Sample Category Title

Loonie Slips on Soft Inflation, Broader Market Stays Quiet as Traders Await Fed

Canadian Dollar is broadly lower in early US trading following weaker-than-expected inflation data. With CPI decelerating further than anticipated, this set of data provides BoC some breathing room to ease monetary policy more aggressively if necessary. The spotlight now shifts to the upcoming September employment report, which will be crucial in determining whether BoC sticks to its current pace of a 25bps rate cut at its October 24 meeting, or more.

Meanwhile, Dollar is edging slightly higher after stronger-than-expected ex-auto sales data. Euro remains mixed despite poor German economic sentiment figures. Overall, market movements are relatively muted as traders appear to be holding their major bets ahead of tomorrow's FOMC rate decision. While Fed is widely expected to begin its policy loosening cycle, the uncertainty remains around whether the rate cut will be 25bps or a larger 50bps reduction.

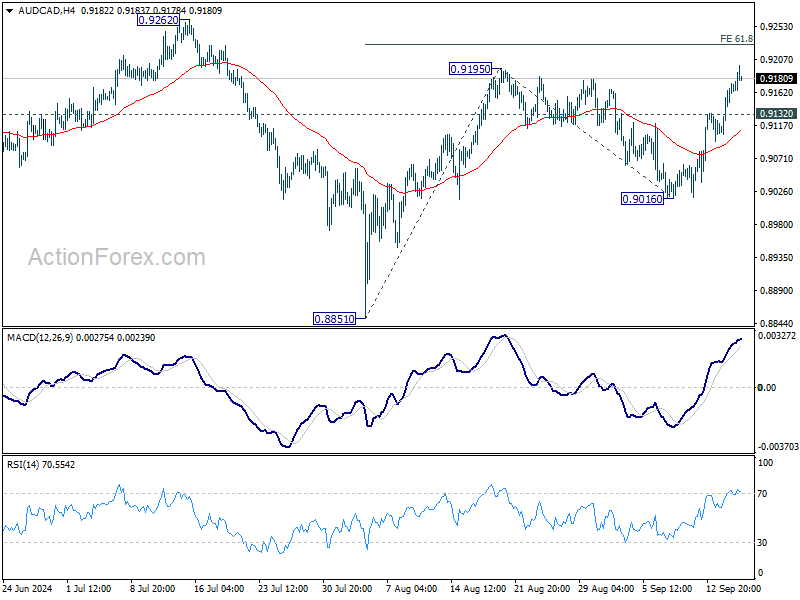

Technically, AUD/CAD's breach of 0.9195 resistance suggest that rise from 0.8851 is resuming. Further rally is expected as long as 0.9132 support holds, towards 61.8% projection of 0.8851 to 0.9195 from 0.9016 at 0.9226. However, strong resistance might emerge at 0.9262 to limit upside, at least on first attempt.

In Europe at the time of writing, FTSE is up 0.60%. DAX is up 0.86%. CAC is up 0.95%. UK 10-year yield is up 0.0146 at 3.778. Germany 10-year yield is up 0.0099 at 2.134. Earlier in Asia,Nikkei fell -1.03%. Hong Kong HSI rose 1.37% China Shanghai SSE fell -0.48%. Singapore Strait Times rose 0.64%. Japan 10-year JGB yield fell -0.0158 to 0.830.

US retail sales rises 0.1% mom in Aug, ex-auto sales up 0.1% mom

US retail sales rose 0.1% mom to USD 710.7B in August, above expectation of -0.1% mom. Ex-auto sales rose 0.1% mom to USD 576.4B, below expectation of 0.2% mom. Ex-gasoline sales rose 0.1% mom to USD 658.8B. Ex-auto, gasoline sales rose 0.2% mom to USD 524.5B.

Total sales for the June through August period were up 2.3% from the same period a year ago.

Canada's CPI slows to 2% in Aug, lowest since Feb 2021

Canada's CPI growth slowed to 2.0% yoy in August, down from 2.5% yoy in July, and below market expectations of 2.1%—marking the slowest pace since February 2021. This deceleration is largely attributed to decline in gasoline prices, driven by a combination of lower fuel prices and a base-year effect. Excluding gasoline, CPI still eased to 2.2% yoy from 2.5% yoy, indicating broad softening in inflation.

On a month-to-month basis, CPI fell by -0.2% mom, significantly below the expected 0.2% mom increase, and following a 0.4% mom rise in July. The lower-than-anticipated figures could strengthen the case for BoC to ease monetary policy more aggressively if economic data continues to signal softness.

Core inflation measures also showed signs of cooling. CPI median dipped to 2.3% yoy, slightly higher than expectations of 2.2% yoy, but CPI trimmed dropped to 2.4% yoy from 2.7%yoy, missing forecasts. CPI common index fell from 2.2% yoy to 2.0% yoy, also below expectations of 2.2% yoy.

The overall decline in inflation, especially in the core metrics, offers BoC more room to consider faster rate cuts should economic activity continue to falter. Given Governor Tiff Macklem's recent dovish remarks, these latest inflation figures could push the central bank toward more decisive easing in the near term.

German ZEW plummets to 3.6 as optimism evaporates, Eurozone follows

Germany's ZEW Economic Sentiment dropped sharply in September, falling from 19.2 to 3.6, significantly missing expectations of 18.6. Current Situation Index also saw a stark decline from -77.3 to -84.5, its lowest level since May 2020.

In the broader Eurozone, ZEW Economic Sentiment fell to 9.3, down from 17.9, while Current Situation Index dropped -8 points to -40.4. The data suggests that confidence across the region is waning, though Germany's drop was notably more severe.

ZEW President Achim Wambach highlighted that "the hope for a swift improvement in the economic situation is visibly fading," adding that the balance between optimists and pessimists is now evenly split.

The sharp fall in expectations for Germany signals that economic pessimism is growing faster than elsewhere in the Eurozone. Wambach also noted that most respondents seem to have already accounted for ECB's recent interest rate decision in their expectations.

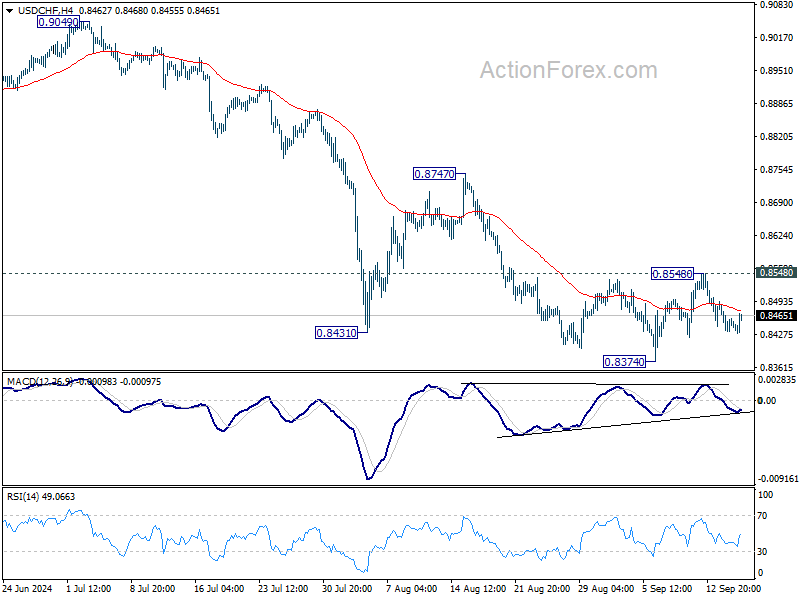

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8426; (P) 0.8457; (R1) 0.8479; More…

USD/CHF is still bounded in range trading and intraday bias remains neutral for the moment. With 0.8548 resistance intact, further decline is still expected. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8548 resistance will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

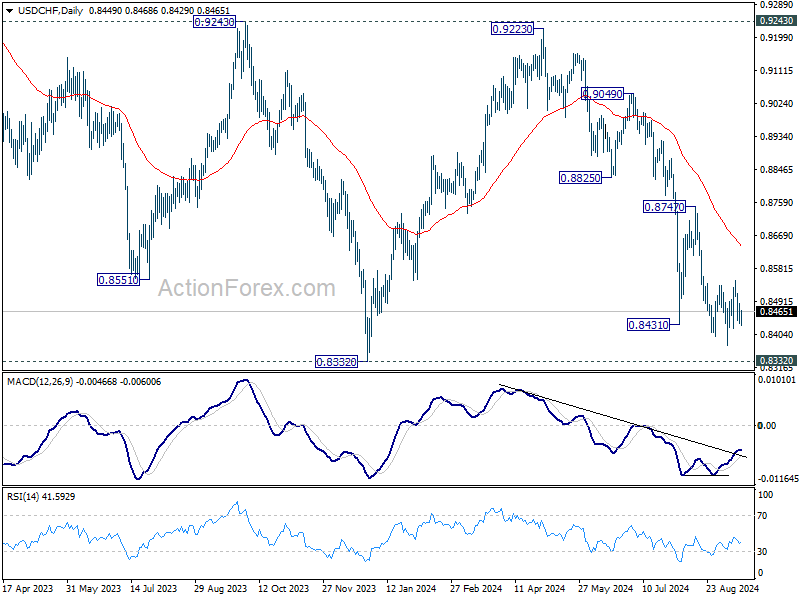

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jul | 1.40% | 1.00% | -1.30% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | 3.6 | 18.6 | 19.2 | |

| 09:00 | EUR | Germany ZEW Current Situation Sep | -84.5 | -77.3 | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | 9.3 | 17.6 | 17.9 | |

| 12:15 | CAD | Housing Starts Y/Y Aug | 217K | 246K | 280K | |

| 12:30 | CAD | CPI M/M Aug | -0.20% | 0.20% | 0.40% | |

| 12:30 | CAD | CPI Y/Y Aug | 2.00% | 2.10% | 2.50% | |

| 12:30 | CAD | CPI Median Y/Y Aug | 2.30% | 2.20% | 2.40% | |

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 2.40% | 2.50% | 2.70% | |

| 12:30 | CAD | CPI Common Y/Y Aug | 2.00% | 2.20% | 2.20% | |

| 12:30 | USD | Retail Sales M/M Aug | 0.10% | -0.10% | 1.00% | 1.10% |

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 0.10% | 0.20% | 0.40% | |

| 13:15 | USD | Industrial Production M/M Aug | 0.80% | 0.20% | -0.60% | -0.90% |

| 13:15 | USD | Capacity Utilization Aug | 78.00% | 77.90% | 77.80% | 77.40% |

| 14:00 | USD | Business Inventories Jul | 0.40% | 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Sep | 42 | 39 |

US retail sales rises 0.1% mom in Aug, ex-auto sales up 0.1% mom

US retail sales rose 0.1% mom to USD 710.7B in August, above expectation of -0.1% mom. Ex-auto sales rose 0.1% mom to USD 576.4B, below expectation of 0.2% mom. Ex-gasoline sales rose 0.1% mom to USD 658.8B. Ex-auto, gasoline sales rose 0.2% mom to USD 524.5B.

Total sales for the June through August period were up 2.3% from the same period a year

ago.

ago.

Full US retail sales release here.

Canada’s CPI slows to 2% in Aug, lowest since Feb 2021

Canada's CPI growth slowed to 2.0% yoy in August, down from 2.5% yoy in July, and below market expectations of 2.1%—marking the slowest pace since February 2021. This deceleration is largely attributed to decline in gasoline prices, driven by a combination of lower fuel prices and a base-year effect. Excluding gasoline, CPI still eased to 2.2% yoy from 2.5% yoy, indicating broad softening in inflation.

On a month-to-month basis, CPI fell by -0.2% mom, significantly below the expected 0.2% mom increase, and following a 0.4% mom rise in July. The lower-than-anticipated figures could strengthen the case for BoC to ease monetary policy more aggressively if economic data continues to signal softness.

Core inflation measures also showed signs of cooling. CPI median dipped to 2.3% yoy, slightly higher than expectations of 2.2% yoy, but CPI trimmed dropped to 2.4% yoy from 2.7%yoy, missing forecasts. CPI common index fell from 2.2% yoy to 2.0% yoy, also below expectations of 2.2% yoy.

The overall decline in inflation, especially in the core metrics, offers BoC more room to consider faster rate cuts should economic activity continue to falter. Given Governor Tiff Macklem’s recent dovish remarks, these latest inflation figures could push the central bank toward more decisive easing in the near term.

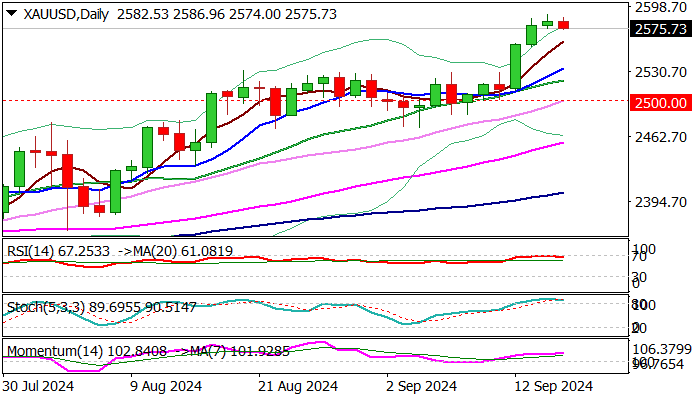

Gold (XAUUSD) Holds Near Record Highs Amid Anticipation of Fed Rate Cut

Gold prices remained stable at around $2580 per troy ounce on Tuesday, hovering close to their record highs. This resilience in the gold market is largely driven by the weakening US dollar and heightened expectations for a substantial interest rate cut by the Federal Reserve.

Current projections from the CME FedWatch tool indicate a 67% likelihood of a 50 basis point cut in today's Fed meeting, a significant increase from the 40% chance noted yesterday. Additionally, there's a 33% probability of a more modest 25 basis point reduction. These expectations have significantly influenced market sentiment, prompting investors to flock to gold as a protective asset.

Recent geopolitical events, such as the attempted assassination of US presidential candidate Donald Trump, have also underscored the metal's appeal as a safe haven, leading to a spike in demand during times of perceived instability.

The potential easing of US monetary policy, expected to be confirmed in Wednesday's Fed announcement, further bolsters gold's attractiveness. With its lack of coupon income, gold becomes more appealing during periods when yields on US government bonds are falling, and the Dollar Index (DXY) is weakening.

Technical analysis of Gold (XAU/USD)

Gold broke through the consolidation range at 2530.00 and executed a growth wave up to 2586.00. The market has now reached the expansion potential of this range and is forming a new consolidation zone at these highs. The primary expectation is for a downward move to 2555.50, potentially extending into a corrective phase towards 2530.00. The MACD indicator supports this scenario, showing signal lines above zero but starting a downward trajectory, indicating the potential for a forthcoming decline.

On the H1 chart, gold reached up to 2588.88 and is currently consolidating just below this peak. A break below this consolidation could lead to a move down to 2555.50. Conversely, a break above could briefly push prices towards 2600.00 before a potential reversal to 2530.00. The Stochastic oscillator, with its signal line below 50 and pointing sharply downward towards 20, corroborates this expected downward movement.

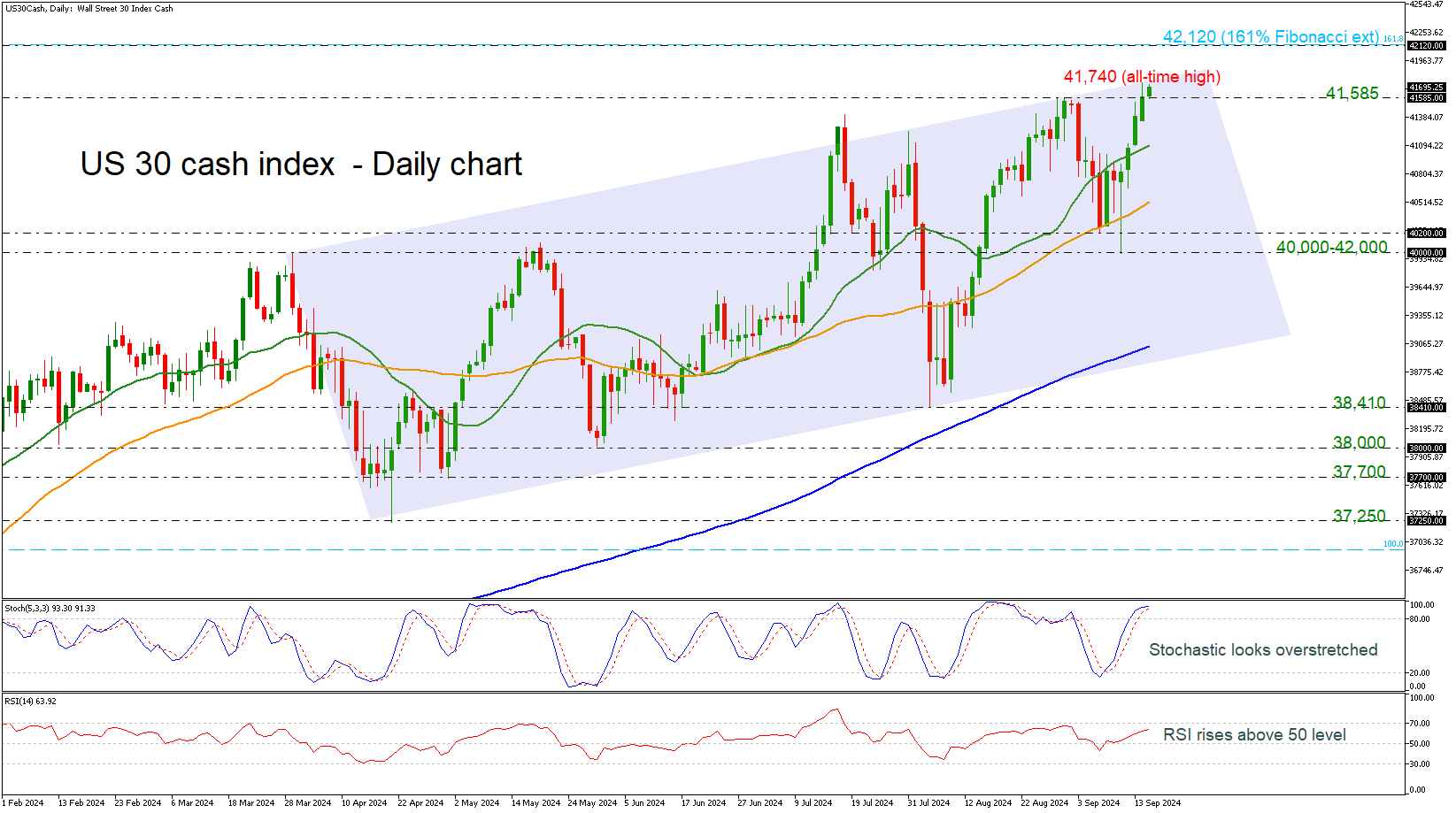

US 30 Index Records Another All-Time High

- US 30 posts several days of gains

- Price holds near upper band of ascending channel

- Stochastic looks overbought

The US 30 cash index experienced a new all-time high during Monday’s session touching the 41,740 level. The price completed four consecutive green days following the strong rebound off the 40,000 psychological mark and continues to hold near the upper boundary of the upward sloping channel.

Technically, the stochastic oscillator is looking overbought as it is turning slightly lower above the 80 level, while the RSI is rising above the neutral threshold of 50.

If the price continues the upside pressure, immediate resistance could come at 42,120 which is the 161.8% Fibonacci extension level of the downward wave from the January 2022 high at 36,950 to the October 2022 low at 28,580. Steeper increases may open the way for the next round number at 43,000.

Alternatively, a decline beneath the previous high of 41,585 may send traders lower to the 20-day simple moving average (SMA) at 41,000 ahead of the 50-day SMA at 40,500. Even lower, the area within 40,000-42,000 could be a critical territory for the bears.

In a nutshell, the US 30 index is creating higher highs, confirming the long-term bullish structure. Only a significant dive below the 200-day SMA, which currently lies at 39,000, could switch the outlook to negative.

XAU/USD Outlook: Gold Takes a Breather Under New Record High Ahead of Fed Rate Decision

Gold price edged lower in European trading on Tuesday as bulls take a breather after hitting new record high on bullish acceleration in past three days.

Overbought daily studies contribute to a partial profit taking, but dips are likely to be shallow and positioning for fresh push higher in anticipation that Fed will cut interest rates on the policy meeting which concludes on Wednesday.

Markets are likely to reduce speed and hold in quiet mode, expecting Fed’s verdict.

Fresh rise in expectations that US policymakers will opt for more aggressive 50 basis points rate cut adds to strong bullish sentiment and favors scenario of fresh longs on shallow dips for attack at psychological $2600 and possible extension higher.

Initial supports lay at $2560/55 zone guarding more significant $2533/31 supports (10DMA / former all-time high) which should contain deeper pullback.

Res: 2589; 2600; 2614; 2628.

Sup: 2561; 2556; 2531; 2520.

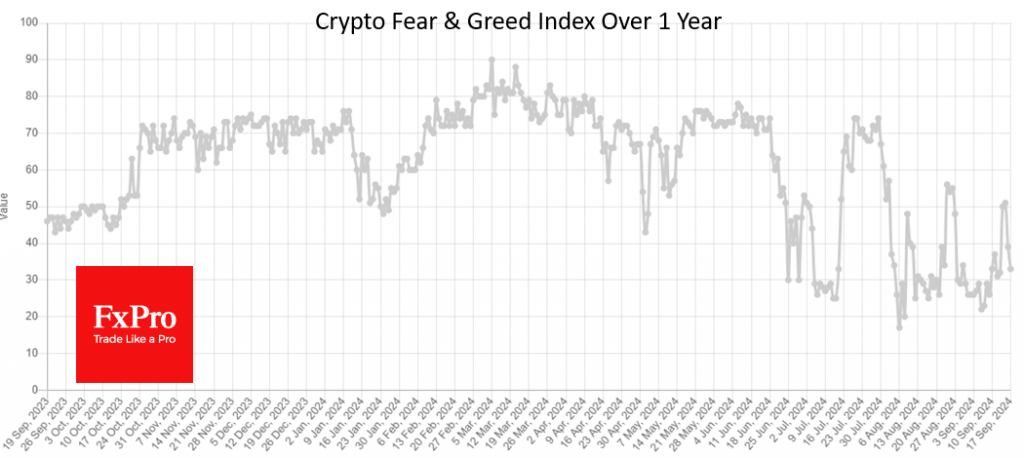

Fear Does Not Leave the Crypto Market

Market Picture

The crypto market capitalisation remained at $2.04 trillion, the same as the previous day, although it fell to $2.01 trillion during the day before rebounding on Tuesday morning. The Cryptocurrency Sentiment Index returned to the fear zone after briefly rising to neutral levels on Saturday and Sunday.

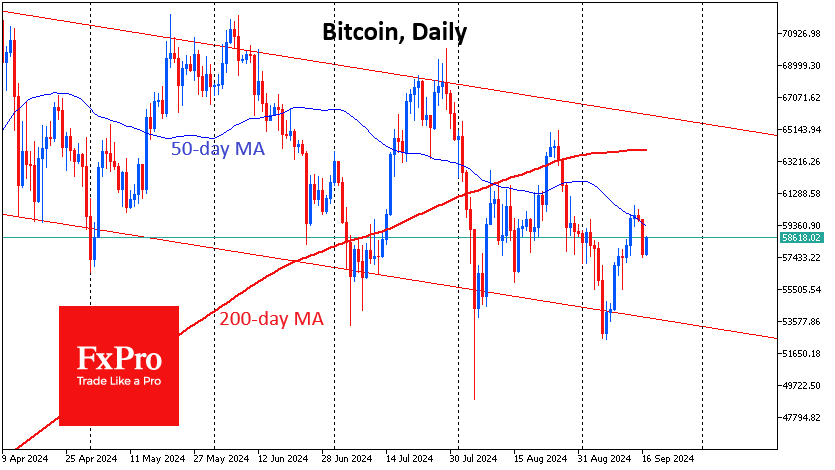

Bitcoin is trading at $58.6K, having gained 1.7% since the start of the day. However, it remains below its 50-day moving average, which is pointing lower. This resistance level has seen increased selling activity, signalling a cautious sentiment ahead of the Fed’s rate decision.

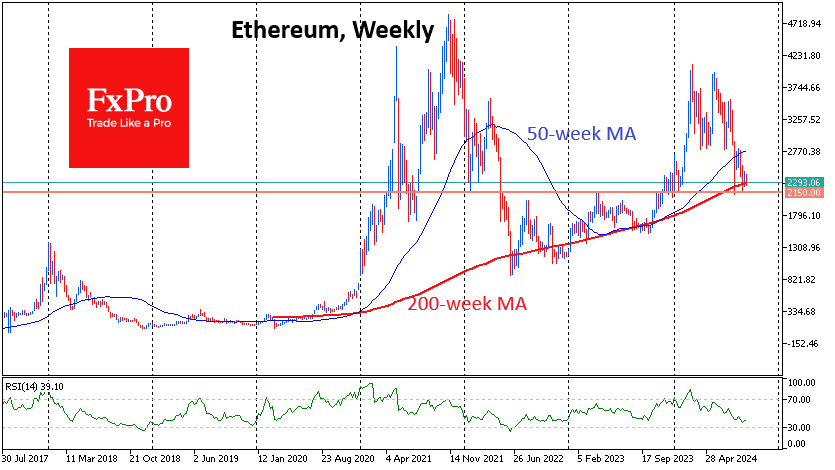

Ethereum is trading around $2300, testing support at the 200-week moving average for the third consecutive week. Since 2020, Ethereum has repeatedly found support from long-term buyers when falling towards this line or shortly after breaking it. However, without visible buyer support this time around, long-term investors may start to capitulate and doubt the prospects of the second-largest cryptocurrency. At the same time, the RSI is approaching the oversold territory, suggesting more chances of a bounce than a continuation of the decline in the absence of buyer capitulation. As such, the coin’s momentum will be telling in the coming weeks.

News Background

According to CoinShares, investments in crypto funds rose by $436 million last week after two weeks of outflows. Investments in Bitcoin increased by $436 million, Solana increased by $4 million, and Ethereum decreased by $19 million. Investments in multi-asset crypto funds increased by $23 million. The surge in inflows at the end of the week was driven by a significant shift in market expectations for a potential 50bps Fed rate cut following comments from former New York Fed President Bill Dudley. Ethereum continues to struggle, which CoinShares believes is due to concerns over the network’s profitability following the Decun update.

WeRate calculated that Bitcoin’s rally could begin in the next 22 days based on previous historical cycles. The rally began around 170 days after the halving, with the peak occurring 480 days later. Crypto investor Lark Davis recalled Bitcoin’s impressive Q4 gains during the halving years. BTC also closed with growth in Q1, Q2 and Q3 of the year after the event.

The Ethereum developers have proposed to split the major Pectra update into two parts. They plan to activate the first phase in early 2025.

USDT stablecoin issuance on the TON blockchain exceeded $1 billion. The Telegram-connected ecosystem climbed to fifth place in terms of issuance of the largest stablecoin from Tether in five months.

German ZEW plummets to 3.6 as optimism evaporates, Eurozone follows

Germany's ZEW Economic Sentiment dropped sharply in September, falling from 19.2 to 3.6, significantly missing expectations of 18.6. Current Situation Index also saw a stark declinefrom -77.3 to -84.5, its lowest level since May 2020.

In the broader Eurozone, ZEW Economic Sentiment fell to 9.3, down from 17.9, while Current Situation Index dropped -8 points to -40.4. The data suggests that confidence across the region is waning, though Germany's drop was notably more severe.

ZEW President Achim Wambach highlighted that “the hope for a swift improvement in the economic situation is visibly fading,” adding that the balance between optimists and pessimists is now evenly split.

The sharp fall in expectations for Germany signals that economic pessimism is growing faster than elsewhere in the Eurozone. Wambach also noted that most respondents seem to have already accounted for ECB's recent interest rate decision in their expectations.

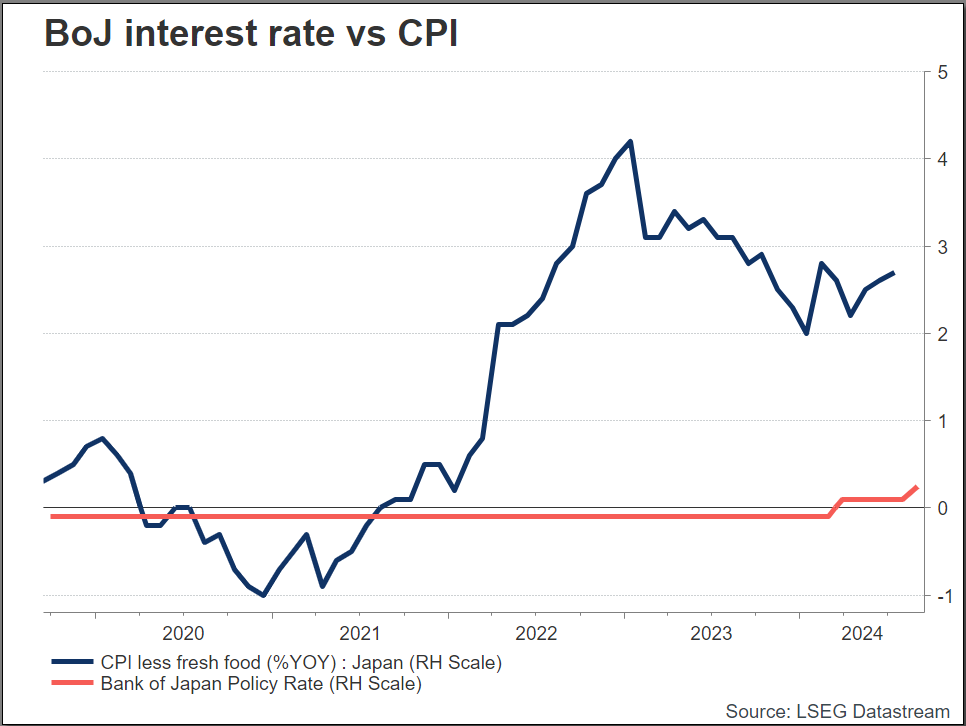

Is BoJ on Hold Until December’s Meeting?

- BoJ expects no change

- Ueda comments may provide insight

- USDJPY remains above 140.00 despite a severe sell-off

- BoJ interest rate decision on Friday at 03:00 GMT

BoJ decision to keep interest rate steady

At its meeting on Friday, the Bank of Japan (BoJ) is anticipated to keep its monetary policy position unchanged. Most market watchers expect the Bank of Japan to maintain its target range for short-term interest rates at 0% to 1%. This move is in line with the Bank of Japan's (BoJ) continuing policy of bolstering economic stability through vigilant monitoring of inflation and financial market circumstances. The Bank of Japan is unlikely to make any hasty adjustments to its interest rates, regardless of the pressures and uncertainties plaguing the global economy. The next likely rate hike is in December. This cautious approach reflects the BoJ's dedication to a measured and deliberate response to economic events. In July, Japanese policymakers raised interest rates by 15 bps and have since signalled that more hikes are looming.

The decision by the Bank of Japan is set against the background of major global central bank activity, including the expected actions of the Federal Reserve and the Bank of England. These international factors further complicate the policy choices of the BoJ. Inflation and financial market stability would most likely continue to be the BoJ's top priorities. The effects of earlier policy shifts have been carefully tracked by the central bank, and it will maintain this practice going forward.

Ueda comments

In his Friday remarks, Bank of Japan Governor Kazuo Ueda is anticipated to highlight the central bank's cautious monetary policy. He would likely emphasize the BoJ's commitment to maintaining its policy stance while closely monitoring economic signs. Ueda will likely indicate that future rate hikes are dependent on the economy and inflation. Ueda's statements suggest additional rate hikes if economic conditions match the BoJ's predictions, strengthening the steady normalization of policy. He may also emphasize watching global economic trends, particularly how other big central banks like the Fed respond. Ueda may also emphasize the need for transparent market communication to reduce volatility, considering recent market reactions to BoJ policy modifications. Ueda's statements should indicate that the BoJ is watchful and sensitive to economic changes while maintaining policy stability.

Japan’s inflation and wage growth

Japan's underlying inflation rate is projected to stabilize at around 2% as a result of continuous wage growth and effective price pass-through. Following the 2024 spring wage negotiations, the job situation has shown a modest improvement, as real earnings have continued to rise. Notwithstanding the effects of price increases, private spending has shown resilience, and the financial conditions have been favorable. The prevailing economic conditions provide a foundation for the Bank of Japan's prudent strategy towards policy modifications, which seeks to strike a balance between the provision of economic assistance and the objective of attaining enduring financial stability.

Technical Analysis on USDJPY

USDJPY plunged towards a new 14-month low of 139.60 during Monday’s session but is currently hovering above the 140.00 round number. After the pullback off the 147.20 resistance, the pair lost more than 5%, continuing the strong selling interest. More downside pressures, especially after the Fed decision on Friday, may take the market to the July 2023 low of 137.20.

On the other hand, a rise above the 20-day SMA at 143.65 could push the price towards the 146.45-147.15 restrictive region.

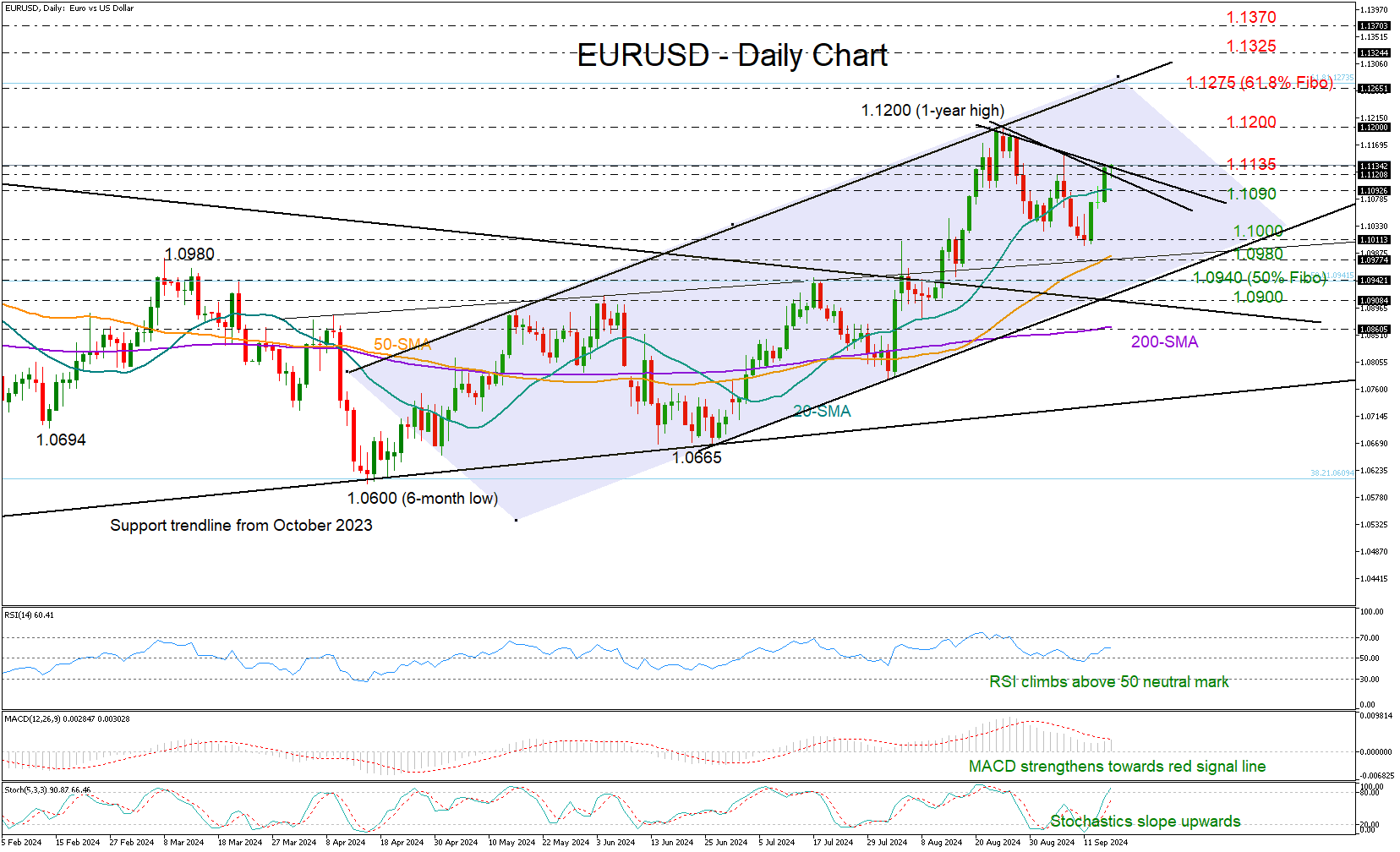

Will EURUSD Take Its Bullish Chances?

- EURUSD slows pace after a quick bounce to 1.1135

- Short-term trendline in focus; technical bias remains positive

- US retail sales due at 12:30 GMT

EURUSD started the week on the right foot, finishing Monday’s session comfortably higher, though around the short-term resistance trendline at 1.1135, which poses a risk.

The pair is currently lacking momentum, but the bulls are still in town according to the technical indicators. Hence, a close above 1.1135 could stage a new bull run towards the August peak of 1.1200, while a more exciting rally could target the upper band of the upward-sloping channel at 1.1275. Strikingly, the latter overlaps with the 61.8% Fibonacci retracement of the 2021-2022 downtrend, a break of which could see a continuation towards the 161.8% Fibonacci extension of the latest bearish wave at 1.1325.

In the event the price slips below its 20-day simple moving average (SMA) at 1.1090, it could once again find support near the 1.1000 round-level. The 50-day SMA could come next into view near 1.0980, while the 1.0900-1.0940 zone might attract greater attention as the channel’s lower boundary, a long -term descending trendline, and the 50% Fibonacci mark are within the neighborhood.

To summarize, although EURUSD is encountering a fresh barrier around the 1.1135 region following a swift bounce back, bullish sentiment remains intact.