Sample Category Title

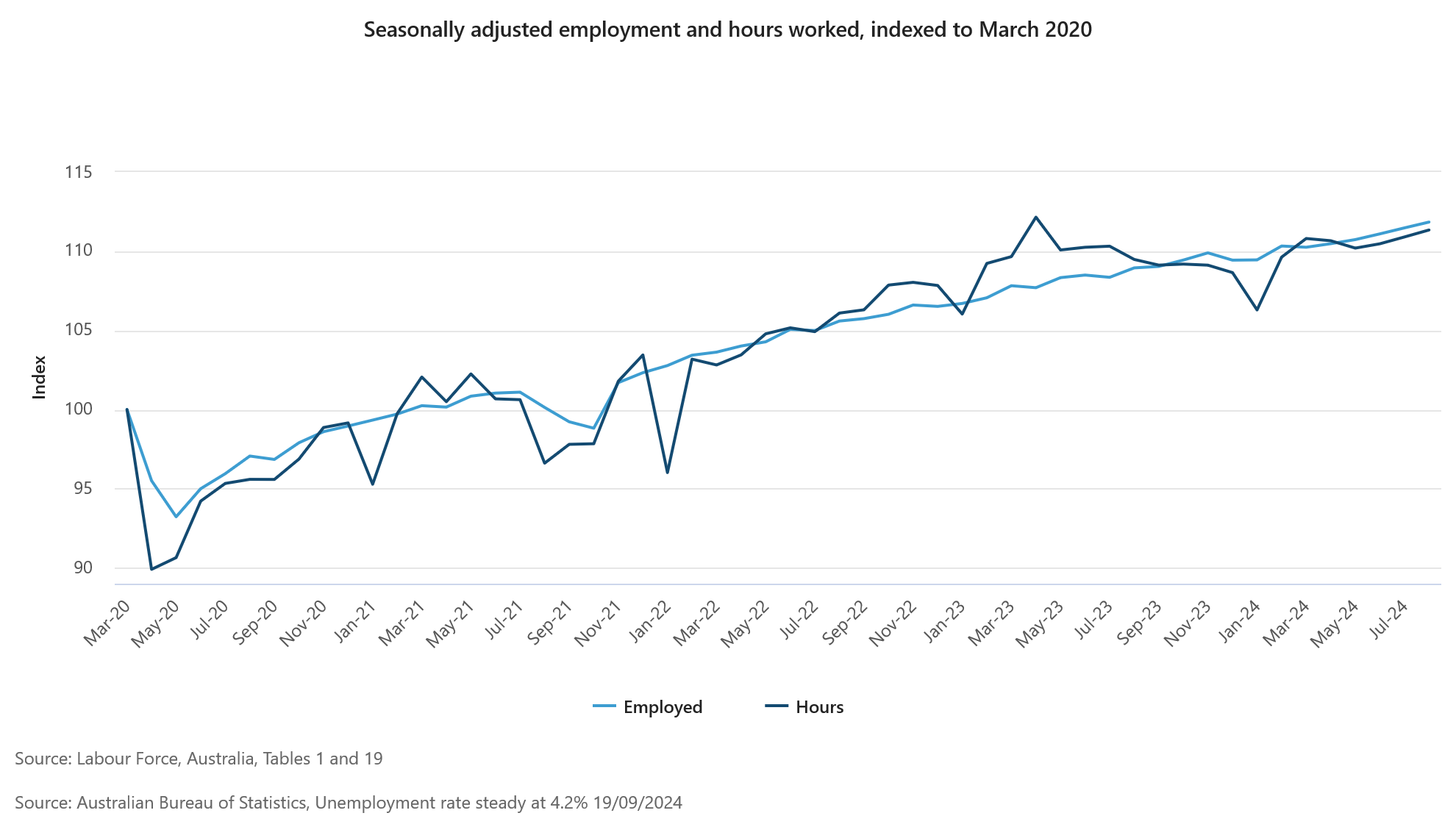

Australia’s employment grows 47.5k in Aug, labor market remains tight

Australia's employment grew by a robust 47.5k in August, significantly exceeding expectations of 25.3k. While full-time employment declined slightly by -3.1k, part-time jobs saw a sharp increase of 50.6k, boosting the overall figure. The employment-to-population ratio edged up by 0.1% to 64.3%, just shy of the record high of 64.4% set in November 2023.

Unemployment rate held steady at 4.2%, as anticipated, with the number of unemployed individuals falling by -10.5k, a -1.6% mom decline. Participation in the labor force remained strong, with the participation rate unchanged at 67.1%. Additionally, monthly hours worked rose by 0.4% mom, reflecting continued labor demand.

Kate Lamb, head of labor statistics at ABS, commented: "The employment and participation measures remain historically high, while unemployment and underemployment measures are still low, especially compared with what we saw before the pandemic. This suggests the labor market remains relatively tight."

New Zealand GDP contracts – 0.2% qoq in Q2, manufacturing offers some resilience

New Zealand’s GDP contracted by -0.2% qoq in Q2, slightly better than the expected -0.4% qoq decline. Despite the overall negative figure, 7 out of 16 industries posted increases, with manufacturing leading the growth.

GDP per capita also saw a decline, falling by -0.5%, marking the fourth consecutive quarter of contraction in this metric. The last time GDP per capita increased was back in Q3 2022.

On the expenditure side, GDP was flat for the quarter, showing no growth or contraction at 0.0%. Household spending, however, provided a small positive with a 0.4% increase. Real gross national disposable income was also flat at 0.0%, reflecting limited income growth in the face of economic headwinds.

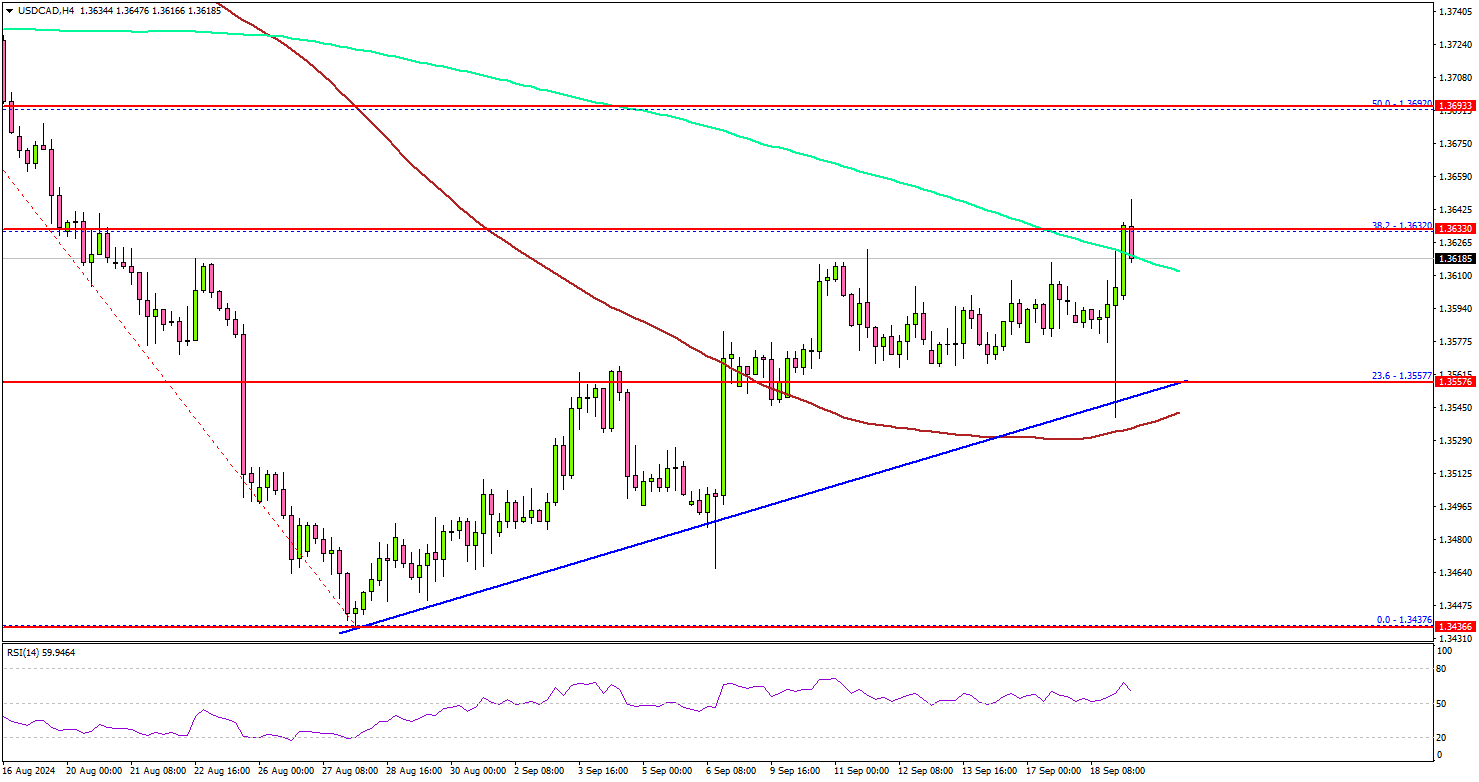

USD/CAD Eyes Additional Gains, Fed Slashes Rates By 0.5%

Key Highlights

- USD/CAD started a decent increase above the 1.3500 resistance.

- A key bullish trend line is forming with support at 1.3550 on the 4-hour chart.

- GBP/USD remained in a bullish zone above the 1.3150 level.

- The Fed reduced interest rates from 5.50% to 5.00%.

USD/CAD Technical Analysis

The US Dollar found support near the 1.3440 zone against the Canadian Dollar. USD/USD started a decent increase above the 1.3500 resistance zone.

Looking at the 4-hour chart, the pair climbed above the 23.6% Fib retracement level of the downward move from the 1.3946 swing high to the 1.3437 low. The pair even cleared the 100 simple moving average (red, 4-hour), but it stayed below the 200 simple moving average (green, 4-hour).

It seems like the pair is now facing hurdles near 1.3620, the 200 simple moving average (green, 4-hour), and the 38.2% Fib retracement level of the downward move from the 1.3946 swing high to the 1.3437 low.

A clear move above the 1.3620 zone might set the pace for a move toward 1.3700. Any more gains might call for a test of the 1.3750 zone.

On the downside, immediate support sits near the 1.3550 level. There is also a key bullish trend line forming with support at 1.3550 on the same chart, below which the pair might test the 100 simple moving average (red, 4-hour).

The next key support sits near the 1.3500 level, below which the pair could dive toward the 1.3440 support zone or the last swing low.

Looking at GBP/USD, the pair remained stable above 1.3150, spiked higher after the UK CPI release, and might aim for more upsides in the near term.

Upcoming Economic Events:

- US Existing Home Sales for August 2024 (MoM) - Forecast -0.1%, versus +1.3% previous.

- US Initial Jobless Claims - Forecast 230K, versus 230K previous.

Stocks end in red as Fed’s 50bps cut seen as catch-up, not new pace

Despite initial rally, major US stock indexes closed lower after Fed officially began its policy easing cycle with a 50bps rate cut, bringing the target range to 4.75-5.00%. While some may attribute the late selloff to the classic “buy the rumor, sell the fact” dynamic, Fed Chair Jerome Powell’s press conference and the new economic projections pointed to a more cautious pace ahead. These suggested that Fed's bold move was more about catching up from July's inaction rather than setting an aggressive pace for future cuts.

Powell acknowledged that Fed "might well have" started lowering rates back in July if the employment data had been available earlier. He emphasized that the 50bps cut was “a sign of our commitment not to get behind” the curve in normalizing rates, calling it “a strong move.” Additionally, he was quick to clarify that this cut is not indicative of a "new pace," stating, “The economy can develop in a way that would cause us to go faster or slower.”

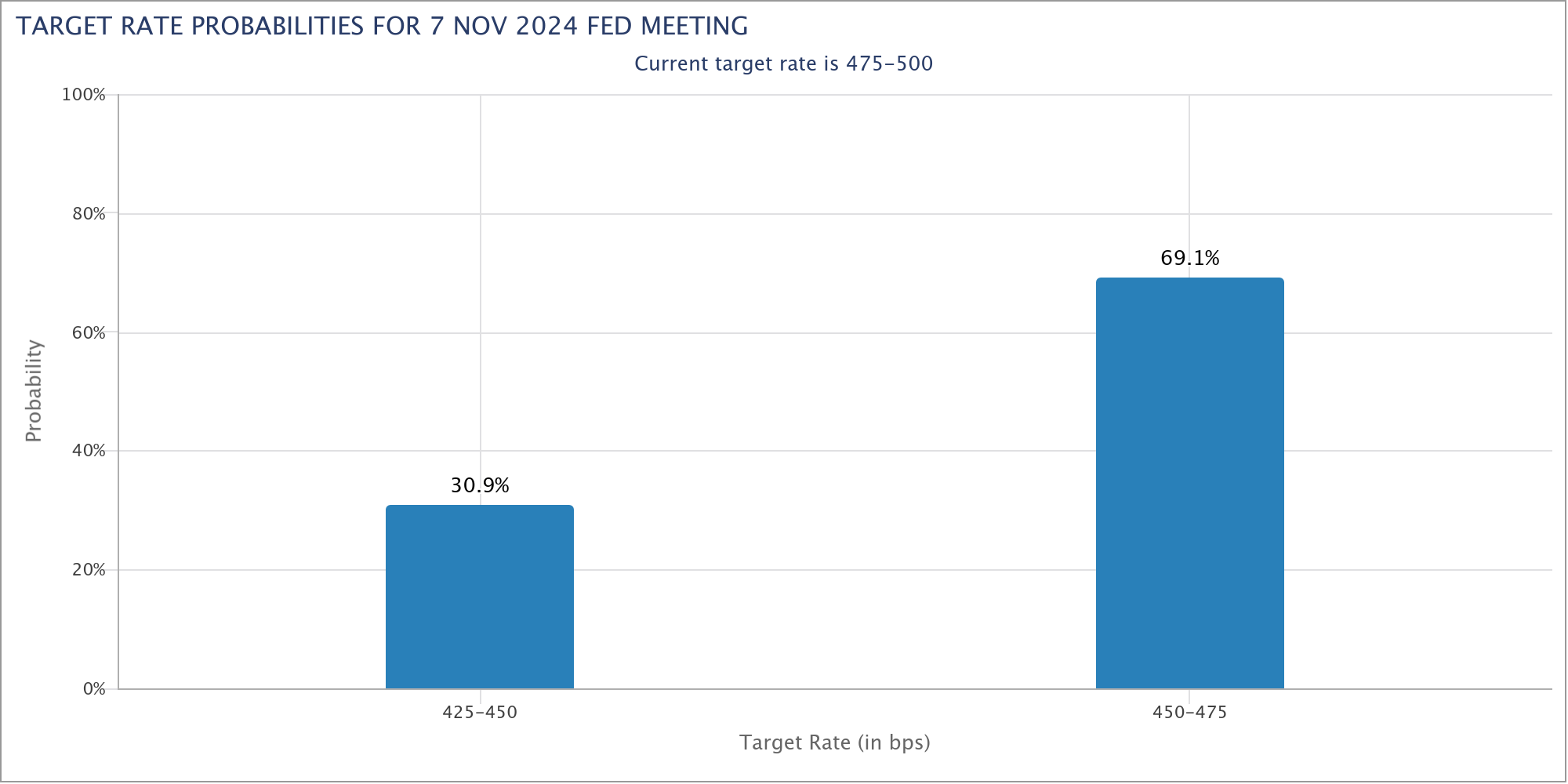

The updated dot plot also revealed a divided Fed. Of the 19 participants, 10 penciled in another 50bps cut by year-end, bringing rates down to 4.25-4.50%, while 9 saw only a 25bps cut to 4.50-4.75%. This suggests Fed would revert to smaller cuts in the coming months, with November likely seeing a 25bps reduction, followed by another 25bps cut in December, or even a few cuts if inflation risks persist.

This sentiment is reflected in market pricing, with fed funds futures currently indicating around 70% chance of a 25bps cut in November and 30% chance of a larger 50bps move.

Technically, while S&P 500 struggled to sustain above 5669.67 key resistance, and some retreat might be seen in the near term, outlook will stay bullish as long as 5402.62 support holds. Sustained trading above 5669.67 will extend the long term up trend to 61.8% projection of 4103.78 to 5669.67 from 5119.26 at 6086.98 later in the year.

NZ First Impressions: GDP, June Quarter 2024

New Zealand’s GDP fell by 0.2% in the June quarter. The result wasn’t as weak as expected, and will ease concerns that the economy might have been taking a turn for the worse.

Key results

- Quarterly change: -0.2% (last: +0.1%, Westpac f/c: -0.4%, market f/c: -0.4%, RBNZ -0.5%)

- Annual change: -0.5% (Last +0.3%, Westpac f/c -0.6%, RBNZ -0.7%)

The New Zealand economy shrank by 0.2% in the June quarter. Estimated growth in the March quarter was trimmed back to a 0.1% rise (previously estimated to be up 0.2%), and there were modest revisions to earlier quarters that largely balanced out.

The 0.2% fall in production GDP was smaller than the 0.4% fall that we and the market were forecasting. Reinforcing that surprise, the less-followed expenditure measure of GDP was unchanged, and the income measure actually rose by 0.2% in real terms.

As we signalled in our preview, the performance across industries was a mixed bag. Retailing, wholesaling and forestry saw the most significant declines. On the positive side, manufacturing saw a strong 1.9% rise, and personal services such as healthcare and recreation held up better than we expected.

As Stats NZ had noted, changes in the timing of tobacco imports have disrupted the pattern of quarterly GDP to some degree, boosting growth in the March quarter and acting as a drag on growth this time.

On the expenditure measure of GDP, there were gains in household spending, government spending and business investment. Goods exports were the main drag on growth, falling back by 4.4% after a strong rise in the March quarter.

Implications

While still soft, these results come as something of a relief. Higher-frequency activity data had taken a marked turn lower in May and especially June, raising concerns that the New Zealand economy’s drawn-out slowdown could be entering a new, much tougher phase. However, not only has the monthly data improved somewhat in July and August, but in GDP terms the June quarter itself turned out to be no worse than what we’ve seen over the last couple of years.

We continue to expect the RBNZ to cut the OCR by 25bps each at the October and November reviews. While financial markets will no doubt fixate on the idea that the US Fed’s decision this morning has opened the door for 50bp rate cuts elsewhere, there isn’t much in the local data that argues for the RBNZ to step up the pace of easing beyond what it had already signalled in its August policy statement.

FOMC’s Normalisation Cycle Begins

50bps delivered and another 50bps seen by year end by the FOMC.

At the September meeting, the FOMC decided to cut by 50bps to begin their policy normalisation cycle. The Committee projects another 50bps of cuts to end-2024 (over two meetings), another 100bps of cuts in 2025, then a final 50bps in 2026, leaving the fed funds rate at 2.9%, which is also the Committee’s upwardly revised ‘longer run’ estimate of neutral.

The Committee’s statement and Chair Powell’s remarks in the press conference were worded carefully to highlight that the 50bp cut was not a signal of concern in the outlook, but rather a response to inflation slowing near target and the risks to achieving its employment and inflation goals now being “roughly in balance”.

The revised forecasts provided by FOMC members also speak to confidence in the economy. GDP growth is forecast to be 2.0%yr in 2024-2027, above their ‘longer run’ estimate of trend growth of 1.8%. The unemployment rate is consequently forecast to peak at 4.4% in 2024 then drift down to 4.2% through 2026 and 2027, where the unemployment rate is today. This implies little-to-no further deterioration in employment growth over the forecast period, in contrast to the marked deceleration in payrolls employment growth seen over the past two years – from 320k per month over the year to March 2023 to a 174k average over the 12 months to March 2024 (incorporating the BLS’ initial annual revision guidance) and now 116k in the three months to August. The inflation projections also point to an economy in robust shape over the outlook, with both headline and core inflation to trough at 2.0%yr not below.

It is worth emphasising however, while the ranges for the activity and price forecasts are narrow, the Committee’s views on the fed funds rate at end-2025, 2026 and 2027 are broad. Whereas the vast majority of the Committee see the fed funds rate only 25bps to 50bps below the current level by end-2024, the December projections for 2025 through 2027 are spread across a 150bp range. In 2027, the FOMC’s full range of estimates for the fed funds rate therefore stretches from 50bps below the their neutral estimate to 100bps above. To us, this speaks to considerable uncertainty over how the balance of risks will evolve and, as per Chair Powell’s remarks, a commitment to take “timely” action and “not to get behind” with policy. The FOMC regard the stance of policy as still materially above neutral and expect to return near it in time. How quickly they do so will be determined by incoming data and the perceived balance of risks.

To us, there is reason to be wary over a further deterioration in conditions and associated risks. We expect lower GDP growth in 2025 and 2026 of 1.8%yr and 1.7%yr versus the FOMC’s 2.0%yr. Westpac also expects a greater degree of weakness in the labour market, with the unemployment rate to rise to 4.7% in 2025 and hold there. Still, we also see inflation modestly above the FOMC’s 2.0%yr expectation in 2025 and 2026 as a result of supply-side pressures which are not easily resolved but, for the sake of inflation expectations, must be managed by the Committee. The 3.375% we have forecast for late-2025 speaks to these diverging risks and their persistence. The flow of data in coming months will be critical to assessing these uncertainties and their implications for the policy outlook.

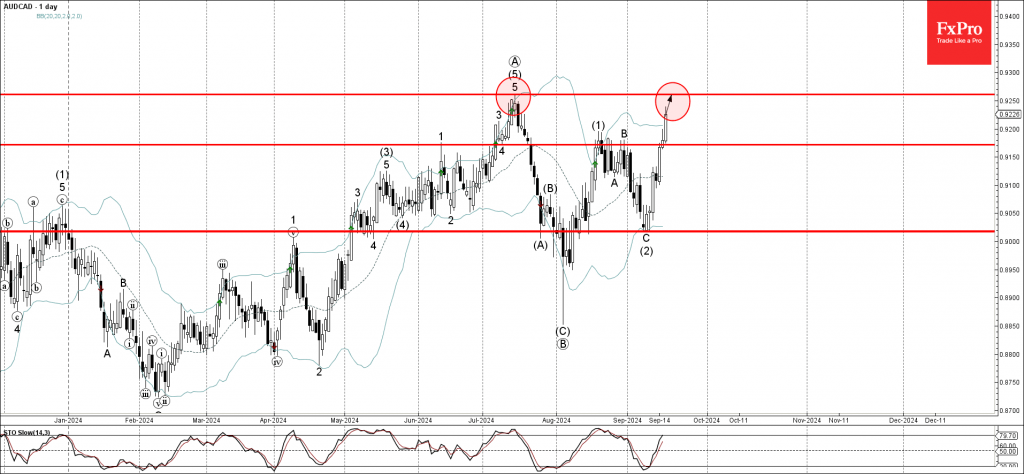

AUDCAD Wave Analysis

- AUDCAD broke pivotal resistance level 0.9170

- Likely to rise to resistance level 0.9260

AUDCAD currency pair recently broke above the pivotal resistance level 0.9170 (which stopped the previous waves (1) and B last month).

The breakout of the resistance level 0.9170 accelerated the active intermediate impulse wave (3).

Given the clear daily uptrend, AUDCAD currency pair can be expected to rise further to the next resistance level 0.9260 (former multi month high from July).

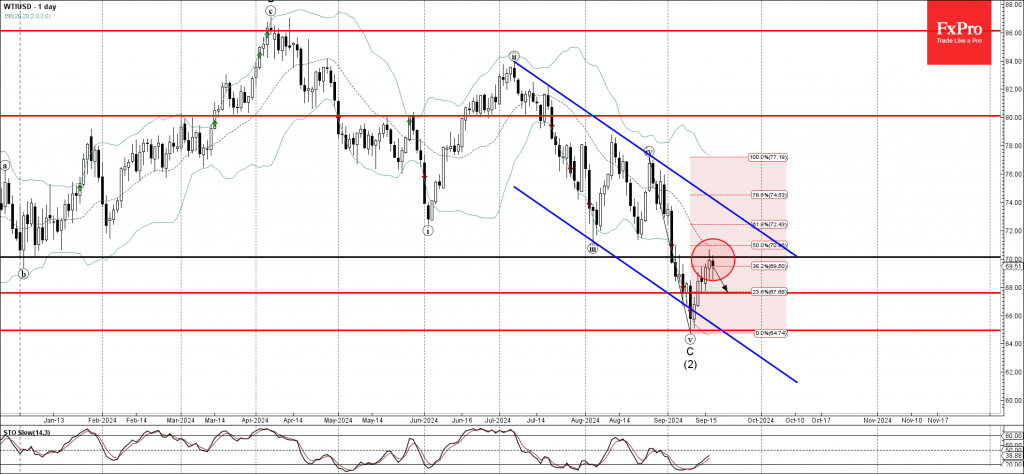

WTI Wave Analysis

- WTI reversed from round resistance level 70.00

- Likely to fall to support level 68.00

WTI crude oil recently reversed down from the round resistance level 70.00 (former strong support from January).

The resistance level 70.00 was strengthened by the nearby 20-day moving average and by the 50% Fibonacci correction of the sharp downward impulse from last month.

Given the clear daily downtrend, WTI crude oil can be expected to fall further to the next support level 68.00.

Fed Review: Going for the Soft Landing

- The Federal Reserve cut rates by 50bp in the September meeting, against our call for only a 25bp cut. The new policy rate target is 4.75-5.00%.

- The updated dots signal a total of 50bp of additional cuts in 2024, 4x25bp of cuts in 2025 and 2x25bp cuts in 2026. Relative to our call, the Fed signals a longer but more gradual rate cutting cycle.

- Powell downplayed recession risks despite the larger-than-expected cut, and most of the decline UST yields and weakening in USD FX reversed over the course of the press conference.

Markets were historically divided between 25bp and 50bp cuts going into the FOMC's September decision. Powell accompanied the larger rate reduction with an overall positive assessment of the economy, ending the press conference saying: 'I don't see anything in the economy right now that suggests likelihood of a downturn is elevated.'

The larger move was motivated by a significant shift in the Fed's risk assessment. 12 out of 18 participants saw risks to unemployment rate tilted to the upside (prev. 4 participants), and the median unemployment rate forecast was revised up through 2024-2026. While GDP forecasts were left mostly unchanged, 7 participants saw risks tilted to the downside also for growth (prev. 3). Inflation is seen stabilizing to 2% faster than previously expected with a balanced risk outlook.

Powell also mentioned that 'it feels to me that neutral rate is probably significantly higher than it was pre-pandemic'. The median long-term 'dot' shifted to 2.9% (from 2.8%) with 7 participants now seeing the long-term rate at or above 3.25% (prev. 4). So, while the risk assessment and distribution of individual dots suggest that the Fed is open for faster rate cuts in the near-term if needed, rates could stabilize at a higher level longer-term.

Ahead of the meeting, some commentators voiced concerns over a larger cut potentially sparking rising recession fears in the markets. While most of the initial market reaction has already faded, Powell successfully maintained financial conditions on an easing trend. Yield curve steepened with 10y UST yield ending the session above its pre-announcement level. This reflects markets downplaying the probability of a recession, as faster rate cuts and consequently easing financial conditions are set to provide support for growth in 2025.

We expect the Fed to ultimately deliver a faster and shorter cutting cycle than the 'dots' suggest. We forecast 25bp cuts in every meeting until June and see the policy rate reaching 3.00-3.25% by end-2025. This is lower than the level implied by the dots (3.25-3.50%).

Markets are now pricing in a cumulative 70bp of additional cuts for the two remaining meetings of 2024, split roughly evenly between November and December. If labour market data continues weakening, we would expect markets to test the Fed's call for only 25bp cuts in the remaining meetings. While we maintain our call unchanged, the bar for another 50bp move in November is now inarguably lower than before. Finally, the Fed maintained the pace of QT unchanged and Powell made it clear that the decisions regarding QT remain separate from rate decisions. We expect QT to run well into 2025.

FOMC Starts Easing Cycle With a Bang

Summary

- The FOMC surprised some market participants today by reducing the target range for the federal funds rate by 50 bps. Concerns about the state of the labor market appear to have been the primary driver of the 50 bps move.

- But the FOMC signaled that it may not necessarily follow today's 50 bps rate cut with additional large reductions in upcoming meetings. The median dot in the so-called "dot plot" implies two 25 bps cuts if further easing is spread evenly over the two remaining meetings this year.

- Only one voter (Governor Michelle Bowman) dissented at today's policy meeting, preferring a 25 bps rate cut instead, but the dot plot indicates that a meaningful share of the Committee appears to be in no hurry to reduce the fed funds rate at a rapid clip.

- The FOMC may indeed slow the pace of rate cuts in coming meetings. But we remain of the view that monetary policy will be back near neutral in one year's time. That is, we look for the federal funds rate to be roughly 3.00%-3.25% or so by this time next year. We will formally update our meeting-by-meeting fed funds forecast in the coming days.

FOMC Front Loads Easing Cycle

Heading into today's FOMC meeting, there was more uncertainty among market participants about the outcome than there has been in some time. A rate cut, which would be the first since March 2020, was universally expected. But would the Committee reduce the target range for the federal funds rate by 25 bps or 50 bps? In the event, the FOMC decided to cut rates by 50 bps. The vote was 11-1 in favor, with the lone dissent coming from Governor Michelle Bowman. Just one dissent is not uncommon, but it is more uncommon for a member of the Board of Governors to vote against the policy decision. Today marks the first governor to dissent since 2005, and the first governor to dissent in favor of tighter policy since 1994.

The post-meeting statement highlighted the cooling in the labor market, saying that job gains had "slowed." In that regard, the economy created 267K jobs per month in the first quarter of the year, but that pace has nearly halved over the past three months (Figure 1). The statement also seemed to hint that concerns about the labor market had been the primary driver of the 50 bps move with the line "in light of the progress on inflation and the balance of risks [emphasis ours], the Committee decided to lower the target range for the federal funds rate by 1/2 percentage point." The idea that the risks are skewed to the downside for the labor market was further reinforced by the addition of a line signaling that the Committee is "strongly committed" to supporting maximum employment in addition to the existing line about returning inflation to 2%.

Summary of Economic Projections Highlights More Balanced Risks

The update to the Summary of Economic Projections (SEP) suggests today's 50 bps cut was an effort to front-load the removal of policy restriction, and that additional 50 bps cuts may not occur at upcoming meetings without a meaningful deterioration in the economy. The median participant projection for the fed funds rate at year-end slipped to 4.375%, implying two 25 bps cuts if further easing is spread evenly over the two remaining meetings this year (Nov. 7 and Dec. 18). However, seven Committee members projected rates to fall only 25 bps further this year, while two projected no change (Figure 2). In other words, only one voter may have dissented in September, but a meaningful share of the Committee is still in no hurry to reduce the fed funds rate.

The disconnect between today's action and the outlook for additional easing in the near term may stem from uncertainty about where the neutral policy setting is. The median estimate of the longer run fed funds rate rose a tick to 2.9% in September, but the range remains wide at 2.4%-3.8%. Yet by that measure, even the more hawkish members of the Committee seem to agree that the prior policy rate of 5.25%-5.50% was very restrictive, allowing space to reduce the target range without inadvertently venturing into "accommodative" territory.

Participants expect further easing in 2025, although at potentially a slower pace. The median dot for 2025 shifted down to 3.375%, implying 100 bps further easing next year.

The more balanced risks between the inflation and employment side of the Fed's mandate were evident in the economic portion of projections. The median estimate for the unemployment rate at year-end rose to 4.4% from 4.0% in June, slightly higher than most participants' longer-run estimates, and is expected to stay at 4.4% in 2025 (Figure 3). Meantime, Committee members seemed more constructive on the inflation outlook. The median estimate for headline inflation in Q4-2024 fell from 2.6% to 2.3%. The FOMC also projects core inflation to descend a touch faster than it did in the last SEP; the median estimate slipped to 2.6% for 2024 and 2.2% for 2025 compared to 2.8% and 2.3% previously. Notably, 16 of 19 participants now see the risks to core inflation as broadly balanced, compared to only seven at the June meeting (Figure 4). At the same time, the majority of the Committee (12 participants) believe the risks to the unemployment rate lie to the upside versus only four when the Committee met in June.

Coming into today's meeting, we expected a 25 bps rate cut today followed by a pair of 50 bps rate reductions at each of the November and December meetings for a cumulative 125 bps decline in the federal funds rate by year-end. With today's decision by the FOMC, a 50 bps move came a bit faster than we were anticipating, but our overarching view that the FOMC will ease materially in the coming months has not changed. It will be a close call whether we get another 50 bps move by year-end or if the Committee slows down to a more-measured 25 bps pace. The employment reports that are slated for release in the next three months will be critical inputs into the FOMC's decisions at the November and December meetings. We will formally update our meeting-by-meeting fed funds forecast in the coming days, but we remain of the view that monetary policy will be back near neutral in one year's time. That is, we look for the federal funds rate to be roughly 3.00%-3.25% or so by this time next year.