Sample Category Title

UK retail sales grows 1% mom in Aug, annual growth highest since Feb 2022

UK retail sales volumes surged 1.0% mom in August, significantly outpacing the expected 0.3% mom growth. This marked the highest sales index level since July 2022. Over the broader three-month period ending in August, sales volumes increased by 1.2% compared to the previous three months.

On an annual basis, sales volumes jumped 2.5% yoy, marking the largest annual rise since February 2022. However, despite these strong gains, retail sales volumes remain -0.4% below their pre-pandemic levels from February 2020.

Hawkish Market Surprises from Norges Bank and Bank of England

In focus today

In the euro area September consumer confidence is due for release. Consumer confidence has been on an upward trend but remains below the historical average and consumer spending is weak. As real incomes are rising and the labour market remains strong, we expect confidence to keep improving, which should support consumption especially next year.

Economic and market news

What happened overnight

In Japan, the Bank of Japan (BoJ) kept its uncollateralized overnight call rate unchanged at 0.25% this morning. In its assessment of the economy, it sounds more upbeat on particularly private spending, which is key for the potential for further rate hikes. BoJ on hold was widely expected and the market reaction is muted.

We got fresh inflation data overnight as well, which showed price pressures picking up and core inflation increasing from 1.6 to 1.7% in August. Broadly, the BoJ will be satisfied with recent developments in the economy and financial markets. Particularly the recent tailwind to JPY makes hiking rates much less acute. With a leadership election within the ruling party (LDP) around the corner, potentially followed by a snap general election, we expect the BoJ will be most comfortable keeping policies unchanged in October as well. The window is open for another rate hike in December, which is our expectation, but much will depend on US data and the Fed cutting cycle. If US labour market cooling intensifies, a JPY rally could pull the breaks on further BoJ hikes.

What happened yesterday

In Norway, Norges Bank left policy rates unchanged including the sight deposit rate at 4.50%. While this was widely expected there were diverging views as to the forward guidance signals on the monetary policy outlook. In short, Norges Bank delivered a hawkish surprise compared with market expectations by pushing back against a rate cut this year. We leave unchanged our forecast for the sight deposit rate and still pencil in the first rate cut in March, and a total of four rate cuts in both 2025 and 2026.

In the UK, the Bank of England (BoE) left the Bank Rate unchanged at 5.00% as widely expected. The bank delivered a hawkish twist to its guidance emphasising their gradual approach to reducing the restrictiveness of monetary policy. We expect the BoE to deliver the next 25bp cut in November and this to be the final cut this year, making it less than markets expect (42bp by YE 2024). 2Y Gilt yields moved higher on the statement but overall, the reaction in rates markets was muted. EUR/GBP moved lower on the announcement following the slightly hawkish vote split and notion of a gradual cutting cycle. See Bank of England Review - Gradual easing cycle supports GBP, 19 September.

In the euro area, ECB comments were split with both dovish and hawkish tones. Schnabel repeated the view of sticky services inflation, while Centeno said that 'we have really to minimize the risk of undershooting, because that's the main risk'. Panetta said that ECB may accelerate rate cuts in the coming months.

In Turkey, the Central Bank of Turkey left the policy rate unchanged as expected and dropped a reference to potential further policy tightening. However, we think the policy rate will be kept at the current level at least for the remainder of this year, and the cutting cycle to kick off only in Q1 next year.

Equities: Global equities were higher yesterday, buoyed by the optimism resulting from the Federal Reserve's 50 basis point cut on Wednesday. Despite the overall market surge, it was a very cyclical-led market, with utilities and consumer staples even closing lower despite the increased risk appetite. Additionally, minimum volatility stocks underperformed while small caps fared well. Much of the equity market's outlook hinges on the US labour market, making the 219K initial jobless claims print a timely boost for risk appetite. In the US yesterday, the indices closed as follows: Dow +1.3%, S&P 500 +1.7%, Nasdaq +2.5%, Russell 2000 +2.1%. This morning, Asian markets are mostly higher, with Japan leading the gains despite a stronger yen following the Bank of Japan's decision to leave policy unchanged. European and US futures are lower this morning.

FI: Following Wednesday's FOMC meeting decision, European yields pivoted around the 10y point yesterday. The 10y point was virtually unchanged across European jurisdictions with the long end sell-off of about 4bp and the short end rallying about the same, thus leading to a noteworthy steepening across the curves. The 2s10s German bond yield curve is just 2bp inverted now. ECB is priced at 38bp of rate cuts and 117bp currently, which is 2bp more than Wednesday's close.

FX: The USD broadly weakened against G10 in yesterday's session, pushing EUR/USD above 1.1150. USD/JPY declined slightly this morning following the BoJ's expected hold, accompanied by a hawkish statement. A hawkish hold from Norges Bank combined with generally positive risk sentiment led the NOK to outperform among G10 currencies yesterday, with EUR/NOK just above 11.70. The Fed's 50bp cut has fuelled some repricing of expectations for the Riksbank next week. EUR/GBP broke below the 0.84 mark during yesterday's session following a hawkish twist delivered by the Bank of England. Oil prices have recovered to near USD 75/bbl this week.

Cliff Notes: 50 Proves the Magic Number

Key insights from the week that was.

The main update for Australia this week was August’s Labour Force Survey. The result again emphasised the strength of labour demand, with employment growing by 47,000, ahead of the 37,000 estimated increase in the labour force. The unemployment rate was unchanged in the month at 4.2%, but only just; at 2 decimal points it declined from 4.24% to 4.16%. The continued meeting of demand with supply points to a broadly balanced labour market and resilient economy, justifying an expectation that economic growth will accelerate in 2025 as inflation abates and the RBA is able to ease policy.

Experiences across the economy are varied, however, as evinced by the latest ACCI-Westpac Survey of Industrial Trends. Australian manufacturers – whom have largely been at the coalface of the discretionary spending slowdown – previously reported difficulties in sourcing skilled labour and now declines in employment, utilising remaining staff at a higher rate when necessary. That stands in contrast to industries providing essential services – such as healthcare and social assistance – which continue to experience persistent growth and thus an ongoing need to increase headcount. Detailed industry-level labour market data, available next week, will provide a better understanding that these underlying imbalances and the risks they pose.

For domestic manufacturing, there were some constructive developments in the latest survey. Businesses have been able to find some pockets of demand over the last six months, seeing new orders increase and output growth remain positive. With demand conditions likely to improve over the year ahead as headwinds abate, manufacturers are eager to invest in buildings, plant and equipment, with a greater degree of confidence than seen prior. The desire to expand capacity and improve the flexibility of their supply chains is understandable given volatile cost pressures and persistent difficulties in obtaining materials and labour.

Next week, we will receive a key partial update on inflation with the August Monthly CPI Indicator. Our preview is now available.

Offshore, markets were focused on the FOMC as it kicked off its long-awaited easing cycle. The BoE in contrast marked time ahead of revised forecasts in November.

At the conclusion of its September meeting, the FOMC decided to cut rates by 50bps to start this easing cycle, bringing the fed funds rate target range to 4.75-5.00%. Chair Powell’s remarks emphasised that the outsized move was a response to balancing risks and so as to not “get behind” with policy. The FOMC’s revised forecasts also made clear members remain constructive on the outlook, the labour market characterised as 'solid' and expected to remain that way, with the unemployment rate to peak only 0.2ppts above the current level at 4.4%. Annual GDP growth is also forecast to be 2.0% in 2024 through 2027, slightly above the Committee’s ‘longer run’ estimate of trend growth of 1.8%. As a result, the FOMC projects a slow normalisation after a rapid start, with another 50bps of cuts seen by end-2024 (noting two meetings remain in 2024), then a further 150bps through 2025 and 2026 to 2.9%, the FOMC’s current estimate of neutral.

We expect US growth to modestly disappoint the FOMC’s forecasts, but also see lingering risks for inflation. We therefore see the fed funds rate reaching a low of 3.375% for this cycle in late-2025, with that rate then held through 2026. Chief Economist Luci Ellis’ essay this week focuses not only on the next steps for central banks but also the determinants of neutral and the global rate structure into the medium term.

Across the Atlantic, as widely expected, the Bank of England kept rates steady in an 8-1 vote in September. Messaging from the Monetary Policy Summary was hawkish, emphasising a need to 'squeeze persistent inflationary pressure' and risks to the inflation outlook. The Monetary Policy Committee considered three cases; the first saw policy eased quickly as weaker headline inflation fed through to pay and price-setting, while the second saw economic slack discouraging price growth, and the third considered a structural change in the price-setting mechanism, necessitating tighter policy for longer. Central to all three was the uncertainty surrounding price and wage determination. Policy easing is therefore expected to be ‘gradual’ through the rest of 2024 and in 2025 and, all the while, to remain data dependent. On that front, earlier in the week, the August CPI rose 0.3% and 2.2% from a year ago. The annual figure is below the BoE's forecast of 2.4%. Annual services inflation remains stubborn and elevated however, at 5.6%.

Coming back close to home, New Zealand’s economy contracted 0.2%qtr in Q2, less than both our and the RBNZ's expectations. Activity was mixed across industries with over half recording declines. Support came from non-food manufacturing, up 4.0% in the quarter but this was more than offset by weakness in consumer-oriented industries like retail and hospitality. In spite of this, household spending rose 0.4%qtr, largely due to spending on essential items such as groceries. Exports were a drag, falling 4.4%qtr after a strong rise in Q1.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1096; (P) 1.1137; (R1) 1.1204; More....

Intraday bias in EUR/USD remains mildly on the upside with focus on 1.1200 resistance. Decisive break there will resume larger the rally from 1.0665 to 1.1274 high. Firm break there will resume larger up trend. On the downside, however, break of 1.1072 will turn bias back to the downside for 1.1001 support instead.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

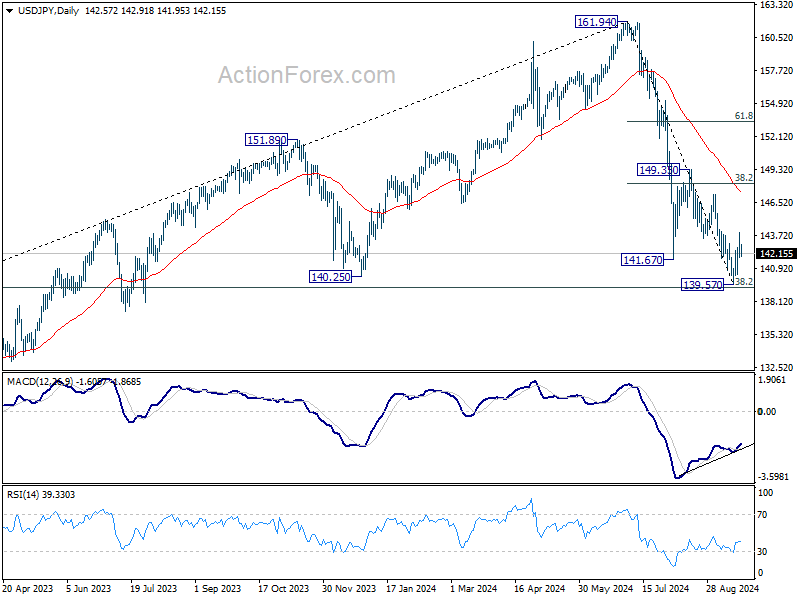

USD/JPY Daily Outlook

Daily Pivots: (S1) 141.70; (P) 142.82; (R1) 143.76; More...

Intraday bias in USD/JPY stays mildly on the upside for the moment. Rebound from 139.57 short term bottom should target 55 D EMA (now at 147.37), and possibly further to 38.2% retracement of 161.94 to 139.57 at 148.11. For now, risk will stay on the upside as long as 139.57 support holds, in case of retreat.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

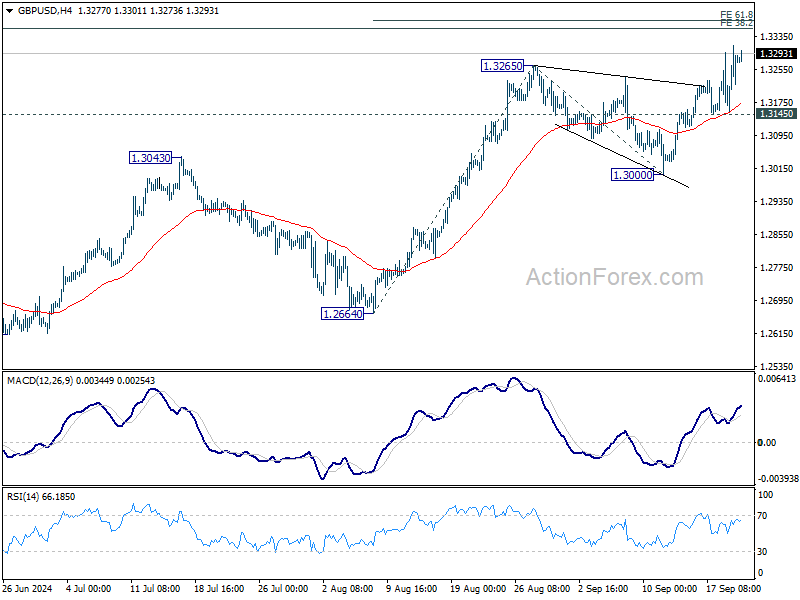

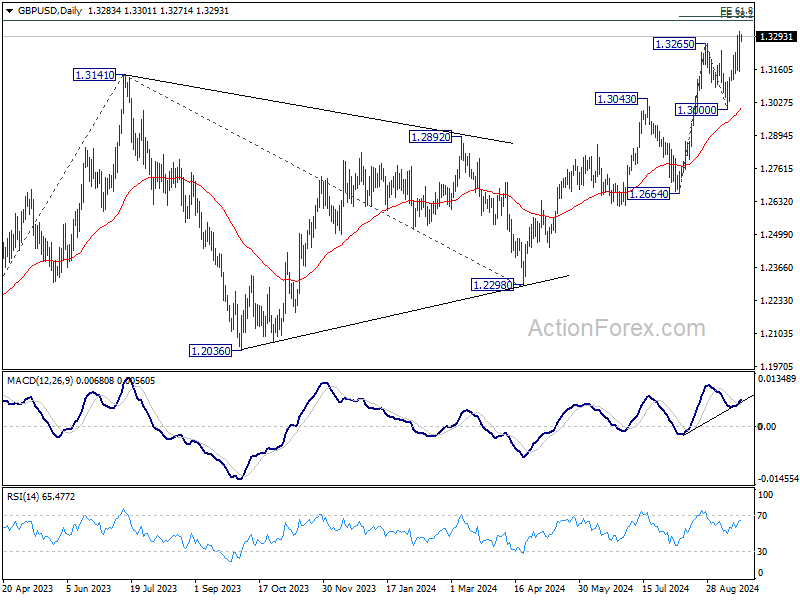

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3188; (P) 1.3251; (R1) 1.3349; More...

GBP/USD's rally is still in progress and intraday bias stays on the upside for 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371 in the near term. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, however, break of 1.3145 support will turn bias to the downside for deeper pullback to 1.3000 support next.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Sustained break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

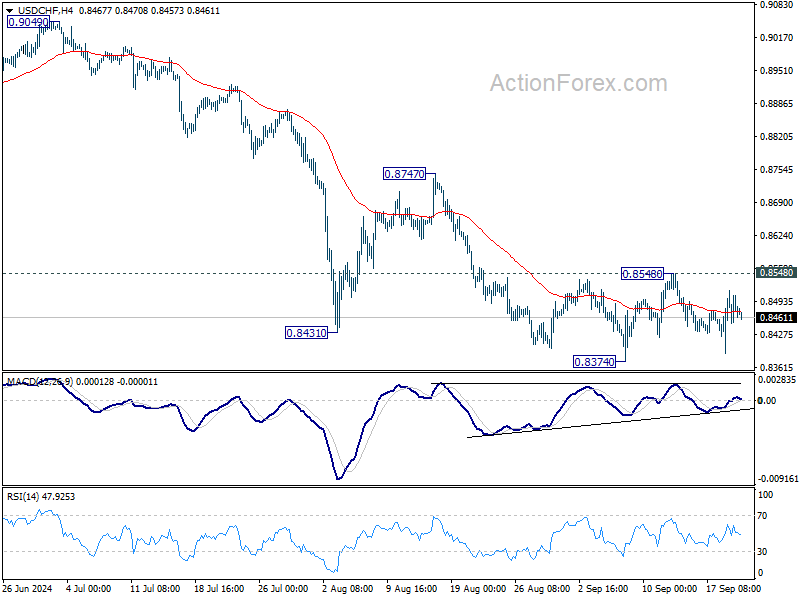

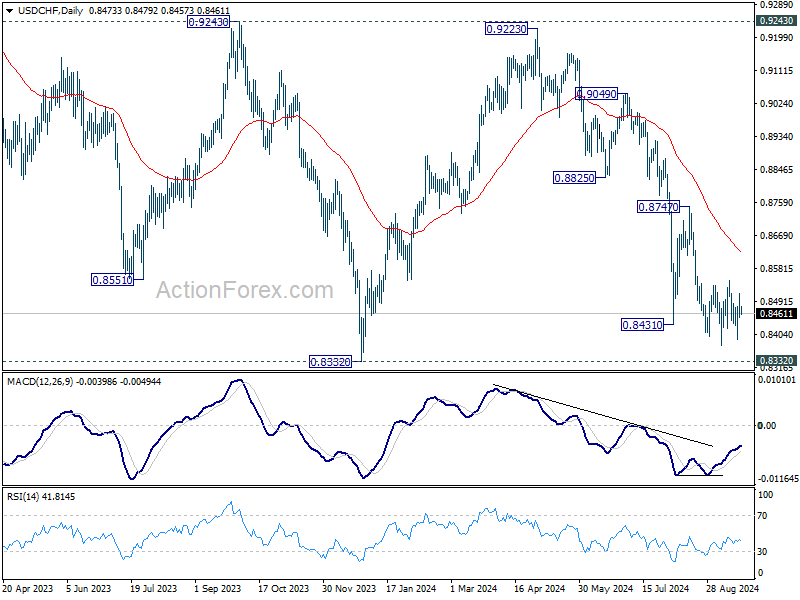

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8446; (P) 0.8480; (R1) 0.8512; More…

Intraday bias in USD/CHF stays neutral as range trading continues. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8548 resistance will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

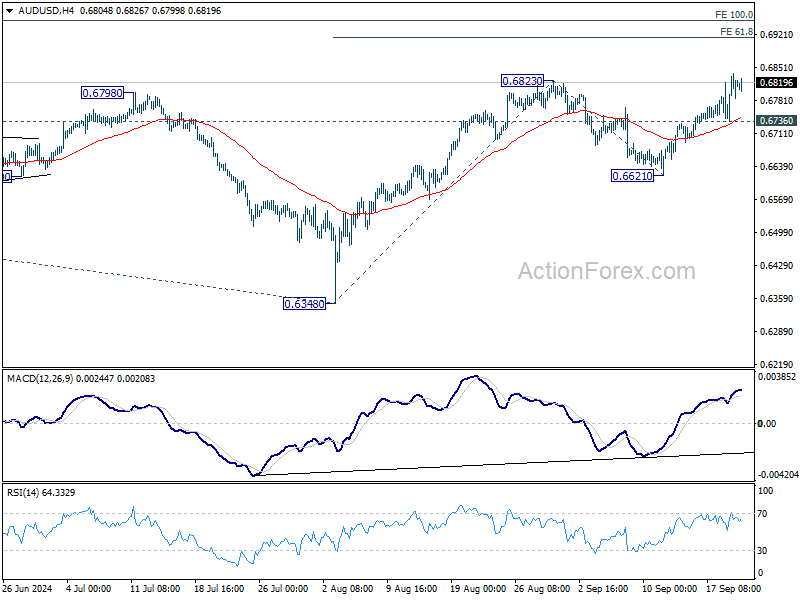

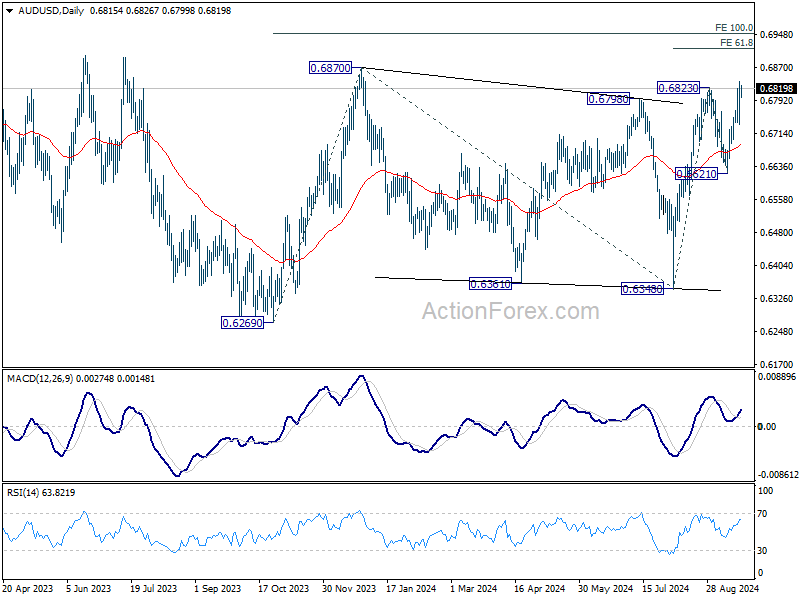

AUD/USD Daily Report

Daily Pivots: (S1) 0.6756; (P) 0.6798; (R1) 0.6856; More...

AUD/USD's break of 0.6823 confirms resumption of rally from 0.6348. Intraday bias stays on the upside for 61.8% projection of 0.6348 to 0.6823 from 0.6621 at 0.6915 next. On the downside, below 0.6376 minor support will turn intraday bias neutral first. But outlook will remain cautiously bullish as long as 0.6621 support holds, in case of retreat.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

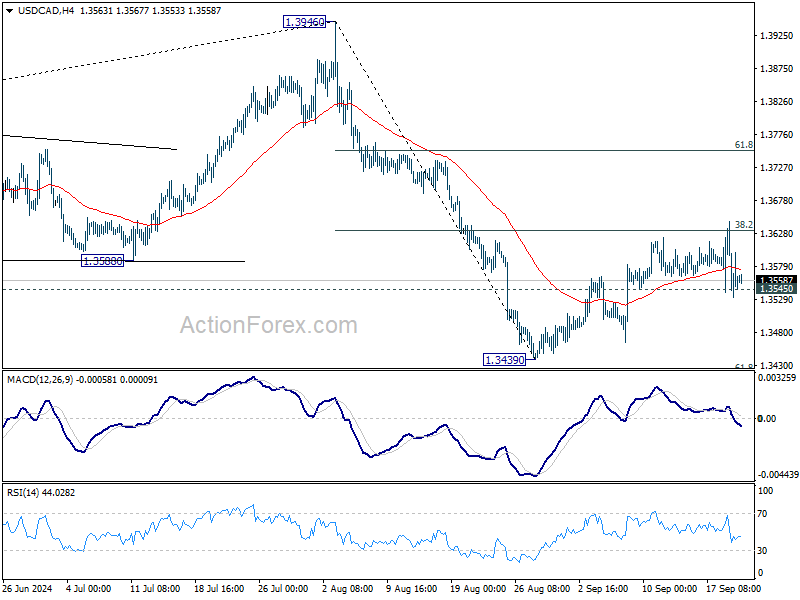

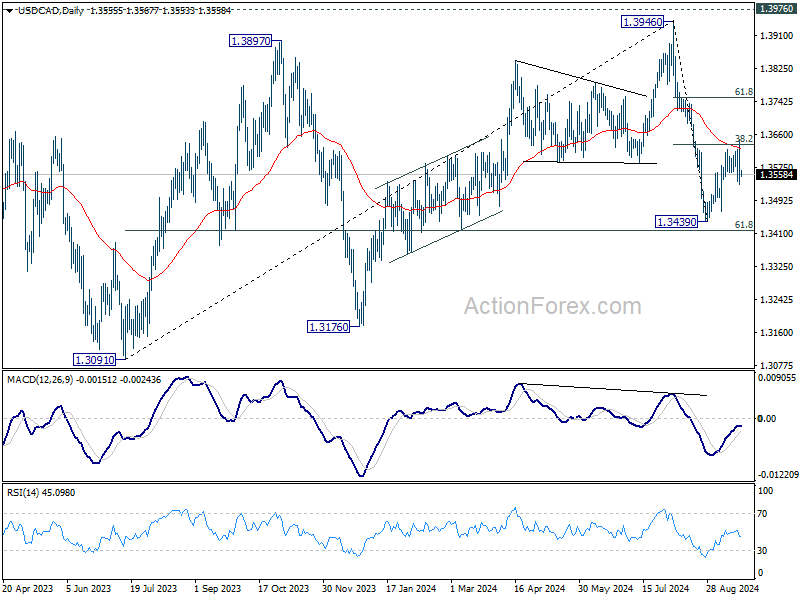

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3511; (P) 1.3580; (R1) 1.3626; More...

Intraday bias in USD/CAD remains neutral at this point. On the downside, firm break of 1.3545 minor support will suggest that recovery from 1.3439 has completed, and turn bias to the downside for retesting this low. Nevertheless, sustained break of 38.2% retracement of 1.3946 to 1.3439 at 1.3633 would argue that the decline from 1.3946 has completed. Stronger rally would then be seen to 61.8% retracement at 1.3752 and above.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

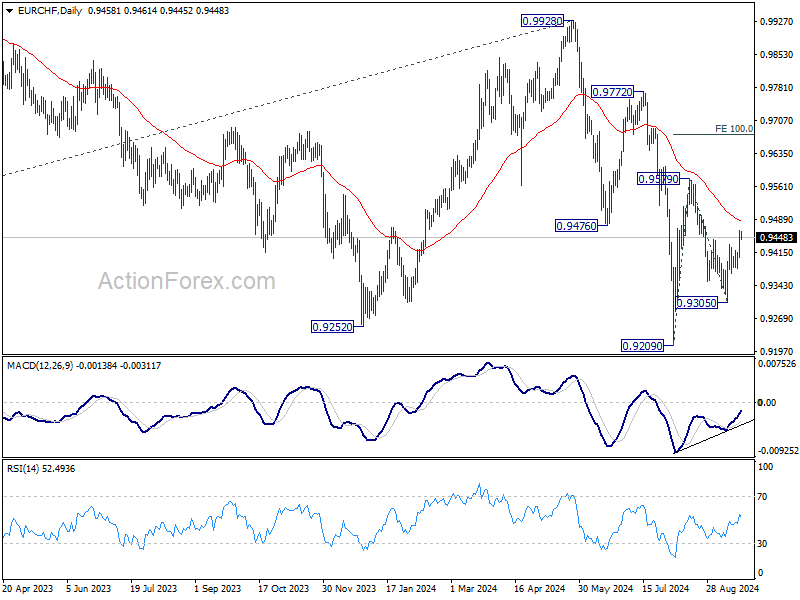

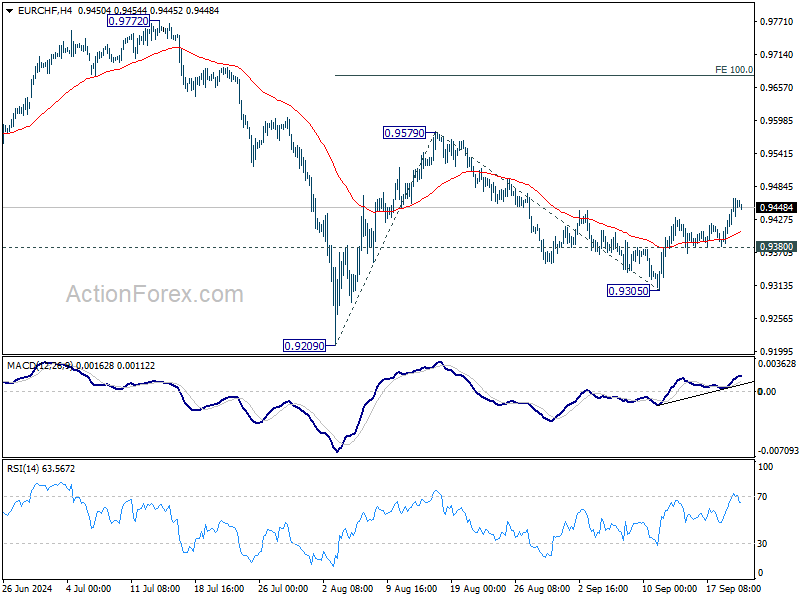

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9409; (P) 0.9438; (R1) 0.9490; More....

Intraday bias in EUR/CHF remains on the upside for the moment. Rise from 0.9305 is seen as the third leg of the pattern from 0.9209. Further rally would be seen to 0.9579 resistance next. On the downside, below 0.9380 minor support will turn bias back to the downside for 0.9305 support instead.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.