Sample Category Title

Cliff Notes: Global Easing Cycle Gains Traction

Key insights from the week that was.

In Australia, the RBA’s August meeting minutes again reinforced the Board’s well telegraphed views on the economy. In short, there is “less spare capacity than previously assumed” given stronger momentum in demand and a weaker assessment of potential supply. The Board also noted that financial conditions appeared to have “eased modestly” over recent months, as house prices and credit growth had picked up. Alongside the uncertainty over the timing of inflation’s sustainable return to target, these judgements were central to the debate over whether to raise or maintain the cash rate at the July meeting.

While the case to leave the cash rate unchanged was deemed stronger, the decision was paired with a need to remain vigilant of inflation risks and guidance that “it was unlikely that the cash rate target would be reduced in the short term”, with the Board of the view that “holding the cash rate target steady at its current level for a longer period than currently implied by market pricing may be sufficient to return inflation to target in a reasonable timeframe”.

Chief Economist Luci Ellis’ essay this week assesses the judgements and points of uncertainty underlying the RBA’s decision making. To us it is evident that, while a “greater-than-usual weight” might be being placed “on the flow of data, relative to the forecasts”, it is only after the RBA judge labour market slack to have emerged that they will shift their stance on policy. We continue to expect 100bps of easing through 2025, beginning at the February meeting.

Offshore, it was also a quiet week, markets largely marking time ahead of tonight’s address to the Jackson Hole Symposium by FOMC Chair Powell.

Ahead of Chair Powell’s address, the minutes of the July FOMC meeting made clear that the Committee is very close to deciding the stance of policy is now unnecessarily tight and should be eased. In their discussions, members expressed growing comfort with the trajectory of inflation, with "some further progress… broad based across the major subcomponents of core inflation". Supply and demand in the labour market was also regarded as coming into better balance.

Not known at the time of the meeting is that nonfarm payrolls over the year to March 2024 was 818k lower than initially estimated. While we won’t know the month-by-month profile until early next year, when this week’s initial revision is finalised, it is equivalent to the average monthly gain over the year to March 2024 being revised from 242k to 174k. Considering payrolls captures the number of jobs, which some people may have two or more of, and as population growth averaged 133k over the year to March 2024, it now looks as though the US labour market has been in balance for more than a year. This fits with CPI ex-shelter inflation holding at or below the 2.0% target since mid-2023.

Note though, activity growth is still characterised by the Committee as robust, so there is no cause for alarm. Instead, the tone of commentary from FOMC officials this week has remained measured, consistent with the “majority” view in the minutes that “if the data continued to come in about as expected, it would likely be appropriate to ease policy at the next meeting".

Of the other data released this week, the inflation readings from the Euro Area and Canada were most significant. Euro Area inflation outcomes for July were unchanged in the final release, prices unchanged in the month and up 2.6%yr. Constructive for the inflation outlook, the ECB’s wage measure also moderated to 3.6%yr from 4.7%yr three months earlier. Canadian annual headline inflation meanwhile edged lower in July from 2.7%yr to 2.5%yr as expected.

The data flow and commentary from officials therefore continues to point to rate cuts in coming months not only in the US but across most of the developed world, including the Euro Area, Canada and the UK.

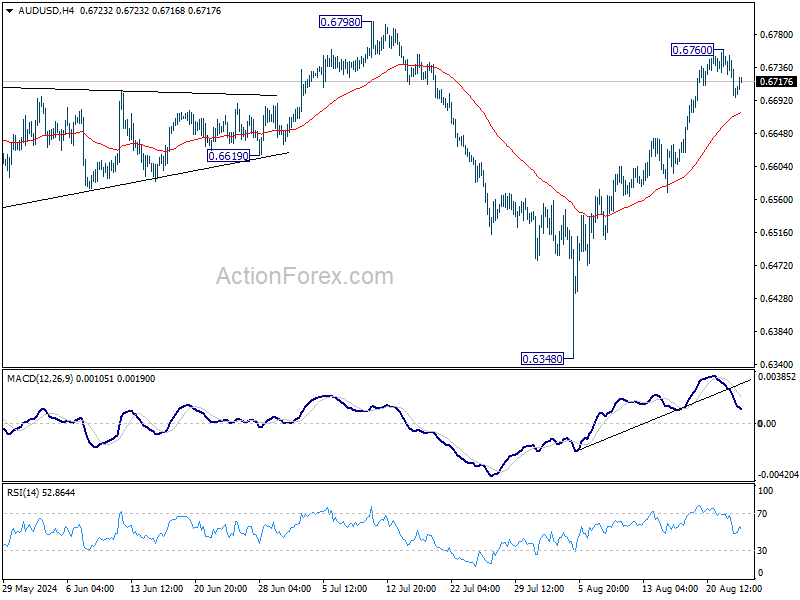

AUD/USD Daily Report

Daily Pivots: (S1) 0.6683; (P) 0.6719; (R1) 0.6740; More...

Intraday bias in AUD/USD remains neutral as consolidations continue below 0.6760 temporary top. Downside of retreat should be contained by 55 4H EMA (now at 0.6676) to bring rebound. Above 0.6760 will target 0.6798 resistance next. Firm break there will argue that larger rise from 0.6269 is ready to resume through 0.6870 resistance. However, sustained break of 55 4H EMA will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 0.6633) and possibly below.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern. Rise from 0.6340 is likely developing into another rising leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

Buckle Up: Markets Brace for Fed Powell’s Jackson Hole Remarks

In the calm before what could be a stormy session, forex markets remained exceptionally quiet during Asian trading. Dollar managed a slight recovery overnight, bolstered by pullback in US equities, but the upward momentum has been notably weak. Traders are now laser-focused on Fed Chair Jerome Powell’s speech at the Jackson Hole Symposium, which might hopefully offer critical insights into Fed’s next moves.

Remarks from various Fed officials have solidified expectations for a September rate cut. However, the consensus appears to be leaning towards a cautious, incremental approach to loosening monetary policy. While some market participants are holding out hope for a 50 bps cut to kickstart the easing cycle, the odds are not in favor, with only about 25% chance priced in by fed fund futures. A more modest 25bps cut seems the more likely scenario, as Fed seeks to avoid overreacting while stay in guard against inflation resurgence.

Meanwhile, Yen is showing modest strength, though the gains are far from robust. Japan’s core inflation has ticked up for the third consecutive month, driven primarily by a temporary spike in energy prices. However, core-core inflation, which excludes both food and energy, continues to decelerate. In a special session of the Japanese parliament, BoJ Governor Kazuo Ueda reiterated the bank’s readiness to continue reducing monetary stimulus, despite recent market volatility. There is ongoing speculation that BoJ might consider another rate hike before the year ends, but such a decision will heavily depend on forthcoming economic data and the stability of financial markets.

Looking at the broader picture for the week, Dollar remains the weakest performer, followed by Canadian Dollar and Australian Dollar. On the flip side, Swiss Franc leads as the strongest currency, with New Zealand Dollar and Yen also showing solid performance. Euro and Sterling are positioned somewhere in the middle.

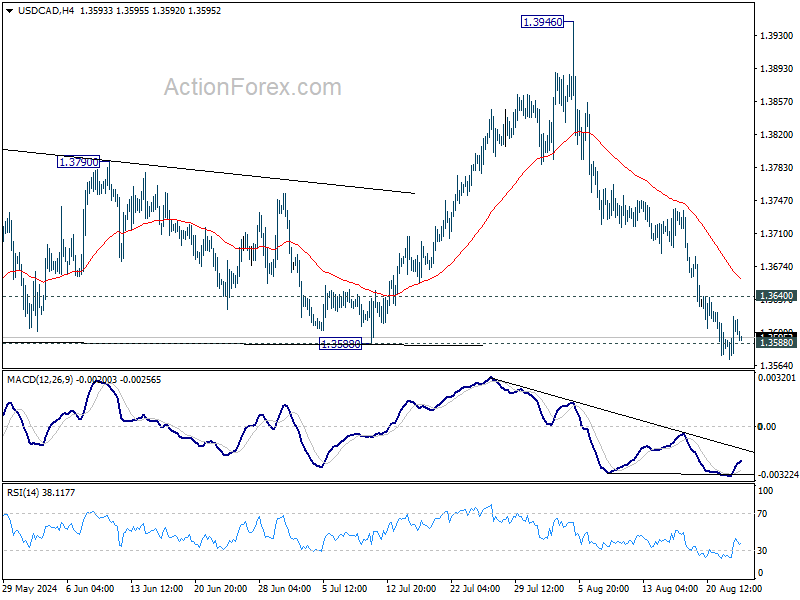

Technically, USD/CAD is still refusing to give up on defending 1.3588 structural support. Strong rebound from current level, followed by break of 1.3640 minor resistance, will argue that correction from 1.3946 has completed. That would also retain near term bullishness and set the stage for retesting 1.3946 high. However, sustained break of 1.3588 will be a near term bearish sign that should at least bring deeper correction. The next move could be heavily influenced by Powell’s remarks or upcoming Canadian retail sales data, which are expected later today.

In Asia, at the time of writing, Nikkei is up 0.50%. Hong Kong HSI is down -0.41%. China Shanghai SSE is down -0.05%. Singapore Strait Times is up 0.19%. Japan 10-year JGB yield is up 0.021 at 0.901. Overnight, DOW fell -0.43%. S&P 500 fell -0.89%. NASDAQ fell -1.67%. 10-year yield rose 0.0840 to 3.862.

BoJ's Ueda ready to scale back easing despite market instability

In a special parliamentary session today, BoJ Governor Kazuo Ueda reiterated the central bank's stance to its current monetary policy, even amidst recent market volatility. He emphasized that there is "no change to our basic stance to adjust the degree of monetary easing" should economic and price trends align with its forecasts.

Addressing concerns over the market turbulence observed in early August, Ueda attributed the instability to rising fears of a US recession, driven by weaker-than-expected economic data. He also noted that BoJ’s interest rate hike in July had triggered a sharp reversal in the "one-sided Yen falls".

He stressed that BoJ would continue to monitor market movements closely, recognizing their potential impact on the central bank's growth and price forecasts.

"Markets at home and abroad remain unstable, so we will be highly vigilant to market developments for the time being," Ueda remarked.

Japan's CPI core ticks up to 2.7% in Jul, but core-core falls to 1.9%

Japan's CPI Core, which excludes food, rose slightly from 2.6% yoy to 2.7% yoy in July, aligning with expectations and marking the 28th consecutive month that core inflation has been at or above the BoJ 2% target.

However, CPI core-core, which excludes both food and energy, fell from 2.2% yoy to 1.9% yoy, dipping below the critical 2% threshold for the first time since September 2022.

Headline CPI remained steady at 2.8% yoy. Notably, electricity prices surged by 22% following the suspension of utility subsidies, which contributed to the overall inflation rate. In contrast, services inflation softened, dropping from 1.7% yoy to 1.4% yoy.

The uptick in core CPI largely reflects the phase-out of government subsidies aimed at reducing household utility costs. Excluding this factor, the broader inflation trend appears to be on a slowing path.

New Zealand retail sales volume falls -1.2% qoq in Q2

New Zealand's retail sales volume fell -1.2% qoq in Q2, , well below the expected -0.1% drop. Retail sales value also decreased by -1.3% qoq. Notably, 11 out of 15 retail industries reported lower sales volumes compared to the previous quarter.

Total volume of retail sales per person fell by -1.5%, marking the tenth consecutive quarter of decline after adjustments for seasonal effects and price inflation.

Ricky Ho, Business Financial Statistics Manager, highlighted the severity of this trend, noting, "Retail sale volumes per person have been falling for the last two-and-a-half years. The last time we saw several quarters of consistent falls was between 2007 and 2009, which coincided with the global financial crisis."

Looking ahead

The European economic calendar is empty today. Canada will release retail sales while US will publish new home sales. But all attention will be on Fed Chair Jerome Powell's Jackson Hole speech.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6683; (P) 0.6719; (R1) 0.6740; More...

Intraday bias in AUD/USD remains neutral as consolidations continue below 0.6760 temporary top. Downside of retreat should be contained by 55 4H EMA (now at 0.6676) to bring rebound. Above 0.6760 will target 0.6798 resistance next. Firm break there will argue that larger rise from 0.6269 is ready to resume through 0.6870 resistance. However, sustained break of 55 4H EMA will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 0.6633) and possibly below.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern. Rise from 0.6340 is likely developing into another rising leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | -1.20% | -1.00% | 0.50% | 0.40% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | -1.00% | -0.80% | 0.40% | 0.30% |

| 23:01 | GBP | GfK Consumer Confidence Aug | -13 | -11 | -13 | |

| 23:30 | JPY | National CPI Y/Y Jul | 2.80% | 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jul | 2.70% | 2.70% | 2.60% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Jul | 1.90% | 2.20% | ||

| 12:30 | CAD | Retail Sales M/M Jun | -0.30% | -0.80% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | -0.40% | -1.30% | ||

| 14:00 | USD | New Home Sales Jul | 630K | 617K |

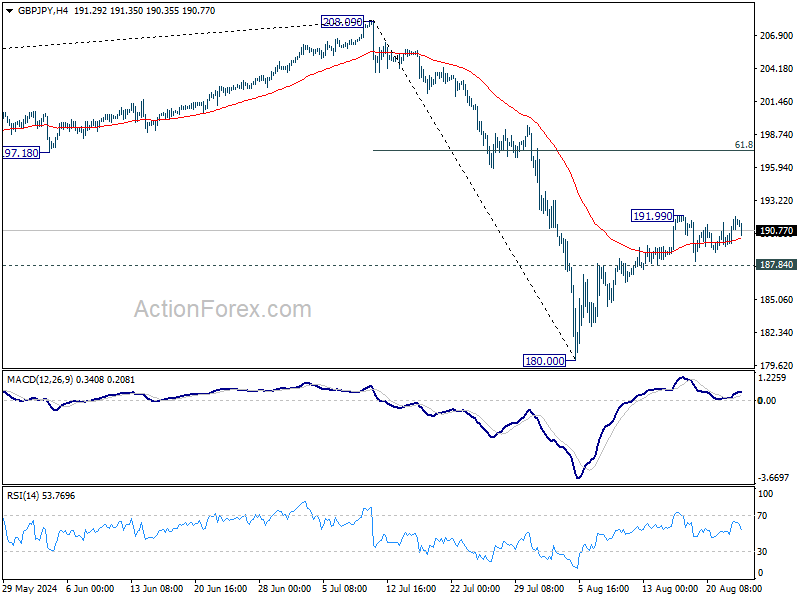

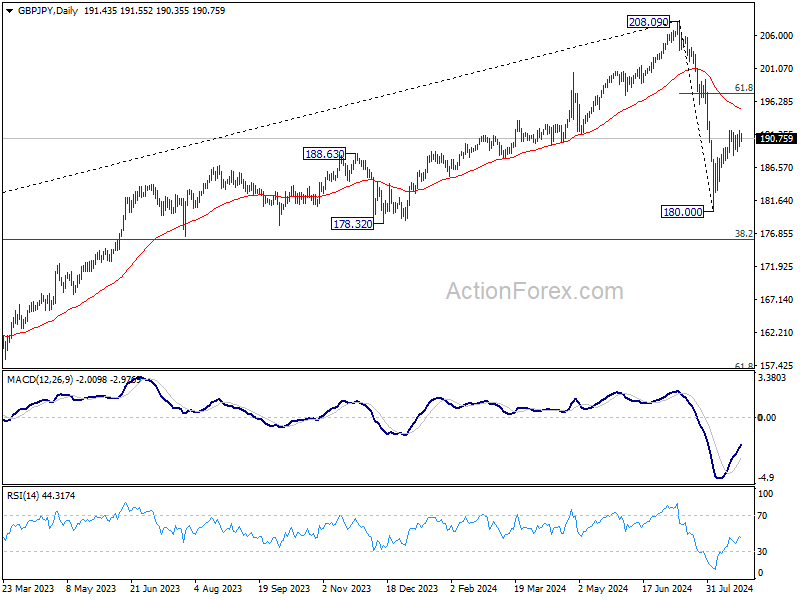

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.06; (P) 191.00; (R1) 192.46; More...

Intraday bias in GBP/JPY remains neutral as consolidation from 191.99 is extending. On the upside, above 191.99 will resume the rally from 180.00, and target 61.8% retracement of 208.09 to 180.00 at 197.35, as the second leg of the corrective pattern from 208.09. On the downside, however, firm break of 187.84 support will argue that rebound from 180.00 has completed, and turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

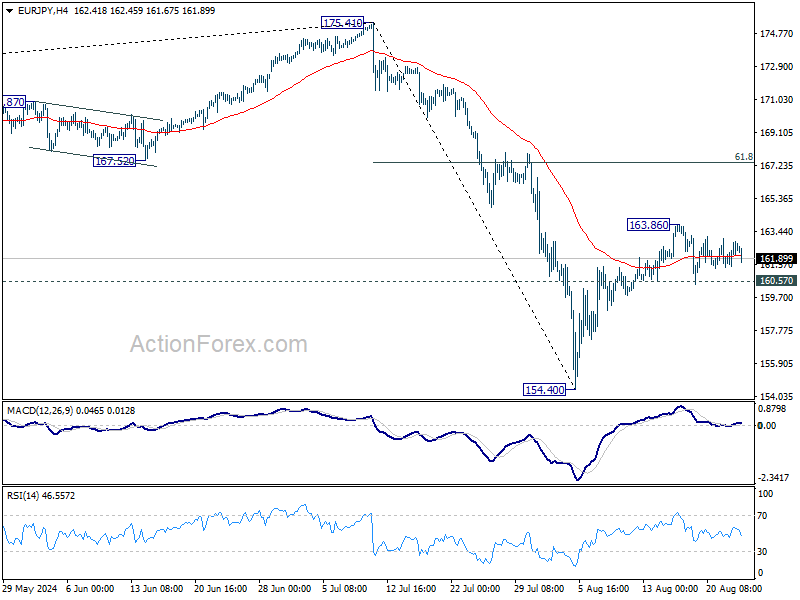

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.69; (P) 162.36; (R1) 163.24; More....

Intraday bias in EUR/JPY stays neutral as consolidation from 163.86 continues. On the upside, break of 163.86 will resume the rise from 154.40 and target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 160.57 support will suggest that the rebound from 154.40 has completed, and turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

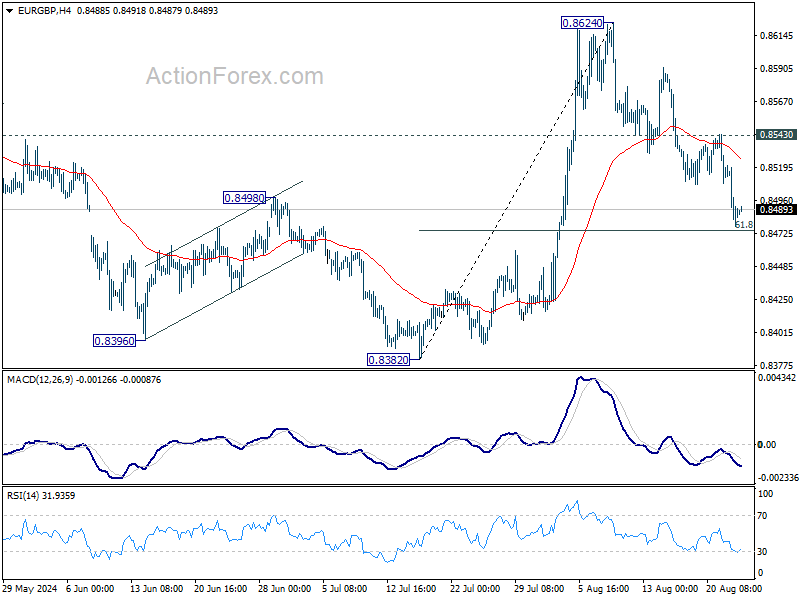

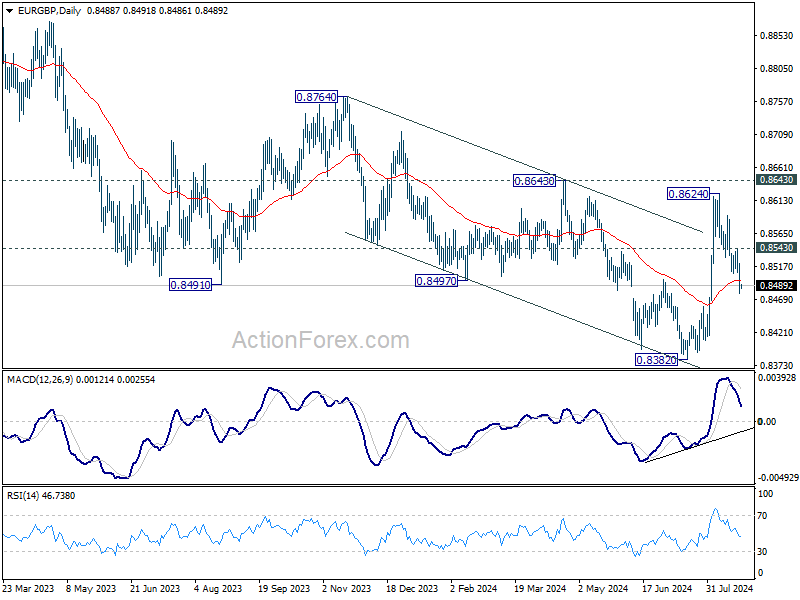

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8470; (P) 0.8496; (R1) 0.8515; More....

Intraday bias in EUR/GBP remains on the downside as fall from 0.8624 is in progress. Firm break of 61.8% retracement of 0.8382 to 0.8624 at 0.8474. will argue that recent down trend is ready to resume through 0.8382 low. For now, risk will stay on the downside as long as 0.8543 minor resistance holds, in case of recovery.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage. However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

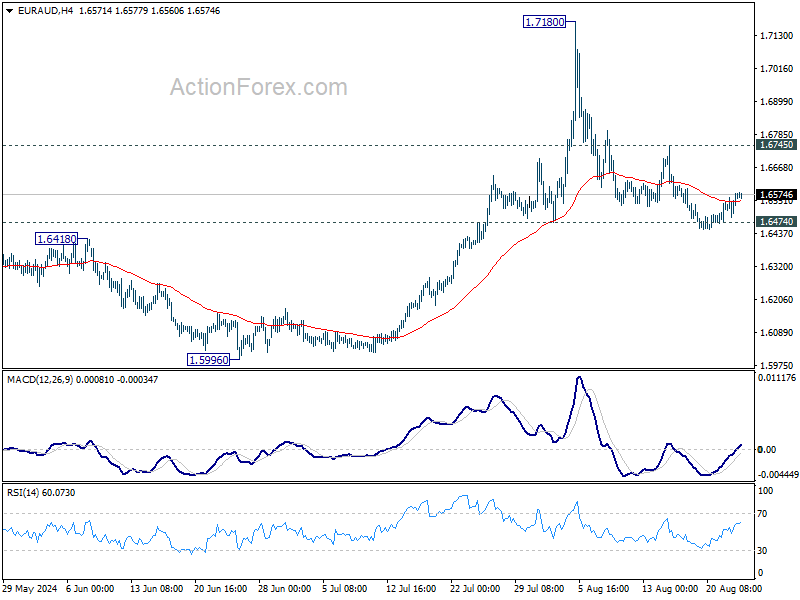

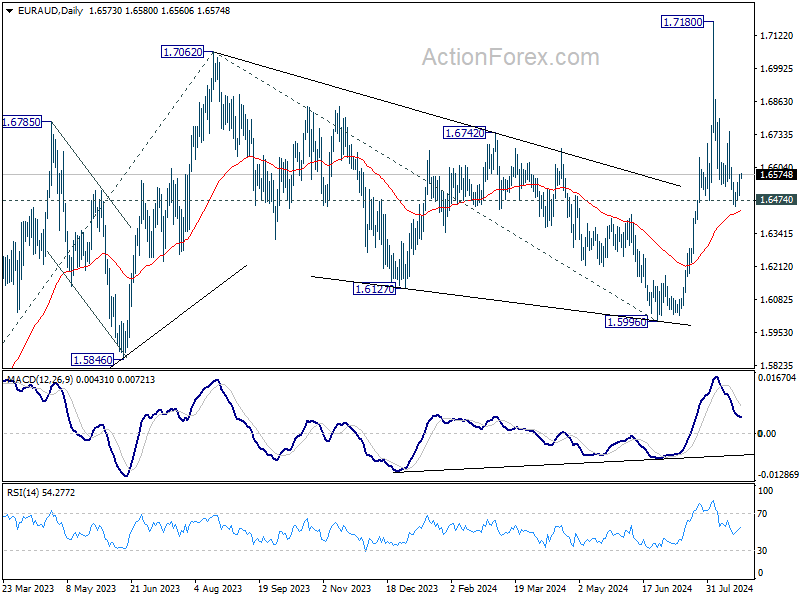

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6516; (P) 1.6548; (R1) 1.6602; More...

Intraday bias in EUR/AUD remains neutral for the moment. Rise from 1.596 is still in favor to continue with 1.6474 support intact. On the upside, break of 1.6745 resistance will suggest that pullback from 1.7180 has completed, and retain near term bullishness. Further rise should then be seen back to retest 1.7180 high. However, decisive break of 1.6474 will argue that rise from 1.5996 has completed, and dampen the larger bullish view.

In the bigger picture, corrective fall from 1.7062 medium term top should have completed at 1.5996. Larger up trend from 1.4281 (2022 low) is resuming. Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. This will now remain the favored case as long as 1.6474 support holds. However, decisive break of 1.6474 will argue that EUR/AUD is still engaging in medium term range trading.

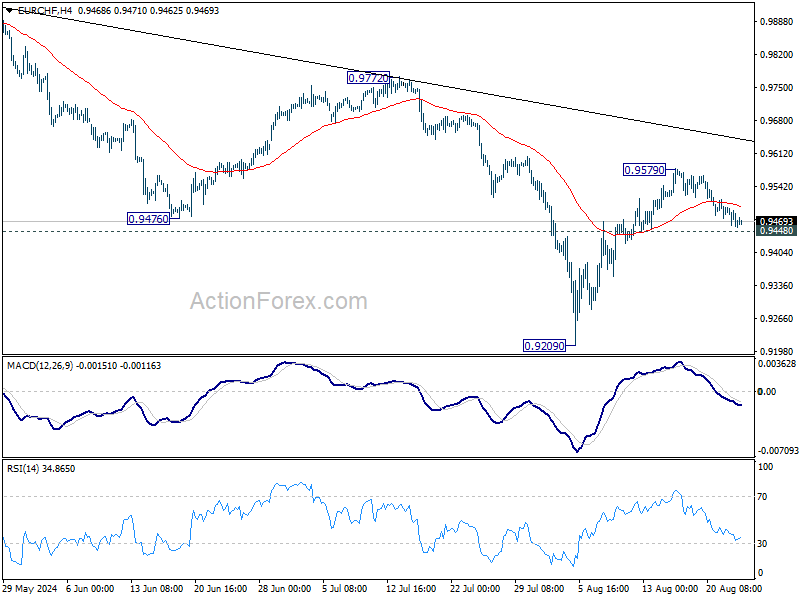

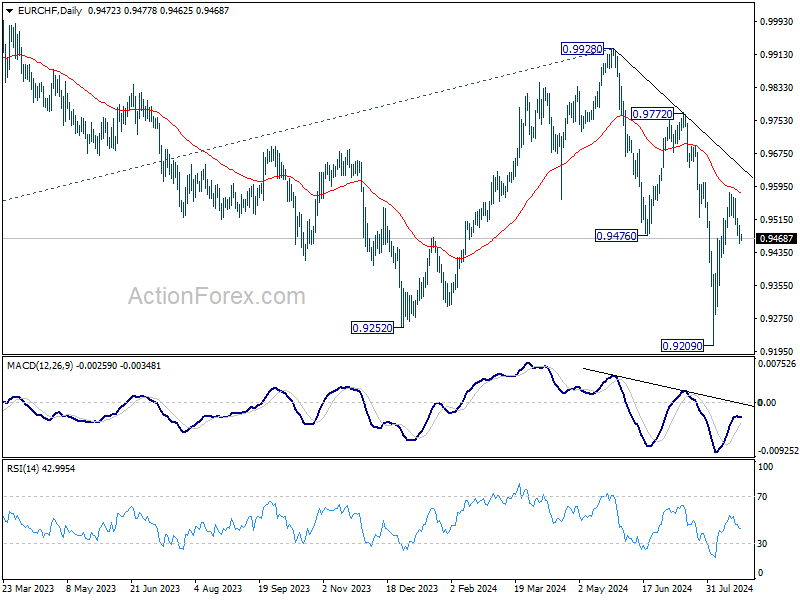

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9448; (P) 0.9479; (R1) 0.9501; More....

Intraday bias in EUR/CHF remains neutral and another rally is still in favor with 0.9448 support intact. On the upside, sustained break of 55 D EMA (now at 0.9576) will pave the way back to 0.9972/0.9928 resistance zone. However, decisive break of 0.9448 will suggest rejection by 55 D EMA, and turn bias back to the downside for 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

BoJ’s Ueda ready to scale back easing despite market instability

In a special parliamentary session today, BoJ Governor Kazuo Ueda reiterated the central bank's stance to its current monetary policy, even amidst recent market volatility. He emphasized that there is "no change to our basic stance to adjust the degree of monetary easing" should economic and price trends align with its forecasts.

Addressing concerns over the market turbulence observed in early August, Ueda attributed the instability to rising fears of a US recession, driven by weaker-than-expected economic data. He also noted that BoJ’s interest rate hike in July had triggered a sharp reversal in the "one-sided Yen falls".

He stressed that BoJ would continue to monitor market movements closely, recognizing their potential impact on the central bank's growth and price forecasts.

"Markets at home and abroad remain unstable, so we will be highly vigilant to market developments for the time being," Ueda remarked.

New Zealand retail sales volume falls -1.2% qoq in Q2

New Zealand's retail sales volume fell -1.2% qoq in Q2, , well below the expected -0.1% drop. Retail sales value also decreased by -1.3% qoq. Notably, 11 out of 15 retail industries reported lower sales volumes compared to the previous quarter.

Total volume of retail sales per person fell by -1.5%, marking the tenth consecutive quarter of decline after adjustments for seasonal effects and price inflation.

Ricky Ho, Business Financial Statistics Manager, highlighted the severity of this trend, noting, "Retail sale volumes per person have been falling for the last two-and-a-half years. The last time we saw several quarters of consistent falls was between 2007 and 2009, which coincided with the global financial crisis."