Sample Category Title

Stocks’ Positive Reaction Might Continue Until the Second Fed Rate Cut

- The Fed announced its first rate cut with a relatively balanced rhetoric

- History points to a high probability of back-to-back moves

- Dollar/yen and Treasury yields tend to drop until the second rate cut

- Barring a major event, stocks’ positive performance could continue

The Fed commenced its monetary policy easing cycle in aggressive fashion by announcing an almost unanimous decision to cut rates by 50bps. The markets were surprised with the US dollar suffering the most. Both the accompanying policy statement and the press conference were relatively balanced as Chairman Powell tried very carefully to avoid scaring the market by talking down the US economy.

The Fed is probably on a preset course, despite Powell advertising the meeting-by-meeting approach shared by other central banks. The dot plot revealed two additional 25bps rate cuts penciled in by Fed members for 2024, slightly below market expectations for another 72bps of easing this year. What does history tell us about the timing and size of the second Fed cut?

Is it standard practice for the Fed to announce back-to-back rate cuts?

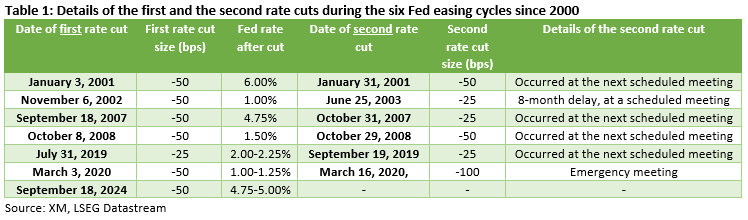

Continuing from a previous special report where six easing cycles were identified since 2000, table 1 below presents the details of the Fed’s first and second rate cuts. As made evident, Fed members decided to cut rates again at the next scheduled meeting in four of the six examined cycles, increasing the possibility for a November 7 rate move.

Interestingly, Fed decisions varied from a 100bps rate cut in 2020, during the outbreak of the Covid pandemic, to just 25bps moves in 2002, 2007 and 2019, when the US economy was not falling off a cliff. Also, the time between the first and the second Fed rate cuts fluctuated from just 13 days in 2020 to almost 8 months in 2002, as the Fed traditionally tries to act appropriately in order to meet its dual mandate.

The next Fed meeting is scheduled for November 7, two days after the US presidential election day. Quite possibly, the result of the election might not be yet finalized, especially if the Republican presidential candidate is losing the battle. This raises the possibility of the Fed refraining from announcing another rate cut until the new president is declared. However, the market is convinced that the November rate cut is a done deal, and it is even assigning a sizeable 43% probability for another 50bps move.

How did the market perform between the first and second Fed rate cuts?

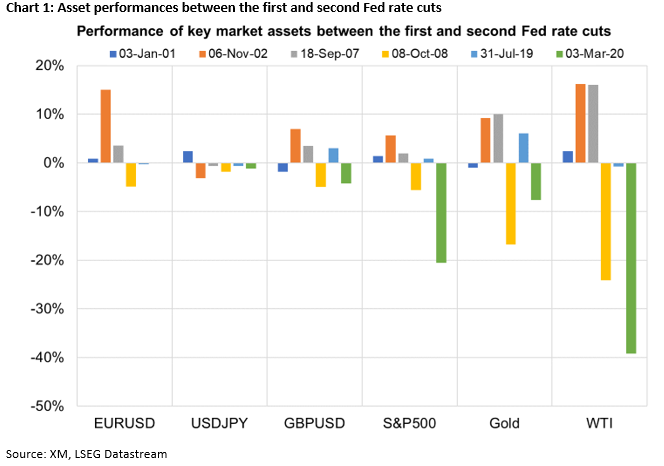

Chart 1 below presents the performance of key market assets in the period between the first and the second Fed rate cuts. Interestingly, dollar/yen dropped by an average of 1.5% in the last five easing cycles, a performance that could repeat this time around as the Bank of Japan is still open to further rate hikes in 2024.

Similarly, US treasury yields tend to fall in the examined time period, with one grave exception. In 2008, yields rose by 20bps as the US administration borrowed heavily from the bond market in order to fund its relief programmes.

Performance for certain assets depends on the underlying economic conditions

As seen in chart 1 below, the remaining assets exhibit a relatively mixed performance. However, digging through the results there is a common pattern emerging in pound/dollar, S&P 500 index, gold and WTI oil price. In periods of distress like 2008 and 2020, these four key assets tend to drop aggressively. For example, the S&P 500 index fell by 5.6% and 20.6% respectively in these two instances, and WTI oil prices collapsed.

In periods of normal economic conditions, like the current situation, the Fed has traditionally opted for a more relaxed approach in terms of its rate cuts. As a result, in 2001, 2002, 2007 and 2019, pound/dollar, S&P 500 index, gold and WTI oil exhibited a stronger tendency to rally. More specifically, the S&P 500 index increased by an average of 2.4% in these four periods, while both gold and WTI oil showed a decent appetite for double-digit jumps.

Putting everything together, dollar/yen and the 10-year US treasury yield tend to decrease in the period between the first and the second Fed rate cuts. The performance of other key assets like pound/dollar, the S&P 500 index, gold and WTI oil depends on the underlying economic conditions. As such, in both 2008 and 2020 these assets dropped aggressively, while during the period between the first and the second Fed rate cuts in 2001, 2002, 2007 and 2019, they recorded strong gains.

The Weekly Bottom Line: Canada – Inflation Hits the Mark

U.S. Highlights

- The Federal Reserve started its easing cycle with a bang, reducing the policy rate by 50 basis points (bps), bringing the target range to 4.75%-5.0%.

- Futures markets are pricing an additional 75 bps of cuts by year-end, slightly more than the updated median FOMC forecast, which shows another 50 bps of cuts.

- Economic data out this week including retail sales, housing starts, and industrial production all came in stronger than expected. Our Q3 GDP tracking sits a 2.1%.

Canadian Highlights

- Headline inflation clocked in at the Bank of Canada’s (BoC’s) 2.0% year-on-year target in August. This marks a symbolic accomplishment for an economy that has been struggling to deal with high inflation for the last three years.

- Retail sales pointed to a strong summertime bounce back, while housing starts and house price growth continue to ebb in the face of still high interest rates.

- The stabilization in inflation has raised odds that the BoC follows the Fed with an outsized 50 basis point cut at either its October or December meeting.

U.S. – FOMC Starts Easing Cycle With a Bang

There was no doubt heading into this week that the Federal Reserve would be cutting its policy rate on Wednesday. What remained in question, was the size of the cut. Right up until the announcement, market pricing remained relatively split on whether the FOMC would cut by 25 or 50 basis points (bps). Ultimately, policymakers opted for the bigger cut and signaled more easing to come. The more dovish tilt pushed U.S. equity markets higher, with the S&P 500 up just over 1% for the week at the time of writing.

Accompanying the policy statement, the FOMC also released revised economic forecasts, known as the Summary of Economic Projections (SEP). The SEP is an aggregation of each Committee members’ individual forecasts but are not “official” Fed projections. Overall, the median forecast showed that the growth outlook remained little changed relative to the June forecast, with GDP still expected to expand by 2.0% per-year between 2024 and 2027. However, the unemployment rate was revised higher for both 2024 and 2025, and core PCE inflation was marked down in both years.

Consistent with the FOMC’s expectations for a slightly softer labor market, and cooler inflation, there were notable downward revisions to the median interest rate outlook (i.e., the “dot plot”) for 2024 through 2026. The revised forecast now shows a total of 100 bps of easing by the end of this year (previously 25 bps) with another 100 bps of cuts projected for 2025, corresponding to a target range of 3.25%-3.5% (Chart 1). This is 75 bps lower than the June SEP.

In the press conference, Chair Powell characterized the larger cut as a “strong start”, but also reiterated that future reductions in the policy rate were by no means on a preset course. Moreover, the Chair pushed back on the notion that this week’s outsized move was driven by a fear that the FOMC had fallen behind the curve. However, he did state that had the FOMC known back at the July 30-31 meeting that the labor market would have cooled as much as it did in the months that followed that rate decision, they probably would have started the easing cycle sooner.

As noted in our recent Quarterly Forecast, we feel that odds favor another 50-bps cut in November. If policymakers are truly concerned that today’s policy stance is too restrictive, it’s more likely that they will want to act quickly to alleviate the pressure, before slowing the pace in December.

This is not a guarantee. The Fed remains data dependent, and nearly all economic data out this week including retail sales, industrial production, housing starts, and initial jobless claims came in better than expected, and remain consistent with an economy that’s still expanding in the 2-2.5% range. Next week’s personal income and spending data will provide more insight on August spending trends and is also likely to show a bit more progress on easing inflationary pressures (Chart 2). But it’s the September and October employment reports that could ultimately be the deciding factor of whether the Fed cuts by 25 or 50 bps in November.

Canada – Inflation Hits the Mark

The U.S. Federal Reserve’s outsized 50 basis point (bp) cut may have dominated headlines, but it was still a busy week for Canadian economic data. Canadian Consumer Price Index (CPI) inflation made a big downward move, hitting the Bank of Canada’s (BoC’s) 2% target (Chart 1). We also got another reading on the housing market, which is still weighed down by high rates. Retail sales, however, sprung to life during the summer months. Progress on inflation and likely some hope the BoC will take its cue from the Fed has led financial markets pricing for the next BoC move to swing between another 25 bp cut in October or a larger 50 bp cut.

Headline inflation clocked in at 2.0% year-on-year (y/y) in August – bang on the central bank’s target. This marks a symbolic accomplishment for an economy that has been struggling to deal with high inflation for the last three years. Even more impressive was that this occurred while services inflation continues to run at a +4% y/y pace. Shelter inflation remains the culprit here, but when we strip out this impact, inflation has slowed to a tepid 0.5% y/y pace.

The continued deceleration in the BoC’s two preferred core inflation rates was also encouraging. Coming in at 2.3% y/y and 2.4% y/y in August (down from 2.4% y/y and 2.7% y/y in July), these rates are effectively at the BoC’s target. The underlying trends in core inflation make us believe that the easing in core rates should be sustained. Not only are the more recent trends in core inflation stabilizing around 2% (on a three-month annualized basis), but the share of goods and services with inflation running hot (the percent of CPI items growing +3%) has returned to historical norms. Couple this with a clear slowing in the real economy – rising unemployment – and we have all the ingredients for inflation to stabilize at current levels.

Speaking of weakness, the Canadian housing market remains stuck in neutral. This week we saw housing prices fall again in August as sales have yet to respond to recent BoC rate cuts. Builders have taken notice of this lackluster demand, resulting in housing starts plunging by double-digits in August. On a positive note, retail sales rebounded in the summer months, driven by a bounce-back in motor vehicle and parts dealers, following a series of cyberattacks that hit retailers in June. Even with this recovery, economic growth is still expected to run below its potential in the third quarter, despite the working age population increasing close to 4% on the quarter!

The BoC’s policy meeting deliberations released this week alongside a slew of speeches have signaled that the bank is done with seeing Canadian economic growth underperform its potential. While that intention is all well and good, our updated quarterly forecast points to continued weakness in the coming months. This will keep the central bank in cutting mode (Chart 2), and possibly at an even quicker pace than we have seen thus far. Market participants are already considering this possibility, with pricing nudging towards a 50 bps move at the bank’s upcoming announcement in October or December.

Weekly Economic & Financial Commentary: An Update to Our Fed Funds Forecast

Summary

United States: Recalibrating the Monetary Policy Stance

- The commencement of monetary policy easing comes at a time when overall economic growth remains solid, supported by stronger-than-expected retail sales, industrial production and residential construction in August. Yet, signs of labor market weakness have posed meaningful threats to the sustainability of growth, which underpinned the FOMC's decision to start the easing cycle with a 50 bps cut, rather than a conventional 25 bps move.

- Next week: New Home Sales (Wed.), Durable Goods (Thu.), Pers. Income & Spending (Fri.)

International: Central Bank Rate Divergences Are Apparent Again

- Central banks were in the spotlight this week. Not just the Federal Reserve, but foreign central banks as well. Institutions across the advanced and emerging markets met to discuss and decide monetary policy settings.

- Next week: Eurozone PMIs (Mon.), Reserve Bank of Australia (Tue.), Bank of Mexico (Thu.)

Interest Rate Watch: An Update to Our Fed Funds Forecast

- The Federal Open Market Committee (FOMC) opted to reduce the target range for the federal funds rate by 50 bps at its meeting this week. Based on what we know now, we believe the FOMC probably leans toward downshifting to a 25 bps pace going forward. Accordingly, we look for the FOMC to cut the federal funds rate by 25 bps at each of its two remaining meetings of the year.

Topic of the Week: Mexico Passes Sweeping Judicial Reforms

- In Mexico, a constitutional amendment that calls for an overhaul of the country’s judicial branch passed through local congress, leaving market participants wondering what the financial, economic and governance-related implications may be. We remain cautiously optimistic on the prospects for Mexican financial markets and the peso for now, though we will be closely watching any developments with ratings agencies' assessment of the country's debt.

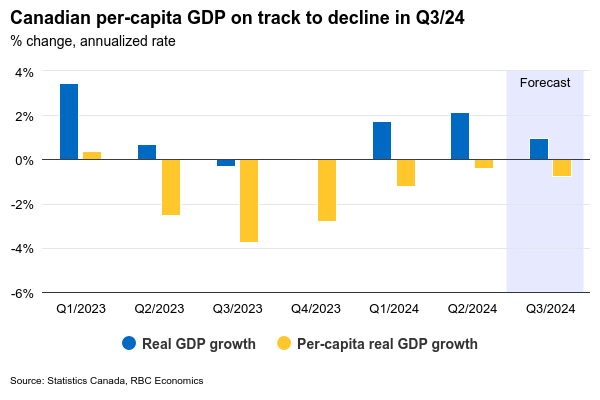

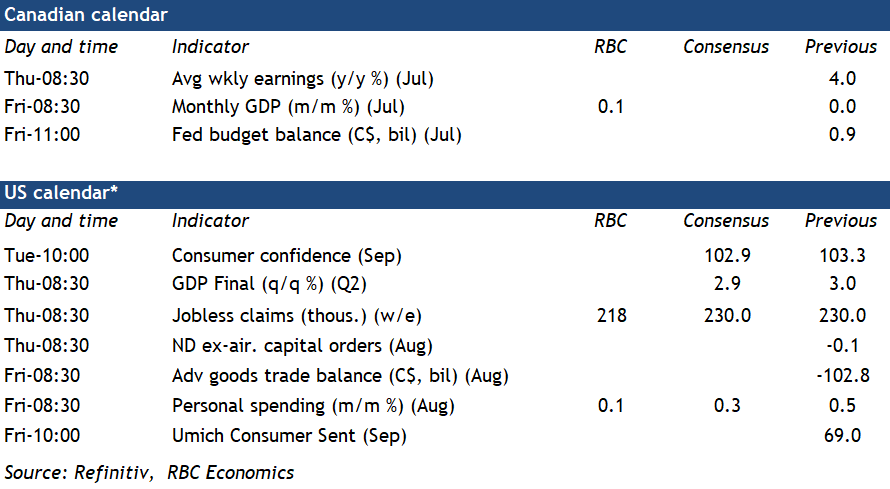

Canadian GDP to Show Modest Growth in July But Below BoC Forecast

Canada’s gross domestic product report for July next Friday will be closely watched to see if cooling in the economy in late Q2 extended into Q3.

Early reports are pointing to a 0.1% increase in July GDP that would be slightly higher than the advance estimate for an unchanged reading a month ago but would still extend a string of softer readings dating back to May. Most of a 2.1% annualized increase in Q2 GDP came from a 0.4% jump in output in April. Growth softened to 0.1% in May followed by no growth in June. The increase we expect in July is still historically soft and would leave output tracking another per-capita GDP decline in Q3—marking the eighth out of the last nine quarters.

We expect the small increase in July growth was evenly split across goods and services. The details of the July manufacturing sales report are consistent with a 0.6% increase in manufacturing GDP. But, a drop in oil sands production in Alberta and a pull-back in oil drilling activity is expected to weigh on growth. Meanwhile, wholesale and retail sales were both up in July, but our tracking of credit card transactions is pointing to little change in spending in the hospitality sector.

Slowing inflation has allowed the Bank of Canada to shift focus to concerns about a softening economy and a rising unemployment rate. Our forecast of around 1% annualized growth in Q3 GDP would be well below the BoC’s July forecast for a 2.8% increase. Our base case forecasts assume the BoC will continue cutting interest rates at a pace of 25 basis points per meeting, but with risks tilted to a faster pace of reductions (in line with the U.S. Federal Reserve’s larger 50 bps initial cut) if the economy softens significantly further.

Week ahead data watch

We expect U.S. personal consumption to edge up 0.1% in August, down from 0.5% in July. Retail sales growth slowed in August on softer auto sales and lower sales at gas stations. U.S. personal income likely increased by 0.4% in August from 0.3% in the previous month. It's consistent with higher wage growth from July to August.

Canadian July SEPH data will be watched closely for further signs of cooling in the labour market. The previously released Labour Force Survey showed a small 3,000 dip in employment in July, followed by a 22,000 bounce back in August. But job openings (captured in SEPH, not the LFS) likely continue to decline on slowing hiring demand. Wage growth in SEPH will also be in focus, because it has been underperforming the same measure in LFS.

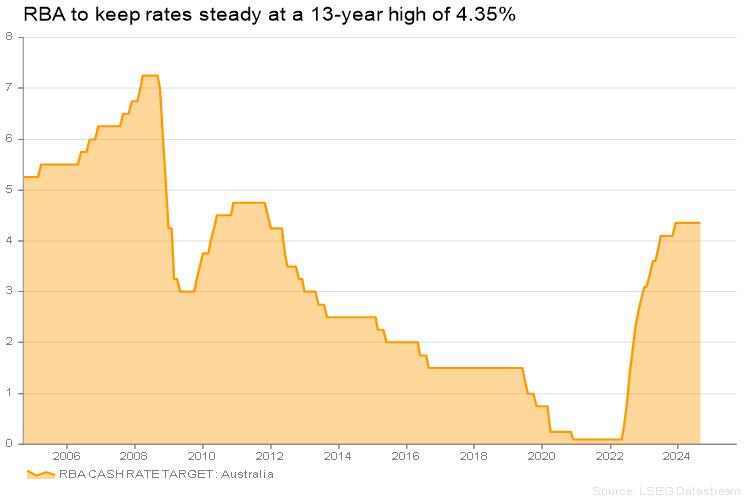

RBA Policy Meeting : It’s Not Time for a Rate Cut Yet

- RBA expected to deviate from the Fed and hold rates steady

- Inflation risks remain a concern; labor market is tight

- AUDUSD faces resistance near 0.6835; next barrier around 0.6875-0.6900

RBA to keep rates steady

It will be time for the Reserve Bank of Australia (RBA) to announce its rate decision when its policy meeting concludes on Tuesday, but don't expect a Fed-like rate surprise.

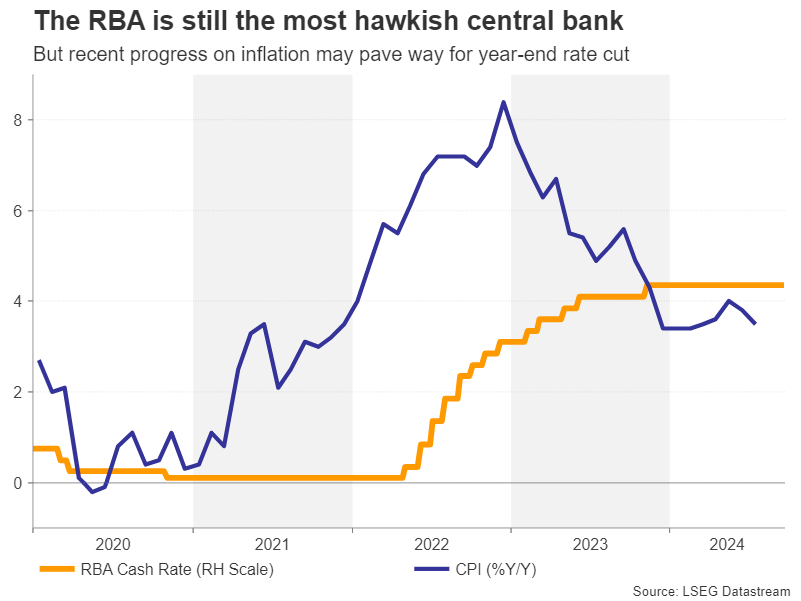

The RBA hasn’t started the phase of rate cuts yet and may stay out of it for the seventh consecutive meeting, keeping interest rates on hold at 4.35% next week. This is lower than the Fed’s and the BoE’s benchmark rates, which peaked higher, and with Australian inflation edging slightly up to 3.8% y/y in Q2 from 3.6% y/y in Q1, policymakers may reasonably abstain from any accommodative moves.

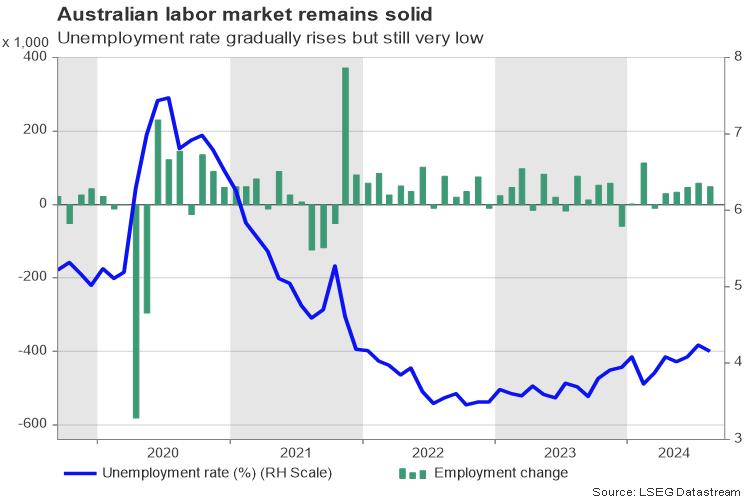

Australian labor market stays solid

Headlines in the labor market have been encouraging since the previous gathering. Employment continued to grow steadily above the pre-pandemic average of 30k for the fifth consecutive month in August, beating analysts’ expectations by a wide margin. The last time Australian jobs showed nonstop growth for more than five months was in 2021.

A steady unemployment rate was also good news despite the measure stabilizing slightly above the record low of 3.5%, and with the participation rate holding near all-time high, the labor market remains tight compared to historical standards and a source of inflationary pressures according to the RBA chief economist Sarah Hunter. Therefore, the labor market is not a serious catalyst yet for a dovish policy turn, meaning the central bank might keep the sentence which states “policy should remain sufficiently restrictive” in place for a bit longer.

Will there be a rate cut this year?

Yet, the economy is not in great shape. The overall pace of economic growth is pale at 0.2% q/q and 1.0% y/y as of Q2, making investors wonder about how long the central bank can wait before cutting interest rates. According to futures markets, investors pushed back their rate cut projections from November to December following the latest upbeat jobs report, but kept the odds below 50%. Instead, they feel more confident that the easing phase may start in February 2025 and include four rate cuts by the end of the year.

AUDUSD levels to watch

In FX markets, AUDUSD has been benefiting from the RBA-Fed policy divergence, hitting a nine-month high of 0.6837 on Thursday. Persisting hawkish signals similar to the August meeting, including steady rates by the end of the year and inflation concerns, may not surprise investors. Perhaps, the aussie could enjoy some gains if the odds for a 25bps rate cut move beyond December to February. Technically, a bounce above 0.6835 could immediately pause within the 0.6875-0.6900 zone. If not, the 0.6980 area taken from February 2023 could be the next obstacle.Alternatively, although the central bank has all the excuses to stand pat on rates, a surprising dovish communication, suggesting the central bank could cut its borrowing costs earlier in 2025 or even in December 2024, might prompt a rapid downfall to 0.6700-0.6740 and then to 0.6620.Later in the week, monthly CPI figures for August could generate fresh volatility in the aussie on Wednesday, while Australian Q3 job vacancies and the RBA’s financial stability review might cause some movement on Thursday.

Week Ahead – SNB to Cut Again, RBA to Stand Pat, PCE Inflation Also on Tap

- SNB is expected to ease for third time; might cut by 50bps

- RBA to hold rates but could turn less hawkish as CPI falls

- After inaugural Fed cut, attention turns to PCE inflation

- September flash PMIs to do the rounds; spotlight on euro area

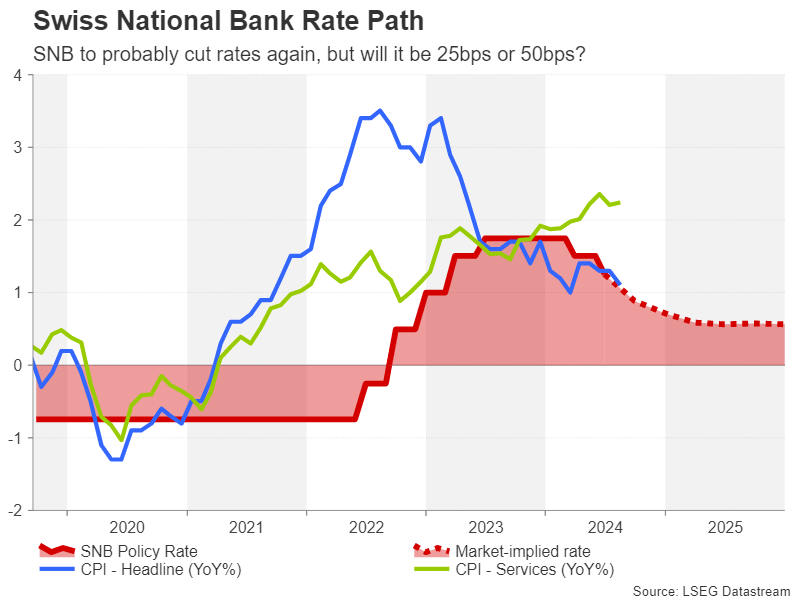

SNB to keep trimming as strong franc bites

The Swiss National Bank (SNB) will be the final major central bank to announce its policy decision in September. Like the Fed, there is a substantial degree of uncertainty around the size of the cut.

Investors have priced in around a 60% probability of a 25-basis-point rate reduction, with the remaining odds being for a 50-bps move. Expectations for a larger cut have gained ground since the beginning of August when the Swiss franc spiked higher against the US dollar and euro.

SNB chief Thomas Jordan, who will chair his last meeting on Thursday before stepping down at the end of the month, has been quite vocal in expressing his displeasure at the franc’s strength amid calls by Swiss exporters for the central bank to do more to stem the currency’s appreciation.

The franc started the year on the backfoot after hitting nine-year highs versus the dollar and euro in December, but reverted to bullish mode in May, erasing its losses.

This has helped push inflation lower in Switzerland; headline CPI fell to 1.1% y/y in August. However, under the bonnet, the inflation picture isn’t quite so subdued as services CPI has been slowly edging higher this year. Moreover, the GDP data does not point to a particularly dire situation for manufacturers.

Thus, despite the grievances about a stronger franc, the case for a 50-bps cut isn’t very convincing. Besides, the SNB has already lowered borrowing costs twice this year by a total of 50 bps and opting for a double cut would deplete its arsenal as the policy rate currently stands at just 1.25%.

Nevertheless, a 50-bps reduction on Thursday would still send a clear signal to traders, potentially sparking a selloff in the franc and offering some respite to the export industry, at least in the short term.

No rate cuts in Australia

Prior to the SNB meeting, it will be the turn of the Reserve Bank of Australia to announce its decision on Tuesday. Although inflation in Australia has started to come down again, taking the pressure off the RBA to hike interest rates further, a cut seems some way off.

The monthly CPI prints for August are due on Wednesday so policymakers may not necessarily have access to the latest data. But even if CPI were to fall further, having dropped to 3.5% y/y in July, the RBA is unlikely to want to discuss a rate cut just yet.

However, it’s possible that policymakers will sound less concerned about the upside risks to inflation and a change in tone could pressure the Australian dollar. Yet, a major policy pivot is not likely before the November meeting when economic projections will be updated. Even then, the markets are ahead of themselves and have already priced in about a 70% probability of a 25-bps rate cut by December, so further downside may be limited for the aussie.

Dollar turns to core PCE for support

The Fed may have surprised markets when it slashed rates by a larger-than-expected 50 basis points at its September meeting, but it’s important to highlight that policymakers have not yet declared victory over inflation. And whilst the decision to kick off the easing cycle with a larger increment can be interpreted as a dovish move, Fed officials are not anticipating further big reductions, and 25-bps cuts are more probable if the latest dot plot is to be believed.

This seems to have put a temporary floor underneath the US dollar, as the sharp selloff over the summer that preceded the September decision may take a breather. Alternatively, investors will be looking for fresh clues on inflation that could potentially bolster dovish expectations.

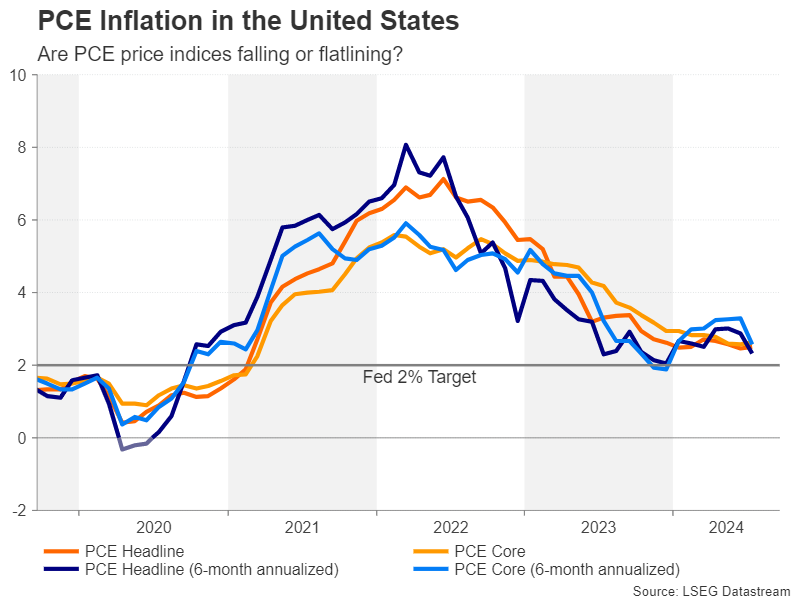

The PCE measures of inflation are due on Friday, along with the personal income and consumption numbers. In July, headline PCE was unchanged at 2.5% while core PCE held steady at 2.6%. Both appear to be flatlining above the Fed’s 2% goal. However, when looking at the 6-month annualized figures, there was a sharp drop in July, suggesting that the PCE gauges will resume their decline over the coming months. This may even have been a factor in the Fed’s decision to lower rates by 50 bps instead of 25 bps.

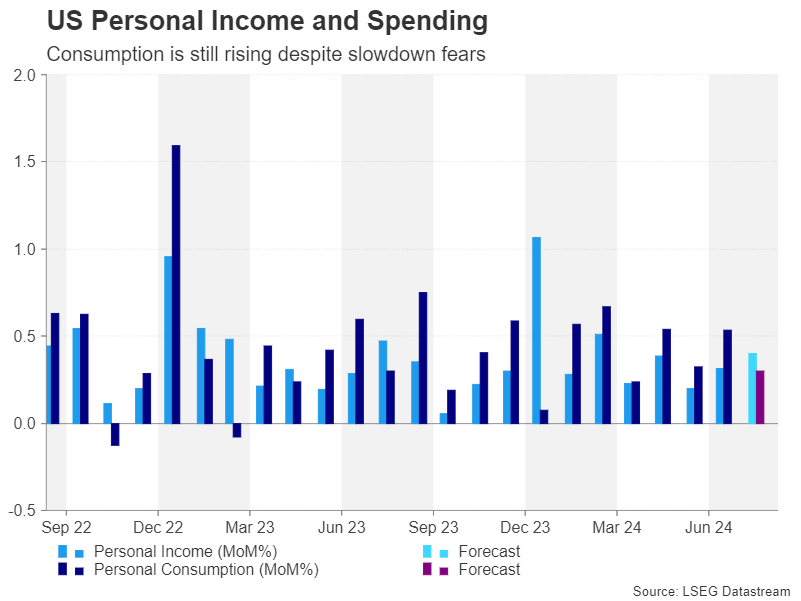

Further supporting the Fed’s actions is the moderation in consumer spending. Personal spending is expected to have risen by 0.3% m/m August after rising by 0.5% m/m in July. Personal income is forecast to have grown by 0.4% m/m.

Ahead of Friday’s data, the S&P Global flash PMIs for September will get the ball rolling on Monday. Although Chair Powell told reporters in his post-meeting press briefing that he doesn’t see any elevated risks of a downturn, any signs of a slowdown in the PMIs could be negative for the dollar.

On Tuesday, the consumer confidence index for September might attract some attention and investors will also be watching a batch of housing indicators that will include new home sales on Wednesday. Also important will be the latest durable goods orders and the final GDP estimate for Q2 on Thursday.

Eurozone PMIs eyed after ECB cut

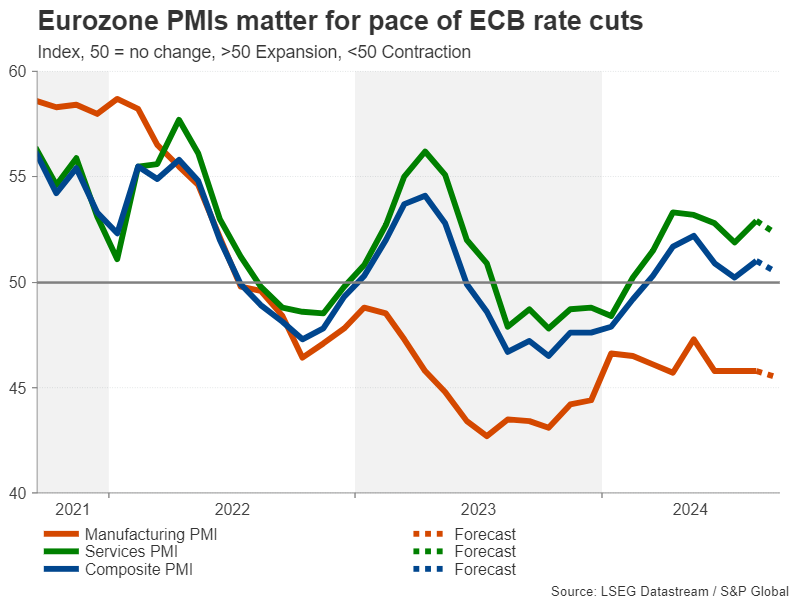

The European Central Bank lowered interest rates for a second time in September but gave little away in terms of the pace of future easing. After a mini bounce back in the spring, the Eurozone economy appears to be losing steam again. The biggest source of weakness is coming from the bloc’s largest economy – Germany – but growth in the rest of the euro area isn’t quite as anaemic.

The good news is that inflation is almost under control and so the ECB is in a position to respond accordingly to a further deterioration in the growth outlook. In August, the composite PMI edged up, thanks mainly to a rebound in services, but the manufacturing PMI remained in contractionary territory.

As long as the services sector continues to prop up the broader economy, the ECB will likely maintain a cautious stance until it can be more confident that inflation has been fully tamed. Hence, the euro might not react much to Monday’s data unless there’s a big negative surprise.

More business surveys will follow on Tuesday in the form of Germany’s ifo business climate index.

Will UK PMIs continue to outperform?

The flash PMIs will also be the main highlight in the United Kingdom. The Bank of England has taken a leaf out of the ECB’s book in not pre-committing to a particular easing path, although a 25-bps cut in November is highly likely after policymakers stood pat in September.

All three of the UK’s PMI indices climbed for a second straight month in August, underscoring the brighter economic picture during 2024. A further improvement in September would likely lessen the urgency for the BoE to switch to a faster pace of rate cuts, boosting the pound.

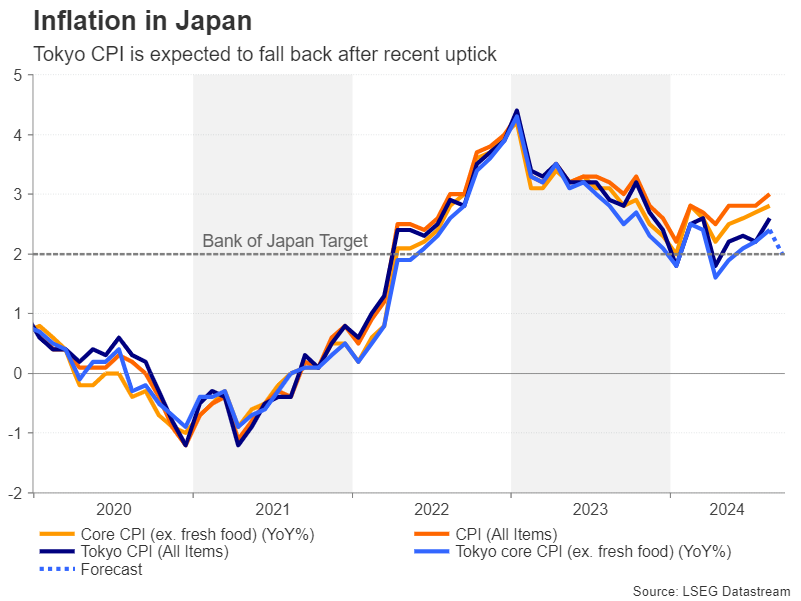

Japanese data could be vital for yen bulls

Finally in Japan, the flash PMIs are up first on the agenda on Tuesday before CPI figures for the Tokyo region come within investors’ radar on Friday.

Markets are undecided if the Bank of Japan will hike interest rates again this year, amid a patchy economic performance and signs that inflationary pressures are no longer so pronounced.

Still, if the PMIs show that the economy is maintaining the recovery that got underway in Q2 and there’s another uptick in the Tokyo CPIs, the yen might be able to resume its uptrend, which came to a halt after the dollar staged an unexpected rebound in the aftermath of the Fed meeting.

Weekly Focus – Fed Initiating the Easing Cycle with 50bp Cut

The main event this week was the monetary policy meeting in the US where markets prior to the meeting were historically divided between a 25bp and 50bp cut. The Federal Reserve chose to lower the policy rate by 50bp to a new target range of 4.75-5.00%. The larger move was motivated by a significant shift in the Fed's risk assessment. 12 out of 18 participants saw risks to unemployment rate tilted to the upside (prev. 4 participants), and the median unemployment rate forecast was revised up through 2024-2026. Despite this, Powell downplayed the probability of a recession during the press conference, as faster rate cuts are set to support growth. The updated dots signal a total of 50bp of additional cuts in 2024, 4x25bp of cuts in 2025 and 2x25bp cuts in 2026. Hence, the Fed signals a longer but more gradual rate cutting cycle compared to our call of 25bp cuts in every meeting until June, leaving a terminal rate at 3.00-3.25% by end of 2025.

This week, we also had monetary policy meetings in the UK, Japan, and Norway (see p. 4). In UK, the Bank of England left the policy rate unchanged at 5.0%. The vote-split revealed 8 members voting for an unchanged rate and one in favour of a 25bp cut. We expect the next rate cut in November and a pause in December before a pick-up in cutting pace in 2025. In Japan, the BoJ kept the policy rate unchanged as widely expected. As growth and inflation has picked up, we expect the next rate hike in December.

China released their monthly batch of data for a wide range of areas. The data painted a picture of an economy that lost even further momentum in August. The weak Chinese demand is contributing to the downward pressure on global commodity prices as well as Chinese export prices leaving China as a key disinflationary force in the world. China is also weighing on the recent weak global manufacturing growth.

In Europe, domestic inflation remains strong while growth momentum weakened. The final euro area inflation data showed that the 'LIMI' measure of domestic inflation declined to 4.2% y/y from 4.3% y/y in July.

Momentum eased but the high yearly growth rate favours a cautious easing approach of the ECB. The German ZEW survey showed the weakest assessment of the economic situation since Covid, and expectations declined to a year-low, highlighting the fragility of the German economy.

Next week focus will be on September PMIs from the US and the euro area. On both sides of the Atlantic, we expect the weakness in manufacturing to continue and services holding up activity. Services PMIs will likely decline in the euro area as the boost from the Olympic games recorded in August fades, but excluding this growth momentum was likely unchanged. On the central bank front, we follow a long list of Fed speakers including Powell on Thursday and rate decisions in China, Australia, and China. We expect the Chinese central bank to ease policy to stimulate the weak economy while the RBA is expected to leave the policy rate unchanged. In Switzerland, we expect the SNB to lower the policy rate by 25bp to 1.0%.

On Friday, we receive the US PCE inflation measure and inflation data from Spain and France ahead of the euro area print. We expect energy prices to pull euro area inflation significantly down to 1.8% y/y while core should remain unchanged at 2.8% y/y (0.20% m/m s.a.) due to sticky services inflation. In Japan, we follow the vote for a new leader and thus prime minister of the ruling party, as it could influence financial markets.

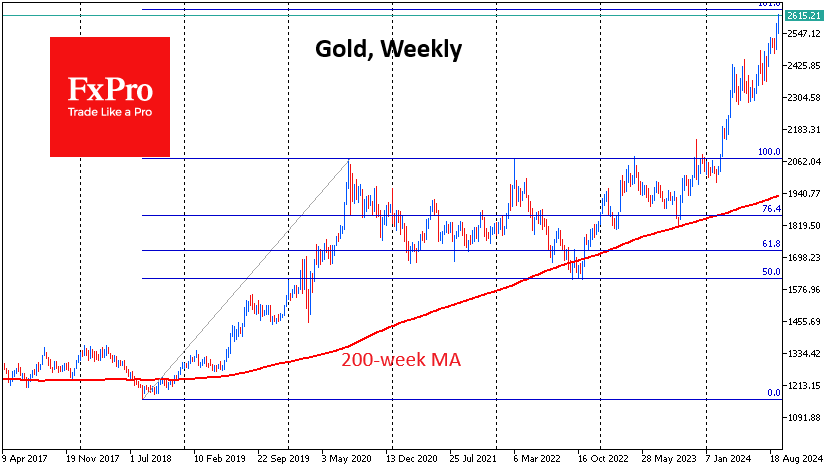

Gold Terminates the Last Sceptics

Gold started the week with new highs and ended the week with a 1.3% gain, digesting a 2% dip on profit-taking following the Fed’s rate decision. The loosening of monetary policy by more than economists had expected and forecasts of further active cuts brought back appetite for risk assets. However, the turnaround in US 10-year government bond yields has set a more cautious tone.

A fall in government bond yields increases interest in gold as an alternative to capital preservation, all other things being equal. This inverse correlation worked well last year but has started to fail this year and broke down this week when gold prices and yields started to rise simultaneously. If this is not a sign of a flight from dollar assets, it may be a sign that gold is nearing a peak.

The forced liquidation of short positions may push the gold price higher into historical highs, as the US dollar generally holds its ground against a basket of major currencies, and rising bond yields create an unfavourable environment for gold.

From a technical point of view, the area of attraction for the price seems to be $2640, which is the 161.8% level from the initial upward momentum in August 2018 to the peak in August 2020. This was followed by two years of trading in a wide range, with the deepest decline in September-October 2022, which set the stage for a new advance.

If gold continues to follow its two-year cycles, the upside momentum could soon be replaced by a sideways or sharp reversal like we saw in 2011.

Major turning points in gold over the past six years have come at the touch of the 200-week simple moving average. It is now almost 40% or over $1100 behind the price. In absolute terms, this is the largest gap since 2011 and in relative terms since 2020. This difference makes the potential for a correction that could take the price to $2000 within a year or two enormous.

The accumulated overbought conditions in gold does not imply an immediate reversal. On the contrary, the most violent part of the rally, with a massive short squeeze, may still be ahead. However, traders should also be on the lookout for signs of growth exhaustion, which could follow a very sharp correction.

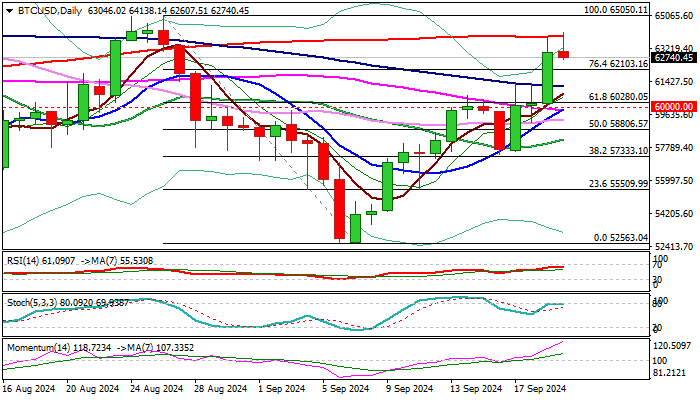

BTCUSD – Bulls Likely to Take a Breather Following Repeated Failure at 200DMA Barrier

BTCUSD edged higher on Friday and hit new three week high, in attempts to extend 4.6% advance on Thursday.

Bitcoin received strong boost from Fed rate cut and underpinned by dovish shift in global rate view.

Technical picture is bullish on daily chart (multiple MA bull-crosses / 14-d momentum is in steep ascend), but bulls face headwinds from overbought conditions, which was presented through repeated failure to break pivotal 200DMA barrier at 63869.

The second consecutive daily close below 200DMA to confirm signal that bulls may take a breather for consolidation before resuming.

Dips are likely to be shallow, as overall picture is bullish and positive sentiment is strong.

Support at 61157 (100DMA) should ideally contain dips and guard lower pivots at 60000 zone (psychological / 10/55 DMA bull-cross) loss of which would sideline bulls.

Res: 63869; 64138; 64500; 65050

Sup: 62607; 62103; 61928; 61156

Sunset Market Commentary

Markets

Main potential market movers already hit the screens this morning before the start of European dealings with the BOJ policy decision and the UK consumer data. The BOJ as expected left its policy rate unchanged at 0.25%, but communication on the timing of future rate hikes was more balanced than expected.

The BOJ upgraded its assessment on private consumption (on a moderate increasing trend versus being reliant previously) as the virtuous cycle from income to spending gradually intensifies. With respect to consumer prices the BOJ still sees (underlying) inflation at a level that is generally consistent with the price stability target in the second half of the policy horizon, even as the impact from past rise in import prices is waning. The statement didn’t reveal any intentions on (the timing of) further hikes. In the news conference, governor Ueda indicated that the BOJ is still prepared to raise rates further, but there’s no rush. Uncertainty on the economic outlook overseas and instability on financial markets are a reason to take time to assess developments. The rise of the yen also eased the upside risk to prices. The BOJ apparently doesn’t want to further accelerate the sharp rise of the yen since late July. More aggressive Fed rate cuts in this respect are also important input for the path of BOJ normalization. An October rate hike now looks unlikely. The yen early this week touched peak levels below USD/JPY 140 for the first time since end-July last year, but today rebounded further to the 144 area.

UK consumer data were mixed. GFK consumer confidence unexpectedly tumbled from -13 to -20 as consumers turn more negative on their personal situation and on the global economy. On the other hand, August retail sales showed solid growth for the second consecutive month (Aug +1.0%, July upwardly revised from 0.5% to 0.7%). The UK data only had limited impact on UK interest rate markets. Gilts are trending in line with Bunds (UK yields +/- 1 bp higher across the curve). EUR/GBP tested the key support at 0.8383, but no sustained break occurred.

Trading on core US and European markets took a pause as positions have been adapted to the 50 bps Fed rate cut, and new guidance. US yields are rising modestly (2-y + 4.5 bps, 30-y +2.5 bps). Markets need more data to become more convinced on potential additional 50 bps steps later this year. In the meantime, key support levels are ‘blocking’ further downside in yields. German yields are rising about 1 bp. After yesterday’s reflationary jump, especially European equites are falling prey to profit taking (Eurostoxx 50 -1.2%, S&P 500 -0.2%). Despite a less buoyant risk sentiment, the dollar is holding near recent lows (DXY 100.75, EUR/USD 1.116), with USD/JPY the exception (cf supra).

News & Views

Belgian consumer confidence took a dive in September from -3 to -7, matching the previous one-year low from May and settling at just below its long-term average. The National Bank of Belgium noted that the loss of confidence affected all components of the indicator. Economic expectations for the next twelve months are down sharply. Concerns about a resurgence in unemployment shot up to its highest level in almost two years. Expectations on the current general economic situation also deteriorated after a rebound last month. The NBB said that the gloom that’s affecting the Belgian industry, particularly the automotive sector, is sapping consumer morale. Households are planning to save less in the months to come and have become slightly less optimistic about their financial situation for the next twelve months.

French prime minister Michel Barnier sat down with president Macron late yesterday to discuss a proposal for a new government. Barnier labelled the talks as constructive and said that after some final changes he’ll announce the team by Sunday. Getting the vote of confidence by parliament is the tricky part though. Not a single group has a majority, so each of them can sink the proposal. Bloomberg citing French media reported that most of the team is made up of figures from Macron’s centrist group and Barnier’s conservative Republicans party. Should the cabinet get the seal of approval, it immediately faces a daunting task: presenting the budget bill to rein in worsening deficits.

Graphs

USD/JPY: yen eases further off recent highs as BOJ turns more balanced on pace of policy normalization.

EUR/GBP testing YTD low on solid UK retail sales. No sustained break yet.

Dow Jones pausing near all-time top as markets are pondering the impact of the Fed turning to support growth.

Gold ($ p/oz): easier global financial conditions propel gold to new record, irrespective of risk sentiment.