Sample Category Title

Brent Crude Oil Rebounds Amid Monetary Easing and Market Dynamics

Brent crude oil has regained its upward momentum, climbing towards 73.63 USD, following a recent decline triggered by comments from US Federal Reserve Chairman Jerome Powell. In his statement, Powell indicated that the Fed would be cautious about further easing monetary conditions, emphasizing that the rate cut schedule should not be seen as a definitive plan for all future actions by the Monetary Policy Committee (MPC).

Despite these cautious remarks, the Fed's recent decision to lower rates by 50 basis points is fundamentally seen as positive for the commodity market. Lower borrowing costs might stimulate economic demand and enhance interest in energy resources.

Concurrently, the latest data from the US Department of Energy showing a decrease in crude oil inventories by 1.63 million barrels—exceeding expectations of a 0.50 million barrel reduction—also supports bullish sentiments in the oil market. This stock reduction is especially significant as it indicates a robust demand backdrop.

Additionally, the market is closely monitoring potential increases in oil production by OPEC+ countries and the economic data coming from China, the world’s largest oil consumer. Recent weaker-than-expected economic indicators from China have cast some doubts on the sustained strength of oil demand.

The geopolitical situation in the Middle East remains a critical factor, with any escalation potentially impacting energy supply routes and market stability.

Technical analysis of Brent Crude Oil

The market has established a consolidation range around 72.00 USD, with current fluctuations extending to a high of 73.73 USD and a low of 71.78 USD. Having found support at 71.78 USD, there is potential for the market to breach the upper boundary of 73.73 USD today. A successful break above this level could indicate a continuation of the growth trend towards 75.15 USD, possibly reaching up to 75.77 USD. The MACD indicator supports this bullish outlook, with the signal line below zero but pointing upwards, suggesting an imminent upward movement.

Today, Brent surpassed the 73.00 USD mark, continuing its ascent towards the target of 75.15 USD. Upon reaching this target, a retest of the 73.00 USD level from above may occur, potentially setting the stage for another upward wave towards 75.77 USD. The Stochastic oscillator, currently above 80, is poised for a temporary decline, indicating that a corrective phase could follow before further gains.

Ethereum Benefits from Fed Decision

- The crypto market has responded favorably to the Fed rate cut

- Ethereum is in the green but a bearish trend is still in place

- Momentum indicators are turning bullish

Ethereum is experiencing a green session today, recovering from Monday’s correction and preparing to test the recent $2,464 high. The crypto world appears to be benefiting from Wednesday’s aggressive Fed rate cut, contrary to the US stock indices being under pressure. However, the bearish trend that started in late May remains firmly in place and is characterized by a series of lower highs and lower lows.

In the meantime, the momentum indicators are trying to send bullish signals. The RSI is edging higher, but it has not managed yet to move above its midpoint. Interestingly, the stochastic oscillator is moving aggressively higher, towards its overbought area and it is building a sizeable gap from its moving average. Should this move pick up pace, it would be seen as a strong bullish signal.

Should the bulls remain confident, they would try to lead Ethereum above the busy 2,513-2,543 area, which is populated by the 61.8% Fibonacci retracement level of the October 13, 2023 – March 12, 2024 uptrend and the 50-day simple moving average (SMA). Even higher, the 2,667 level might prove a smaller obstacle for the bulls than currently anticipated with their focus then potentially turning to the 50% Fibonacci retracement at 2,816, in an attempt to break the recent sequence of lower highs.

On the other hand, the bears are trying to retake market control and keep ethereum below the 2,513 level. They could then gradually push it lower towards the 8-month low at 2,159. Even lower, the 78.6% Fibonacci retracement at 2,081 could really test the bears’ determination to achieve a new 2024 low.

To conclude, ethereum is benefiting from the stronger Fed rate cut but some key resistance areas have to be broken for the current bearish trend to be reversed.

Dollar Trades Mixed After Fed Rate Cut

The Federal Reserve surprised the market yesterday by cutting the dollar rate by 0.5%, with expectations that a similar reduction might occur by the end of the year. The dollar initially dropped sharply following the announcement but then partially recovered after comments from Jerome Powell. The Fed Chair stated that the current decision would not dictate the pace for further rate cuts and should help maintain stability in the labour market under current conditions.

Major currency pairs reacted strongly to the Fed's decision. The GBP/USD pair hit a new high for the year, dropping to 1.3100, while USD/JPY fell to 140.50 before strengthening by more than 200 pips. The USD/CAD pair managed to rise above 1.3600.

USD/JPY

The USD/JPY pair is under dual pressure. On one side, the US regulator is aggressively cutting rates, while the Bank of Japan plans to raise rates after a long period of ultra-low rates. In such conditions, the pair experiences high volatility, with a daily range of 200 pips.

According to technical analysis, the pair is undergoing a corrective pullback after forming a "hammer" pattern on the daily timeframe. Currently, the rise is constrained by a significant resistance level at 144.00. The price has been testing this level for about two weeks, and if buyers fail to hold above it in the upcoming trading sessions, a return to 141.00-140.00 is possible.

Factors influencing USD/JPY include:

- Today at 09:00 (GMT +3:00), the release of the Philadelphia Fed manufacturing index (US).

- Today at 09:00 (GMT +3:00), the release of initial jobless claims in the US.

- Tomorrow at 05:30 (GMT +3:00), the Bank of Japan’s monetary policy report.

USD/CAD

Yesterday, the USD/CAD pair managed to break above 1.3600 and tested the key level of 1.3650. If buyers can maintain the 1.3600-1.3580 range as support, the corrective rise may continue towards 1.3800-1.3700. If the minimum of 1.3440 from yesterday is revisited, the downtrend may resume with renewed strength.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

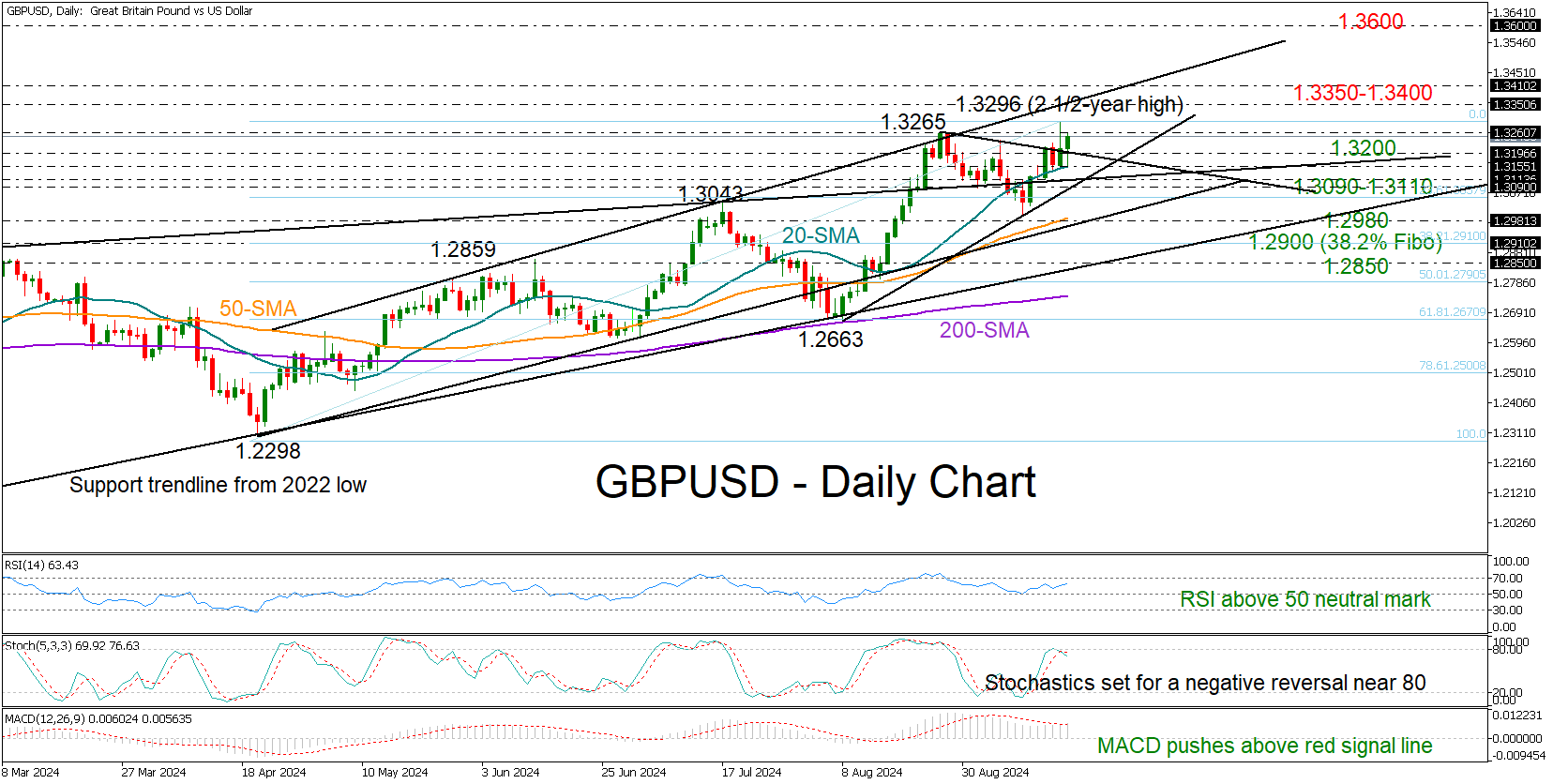

GBPUSD Unlocks New High, But Eyes Remain on 1.3200

- GBPUSD prints new high near 1.3300 after FOMC rate decision

- Technical signals remain bullish but clear close above 1.3200 is needed

- BoE expected to leave rates steady at 11:00 GMT

GBPUSD remains committed to closing above the 1.3200 level for one more day. The Fed delivered a surprise double rate cut of 50bps on Wednesday, lifting the pair to a new 2 ½-year high of 1.3296. Powell expressed confidence in avoiding a downturn but gave no clear indication of the pace of the easing cycle, causing the price to drop below 1.3200 again.

The BoE’s rate decision is the next highlight on the calendar, and the pair is currently flirting with the August bar of 1.3265. With the RSI consistently rising above 50 and the MACD about to cross its red signal line in the positive region, the risk is skewed to the upside. Yet, with the stochastic oscillator preparing for a downturn, room for improvement might be limited.

Above 1.3265, the price could get congested around the resistance line from May currently seen at 1.3350. The 1.3400 psychological mark could also challenge the bulls. If not, the pair could rocket up to 1.3600 last seen in February 2022.

On the downside, there are a couple of support levels to keep in mind. The 20-day SMA at 1.3155 and the trendline zone of 1.3090-1.3110 will be closely watched if the price pulls back below 1.3200. Even lower, the spotlight might shift to the 50-day SMA and the ascending line at 1.2980. Another violation there could take a rest near 1.2900.

Overall, for GBPUSD to sustain its pattern of higher highs and higher lows, it must stay buoyant above 1.3200.

SECO: Swiss economic growth sluggish in 2024, moderate recovery expected in 2025

Switzerland’s State Secretariat for Economic Affairs forecasts the economy to perform "considerably below average" in 2024, with modest growth expected to pick up in 2025. Adjusted for major sporting events, GDP growth is projected to be at 1.2% for 2024, unchanged from June's estimates. However, the outlook for 2025 has been slightly downgraded to 1.6%, compared to June forecast of 1.7%.

Inflation is now expected to decline faster than previously thought, with projections for 2024 revised down to 1.2% (from 1.4% in June) and 0.7% for 2025 (down from 1.1%). This easing of inflationary pressures reflects lower price growth, especially in sectors impacted by the strong appreciation of the Swiss Franc.

SECO acknowledged the challenges posed by sluggish economic activity in Europe, which, alongside the real appreciation of the Swiss Franc, is straining export-sensitive sectors in Switzerland this year. Looking ahead, gradual recovery in Europe is expected to support Swiss exports and boost investments in 2025, helping to stabilize growth across key sectors.

Elliott Wave View on EURJPY Expects Rally to Fail

Short term Elliott Wave view on EURJPY suggests cycle from 8.16.2024 high ended at 155.14 as wave A. Internal subdivision of wave A unfolded as 5 waves impulse. Down from 8.16.2024 high, wave ((i)) ended at 160 and wave ((ii)) rally ended at 162.89. Wave ((iii)) lower ended at 155.446 and rally in wave ((iv)) ended at 157.51. The pair then extended lower in wave ((v)) towards 155.14 which completed wave A.

Wave B rally is currently in progress to correct cycle from 8.15.2024 high. Internal subdivision of wave B is unfolding as a double three Elliott Wave structure. Up from wave A, wave (a) ended at 157.1 and pullback in wave (b) ended at 156.04. The pair then rallied higher in wave (c) towards 158.33 which completed wave ((w)). Pullback in wave ((x)) ended at 157.03 and it has since turned higher again in wave ((y)). Up from wave ((x)), wave (a) ended at 158.03 and pullback in wave (b) ended at 157.10. Wave (c) higher is now in progress towards 160.25 – 162.24 and this should also complete wave ((y)) of B in higher degree. Near term, as far as pivot at 162.91 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

EURJPY 60 Minutes Elliott Wave Chart

EURJPY Elliott Wave Video

https://www.youtube.com/watch?v=5nUdihd7Zjo

Fed Took a First, Bold Step

Markets

We’re finally here. The US Fed took a first, bold step in paring back monetary restrictiveness after keeping rates steady for more than a year. The decision to cut by 50 bps (to 4.75-5%) in the new pursuit to neutral comes amid a shift in the balance of risks in its employment and inflation goals. The statement is now saying that both are roughly in balance (vs. being in the process of). Money markets were divided on the size of yesterday’s cut. For Powell the near-unanimous (Fed governor Bowman dissented) move was a way to demonstrate the central bank’s resolve to protect the labour market and economy from further undue weakness. The dot plot showed another 50 bps of cuts this year, followed by 100 bps more in 2025 and 50 bps in 2026 with a flat rate in the first print for 2027 (2.75-3%). Just as Powell did in the presser we’d downplay the relevance of these individual guesstimates, especially in an easing cycle - which is never as gradual as the dot plot suggests. The chair referred to the dot plot as a baseline scenario from which they can deviate. All it takes is one downside surprise in one of the two payrolls reports due between today and the November 7 meeting and the Fed is ready to jump in. Adding to the argument is their very conservative 4.4% peak forecasted for the unemployment rate which risks being caught up by reality soon. We do retain another upward appreciation of the neutral rate from 2.8% to 2.9%. Powell was explicit in saying that this equilibrium rate was “probably significantly higher” than it was before the pandemic. For most of the presser, Powell sought to spiraling market expectations by not committing to anything, just as anyone would have expected him to do. That sufficed from a daily point of view. US yields reversed kneejerk losses and ended up between 1.4 and 6.1 bps higher in a curve steepener. A similar U-turn kept the US dollar at bay. First resistance in EUR/USD (1.1119) at 1.1202 was never really under threat. We’re curious to the market’s second reading of the Fed today though. In any case we remain cautious on US yields and the dollar and look out for the first major US data releases early October.

The Bank of England is in the spotlights today. We don’t expect the central bank to follow the ECB and Fed with a cut. The one in August was a close call for some and we think the recent string of data, including yesterday’s rising (services) CPI, won’t have those same policymakers voting for another move down again just yet. The November meeting, featuring updated forecast, on the other hand is a live one. This is exactly what is priced in. Sterling’s reaction to the status quo at 5% should therefore stay limited.

News & Views

The Brazilian central bank (BCB) raised its policy rate yesterday by 25 bps, from 10.50% to 10.75%, bucking the global trend and showing what a soft landing might entail. The BCB was frontrunner in the early stages of the pandemic recovery to spot the inflation danger and start an aggressive tightening cycle, bringing the policy rate from 2% to 13.75%. As disinflation started, they gradually lowered the Selic target rate to 10.50%. It remained there since May until yesterday. Domestic indicators on the economic activity and the labour market have been stronger than expected, suggesting a positive output gap. Headline and core inflation measures moved back above the central bank’s inflation target. Inflation expectations remain deanchored and are one of the upside inflation risks together with services inflation. The BCB commits to further rate adjustments, but will let inflation decide on the pace and on the total magnitude. Lack of synchrony in monetary policy cycles across counties, and especially the US, continue to require caution. USD/BRL yesterday tested 5.40, the neckline of a technical head-and-shoulders pattern.

The August Australian labour market report was close to consensus. Employment increased by 47.5k (vs 26k expected) but following a downward revision to July figures (48.9k from 58.2k). Details showed a small decrease in the number of full-time employed people (-3.1k) with half-time jobs accountable for the August increase (+50.6k). The unemployment and labour force participation rates stabilized respectively at 4.2% and 67.1%. Head of the Australian Bureau of Statistics, Kate Lamb, said that the employment and participation measures remain historically high, while unemployment and underemployment measures are still low. This suggests the labour market remains relatively tight. The Aussie dollar profits this morning with AUD/USD testing the 0.68 resistance area as data strengthen the RBA’s current higher-for-longer approach.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) make follow-up moves less evident. We expect the central bank to stick with the quarterly reduction pace. Disappointing US and unconvincing EMU activity data dragged the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed kicked off its easing cycle with a 50 bps move. It is headed towards a neutral stance now that inflation and employment risks are in balance. Conservative SEP unemployment forecasts risk being caught up by reality and with it the dot plot (50 bps more cuts in 2024). We hold our call for two more 50 bps cuts this year. Pressure on the front of the curve and weakening eco data keeps the long end in the defensive for now as well.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. EUR/USD 1.1276 (2023 top) serves as next technical references.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Recent better UK activity data and a cautious assessment of BoE’s Bailey at Jackson Hole are pushing EUR/GBP lower in the 0.84/0.086 range.

Fed Delivers ‘Hawkish’ 50bp Rate Cut

In focus today

Today we will focus on multiple central bank monetary policy meetings.

Norges Bank (NB) will announce its rate decision at 10.00 CET followed by a press conference at 10.30 CET. We believe that NB will keep the policy rates unchanged, and signal that rates will be kept at that level for some time. We expect that the rate path in the monetary policy report will be adjusted downwards, signaling roughly a cut every quarter next year, significantly less than today's market price indicates, so a hawkish signal to markets.

In the UK, Bank of England (BoE) will announce its bank rate decision following the monetary policy meeting at 13.00 CET. We expect BoE to keep the bank rate unchanged at 5.00% in line with consensus and market pricing. In terms of communication, we anticipate BoE to stick to a cautious language and deliver a dovish twist to its communication. We expect a rather muted rection in EUR/GBP with risks tilted to the topside. Read more in Bank of England Preview - Proceeding with caution, 16 September.

We expect the Central Bank of Turkey to keep the policy rate unchanged today, in line with market consensus. The momentum in underlying inflation continued to accelerate in August. However, in our view this does not yet constitute a "significant and persistent deterioration in inflation" that is the CBRT's pre-condition for further policy tightening.

Early Friday, we will have a rate decision and August CPI print out of Japan. We expect no changes from the Bank of Japan following the hawkish turnaround at the late-July meeting. The bond market rally since then and cheaper oil prices have been a boon to JPY, which makes the initial motive for hiking rates less acute. We expect the next hike from the BoJ in December.

Regarding the CPI print, we previously got Tokyo CPI data indicating that price pressures picked up in August. Core inflation remains below 2%, though. The big question remains whether the recent recovery in purchasing power will support a pick-up in spending and push core inflation back above 2%.

Economic and market news

What happened yesterday

In the US, the Federal Reserve (Fed) decided to cut its target rate range by 50bp to 4.75-5.00%. This was a bigger cut than we expected. During this week markets gradually priced in a higher probability of the 50bp rate cut rather than the 25bp that we expected. The updated dot plot signals a total of 50bp of additional cuts for remainder of 2024 (so 25bp at each of the remaining meetings). For 2025, the Fed signals 4x25bp worth of additional cuts and 2x25bp also for 2026. We expect the Fed to ultimately deliver a faster and shorter cutting cycle than the 'dots' suggest. See Research US - Fed review: Going for the soft landing, 18 September.

The initial market reaction was for declining rates and weaker USD. However, the market reaction turned around and 10Y UST yields ended the session up by 6bp, while the 2Y tenor was close to unchanged. EUR/USD initially rallied towards 1.1190 following the 50bp rate cut but returned to around the 1.1120 mark after the press conference. USD strengthened further overnight where we briefly saw EUR/USD hit 1.070, but it is now back just below the 1.112 mark where it all started prior to the announcement.

In the euro area, the final HICP print confirmed the flash release at 2.2% y/y and core inflation at 2.8% y/y. Domestic inflation in the euro area measured by the ECB's 'LIMI' indicator declined to 4.22% y/y in August from 4.26% in July. With the August data we thus still see this very sticky domestic inflation with strong momentum.

In the UK, August CPIs were fully in line with consensus expectations; headline at 2.2% (prior: 2.2%), core at 3.6% (prior: 3.3%) and services at 5.6% (prior: 5.2%). Monthly pressures slightly higher in the core and service measure with upward contributions stemming from transport (air fares) and recreation and culture, explaining the slight move lower in EUR/GBP on the release. The print does not change our view of an unchanged decision from BoE later today.

Equities: Global equities were lower yesterday, but the movements were minor considering the stakes at the Federal Reserve meeting. Add to the puzzle the positive trends in Asia this morning and the markedly higher futures in Europe and the US. For those not following intraday movements, it is important to note that the initial equity market reaction to the policy statement was quite positive. It was not until after Powell's press conference that we observed a decline in equities. Without delving deeper into the details, the Fed managed to implement what we previously termed a semi-hawkish 50 basis point cut, without emphasizing the weakness in the labour markets too heavily. Although there was some divergence within sectors, it was minimal, and most notably, there was a slight outperformance in small caps. In the US yesterday, the indices closed as follows: Dow -0.3%, S&P 500 -0.3%, Nasdaq -0.3%, and Russell 2000 +0.04%. This morning, Asian markets are experiencing gains, led by a strong performance in Japan and a weakening yen. Futures in Europe and the US are also trending higher.

FI: Yesterday's 50bp rate cut 'surprise' from the Fed did not trigger significant volatility, as the central bank kept its guidance of a gradual return to normal. The initial market reaction to the rate cut announcement was a bullish steepening of the UST curve, but the move faded through the press conference as Powell struck a relatively upbeat tone on the economic outlook.

FX: The 50bp Fed cut initially led to a softer USD across the board, but most of the reactions reversed during Powell's press conference. GBP, NOK, CHF gained most against the USD in the G10 space, while EUR/USD remains more or less unchanged, just above the 1.11 mark. In the Scandies today's most important event is the Norges Bank meeting.

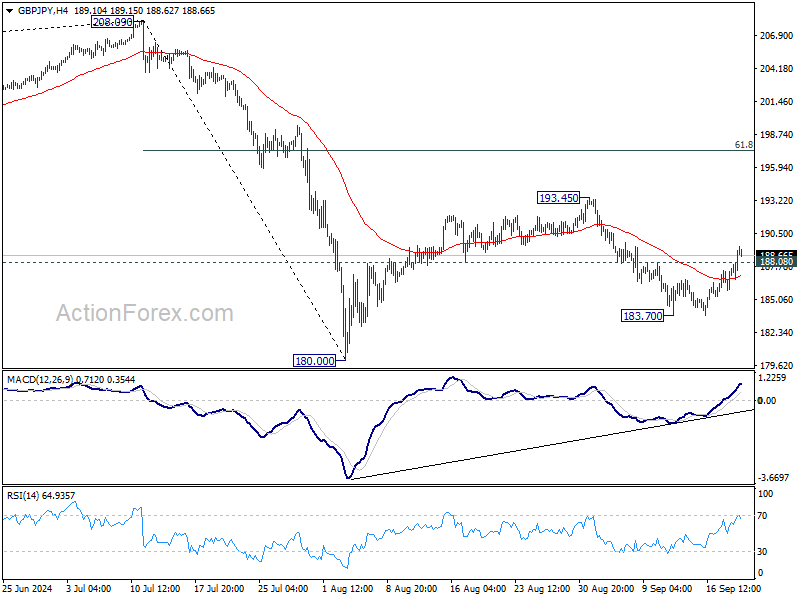

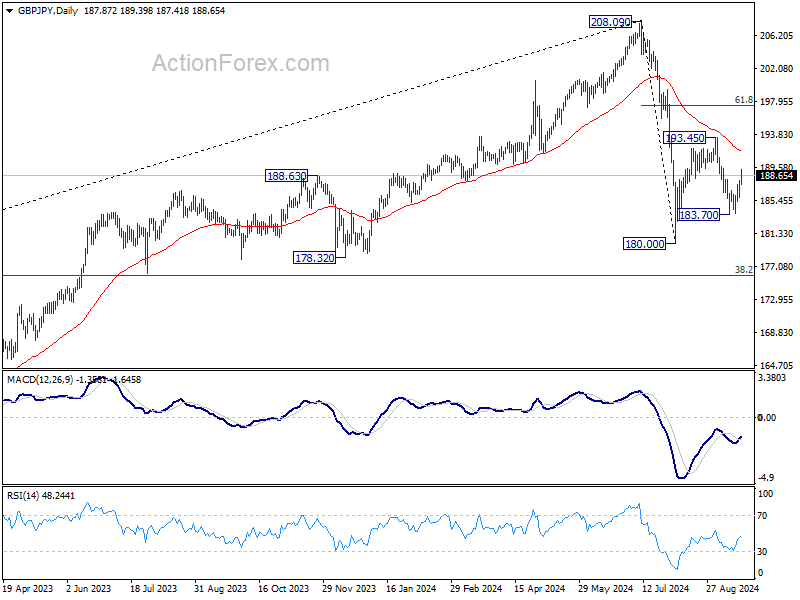

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.51; (P) 187.28; (R1) 188.74; More...

GBP/JPY's break of 188.08 minor resistance suggest that fall from 193.45 has completed at 183.70 already. Rise from there is seen as the third leg of the corrective pattern from 180.00. Intraday bias is back on the upside for 193.45 and possibly further to 61.8% retracement of 208.09 to 180.00 at 197.35.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

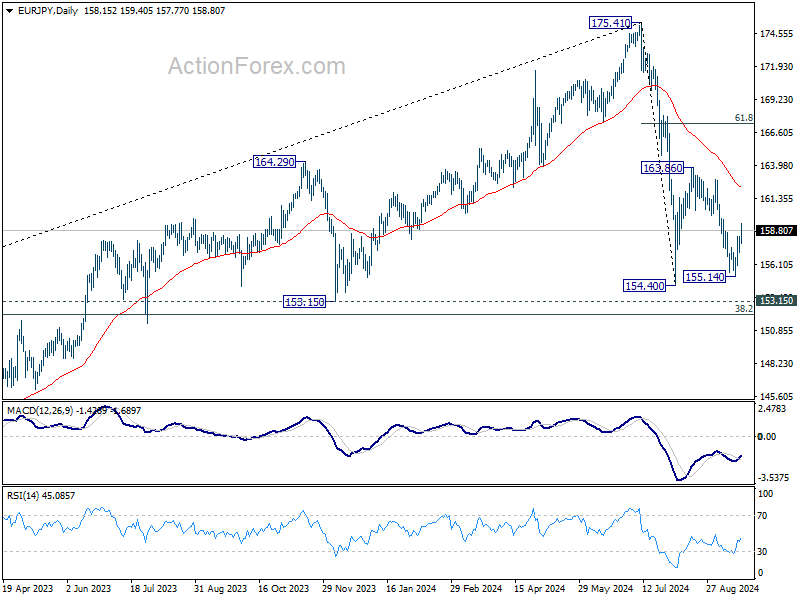

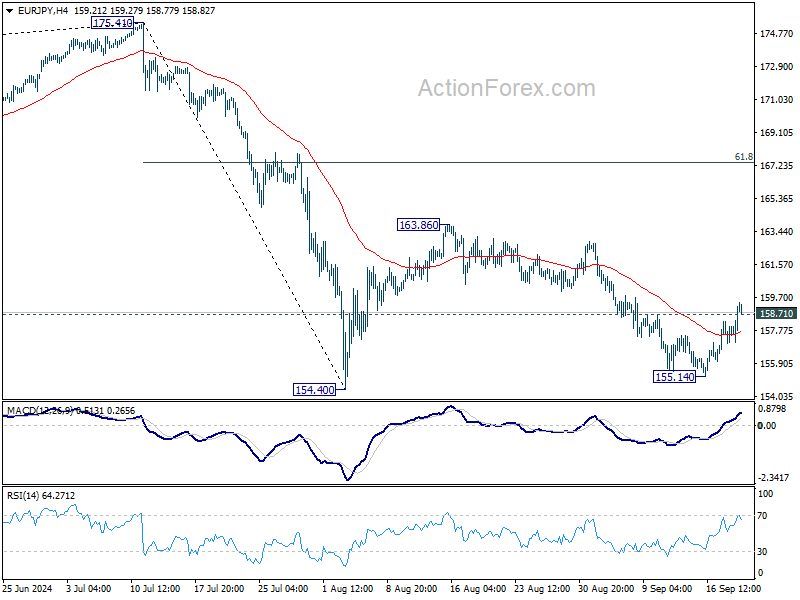

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.36; (P) 157.87; (R1) 158.69; More....

EUR/JPY's break of 158.71 minor resistance suggests that fall form 163.89 has completed at 155.14 already. Rebound from there is seen as the third leg of the corrective pattern from 154.40. Intraday bias is back on the upside for 163.89, and possibly further to 61.8% retracement of 175.41 to 154.40 at 167.38.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.