Sample Category Title

Analysis of GBP/CAD: Price Falls Below 1.800 Level

In the first nine months of 2024, the GBP/CAD exchange rate rose by over 7%, surpassing the significant 1.800 level.

The last time GBP/CAD remained consistently above this level was back in 2016, but it later dropped below. Since then, bulls have made two attempts to push the price above 1.800: in 2018 and again in 2020 (during the coronavirus panic) – both of which failed.

A third attempt occurred when GBP/CAD climbed above 1.800 in September 2024, but yesterday’s large bearish candles (marked with an arrow) suggest that this attempt to stay above 1.800 may also fail.

Yesterday’s decline in GBP/CAD was driven by a combination of factors, including:

→ A rise in oil prices, which strengthens the Canadian dollar as Canada is a major exporter of oil;

→ A slowdown in manufacturing activity in the UK during September, as reported by Reuters.

Technical analysis of the GBP/CAD chart shows the price is moving within an ascending channel (marked in blue), which has remained relevant since the start of 2024.

Support levels for the price could be

→ The 1.78500 level (which acted as resistance from mid-July before being broken in September);

→ The median line of the ascending channel;

→ The orange trendline.

However, it is possible that these support levels may not be strong enough to ensure that GBP/CAD can consistently hold above the 1.800 level, which has historically acted as key resistance.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Japanese Yen Slides as Political Drama Continues

The yen is sharply lower on Wednesday. In the European session, the USD/JPY is trading at 144.82 at the time of writing, up 0.89%.

New finance minister makes markets uneasy

In Japan, the dust is yet to settle on the political drama. On Tuesday, the new Prime Minister, Shigeru Ishiba, appointed Katsunobu Kato as finance minister. Kato is a supporter of “Abenomics” which advocates monetary easing. This could complicate the BoJ’s plans to tighten policy and the yen has responded with sharp losses today.

Ishiba is on record for supporting a tighter policy but may have chosen Kato to ease concerns that Ishiba will make a significant shift in monetary policy with a snap election on October 27. The election will be followed by the next BoJ meeting on October 31, with the BoJ expected to maintain its policy settings.

Japan and US manufacturing PMIs continue to contract

Manufacturing continues to sputter in both the US and Japan. The Japanese manufacturing PMI eased to a revised 49.7 in September, down from 49.8 in August and above the market estimate of 49.6. This was the third straight month of contraction in factory activity, with a strong decrease in export orders. Business confidence dropped to its lowest since December 2022, as manufacturers don’t see a light at the end of the tunnel for the troubled manufacturing sector.

In the US, the ISM manufacturing PMI was unchanged in September at 47.2, below the market estimate of 47.5. The contraction in manufacturing has extended for six straight months. New orders decreased in September, demand remains weak and manufacturers face uncertainty over the Federal Reserve’s monetary policy and the upcoming US election.

USD/JPY Technical

- USD/JPY has pushed above resistance at 143.69 and 144.41. Above, there is resistance at 145.25

- There is support at 142.85 and 142.13

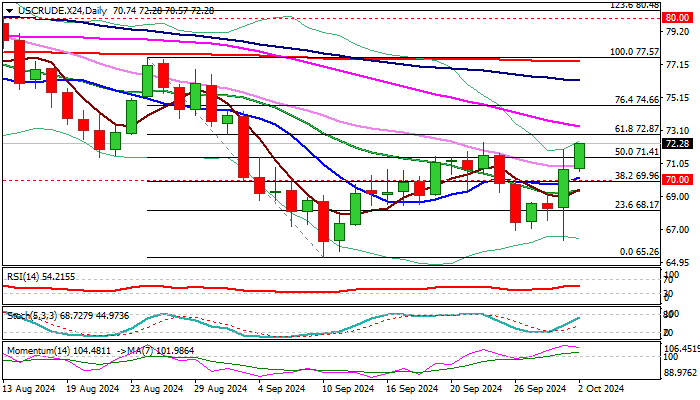

WTI Oil Outlook: Crude Prices Extend Gains on Escalation of the Middle East Crisis

Oil price extends strong rise into second consecutive day, advancing 1.6% during European session on Wednesday, following 3.45% advance on Tuesday (the biggest daily gain since Aug 12).

Growing fears that further escalation of the war in the Middle East could disrupt crude supply from the region, lifted oil prices significantly during past two sessions.

The latest rally improved the structure on daily chart, as the price rose above 50% retracement of $77.57/$65.26 bear-leg and psychological $70 level, underpinned by strong positive momentum and 10/20DMA’s in bullish configuration.

Bulls pressure pivotal resistance at $72.38 (Sep 24 lower top), break of which to generate fresh bullish signal on completion of bullish failure swing pattern on daily chart and soften strong bearish structure on weekly chart (multiple MA Death crosses / strong negative momentum).

Broken daily Kijun-sen ($71.08) should ideally contain dips and maintain bullish bias.

Caution on breach of $70 level (reinforced by 10DMA), which reverted to solid support and marks a breakpoint.

Fundamentals, however, are likely to play a key role in coming days, with further conflict escalation to provide fresh boost to oil price and open way for stronger upside acceleration.

Res: 72.38; 72.87; 73.37; 74.27.

Sup: 71.41; 70.88; 70.00; 69.26.

Brent Crude Oil Prices Rise Amid Geopolitical Tensions

Brent crude oil prices climbed to 74.55 USD per barrel by Wednesday, marking a significant increase driven by escalating geopolitical tensions in the Middle East. The previous session saw prices surge by over 2% as fears grew over potential crude oil shortages due to the intensifying conflict in the region, particularly with Iran's heightened involvement.

Iran, a key member of OPEC, holds substantial influence over global oil supplies. Its assertive stance in the Middle East conflict raises concerns about disruptions in energy exports, which could tighten the global oil market and push prices higher.

Mixed market sentiments

Despite the upward pressure from geopolitical factors, the overall sentiment in the oil market remains mixed. One of the dampening factors is the weak demand from China, the world's largest oil importer. China's sluggish economic indicators have limited the potential for a sustained recovery in oil prices, as reduced industrial activity translates to lower energy consumption.

Adding to the complex market dynamics, the American Petroleum Institute (API) reported that US crude oil inventories decreased by 1.5 million barrels during the week. This decline was less than the anticipated drop of 2.1 million barrels, marking the second consecutive weekly decrease but suggesting that demand may not be as robust as expected.

Furthermore, the appreciating US dollar has not yet significantly impacted crude oil prices but could do so in the future. Typically, a stronger dollar makes oil more expensive for holders of other currencies, potentially reducing global demand and applying downward pressure on prices.

Technical analysis of Brent crude oil

On the H4 chart, Brent crude found support at 69.90 USD, forming an upward wave targeting the 75.50 USD level. After reaching this point, a correction back to 72.66 USD is possible. Subsequently, there is potential for a new bullish wave extending to 78.20 USD, which serves as a local target. The MACD indicator technically supports this scenario; its signal line is below zero but trending sharply upwards, indicating increasing bullish momentum.

On the H1 chart, Brent broke above the 72.66 USD level and reached a local target at 75.30 USD. A consolidation range is expected to form below this level. A corrective move back to 72.66 USD (retesting from above) is possible, potentially leading to a downward exit from the consolidation. Once this correction is completed, the price may resume upward towards 75.50 USD, the initial target. The Stochastic oscillator technically confirms this outlook, with its signal line below the 80 level and preparing to decline, suggesting a short-term correction before further gains.

Conclusion

The interplay of escalating geopolitical tensions and mixed economic signals continues to influence Brent crude oil prices. While concerns over supply disruptions due to Middle Eastern conflicts push prices upward, weak demand from China and inventory data from the US temper this rise. Additionally, the strengthening of the US dollar could impact global oil demand in the near future. Traders and investors should closely monitor these factors, as they will likely contribute to continued volatility in the oil market.

US ADP employment rises 143K, wage growth slows

US ADP report for September showed private employment increased by 143k, surpassing expectations of 120k. The goods-producing sector added 42k jobs, while the service-providing sectors contributed 101k new jobs.

By establishment size, small companies saw a loss of -8k jobs, while medium-sized businesses added 64k and large companies increased their workforce by 86k.

Wage growth continued to slow, with year-over-year pay gains for job-stayers easing to 4.7%. The decline was more pronounced for job-changers, whose wage growth fell from 7.3% to 6.6%.

Nela Richardson, ADP’s chief economist, noted that "stronger hiring didn't require stronger pay growth last month." She also pointed out that the premium job-changers usually enjoy over job-stayers narrowed to 1.9%, matching the low last seen in January.

ECB’s de Guindos cites weaker growth outlook, expects recovery to strengthen over time

In a speech today, ECB Vice President Luis de Guindos acknowledged that Eurozone growth was weaker than expected in Q2, leading to a downward revision in the growth outlook for the region. He added that risks to growth remain "tilted to the downside".

Despite this, de Guindos expressed optimism for the future, expecting the recovery to "strengthen over time". He cited rising real incomes and the waning impact of restrictive monetary policy as key factors that should bolster consumption and investment. Additionally, he pointed to boost in exports as global demand improves, contributing to the recovery.

BoJ’s Ueda vows extremely high vigilance amid domestic and global economic uncertainties

BoJ Governor Kazuo Ueda reaffirmed today that Japan's economy is expected to sustain a moderate recovery, which should support underlying inflation in converging toward 2% target over the coming years. However, Ueda did not repeat the usual pledge to continue raising interest rates if inflation moves in line with forecasts, signaling a shift in tone towards a more cautious approach.

Ueda highlighted the ongoing uncertainties surrounding Japan's economy and inflation, stating that "uncertainty regarding Japan's economy and prices remain high." He also pointed to external risks, noting that the outlook for overseas economies, including the US, remains unclear, while financial markets continue to show signs of instability.

Given these risks, Ueda emphasized the need for "extremely high vigilance" in assessing economic developments. For now, BoJ will maintain a cautious stance, closely scrutinizing both domestic and global factors before tightening monetary policy again.

Eurozone unemployment rate unchanged at 6.4%, EU down to 5.9%

Eurozone’s unemployment rate was unchanged at 6.4% in August, aligning with market expectations. Meanwhile, EU unemployment rate fell slightly from 6.0% to 5.9%.

The report estimates that 13.027m people in EU, including 10.925m in Eurozone, were unemployed in August. Compared with the previous month, unemployment decreased by -108k across EU and by -94k within Eurozone.

On an annual basis, the improvement was even more notable. Compared to August 2023, the number of unemployed people dropped by -142k in EU and by -233k in Eurozone.

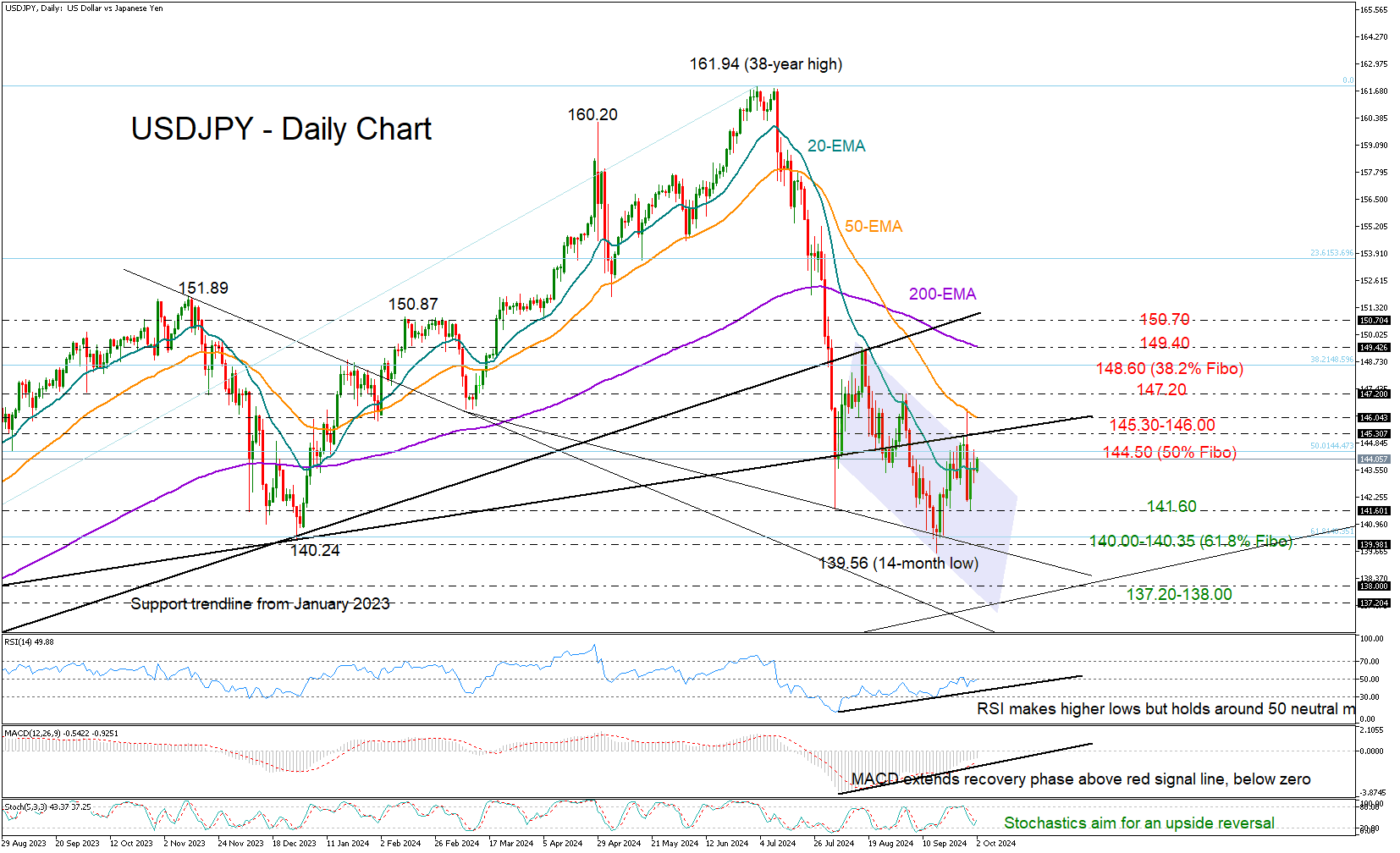

USDJPY Outlook Remains Gloomy

- USDJPY holds below key resistance levels as October’s session starts

- Technical signals cannot warrant a bullish trend reversal

USDJPY had a lackluster beginning to October, with a neutral close around its 20-day EMA and previously a rejection near the 50% Fibonacci retracement of the 2023-2024 upleg at 144.50.

Currently, the pair is attempting to reach the 144.50 territory again, but there may be more hurdles to overcome. Another challenge could emerge somewhere between the broken support trendline at 145.30 and the 50-day EMA at 146.00, while higher, the bulls may face a wall near September’s high of 147.20. If the latter proves easy to overcome, the spotlight might next shift to the 38.2% Fibonacci mark of 148.60 and then towards the 200-day EMA at 149.40.

Should the bears take control once more and push the price below its 20-day EMA at 143.60, there is a possibility of a new downward movement towards the 141.60 floor. Breaking lower, the pair could initially seek shelter around the critical 61.8% Fibonacci area of 140.35 and the 140.00 psychological mark. A failure to bounce back may result in a significant sell-off towards the 137.20-138.00 area, which was last seen in July 2023.

While trend signals are stagnant, there is encouraging movement in technical indicators like the RSI and MACD, indicating bullish divergence. Yet, an imminent upside reversal in the price cannot be warranted as long as the RSI is still around its 50 neutral mark and the latter is hovering below zero.

Overall, the short-term outlook for USDJPY is not favorable. For the pair to resume its previous upward trajectory, it must successfully climb sustainably above 150.70. On the downside, a close below 140.00 could further worsen the bearish trend.

Changing of Guard at Swiss National Bank

The Swiss franc is calm on Wednesday. In the European session, USD/CHF is trading at 0.8454, up 0.13% on the day.

SNB welcomes Schlegel – will he bring more of the same?

Martin Schlegel has taken over as the new president of the Swiss National Bank, replacing long-term head Thomas Jordan. Schlegel gave his first speech as president on Tuesday and investors are keen to know whether he will continue Jordan’s policies.

Under Jordan, the SNB was one of the first major central banks to raise interest rates in response to rising inflation. In the case of the SNB, that meant ensuring that inflation did not stray far from the upper level of the 0%-2% target. The SNB got the job done and the SNB has been aggressive in cutting rates as inflation has been falling. The SNB has lowered rates at three consecutive meetings since March, bringing the cash rate to 1%.

Schlegel didn’t make any waves with his first speech, which was no surprise. He said that the central bank’s “main instrument” was the policy rate and hinted at further rate cuts, saying that the downward risks to inflation were higher than the upside risks and that negative rates “can’t be excluded”.

Schlegel was vague about the SNB intervening in the currency markets, saying such a move couldn’t be excluded. The Swiss franc has soared a massive 8% since May 1 and the spike in tensions in the Middle East could push the safe-haven asset even higher. The SNB has intervened in the past when the franc has sharply appreciated in order to keep Swiss exports competitive and there is speculation that the SNB might step in if the Swissy’s appreciation continues.

On the data calendar, Switzerland will release the September inflation report on Thursday. The market estimate stands at 0%, compared to -0.1% in August. Yearly, inflation is expected to remain unchanged at 1.1%.

USD/CHF Technical

- USD/CHF is testing support at 0.8460. Below, there is support at 0.8438

- 0.8488 and 0.8510 are the next resistance lines