Sample Category Title

RBA minutes: Inflation vigilance remains key focus

Minutes from RBA's September meeting revealed the consensus to keep the cash rate unchanged, as members felt there had been no significant changes since the previous meeting to justify a shift in policy.

Members discussed scenarios that could lead to policy being "held restrictive for a prolonged period or tightened further". One scenario involved stronger-than-expected "consumption growth", driven by rising household disposable income. Another involved more "constrained" than expected "aggregate supply" outlook. Financial conditions could turn out to be "insufficiently restrictive".

Conversely, they acknowledged scenarios where policy could become less restrictive, such as the economy proved to be "significantly weaker than expected". Or, "inflation proved less persistent than assumed", even without significant economic weakness.

The board reiterated their vigilance to "upside risks to inflation" and emphasized that policy will remain sufficiently restrictive until inflation is clearly moving toward target. They reiterated that future rate changes could not be "ruled in or ruled out" based on current data, leaving the door open for adjustments if necessary.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Hybrid – 23 and 24 September 2024

Members participating

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor), Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Carol Schwartz AO, Alison Watkins AM

Members had granted leave of absence to Ian Harper AO, in accordance with section 18A of the Reserve Bank Act 1959.

Others participating

Sarah Hunter (Assistant Governor, Economic), Brad Jones (Assistant Governor, Financial System), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Future Hub), Susan Black (Acting Head, Domestic Markets Department), Andrea Brischetto (Head, Financial Stability Department), Sally Cray (Chief Communications Officer), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department)

Economic conditions

Members began their discussion by noting that the economic data received since the previous meeting had been broadly in line with the staff’s expectations.

Recent data on inflation had been consistent with a further gradual easing in underlying inflationary pressures. Looking ahead, monthly CPI data for August – to be released the day after the meeting – were expected to show a sharp decline in headline inflation, partly because of federal and state government cost-of-living relief. But underlying inflation was expected to remain above target. Inflation for some components had remained high and persistent, but the easing in the rate of growth in advertised rents over the preceding three months was expected to feed through gradually to lower rent inflation in the CPI.

Growth in GDP in the June quarter had been in line with the staff’s expectations. However, the composition of that growth suggested somewhat less underlying momentum in aggregate demand than the staff had assumed. Notably, household consumption had been significantly weaker than expected, while the offsetting stronger-than-expected outcomes were in components that tended to be more volatile from quarter to quarter. Members observed that weak growth in output was closing the gap between aggregate demand and the economy’s estimated supply capacity, but that the two were not yet aligned.

Members discussed the implications of the weaker-than-expected outcome for household consumption in the June quarter. This was seen to have reflected a combination of a genuine slowing in momentum and the unwinding of one-off spending in the March quarter. Bank transaction data suggested that the recent weakness in household spending had been broadly based across different types of households, including those without mortgages. Strong growth in government consumption – which includes the provision of services to households – meant that overall consumption growth had been more resilient than implied by household consumption alone but was still below its pre-pandemic average.

A key question was how spending was evolving in the September quarter. The staff had previously forecast household consumption to strengthen in response to a recovery in real incomes, including because of the implementation of the Stage 3 tax cuts in July. Members considered whether this forecast was still consistent with available timely indicators of household spending, including the signals derived from bank transaction data and retail sales. These suggested that growth in spending had been weak in July but had strengthened somewhat in August. Retailers in the RBA’s liaison program had reported that conditions had remained stable over prior months and were generally expected to stay that way over coming months. Based on this information, members judged that it was still reasonable to expect a pick-up in consumption growth over the second half of the year, but it was too soon to form firm views based on these partial indicators and there was some risk that the pick-up could be somewhat slower than previously expected. Members also noted that the official statistical treatment of the cost-of-living subsidies provided to households would have the effect of reallocating measured spending in the September quarter from household to public consumption.

Turning to the prospects for trade, members noted that global economic indicators had been somewhat weaker over preceding months. The outlook for the Chinese economy had softened and this had been reflected in weaker demand for iron ore and lower commodity prices, despite the earlier easing of monetary policy. In many advanced economies, conditions in labour markets had eased materially and job vacancies had returned to pre-pandemic levels, unlike in Australia. Inflation had also declined in these economies and central banks had become more confident of returning inflation sustainably to target. In that context, some central banks – including the US Federal Reserve – had focused on downside risks to labour markets in recent communications.

The cap on international student commencements to be applied to the higher education and vocational education and training sectors in Australia from 2025 was expected to weigh on services exports. Members noted that the cap was in addition to the earlier tightening in requirements for student visa applicants, which had already seen a fall in student visa grants. However, the implications of lower student arrivals for the balance between aggregate demand and supply, and hence for the inflation outlook, were less clear. Lower numbers of international student arrivals would be likely to reduce aggregate demand (including for housing), but also lower growth in population and therefore the economy’s supply capacity. The implications of these various effects would be assessed more carefully as part of the subsequent forecast update.

Members judged that labour market conditions in Australia were still tight relative to both full employment and conditions in other economies. The share of unemployed people finding jobs was high and the share of workers losing their jobs was very low. Conditions had nonetheless continued to ease as expected and indicators of future labour market conditions suggested that would continue. The unemployment rate had increased a little over preceding months as strong growth in the supply of labour (including through higher participation) was only partially absorbed by solid employment growth. Members noted that the rise in participation reflected a combination of jobs being readily available and the effect of financial pressures from the higher cost of living.

Members considered medium-term developments in labour productivity growth, which remained subdued. In part, that reflected a rising share of employment in the non-market sector, where measured productivity had declined over prior years. However, productivity outcomes had also been weak in a range of market industries, a trend evident in many other economies. Overall, the information received from the June quarter national accounts had reinforced concerns about future growth in supply. In turn, this could have implications for the sustainable pace of wages growth. Members noted that wages growth had continued to ease in the June quarter from high levels, broadly as expected.

Financial conditions

Members commenced their discussion of financial conditions by noting that several advanced economy central banks had reduced their policy rates since the previous meeting, in response to easing labour market conditions and progress in returning inflation sustainably to target; they had also communicated that further policy easing was likely. Market participants expected policy rates to reach central bank estimates of neutral levels by around the end of 2025. An exception was the Bank of Japan, which had communicated that it would be appropriate to raise its policy rate further from current low levels if underlying inflation increased as forecast.

Financial market conditions had been calmer following the bout of extreme volatility around the time of the previous meeting. However, several of the factors that had contributed to the volatility remained in place, such as elevated risk-taking and leveraged positions.

Members noted that financial market pricing across a range of asset classes in advanced economies was consistent with expectations of a soft economic landing. Sovereign bond yields in most advanced economies had declined further since the August meeting, reflecting both an easing in expectations for policy rates and a decline in inflation expectations. Other measures of financial conditions had also eased as volatility subsided and risk premia declined. Corporate bond yields in the United States and European countries had declined to year-to-date lows, including because of narrower spreads to sovereign bonds.

In China, weakness in the property sector had continued to weigh on credit demand and economic activity. Authorities had intervened to lean against declines in longer term government bond yields and the renminbi had appreciated alongside a narrowing of China–US interest rate differentials.

The Australian dollar trade-weighted index had traded within the range observed since early 2022, despite some volatility around the time of the August meeting. The exchange rate had been affected by a widening in yield differentials arising from market participants’ expectations that other central banks would reduce their policy rates by more than the RBA. The effect of this on the exchange rate had been offset somewhat by declines in commodity prices.

Members judged that Australian financial conditions remained restrictive overall but had eased somewhat over preceding months. Market expectations for the path of the cash rate were materially lower than a few months earlier, and bond yields and some lending and deposit rates had declined in tandem. Housing credit growth had also gradually increased, and business credit growth was above its average pace since the global financial crisis. Funding conditions more generally for Australian financial and non-financial corporations remained favourable. Members discussed the implications of this for future business investment and concluded that it seemed unlikely financial conditions would be a binding constraint on investment for most businesses.

While market expectations for the path of the cash rate were lower than a few months earlier, members noted that they had risen in response to the Governor’s comments that, based on data to hand at the August meeting, the Board did not expect to lower rates in the near term. Market pricing suggested that participants expected the RBA to start cutting the cash rate from around late 2024 or early 2025, but at a more gradual pace than that expected in several other advanced economies. That was consistent with the fact that policy rates in most other advanced economies had been increased earlier and to more restrictive levels than in Australia, and that inflation appeared to be returning sustainably to target more quickly in those economies. Market expectations were nevertheless for the stance of monetary policy in those countries (as measured by gaps between the policy rate and central bank estimates of the neutral interest rate) to be more restrictive than in Australia until around late 2025.

Financial stability assessment

Members discussed the staff’s semi-annual assessment of financial stability risks. In the context of an easing in inflation globally and an uncertain economic outlook, the staff’s assessment was that vulnerabilities in the global financial system remain. Three vulnerabilities stood out as having the potential to affect financial stability in Australia significantly, namely:

- increased complexity and interconnectedness in the financial system, in part reflecting digitalisation and rapid technological development, had created operational vulnerabilities and central points of failure

- low market risk premia had raised the prospect of a disorderly adjustment in financial asset prices, including if expectations for a soft landing in the global economy were not realised and particularly in the context of rising government debt and the absence of medium-term fiscal frameworks

- longstanding vulnerabilities in the Chinese financial system – affecting banks, non-banks and local governments – had been exacerbated by the ongoing weakness in the Chinese real estate sector.

Members observed the potential for global threats originating from outside the financial system, such as geopolitical risks and climate change, to interact with these vulnerabilities with adverse effects. For example, heightened geopolitical tensions had increased the prospect of cyber-attacks that could have systemic implications. Members noted that the RBA is working with market participants and the other agencies of the Council of Financial Regulators to strengthen the operational resilience of the Australian financial system.

Domestically, members recognised that financial pressures from persistent inflation and restrictive monetary policy meant many households were having to make difficult adjustments to their spending and financial arrangements. At the same time, risks to the Australian financial system from lending to households and businesses remained contained. In part, that reflected the fact that banks had maintained prudent lending standards and built substantial capital over recent years, leaving them well positioned to continue supporting the economy through credit provision. But it also reflected the fact that the share of borrowers experiencing severe financial stress had remained small, with housing loan arrears having increased only gradually from low levels. The increase was greatest for highly leveraged borrowers, but these comprised a very small share of lending. Very few borrowers were in negative equity.

Members observed that borrowers’ resilience had been supported by prevailing savings buffers and the ongoing strength in the labour market. Most borrowers had maintained or added to their mortgage prepayment buffers over the preceding year; that said, there was a range of experiences and some borrowers were regularly drawing on their savings. High-income borrowers were the only group that in aggregate were running down their prepayment buffers, but their buffers remained large and were declining partly to fund discretionary consumption. Most borrowers were still likely to have spare cash flow under a range of plausible scenarios, including one in which there was a marked deterioration in the labour market. A more sustained reduction in inflation would also help to ease financial pressures.

The strong financial position of most businesses prior to the slowing in the economy had supported their ability to navigate the recent period. Members noted that the sharp increase in business insolvencies – particularly for small businesses and in the hospitality sector – partly reflected a period of catch-up following the removal of pandemic-era support. The cumulative level of insolvencies was still below the pre-pandemic trend, and most insolvencies so far had involved small businesses with little debt, limiting the broader spillovers to lenders. The share of banks’ business loans in arrears had remained low.

Members discussed the expansion of business lending by non-banks, as favourable funding conditions had enabled them to claim market share from banks. While there was limited information about the quality of this lending, its small size limited systemic risks. Elsewhere in the non-bank sector, the significant growth of the superannuation sector had increased its importance to the smooth functioning of the financial system. While financial stability risks were limited by most funds having a defined contribution structure in which leverage was restricted, the growing size of the industry underscored the importance of maintaining strong liquidity risk management practices.

Members agreed that financial stability concerns were not a constraint on monetary policy at the time of the meeting. However, looking ahead, they discussed the potential for financial sector vulnerabilities to build if easier financial conditions were to lead higher risk borrowers to take on excessive debt and/or lenders to compete more aggressively by lowering lending standards. Members noted the RBA Review’s recommendation that decisions about monetary and macroprudential policy should be coordinated in such a situation.

Review of the Term Funding Facility

Members discussed the staff review of the Term Funding Facility (TFF), which was one component of the monetary policy package to support the Australian economy during the COVID-19 pandemic. The review concluded that the TFF had met its policy goals, which were to: reinforce the benefits to the economy of a lower cash rate by reducing the funding costs of banks and, in turn, interest rates paid by borrowers; and encourage banks to support businesses during a difficult period. Members agreed that the TFF had contributed effectively to restoring confidence in financial markets, keeping credit flowing and stimulating aggregate demand. They agreed that a facility of this type should remain one of the policy options to be considered if future circumstances warranted the use of unconventional monetary policy.

Members discussed the lessons from the experience with the TFF. They noted the importance of effective contingency planning ahead of considering the use of unconventional monetary policy tools, including ensuring operational readiness, effective risk management and appropriate governance. Members also observed the trade-offs that could be considered in the design of any future scheme. For instance, the fixed rate feature of the TFF was judged at the time to be important to ensure consistency with other elements of the monetary policy package deployed in response to the pandemic, despite bringing greater financial risk to the RBA.

Nearly half of the financial losses stemming from the TFF were because of its extension in September 2020. Members discussed whether that decision was appropriate, given the information available at the time. They highlighted: the international evidence supporting the need for strong action when interest rates are near zero; the value of coordinating with fiscal responses in such circumstances; the extreme uncertainty about the impact of the virus on the economy and of the impending end of the JobKeeper scheme at the time; and the way the TFF reinforced other elements of the monetary policy package. On the other hand, the lack of drawdown by banks until close to the September 2020 deadline signalled that they might not have needed additional funding. In addition, the potential implications for the RBA’s finances of the TFF extension had been subject to only limited stress testing. Members concluded that these observations emphasised the importance of considering a wide range of scenarios when making any future policy decisions involving unconventional monetary policy measures.

The Board agreed to publish the review, which would be accompanied by a speech by the Assistant Governor (Financial Markets).

Considerations for monetary policy

Turning to considerations for the immediate policy decision, members noted that the information received since the previous meeting had been mixed. Taken together, the information had not materially altered their assessment of the economic outlook as of this meeting. Underlying inflation was still too high and, in quarterly terms, had fallen very little over the preceding year.

Output growth remained weak: GDP growth in the June quarter had been in line with expectations but household consumption had been notably weaker than expected. The staff still judged it as likely that consumption growth would pick up alongside the expected recovery in real disposable income in the second half of the year. It was too soon to judge how rapidly this would occur, though higher frequency data suggested there was a risk that it could be delayed somewhat.

Risks around the outlook for Australia’s exports had shifted to the downside since the prior meeting. In part, this reflected a greater prospect of slower global output growth, given further increases in unemployment rates in some countries and the weakness in the Chinese economy. Members observed that services exports were also likely to be weaker than forecast in August because of the various policy measures relating to overseas student numbers. The implications of this for inflation were less clear though, given the potential offsetting implications for labour supply.

Growth in employment had remained solid over prior months, including in comparison with other economies. The unemployment rate had risen gradually but conditions in the labour market still appeared to be tighter than those consistent with sustainable full employment. Members judged that the level of aggregate demand was still above the level of aggregate supply. Weak productivity growth was constraining the economy’s potential growth rate.

Financial conditions had eased over prior months, as cash rate expectations and bond yields declined and equity prices rose. Credit growth had picked up and banks were well placed to support the economy. Members observed that many households were experiencing financial pressure but only a small share of households and firms were not able to service their loans. The exchange rate had appreciated a little but, in trade-weighted terms, was within its range of recent years.

Taken together, members felt that not enough had changed since the previous meeting to alter their assessment that the current level of the cash rate best balanced the risks to inflation and the labour market. They therefore agreed that it was appropriate to leave the cash rate target unchanged at this meeting.

Looking ahead, members reiterated that the data and the evolving assessment of risks would guide their future decisions on what path of interest rates would bring inflation to target within a reasonable timeframe, while preserving the gains in the labour market.

Members then discussed scenarios in which future monetary policy might need to be held restrictive for a prolonged period or tightened further. One of these was if consumption growth were to pick up materially in response to the recovery in real household disposable income that was likely to have begun around mid-year. If that were to occur, labour market outcomes could be stronger than forecast and inflation would return to target more slowly. Another was if the outlook for aggregate supply proved to be more constrained than currently expected – for instance, if the economy’s current supply potential had been overestimated or if future productivity growth turned out to be weaker than assumed. Members also considered a formal analysis in which the economy’s supply capacity was more limited than currently assumed. In this case, the cash rate might need to be noticeably higher than the market path underpinning the August forecasts, in order to bring inflation sustainably back to target by 2026.

Members observed that monetary policy could need to be tightened, even if the Board’s judgements about consumption, the labour market and supply potential prove correct, should present financial conditions turn out to be insufficiently restrictive to return inflation to target. Members noted that the easing in financial conditions over prior months and the pick-up in credit growth made this scenario somewhat more plausible, as did the observation that banks were well placed to facilitate any strengthening in credit demand.

On the other hand, members observed that there were scenarios in which future financial conditions might need to be less restrictive than they were at present. One such scenario was if the economy proved to be significantly weaker than expected and this placed more downward pressure on underlying inflation than expected. This could occur if households saved a significantly larger proportion of their incomes than currently assumed, perhaps because of earlier declines in real income and/or more persistent uncertainty. It could also occur if the labour market weakened more sharply than forecast. Another scenario was if inflation proved less persistent than assumed, even without weaker-than-expected activity. This could occur, for instance, if rent inflation fell more rapidly, falling petrol or other commodity prices materially reduced firms’ cost base or the decline in discretionary spending flowed through materially more quickly to services inflation.

Members noted that each of these outcomes was conceivable given the considerable uncertainty about the economic outlook. Therefore, future financial conditions might need to be either tighter or looser than at present to achieve the Board’s objectives. Members agreed that, while it was important to take account of economic developments abroad, it was not necessary for the cash rate target to evolve in line with policy rates in other economies since Australian inflation was higher, the labour market stronger and monetary policy less restrictive than in many other advanced economies. The exchange rate could also adjust as interest rate differentials between Australia and other economies evolved.

In finalising the Board’s statement, members agreed that it was important to convey that the Board remained vigilant to upside risks to inflation. They also affirmed that monetary policy would need to be sufficiently restrictive until members were confident that inflation was moving sustainably towards the target range and, based on the information available at the time of the meeting, that it was not possible to either rule in or rule out future changes in the cash rate target at this time. Members would rely upon the data and the evolving assessment of risks to guide the Board’s decisions. Returning inflation to target remains the Board’s highest priority and it will do what is necessary to achieve that outcome.

The decision

The Board decided to leave the cash rate target unchanged at 4.35 per cent, and the interest rate on Exchange Settlement balances unchanged at 4.25 per cent.

Australia’s NAB business confidence improves to -2, inflation pressures still high despite easing costs

Australia’s NAB Business Confidence improved in September, rising from -5 to -2. Business conditions also increased from 4 to 7, with key components such as trading conditions rising from 8 to 12, profitability up from 2 to 5, and employment conditions also climbing from 1 to 5.

A key positive development was the continued easing in input cost pressures. Labour cost growth slowed to 1.7% in quarterly equivalent terms, down from 1.8% in August. Purchase cost growth eased to 1.2%, from 1.6%.

NAB’s Head of Australian Economics, Gareth Spence, noted that while business conditions have been trending lower over the past 24 months due to slower economic growth, capacity utilization remains significantly above its long-run average.

Spence remarked, “This remains an important dynamic for the RBA where, despite slow growth, inflation remains too high, suggesting that the balance of supply and demand in the economy is yet to fully normalize.”

Australian Westpac consumer sentiment hits 2.5-year high as rate hike fears ease

Australia's Westpac Consumer Sentiment surged by 6.2% yoy in October to 89.8, marking the highest reading since RBA began its tightening cycle two and a half years ago.

Westpac noted that consumer sentiment has been buoyed by interest rate cuts overseas and improving inflation conditions domestically. "Consumers are no longer fearful that the RBA could take interest rates higher," Westpac commented.

In particular, the Mortgage Rate Expectations Index, which tracks expectations for variable mortgage rates over the next 12 months, saw a significant drop of -14.1% mom to 106.4. The index has now declined by one-third since July, as households feel less pressure from future rate increases.

Westpac anticipates that RBA's cash rate target will remain unchanged for the rest of the year. While Q3 CPI data, due on October 30, is expected to show inflation tracking lower, it may not be enough for RBA to "shift to an explicit easing bias" at the November meeting. However, Westpac believes the Board could begin easing its "hawkish hold" and adopt a more neutral policy stance as inflation pressures show signs of abating.

Japan’s real wages fall -0.6% yoy in Aug as inflation outpaces wage growth

Japan's real wages declined by -0.6% yoy in August, marking the first drop in three months. Nominal wages rose for the 32nd consecutive month, increasing by 3.0% yoy, slightly missed market expectations of 3.1% .

The wage growth was not enough to offset inflationary pressures. The CPI used to calculate real wages, which includes fresh food prices but excludes owners' equivalent rent, surged by 3.5% yoy in August, the highest increase since October 2023.

On a positive note, base wages (excluding bonuses and overtime) saw a significant 3.0% yoy increase, the largest rise in nearly 32 years. Overtime pay grew by 2.6% yoy. However, these gains were still outpaced by inflation.

In other data, household spending fell -1.9% yoy in August, but the decline was less severe than the market's expected drop of -2.6%.

Fed’s Musalem urges patience as Kashkari flags shifting balance of risks

In a speech overnight, St. Louis Fed President Alberto Musalem noted last week's employment report, despite exceeding expectations, did not prompt him to alter his baseline outlook for the economy. He added that both inflation and the labor market are currently in a "good place," with risks to the Fed's dual mandate—price stability and full employment—"roughly balanced."

Nevertheless, Musalem expressed caution, arguing that the "costs of easing too much too soon" would outweigh the risks of easing too little. He added that should maintain its approach of "gradual reductions" in interest rates over time, highlighting that "patience" has been key to Fed’s progress on inflation. He maintained that this approach "has served the FOMC well" but was careful not to commit to any specifics regarding the size or timing of future rate cuts.

Separately, Minneapolis Fed President Neel Kashkari echoed Musalem’s sentiment regarding the resilience of the labor market, noting, “It looks like it is still a strong labor market.”

Kashkari acknowledged that traditionally, Fed’s aggressive rate hikes would have led to more significant weakness in employment, but so far, that hasn’t materialized. "We have not seen that, so that's a really good fact that the job market has stayed strong while inflation has come down," Kashkari said.

However, Kashkari did caution that the balance of risks is now shifting "away from higher inflation towards maybe higher unemployment"

ECB’s Cipollone sees slower growth and faster inflation deceleration

ECB Executive Board member Piero Cipollone suggested in an interview that growth may come in "a little bit slower" than previously expected. Weak PMI data is also raising concern. The "signals coming from the real side of the economy are a little bit weak", he added.

Cipollone also noted that inflation is "decelerating faster" than anticipated. "So we will get all this information and reassess the situation on the next monetary policy meeting," he said.

Separately, Governing Council member Robert Holzmann emphasized that, while inflation is "on the right track," core inflation remains problematic. He attributed much of the recent inflation drop to lower energy costs but warned that the underlying inflation picture still "doesn't look so good." Holzmann, who backed the September rate cut, cautioned against assuming that further rate cuts are imminent.

JPY Pairs Approach Key Levels Rapidly

The USDJPY pair has pulled back after reaching its highest level since mid-August, dropping to around 148.00 before recovering slightly. The Japanese Yen gained strength due to comments from Japan’s Vice Finance Minister for International Affairs, which raised concerns about potential market intervention. Additionally, global risk sentiment shifted, with rising geopolitical tensions in the Middle East driving investors towards safer assets like the Yen. However, the US Dollar remains strong after a solid US jobs report on Friday, which lowered expectations of a large interest rate cut by the Federal Reserve. Traders are likely cautious ahead of key events this week, including the release of the Fed’s meeting minutes and important US inflation data. These factors will play a major role in guiding the next moves in the USDJPY pair. In the meantime, market participants will keep an eye on any statements from Fed officials for short-term trading opportunities.

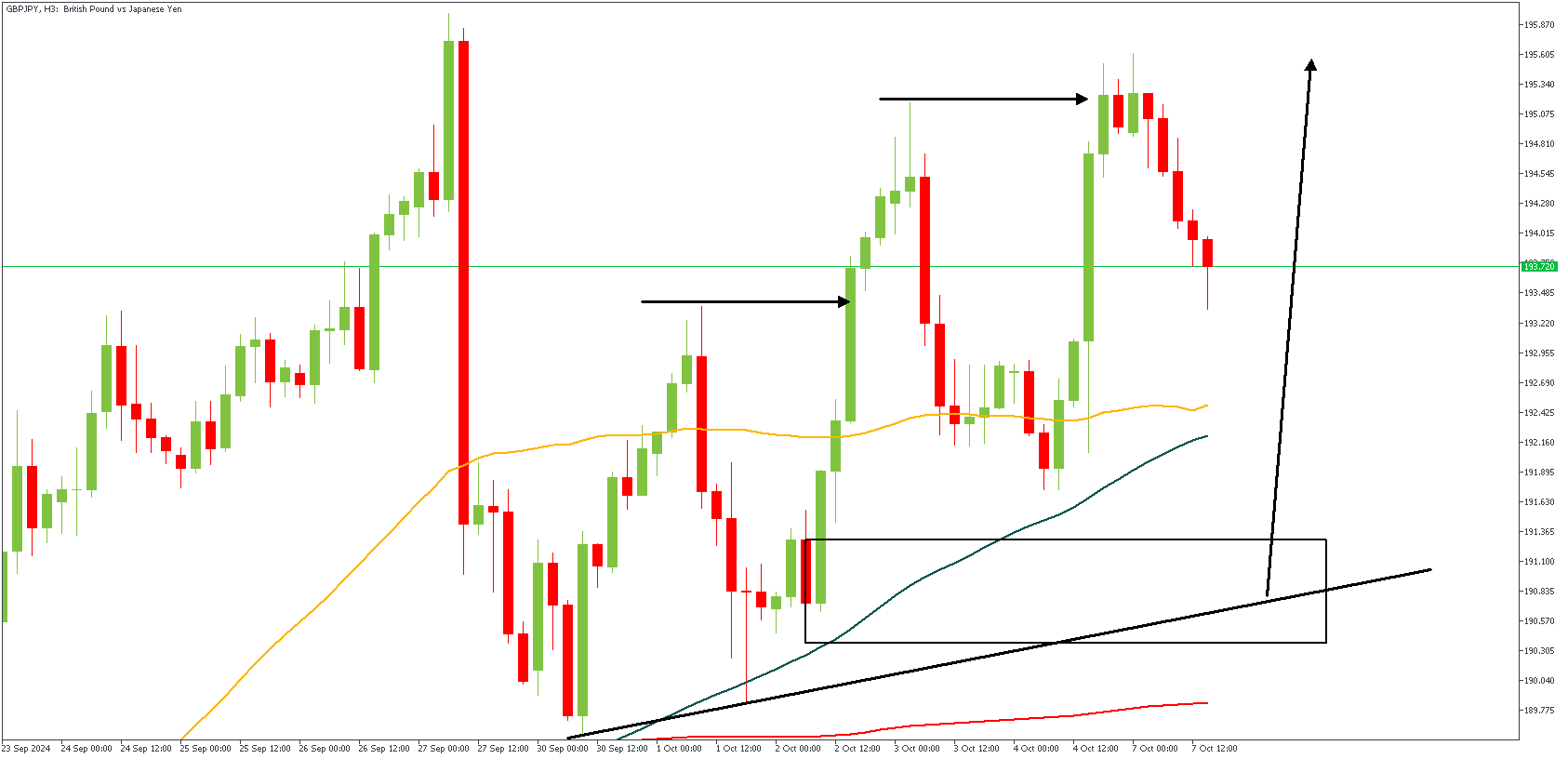

GBPJPY – H3 Timeframe

The 3-hour timeframe of GBPJPY on the currently shows the moving averages arranged in a bullish array. The trendline support is another viable confluence to consider. Additionally, we can see the demand zone, and the break of structure, all these point in favor of a bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 195.623

- Invalidation: 189.899

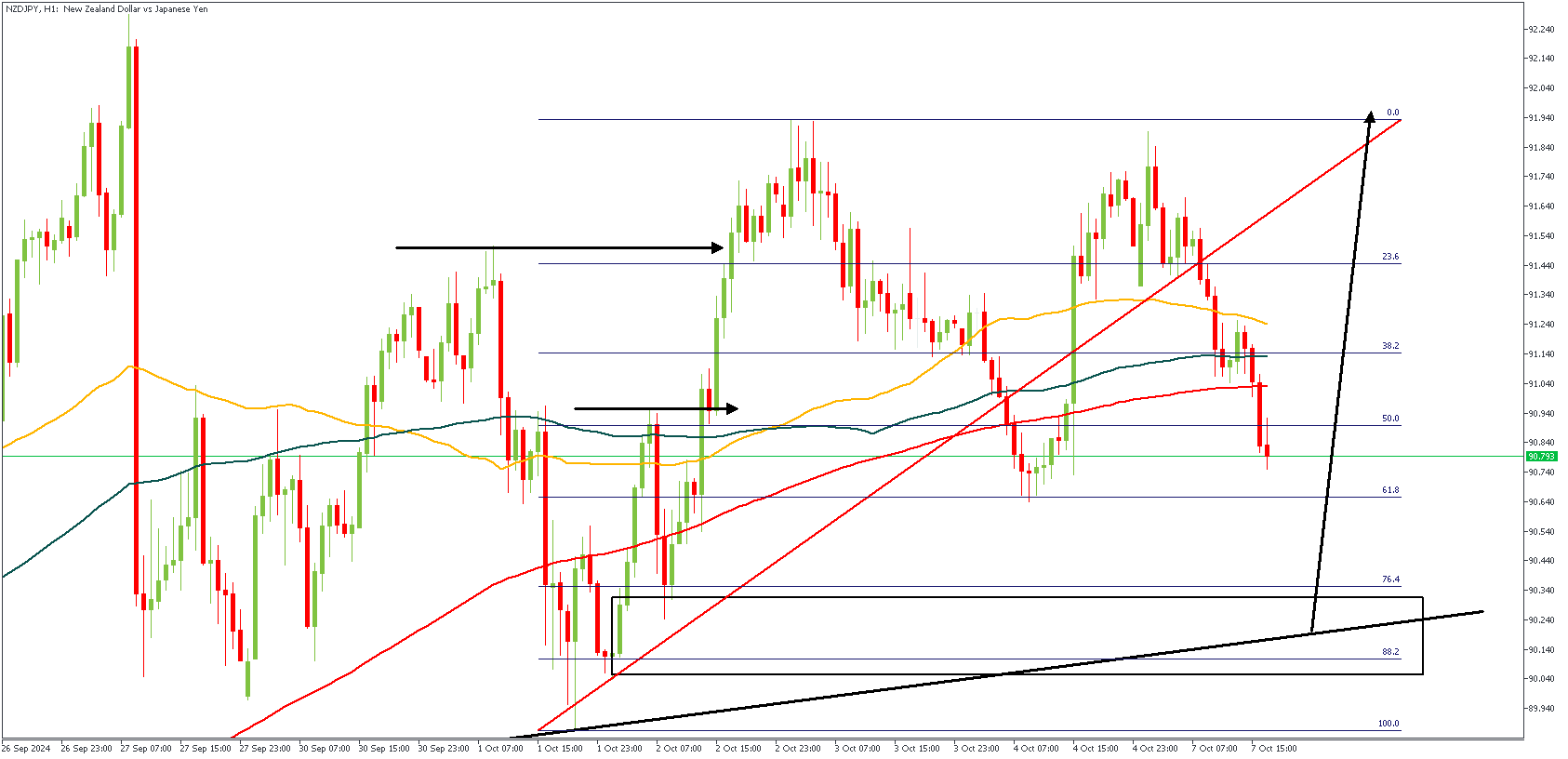

NZDJPY – H1 Timeframe

On the 1-hour timeframe of NZDJPY, we can see the recent break above the previous high. The break of structure is the initial basis of my bullish sentiment. The next confluence is the 76% of the Fibonacci retracement; since it overlaps a drop-base-rally demand zone. The trendline support lends the final clue in favor of the bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 91.970

- Invalidation: 89.838

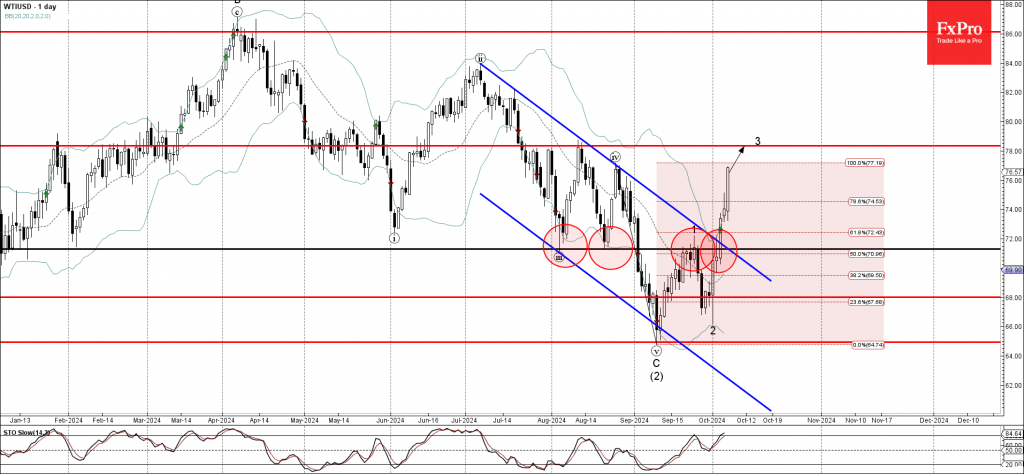

WTI Wave Analysis

- WTI under strong bullish pressure

- Likely to rise to resistance level 78.3

WTI crude oil under the strong bullish pressure after the price broke the resistance level 71.30 (former strong support from August) intersecting with the resistance trendline of the daily down channel from July.

The breakout pf the resistance level 71.30 accelerated the active short-term impulse wave 3.

Given the fact that the price is currently rising inside two impulse waves 3 and (3), WTI crude oil can be expected to fall rise further to the next resistance level 78.3, target for the completion of wave 3.