Sample Category Title

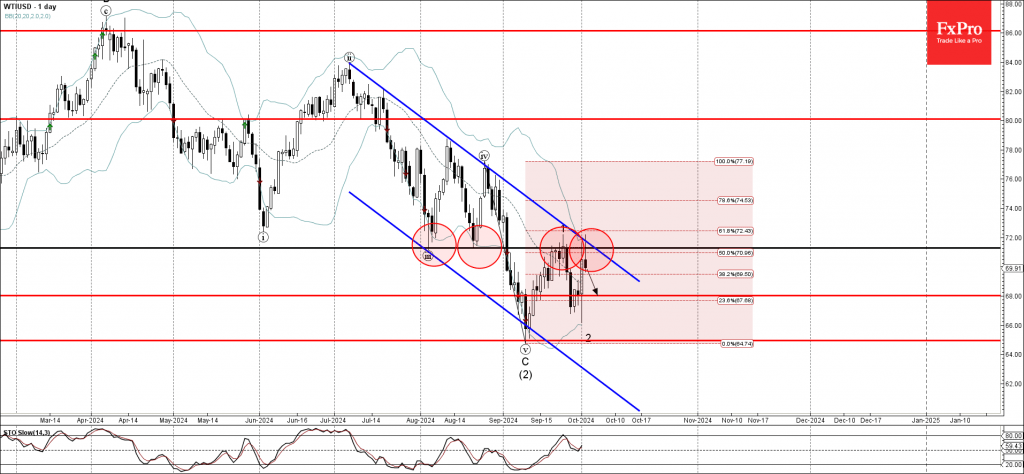

WTI Wave Analysis

- WTI reversed from pivotal resistance level 71.30

- Likely to fall to support level 68.00

WTI crude oil recently reversed down from the pivotal resistance level 71.30 (former double bottom from August) intersecting with the upper daily Bollinger Band and the resistance trendline of the daily down channel from July.

The downward reversal from the resistance level 71.30 is likely to form the daily Japanese candlesticks reversal pattern Shooting Star.

Given the clear daily downtrend, WTI crude oil can be expected to fall further to the next support level 68.00.

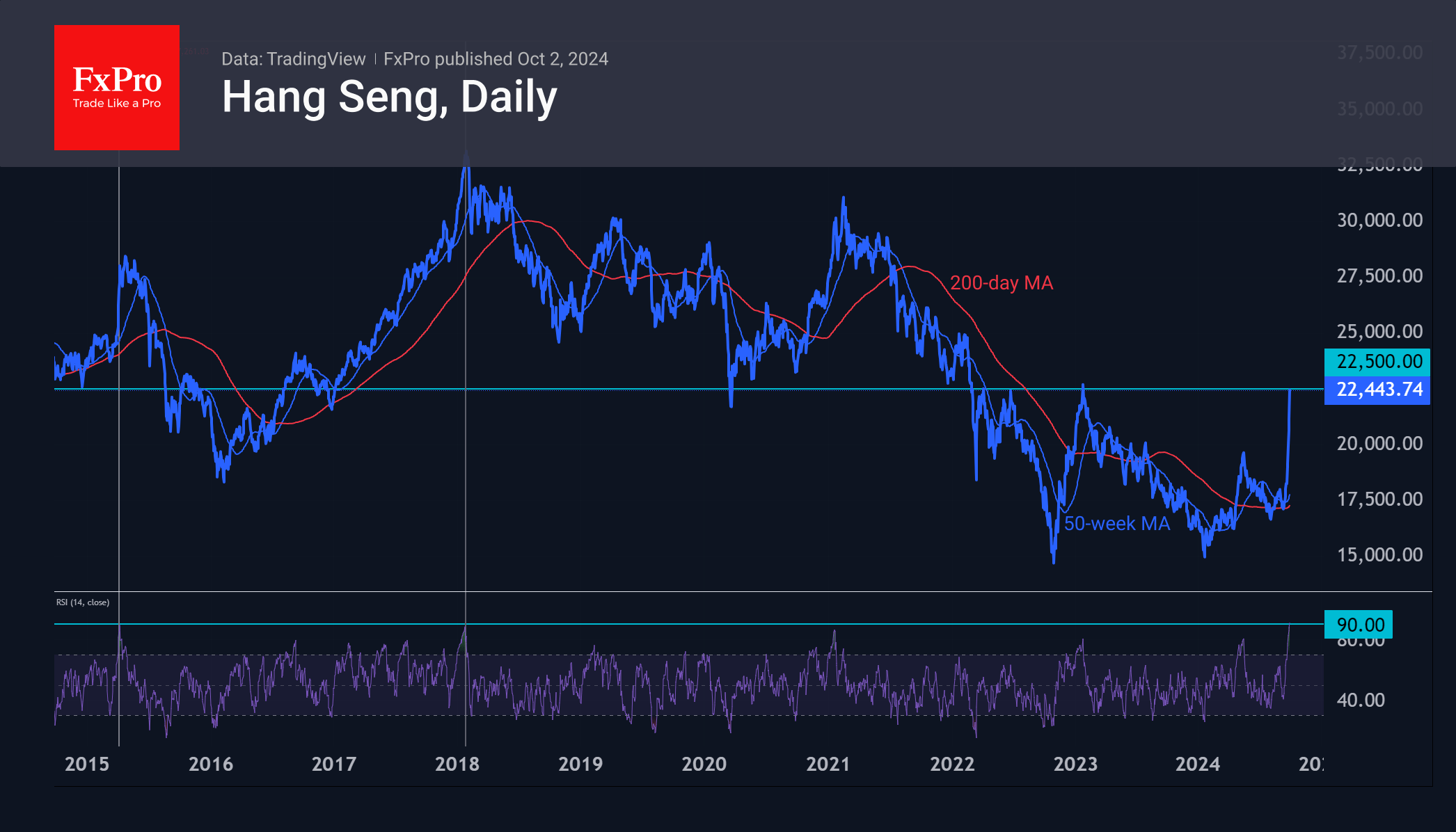

Hang Seng Is Too Hot Now, but Long-Term Attractive

The Chinese stock market is closed for a national holiday, but futures and ETFs are trading and are on another strong run today. The Hang Seng Index is up 9.6% from its close on 30 September (there was no trading on Tuesday), the second strongest rise since the surge on 16 March 2022. Then it rebounded after a setback, but now it is an acceleration of the rally, taking the index cumulatively up 34% from the 11 September lows.

Wednesday’s rally is the result of a short squeeze, as it comes at the close of the main Chinese markets and is not fuelled by optimism on global exchanges. On the contrary, global markets have moved away from risk in recent days, and the S&P 500 has been trading near the top for almost a week.

On a daily timeframe, RSI is approaching 91, the highest reading since 1987. The market was almost as hot in recent years in January 2018 and April 2015. In both cases, it fell for almost a year.

While this is a different case, and the multi-year sell-off in Chinese equities should be considered, the current overbought situation on daily timeframes could still be a good reason to shake out positions locally when the major Chinese markets open on 8 October.

Moreover, at current levels, the Hang Seng is approaching the 22500-resistance area, which has been in place since March 2022, and this will strengthen the resistance to growth in the short term.

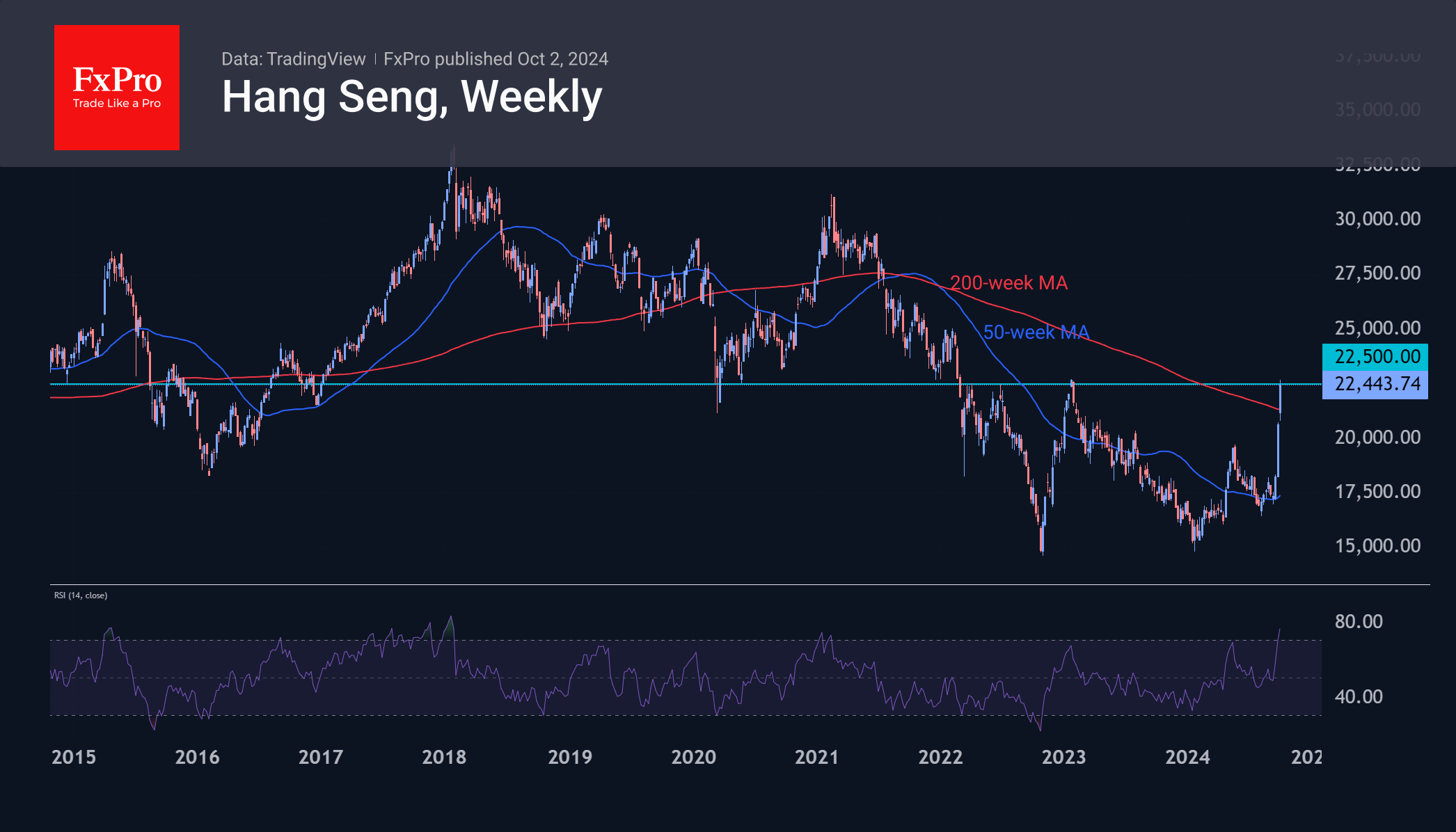

However, one cannot overlook the more global picture emerging on the weekly timeframe. This week, the price has broken above the 200-week moving average after retreating from the 50-week average in early September.

This could potentially attract more capital and provide fuel for further upside. The RSI is also moving into overbought territory (above 70), but past examples suggest further upside, and a sharp drop to levels below 70 should be seen as a correction signal.

In the long term, a successful break of 22500 would open the door to 25000 and on to 30000, where we have seen major portfolio corrections in the past.

EUR/USD Update – Euro Vulnerable on Rate Cut Bets and Safe Haven Flows

- The Euro’s appeal has diminished due to expectations of ECB rate cuts, fueled by softer economic data and dovish policymaker comments.

- The US Dollar is gaining strength amid Middle East tensions, potentially attracting safe-haven flows.

- EUR/USD has formed a double top pattern at 1.1200 and is facing immediate support at 1.1000.

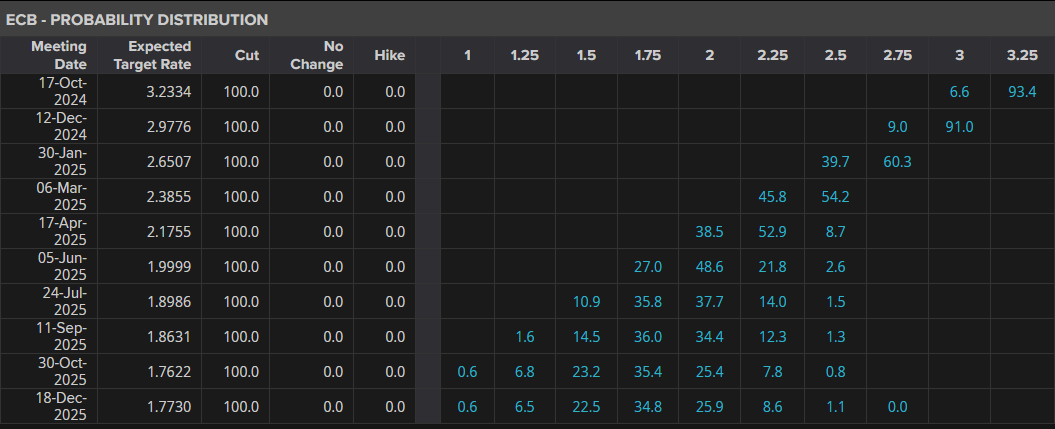

The Euro has lost some of its appeal over the past two weeks as softer data has increased the likelihood of an October rate cut. ECB Policymakers have struck a dovish tone as well with German Economy Minister Robert Habeck stating rate cuts are coming too slowly for his liking.

This should come as no surprise to anyone who has been following developments around the German economy over the last 12 months. Europe’s most industrialized economy which is usually a driver of growth is struggling.

Yesterday’s inflation data from the EU has ramped up rate cut expectations which means Minister Habeck may soon get his wish. This was followed by a UBS warning today that the ECB may have to drop rates to the 1-1.5% range if growth does not improve in the coming quarters. As many analysts have suggested, the ECB may pivot its focus to growth now that inflation appears out of the way.

Markets are now pricing in around six consecutive rate cuts from the ECB starting in October. A 25 bps cut in October is now priced at around 93% which is a stark increase from where we were a month ago.

Source: LSEG

This could not come at a worse time for the Euro as the DXY has begun a recovery and may also benefit from some safe haven flows. The increasing tension in the Middle East could reignite some safe haven appeal in the US Dollar and thus weigh further on EUR/USD.

There is of course still some data ahead this week with the NFP report on Friday likely to lead to some volatility as well. Markets have shifted their focus in the US to the Labor market and thus the importance of Friday’s release. If the US unemployment rate remains steady I could see EUR/USD revisiting the 1.1000 handle and possibly lower.

Technical Analysis

EUR/USD has been on a steady move lower since forming a double top pattern at the key 1.1200 handle. The move has been swift and this leaves the door open for a potential retracement before the next leg to the downside.

Immediate support is at the 1.1000 psychological level with a break below opening up a retest of 1.0950. The 100-day MA rests at 1.09260 and would be the next hurdle to pay attention to.

Conversely, a bullish move from here first needs to gain acceptance back above the 1.1100 handle before the recent highs and double at 1.1200 become an area of focus.

The NFP report on Friday could be a catalyst for a significant move in either direction while further escalation in the Middle East could increase the US Dollars’ haven appeal and push EUR/USD below the 1.1000 handle.

EUR/USD Daily Chart, October 2, 2024

Source: TradingView.com

Support

- 1.1000

- 1.0950

- 1.0900

Resistance

- 1.1100

- 1.1200

- 1.1300

Sunset Market Commentary

Markets

Oil markets show some of the biggest swings today. Brent rose as much as 3.5% before paring gains to 2.7% currently in response to Iran’s missile attack on Israel yesterday. Israeli PM Netanyahu vowed to retaliate and singled out Iran’s oil infrastructure as potential target. As the tit-for-tat strategy intensifies and geopolitical tensions flare up so do fears for a supply disruption. The black gold is currently trading north of $75, compared to $70 less than two days ago. Oil prices are boosting the likes of the Norwegian krone on currency markets. The NOK outperforms G10 peers with EUR/NOK easing to 11.66. First support in the pair approaches around 11.6. On the other side of the FX spectrum is the Japanese yen. JPY slips more than 1%, hurling USD/JPY back above 145. Japan’s freshly appointed prime minister Shigeru Ishiba sat down with Bank of Japan governor Ueda today. Ishiba said in the wake of that meeting that he doesn’t “think that the environment is ready for an additional rate hike”. Whatever little was still priced in for October is now all but gone. Not much happens in between both extremes. EUR/USD is holding a tight sideways 1.105/1.108 range. Some minor dollar strength kicked in after ADP jobs data. The September report topped estimates, coming in at 143k vs 125k expected, following the 103k in August. ADP said “job creation showed a widespread rebound after a five-month slowdown. Only one sector, information, lost jobs. Manufacturing added jobs for the first time since April.” Year-over-year pay gains eased slightly last month, to 4.7%. The small beat is enough to push DXY a tad higher towards 101.47. US Treasuries extended previous losses. The 2-yr yield even printed a small gap following the release of what is usually considered a second tier data point, suggesting perhaps the front end gets a bit crowded with Fed easing bets. Net daily changes vary between 4.5 (2-yr) and 8.2 bps (30-yr). German Bund yields follow closely with gains ranging from +3.5 (2-yr) to +7.5 bps (10-yr). Yesterday’s break of the 10-yr below the August low doesn’t get confirmed today and the failed test of the 2-yr below 2% now triggers some return action higher, even as Latvian governing council member of the ECB Kazaks today greenlighted market expectations for an October cut. The usually hawkish policymaker said “recent data clearly point in the direction of a cut”, adding that “the direction for rates also after October [December] is going to be down”. Both are fully discounted.

News & Views

The Hungarian government debt management agency, AKK, updated this year’s funding plan after the government on Monday reported government deficit and debt levels. AKK won’t change its finance plan because it has a sufficient cash buffer to deal with a higher government cash-flow deficit. That’s mainly because of higher than expected HUF institutional bond (96% of HUF 2481bn target) and T-bill issuance in the first three quarters of the years. By the end of September 2024, 77% of the 2024 annual funding plan (HUF 717bn vs HUF 9277bn target) was met. The average term-to-maturity of central government debt was 5.9y at the end of September, a slight decline from 6y at the end of June but still above the 5.5y benchmark target. Contrary to previous plans, and with particular regard to the 30% FX debt share benchmark, there will be neither an FX issuance in the Chinese market, nor a private placement in 2024, which could result in a lower FX debt ratio at the end of the year. The forint suffers in toughening risk climate with EUR/HUF heading to the key resistance and psychological level of 400.

The BoE’s Financial Policy Committee in its quarterly assessment concludes that risks to UK financial stability are broadly unchanged since the June report. Significant financial market and global vulnerabilities remain. The spike in volatility across global markets early August was short-lived. However, the extent of the moves, in response to relatively limited economic news, illustrates the potential for vulnerabilities. Due to a quick rebound thereafter, valuations of equities in particular are seen as having returned to stretched levels. Markets remain susceptible to a sharp correction, which could affect the cost and availability of credit. With respect to the domestic market, there have been further signs of easing in UK credit conditions, reflecting improvements to the macroeconomic outlook. UK household and corporate borrowers remain resilient to the higher interest rate environment although some highly leveraged firms remain under pressure. The UK banking system is seen as being in a strong position to support households and businesses, even if economic and financial conditions were substantially worse than expected.

Graphs

EUR/PLN nears recent highs as the zloty awaits NBP governor Glapinski’s presser following another status quo decision

German 2-yr yield’s test of the 2% barrier failed, triggering some return action higher in a broader core bond decline today

Brent ($/b) extends recent rally as rising geopolitical tensions poses risks for supply

EuroStoxx 50’s topside test failed, edging back below the 5k barrier

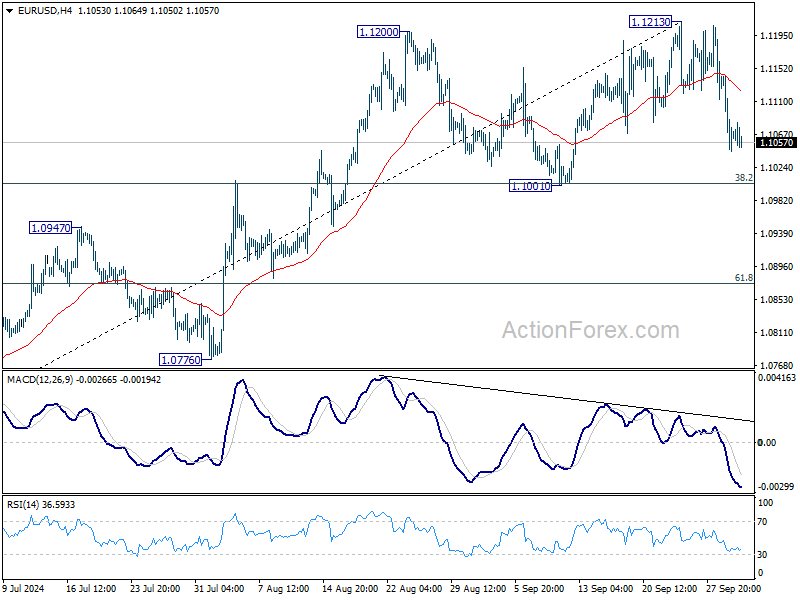

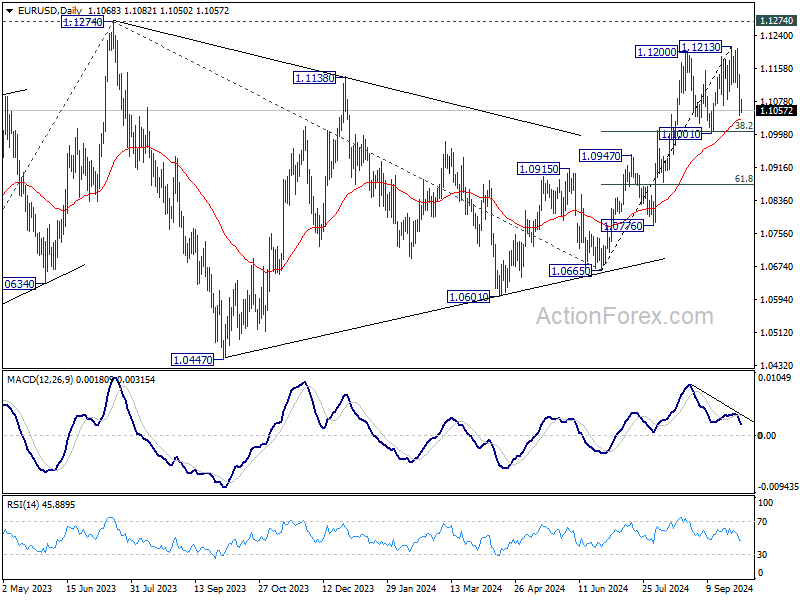

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1028; (P) 1.1086; (R1) 1.1127; More....

No change in EUR/USD's outlook and intraday bias stays neutral for consolidations below 1.1213 short term top. Further rally is still expected 1.1001 cluster support holds (38.2% retracement of 1.0665 to 1.1213 at 1.1004). Break of 1.1213 will target 1.1274 high. However, decisive break of 1.1001/4 will confirm near term bearish reversal.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.

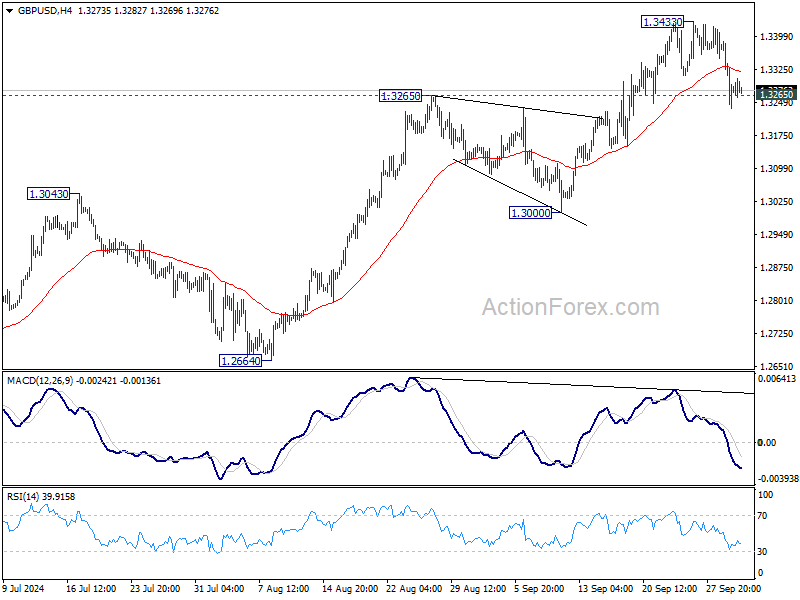

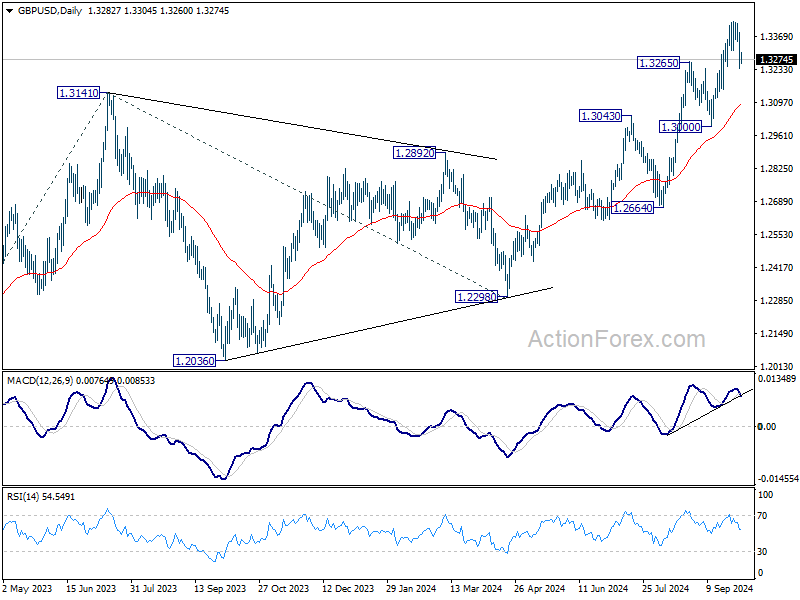

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3218; (P) 1.3304; (R1) 1.3370; More...

Outlook in GBP/USD remains unchanged and intraday bias stays neutral at this point. Another rally is still in favor as long as 1.3265 resistance turned support holds. Above 1.3433 will resume the rise from 1.2298. However, firm break of 1.3265 will confirm short term topping, and turn bias back to the downside for 1.3000 support instead.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. For now, outlook will stay bullish as long as 1.3000 support holds, even in case of deep pullback.

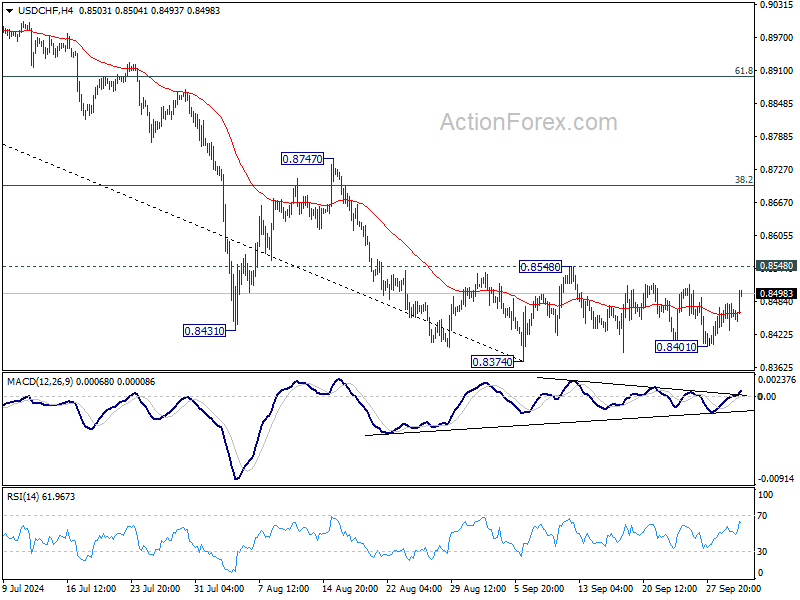

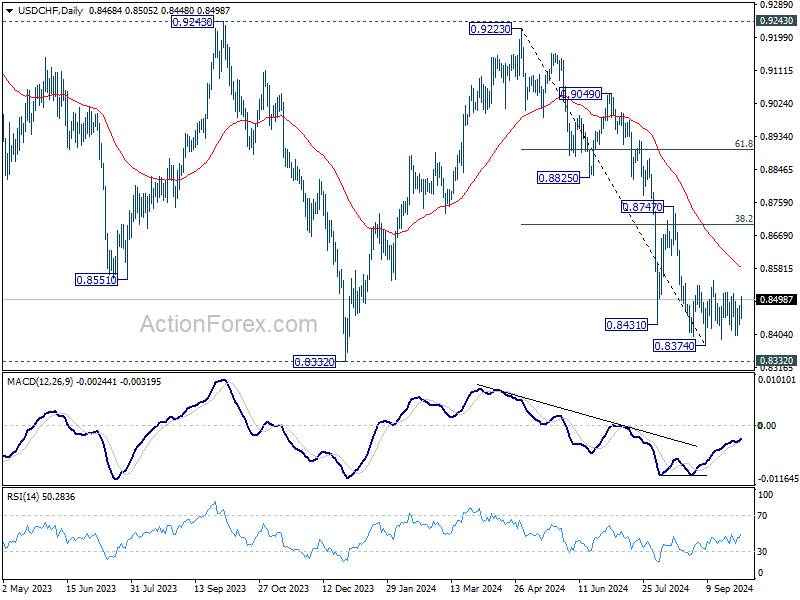

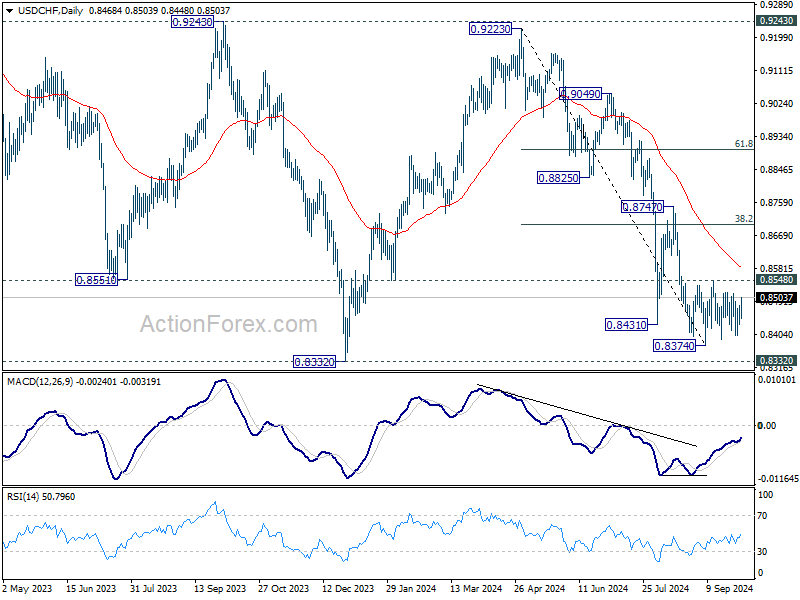

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8438; (P) 0.8460; (R1) 0.8488; More…

USD/CHF is still bounded in range trading and intraday bias stays neutral for the moment. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. Nevertheless, firm break of 0.8548 will argue that it's correcting whole fall from 0.9223. Intraday bias will be back on the upside for 38.2% retracement of 0.9223 to 0.8374 at 0.8698 at least.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

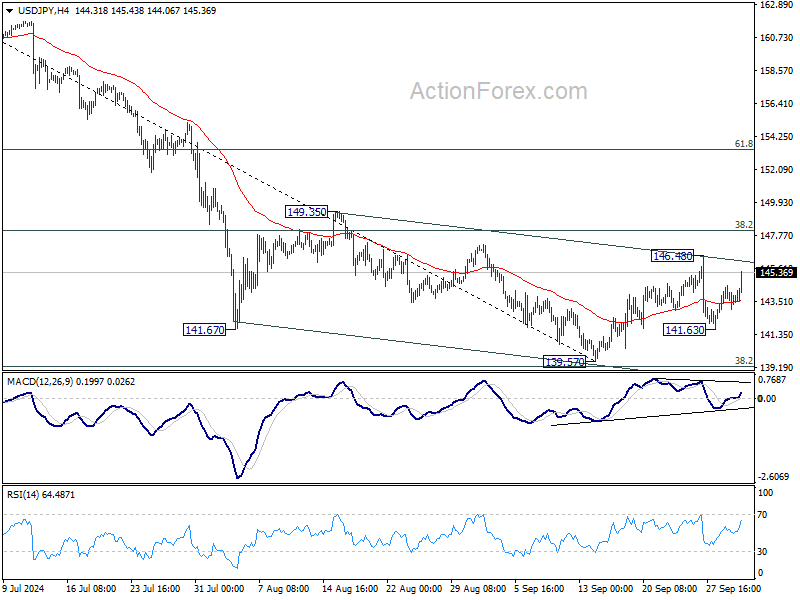

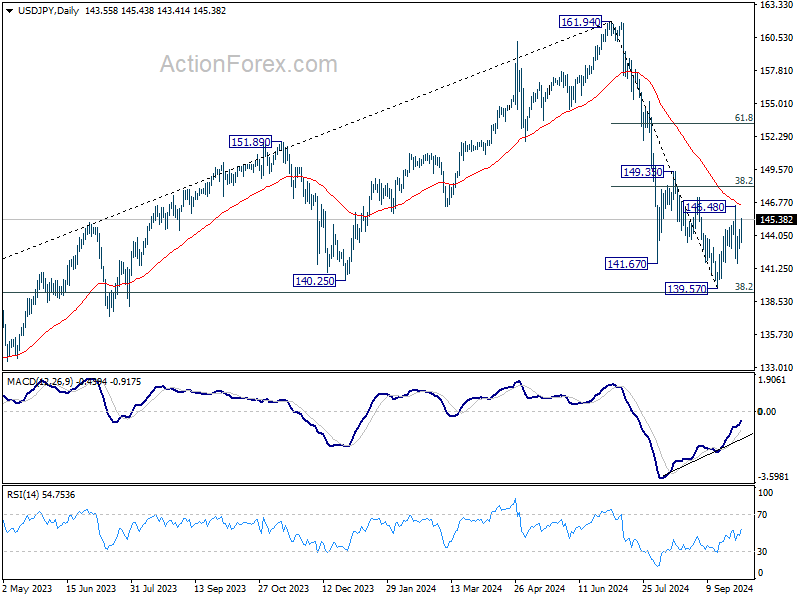

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.85; (P) 143.69; (R1) 144.41; More...

USD/JPY rebounded strongly today and focus is now on 146.48 resistance. Firm break there will resume the rebound from 139.57 to 38.2% retracement of 161.94 to 139.57 at 148.11. On the downside, below 141.63 will turn bias to the downside for 139.57 support. But in this case, strong support could be seen again from 139.26 fibonacci level to bring rebound.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Weakens as Ishiba Softens Rate Hike Stance, US Yields Rise

Japanese Yen weakened notably in early US session, reacting to rising US Treasury yields, which were boosted by stronger-than-expected US ADP job data. Adding to Yen’s decline, Japan’s new Prime Minister, Shigeru Ishiba, who was initially perceived as a monetary hawk, has softened his stance on interest rate hikes. After meeting with BoJ Governor Kazuo Ueda, Ishiba said he does not believe it is the right time for the BoJ to raise rates further, dampening expectations of another rate hike in December.

Reinforcing this dovish tone, Japan's newly appointed Economy Minister, Ryosei Akazawa, emphasized in a press conference that Japan's "top priority" is to ensure a "complete exit from deflation." Akazawa further clarified that Ishiba’s previous comments on monetary Japanese Yen weakened notably in early US session, reacting to rising US Treasury yields, which were boosted by stronger-than-expected US ADP job data. Adding to Yen’s decline, Japan’s new Prime Minister, Shigeru Ishiba, who was initially perceived as a monetary hawk, has softened his stance on interest rate hikes. After meeting with BoJ Governor Kazuo Ueda, Ishiba said he does not believe it is the right time for the BoJ to raise rates further, dampening expectations of another rate hike in December.policy normalization were contingent on several "conditions," signaling that any rate hikes would depend on broader economic circumstances.

Elsewhere, Dollar has strengthened against both Yen and Swiss Franc but is struggling to extend its recovery against other major currencies. Traders are adopting a cautious stance, waiting for developments in the Middle East and key US economic reports, including ISM Services PMI and non-farm payrolls data, which could impact sentiment and influence Fed's policy outlook.

In terms of performance today, Australian Dollar is leading the market, followed by New Zealand Dollar and Canadian Dollar. Yen is the worst performer, followed by Swiss Franc and Dollar, while Euro and British Pound are trading in middle positions.

Techinically, USD/CHF is worth a watch in the next 24 hours given then Swiss CPI data will be released tomorrow. Break of 0.8548 resistance will suggest that rebound from 0.8374 is at least correcting the whole decline from 0.9223. In this case, further rally should be seen to 38.2% retracement of 0.9223 to 0.8374 at 0.8698 at least.

In Europe, at the time of writing, FTSE is up 0.11%. DAX is down -0.58%. CAC is down -0.08%. UK 10-year yield is up 0.099at 4.043. Germany 10-year yield is up 0.065 at 2.106. Earlier in Asia, Nikkei fell -2.18%. Hong Kong HSI rose 6.20%. China was on holiday. Singapore Strait Times rose 0.10%. Japan 10-year JGB yield fell -0.0331 to 0.820.

US ADP employment rises 143K, wage growth slows

US ADP report for September showed private employment increased by 143k, surpassing expectations of 120k. The goods-producing sector added 42k jobs, while the service-providing sectors contributed 101k new jobs.

By establishment size, small companies saw a loss of -8k jobs, while medium-sized businesses added 64k and large companies increased their workforce by 86k.

Wage growth continued to slow, with year-over-year pay gains for job-stayers easing to 4.7%. The decline was more pronounced for job-changers, whose wage growth fell from 7.3% to 6.6%.

Nela Richardson, ADP’s chief economist, noted that "stronger hiring didn't require stronger pay growth last month." She also pointed out that the premium job-changers usually enjoy over job-stayers narrowed to 1.9%, matching the low last seen in January.

ECB's de Guindos cites weaker growth outlook, expects recovery to strengthen over time

In a speech today, ECB Vice President Luis de Guindos acknowledged that Eurozone growth was weaker than expected in Q2, leading to a downward revision in the growth outlook for the region. He added that risks to growth remain "tilted to the downside".

Despite this, de Guindos expressed optimism for the future, expecting the recovery to "strengthen over time". He cited rising real incomes and the waning impact of restrictive monetary policy as key factors that should bolster consumption and investment. Additionally, he pointed to boost in exports as global demand improves, contributing to the recovery.

Eurozone unemployment rate unchanged at 6.4%, EU down to 5.9%

Eurozone’s unemployment rate was unchanged at 6.4% in August, aligning with market expectations. Meanwhile, EU unemployment rate fell slightly from 6.0% to 5.9%.

The report estimates that 13.027m people in EU, including 10.925m in Eurozone, were unemployed in August. Compared with the previous month, unemployment decreased by -108k across EU and by -94k within Eurozone.

On an annual basis, the improvement was even more notable. Compared to August 2023, the number of unemployed people dropped by -142k in EU and by -233k in Eurozone.

BoJ’s Ueda vows extremely high vigilance amid domestic and global economic uncertainties

BoJ Governor Kazuo Ueda reaffirmed today that Japan's economy is expected to sustain a moderate recovery, which should support underlying inflation in converging toward 2% target over the coming years. However, Ueda did not repeat the usual pledge to continue raising interest rates if inflation moves in line with forecasts, signaling a shift in tone towards a more cautious approach.

Ueda highlighted the ongoing uncertainties surrounding Japan's economy and inflation, stating that "uncertainty regarding Japan's economy and prices remain high." He also pointed to external risks, noting that the outlook for overseas economies, including the US, remains unclear, while financial markets continue to show signs of instability.

Given these risks, Ueda emphasized the need for "extremely high vigilance" in assessing economic developments. For now, BoJ will maintain a cautious stance, closely scrutinizing both domestic and global factors before tightening monetary policy again.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.85; (P) 143.69; (R1) 144.41; More...

USD/JPY rebounded strongly today and focus is now on 146.48 resistance. Firm break there will resume the rebound from 139.57 to 38.2% retracement of 161.94 to 139.57 at 148.11. On the downside, below 141.63 will turn bias to the downside for 139.57 support. But in this case, strong support could be seen again from 139.26 fibonacci level to bring rebound.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.