Sample Category Title

AUD/USD Struggles With Gains, Faces A Downturn

Key Highlights

- AUD/USD faced resistance near 0.6940 and started a downside correction.

- A key bullish trend line is forming with support at 0.6880 on the 4-hour chart.

- Gold could rise again and trade toward the $2,700 level.

- Bitcoin trimmed gains and traded below the $64,000 level.

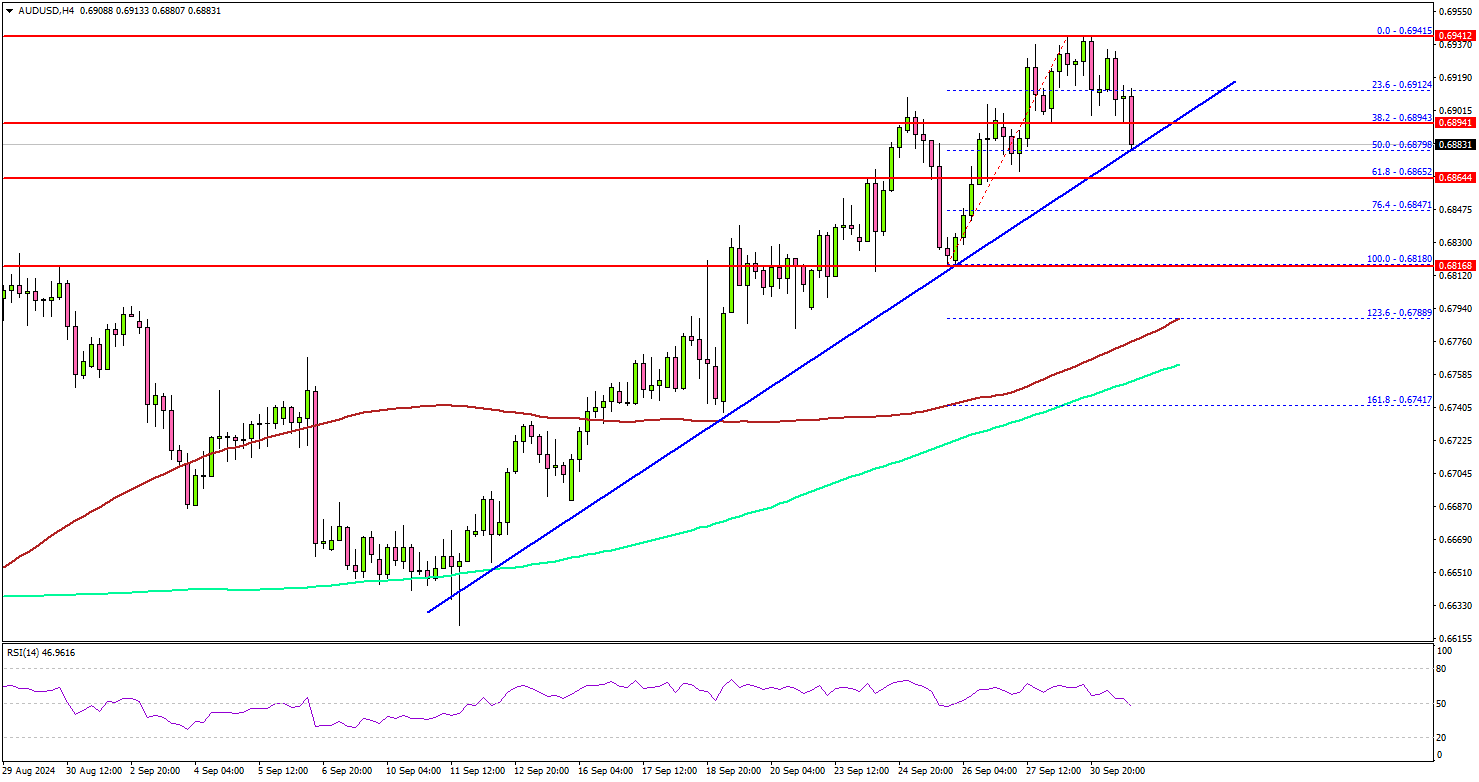

AUD/USD Technical Analysis

The Aussie Dollar climbed higher toward 0.7000 against the US Dollar. AUD/USD failed to continue higher and started a correction phase.

Looking at the 4-hour chart, the pair traded as high as 0.6941 and recently corrected lower. There was a move below the 0.6920 level, but the pair remained well above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

On the downside, immediate support sits near the 0.6880 level. There is also a key bullish trend line forming with support at 0.6880 on the same chart, below which the pair might test 0.6865. The next key support sits near the 0.6800 level and the 100 simple moving average (red, 4-hour).

Any more losses could send the pair toward the 0.6750 support zone. On the upside, the bears are active near the 0.6920 level. A close above the 0.6920 level could set the tone for another increase.

The next major resistance could be 0.6940. A clear move above the 0.6940 level might send AUD/USD toward 0.7000. Any more gains might call for a test of the 0.7045 zone.

Looking at Gold, the bulls are now aiming for another increase and might aim for a move toward the $2,700 level.

Upcoming Economic Events:

- US ADP Employment Change for Sep 2024 - Forecast 120K, versus 99K previous.

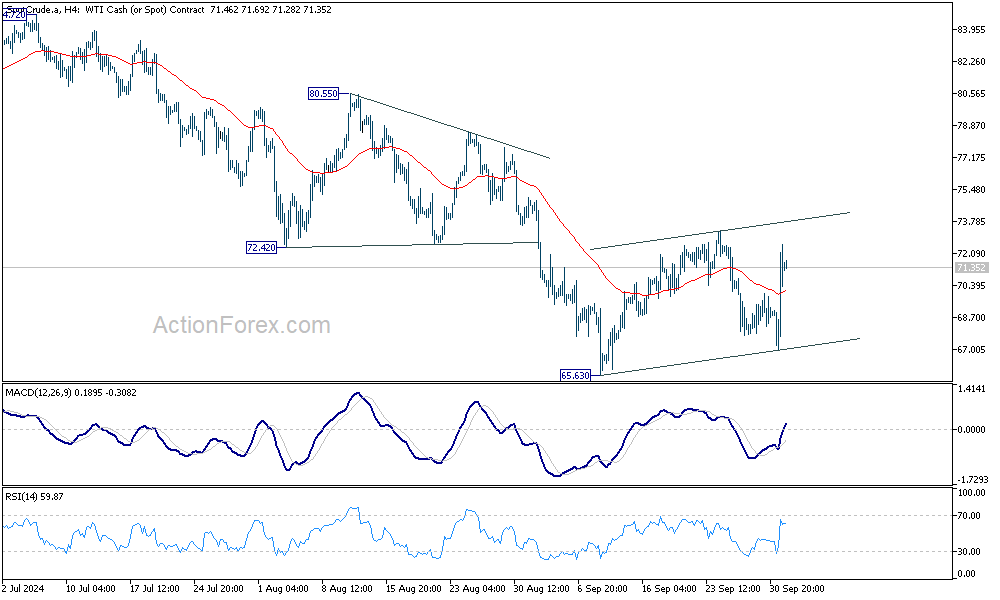

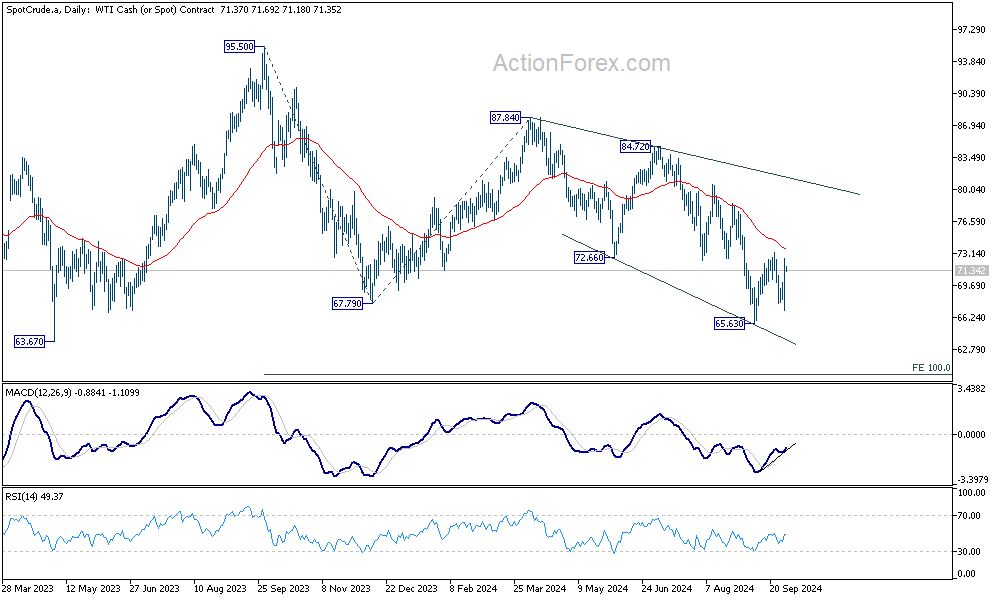

WTI surges on Middle East Conflict, but viewed as corrective move

Oil prices surged overnight, with WTI crude breaking back above 70 as tensions in the Middle East escalated. Iran launched a retaliatory strike on Israel in response to the recent killing of Hezbollah leader Hassan Nasrallah and an Iranian commander in Lebanon. This has fueled concerns that Israeli retaliation could target Iran's oil infrastructure, posing a significant risk to global oil supplies.

As Israel shifts its focus from Gaza to Lebanon and Iran, the conflict is entering a phase with greater implications for energy markets. The prospect of disruptions in one of the world's most critical oil-producing regions has led to heightened market anxiety, with fears of further price increases if the conflict intensifies.

Technically, despite the rebound, WTI is seen as extending the near term consolidations pattern from 65.53 only. While further rise cannot be ruled out, outlook will stay bearish as long as 55 D EMA (now at 73.72) holds. Larger down trend is still expected to extend through 65.53 to 63.67 (2023 low) at a later stage. Tentatively, the medium term target is 100% projection of 95.50 to 67.79 from 87.84 at 60.13.

However, sustained break of 55 D EMA will argue that a medium bottom was already from, and stronger rebound would be seen back towards 80 psychological level.

ECB’s Kazaks: Recent data clearly points towards Oct rate cut

ECB Governing Council member Martins Kazaks indicated that recent data "clearly point in the direction of a cut" in interest rates at the upcoming October meeting. Kazaks highlighted the increasing risks to the Eurozone economy, noting that the balance between stubborn inflation, particularly in services, and weak growth is tilting toward the latter.

He emphasized that even after another 25bps cut, which would bring the deposit rate to 3.25%, the rate would still "restricts economic activity" and curb inflation in the services sector.

Kazaks expressed concern over the “worrying” state of the economy, especially the potential for a sudden weakening of the job market. "If corporates start to shed labor, this snowball may start rolling," he cautioned, warning of the risks of a tipping point that could exacerbate economic decline.

SNB’s Schlegel: Prepared for more rate cuts as inflation downside risks outweigh upside

At an event overnight, new SNB Chair Martin Schlegel indicated that the central bank is prepared to continue easing monetary policy if necessary to maintain medium-term price stability, and the central bank "can't rule out negative rates either."

Schlegel emphasized that SNB sees "downward risks to Swiss inflation as bigger than upward risks," suggesting that deflationary pressures are a significant concern for the Swiss economy.

He also acknowledged the challenges posed by the strong Swiss franc for exporters. However, he pointed out that the primary issue facing Swiss companies is "weak foreign demand," rather than currency strength alone.

Markets are currently pricing in an 85% probability that SNB will lower rates further by 25bps to 0.75% at its December meeting.

RBNZ: What Are You Waiting for? OCR to be Cut 50bps in Both October and November

- We now expect the RBNZ to cut the OCR by 50bps to 4.75% at the October Monetary Policy Review.

- We also expect another 50bps cut to 4.25% at the November Monetary Policy Statement.

- The projected step up in the pace of easing in October is a more finely balanced decision (perhaps a 60% probability) whereas the probability of a larger easing in November looks much higher.

- The inflation outlook now looks set to settle close to 2% from Q3 2024 and gives the RBNZ more room to move more quickly back to neutral settings.

- We continue to see the terminal OCR at 3.75% - the cuts expected by Christmas merely bring the OCR closer to neutral more quickly.

- We don’t see a case for expansionary settings as there are tentative signs the economy is responding to easier conditions.

- We hope the RBNZ will be more circumspect on how quickly the OCR will change in 2025 as the OCR will be closer to neutral wherever defined.

RBNZ decision and associated communication.

We are changing our forecasts for the OCR and now expect the OCR to move more quickly to neutral than previously forecast. We now see two consecutive 50bp cuts in the OCR in the October and November meetings which will take the OCR to 4.25% at the end of 2024. This will leave the OCR just 50bps above our long-term neutral rate of 3.75%. The projected step up in the pace of easing in October is a more finely balanced decision (perhaps a 60% probability) whereas the probability of a larger easing in November looks much higher.

We anticipate a much slower, highly data dependent and uncertain path lower in the OCR in 2025. We have pencilled in 25bp cuts in each of the February and May Monetary Policy Statements taking the OCR to the longterm terminal rate of 3.75% by mid-2025.

A key driver behind this change in view has been the strong signs that the forward inflation profile will be much more benign in aggregate that we have seen since 2021. Our current forecast for annual inflation in Q3 is for an annual rate of 2.4% falling to 2.2% in Q4 this year. There may be some downside risks to those short-term forecasts. Yesterday’s QSBO confirmed a benign picture for short term pricing pressures and leaves us thinking that the RBNZ will not see either headline inflation or inflation expectations pressures as an impediment to bringing the OCR to neutral levels relatively quickly.

Another issue is that the global interest rate cycle has decisively turned in recent months. Central banks have been responding to a global inflation shock and have generally responded in similar ways. We now find the RBNZ fitting well into the group of advanced economy central banks who have already eased significantly, and look set to ease by a deal more by the end of Q1 2025. The RBNZ will need to reduce the degree of restriction relatively quickly to keep pace with its peers. And now with inflation projected to be close to target, and the economy operating a fair margin below its productive capacity, there is a less obvious case for maintaining restrictive settings.

As suggested in our recent Hawks and Doves note, reasonable arguments can be made for both maintaining a 25bp point pace of easing and accelerating the pace to more quickly return policy to a neutral stance. Given the latest information, on balance we find the dovish arguments more compelling. Domestically generated non-tradable inflation remains very high, and there has already been a significant easing in financial conditions that could see the economy rebound relatively quickly and frustrate the disinflation process. However, these concerns seem less important considering yesterday’s QSBO which confirms that near-term economic momentum likely remains in negative territory. While businesses in particular are more confident of better times next year, we have some distance to travel before those become front of mind from a policy standpoint.

Housing market data similarly show increased activity, but also depressed and still falling prices, indicating the housing market recovery is most likely a 2025 as opposed to 2024 story. The stronger outlook for the primary sector is another factor that seems likely to lend significant support to the economy. But again, this is most likely to be a consideration in 2025 given commodity prices and the terms of trade are recovering from weak levels and costs remain high in the primary sector.

In conclusion, we think the RBNZ MPC will be asking themselves “What are we waiting for?” when considering the case for maintaining the OCR at what are reasonably tight levels (even based on Westpac’s 3.75% neutral OCR, let alone the RBNZ’s 3.0% to 3.5% range of shorter run neutral OCR estimates). If the answer to that question is “not much” then the path ahead seems clear, especially given the RBNZ has a long gap between meetings from November 2024 to February 2025.

We had thought for a while that if a 50bp cut was to occur, then the November Monetary Policy Statement seemed the most compelling time given that gap in the calendar. And if the case for a 50bp cut in November is strong, then the case for that move to come in October also seems compelling. We don’t think there will be enough risk in the Q3 CPI or labour market reports coming mid October/early November to really shake the case for more substantial OCR adjustment before Christmas. If those risks materialise, then there is plenty of scope for the RBNZ to cut the OCR by less in November if need be.

The challenge now for the RBNZ will be to maintain firmer control on the market’s tendency to extrapolate OCR cutting expectations. Moving the OCR closer to neutral will help with that goal. But we also hope the RBNZ will provide a clearer set of parameters on how they would expect to operate policy in 2025. Monetary policy since 2019 has ended up being strongly procyclical – far too easy in 2019-21, necessitating very tight policy settings in 2023-24. We hope the RBNZ will avoid the temptation to cut rates too aggressively in 2025 unless well justified by the inflation and economic outlook. Making the point now that a faster removal of restriction implies less need to cut so deeply later would be a good way to try and deliver the “hawkish cut” that could stabilise output and employment without driving house prices further out of reach of the public.

Developments since the August MPS.

We think the following have been the key developments since the August MPS:

- Activity: GDP fell 0.2% in the June quarter, slightly less than the RBNZ had expected. Top-down indicators, such as those in the QSBO, suggest that GDP likely continued to contract in the September quarter, while early indicators for the December quarter point to subdued growth and thus a continued build-up of slack in the economy.

- Inflation indicators: Partial indicators from the monthly Selected Price Indexes for July and August suggest that Q3 CPI inflation is likely to print close to the RBNZ’s August MPS forecast of 2.3%y/y. However, survey indicators from the QSBO suggest some potential downside risk to our forecast.

- Labour market: While measures of filled jobs have stabilised in recent weeks, indicators continue to suggest that unemployment rate likely lifted in the September quarter, broadly in line with the RBNZ’s expectations. Surveys suggest that looser labour market conditions are placing downward pressure on labour cost inflation.

- Sentiment: Headline measures of business sentiment and expectations regarding activity a year ahead have improved sharply, especially those in the ANZ Business Outlook Survey. However, the improvement seen in survey measures of consumer confidence remains modest.

- Housing: House prices appear to have contracted further in the September quarter, and probably by more than the RBNZ had expected. Indicators and anecdotes point to some lift in activity of late, but house prices seem likely to remain subdued in the near-term given the overhang of inventory on the market.

- Commodity prices: There has been some further improvement in key commodity prices, notably in the dairy sector where Fonterra has recently raised its midpoint forecast for this season’s milk price to $9.00.

- Global growth: The most significant trading partner development has been in China, where continued weak data has recently prompted policymakers to announce a slew of stimulus measures. It’s uncertain whether the RBNZ will regard these measures as sufficient to allay concerns about a potential deflationary impulse from that economy.

- Financial conditions: Domestic wholesale interest rates have continued to move lower, in part reflecting the Fed’s 50bp policy easing last month. However, with the US dollar weakening, the NZ dollar TWI is trading more than 3% above the RBNZ’s assumption for the current quarter and beyond – if sustained, this will cause the RBNZ to revise down its near-term inflation forecasts.

Gold Wave Analysis

- Gold reversed from support level 2625.00

- Likely to rise to resistance level 2685.00

Gold recently reversed up from the support level 2625.00 intersecting with the upper trendline of the daily up channel from July (acting as the support after it was broken in September).

The upward reversal from the support level 2625.00 continues the active short-term impulse wave 5 of the higher order impulse wave (5) from last year.

Given the overriding daily uptrend, Gold can be expected to rise further to the next resistance level 2685.00 (top of the previous impulse wave i).

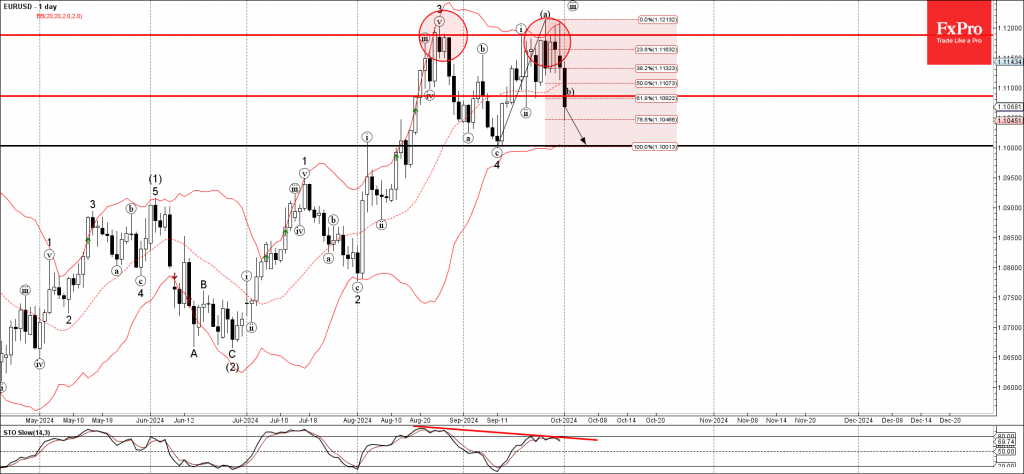

EURUSD Wave Analysis

- EURUSD broke key support level 1.1085

- Likely to fall to support level 1.1000

EURUSD currency pair recently broke the key support level 1.1085 (which stopped the previous correction ii) coinciding with the 61.8% Fibonacci correction of the upward impulse from the start of September.

The breakout of the support level 1.1085 should accelerate the active wave b of the higher impulse wave iii from the middle of September.

Given the bearish divergence on the daily Stochastic and the strongly bullish US dollar sentiment seen today, EURUSD currency pair can be expected to fall further to the next support level 1.1000 (which stopped the previous correction 4).

Euro Extends Losses as Eurozone CPI Slows to 1.8%

The euro continues to lose ground and is trading at 1.1080 in the North American session, down 0.49% on the day. The euro is down for a third consecutive day and has declined 0.9% during that time.

Eurozone CPI lower than expected

Eurozone inflation eased to 1.8% y/y in September, down from 2.2% in August and below the market estimate of 1.9%. This was the lowest rate since April 2021 and below the European Central Bank’s inflation target of 2%. The drop in inflation was largely driven by the sharp decrease in energy prices. Monthly, inflation declined by 0.1%, down from the 0.1% gain in August.

Services inflation, which has been a headache for the ECB, dropped from 4.1% to 4.0%. The core rate, which is a better indicator of long-term inflation trends, fell to 2.7%, down from 2.8% in August and below the market estimate of 2.8%. Inflation declined across the bloc, with Germany, France, Italy and Spain all recording inflation rates below 2%.

The ECB has approached the new rate-cutting cycle with caution, as high services inflation and wage growth are reminders that the battle against inflation isn’t over. The markets expect the ECB to remain on the sidelines at the October meeting and re-evaluate a possible rate cut in December.

The Federal Reserve is expected to be aggressive in its rate-cutting cycle, which started last month with a large cut of 50 basis points. On Monday, Fed Chair Powell poured cold water on expectations for another jumbo rate cut, saying that the economy was in “solid shape” and that the Fed was not in any rush to cut rates quickly. Powell’s remarks have lowered market odds of a 50-bps cut to 40%, compared to 58% one week ago, according to CME’s FedWatch.

EUR/USD Technical

EUR/USD pushed below support at 1.1096 and tested support at 1.1058 earlier. The next support level is 1.1001

1.1153 and 1.1191 are the next resistance lines

US: Manufacturing Index unchanged in September

The ISM Manufacturing Index was unchanged in September, holding at 47.2 and a smidge below expectations for a 47.5 print. As in July and August, only five of 18 industries reported growth for the month, but as only one of the six largest industries grew, a greater share of manufacturing GDP contracted (77% vs. 65% in August).

Demand conditions remain soft. Although, the new orders index improve marginally for the month (46.1 from 44.6) it, along with new export orders, continues to signal a contraction. Backlogs or Orders also shrank at roughly the same pace as the month prior (44.1 vs 43.6).

One silver lining is that the production index rose 5 percentage points to 49.8 – close to the breakeven level. However, employment conditions deteriorated further in September, signaling a faster clip of contraction.

Last month's uptick in prices has faded, with the index falling back into contraction (48.3) for the first time since December 2023.

Key Implications

Not much change from last month in the manufacturing sector. New demand continues to shrink, and payrolls are coming under pressure again.

While the report paints a challenging picture for the sector, there are some reasons for optimism. The prices paid index signaled falling raw materials prices for the first time since late last year. Combined with the Fed embarking on its rate cutting cycle, there are some glimmers of optimism for a sector that has struggled under the weight of higher interest rates.