Sample Category Title

Could BoE Surprise With a Rate Cut on Thursday?

- BoE meeting concludes on Thursday, the day after the Fed

- Economists assign an almost zero chance of a rate cut

- Wednesday’s CPI and the Fed rate cut could lead to a surprise BoE move

- Pound to benefit from an uneventful meeting

BoE will announce its rate decision on Thursday

The Bank of England is joining the chorus of the central bank meetings on Thursday. While the market will be digesting the first Fed rate cut since March 2020, Governor Bailey et al will announce their rate decision, after a meeting that does not feature the publication of quarterly projections and a press conference.

UK data flow is not conducive to another rate cut…

Since the August 1 BoE rate cut, the data flow has been rather positive and has resulted in a significant decrease in the September rate cut expectations. Specifically, PMI surveys continue to point to underlying strength in the economy while the industrial sector continues to recover. Similarly, the labour market remains relatively tight as observed by the satisfactory growth in average earnings. Consumer spending remains under the weather even though housing prices have comfortably returned to experiencing positive yearly changes.

… but August CPI and a more aggressive Fed rate cut could prove decisive

Therefore, economists are overwhelmingly expecting an uneventful gathering. That could potentially change though if:

(1) the Fed actually opts for a more aggressive start to its monetary policy easing cycle than originally anticipated. The market is currently pricing in 63% probability of a 50bps Fed rate cut on Wednesday following last week’s weaker producer and import prices indices, and a WSJ report that a 50bps move is being considered. And,

(2) Wednesday’s August CPI report shows aggressively weakening inflation pressures. The market is looking for an unchanged 2.2% annual growth in headline CPI figure, but the core indicator, which excluded energy and food prices, could accelerate to 3.5%. A significant downside surprise, partly on the back of lower oil prices in August, could put pressure on the BoE to act sooner rather than later. The market is acknowledging that there is a reasonable chance of a rate cut surprise since it is currently pricing a 37% probability for a 25bps move.

Uneventful meeting expected but voting pattern matters

Barring a major surprise, expectations for an unexciting meeting will most likely be confirmed as the BoE’s chief economist is expected to propose rates to be kept stable. The focus will then turn to the November meeting that includes the critical quarterly projections and the usual press conference.

A total of 50bps rate cut is currently priced in with the BoE seen announcing 25bps cuts in both November and December, thus adopting a slower pace compared to the Fed’s 120bps of easing currently anticipated.

The market will also be interested in Thursday's voting pattern. The August decision was reached by the slimmest possible majority, and it would be important to see if the two members, Dhingra and Ramsden, that voted for a rate cut in June, continue to push for further easing.

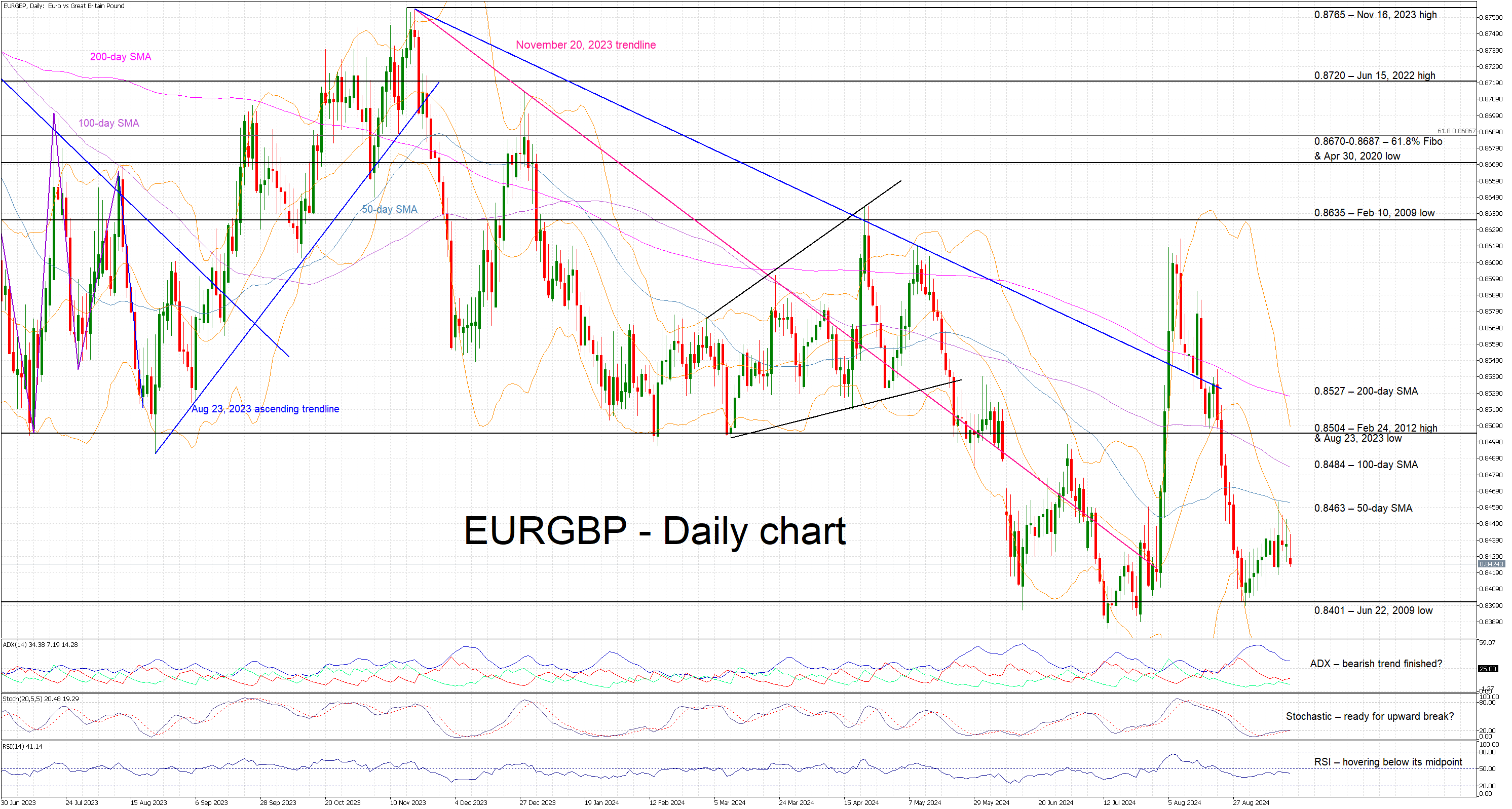

Pound could benefit from a balanced meeting

Despite the overall negative newsflow for the eurozone and the evident divergence in the economic outlook, the pound has been failing to materially benefit against the euro. Going into the BoE meeting, market sentiment will be clearly affected by the Wednesday Fed meeting.

Assuming nothing groundbreaking comes from the other side of the pond, a unanimous BoE decision to keep rate unchanged and an overall balanced tone at the press statement could help euro/pound finally break below the 0.8401 and make a move towards the 0.8339 level.

On the flip side, a 50bps rate cut by the Fed could force the BoE to turn more dovish than widely expected, potentially leading to a small number of doves voting in favour of a BoE rate cut. In this case, euro/pound bulls will probably have the chance to target the 0.8487 level and recoup part of their summer losses.

Bank of England Preview – Proceeding With Caution

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.00% on 19 September in line with consensus and market pricing.

- Overall, we expect the BoE to stick to a cautious language and deliver a dovish twist to its communication.

- We expect the reaction in EUR/GBP to be rather muted with risks tilted to the topside.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.00% on 19 September in line with consensus. Markets currently price 5bp worth of cuts for the meeting. We expect the vote split to be 7-2 with the majority voting for an unchanged decision and Ramsden and Dhingra voting for a cut. Note, this meeting will not include updated projections nor a press conference.

Since the last monetary policy decision in August, data has been to the weak side of expectations across both inflation and growth while labour market data has been more of a mixed bag. Growth was slightly weaker than expected in Q2 at 0.6% q/q (BoE forecast 0.7%) and preliminary monthly GDP numbers indicate that growth will undershoot the Q3 forecast. Inflation was slightly weaker than expected in July at 2.2%y/y (BoE forecast: 2.4%) with services proving a large part of the downside surprise although mainly due to volatile components such as hotel prices. Note, that inflation for August is released the day before the meeting and will likely be instrumental for the guidance that we will receive.

Communication from the MPC has been limited since the last meeting with speeches from Bailey at Jackson Hole and the hawkish camp including Mann and Pill. Bailey struck a more cautious tone noting that "We are not yet back to target on a sustained basis", "policy setting will ned to remain restrictive for sufficiently long" and that "the course will therefore be a steady one." Until data sufficiently warrants it, we think the BoE will be on steady course pausing at the September and December meeting this year with service inflation and wage growth still elevated.

On QT, we expect the MPC to announce another GBP 100bn of quantitative tightening for the coming year starting October. Given the maturity profile, the largest part will stem from maturities (GBP 87bn) and to a much lesser extent from outright sales (GBP 13bn).

BoE call. We expect the BoE to deliver the next 25bp cut in November and for this to be the final cut this year This is less than markets expect (55bp by YE 2024). In 2025, we expect cuts at every meeting starting in February and until H2 2025 where we expect a step down to a quarterly pace. This leaves the Bank Rate at 3.25% by YE 2025 in line with market pricing.

FX. We expect the market reaction to be rather muted upon announcement, barring any notable surprise in CPI on Wednesday altering the guidance. On balance, we tilt towards a dovish twist which does suggest some slight EUR/GBP topside following the release of the statement, as has been the case the past meetings (chart 2). That said, we more generally still expect EUR/GBP to continue its recent move lower driven by UK economic outperformance, BoE lagging peers in an easing cycle for the time being and tight credit spreads. The key risk is policy action from the BoE.

Sunset Market Commentary

Markets

A range of ECB speeches in the wake of last week’s policy decision confirmed the different approach of Frankfurt – in all likelihood – is taking compared to the Fed. Kazaks (Latvia) and Holzmann (Austria) did so last week. Kazimir (Slovakia) today said that the next move (down) “must almost surely wait until December”. De Guindos and Lane, the VP and chief economist respectively, doubled down on president Lagarde’s message of gradualism and data-dependency. The latter added that there should be optionality about the easing speed though. It is nevertheless an increasingly stark contrast with the kind of frontloading the Fed may be prepping for. With 42 bps of cuts priced in for Wednesday, markets attach a +/- sizeable 65% probability of a large inaugural cut. Not delivering on these bets could unsettle markets. That leads some to believe that if there is no unofficial communication in the next several hours (through the likes of WSJ), the Fed will (have to) start off big. The heated topic keeps US yields in the defensive. The first unexpected positive reading since November 2023 of the NY Fed’s manufacturing survey (11.5 from -4.7 with the 6-month ahead gauge at the highest since March 2022) did little to alter the move but kept the intraday lows away. Front end outperformance brings about a decline of 2.7 bps (2yr). The long end eases <1 bps. Bund yields are marginally down 0.7-1.3 bps across the curve in sympathy. The US dollar hangs in the ropes once again. The trade-weighted DXY is testing December 2023 support around 100.6. EUR/USD jumped beyond 1.11 and fell just short of a test of a first intermediate resistance around 1.1139. USD/JPY hit a new YtD low with the 140 barrier looking shaky. Sterling captures a nice bid against USD (Cable tests 1.32) and the euro (EUR/GBP 0.843). The Bank of England is meeting on Thursday but is expected to leave the policy rate unchanged at 5%.

News & Views

Eurostat published Q2 labour cost data today. They rose by 4.7% Y/Y for the euro area and by 5.2% Y/Y for the EU, respectively down from 5% Y/Y and 5.5% Y/Y in Q1. On a country level, the highest increases in hourly wage costs for the whole economy were recorded in Croatia (+17.6%), Bulgaria (+15.4%), Romania (+15.0%), Hungary (+13.2%) and Poland (+13.0%). Two more EU Member States recorded an increase above 10%, namely: Latvia (+11.0%) and Lithuania (+10.9%). In the EMU, the cost of hourly wages & salaries increased by 4.5% Y/Y while the non-wage component increased by 5.2% Y/Y. On a sectoral level, wages went up by 4.5% in services, by 4.8% in industry and by 5.3% in construction. Today’s data add to evidence that underlying price pressure in the euro area remains sticky, preventing the ECB from making monetary policy less restrictive at a rapid pace.

• The National Bank of Poland today published core inflation data for the month of August. The Polish statistical office already published general CPI data earlier, with headline CPI at 0.1% M/M and 4.3% Y/Y. The NBP publishes four core calculations. Core inflation excluding food and energy prices came in at 0.3% M/M and 3.7% Y/Y (down from 3.8%). Other measures remained modest at 0.1% M/M for CPI ex administered prices (2.9% Y/Y), 0.1% M/M also for the series excluding most volatile price components (4.8% Y/Y) and the 15% trimmed mean average at 0.2% M/M and 4.0%. The NBP targets inflation at 2.5% with a 1.0% +/- tolerance band. Polish headline inflation in July jumped above the NBP’s tolerance band as the government phased out some inflation shield measures. Higher headline inflation, a loose budget and strong wage growth are mentioned by the NBP as factors preventing a rate cut in the near term. Still some MPC members recently opened de door to start discussion in the first quarter of next year.

The Bank of International Settlements (BIS) published its quarterly review, titled “carry off, carry on”. One of the main lessons is that the unwinding of leveraged positions, including carry trades, which triggered short-lived bouts of extreme market volatility and FX movements early August isn’t going the be a one-off. “It’s part of the bigger picture, the inevitable withdrawal symptoms that markets suffer as they transition away from the extraordinary period of exceptionally low interest rates and ample liquidity”, according to BIS head of the monetary and economics department Borio. Markets have become hypersensitive to growth-related news surprises and the associated revisions to expectations of the policy stance ahead. In contrast to equity markets, volatility in credit markets remained subdued and conditions generally benign.

Graphs

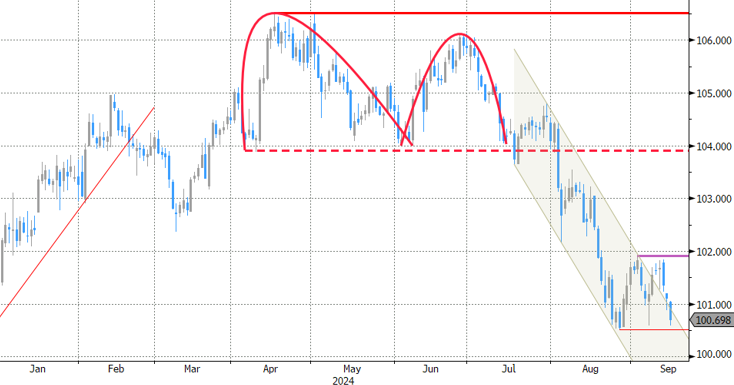

US 2y yield tests March 2023 low as odds for big Fed start rise

DXY: trade-weighted dollar index suffers under loss of yield support

Vix equity volatility index eases from recent highs but remains at elevated levels compared to recent history

EUR/PLN nears the recent lows as PLN investors try to figure out the NBP easing intensions

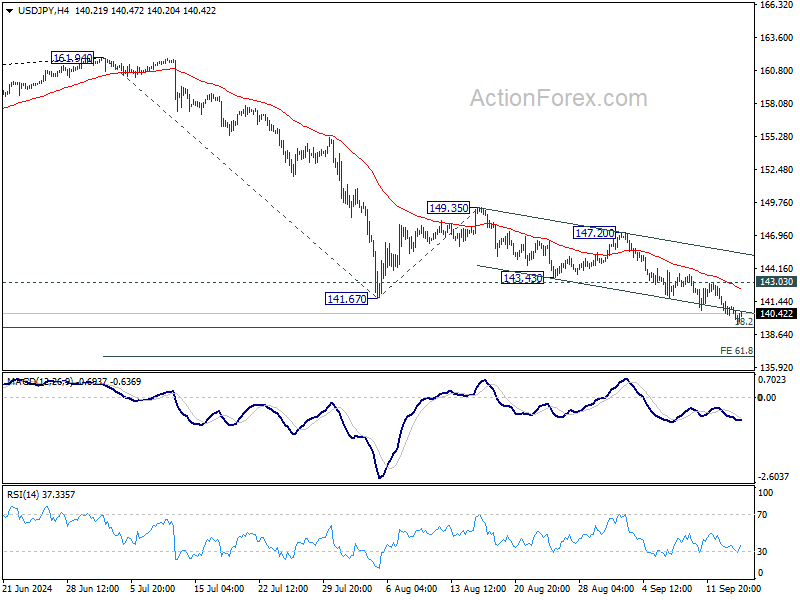

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.08; (P) 140.99; (R1) 141.69; More...

Outlook in USD/JPY is unchanged and intraday bias stays on the downside. Some support could be seen from 139.26 fibonacci level to bring rebound. But outlook will remain bearish as long as 143.03 resistance holds. Decisive break of 139.26 would carry larger bearish implications, and target 61.8% projection of 161.94 to 141.67 from 149.35 at 136.82.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. Strong support could be seen there to bring rebound. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

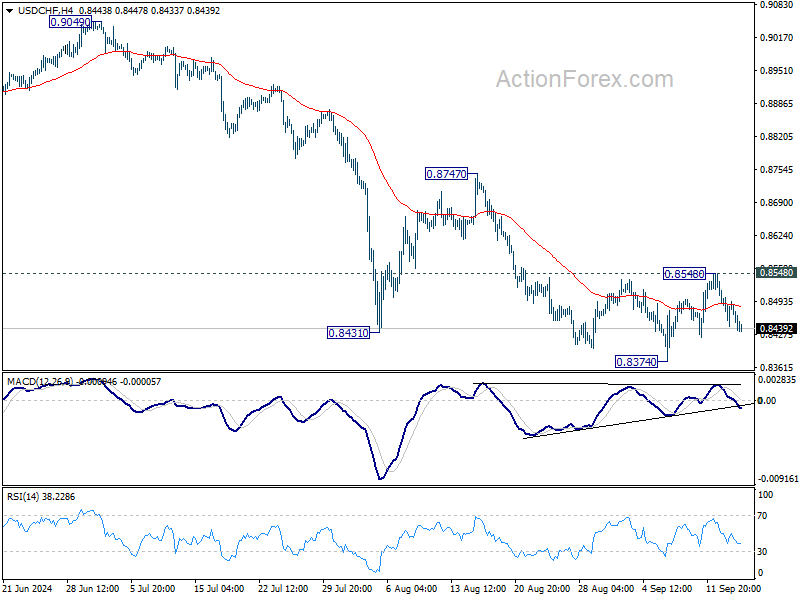

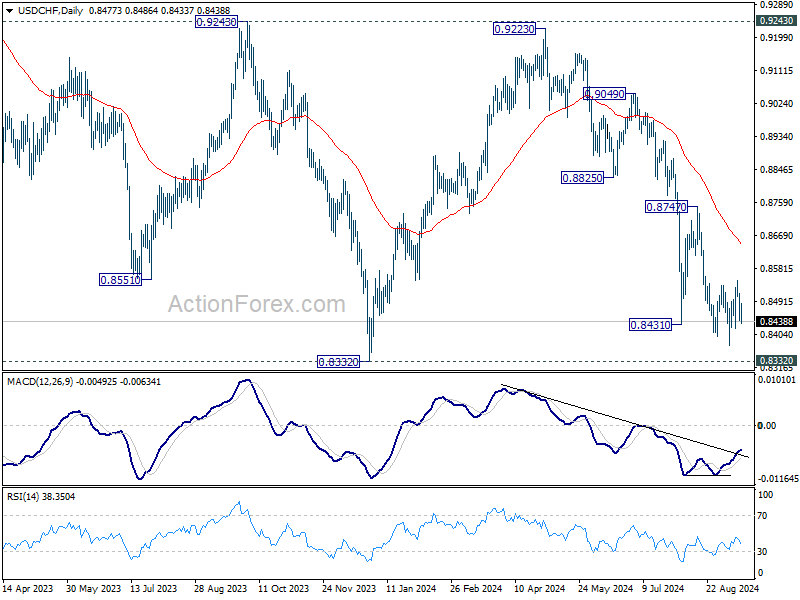

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8441; (P) 0.8494; (R1) 0.8544; More…

Range trading continues in USD/CHF and intraday bias stays neutral at this point. Further decline is expected with 0.8548 resistance intact. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8548 resistance will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

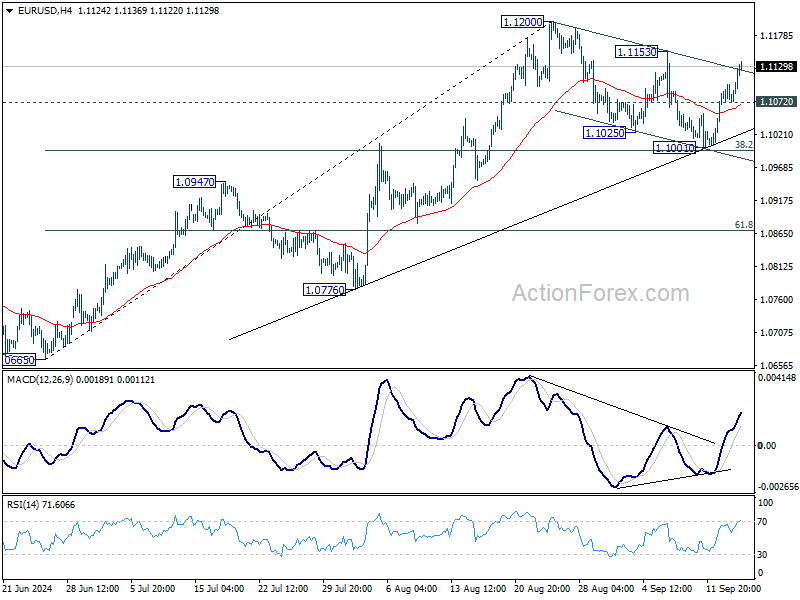

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1063; (P) 1.1083; (R1) 1.1095; More....

EUR/USD's rebound from 1.1001 extends higher today but stays below 1.1153 resistance. Intraday bias remains neutral first. On the upside, break of 1.1153 resistance will suggest that later rally is ready to resume and target 1.1200, and then 1.1274 high. On the downside, below 1.1072 minor support will turn bias back to the downside for 38.2% retracement of 1.0665 to 1.1200 at 1.0996 again.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

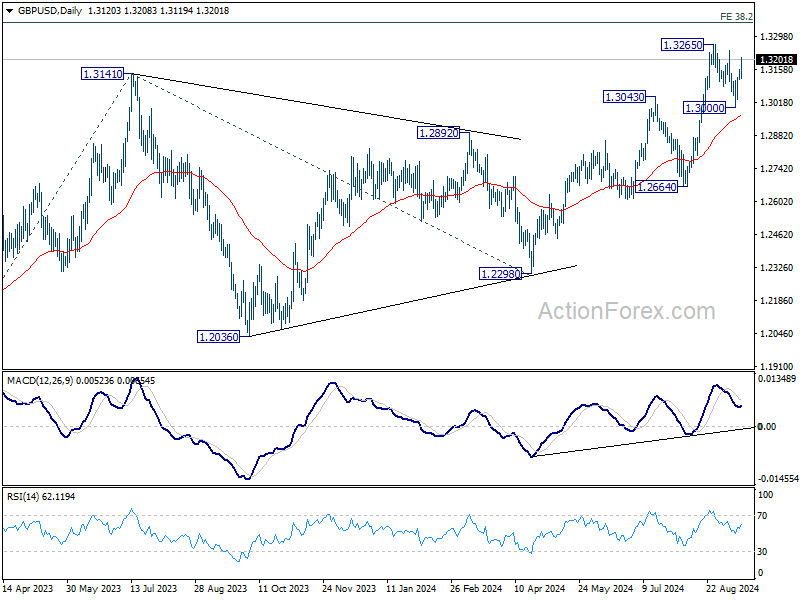

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3109; (P) 1.3133; (R1) 1.3152; More...

GBP/USD's rebound from 1.3000 extends higher today but stays below 1.3265 resistance. Intraday bias remains neutral first. On the upside, decisive break of 1.3265 will resume larger rally 1.3364 projection level next. On the downside, below, 1.3177 minor support will turn bias to the downside, to extend the correction from 1.3265 through 1.3000 support.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Dollar Weakens as Traders Boost Bets on 50bps Fed Cut

Traders continue to ramp up bets on a 50bps rate cut by Fed this Wednesday, with market odds now sitting at 65%. This increasing expectation is driving DOW futures higher, positioning the index for a potential new record high in the upcoming regular trading session. However, S&P 500 and NASDAQ are showing less momentum, struggling to match DOW's rally for now.

In the currency markets, Dollar is facing renewed selling pressure, making it the worst performer today at this point. USD/JPY is currently testing the key psychological level of 140, and the greenback is under threat of retesting recent lows against the major European currencies even before the FOMC's rate decision. Other currencies are showing mixed performance, with Yen displaying some tentative strength, while the Canadian Dollar remains on the weaker side.

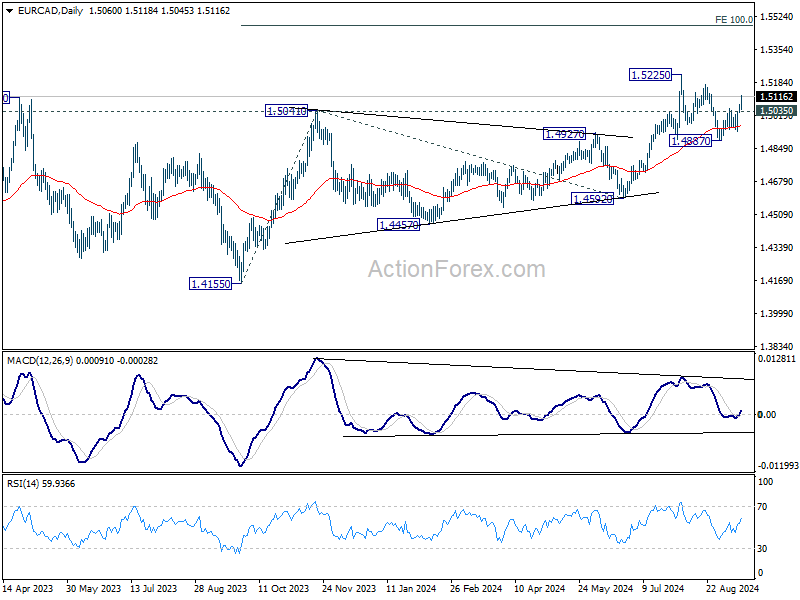

Technically, EUR/CAD's rebound from 1.4887 accelerates higher today. The development affirms that case that correction from 1.5225 has already completed. Further rise is in favor as long as 1.5035 minor support holds. Retest of 1.5225 should be seen next. Firm break there will resume whole rise from 1.4155 to 100% projection of 1.4155 to 1.5041 from 1.4592 at 1.5478.

In Europe, at the time of writing, FTSE is down -0.05% DAX is down -0.31%. CAC is down -0.18%. UK 10-year yield is down -0.0055 at 3.762. Germany 10-year yield is down -0.021. Earlier in Asia, Japan and China were on holiday. Hong Kong HSI rose 0.31%. Singapore Strait Times rose 0.22%.

ECB's Lane expects rapid inflation decline by 2025

ECB Chief Economist Philip Lane provided insight into the central bank's inflation expectations in a speech today. In the near term, headline inflation is anticipated to fluctuate, with a temporary dip in September followed by a rebound later this year.

But more significantly, ECB projects a "rapid decline" in inflation over the next two years, from 2.6% in Q4 2024 to 2.0% in Q4 2025. Core inflation, which is primarily driven by services, is expected to follow a "even sharper" drop, falling from 2.9% at the end of this year to 2.1% by the same period in 2025.

The projections align with weaker economic growth and declining wage pressures, both of which are expected to accelerate the disinflationary process throughout 2025. Lane noted that this slowdown in wage growth is consistent with the recent data, reflecting the end of the “catch-up” dynamics seen in recent years. Additionally, the disinflation process will be supported by well-anchored forward-looking inflation expectations, with reduced price-price and price-wage dynamics compared to the higher inflation environment of 2023.

Looking forward, Lane emphasized that a "gradual approach" in reducing policy restrictiveness will be appropriate, provided the data aligns with ECB's baseline projection. However, he cautioned that the central bank will "retain optionality" about the pace of adjustment, indicating flexibility depending on future economic developments.

ECB's Kazimir: December almost surely the decision point for next rate cut

ECB Governing Council member Peter Kazimir expressed his cautious stance regarding future rate cuts, noting in a blog post that “We will almost surely need to wait until December for a clearer picture before making our next move.”

Kazimir also underscored the importance of receiving a "significant shift" or a "powerful signal" in the economic outlook to support backing another cut in October.

However, "the fact is that very little new information is in the pipeline" before October meeting, he added.

The Governing Council member argued that it is essential for the central bank to ensure incoming data aligns with projections, warning that acting too quickly could lead to regret if inflation has not been sustainably brought under control.

Eurozone goods exports rises 10.2% yoy in Jul, imports up 4.0% yoy

Eurozone goods exports rose 10.2% yoy to EUR 252.0B in July. Goods imports rose 4.0% yoy to EUR 230.8B. Trade balance showed a EUR 21.2B surplus. Intra-Eurozone trade rose 4.3% yoy to EUR 221.0B.

In seasonally adjusted term, Eurozone goods exports rose 0.8% mom to EUR 239.0B. Goods imports rose 1.6% mom to EUR 223.5B. Trade surplus narrowed from June's EUR 17.0B to EUR 15.5B, smaller than expectation of EUR 20.3B. Intra-Eurozone trade rose 0.9% mom to EUR 21.4B.

NZIER downgrades New Zealand's growth forecast to flat in 2025, recovery delayed

New Zealand's economic outlook has been notably downgraded by the New Zealand Institute of Economic Research (NZIER), with projections pointing to zero GDP growth for fiscal 2025, a stark revision from the previous forecast of 0.6%.

Growth is expected to pick up modestly to 2.2% in 2026 and further to 2.8% in 2027, though these estimates are also lower than those given earlier in the year. The institute's June forecast had previously anticipated 2.4% growth in 2025 and 3.0% in 2026, highlighting the extent of the shift in expectations.

Inflation estimates have similarly been revised downward. CPI is now expected to come in at 2.3% for 2024, down from the 2.6% forecast in June. For 2025, CPI is projected at 2.0%, revised from the earlier estimate of 2.1%, while the 2026 forecast remains unchanged at 2.1%.

NZIER pointed to concerning signals from its own Quarterly Survey of Business Opinion, which has shown a sharp drop in business confidence and in firms' trading activity. This data suggests that the near-term outlook is particularly weak, with businesses expecting tougher conditions ahead. The slowdown is expected to persist through 2025, with lower interest rates forecasted to provide some support in stimulating a recovery beyond that.

NZ BNZ services ticks up to 45.5, longest contraction since GFC

New Zealand's BusinessNZ Performance of Services Index edged up slightly in August, rising from 45.2 to 45.5, but still remains well below the long-term average of 53.2. The data shows that the service sector is continuing to struggle, with the index remaining in contraction for the sixth consecutive month, marking the longest period of decline since the global financial crisis.

Breaking down the numbers, activity/sales increased from 41.2 to 43.9, while employment also saw a slight rise from 47.0 to 43.9. However, new orders/business fell from 47.0 to 46.6, and stocks/inventories dropped from 45.3 to 44.6. Supplier deliveries improved marginally from 41.1 to 43.3.

The proportion of negative comments decreased to 60.8% in August, down from 67.0% in July and June. Despite the modest improvement, businesses continued to cite the high cost of living and challenging economic conditions as key concerns.

BNZ's Senior Economist Doug Steel noted, "Smoothing through monthly volatility, the PSI's 3-month average remains deep in contractionary territory at 43.9. The PSI has been in contraction for six consecutive months, which is the longest continuous period of decline since the GFC."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3109; (P) 1.3133; (R1) 1.3152; More...

GBP/USD's rebound from 1.3000 extends higher today but stays below 1.3265 resistance. Intraday bias remains neutral first. On the upside, decisive break of 1.3265 will resume larger rally 1.3364 projection level next. On the downside, below, 1.3177 minor support will turn bias to the downside, to extend the correction from 1.3265 through 1.3000 support.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | 45.5 | 44.6 | 45.2 | |

| 23:01 | GBP | Rightmove House Price Index M/M Sep | 0.80% | -1.50% | ||

| 06:30 | CHF | Producer and Import Prices M/M Aug | 0.20% | 0.10% | 0.00% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | -1.20% | -1.70% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | 15.5B | 20.3B | 17.5B | 17.0B |

| 12:30 | CAD | Manufacturing Sales M/M Jul | 1.40% | 0.70% | -2.10% | |

| 12:30 | USD | Empire State Manufacturing Index Sep | 11.5 | -3.9 | -4.7 |

ECB’s Lane expects rapid inflation decline by 2025

ECB Chief Economist Philip Lane provided insight into the central bank’s inflation expectations in a speech today. In the near term, headline inflation is anticipated to fluctuate, with a temporary dip in September followed by a rebound later this year.

But more significantly, ECB projects a "rapid decline" in inflation over the next two years, from 2.6% in Q4 2024 to 2.0% in Q4 2025. Core inflation, which is primarily driven by services, is expected to follow a "even sharper" drop, falling from 2.9% at the end of this year to 2.1% by the same period in 2025.

The projections align with weaker economic growth and declining wage pressures, both of which are expected to accelerate the disinflationary process throughout 2025. Lane noted that this slowdown in wage growth is consistent with the recent data, reflecting the end of the “catch-up” dynamics seen in recent years. Additionally, the disinflation process will be supported by well-anchored forward-looking inflation expectations, with reduced price-price and price-wage dynamics compared to the higher inflation environment of 2023.

Looking forward, Lane emphasized that a "gradual approach" in reducing policy restrictiveness will be appropriate, provided the data aligns with ECB's baseline projection. However, he cautioned that the central bank will "retain optionality" about the pace of adjustment, indicating flexibility depending on future economic developments.

New Zealand Dollar Jumps as Services PMI Accelerates

The New Zealand dollar has started the new trading week with strong gains. NZD/USD is up 0.55% today, trading at 0.6191 in the European session at the time of writing.

NZ Services PMI improves

New Zealand’s services sector hasn’t shown growth in sixth months but there was a bit of positive news today as the services PMI improved to 45.5 in August, up from an upwardly revised 45.2 in July. This was its highest level since April. On Friday, New Zealand’s manufacturing PMI also improved, rising in August from an upwardly revised 44.4 to 45.8, although shy of the forecast of 47.0.

Although services and manufacturing remain firmly in contraction territory (the 50 level separates contraction from expansion), the acceleration in August and the upward revisions a month earlier point to some positive momentum.

The Reserve Bank of New Zealand joined the rate-cutting club last month, lowering rates by 25 basis points to 5.25%. The economy has been struggling and with inflation down to 3.3%, the central bank has started a rate-cut cycle as it tries to boost weak economic activity.

The RBNZ meets next on October 9 and the sole tier-1 event until then is second-quarter GDP, which will be released on Thursday. The markets are braced for grim numbers as the economy is expected to have contracted in the second quarter (-0.4% q/q and 0.5% y/y) after posting small gains in the first quarter. If GDP contracts in Q2, there will be further pressure on the RBNZ to lower rates at the next meeting.

NZD/USD Technical

- NZD/USD is putting pressure on resistance at 0.6199. Above, there is resistance at 0.6240

- 0.6153 and 0.6112 are providing support