swiss National Bank may welcome a weaker CHF due to pressure from the swiss export sector.

- Upcoming US data and geopolitical events, including the IMF meeting and US election, could impact USD/CHF.

Eyeing an extended move to the upside as it hovers around a support area on Monday. Safe Haven appeal appears to be keeping the Swiss Franc supported at present as USD bulls eye further gains.

As expectations around Fed policy continue to shift, the CHF and the Swiss National Bank have faced different challenges. After exporters urged the government to do something and the strong CHF, the Central Bank will actually welcome some organic weakness in the CHF.

Switzerland has enjoyed easing price pressures for a while now which have raised expectations for further rate cuts from the Swiss National Bank (SNB). In September, Switzerland’s annual Consumer Price Index (CPI) slowed to 0.8%, the lowest in over three years, even though the Swiss National Bank cut its key interest rates at all three meetings this year.

This could lead to policy divergence if the trend continues and this could weigh on the CHF and thus push USD/CHF higher.

Swiss National Bank Interest Rate Probabilities

Source: LSEG Workspace

US Data Ahead

There is not a lot in terms of data from the US this week with larger volatility and price swings expected from the IMF meeting in Washington. The meeting will provide a platform for major Central Bank Governors to provide comments and discuss what they see as the path forward.

Geopolitical tensions remain key given the CHF often attracted haven demand. The US election has been adding another layer of uncertainty as it draws nearer.

Technical Analysis

From a technical standpoint, USD/CHF on a weekly chart below finished last week extremely bullish and just a few pips off the weekly high. USD/CHF is experiencing a slight pullback today as it languishes between the inner and outer trendline.

USD/CHF Weekly Chart, October 21, 2024

Source: TradingView (click to enlarge)

Looking down to the daily chart below and you can see price is currently resting on the support handle.Immediate resistance rests at 0.8700 which is the 100-day MA before.

A break above this level will finally give the pair a chance to retest the descending trendline. Will we get a break or a bounce?

Now there are other scenarios that may develop depending on external circumstances. There may be a short-term pullback toward 0.8550 support or the 0.8500 handle.

USD/CHF Daily Chart, October 21, 2024

Source: TradingView (click to enlarge)

Support

- 0.8633

- 0.8550

- 0.8400

Resistance

- 0.8700

- 0.8756

- 0.8890

EUR/USD Lower, ECB’s Kazimir Confident in ‘Disinflation Path’

The euro has edged lower on Monday. In the North American session, EUR/USD is trading at 1.0838, down 0.24% on the day.

ECB’s Kazimir says disinflation continuing

The European Central Bank lowered its key interest rate last week by a 25 basis points to 3.25%, the first back-to-back rate cuts since December 2011. The rate cut was the third time the ECB has lowered rates this year, as it has been aggressive in its rate-cutting cycling, totaling 75 basis points.

The rate statement from last week’s meeting noted that the “disinflationary process is well on track” and that the inflation outlook had improved due to “recent downside surprises” in economic activity. The September inflation report, released just before the rate announcement on Thursday, indicated that inflation dropped to 1.7% y/y, down from 1.8% in August. This was a milestone as it was the first time inflation has dropped below the ECB’s target of 2% since July 2021.

The optimistic stance was reiterated by ECB Governing Council member Peter Kazimir, who said on Monday that he expects inflation to drop to the 2% target in 2025. Kazimir said he was “increasingly confident that the disinflation path is on a solid footing” which would allow the ECB to continue cutting interest rates.

The ECB remains somewhat cautious, particularly over wage growth and services inflation which have been stubbornly high and are upside risks to the inflation outlook. Still, after three rate cuts this year it’s clear that the direction of the rate path is down and the markets expect the ECB to continue trimming rates right through to March 2025.

EUR/USD Technical

- EUR/USD has pushed below support at 1.0854 and is testing support at 1.0837. Below, there is support at 1.0808

- 1.0884 and 1.0900 are the next resistance lines

Sunset Market Commentary

Markets

Core bonds are dropping at the start of the week and no one really knows why. It’s obviously not the constructive risk environment. European stocks shed about 1% at some point before paring losses to 0.5%. Wall Street opened marginally lower, be it near the record highs. There’s an interesting sectoral divide though with energy companies the only category showing gains (Europe). That brings us to oil markets and the conflict in the Middle East. Tensions rose again after a Hezbollah drone managed to evade Israel’s aerial defenses and exploded next to PM Netanyahu’s private home. That prompted another round of hawkish talk. Brent rises 1.5% to $74.1. While only recouping just a tad of last week’s hefty losses, rising prices and the geopolitical narrative do dovetail with rising bond yields and the mild risk off environment. Bunds underperform US Treasuries, adding 6.1-8.7 bps in a bear steepener, drawn out over the entire European session. US Treasury yields rise 4.1-5.1 bps across the curve. Some more ECB policymakers hit the wires after last week’s meeting. Lithuanian governor Simkus said it is possible the ECB will have to cut to below the natural level of somewhere between 2-3% if a fall in inflation becomes entrenched. He doesn’t think steps bigger than 25 bps are necessary for the time being. Governing council member Kazimir said the December meeting is wide open after having cut at the in between meeting in October. But money markets made up their mind. If anything, Thursday’s October PMI’s pose a risk for more aggressive bets should they disappoint.

The dollar holds the advantage on currency markets. EUR/USD sought to build on Friday’s momentum but ran aground pretty fast. The pair is currently hovering around 1.085. USD/JPY hasn’t given up on the 150 barrier, unfazed by Japan’s top FX official verbal warning end of last week. The trade-weighted dollar marginally rises from 103.4 towards 103.7. DXY on Friday incurred only it’s third loss this month so far, with the 200dMA proving too big a hurdle for the time being. EUR/GBP holds near the recent lows just north of 0.83 after testing that big figure (which coincided with the lower bound of the November ‘23 downward trend channel) end last week.

News & Views

Several Polish September data published today printed soft/softer than expected. Sold production rebounded 9.0% in September from August, but the level was still 0.3% lower compared to the same month last year. According to Statistics Poland, among the main industrial groupings there was a 2.6% Y/Y decrease in the production of intermediate goods and by 1.2% in capital goods. An increase was observed in the production of non-durable consumer goods (+ 2.7%) and durable consumer goods (2.3%) and a modest rise in energy production (0.1%). Despite a (seasonal) monthly rebound (12.0%), construction output remained 9.0% below the level of the same month last year. September labour market data also suggest a cooling. Average wage growth decelerated further (-0.6% M/M and 10.1%Y/Y; 11.0% Y/Y was expected). Employment also declined -0.1% M/M and -0.5% Y/Y. At the same time producer prices also showed a further easing price pressures (-0.5% M/M, -6.3% Y/Y). The data, while volatile, suggest that underlying trends are falling in place for the National Bank of Poland to gradually reconsider rate cuts (currently 5.75%). Most NBP comments recently held the line that a rate cut will only be possible after the March 2025 MPC meeting at best. The zloty weakens from EUR/PLN 4.305 to currently 4.3175, but to move is in line with other regional FX was mainly already occurred before the data release.

According to UK property website Rightmove, average seller asking prices for British homes rose 0.3% M/M in October, but this was much lower than the average seasonal monthly increase for this time of the year. Prices were 1.0% higher compared to the same month last year. The modest rise occurs even as market activity remains strong. The number of sales is rising sharply. As explanation for the modest rise Rightmove mentions that buyers are using a greater choice of properties available to increase their negotiating power. Rightmove still maintains a positive assessment on 2025 even as affordability pressures remain. Some buyers may be waiting for Budget clarity and cheaper mortgage rates before acting.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0838; (P) 1.0854; (R1) 1.0884; More...

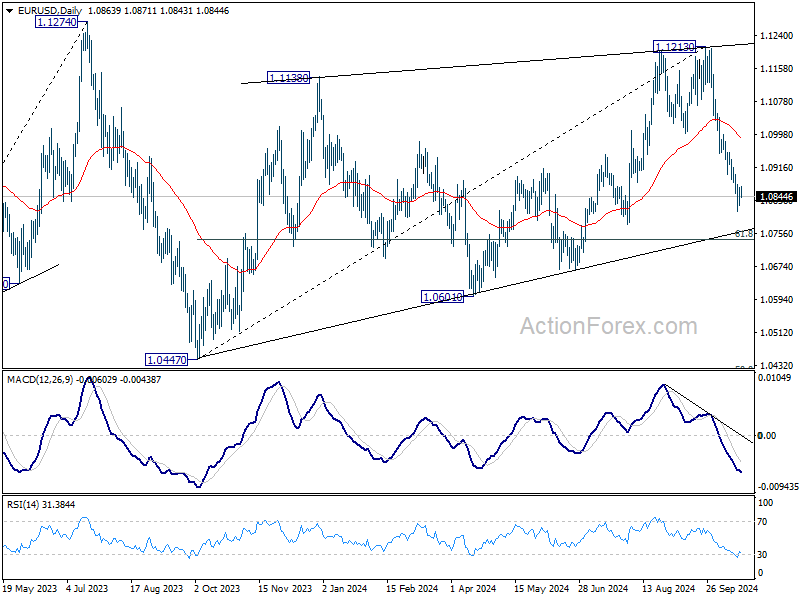

EUR/USD is staying in consolidation above 1.0810 temporary low and intraday bias stays neutral. Outlook will stay remain as long as 1.0954 resistance holds. Below 1.0810 will resume the fall from 1.1213 to 61.8% retracement of 1.0447 to 1.1213 at 1.0740. Firm break there will target 1.0601 support next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3011; (P) 1.3041; (R1) 1.3083; More...

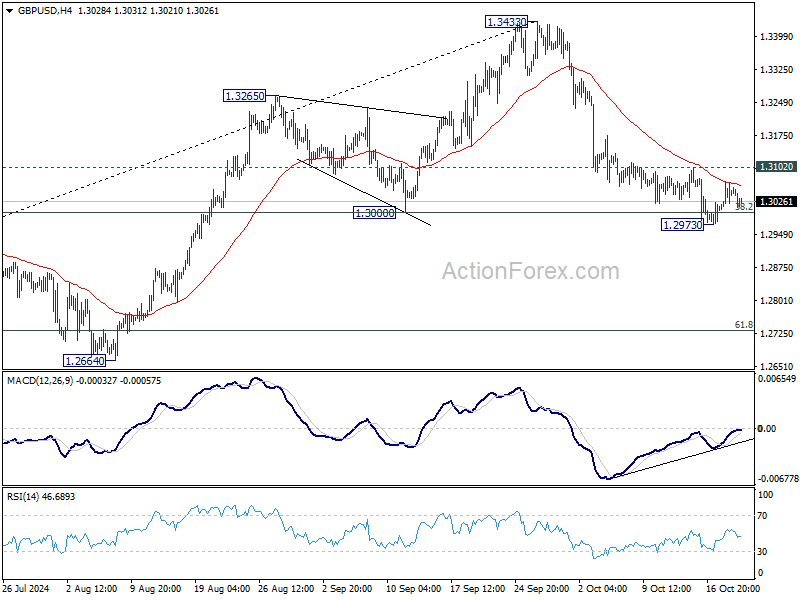

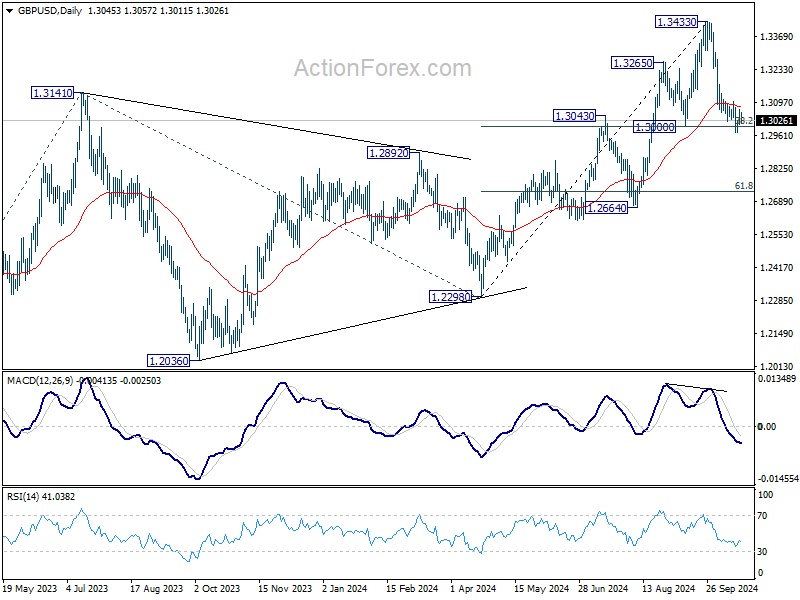

GBP/USD is staying in consolidation above 1.2973 temporary low and intraday bias stays neutral first. On the upside, firm break of 1.3102 resistance will argue that pullback from 1.3433 has completed, and turn bias back to the upside for stronger rebound. On the downside, however, sustained break of 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) will argue that whole rise from 1.2298 has completed and bring deeper fall to 61.8% retracement at 1.2732.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

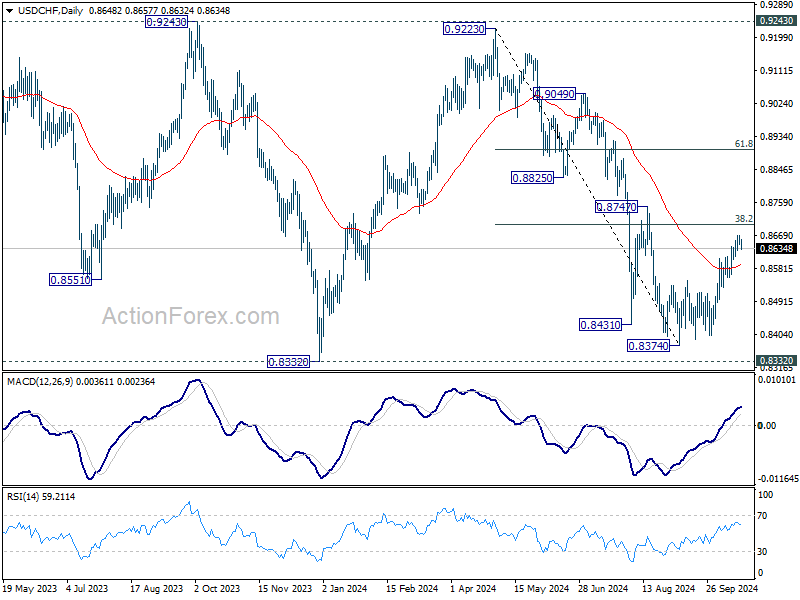

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8639; (P) 0.8654; (R1) 0.8663; More…

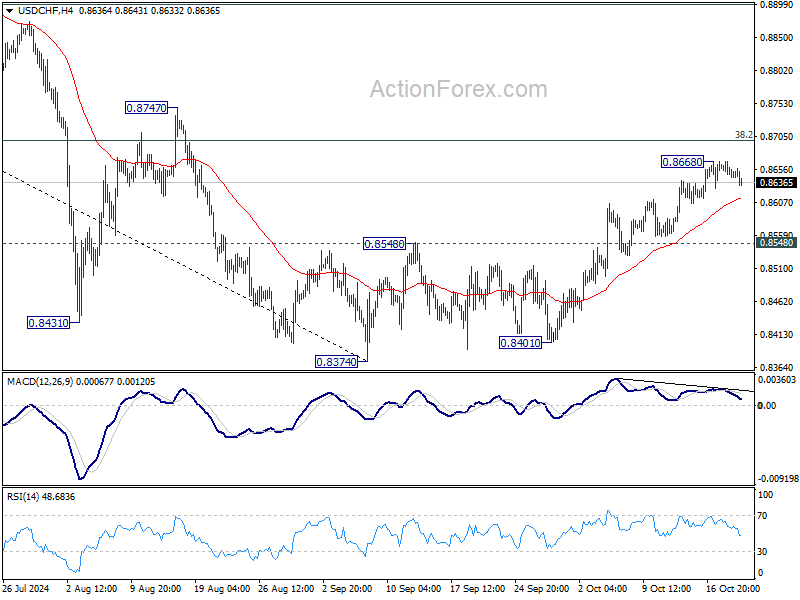

Intraday bias in USD/CHF remains neutral for the moment, and some more consolidations could be seen below 0.8668 temporary top. Further rally is expected as long as 0.8548 resistance turned support holds. Above 0.8668 will target 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed at 0.8374, after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

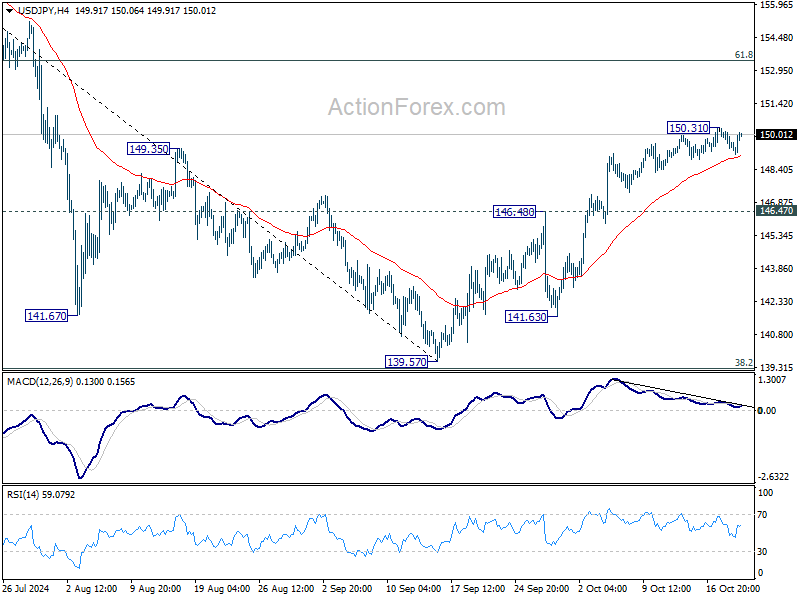

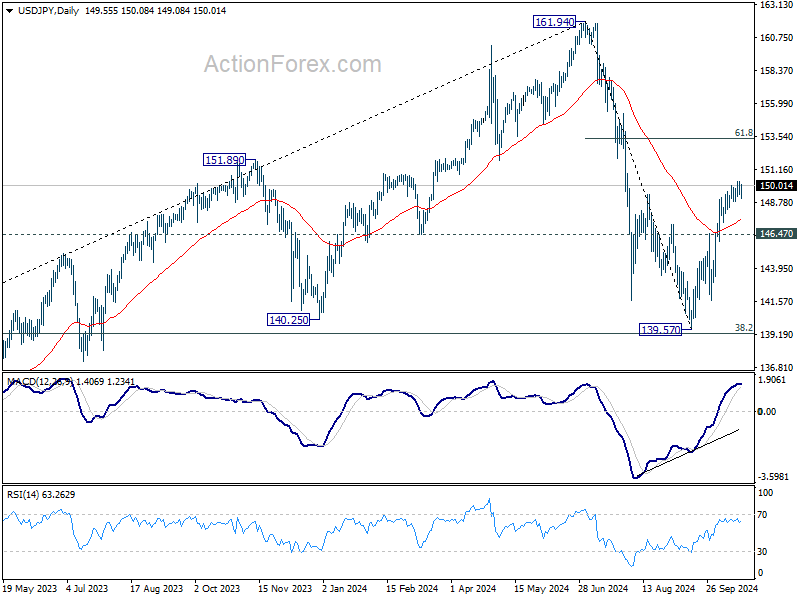

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.19; (P) 149.74; (R1) 150.10; More...

USD/JPY recovered mildly ahead of 4H MACD, but stays below 150.31 temporary top. Intraday bias remains neutral first. Further rally is expected as long as 146.47 resistance turned support holds. Above 150.31 will resume the rebound from 139.57 to 61.8% retracement of 161.94 to 139.57 at 153.39. However, break of 146.48 resistance turned support will indicate that rebound from 139.57 has already completed.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Dollar Hold Firm as Yen Weakens Amid Subdued Trading

In the largely uneventful Asian and European sessions today, major currencies remained within familiar ranges, as the absence of key economic data releases kept markets subdued. Central bank commentary continued to dominate the narrative, particularly from ECB officials, who maintained their dovish stance. However, this comes as little surprise, with expectations largely baked in that ECB is likely to reduce rates again in December unless a sharp improvement in economic activity or inflation data emerges.

On the currency front, Swiss Franc and Dollar are the stronger performers, followed by Euro. Yen, however, turned under pressure as the weakest currency today, with Aussie and Sterling also facing losses. Canadian Dollar and New Zealand Dollar are positioned in the middle. But overall, major pairs and crosses remain range-bound, with today's moves offering little insight into underlying trends.

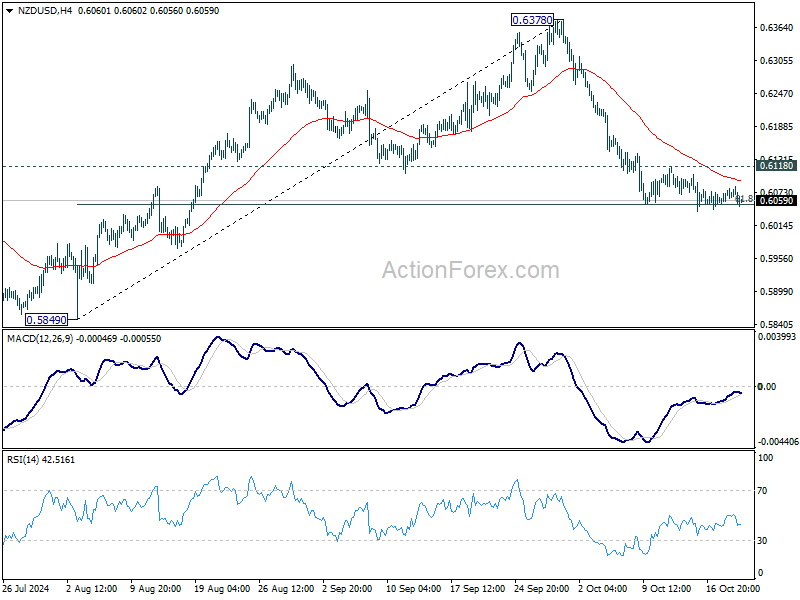

Technically, NZD/USD continues to press 61.8% retracement of 0.5849 to 0.6378 at 0.6051, and it should be about time for a breakout from the tight range. Decisive break of 0.6051 would resume the fall from 06378 towards 0.5849 support Nevertheless, strong bounce from current level, followed by break of 0.6118 resistance will argue that the fall has completed an bring stronger rebound towards 0.6378 instead.

In Europe, at the time of writing, FTSE is down -0.29%. DAX is down -0.78%. CAC is down -0.75%. UK 10-year yield is up 0.064 at 4.118. Germany 10-year yield is up 0.081 at 2.272 Earlier in Asia, Nikkei fell -0.07%. Hong Kong HSI fell -1.57%. China Shanghai SSE rose 0.20%. Singapore Strait Times fell -0.70%. Japan 10-year JGB yield fell -0.0086 to 0.962.

ECB’s Kazimir: Disinflation progress encouraging, but further proof needed

ECB Governing Council member Peter Kazimir expressed growing confidence in the disinflation trend, stating in a blog post today that the path to lower inflation appears to be on "solid footing".

Kazimir added that if upcoming data continues to confirm accelerated disinflation, the ECB would be in a "strong and comfortable position to continue the easing cycle."

However, he noted that wage growth and services inflation, two critical elements, have yet to show the expected decline. He added, "If new information points toward higher inflation, we can still slow down the pace at which we remove restrictions in the coming meetings."

ECB's Simkus: Rates to move toward neutral as disinflation stays on track

ECB Governing Council member Gediminas Simkus commented today that the disinflationary trend is progressing steadily, though he acknowledged that services inflation remains elevated.

Simkus expects monetary policy to gradually become less restrictive, with the central bank lowering interest rates toward a "natural" level, estimated to be between 2-3%.

However, he emphasized that if the disinflation process becomes deeply "entrenched", rates could potentially fall below the natural level.

RBA's Hauser signals no early rate cuts as inflation remains too high

RBA Deputy Governor Andrew Hauser emphasized today that inflation remains "too high" for the central bank to consider immediate rate cuts.

Recent strong employment data led markets to push back the expected timing for the first rate cut from February to April. Hauser refrained from commenting on the market’s pricing, but noted, "the response of rates to the data does seem to be quite encouraging.”

While acknowledging the importance of data, Hauser stressed that RBA is “data-dependent but not data-obsessed,” noting that broader economic conditions also factor into policy decisions.

“Activity has been weak, very weak, and we haven’t seen the inflation number for the third quarter yet,” he added.

The RBA’s cautious approach contrasts with other central banks that have already begun easing, highlighting Australia’s persistent inflationary pressures. The market will be closely watching the third-quarter inflation data to gauge the timing and magnitude of future policy changes.

PBoC slashes loan prime rates

People's Bank of China lowered its one-year loan prime rate to 3.1% and trimmed the five-year LPR to 3.6%, as anticipated by market watchers. This move, at the upper end of the 20-25 basis point range suggested by Governor Pan Gongsheng during a Beijing forum last Friday, impacts a broad spectrum of loans in China. The one-year LPR directly influences corporate and household loans, while the five-year LPR serves as a benchmark for mortgage rates.

While this rate cut signifies some level of monetary stimulus, analysts continue to stress that China's core issue is not the supply of credit, but rather a lack of demand. Many argue that without substantial fiscal stimulus, the impact of these rate adjustments will remain muted.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.19; (P) 149.74; (R1) 150.10; More...

USD/JPY recovered mildly ahead of 4H MACD, but stays below 150.31 temporary top. Intraday bias remains neutral first. Further rally is expected as long as 146.47 resistance turned support holds. Above 150.31 will resume the rebound from 139.57 to 61.8% retracement of 161.94 to 139.57 at 153.39. However, break of 146.48 resistance turned support will indicate that rebound from 139.57 has already completed.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.