Sample Category Title

Sunset Market Commentary

Markets

A series of weaker-than-expected national inflation figures culminated in the first sub 2% European-wide reading for September today. The 1.8% y/y outcome was the lowest since April 2021 with the first negative m/m (-0.1%) print since January this year. The limited details available yet do show it’s mainly an energy-driven event, with favourable base effects pushing prices a whopping 1.6% down in m/m terms (-6% y/y). There’s ongoing stickiness in services inflation, which barely eased from 4.1% in August to 4% last month. Core inflation (ex. food and energy) decelerated as slightly as consensus expected: from 2.8% to 2.7%. ECB president Lagarde fired up the debate about an October cut yesterday before the European Parliament. Markets are all but certain the ECB will pull the trigger for such a back-to-back move. They even added to their bets today (+/- 93% discounted) with the likes of Finish governing council member Rehn supporting the case. He said it’s too early to declare a soft landing and said there are more grounds for cutting rates at the October meeting. We think the implications of today’s data for the October meeting are less straightforward as money market pricing currently suggest. But it’s duly noted. The European yield curve move is interesting though with significant long end outperformance (-10 bps in Germany’s 30-yr, -4.4 bps in the 2-yr). With an October (and December) cut basically priced in and a terminal rate of a mere 1.75% (vs. 2-2.5% neutral), downward market pressure on yields now seems to shift towards longer maturities. The 10-yr yield snapped below the August low of 2.078%, triggering a technical acceleration that’s currently running to 2.03%. US Treasuries underperform a tad, with yields declining between -1.8 (2-yr) to -6 bps (30-yr) ahead of the first key data of this week. Dollar-favourable interest differentials push EUR/USD below the 1.11 handle. DXY advances towards 101.2.

US job openings picked up from 7711k to 8040k in August, defying expectations for a decline to 7693k. The manufacturing ISM came close to expectations on a headline basis (47.2 vs a marginal uptick to 47.5 expected). The underlying components were unconvincing with the order book only shrinking at a slower pace (46.1 from 44.6). Employment is declining at an accelerated tempo though (43.9), nearing the post pandemic low of July. Prices paid dropped in contraction territory for the first time this year. US yields extends their initial declines in a first response that’s concentrated at the ISM rather than the JOLTS. The dollar pares some of the earlier gains.

News & Views

The Riksbank published the minutes of the September 25 policy meeting when it decided to further reduce the policy rate by 25 bps to 3.25%. The RB flagged the possibility of a 50 bps step at one of the two remain meetings. It also sees room for one or two additional cuts next year. Deputy governor Perr Jansson raised the issue how the RB should react to headline inflation falling substantially below 2.0% (1.2%). The RB takes a symmetrical approach on over- and undershoots. Even so, developments in the real economy also play a major role in its assessment why it is now appropriate to opt for a slightly greater easing in monetary policy. Now that upside risks to inflation are clearly smaller than before, it is a good time to try to stimulate the real economy. It is important in itself that economic activity strengthens, but it is also a condition for inflation to stabilize near target. Most other governors with nuances mostly joined this analysis. Governor Thedeen ‘summarized’ that cuts in larger steps, given the favourable inflation outlook, this is now part of the RB gradual monetary policy strategy. The krone didn’t show much of a reaction to the soft RB assessment which is probably to a large extent discounted. EUR/SEK traders near 11.85.

The EU announced that from October 7 2024, it will launch its Repurchase Agreement (Repo) facility. According to the statement, the facility marks the implementation of the final measure to support the EU bond market that the EU committed to in its communication from December 2022. It marks a natural next step in the development of the EU as an issuer. The introduction of the facility aims to strengthen the role of EU-bonds as liquid and safe collateral, following the exponential growth in the secondary market. Under the facility, the EU will offer its Primary Dealers the possibility to source specific EU-Bonds on a temporary basis. By acting as a backstop to the Primary Dealers’ secondary market activity, the facility will allow investors to be more confident in the terms on which they can trade EU-Bonds in the secondary market, improving the overall efficiency and fluidity of the EU-bonds market, the statement says.

Graphs

EUR/USD: euro slides as money markets up bets for an October cut following Rehn’s endorsement and sub 2%-inflation print

German 10-yr yields snaps below August low. Downward market pressure shifts to longer maturities as front-end gets very crowded

EUR/SEK: SEK shrugs at Riksbank officials openly flirting with 50 bps cuts in September meeting minutes, suggesting it’s priced in

Brent oil ($/b) looks for a short-term equilibrium between $70-75 as China boost fades

US ISM manufacturing unchanged at 47.2, continued contraction

US ISM Manufacturing PMI was unchanged at 47.2 in September, falling short of expectations of 47.8. This marks the sixth consecutive month of contraction in the manufacturing sector, which has now shrunk in 22 of the past 23 months.

Among the key components, new orders showed a modest improvement, rising from 44.6 to 46.1, while production saw a notable jump from 44.8 to 49.8, approaching the neutral 50 level.

However, employment declined sharply, dropping from 46.0 to 43.9, with the past three months reflecting some of the weakest employment figures since July 2020. Price pressures also eased significantly, with the prices index falling from 54.0 to 48.3.

Historically, the relationship between the ISM Manufacturing PMI and overall economic activity suggests that the September reading of 47.2 corresponds to a modest 1.3% annualized increase in real GDP.

European Central Banks Quickening Pace Of Their Monetary Easing

Summary

- The European Central Bank (ECB) initially adopted a cautious and gradual approach to rate cuts during the early stages of its monetary easing cycle. However, given some deterioration in sentiment surveys, evidence of subsiding inflationary pressures, and recent benign comments from ECB President Lagarde, we now expect a more regular pace of rate cuts from the ECB over the next several months.

- We look for the ECB to cut rates by 25 bps at its October 2024, December 2024, January 2025 and March 2025 announcements. As ECB policy rates move closer to a neutral level, we see the central bank paring back the pace of its rate cuts to a quarterly frequency. We see the ECB cutting interest rates by 25 bps at the June 2025 and September 2025 meetings, bringing its policy rate to a low of 2.00% by late next year.

- The Riksbank is also set to ease monetary policy at a faster pace, after it cut its policy rate last week by 25 bps to 3.25%, lowered its growth and inflation forecasts, and offered dovish policy guidance in its accompanying statement. Soft data and dovish guidance means we now see a 50 bps rate cut in November, and with regular 25 bps rate cuts at each meeting thereafter, we expect the Riksbank's policy rate to reach a low of 2.00% by the end of Q1-2025.

- The Swiss National Bank (SNB) lowered its policy rate by 25 bps to 1.00% last week, while also noting a significant reduction of inflationary pressures and a recent strengthening of the Swiss franc. Given the potential for further franc gains against a backdrop of European Central Bank (and Federal Reserve) easing, and given the subdued outlook for Swiss inflation, we now expect the SNB to ease monetary policy further, and forecast a 25 bps rate cut in the SNB's policy rate, to 0.75%, at its December monetary policy announcement.

European Central Bank To Step Up The Pace Of Rate Cuts

During the early stages of its rate cut cycle, the European Central Bank (ECB) has adopted a cautious and gradual approach toward monetary easing. Given lingering concerns about elevated wage growth and persistent services inflation, the ECB lowered its policy rate 25 bps in June, paused in July, and delivered another 25 bps rate cut in September, bringing its Deposit Rate to 3.50%. However, with recent data pointing toward weaker growth and softening inflation, we believe the ECB is likely to pursue a more regular pace of rate cuts over the next several months. We expect the European Central Bank to lower its policy rate by 25 bps at every meeting through March of next year, before reverting to a quarterly pace of rate cuts thereafter. That would lower the ECB's Deposit rate to a terminal rate of 2.00% by September 2025.

After enjoying a moderate rebound in economic growth during the first half of this year, Eurozone expansion appears to be losing momentum during the second half of 2024. The ECB has increasingly indicated at recent announcements that risks to economic growth are tilted to the downside. That message was reinforced with the release of the Eurozone PMI surveys for September. The manufacturing PMI fell to 45.0, the lowest level since December of last year, with German manufacturing remaining especially weak. Meanwhile, the services PMI dropped much more than expected to 50.5, the lowest level since February, in part as the French services PMI reversed an Olympics-related boost seen in August. Combining both the manufacturing and services sector, the composite (or economy-wide) PMI dropped to 48.9 in September, which was also the first reading in contraction territory since February this year. In addition to the disappointing headline figures, the details of the PMI reports were also discouraging. The manufacturing PMI showed a softening in new orders and order backlogs, while the services PMI showed a softening in incoming new business.

The “hard” activity data, although a bit more dated, are similarly weak with growth in retail sales volumes (-0.1% year-over-year) and industrial output (-2.2% year-over-year) both in negative territory in July. Finally, in terms of fundamental growth drivers, while gains in real household disposable income should support modest gains in consumer spending over time, falling net entrepreneurial income (a proxy for corporate profits) and declining capacity utilization suggest a retrenchment in investment spending. Against this backdrop we recently revised our Eurozone GDP growth forecasts lower to 0.7% for 2024 and 1.2% for 2025, though the risks are arguably still tilted to the downside.

In addition to the downside risks to growth, there are more encouraging signs that Eurozone inflation pressures are ebbing. The Eurozone September PMI surveys were also notable for a reported softening in input costs and output prices. That comes on the back of slower wage growth reported for Q2-2024, as the ECB's Indicator of Negotiated Wages slowed to 3.6% year-over-year and Compensation per Employee slowed to 4.3%. Importantly, those signals of reduced price pressure were also confirmed by the Eurozone September CPI. Headline inflation slowed to 1.8% year-over-year, below the ECB's inflation target for the first time since June 2021, while core inflation also eased to 2.7%, as did services inflation, to 4.0%.

The worsening growth outlook along with ebbing inflation pressures will, we think, provide ECB policymakers with enough comfort to once again lower interest rates at their October monetary policy announcement. Indeed, some recent dovish comments from ECB President Lagarde to the European Parliament appear consistent with that view. Lagarde said that disinflation has accelerated in the last two months, that the “latest developments strengthen our confidence that inflation will return to target in a timely manner,” and that we “will take that into account in our next monetary policy meeting in October.” In addition, sentiment surveys suggest the news on economic growth is likely to get worse before it gets better, while over time we would also expect wage growth and underlying inflation trends to continue a gradual deceleration. Against this backdrop, we expect a steady series of ECB rate cuts in the months ahead. We look for the ECB to cut rates by 25 bps at its October 2024, December 2024, January 2025 and March 2025 announcements. As ECB policy rates move closer to a neutral level, and as growth in economic activity perhaps starts to stabilize, we see the central bank paring back the pace of its rate cuts to a quarterly frequency. We see the ECB cutting interest rates by 25 bps at the June 2025 and September 2025 meetings, bringing its policy rate to a low of 2.00% by late next year.

Sweden's Riksbank To Also Get A Move On

The European Central Bank is not the only central bank for which we are now forecasting a faster pace of easing; Sweden’s Riksbank also makes the list. Underpinning our outlook for more timely Riksbank easing, last week the central bank cut its policy rate by 25 bps—for the 3rd time this year—to 3.25%, and communicated an overall dovish stance. In explaining the case for the rate cut, policymakers pointed to a fall in inflation pressures over the year. Officials also noted how they have shifted their concern from primarily price pressures, to economic activity, stating that the economy has been recovering at a slower pace than previously expected. The announcement also included more dovish updated forward guidance, with policymakers stating that “the policy rate can be cut at a faster pace than the Riksbank has previously communicated”. More specifically, if the outlook for prices and GDP growth remains unchanged, policy rate reductions can also be delivered at the November and December meetings, and most significantly, they signaled that there could be a 50 bps rate cut at a coming meeting. The Riksbank also added that one or two additional cuts could come in the first half of next year. Overall, this announcement was consistent with the general trend of increasingly dovish forward guidance from the Riksbank that we have seen over the course of this year.

When looking at the data from recent months, it is not surprising, in our view, that the Riksbank has continuously inched in a more dovish direction. CPIF inflation has continued to slow, coming in at just 1.2% year-over-year in August—below the central bank’s 2% target for the measure. Underlying price pressures measured via the CPIF excluding energy have also largely abated, having slowed from an above-4% year-over-year pace at the beginning of 2024 to 2.2% year-over-year in August. Nominal wage growth in Sweden—an area of concern for many other global central bankers amidst their respective battles against inflation—has also slowed consistently since the early part of this year. Meanwhile, GDP growth has also been subdued, with the Swedish economy having contracted on a quarter-over-quarter basis for four out of the past seven quarters, while the unemployment rate has also trended upward over the past year. This softer picture for price pressures and economic growth was also reflected in the Riksbank’s updated economic projections published last week. The central bank downwardly revised its CPI and CPIF inflation forecasts for this year and next, and downwardly revised its GDP forecast for 2024, to 0.8% from 1.1% previously.

Looking ahead, we believe that the trend will remain for subdued inflation and economic growth data in the near term. In our view, an outlook for softer inflationary pressures coupled with more subdued economic growth justify a faster pace of easing from the Riksbank. In addition to domestic economic data, we believe actions by other major central banks, specifically the ECB and Federal Reserve, will help Riksbank policymakers feel comfortable adopting a more accelerated easing approach. The Fed started its easing cycle with a bang in September with a 50 bps rate cut, and we now also expect the ECB to pick up the pace of its easing to a 25-bps-per-meeting rate cut pace over the next several meetings. Taking together the considerations of near-term subdued price pressures and economic growth, downgrades to the Riksbank’s inflation forecasts and dovish forward guidance, along with other major central banks likely adopting a more hastened pace of rate cuts, we have adjusted our outlook for Riksbank monetary policy to include a faster pace of easing than previously expected. Near-term softness in the data and central bank signals lends itself, in our view, to a 50 bps rate cut at the Riksbank’s November meeting. After that, we see the central bank delivering 25 bps rate cuts at each meeting through the end of Q1-2025, to reach a policy rate of 2.00%. As the fairly aggressive pace of easing we expect to see through year-end 2024, and further easing in early 2025, helps the central bank to approach a neutral policy rate and helps Sweden’s economic recovery to gain steam, we see the Riksbank pausing its easing cycle once the policy rate reaches 2.00% in the early part of next year.

Swiss National Bank Likely To Cut Rates Again In December

The Swiss National Bank (SNB) was another central bank to offer a dovish perspective at its monetary policy announcement last week. The SNB lowered its policy rate by 25 bps to 1.00%, matching widespread expectations. The SNB said inflationary pressures in Switzerland had decreased significantly compared to the previous quarter, reflecting among other things the appreciation of the Swiss franc over past three months. Indeed, even incorporating the latest rate cut, the central bank significantly lowered its medium-term inflation forecast, reflecting the strength of the franc, lower oil prices and announced electricity price cuts, as well as weaker second-round price effect given lower headline inflation. The central bank's updated forecast is within the SNB's price stability range over its entire forecast horizon, envisaging annual inflation of 1.2% for 2024, 0.6% for 2025 and 0.7% for 2026.

Considering the benign inflation outlook, the SNB said further cuts in the policy rate may become necessary in the coming quarters to ensure price stability over the medium term. Given our outlook for more accelerated European Central Bank interest rate cuts, we see increased potential for further appreciation in the Swiss franc—a currency that is already at historically elevated levels as measured on a real effective exchange rate basis. Accordingly, given the likelihood of further franc gains against a backdrop of European Central Bank (and Federal Reserve) easing, and given the subdued outlook for Swiss inflation, we now expect the SNB to ease monetary policy further, and forecast a 25 bps rate cut in the SNB's policy rate, to 0.75%, at its December monetary policy announcement.

Brent Crude – Oil Slides 2% in European Trade Before a Recovery, OPEC+ Meeting Next

- Oil prices fell by 2.4% in early European trade, possibly due to demand concerns and rebalancing.

- Concerns about China’s economic recovery and the possibility of increased Libyan oil production are also weighing on oil prices.

- From a technical perspective, the H4 chart showing RSI divergence. Higher prices ahead?

Oil prices fell off sharply in early European trade, declining around 2.4% with Brent trading at 70.600 at the time of writing. There does not appear to be one reason in particular for the selloff, however demand concerns remain in play with Japan and China reporting underwhelming factory data.

When you factor in that today is the first day of Q4, could rebalancing be at play as well? This is along the line of my thinking given the lack of any singular reason for the drop in price.

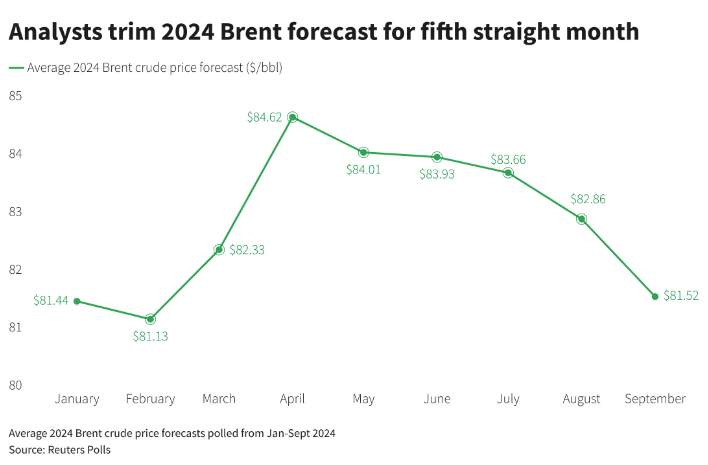

The Reuters September poll on Oil prices downgraded for a fifth consecutive month. This is in line with what we have been seeing of late with oil prices as there seems to be concern around demand and potentially excess supply in Q4 and 2024 and Q1 2025.

Looking more closely at the Reuters Poll of 41 analysts and economists conducted over the past two weeks, the projection for Brent Crude was revised down to 81.52 a barrel from a previous 82.86. (period average forecasts).

Source: LSEG, Reuters

This follows downgrades from both the IEA and OPEC + ahead of tomorrow’s meeting by the oil cartel. Markets still seem concerned that OPEC + may go ahead with an increase in production from December with many analysts believing the same. However, given the rhetoric from OPEC + members and Saudi Arabia and Russia in particular I think this may be a misguided notion. I foresee further delays in the production increase as long as oil prices remain in the lower $70-75 a barrel range.

China a Concern as Stimulus Needs Time to Take Effect

Meanwhile concerns were raised once more around China following the release of Manufacturing PMI data yesterday. This comes a week after the stimulus measures which have had a profound impact on the Chinese stock market as well as those of emerging markets and commodities.

However, on the Oil front there remains concerns that the stimulus will not be enough for China to reach its 2024 GDP target and may be too late to see a stark increase in oil demand. This could be another factor weighing on Oil in the European session.

Libya Oil Production and Oil Inventories

An agreement in Libya has also gained traction following yesterday’s announcement by Libya’s eastern based parliament that a new Central Bank Governor would be approved for nomination. This could see the return of Libyan Oil production and exports which could add around 1-1.5 million barrels back to the market at full capacity.

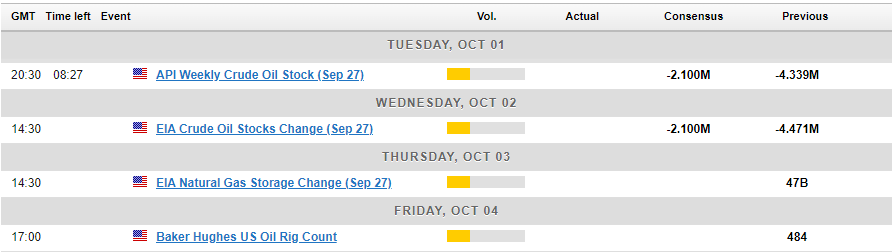

US PMI data this week could also have a minor impact on oil prices before inventory data will once again be key. A poll was conducted by Reuters for US Crude stockpiles which estimated a drop of around 2.1 million barrels for the week ended September 27, 2024. The API will release their data at 20h30 GMT on Tuesday.

Technical Analysis

From a technical perspective, oil has printed a lower high and looks poised for a lower low. However the whipsaw price action in European trade does not instill a lot of confidence in bears at this stage, so close to the psychological 70 a barrel mark.

The daily candle close today could go some way to providing a clearer picture in regard to Oils technical outlook in the near term.

Given the messy picture i have dropped down to a four-hour chart (H4) where we are seeing an aggressive bounce following the selloff this morning. This has now led to a RSI divergence play coming into focus as you can see on the chart below. RSI made a higher low while price made a lower low which could lead to a deeper recovery in oil prices.

Immediate resistance rests at 72.39 before the 100-day MA at 72.95. A break above this could open the door for an aggressive run toward the 200-day MA and the 75.00 psychological level,

Brent Crude Oil Daily Chart, October 1, 2024

Source: TradingView (click to enlarge)

Support

- 70.50

- 70.18

- 69.50 (key area of confluence)

Resistance

- 72.39

- 72.95

- 75.00

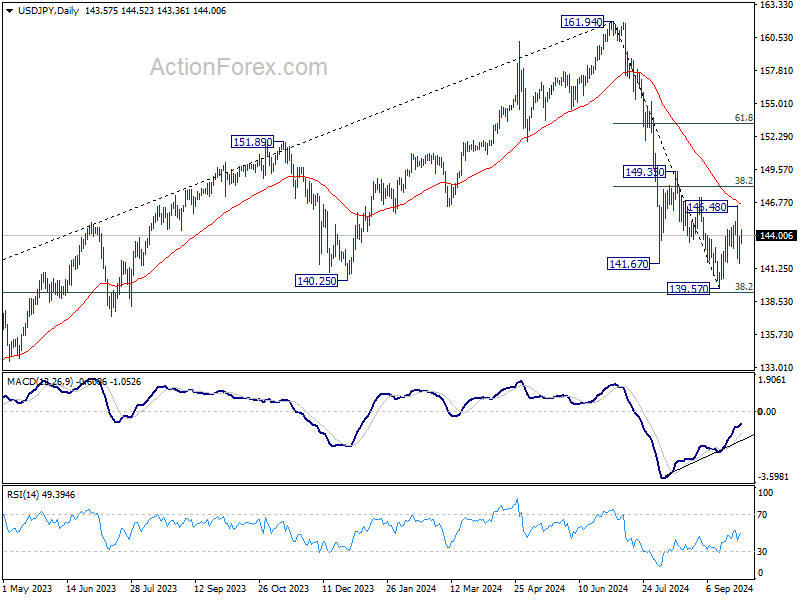

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.21; (P) 143.07; (R1) 144.48; More...

Intraday bias in USD/JPY remains neutral for the moment. On the downside, below 141.63 will target 139.57 low. But strong support could be seen again from 139.26 fibonacci level to bring rebound. On the upside, above 146.48 will resume the rebound from 139.57 to 38.2% retracement of 161.94 to 139.57 at 148.11. However, firm break of 139.26 will carry larger bearish implications.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

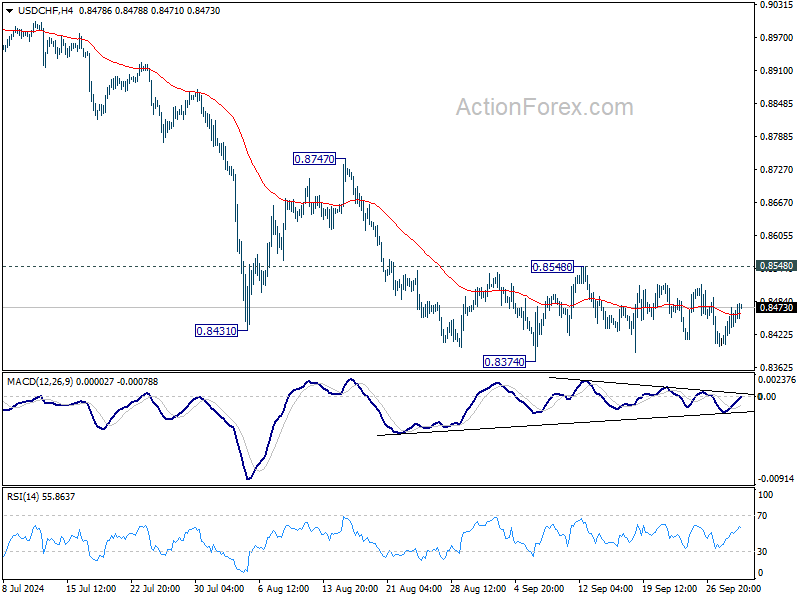

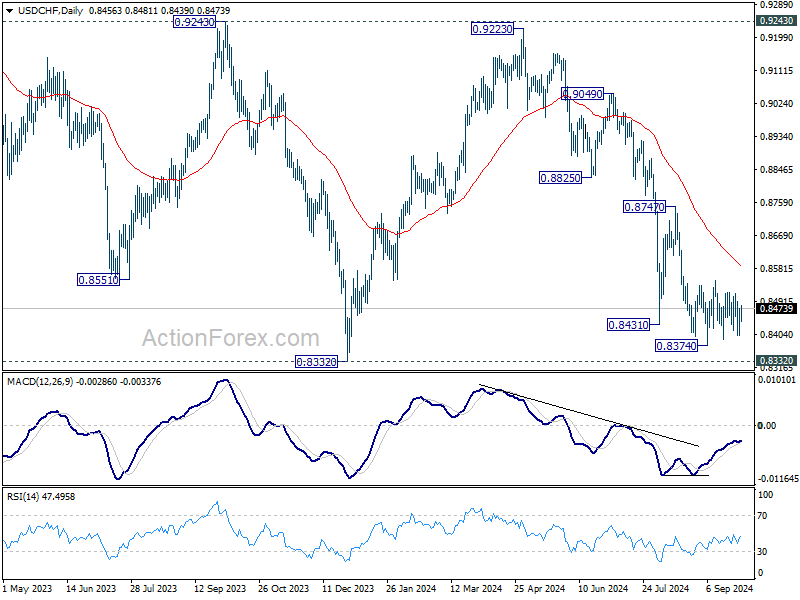

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8415; (P) 0.8445; (R1) 0.8486; More…

Intraday bias in USD/CHF remains neutral as range trading continues. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. Nevertheless, firm break of 0.8548 will turn bias back to the upside for stronger rebound to 0.8747 resistance instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

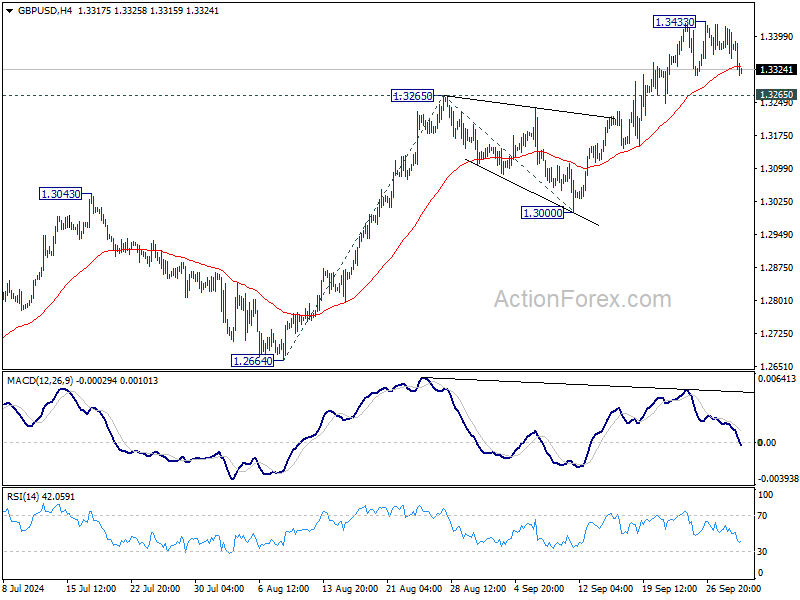

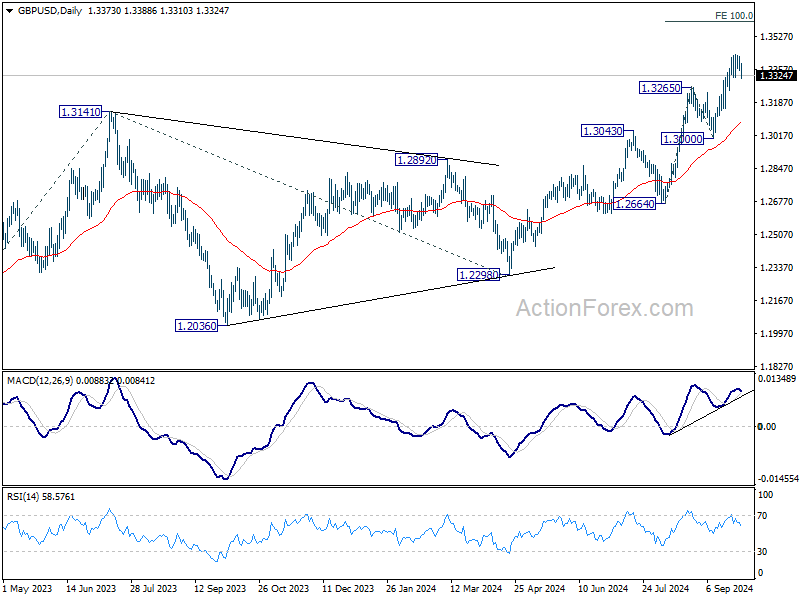

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3344; (P) 1.3383; (R1) 1.3417; More...

GBP/USD is extending consolidation from 1.3433 and intraday bias stays neutral. Further rally is expected as long as 1.3265 resistance turned support holds. Above 1.3433 will resume larger rise to 100% projection of 1.2664 to 1.3265 from 1.3000 at 1.3601 next. Nevertheless, considering bearish divergence condition in 4H MACD, firm break of 1.3265 will indicate short term topping and turn bias back to the downside for 1.3000 support instead.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. For now, outlook will stay bullish as long as 1.3000 support holds, even in case of deep pullback.

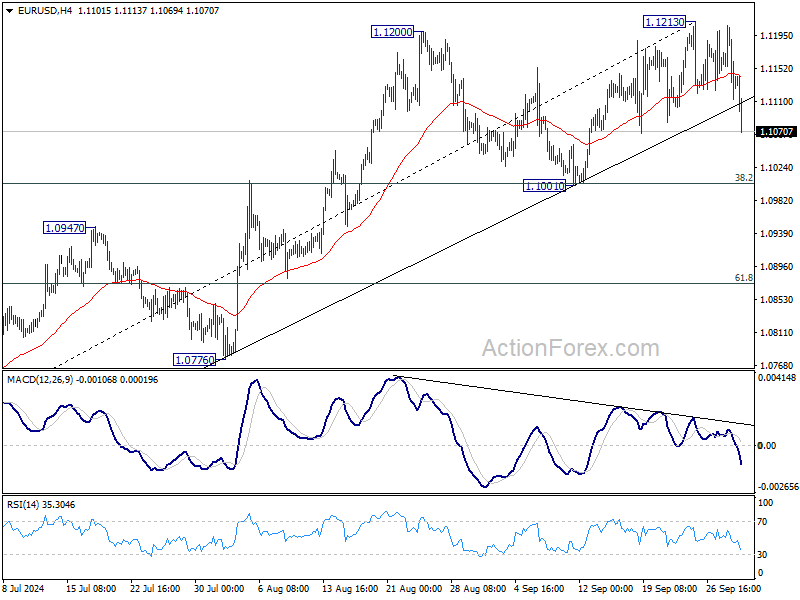

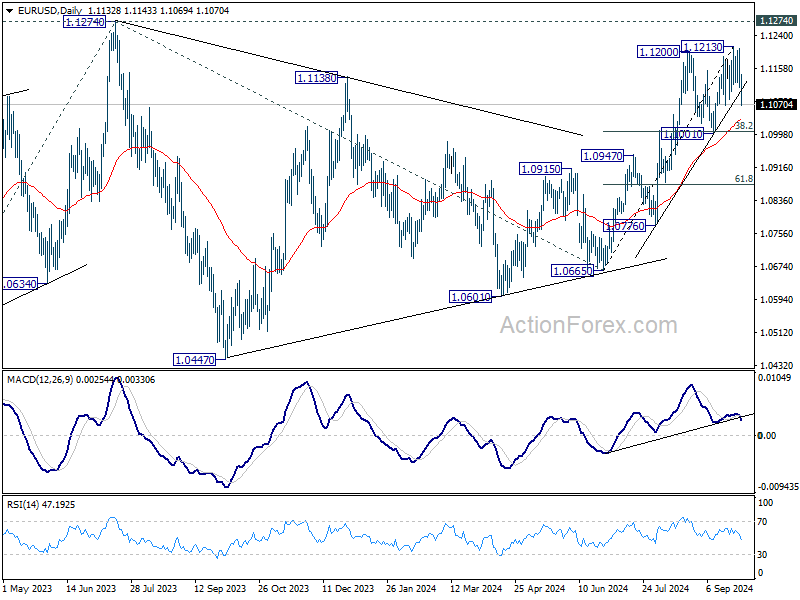

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1096; (P) 1.1153; (R1) 1.1191; More....

EUR/USD's pullback from 1.1213 accelerated lower today, and the break of trend line support indicates short term topping. While deeper fall might be seen outlook will stay bullish as long as 1.1001 cluster support holds (38.2% retracement of 1.0665 to 1.1213 at 1.1004). Break of 1.1213 will target 1.1274 high. However, decisive break of 1.1001/4 will confirm near term bearish reversal.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.

Euro Falls on Increased Bets of ECB Oct Rate Cut, Dollar Builds Momentum

Euro declined broadly today after ECB Governing Council member Olli Rehn became the first official to openly indicate that risks are now tilted toward another rate cut in October. Additionally, data showed that Eurozone's headline CPI fell below the ECB's 2% target for the first time since 2021, even though core inflation remains elevated.

A 25 bps cut at this month's ECB meeting is now nearly fully priced in, with major banks forecasting this outcome too. Market focus is also shifting to actions beyond October, with Deutsche Bank considering a 50 bps cut in December a close call.

Meanwhile, Dollar is gaining momentum, continuing to build on Fed Chair Jerome Powell's comments from yesterday. While Powell acknowledged that additional rate cuts are forthcoming, he emphasized there is no hurry to proceed with rapid policy easing. Robust ISM data and non-farm payroll figures due this week could reinforce expectations that Fed will opt for only a 25 bps cut in November.

In the currency markets, Japanese Yen remains the weakest performer for the week so far, but the gap is narrowing as it rebounds following declines in US and European yields. Swiss Franc is the second weakest, with Euro potentially overtaking it. Australian Dollar remains the strongest, buoyed by optimism in Chinese markets. Dollar is now the second strongest, followed by the Canadian Dollar, while New Zealand Dollar and British Pound are positioned in the middle.

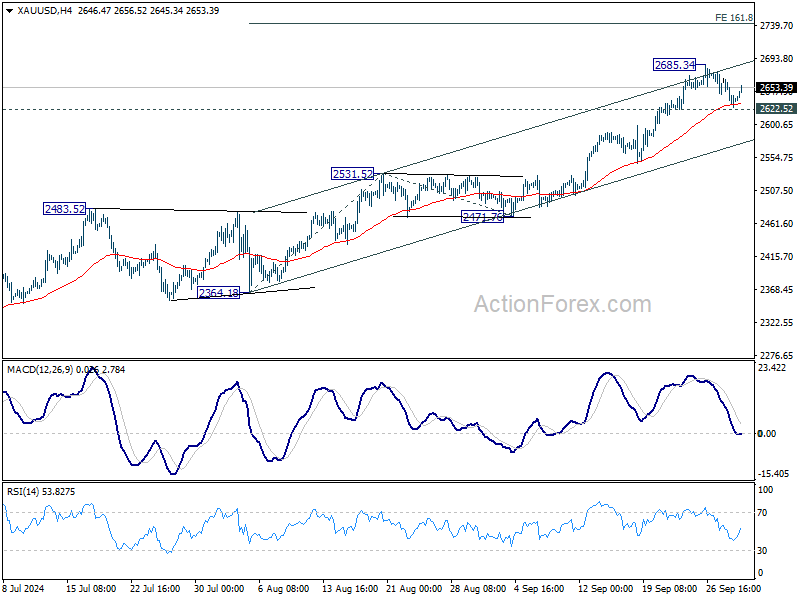

Technically, Gold's bounce today argues that pullback from 2685.34 has completed ahead of 2622.52 support, and that keeps near term outlook bullish. Break of 2685.34 will resume the long term up trend. Next target is 161.8% projection of 2364.18 to 2531.52 from 2471.76 at 2742.51.

In Europe, at the time of writing, FTSE is up 0.38%. DAX is up 0.59%. CAC is up 0.11%. UK 10-year yield is down -0.065 at 3.942. Germany 10-year yield is down -0.081 at 2.048. Earlier in Asia, Nikkei rose 1.93%. Japan 10-year JGB yield fell -0.0041 to 0.853. Singapore Strait Times fell -0.12%. Hong Kong and China were on holiday.

ECB’s Rehn sees growing case for Oct rate cut

ECB Governing Council member Olli Rehn suggested today that slowing inflation and weaker growth prospects in Eurozone has provided "more grounds" for another rate cut at the October meeting.

Additionally, Rehn pointed to the "prevailing headwinds" facing economic growth in the Eurozone, noting that these challenges "tilt the scales" toward a more accommodative policy stance.

He also cautioned that it is too early to declare a "soft landing" for the economy, as risks to growth remain prominent.

Rehn repeated ECB’s data-driven approach, adding, "let’s follow the figures closely and make a comprehensive analysis before making decisions, as always."

Eurozone CPI falls to 1.8% in Sep, CPI core down to 2.7%

Eurozone CPI fell from 2.2% yoy to 1.8% yoy in September, below ECB's 2% target for the first time since 2021. CPI core (ex-energy, food, alcohol & tobacco), ticked down from 2.8% yoy to 2.7% yoy. Both matched expectations.

Looking at the main components, services is expected to have the highest annual rate in September (4.0%, compared with 4.1% in August), followed by food, alcohol & tobacco (2.4%, compared with 2.3% in August), non-energy industrial goods (0.4%, stable compared with August) and energy (-6.0%, compared with -3.0% in August).

Eurozone PMI manufacturing finalized at 45, output and orders decline

Eurozone’s PMI Manufacturing was finalized at 45.0 in September, down from 45.8 in August, marking a 9-month low and reflecting further deterioration in the region’s manufacturing sector. Germany posted the weakest performance with a 12-month low PMI of 40.6, while Spain led with a 4-month high of 53.0.

According to Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, Eurozone industrial production is expected to decline by around -1% in Q3, with further contractions likely by year-end as new orders continue to fall sharply.

While lower oil and gas prices helped reduce input costs in September, de la Rubia warned that this relief could be temporary given ongoing geopolitical risks in the Middle East, which may lead to another spike in energy prices.

Adding to the challenges, supply-chain disruptions have worsened, despite weakening demand. For the first time since February, businesses reported longer wait times for goods, indicating that geopolitical tensions are affecting both supply chains and production across the Eurozone.

UK PMI manufacturing finalized at 51.5, confidence drops and price pressures rise

UK manufacturing sector expanded at a slower pace in September, with the PMI finalizing at 51.5, down from 52.5 in August.

According to Rob Dobson, Director at S&P Global Market Intelligence, the sector continues to expand at a "solid, albeit slightly slower, pace," supported by steady domestic demand. However, growing concerns are emerging, as business confidence for the year ahead has dropped to its lowest level in nine months.

The decline in optimism was notable, with only March 2020, just before COVID lockdowns, seeing a sharper fall. Uncertainty surrounding government policy ahead of the Autumn Budget is weighing heavily on sentiment, alongside broader concerns about global geopolitical risks and economic growth risks.

Inflationary pressures have intensified, with input cost inflation reaching a 20-month high. Manufacturers are being forced to raise prices as a result, with rising freight costs cited as a major contributor. Ongoing supply chain disruptions, driven by the Red Sea crisis and global conflicts, are exacerbating these price increases, keeping inflationary pressures elevated across the sector.

BoJ opinions highlight divergence over timing of future rate hikes

The Summary of Opinions from BoJ's meeting on September 19 and 20 acknowledged that while outlook for Japan's economic activity and inflation will guide future changes in monetary accommodation, policymakers remain vigilant about developments in overseas economies, particularly the US, and their potential impact on Japan's financial markets and price stability.

With Yen's depreciation retracing and import price pressures easing, one view noted that BoJ has "enough time to assess the situation". Another opinion stressed that Japan's economy is not at risk of "falling behind the curve" if interest rates are not raised swiftly. BoJ should not raise interest rate when "financial and capital markets are unstable".

Another member suggested that while price stability has not yet been achieved and uncertainties persist, a shift to "full-fledged monetary tightening" would be undesirable at this stage.

However, a contrasting opinion within the BoJ indicated that if economic conditions remain stable and the outlook is confirmed, it would be preferable for the bank to raise rates "without taking too much time."

This divergence highlights the ongoing debate within BoJ about the timing of future rate hikes.

Japan's Q3 Tankan shows stability in manufacturing, slight gains in non-manufacturing

Japan's Q3 Tankan Large Manufacturing Index remained steady at 13, unchanged from Q2 and in line with market expectations, indicating stability in the country's manufacturing sector. Manufacturers’ outlook for the next three months improved slightly to 14, signaling cautious optimism about future business conditions.

Large Non-Manufacturers Index showed a modest rise to 34, up from 33 in June, surpassing expectations of 32. However, the outlook for non-manufacturers over the next three months dipped to 28, reflecting some uncertainty in the service and retail sectors.

Capital spending plans by big companies were revised down, with firms now expecting a 10.6% increase for the fiscal year ending in March 2025. This is below the median forecast of an 11.9% rise and down from an 11.1% forecast three months ago, suggesting some cooling in business investment intentions.

The Tankan survey results will be closely monitored by BoJ as it prepares for its monetary policy meeting on October 30-31, where it will set new growth and inflation forecasts.

Japan’s PMI manufacturing PMI finalized at 49.7, output and new orders in contraction

Japan's Manufacturing PMI for September was finalized at 49.7, marginally lower than August's reading of 49.8, signaling continued contraction in the sector.

According to Usamah Bhatti from S&P Global Market Intelligence, the data reflected "muted trends" in Japan's manufacturing industry. Both output and new orders remained in negative territory, while the rate of job creation "slowed to a crawl."

While businesses expressed optimism about output growth over the next 12 months, the level of optimism softened, marking the weakest positive outlook since the end of 2022. Some manufacturers highlighted concerns over the "timing of a demand recovery," reflecting cautiousness in the face of global and domestic uncertainties.

Australia's retail sales rises 0.7% mom in Aug, driven by record warm weather

Australia's retail sales turnover increased by 0.7% mom in August, surpassing the expected rise of 0.4% mom. On a year-over-year basis, retail sales were up 3.1%. This stronger-than-expected growth was largely attributed to unusually warm weather, which boosted spending on items typically associated with spring.

Robert Ewing, head of business statistics at the Australian Bureau of Statistics (ABS), explained that “this year was the warmest August on record since 1910, which saw more spending on items typically purchased in spring." Categories that saw increased demand included summer clothing, liquor, outdoor dining, hardware, gardening supplies, camping gear, and outdoor equipment.

NZ business confidence surges as firms anticipate more RBNZ rate cuts

NZIER Quarterly Survey of Business Opinion reveals significant improvement in business confidence in New Zealand during Q3. A net 5% of firms now expect deterioration in general economic conditions, a stark improvement from the net 40% expressing pessimism in the June quarter.

Firms are still facing challenges in demand. A net 31% of businesses reported weaker trading activity. However, looking ahead, only a net 2% of firms expect activity to decline in the next quarter.

This shift in sentiment comes as firms anticipate more supportive economic conditions following RNBZ's decision to begin cutting interest rates in August, with expectations of further reductions in the coming year.

Cost pressures remained present, with a slight increase in the proportion of firms reporting higher costs. However, pricing power has diminished significantly, with only a net 3% of firms able to pass on these costs to consumers, compared to 23% in the previous quarter.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1096; (P) 1.1153; (R1) 1.1191; More....

EUR/USD's pullback from 1.1213 accelerated lower today, and the break of trend line support indicates short term topping. While deeper fall might be seen outlook will stay bullish as long as 1.1001 cluster support holds (38.2% retracement of 1.0665 to 1.1213 at 1.1004). Break of 1.1213 will target 1.1274 high. However, decisive break of 1.1001/4 will confirm near term bearish reversal.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Aug | -5.30% | 26.20% | 26.40% | |

| 22:00 | NZD | NZIER Business Confidence Q3 | -1 | -44 | ||

| 23:30 | JPY | Unemployment Rate Aug | 2.50% | 2.60% | 2.70% | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 13 | 13 | 13 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 14 | 14 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q3 | 34 | 32 | 33 | |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q3 | 28 | 27 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 10.60% | 11.90% | 11.10% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 00:30 | JPY | Manufacturing PMI Sep F | 49.7 | 49.6 | 49.6 | |

| 00:30 | AUD | Retail Sales M/M Aug | 0.70% | 0.40% | 0.00% | 0.10% |

| 00:30 | AUD | Building Permits M/M Aug | -6.10% | -4.30% | 10.40% | 11.00% |

| 06:30 | CHF | Real Retail Sales Y/Y Aug | 3.20% | 2.60% | 2.70% | 2.90% |

| 07:30 | CHF | Manufacturing PMI Sep | 49.9 | 48.2 | 49 | |

| 07:45 | EUR | Italy Manufacturing PMI Sep | 48.3 | 49.4 | 49.4 | |

| 07:50 | EUR | France Manufacturing PMI Sep F | 44.6 | 44 | 44 | |

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 40.6 | 40.3 | 40.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 45 | 44.8 | 44.8 | |

| 08:30 | GBP | Manufacturing PMI Sep F | 51.5 | 51.5 | 51.5 | |

| 09:00 | EUR | Eurozone CPI Y/Y Sep P | 1.80% | 1.80% | 2.20% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep P | 2.70% | 2.70% | 2.80% | |

| 13:30 | CAD | Manufacturing PMI Sep | 49.5 | |||

| 13:45 | USD | Manufacturing PMI Sep F | 47 | 47 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | 47.8 | 47.2 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 55 | 54 | ||

| 14:00 | USD | Construction Spending M/M Aug | 0.20% | -0.30% |

EUR/USD Rate Accelerates Decline Following European Inflation News

According to the Eurostat data released today:

→ Core CPI Flash Estimate (YoY): actual = 2.7%, expected = 2.7%, previous = 2.8%;

→ CPI Flash Estimate (YoY): actual = 1.8%, expected = 1.8%, previous = 2.2%.

This news, coupled with yesterday’s statements from the Fed Chair, led to the EUR/USD rate dropping by over 1% from yesterday’s high.

Could the downward trend continue?

Technical analysis of the EUR/USD chart shows that:

→ In the second half of September, bullish sentiment dominated, resulting in the formation of an ascending channel (shown in blue). However, near the key resistance at 1.1200 (drawn from the August peak), the bullish momentum faded, and the price entered a range between 1.1200 and 1.1122.

→ The bearish momentum that started from yesterday’s peak (B) is developing strongly. The price has broken both the lower boundary of the 1.1122 range and the lower boundary of the blue channel. Moreover, it has dropped below 1.1108, approximately the 50% retracement of the A→B rise.

This suggests that the first day of October could see bulls losing much of the gains from the previous month. A glimmer of hope for them may lie in the psychological support at 1.1080.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.