Sample Category Title

US ISM and Swiss Inflation on Today’s Menu

In focus today

In the afternoon, US ISM Services index is due for release. While the index has been volatile over the past years, flash PMIs released earlier signalled still solid growth in services sector activity in September.

In Switzerland, we get inflation data for September. Consensus expects a drop to 1.0% in headline inflation (from 1.1%) and core to remain steady at 1.1%. This should leave inflation in line with the SNBs Q3 forecast at 1.1%. In line with the SNB, we expect inflation to continue to edge lower into the lower end of the inflation target range of 0-2%.

Economic and market news

What happened overnight

In Japan, the newly appointed Prime Minister, Shigeru Ishiba, stated it is too early for additional rate hikes after meeting with Bank of Japan (BoJ) Governor Kazuo Ueda. Ueda echoed this, saying the BoJ will move cautiously on rate hikes, and board member Noguchi stressed the need to maintain a loose monetary policy. As of this morning, USD/JPY is trading around 146.85 after the dovish remarks.

What happened yesterday

In the US, ADP private sector employment growth for September exceeded expectations at 143k (cons: 120k), with the August figure being revised up to 103k (prior: 99k). Gains were broad-based occurring in leisure and hospitality (34k), construction (26k) and education and health services (24k). While on a cooling trend the past months, the reading suggest that labour market conditions remain solid. The print also points to a potentially decent labour market report on Friday, where we forecast NFP at 160k, slightly above consensus.

In the euro area, the unemployment rate remained at 6.4% in August as expected, with the number of unemployed persons declining by 94k. This indicates that the labour market remains historically strong. The decline was driven by a reduction in Spain, Italy and Greece, while the number of unemployed increased somewhat in Germany and France. Despite the low unemployment rate, more timely indicators show that recent employment growth has cooled or turned negative, reflecting an overall stagnant private labour market. Germany and France face the weakest labour markets, and largest risks of employment declines, while growth is expected to continue in Spain, Portugal and Greece.

ECB board member Isabel Schnabel noted that euro area inflation is increasingly likely to approach the 2% target amid signs of softening labour demand and further progress in disinflation. On the other hand, the Portuguese central bank chief Mario Centeno warned of the risk of undershooting its target, which could hinder economic growth.

In France, President Emmanuel Macron backed a temporary tax on the country's largest firms to support his new government's strategy. The French government unveiled plans for an EUR 60bn budget squeeze via spending cuts and tax hikes next year to curb the spiralling budget deficit and stabilise the country's financial outlook.

In Poland, as widely expected, the Monetary Policy Council kept its key policy rate steady at 5.75%.

In commodities space, the oil price remained bid amid concerns of supply disruptions from potential Israeli retaliation against Iran. Albeit OPEC+ is still weighing a December output increase, supported by recent price rises. Rising supply should help balance sentiment in the oil market amid escalation of the ongoing conflict in the Middle East.

Equities: Global equities were flat yesterday, with China being the regional exception, experiencing a sharp rise in Hong Kong. It is somewhat intriguing to observe both European and US equity markets being flat amidst substantial uncertainty across various parameters, including politics, geopolitics, macroeconomics, and monetary policy. In other words, all the elements are present that could potentially drive volatility higher as well as trigger significant movements in either direction for equities. The US job market data is a major catalyst in this context, and we will gain more insights on this front both today and tomorrow. In the US yesterday, the Dow closed up 0.1%, the S&P 500 slightly up by 0.01%, the Nasdaq increased by 0.1%, and the Russell 2000 decreased by 0.1%. The Chinese market's honeymoon appears to be over this morning, with markets down approximately 3% in Hong Kong. Conversely, in Japan, stocks are up more than 2% following dovish monetary statements, which have led to a renewed weakening of the yen. Futures in Europe and the US are lower this morning.

FI: There was a decent rebound in global bond yields and interest rates yesterday as 10Y US Treasury yields rose some 5bp and the curve steepened between 2Y and 10Y as well as 2Y and 30Y on the back of better-than-expected US labour market data and rising oil prices. We have seen a similar move in European government bond yields where yields rose, and the curves steepened from the long end. Furthermore, the Bund ASW-spread tightened once again.

FX: Risky assets saw some stabilisation despite continued geopolitical stress. Oil prices remained bid, although Brent closed some 2% below the intraday high. NOK/SEK pushed above 0.97 once more and the yen had a rough session following dovish remarks from new PM Ishiba, with USD/JPY rising 2% on the day. NBP left rates unchanged amid accelerating inflation with EUR/PLN trading close to our 1-3M target of 4.30.

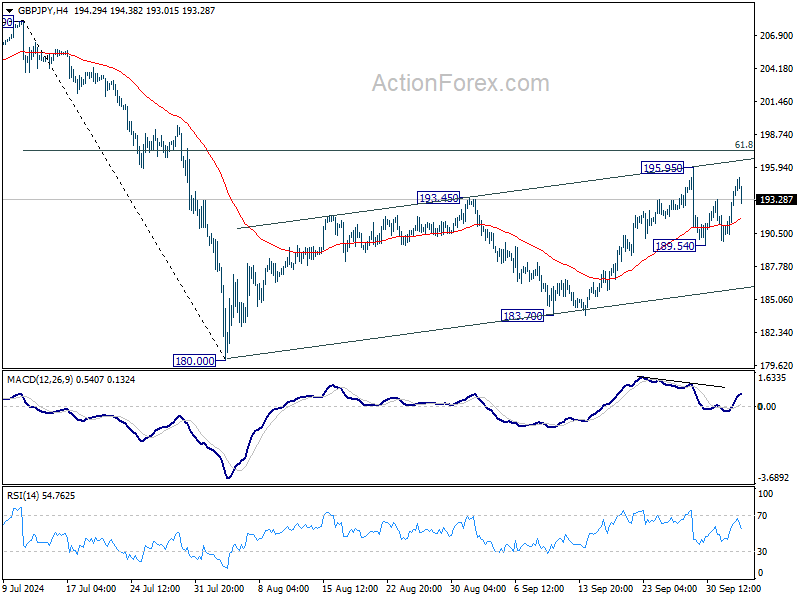

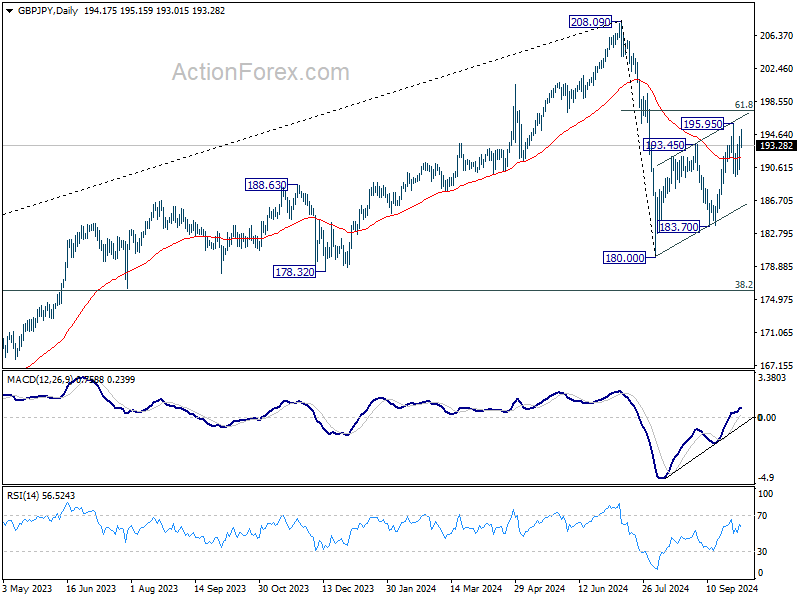

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.68; (P) 193.05; (R1) 195.69; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, below 189.54 will bring deeper fall to 183.70 support. On the upside, above 195.95 will resume the rise from 180.00 to 61.8% retracement of 208.09 to 180.00 at 197.35.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

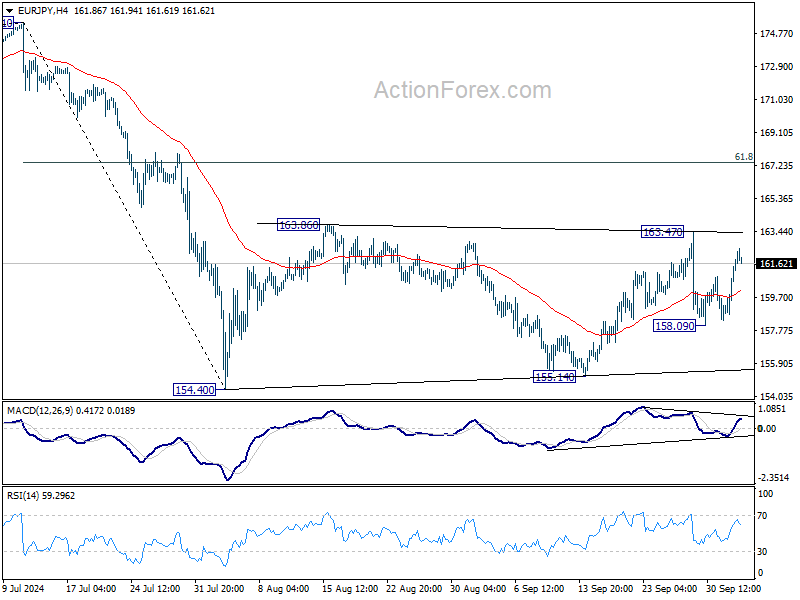

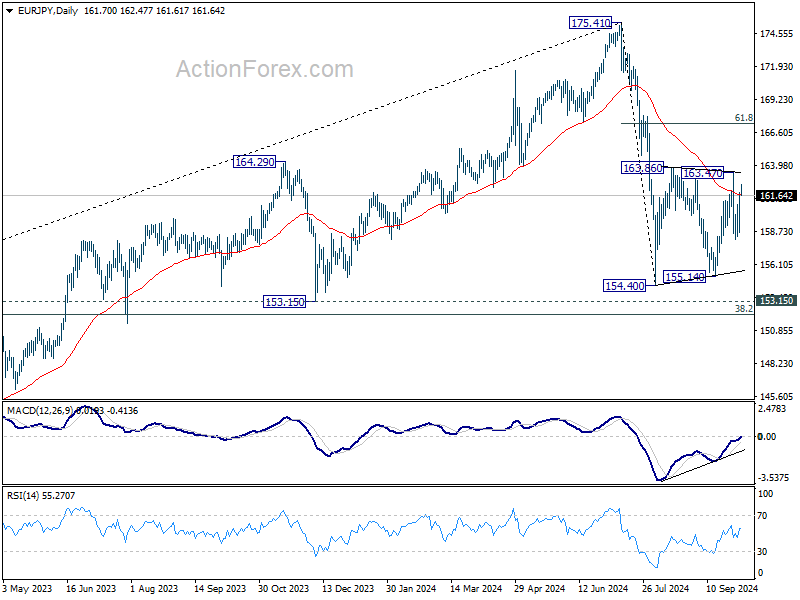

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.70; (P) 160.79; (R1) 162.88; More....

Intraday bias in EUR/JPY remains neutral for the moment. Risk is mildly on the downside as long as 163.47 resistance intact. Below 158.09 will bring deeper fall back to 154.40/155.14 support zone. ON the upside, though, break of 163.47 will resume the rise from 155.14 to 61.8% retracement of 175.41 to 154.40 at 167.38.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

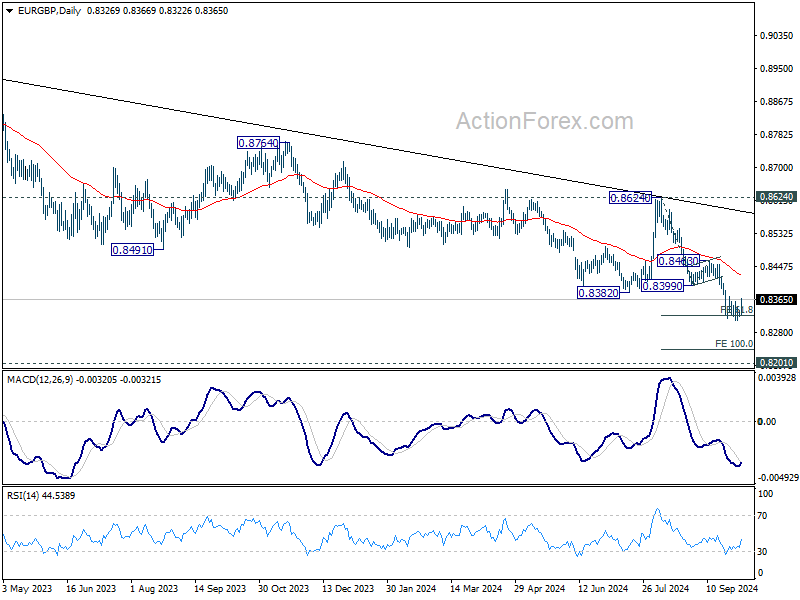

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8319; (P) 0.8329; (R1) 0.8335; More...

Intraday bias in EUR/GBP is turned neutral with current recovery. On the upside, firm break of 0.8370 resistance will indicate short term bottoming at 0.8309. Intraday bias will be turned back to the upside for 0.8399/8463 resistance zone. On the downside, firm break of 0.8309 will resume the fall from 0.8624 to 100% projection of 0.8624 to 0.8399 from 0.8463 at 0.8237 next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.

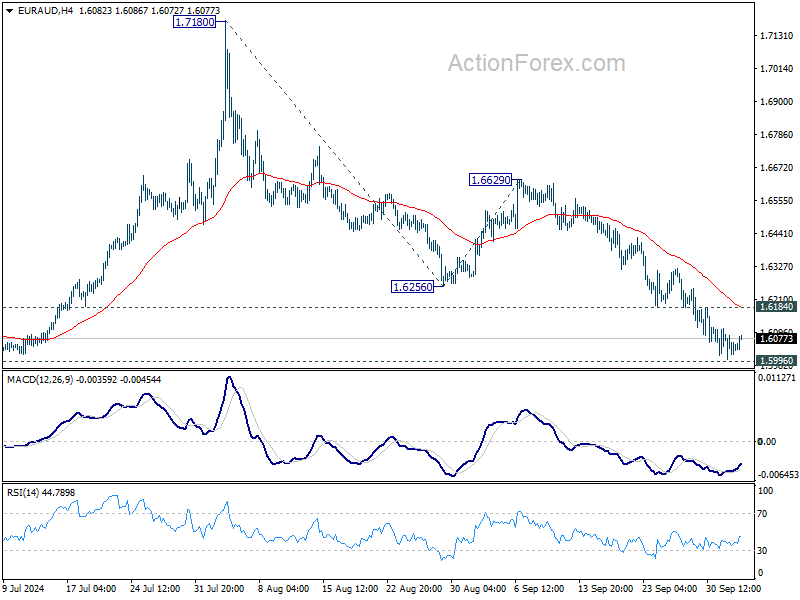

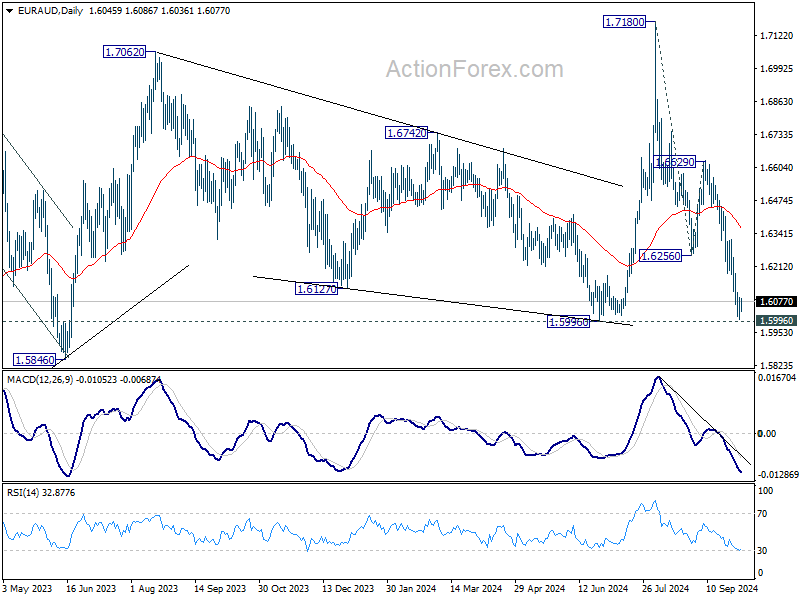

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6001; (P) 1.6046; (R1) 1.6089; More...

Intraday bias in EUR/AUD Remains neutral for the moment. Strong rebound from 1.5996 support, followed by 1.6184 minor resistance, will indicate short term bottoming. Intraday bias will be turned back to the upside for stronger rebound. However, decisive break of 1.5996 will carry larger bearish implications. Next target will be 100% projection of 1.7180 to 1.6256 from 1.6629 at 1.5705.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still in favor to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed.

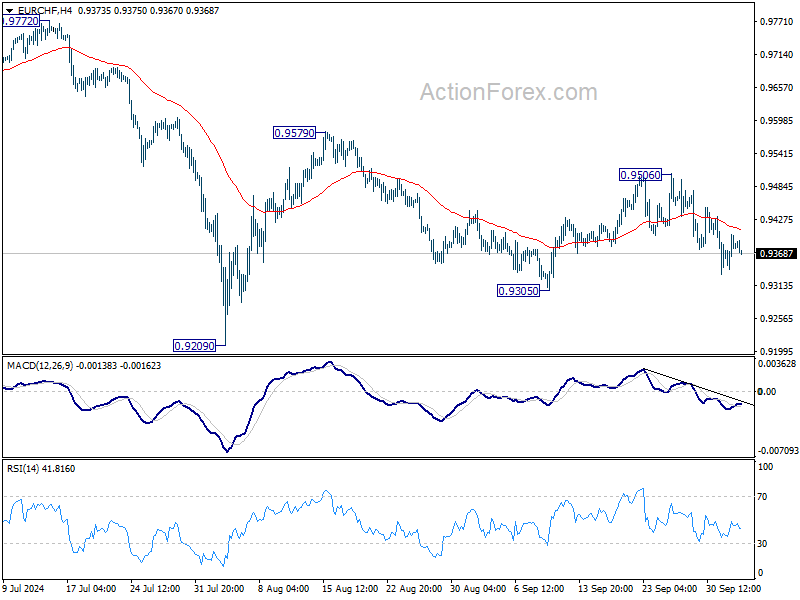

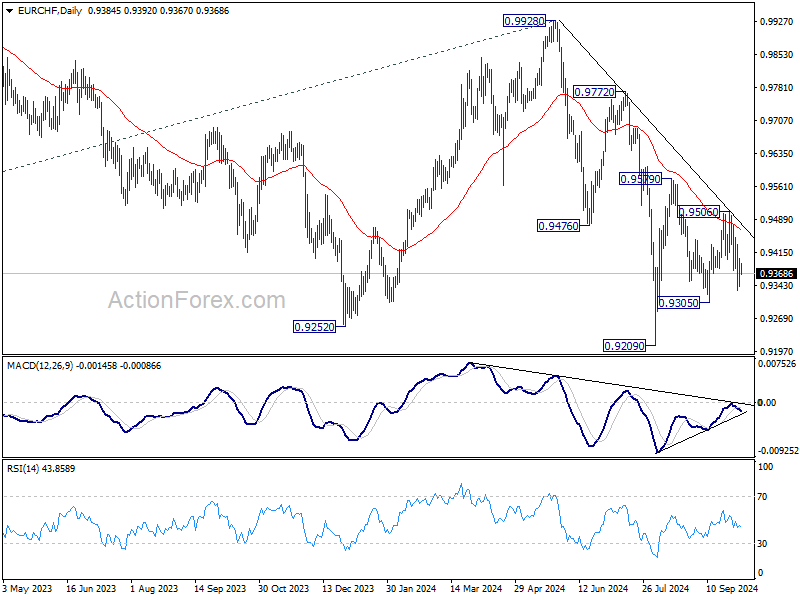

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9352; (P) 0.9377; (R1) 0.9413; More....

No change in EUR/CHF's outlook and intraday bias stays neutral. On the downside, break of 0.9305 will resume the fall from 0.9579 to retest 0.9209 low. On the upside, above 0.9506 will resume the rebound from 0.9305 to 0.9579 resistance.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

EURUSD Looking for Expanded Flat Elliott Wave Correction

Short Term Elliott Wave View in EURUSD suggests that cycle from 4.16.2024 low is in progress as a 5 waves impulsive Elliott Wave structure. Rally to 1.12 ended wave (3) of the impulse. Pullback in wave (4) is now in progress with internal subdivision as an expanded Flat structure. Down from 8.26.2024 high, wave A ended at 1.10. Rally in wave B unfolded as a double three Elliott Wave structure. Up from wave A, wave ((w)) ended at 1.1189 and pullback in wave ((x)) ended at 1.1065. Wave ((y)) higher ended at 1.1213 which completed wave B.

The pair turned lower in wave C with subdivision as a 5 waves impulse. Down from wave B, wave ((i)) ended at 1.1119 and rally in wave ((ii)) ended at 1.1209. Internal subdivision of wave ((ii)) unfolded as a double three where wave (w) ended at 1.1189 and wave (x) ended at 1.1122. Wave (y) higher ended at 1.1209 which completed wave ((ii)). Pair resumed lower in wave ((iii)) towards 1.1043 and wave ((iv)) ended at 1.1082. Expect wave ((v)) of C of (4) to complete soon and pair to turn higher in 3 waves at least.

EURUSD 60 Minutes Elliott Wave Chart

EURUSD Elliott Wave Video

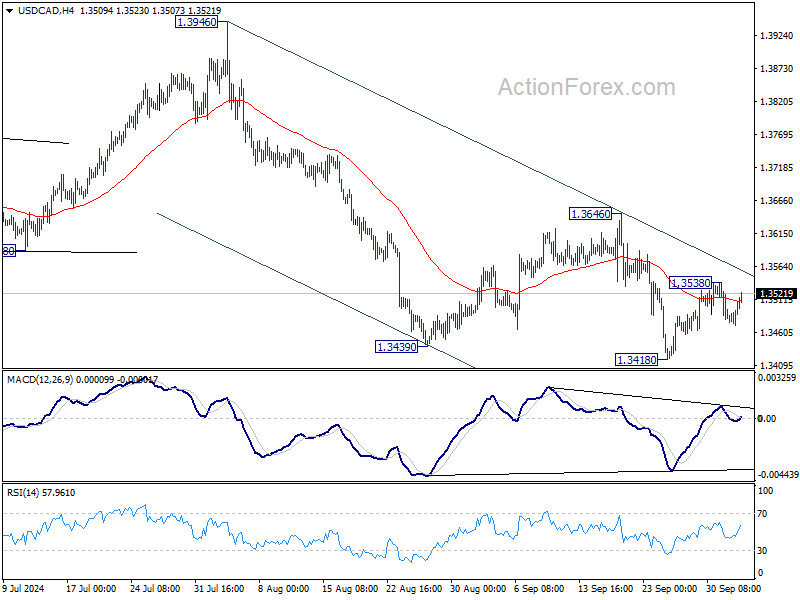

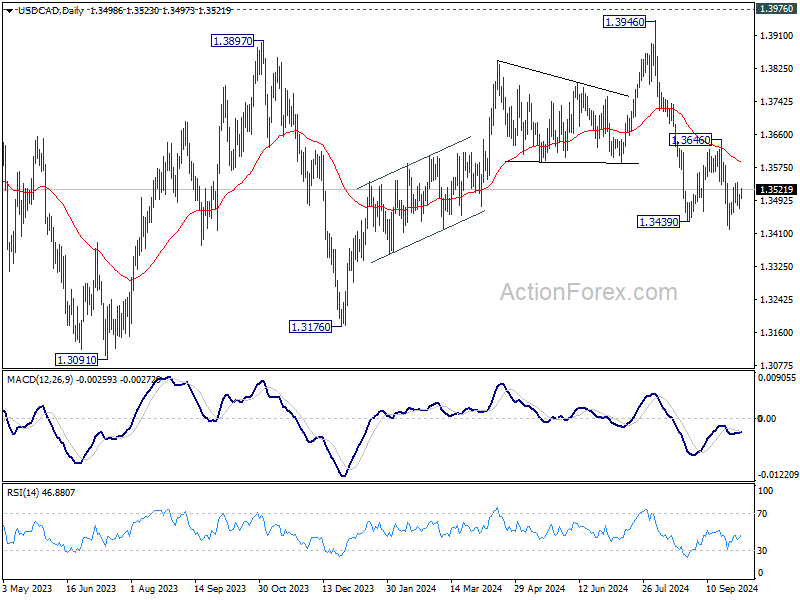

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3480; (P) 1.3495; (R1) 1.3517; More...

Intraday bias in USD/CAD remains neutral first. On the upside, above 1.3538 will resume the rebound from 1.3418 to 1.3646 resistance. ON the downside, firm break of 1.3418 will resume whole decline from 1.3946 towards 1.3176 key support.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

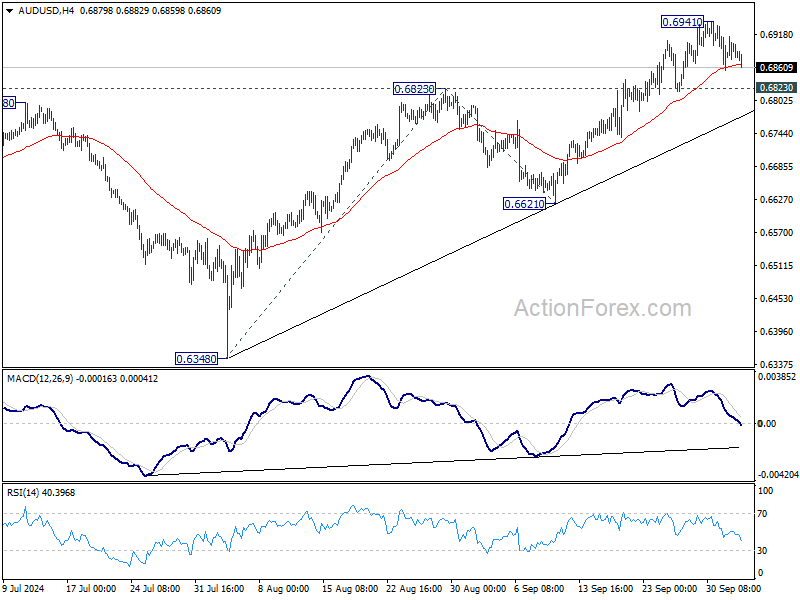

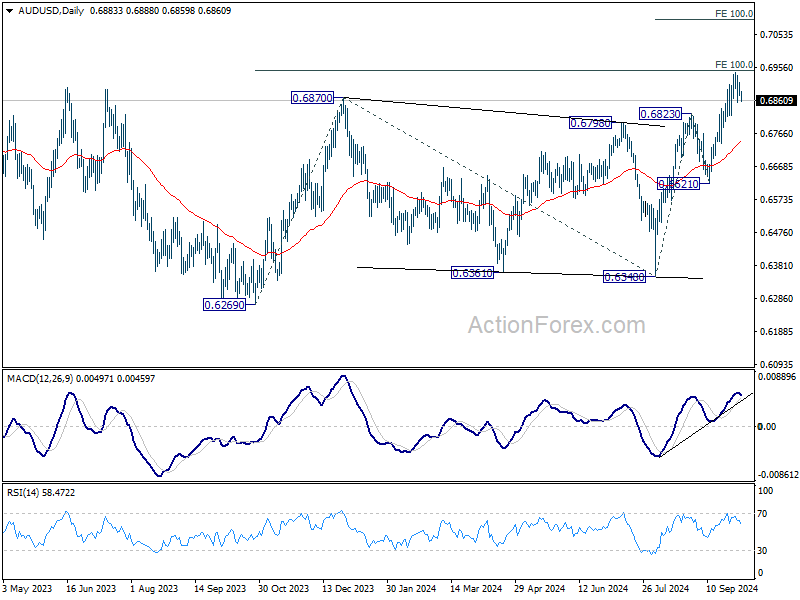

AUD/USD Daily Report

Daily Pivots: (S1) 0.6869; (P) 0.6892; (R1) 0.6909; More...

Intraday bias in AUD/USD remains neutral for consolidation below 0.6941. Further rally is expected as long as 0.6823 resistance turned support holds. Above 0.6941 will resume the rise from 0.6348 to 100% projection of 0.6348 to 0.6823 from 0.6621 at 0.7096. However, firm break of 0.6823 will turn bias to the downside for deeper pullback to 55 D EMA (now at 0.6742).

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

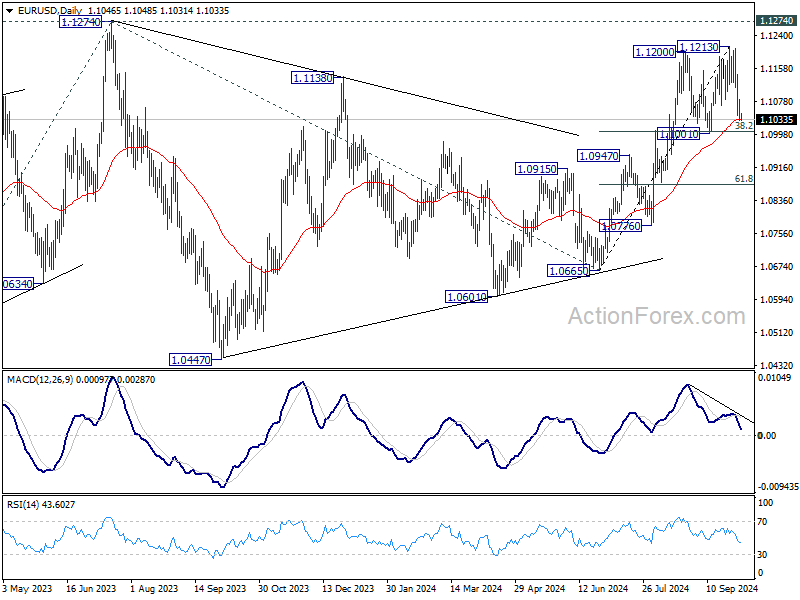

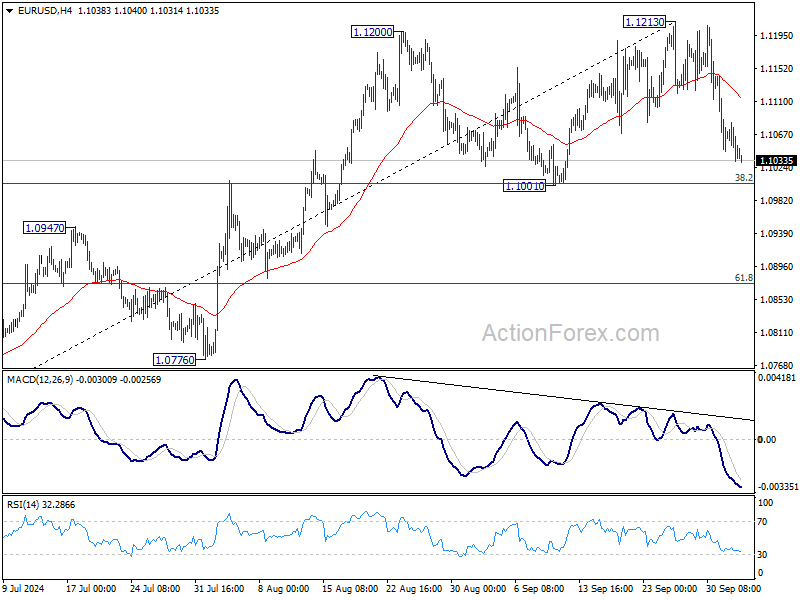

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1024; (P) 1.1054; (R1) 1.1074; More....

Intraday bias in EUR/USD remains neutral and further rally is still expected 1.1001 cluster support holds (38.2% retracement of 1.0665 to 1.1213 at 1.1004). Break of 1.1213 will target 1.1274 high. However, decisive break of 1.1001/4 will confirm near term bearish reversal. Intraday bias will be turned back to 61.8% retracement at 1.0874.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.