Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1096; (P) 1.1137; (R1) 1.1204; More....

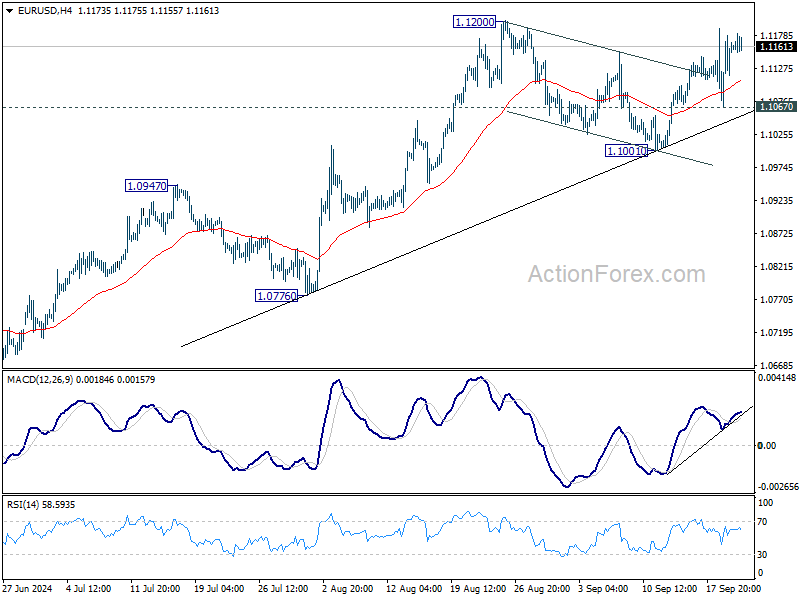

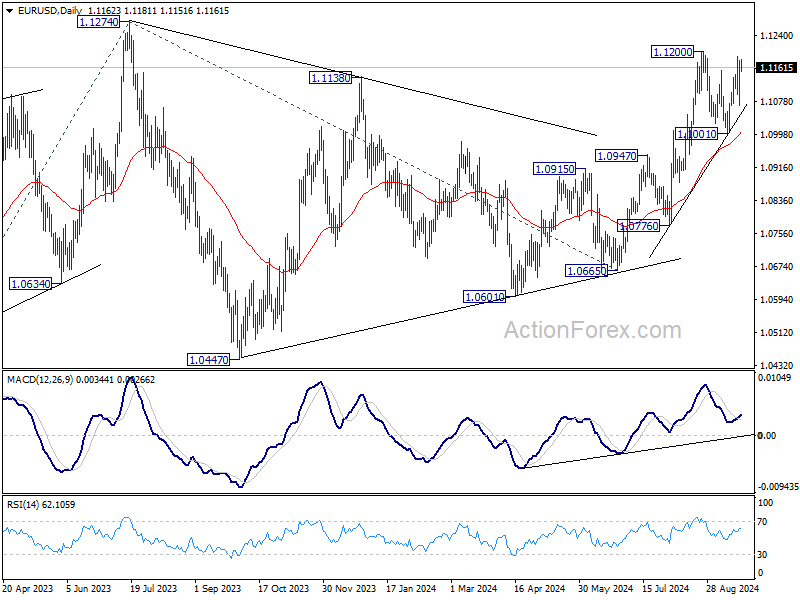

No change in EUR/USD's outlook and intraday bias stays on the upside. Decisive break of 1.1200will resume larger the rally from 1.0665 to 1.1274 high. Firm break there will resume larger up trend. On the downside, however, break of 1.1072 will turn bias back to the downside for 1.1001 support instead.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

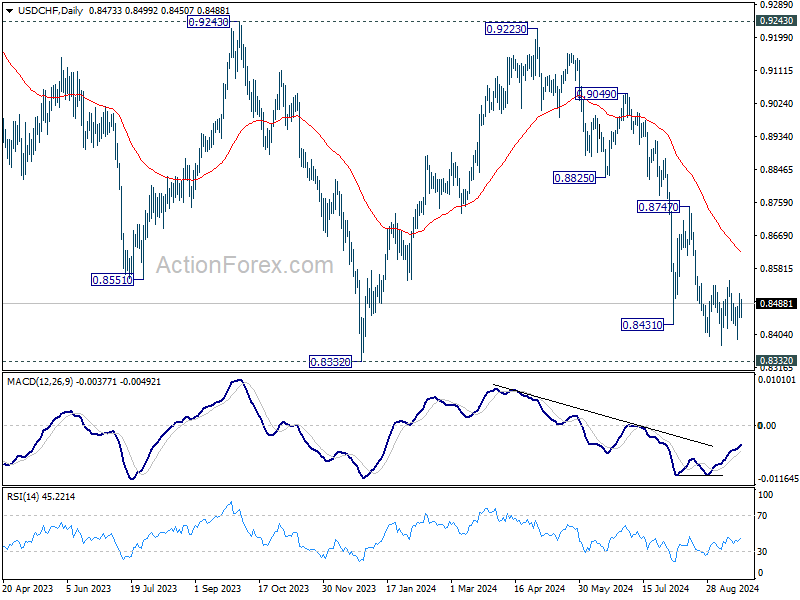

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8446; (P) 0.8480; (R1) 0.8512; More…

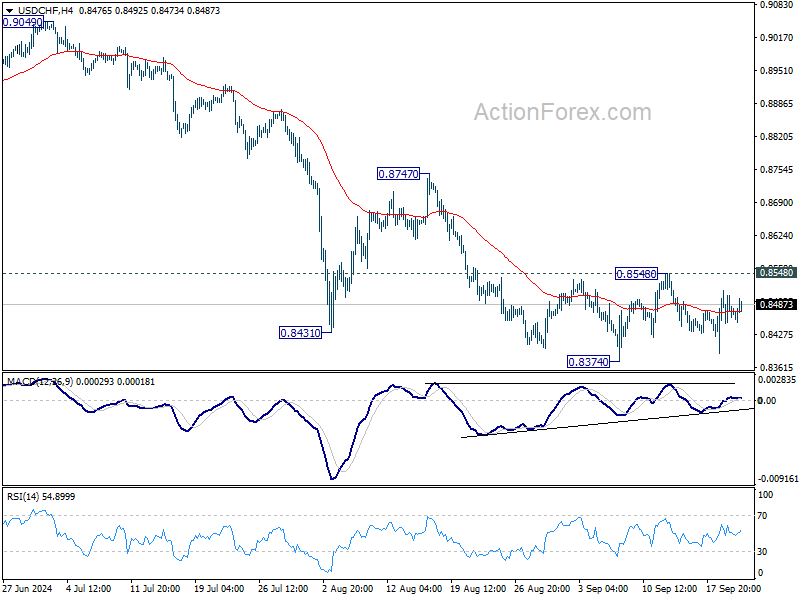

No change in USD/CHF's outlook as range trading continues. Intraday bias remains neutral at this point. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8548 resistance will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

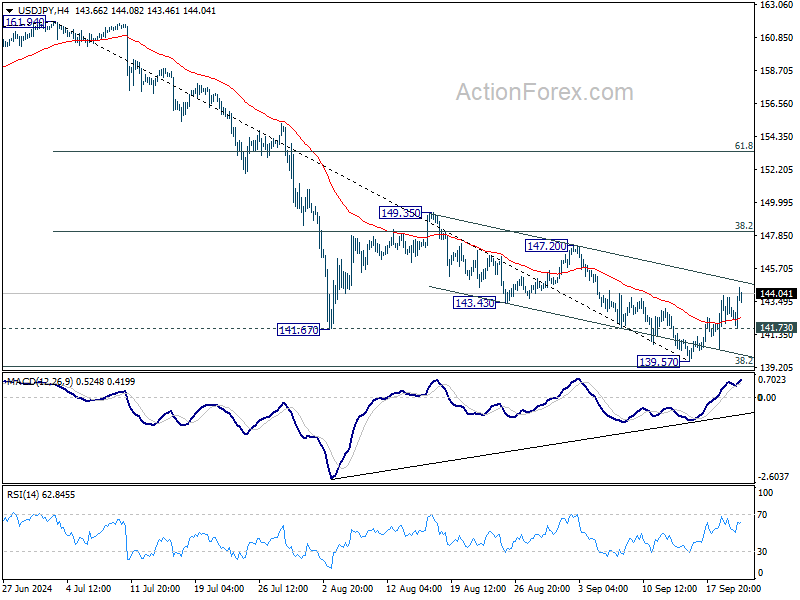

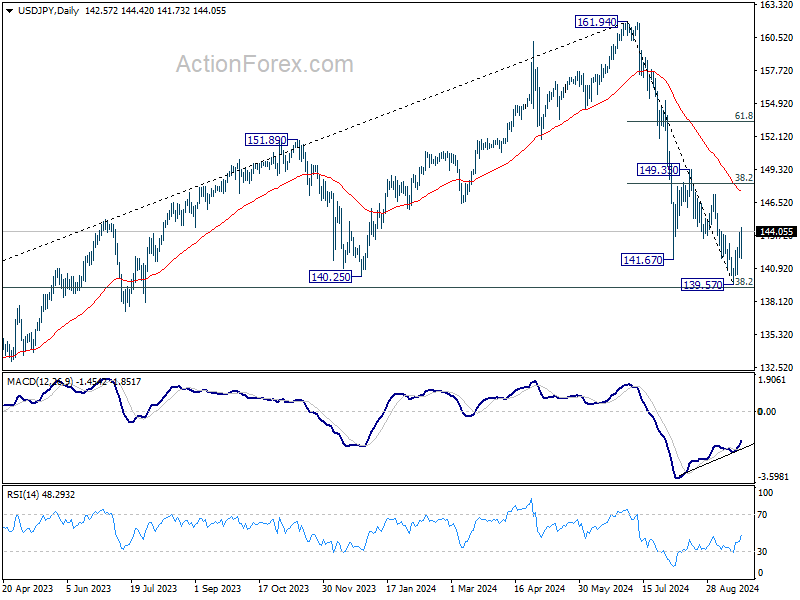

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.70; (P) 142.82; (R1) 143.76; More...

Intraday bias in USD/JPY remains on the upside at this point. Rebound from 139.57 short term bottom should target 55 D EMA (now at 147.37), and possibly further to 38.2% retracement of 161.94 to 139.57 at 148.11. On the downside, below 141.73 minor support will turn bias to the downside for retesting 139.57 instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Canada: Retail Sales Recover from Two-Month Slump.

Retail sales rose by 0.9% month-on-month (m/m) in July, reversing the two-month downward trend. This was higher than the Statistics Canada's advanced estimate of a 0.6% gain.

Adjusting for the impact of inflation, the volume of retail sales was up 1.0% m/m in July.

Sales at motor vehicle and parts dealers rose by 2.2% m/m, following June's 2.1% contraction attributed to operational difficulties due to a series of cyberattacks.

Receipts at gas stations and fuel vendors fell 0.5% m/m in nominal terms, despite higher prices at the pump (2.4% m/m growth in July).

Excluding auto sales and receipts at gas stations, core retail sales were up by 0.6% m/m in July.

- The gain in core sales was led by food and beverage stores and general merchandise stores, which both gains 0.8% on the month.

- Building material and garden equipment and supplies dealers (-1.4% m/m) was the largest loser of today's report.

E-commerce sales rose by 3.4% m/m following an upwardly revised reading in June ( +0.2% m/m from -2.4% m/m reported in the advance estimate).

Statistics Canada's advanced estimate for August points to another month of growth of 0.5% m/m.

Key Implications

Today's rebound in retail sales was led by stronger auto sales, which recovered from an operational setback in June. This was enough to bring three-month average auto sales growth into positive territory for the first time since January. The rest of the categories also told an encouraging story as growth in core sales accelerated on the month, likely driven by strong population. We expect the rebound in durable goods will support growth in goods spending for Q3 resulting in total personal consumption expenditures gain of 1.0% quarter-on-quarter (annualized).

A good start to the quarter is unlikely to sway the odds decisively on whether the Bank of Canada will cut rates by 50 basis points in October. Despite the good news today and another month of projected growth, the downward trend in retail spending per capita is clear. In addition to employment and inflation figures, the Bank’s communication will be critical to watch for any signs of change in the pace of easing.

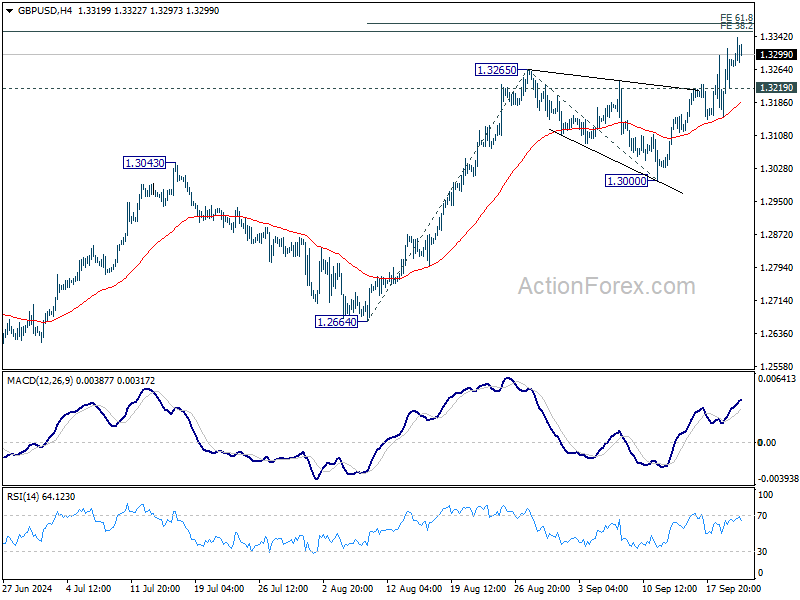

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3188; (P) 1.3251; (R1) 1.3349; More...

Intraday bias in GBP/USD remains on the upside for 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, below 1.3219 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3000 support holds.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Sustained break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Sterling Rallies on Strong Retail Sales as Yen Struggles

Sterling climbed broadly today, fueled by unexpectedly strong UK retail sales data that more than compensated for the lackluster consumer confidence report. Despite ongoing high interest rates and persistent inflation, British consumers appear to be resilient, continuing to spend. This bolsters the position of hawkish members within the BoE's MPC, who may push harder for a measured, gradual approach to reducing interest rates.

Looking at the broader market, Australian Dollar has maintained its position as the top performer for the week, driven by post-FOMC risk-on sentiment. However, with risk appetite fading as the weekend approaches, Sterling, currently in second place, has a real chance of overtaking the Aussie. Meanwhile, New Zealand Dollar follows closely as the third strongest currency this week.

On the downside, Japanese Yen remains the weakest performer, extending its selloff after BoJ's decision to hold rates steady earlier today. The rise in US and European bond yields has further weighed on the Yen, as the growing yield differential makes it less attractive. Dollar and Swiss Franc are also under pressure, lacking the safe-haven appeal in the current risk-on environment. Euro and Canadian Dollar remain relatively mixed in the middle.

In Europe, at the time of writing, FTSE is down -0.85%. DAX is down -0.74%. CAC is down -0.77%. UK 10-year yield is up 0.0041 at 3.897. Germany 10-year yield is up 0.005 at 2.207. Earlier in Asia, Nikkei rose 1.53%. Hong Kong HSI rose 1.36%. China Shanghai SSE rose 0.03%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield rose 0.0106 to 0.864.

Canada's retail sales rises 0.9% mom, 7 of 9 subsectors grow

Canada's retail sales rose 0.9% mom to CAD 66.4B in July, well above expectation of 0.5% mom. Sales were up in seven of nine subsectors, led by increases at motor vehicle and parts dealers. In volume terms, sales were also up 1.0% mom.

Advance estimate suggests that sales increased 0.5% mom in August.

ECB's de Guindos keeps all option open data will drive future rate cuts

In an interview with Expresso, ECB Vice President Luis de Guindos reaffirmed the central bank's cautious approach regarding rate cuts in the upcoming meetings. He stressed that ECB remains "fully committed" to a data-dependent strategy, making decisions on a "meeting-by-meeting" basis.

While he acknowledged the possibility of cuts in both October and December, De Guindos highlighted that December would provide a clearer picture. "We will have more information and a new round of projections," he noted.

Nevertheless, he emphasized ECB plans to keep "all options open" to retain flexibility, with future moves hinging entirely on evolving economic data.

BoE's Mann favors extended tight policy before swift, aggressive cuts

In a speech today, BoE MPC member Catherine Mann emphasized the importance of a cautious approach to easing monetary policy, stating that it's preferable to remain restrictive longer amid inflation uncertainties.

She argued that "a risk management assessment implies it is better, under inflation uncertainty, to remain restrictive for longer, until right tail risks to the inflation process dissipate, and then to cut more aggressively."

This "more activist strategy", according to her, would allow for a sustainable inflation outcome with less impact on the economy, as she mentioned it helps achieve the target "at a lower sacrifice ratio."

Despite agreeing with the majority of the MPC members on holding rates steady in the latest meeting, Mann has expressed a "guarded view" on starting the cutting cycle. Having voted against the 25bps rate cut in August, Mann again voted to hold yesterday.

UK retail sales grows 1% mom in Aug, annual growth highest since Feb 2022

UK retail sales volumes surged 1.0% mom in August, significantly outpacing the expected 0.3% mom growth. This marked the highest sales index level since July 2022. Over the broader three-month period ending in August, sales volumes increased by 1.2% compared to the previous three months.

On an annual basis, sales volumes jumped 2.5% yoy, marking the largest annual rise since February 2022. However, despite these strong gains, retail sales volumes remain -0.4% below their pre-pandemic levels from February 2020.

UK Gfk consumer confidence plummets to -20 ahead of expected painful budget

UK GfK Consumer Confidence dropped sharply in September, falling from -13 to -20, marking the biggest decline since April 2022. The seven-point drop reflects growing concerns about the economic outlook and personal finances, with households bracing for a difficult budget next month.

Key forward-looking indicators worsened significantly. Expectations for the general economy over the next 12 months dropped by -12 points to -27, while personal finance expectations fell by -9 points to -3. The major purchase index, which gauges consumers' willingness to buy big-ticket items, also dropped -10 points to -23.

GfK noted, "Despite stable inflation and the prospect of further rate cuts, this is not encouraging news for the UK's new government." Neil Bellamy, Consumer Insights Director at GfK, linked the drop to concerns over Prime Minister Keir Starmer's warnings of a "painful" budget. Bellamy said, "Consumers are nervously awaiting the Budget decisions on Oct. 30 after the withdrawal of winter fuel payments and warnings of further difficult measures."

BoJ stands pat at 0.25%, sees gradual inflation rise and economic growth

BoJ left its uncollateralized overnight call rate unchanged at around 0.25% during today's meeting, as widely anticipated and decided by unanimously.

In the accompanying statement, BoJ maintained a positive outlook for the Japanese economy, projecting continued growth at a rate above its potential. The central bank expects "overseas economies will continue to grow moderately," further supporting Japan's economic expansion. Domestically, the "virtuous cycle from income to spending" will gradually intensify, aided by accommodating financial conditions.

On the inflation front, core CPI is forecast to rise through fiscal 2025. BoJ also noted that underlying inflation will "increase gradually" as output gap narrows and medium- to long-term inflation expectations firm up.

However, the central bank also outlined several risks to its outlook, including global economic developments, commodity prices, and the pace at which firms adjust wage and price setting.

Japan's CPI core rises to 2.8% in Aug, core-core up to 2.0%

Japan's core CPI, excluding fresh food, rose to 2.8% yoy in August, matching expectations and marking the fourth consecutive month of acceleration. This increase is up from 2.7% yoy in July and continues the upward trend from 2.2% yoy in April, keeping inflation above BoJ's 2% target since April 2022.

Core-core CPI, which strips out both fresh food and energy, also rose from 1.9% yoy to 2.0% yoy, highlighting broader inflationary pressures in Japan. Headline CPI, which includes all categories, increased from 2.8% yoy to 3.0% yoy.

Energy prices surged 12.0% yoy, while food prices increased by 2.9% yoy, and household durable goods saw a significant rise of 7.7% yoy. These numbers indicate persistent inflationary pressures across a wide range of goods and services.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3188; (P) 1.3251; (R1) 1.3349; More...

Intraday bias in GBP/USD remains on the upside for 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, below 1.3219 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3000 support holds.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Sustained break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Sep | -20 | -13 | -13 | |

| 23:30 | JPY | CPI Y/Y Aug | 3.00% | 2.80% | ||

| 23:30 | JPY | CPI Core Y/Y Aug | 2.80% | 2.80% | 2.70% | |

| 23:30 | JPY | CPI Core-Core Y/Y Aug | 2.00% | 1.90% | ||

| 01:00 | CNY | 1-Y Loan Prime Rate | 3.35% | 3.35% | 3.35% | |

| 01:00 | CNY | 5-Y Loan Prime Rate | 3.85% | 3.85% | 3.85% | |

| 02:52 | JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 06:00 | EUR | GermanyPPI M/M Aug | 0.20% | 0.00% | 0.20% | |

| 06:00 | EUR | GermanyPPI Y/Y Aug | -0.80% | -1.00% | -0.80% | |

| 06:00 | GBP | Retail Sales M/M Aug | 1.00% | 0.30% | 0.50% | 0.70% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 13.7B | 12.3B | 2.2B | 3.1B |

| 12:30 | CAD | Retail Sales M/M Jul | 0.90% | 0.50% | -0.30% | -0.20% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | 0.40% | 0.20% | 0.30% | |

| 12:30 | CAD | Industrial Product Price M/M Aug | -0.80% | -0.30% | 0.00% | -0.10% |

| 12:30 | CAD | Raw Material Price Index Aug | -3.10% | -2.00% | 0.70% | |

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -13 | -13 |

Canada’s retail sales rises 0.9% mom, 7 of 9 subsectors grow

Canada's retail sales rose 0.9% mom to CAD 66.4B in July, well above expectation of 0.5% mom. Sales were up in seven of nine subsectors, led by increases at motor vehicle and parts dealers. In volume terms, sales were also up 1.0% mom.

Advance estimate suggests that sales increased 0.5% mom in August.

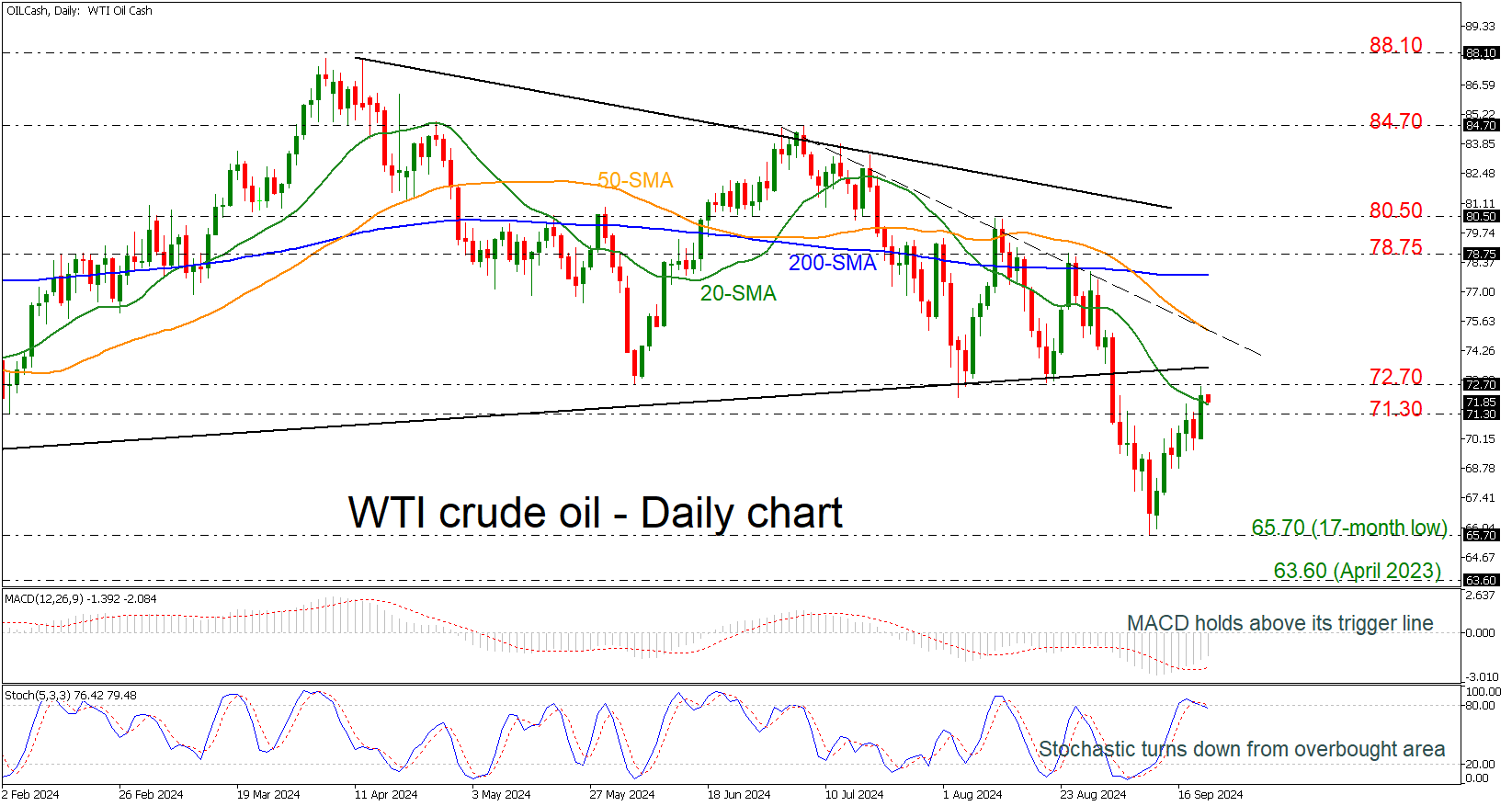

WTI Crude Oil Tries to Extend Its Bullish Correction

- WTI crude oil rebounds off 17-month low

- Technical oscillators are mixed

WTI crude oil prices have been creating a notable bullish correction after the significant bounce off the 17-month low of 65.70. Technically, the MACD oscillator is gaining some ground above its trigger line; however, the stochastic posted a bearish crossover within its %K and %D lines in the overbought region.

In case of more buying interest then the market may fight with the 72.70 resistance level ahead of the short-term descending trend line at 75.20, which overlaps with the 50-day simple moving average (SMA). Even higher, a strong obstacle could come from the 200-day SMA at 77.80.

On the flip side, a drop beneath the 71.30 support may drive the bears until the previous bottom of 65.70. Below that, the door could open for the April 2023 trough at 63.60.

All in all, WTI crude oil has been in a bearish tendency since it peaked at 84.70 on July and only a rally above the 200-day SMA may change the outlook to a more neutral one.

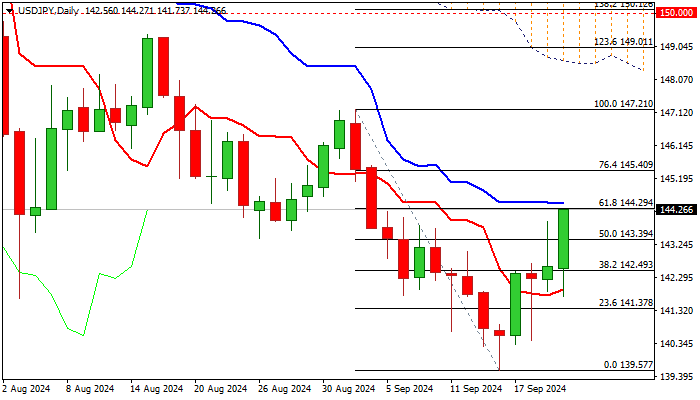

USD/JPY Outlook: Loses Ground as BoJ Keeps Rates on Hold and Says Not in Hurry for Further Tightening

USDJPY jumped over two figures on Friday after Bank of Japan kept interest rates unchanged and signaled it was not in rush for further hikes, despite the borrowing cost is still very low.

Renewed attempt higher comes after Thursday’s rally of almost identical size stalled on approach to 144 barrier, with subsequent pullback contributing to daily candle with long upper shadow.

This could be a significant warning despite today’s renewed strength, as key barriers at 144.29/45 (Fibo 61.8% of 147.21/139.57/ daily Kijun-sen) need to be cleared to sideline persisting downside risk.

Daily studies point to bearish signals from still strong negative momentum, thickening descending daily cloud and overbought stochastic, partially offset by 10/20DMA’s now turning to bullish setup.

Fresh recovery is expected to keep in play while holding above broken 20DMA (143.42) though larger picture to remain biased lower as long as the price action holds below daily Kijun-sen.

Res: 144.45; 145.00; 145.40; 146.07.

Sup: 143.42; 142.49; 142.27; 142.00.

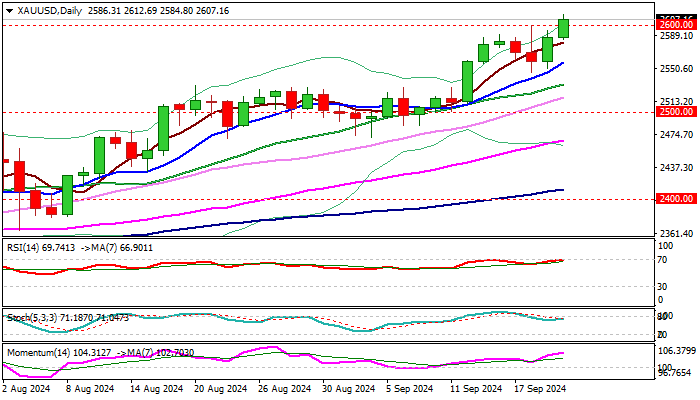

XAU/USD Outlook: Gold Surges to New All-Time High Above $2,600

Gold broke through psychological $2600 barrier and hit new all-time high on Friday morning, on track to register clear break higher after the resistance was cracked in post-Fed jump but resisted attack.

The yellow metal shined after market digested Fed’s decision, with prospects for more rate cuts, deteriorating geopolitical situation, growing uncertainty over fiscal conditions in a number of Western economies and ongoing destabilization of the US dollar, boosting its safe haven appeal.

Fresh bull-leg $2546 (low of a shallow correction) signals continuation of larger uptrend, with close above $2600 to confirm signal.

Gold is also on track for the second consecutive weekly gain, which came after a triple weekly Doji candles, adding to bullish continuation signals.

Gold price has moved at a high speed and rose from $2000 (which marked very strong resistance) to $2600 in about ten months.

The sentiment is very bullish and sustained break above $2600 would look for targets at $2628 and $2650 (Fibo projections) initially, with stronger bullish acceleration to bring in focus $2700.

Dips on partial profit taking should be shallow and mark positioning for further advance.

Res: 2614; 2628; 2636; 2650.

Sup: 2600; 2589; 2581; 2557.