Sample Category Title

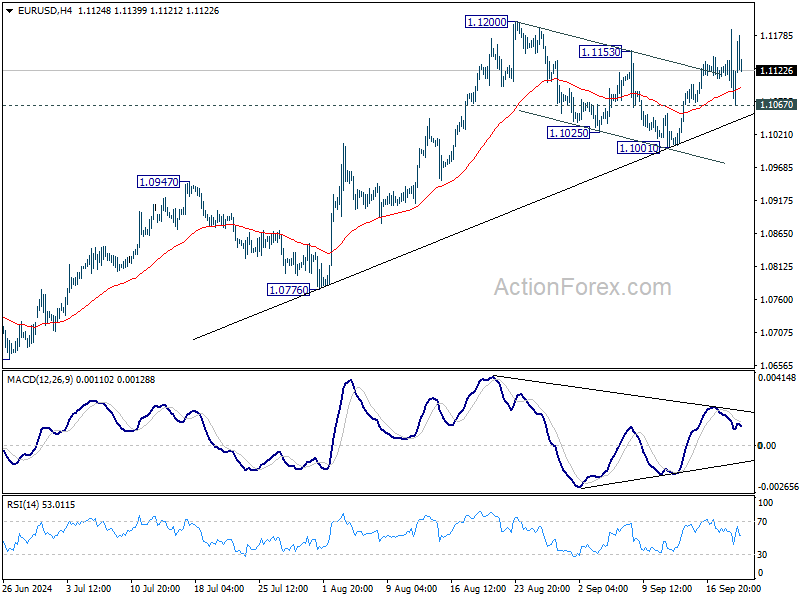

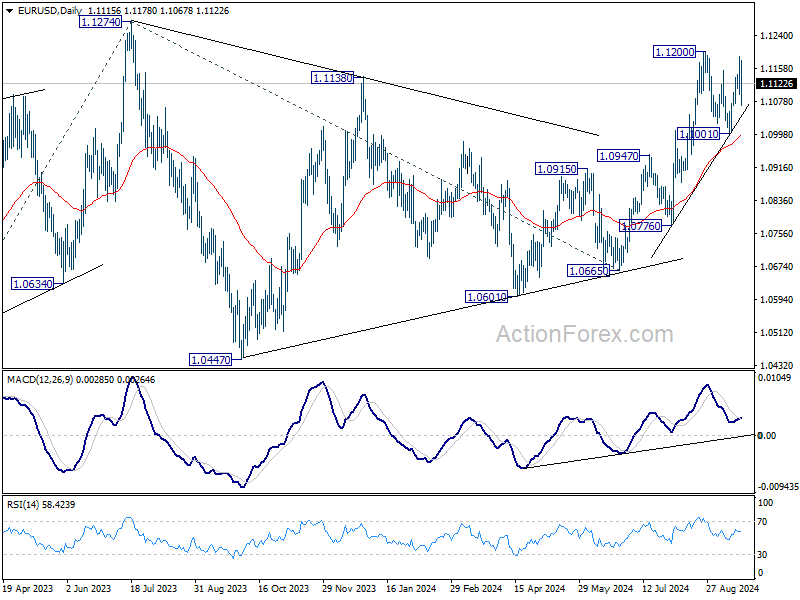

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1080; (P) 1.1135; (R1) 1.1172; More....

Intraday bias in EUR/USD stays mildly on the upside at this point. Decisive break of 1.1200 will resume larger rally from 1.0665 to 1.1274 high next. On the downside, however, break of 1.1072 will turn bias back to the downside for 1.1001 support instead.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Bank of England Review – Gradual Easing Cycle Supports GBP

- At today's monetary policy meeting the BoE left the Bank Rate unchanged at 5.00% as widely expected.

- The BoE delivered a hawkish twist to its guidance emphasising their gradual approach to reducing the restrictiveness of monetary policy. We think this supports our base case of the next cut in November and a pause in December.

- Gilt yields tracked higher and EUR/GBP moved lower on the hawkish vote split and communication.

As expected, the Bank of England (BoE) decided to keep the Bank Rate unchanged at 5.00%. The vote split was 8-1 with the majority of members voting for an unchanged decision and dove Dhingra voting for a 25bp cut.

The BoE retained much of its previous guidance noting that "monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further" but added that "In the absence of material developments, a gradual approach to removing policy restraint remains appropriate". Combined with the vote split, this delivered a slight hawkish twist pushing back on market expectations of a cut at every meeting. While data on balance has been slightly better than expected compared to the August MPR, the BoE noted upside risks to pay growth. Likewise, the BoE noted that "Bank staff expected services inflation to ease slightly further in Q4", which at 5.6% y/y in August remains uncomfortably elevated.

We think the communication today further supports our call of a more gradual approach to a cutting cycle. We expect the next 25bp cut in November with the Bank Rate ending the year at 4.75%.

On QT, the MPC announced another GBP 100bn of quantitative tightening for the coming year starting October. Given the maturity profile, the largest part will stem from maturities (GBP 87bn) and to a much lesser extent from sales (GBP 13bn).

Rates. 2Y Gilt yields moved higher on the statement but overall, the reaction in rates markets was muted. Markets price 28bp for November and 14bp in December. We see it as more likely that the BoE will pause in December.

FX. EUR/GBP moved lower on the announcement following the slightly hawkish vote split and notion of a gradual cutting cycle. The guidance delivered today highlights the more cautious approach of the BoE, which supports our case of a continued move lower in EUR/GBP. This is further amplified by UK economic outperformance and tight credit spreads. The key risk is policy action from the BoE. We stay long GBP/CHF.

Our call. We expect the BoE to deliver the next 25bp cut in November and this to be the final cut this year, making it less than markets expect (42bp by YE 2024). In 2025, we expect cuts at every meeting starting in February and until H2 2025 where we expect a step Bank of England Review - Gradual easing cycle supports GBP Bank of England Review - Gradual easing cycle supports GBP down to a quarterly pace. This leaves the Bank Rate at 3.25% by YE 2025.

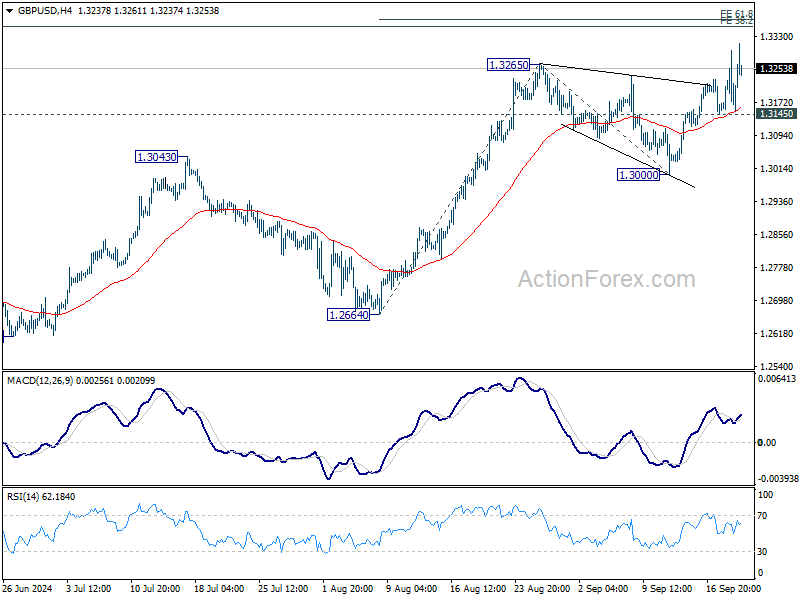

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3145; (P) 1.3221; (R1) 1.3290; More...

Intraday bias in GBP/USD remains on the upside at this point. Current rally should target 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371 in the near term. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, however, break of 1.3145 support will turn bias to the downside for deeper pullback to 1.3000 support next.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Sustained break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Sterling Gains on Cautious BoE, Investors Embrace Fed’s Message

Sterling surged notably today and reached its highest level against Dollar since March 2022. The move followed BoE's decision to hold interest rates steady as expected. The surprise came from Deputy Governor Dave Ramsden, who chose not to vote for a rate cut. The overall tone from BoE suggests that while further rate cuts are still on the horizon, they will likely proceed with caution. Concerns over persistently high inflation, especially in the services sector, remain a key issue for policymakers. For now, November is still seen as the most likely time for the next rate cut, but the path forward is far from set in stone.

Meanwhile, US markets seem to have come to terms with yesterday's 50 bps rate cut by Fed. Stock futures point to a sharp rally, with both DOW and S&P 500 poised to hit new all-time highs. At the same time, 10-year Treasury yields surged past 3.75%. Fed fund futures now price in a 67% chance of a smaller 25bps cut in November. The mix of rising stock prices, higher yields, and fed pricing reflects the market's confidence in Fed's strategy, with Jerome Powell having successfully conveyed that the aggressive rate cut was a preemptive measure rather than a panic reaction to economic weakness. Investors remain optimistic even with a gradual pace of easing moving forward.

Overall, Aussie and Kiwi have outpaced Sterling as the day's strongest performers so far, buoyed by risk-on sentiment. Aussie received additional support from strong employment data released earlier in the Asian session. Meanwhile, Yen and Swiss Franc are the weakest performers, reacting to the positive market sentiment and rising US and European yields. Dollar is also softening but cushioned by rising yields, while Euro and Canadian Dollar are in the middle of the pack.

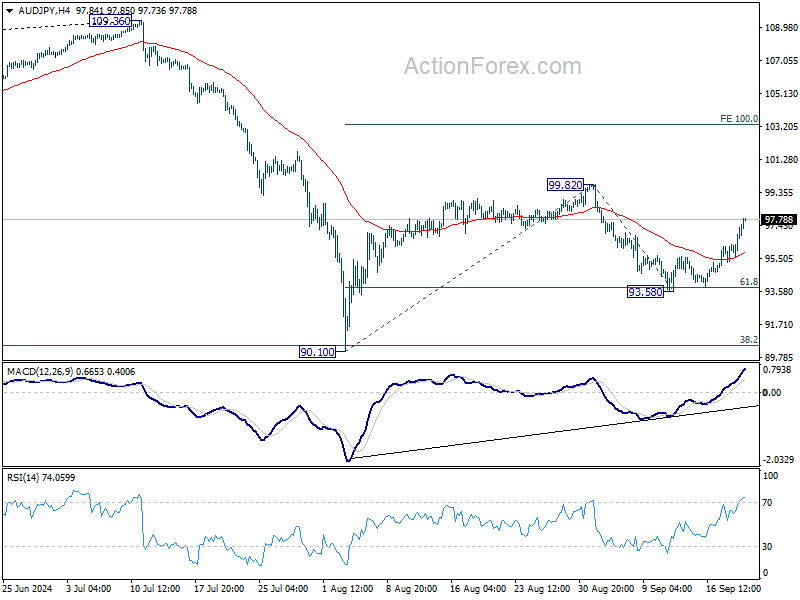

Technically, AUD/JPY is currently the top mover of the day, and the strong rally suggests that pull back from 99.82 has completed at 93.58 already, after drawing support from 61.8% retracement of 90.10 to 99.82. Further rise is now expected as long as 55 4H EMA holds (now at 95.88). Firm break of 99.82 will resume the whole rebound from 90.10. and target 100% projection of 90.10 to 99.82 from 93.58 at 103.30. Japan's CPI release and BoJ rate decision could both be the trigger of the next move.

In Europe at the time of writing, FTSE is up 0.98%. DAX is up 1.57%. CAC is up 1.95%. UK 10-year yield is up 0.050 at 3.896. Germany 10-year yield is up 0.005 at 2.202. Nikkei rose 2.13%. Hong Kong HSI rose 2.00%. China Shanghai SSE rose 0.69%. Singapore Strait Times rose 1.13%. Japan 10-year JGB yield rose 0.0268 to 0.854.

US jobless claims falls to 219k, vs exp 232k

US initial jobless claims fell -12k to 219k in the week ending September 14, below expectation of 232k. Four-week moving average of initial claims fell -3.5k to 227.5k.

Continuing claims fell -14k to 1829k in the week ending September 7. Four-week moving average of continuing claims fell -6.5k to 1844k.

BoE holds rates steady at 5% by hawkish 8-1 vote

BoE opted to keep the Bank Rate unchanged at 5.00%, as expected, with an 8-1 vote. Swati Dhingra, a known dove, was the only member voting for a 25bps rate cut. Deputy Governor Dave Ramsden, who has consistently supported cuts since May, chose not to vote for a reduction this time.

In its statement, BoE noted that UK economic indicators have shown "limited news" relative to expectations outlined in the August MPR. Inflation stood at 2.2% in August and is anticipated to rise to around 2.5% by year-end as the effects of last year's energy price declines drop out of the annual comparison. Services inflation remains notably elevated at 5.6%, while private sector wage growth slowed to 4.9% in the three months to July.

BoE emphasized that "absence of material developments", it will continue to follow a "gradual approach" to unwinding policy restrictions. Monetary policy is expected to stay restrictive for a sufficiently long period until inflation risks subside, ensuring it returns to the 2% target. The central bank reaffirmed its commitment to closely monitor inflation persistence and determine the necessary level of restrictiveness "at each meeting."

ECB's Schnabel: Sticky services inflation persists, wage growth expected to ease

In a speech today, ECB Executive Board member Isabel Schnabel noted the ongoing challenge of "sticky" services inflation, which continues to keep headline inflation elevated. She highlighted that price pressures within the services sector are "broad-based and global," and that the momentum remains high, well above levels that would be consistent with price stability. This persistent inflation in services is a key concern for the ECB's outlook.

However, there is some optimism regarding easing wage pressures. Schnabel pointed to expectations that wage growth will slow as the effects of past price shocks begin to fade. Additionally, firms are projecting moderation in selling price increases, as "profit margins buffer higher wages". She also noted that while demand for services has remained resilient, there are signs it is beginning to soften.

Schnabel also addressed the risks posed by geopolitical uncertainty, stating that it continues to be a significant factor influencing inflationary pressures. She cautioned that inflation perceptions remain high, which makes inflation expectations more "fragile to new shocks."

SECO: Swiss economic growth sluggish in 2024, moderate recovery expected in 2025

Switzerland's State Secretariat for Economic Affairs forecasts the economy to perform "considerably below average" in 2024, with modest growth expected to pick up in 2025. Adjusted for major sporting events, GDP growth is projected to be at 1.2% for 2024, unchanged from June's estimates. However, the outlook for 2025 has been slightly downgraded to 1.6%, compared to June forecast of 1.7%.

Inflation is now expected to decline faster than previously thought, with projections for 2024 revised down to 1.2% (from 1.4% in June) and 0.7% for 2025 (down from 1.1%). This easing of inflationary pressures reflects lower price growth, especially in sectors impacted by the strong appreciation of the Swiss Franc.

SECO acknowledged the challenges posed by sluggish economic activity in Europe, which, alongside the real appreciation of the Swiss Franc, is straining export-sensitive sectors in Switzerland this year. Looking ahead, gradual recovery in Europe is expected to support Swiss exports and boost investments in 2025, helping to stabilize growth across key sectors.

New Zealand GDP contracts - 0.2% qoq in Q2, manufacturing offers some resilience

New Zealand's GDP contracted by -0.2% qoq in Q2, slightly better than the expected -0.4% qoq decline. Despite the overall negative figure, 7 out of 16 industries posted increases, with manufacturing leading the growth.

GDP per capita also saw a decline, falling by -0.5%, marking the fourth consecutive quarter of contraction in this metric. The last time GDP per capita increased was back in Q3 2022.

On the expenditure side, GDP was flat for the quarter, showing no growth or contraction at 0.0%. Household spending, however, provided a small positive with a 0.4% increase. Real gross national disposable income was also flat at 0.0%, reflecting limited income growth in the face of economic headwinds.

Australia's employment grows 47.5k in Aug, labor market remains tight

Australia's employment grew by a robust 47.5k in August, significantly exceeding expectations of 25.3k. While full-time employment declined slightly by -3.1k, part-time jobs saw a sharp increase of 50.6k, boosting the overall figure. The employment-to-population ratio edged up by 0.1% to 64.3%, just shy of the record high of 64.4% set in November 2023.

Unemployment rate held steady at 4.2%, as anticipated, with the number of unemployed individuals falling by -10.5k, a -1.6% mom decline. Participation in the labor force remained strong, with the participation rate unchanged at 67.1%. Additionally, monthly hours worked rose by 0.4% mom, reflecting continued labor demand.

Kate Lamb, head of labor statistics at ABS, commented: "The employment and participation measures remain historically high, while unemployment and underemployment measures are still low, especially compared with what we saw before the pandemic. This suggests the labor market remains relatively tight."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3145; (P) 1.3221; (R1) 1.3290; More...

Intraday bias in GBP/USD remains on the upside at this point. Current rally should target 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371 in the near term. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, however, break of 1.3145 support will turn bias to the downside for deeper pullback to 1.3000 support next.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Sustained break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | -0.20% | -0.40% | 0.20% | 0.10% |

| 01:30 | AUD | Employment Change Aug | 47.5K | 25.3K | 58.2K | 48.9K |

| 01:30 | AUD | Unemployment Rate Aug | 4.20% | 4.20% | 4.20% | |

| 06:00 | CHF | Trade Balance (CHF) Aug | 4.58B | 5.05B | 4.89B | 4.88B |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | 39.6B | 40.3B | 50.5B | |

| 11:00 | GBP | BoE Interest Rate Decision | 5.00% | 5.00% | 5.00% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0--1--8 | 0--2--7 | 0--5--4 | |

| 12:30 | USD | Initial Jobless Claims (Sep 13) | 219K | 232K | 230K | 231K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Sep | 1.7 | 2.4 | -7 | |

| 12:30 | USD | Current Account (USD) Q2 | -266.8B | -260B | -238B | -241B |

| 14:00 | USD | Existing Home Sales Aug | 3.85M | 3.95M | ||

| 14:30 | USD | Natural Gas Storage | 53B | 40B |

US jobless claims falls to 219k, vs exp 232k

US initial jobless claims fell -12k to 219k in the week ending September 14, below expectation of 232k. Four-week moving average of initial claims fell -3.5k to 227.5k.

Continuing claims fell -14k to 1829k in the week ending September 7. Four-week moving average of continuing claims fell -6.5k to 1844k.

ECB’s Schnabel: Sticky services inflation persists, wage growth expected to ease

In a speech today, ECB Executive Board member Isabel Schnabel noted the ongoing challenge of "sticky" services inflation, which continues to keep headline inflation elevated. She highlighted that price pressures within the services sector are "broad-based and global," and that the momentum remains high, well above levels that would be consistent with price stability. This persistent inflation in services is a key concern for the ECB’s outlook.

However, there is some optimism regarding easing wage pressures. Schnabel pointed to expectations that wage growth will slow as the effects of past price shocks begin to fade. Additionally, firms are projecting moderation in selling price increases, as "profit margins buffer higher wages". She also noted that while demand for services has remained resilient, there are signs it is beginning to soften.

Schnabel also addressed the risks posed by geopolitical uncertainty, stating that it continues to be a significant factor influencing inflationary pressures. She cautioned that inflation perceptions remain high, which makes inflation expectations more "fragile to new shocks."

BoE holds rates steady at 5% by hawkish 8-1 vote

BoE opted to keep the Bank Rate unchanged at 5.00%, as expected, with an 8-1 vote. Swati Dhingra, a known dove, was the only member voting for a 25bps rate cut. Deputy Governor Dave Ramsden, who has consistently supported cuts since May, chose not to vote for a reduction this time.

In its statement, BoE noted that UK economic indicators have shown "limited news" relative to expectations outlined in the August MPR. Inflation stood at 2.2% in August and is anticipated to rise to around 2.5% by year-end as the effects of last year’s energy price declines drop out of the annual comparison. Services inflation remains notably elevated at 5.6%, while private sector wage growth slowed to 4.9% in the three months to July.

BoE emphasized that "absence of material developments", it will continue to follow a "gradual approach" to unwinding policy restrictions. Monetary policy is expected to stay restrictive for a sufficiently long period until inflation risks subside, ensuring it returns to the 2% target. The central bank reaffirmed its commitment to closely monitor inflation persistence and determine the necessary level of restrictiveness "at each meeting."

(BOE) Bank Rate maintained at 5%

Monetary Policy Summary, September 2024

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 18 September 2024, the MPC voted by a majority of 8–1 to maintain Bank Rate at 5%. One member preferred to reduce Bank Rate by 0.25 percentage points, to 4.75%. The Committee voted unanimously to reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the next 12 months, to a total of £558 billion.

Monetary policy decisions have been guided by the need to squeeze persistent inflationary pressures out of the system so as to return CPI inflation to the 2% target both in a timely manner and on a lasting basis. Policy has been acting to ensure that inflation expectations remain well anchored. As set out at the time of the August Monetary Policy Report, the Committee’s deliberations have been supported by the consideration of a range of cases, to which different probabilities and different risks can be attached.

In the first case, the unwinding of the global shocks that drove up inflation and the resulting fall in headline inflation should continue to feed through to weaker pay and price-setting dynamics. The persistence of inflationary pressures would therefore dissipate with a less restrictive stance of monetary policy than in other cases.

In the second case, a period of economic slack, in which GDP falls below potential and the labour market eases further, may be required in order for pay and price-setting dynamics to normalise fully. Domestic inflationary persistence would then be expected to fade away, owing to the opening up of slack from a more restrictive stance of monetary policy relative to the first case.

In the third case, the economy may be subject to structural shifts such as changes in wage and price-setting following the major supply shocks experienced over recent years. The degree of restrictiveness of monetary policy may be less than embodied in the Committee’s latest assessment, meaning that monetary policy would have to remain tighter for longer.

Since the MPC’s previous meeting, global activity growth has continued at a steady pace, although some data outturns suggest greater uncertainty around the near-term outlook. Oil prices have fallen back, reflecting in large part weaker demand. Market-implied paths for policy rates across major advanced economies have declined.

There has generally been limited news in UK economic indicators relative to the Committee’s expectations in the August Monetary Policy Report. Headline GDP growth is expected to return to its underlying pace of around 0.3% per quarter in the second half of the year. Twelve-month CPI inflation was 2.2% in August, and is expected to increase to around 2½% towards the end of this year as declines in energy prices last year fall out of the annual comparison. Services consumer price inflation remained elevated at 5.6% in August. Private sector regular average weekly earnings growth declined to 4.9% in the three months to July.

At this meeting, the Committee voted to maintain Bank Rate at 5%.

In the absence of material developments, a gradual approach to removing policy restraint remains appropriate. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The Committee continues to monitor closely the risks of inflation persistence and will decide the appropriate degree of monetary policy restrictiveness at each meeting.

Minutes of the Monetary Policy Committee meeting ending on 18 September 2024

1: Before turning to its immediate policy decisions, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

1: UK-weighted global GDP was estimated to have grown by 0.5% in 2024 Q2, broadly in line with the projection in the August Monetary Policy Report, and consistent with steady growth over recent quarters. US GDP had grown more strongly than had been anticipated, while GDP growth had moderated in the euro area and in China in the second quarter.

2: In the third quarter, euro-area GDP growth was expected to be a little weaker than had been anticipated in the August Report, and US GDP growth was expected to moderate somewhat, in line with previous expectations. Activity indicators such as PMIs suggested ongoing weakness in the manufacturing sector in both economies over recent months, while the services sector had continued to expand.

3: Labour market outturns in the United States had been softer in July and August relative to previous months. Unemployment in the euro area had remained low, pointing to some continuing tightness. Wage growth had continued to moderate across both regions.

4: Headline consumer price inflation had declined further towards central bank targets in the euro area and in the United States. In the euro area, 12-month HICP inflation had been 2.2% in August, while core inflation had ticked down to 2.8%, in line with market participants’ expectations. US CPI inflation had fallen to 2.5% in August, while core CPI inflation had remained unchanged at 3.2%, also in line with market expectations. Annual services price inflation had remained elevated in both economies, although higher frequency measures pointed to some easing over recent months.

5: There were tentative signs of a shift in the balance of risks to global activity towards the downside. Consistent with that, since the MPC's previous meeting, the Brent spot oil price had declined by around 6%, to $75 per barrel. Market contacts had ascribed the moves largely to weaker demand in China, as indicators of domestic demand there had continued to be soft.

Monetary and financial conditions

6: Since the MPC’s previous meeting, government bond yields had fallen across major advanced economies in response to the softening in US labour market data and associated FOMC communications. Market-implied paths for policy rates across economies had generally ended the period lower. Coupled with UK data releases in that period having been largely in line with market expectations, that meant UK interest rate movements had been driven primarily by developments in the United States. Nevertheless, the UK market-implied path had fallen by less than in the United States. That had been associated with an appreciation of sterling against the dollar of 3%, which had accounted for most of the 1% increase in the sterling effective exchange rate since the previous MPC meeting.

7: Movements in yields across major advanced economies had been particularly pronounced early in August, alongside large moves in asset prices more generally. Market-specific factors including seasonally low market liquidity were likely to have exacerbated reactions to news. While these early August moves had unwound quickly, yields across countries had nevertheless ended the period lower. In contrast, UK equity prices had been little changed since the MPC’s previous meeting and the S&P 500 and Euro Stoxx 50 had both increased somewhat.

8: At its meeting on 12 September, the ECB Governing Council had reduced its key policy rate by 25 basis points, in line with market expectations. In its statement, the Governing Council had reiterated its data-dependent and meeting-by-meeting approach, focused on the inflation outlook and strength of policy transmission. At its meeting ending on 18 September, the FOMC was expected to reduce the federal funds rate by either 25 or 50 basis points.

9: In the United Kingdom, Bank Rate expectations implied by market pricing had continued to suggest that the next 25 basis point cut would occur in November. That was consistent with the Bank’s latest Market Participants Survey (MaPS). Beyond November, while the median MaPS profile implied a slightly slower pace of reduction in Bank Rate than the market-implied path, both pointed to much more gradual reductions than were expected in the United States and to a lesser extent in the euro area.

10: Regarding credit conditions, it was too soon to assess fully the extent to which the Bank Rate reduction in August had passed through to the relevant saving and borrowing rates facing households and corporates. Nevertheless, as had been anticipated, mortgage rates had fallen since the MPC’s previous meeting broadly in line with declines in risk-free reference rates.

11: The share of two-year fixed-rate mortgages within new secured household lending had been increasing since 2023 Q1, despite rates on these mortgages being above five-year fixed rates over this period. That had reversed the previous trend whereby longer-duration mortgage fixes had increased in popularity since 2016, probably reflecting household expectations of lower interest rates. Slow mortgage stock turnover meant that the share of five-year fixed-rate mortgages in outstanding lending had remained historically high.

12: Household saving preferences had also adjusted over the past year, as rates offered on time deposits had become relatively less attractive, reflecting the declines in risk-free reference rates. Deposit flows had shifted into sight deposits and ISAs, many of which were instant access. Household deposits had continued to be the main driver of aggregate sterling broad money growth. The latter had increased to 1.6% on an annual basis in July, but had remained weak by historical standards.

Demand and output

13: UK GDP had increased by 0.6% in 2024 Q2, 0.1 percentage points lower than had been expected in the August Monetary Policy Report. That had followed 0.7% growth in Q1, but Bank staff judged that the underlying pace of growth had been somewhat weaker during the first half of the year.

14: Within the expenditure components of Q2 GDP, household consumption had risen by 0.2% on the quarter, while business and housing investment had both declined by 0.1%. Real government expenditure had increased by 1.6%, and there had continued to be some evidence of greater-than-projected central government spending in recent public sector finances data.

15: GDP had been unchanged on the month in both July and June but had grown by 0.5% on a three-month-on-three-month basis in July. Slightly weaker-than-expected output in July had been concentrated in the manufacturing and professional services sectors.

16: Bank staff now expected GDP growth of 0.3% in 2024 Q3, marginally weaker than the 0.4% rate that had been incorporated in the August Report. That was broadly in line with estimates of the underlying growth rate that had been extracted from models based on a range of business survey indicators and on disaggregated GDP data. The latest intelligence from the Bank’s Agents suggested that improving real incomes, the August Bank Rate reduction and anticipated further cuts in interest rates had underpinned improved sentiment and expectations of increased activity across most sectors around the turn of the year.

17: There had been little news from most indicators of consumer spending, although housing market data had strengthened somewhat. Retail sales volumes had been volatile, around a very gradually rising trend since the start of the year. GfK consumer confidence had been unchanged in August. Forward-looking indicators in the housing market had continued to point to a recovery in home buyer enquiries and prices, while mortgage approvals for house purchase had increased to their highest level since September 2022.

18: The Committee discussed the near-term outlook for activity and the evolution of the output gap. Although uncertainties surrounded this assessment, overall demand and supply were judged to have been broadly in balance over recent quarters. A continuation of the current pace of underlying GDP growth would, given the Committee’s view of potential supply growth, be consistent with little change in the output gap through the end of this year. That path was a little stronger than the August Report projections, however, in which demand growth had been expected to slow at the end of this year and a significant margin of spare capacity had been projected to open up over time. That projection in part reflected the previously announced medium-term tightening in the stance of fiscal policy, prior to the upcoming Budget. The Committee would also continue to monitor closely how the different channels of the monetary transmission mechanism were interacting with the dynamics of the household saving ratio, and in turn the outlook for consumer demand.

Supply, costs and prices

19: Labour market data quality issues continued to be an area of concern. Very low achieved sample sizes meant Labour Force Survey (LFS)-based estimates of labour market dynamics remained subject to considerable uncertainties. This was making it difficult to gauge the underlying state of labour market activity. The MPC had, for some time, utilised a wide range of data to inform its judgements on the labour market, including official data, business surveys and intelligence from the Bank’s Agents.

20: A Bank staff indicator model of underlying employment continued to point to growth of around 0.2% per quarter, broadly in line with population growth. There was greater dispersion among outturns from individual employment indicators. The KPMG/REC/S&P Global UK Report on Jobs had continued to point to a contraction in employment while the Lloyds Business Barometer suggested an expansion.

21: In line with softening labour demand, vacancies had continued to fall back gradually, although at a slower pace than in 2023 and they had remained above pre-pandemic levels. The REC Report and Agents’ intelligence signalled a continued easing in recruitment difficulties, with the latter suggesting improved job retention in some sectors. The vacancies-to-unemployment ratio had returned to its pre-pandemic average at the start of 2024 Q2. A Bank staff indicator model suggested that underlying unemployment had increased steadily over the past few quarters, in contrast to more volatile LFS data.

22: Indicators of households’ inflation expectations had largely normalised to close to their historical averages. The Bank of England/Ipsos Inflation Attitudes Survey’s measure of median short-term inflation expectations had fallen to 2.7% in August. The corresponding measure of medium-term expectations had remained close to, but below, its historical average. The Citi/YouGov indicator of households’ short-term inflation expectations had increased slightly to 3.1% in August from 2.7% previously, possibly owing to media reports of a rise in the Ofgem utility price cap in October. Businesses’ own price expectations, as reported in the DMP Survey, had remained at slightly more elevated levels, although on a continued downward path.

23: This normalisation in inflation expectations, as well as, to a lesser extent, the easing in labour market tightness, had supported continued moderation in pay growth. Annual private sector regular average weekly earnings growth had eased to 4.9% in the three months to July from 5.3% in the three months to June, broadly in line with August Monetary Policy Report projections. Other surveys suggested that wage growth would continue to moderate, although remain above inflation target-consistent levels, with the DMP Survey indicating a fall to approximately 4% over the next year. The latest Agents’ intelligence indicated that pay settlements over the second half of the year were, as expected, coming in at lower rates compared to H1, and 2025-expected settlements might be in a 2 to 4% range. There remained the possibility of some upside risk to pay growth depending on the trajectory of the National Living Wage (NLW) in the first half of next year.

24: Twelve-month CPI inflation had been 2.2% in August and July, slightly lower than August Report expectations. Consumer core goods and food price inflation had remained subdued as the cost pressures from previous global shocks had unwound further, and producer price levels had been broadly flat. Energy prices had continued to drag on CPI inflation.

25: Services price inflation had increased to 5.6% in August compared to 5.2% in July and 5.7% in June. This was slightly lower in August than had been expected at the time of the August Report. There had been volatility in a number of services sub-components in the July and August outturns, including accommodation and catering prices and airfares.

26: The Committee discussed momentum in services price inflation and price-setting behaviour in firms. Strength in services price inflation was supported by evidence from the DMP Survey which showed firms’ own-price inflation continuing to fall, but to a lesser extent among services firms. July CPI microdata pointed to a higher proportion of services prices being raised each month than was the case pre-Covid, though with some easing in catering services where food input costs had moderated. The monthly annualised inflation rates of a seasonally adjusted services price measure, which excluded indexed and volatile components, rents and foreign holidays, had averaged around 4% in the three months to August, close to its average since the end of 2023. Although it had fallen from its peak level, the apparent stability in this measure suggested further pass-through from lower labour costs and easing inflation expectations was still to come. Accordingly, Bank staff expected services inflation to ease slightly further in Q4.

27: CPI inflation was expected to increase somewhat over the remainder of this year, owing to the smaller drag on 12-month inflation from domestic energy bills. The announced uptick in utility prices to take effect in October was likely to be offset somewhat by the recent decrease in petrol prices.

The immediate policy decisions

28: The Monetary Policy Committee sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

29: Monetary policy decisions had been guided by the need to squeeze persistent inflationary pressures out of the system so as to return CPI inflation to the 2% target both in a timely manner and on a lasting basis. Policy had been acting to ensure that inflation expectations remained well anchored. As set out at the time of the August Monetary Policy Report, the Committee’s deliberations had been supported by the consideration of a range of cases, to which different probabilities and different risks could be attached.

30: In the first case, the unwinding of the global shocks that had driven up inflation and the resulting fall in headline inflation should continue to feed through to weaker pay and price-setting dynamics. The persistence of inflationary pressures would therefore dissipate with a less restrictive stance of monetary policy than in other cases.

31: In the second case, a period of economic slack, in which GDP fell below potential and the labour market eased further, might be required in order for pay and price-setting dynamics to normalise fully. Domestic inflationary persistence would then be expected to fade away, owing to the opening up of slack from a more restrictive stance of monetary policy relative to the first case.

32: In the third case, the economy might be subject to structural shifts such as changes in wage and price-setting following the major supply shocks that had been experienced over recent years. The degree of restrictiveness of monetary policy might be less than embodied in the Committee’s latest assessment, meaning that monetary policy would have to remain tighter for longer.

33: The Committee continued to monitor the accumulation of evidence from a broad range of indicators, with a focus on the extent to which it was possible over time to use developments in data series to assess the various cases.

34: Since the MPC’s previous meeting, global activity growth had continued at a steady pace, although some data outturns suggested greater uncertainty around the near-term outlook. Oil prices had fallen back, reflecting in large part weaker demand. Market-implied paths for policy rates across major advanced economies had declined.

35: There had generally been limited news in UK economic indicators relative to the Committee’s expectations in the August Monetary Policy Report. Headline GDP growth was expected to return to its underlying pace of around 0.3% per quarter in the second half of the year. Based on a broad set of indicators, the MPC judged that the labour market continued to loosen but that it remained tight by historical standards.

36: Twelve-month CPI inflation had been 2.2% in August, and was expected to increase to around 2½% towards the end of this year as declines in energy prices last year fell out of the annual comparison. Services consumer price inflation had remained elevated at 5.6% in August. Private sector regular average weekly earnings growth had declined to 4.9% in the three months to July. Households’ inflation expectations had largely normalised to close to their historical averages, although businesses’ inflation expectations had remained at slightly more elevated levels.

37: Different members took different views on the probabilities and risks associated with the various cases that the Committee was considering, which were informing their votes on Bank Rate.

38: Eight members preferred to maintain Bank Rate at 5% at this meeting. Wage and price-setting had continued to normalise and UK activity growth had been broadly in line with expectations, although there was some greater uncertainty around the near-term global outlook. There was a range of views among these members on the degree to which the unwinding of past global shocks, the normalisation in inflation expectations and the current restrictive policy stance would lead underlying domestic inflationary pressures to continue to unwind, or whether these pressures could prove more entrenched, possibly as a result of more structural factors or greater momentum in demand. Despite these differences of view, the current policy stance was judged to be appropriate. For most members, in the absence of material developments, a gradual approach to removing policy restraint would be warranted.

39: One member preferred a 0.25 percentage point reduction in Bank Rate at this meeting. Bank Rate needed to become less restrictive now to enable a smooth and gradual transition in the policy stance, and to account for lags in transmission. CPI inflation had been on a firm downward trajectory for some time. Data developments remained consistent with CPI inflation staying sustainably at target, given the further easing in the labour market, continued falls in inflation expectations and forward-looking indicators of pass-through, and the subdued outlook for demand.

40: Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further. The Committee continued to monitor closely the risks of inflation persistence and would decide the appropriate degree of monetary policy restrictiveness at each meeting.

41: The MPC would make a full assessment of recent and prospective developments as part of its forthcoming November forecast round.

Annual decision on the pace of reduction in the stock of UK government bond purchases held for monetary policy purposes

42: As set out in the minutes of its August 2022 meeting, the MPC had committed to review the reduction in the Asset Purchase Facility (APF) annually and, as part of that, to set an amount for the reduction in the stock of purchased UK government bonds (gilts) over the subsequent 12-month period. Box A of the August 2024 Monetary Policy Report had set out an assessment of the process of quantitative tightening over the previous year.

43: The Committee continued to judge that reducing the size of the APF had the benefit of reducing the risk of a ratchet upwards in the size of the Bank’s balance sheet over time, and thus should increase the headroom and flexibility available to the Bank to use its balance sheet in the future if needed.

44: The appropriate pace of gilt stock reduction would continue to be guided by a set of key principles, which the MPC had first outlined in the August 2021 Monetary Policy Report. First, the Committee intended to use Bank Rate as its active policy tool when adjusting the stance of monetary policy. Second, sales would be conducted so as not to disrupt the functioning of financial markets. Third, to help achieve that, sales would be conducted in a gradual and predictable manner over a period of time.

45: As set out in the Box in the August 2024 Report, the Committee judged that quantitative tightening had continued to proceed smoothly. There was no evidence of a negative impact of gilt sales on market functioning across a range of financial market measures. In particular, measures of gilt market liquidity had further improved. APF reduction was likely to have had some tightening effect on yields, which, while difficult to measure precisely, was judged to have been modest. That was in line with the MPC’s previous expectations, and was broadly consistent with findings from other empirical studies and central banks. The Committee would continue to learn from monitoring developments as the process progressed.

46: While it remained hard to measure precisely the marginal effect of quantitative tightening on the economy, the MPC’s forecasts were conditioned on asset prices that incorporated announced and expected APF reductions. The MPC had therefore taken this effect into account when setting the desired monetary policy stance using Bank Rate. Any tightening effect from the reduction in the APF would have led to a slightly lower path for Bank Rate, all else equal. Given that the impact of APF reduction was judged to have been modest, this was unlikely to have made a material difference to the appropriate path for Bank Rate over the past year.

47: The Committee considered the case to maintain the pace of gilt stock reduction at £100 billion over the 12 months ahead, of which £87 billion would be maturing APF gilt holdings. Bank staff had briefed the MPC on the current state of economic and market conditions. The Financial Policy Committee (FPC) had also been briefed on the MPC’s deliberations.

48: All members of the MPC agreed at this meeting that the Bank of England should reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the 12-month period from October 2024 to September 2025, comprising both maturing gilts and sales.

49: The MPC also reaffirmed that there would be a high bar for amending the planned reduction in the stock of purchased gilts outside a scheduled annual review. That was in order to remain consistent with the principles that Bank Rate should be the active policy tool when adjusting the stance of monetary policy, and that APF reduction should be predictable. In judging whether that bar was met, the FPC would also have a role through its assessment of financial stability.

50: The Chair invited the Committee to vote on the propositions that:

- Bank Rate should be maintained at 5%; and

- The Bank of England should reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the next 12 months, to a total of £558 billion.

51: Eight members (Andrew Bailey, Sarah Breeden, Megan Greene, Clare Lombardelli, Catherine L Mann, Huw Pill, Dave Ramsden and Alan Taylor) voted in favour of the first proposition. Swati Dhingra voted against this proposition, preferring to reduce Bank Rate by 0.25 percentage points, to 4.75%.

52: The Committee voted unanimously in favour of the second proposition.

Operational considerations

53: On 18 September 2024, the stock of UK government bonds held for monetary policy purposes was £659 billion.

54: At this meeting, the MPC had voted to reduce the stock of UK government bond purchases held for monetary policy purposes by £100 billion over the 12-month period from October 2024 to September 2025. The details of the first quarter of the associated gilt sales programme, covering 2024 Q4, were set out in a Market Notice accompanying these minutes. The Bank would continue to set auction sizes each quarter, to meet the MPC’s annual target as closely as practicable.

55: The following members of the Committee were present:

Andrew Bailey, Chair

Sarah Breeden

Swati Dhingra

Megan Greene

Clare Lombardelli

Catherine L Mann

Huw Pill

Dave Ramsden

Alan Taylor

Sam Beckett was present as the Treasury representative.

David Roberts was present on 12 September, and Jonathan Bewes on 16 September, as observers for the purpose of exercising oversight functions in their roles as members of the Bank’s Court of Directors.

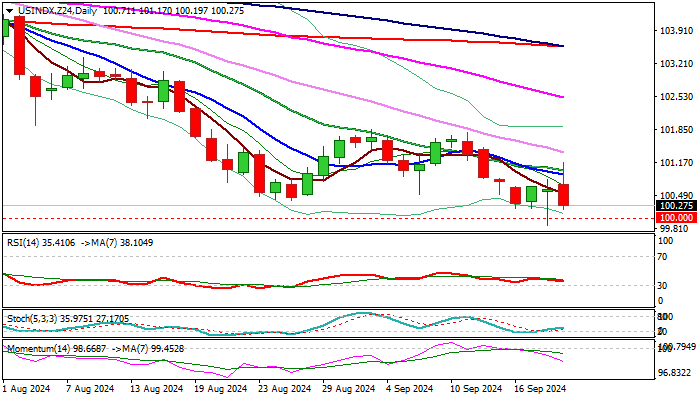

Dollar Index Outlook: Lacks Direction Signals in Post-Fed Trading

Wide post-Fed swings signal that the dollar is still looking for direction, as long-tailed Wednesday’s candle and long upper shadow forming today, support scenario of extended directionless mode.

Short-lived spike below psychological 100 support (hit 14-month low in immediate reaction to Fed’s decision) was followed by rise to one-week high, which failed to sustain gains, keeping the price within a range.

Confronting signals from a jumbo rate cut and renewed narrative of soft landing, due to still resilient economy, keep the dollar on hold for now.

On the other hand, daily studies remain in full bearish setup and contribute to signals of continuation of larger downtrend, after recent correction (100.38/101.79) was completed.

However, bears need to register a weekly close below 200WMA (100.33) and clear break below 100 level, to open way for extension of the bear-leg from 105.78 (Jun 28 high), towards a higher base at 99.20 zone (July 2023) and Fibo support at 98.92 61.8% of 89.15/114.72 uptrend).

Near-term action is expected to remain biased lower while holding below converged descending 10/20DMA’s (100.91/101.01).

Res: 100.91; 101.01; 101.37; 101.79.

Sup: 100.00; 99.86; 99.20; 98.92.

.

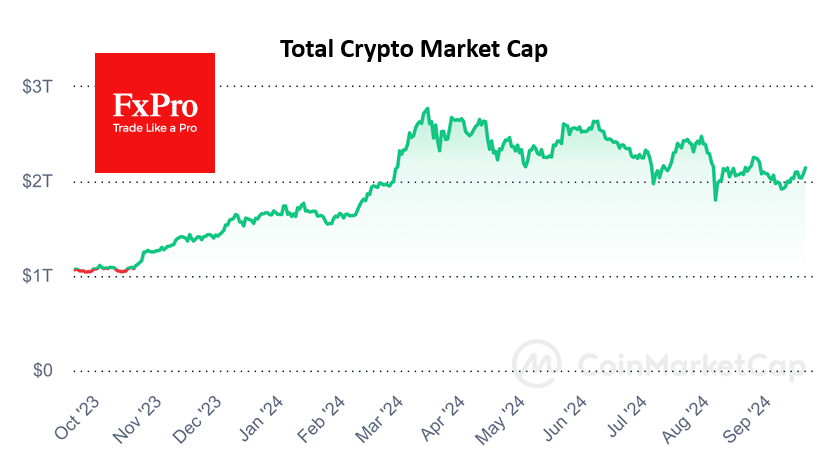

Crypto Market Climbs Out of the Pit

Market Picture

The crypto market rallied solidly by 3% to $2.15 trillion, gaining further momentum after the Fed’s decisive rate cut. Increased risk appetite in the markets after the Fed’s decision helped cryptocurrencies hit highs over the past three weeks. The crypto market has been moving within a downward corridor since mid-March, and only a surpassing of the recent $2.25 trillion peaks could change this trend.

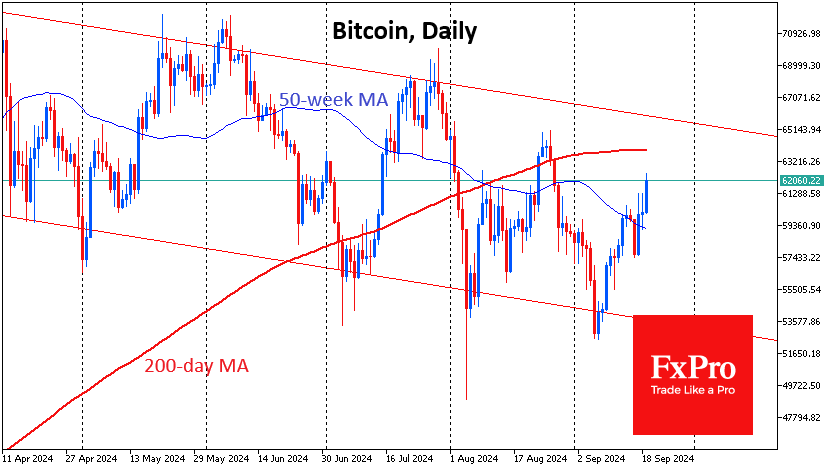

Bitcoin has reached the $62K level. That’s an impressive 19% gain since the lows in early September, but only +7% in 7 days and less than +2% in 30 days. The downtrend has been in place since March, and the previous peak of around $64K roughly coincides with the 200-day moving average. We assume that Bitcoin may encounter serious resistance at this level, overcoming which would clear the way up.

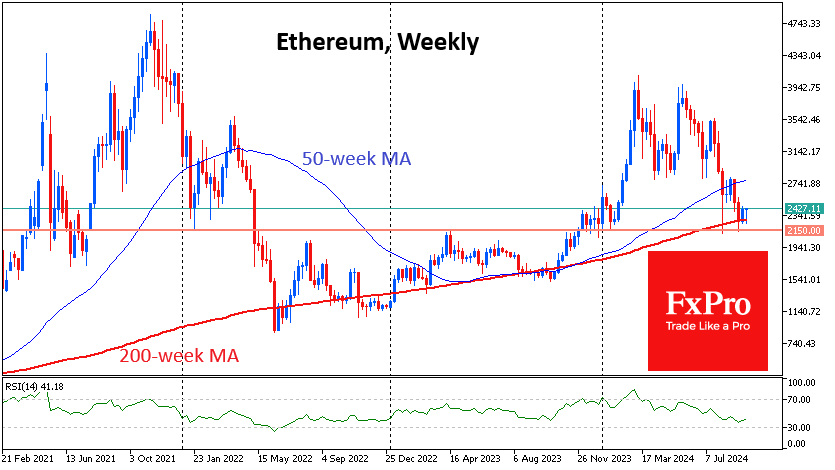

Ethereum has shown a promising rebound from its 200-week average, ending the week in positive territory. From current levels above $2400, significant resistance is unlikely to be encountered until the $2800 area, near the 50-week average.

News background

Bitcoin balances on centralised platforms have fallen by around 15% since the start of the year to 470,000 BTC, CryptoQuant noted. That’s the lowest since 2016, potentially easing selling pressure.

The Bitcoin market has seen a general decline in demand and activity from investors. At the same time, the prevailing sentiment is to hold coins. This “equilibrium” position has coincided with an increase in the capitalisation of stablecoins, which creates a compressed spring effect for the bitcoin price, Glassnode notes.

The Republican congressmen said in a letter to agency head Gary Gensler that the SEC should clearly define airdrops. The SEC has previously said that airdrops could be considered a “sale or distribution of securities.”

Cryptocurrency exchange Bitget and fund Foresight Ventures announced a $30 million acquisition of Toncoin (TON) coin from large holders. The investment will be used to develop the TON blockchain and other Telegram-based projects, including clicker games such as Notcoin and Hamster Kombat.