Sample Category Title

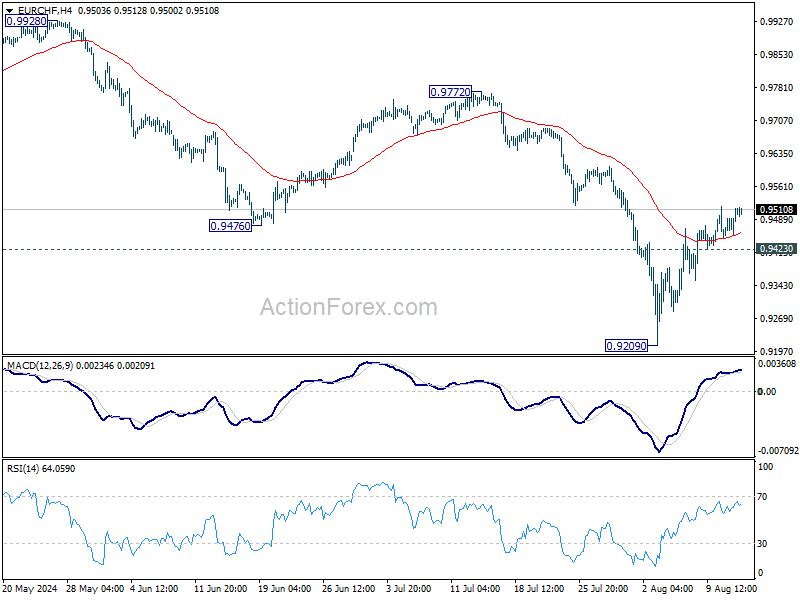

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9470; (P) 0.9492; (R1) 0.9529; More....

Intraday bias in EUR/CHF remains on the upside as rebound from 0.9209 short term bottom is in progress. Further rise should be seen to 55 D EMA (now at 0.9594). ON the downside, below 0.9423 minor support will turn intraday bias neutral first.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

More Benign Inflation Suggests BoE’s Close Call to Cut Right

Markets

Markets rallied in the wake of yesterday’s benign July producer price inflation (0.1% M/M for headline and 0% for core). Stock markets extended their comeback after last Monday’s melt down with key US gauges adding 1% (Dow) to 2.4% (Nasdaq). US Treasuries rallied as well, with investors piling up on bets that the Fed will start its cutting cycle with a 50 bps rate cut rather than a 25 bps move. A cumulative 100 bps of rate cuts is discounted at the US central banks’ remaining three policy meetings this year. Though we don’t fight current sentiment, it’s fair to say that no Fed governor talked about a potential 50 bps move so far. On the contrary. Atlanta Fed Bostic (voter) yesterday indicated that he's looking for a little more data before supporting a rate cut. For now, he sticks with his timing of a first move only by year-end. “We want to be absolutely sure. It would be really bad if we started cutting rates and then had to turn around and raise them again.” He adds that he is definitely concerned by the rise joblessness but points out that it is more due to a larger supply of workers rather than a slump in demand. Markets ignored the Bostic comments. The PPI rally eventually pushed US yields 4.2 bps (30-yr) to 8.7 bps (2-yr) lower. German Bund yields lost 3.2 bps (30-yr) to 5.2 bps (2-yr). EUR/USD in first instance dipped from 1.0940 to 1.0920 on a very weak German ZEW investor survey before the pair rebounded to just below 1.10 driven by USD weakness. Today risks becoming a repeat of yesterday as US July consumer prices line up. Consensus expects 0.2% M/M increases for both headline and core CPI gauges with the Y/Y print stabilizing at 3% and dipping from 3.3% to 3.2% respectively. Yesterday’s solid UK labour market update is followed by lower than expected July inflation figures. Headline CPI fell by 0.2% M/M (vs -0.1% M/M) with the annual figure rising to 2.2% from 2% (vs 2.3% forecast). Core CPI slowed to 0.1% M/M and 3.3% Y/Y (from 3.5% Y/Y). The more benign inflation print suggests the BoE’s close call to cut its policy rate by 25 bps early August was the right one with follow-up action becoming very likely. EUR/GBP spikes from 0.8540 to 0.8570.

News & Views

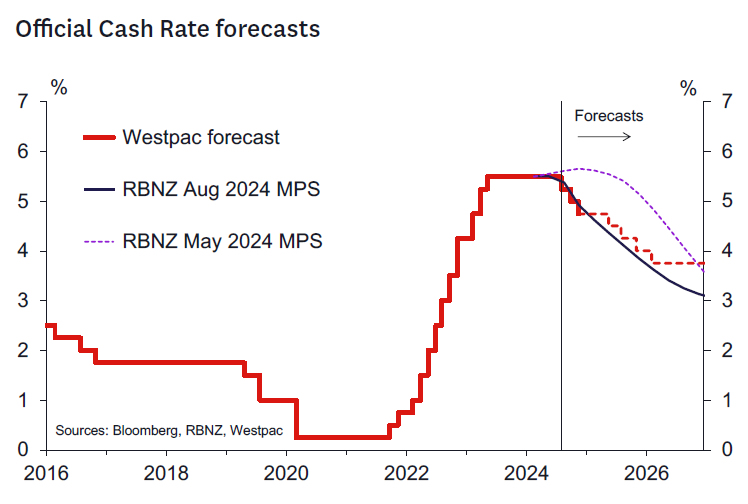

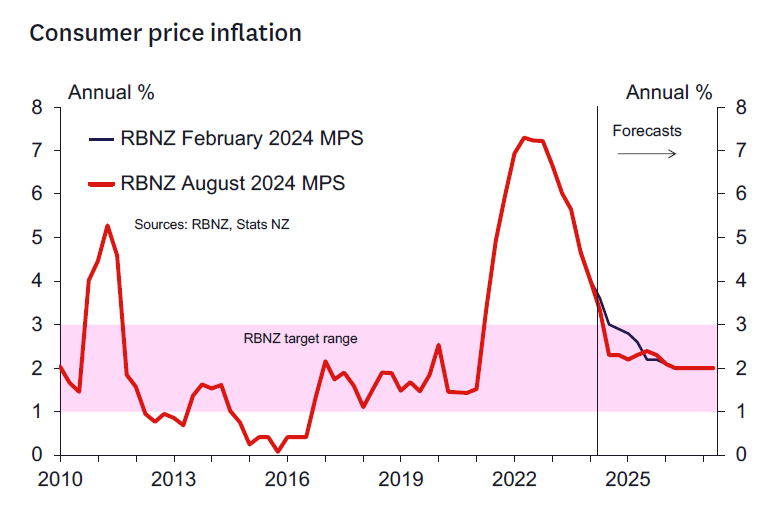

The Reserve Bank of New Zealand lowered its policy rate by 25 bps to 5.25%. It was the first cut since hitting the 5.5% peak rate in May of last year. Markets were split in the run-up to the meeting, attaching a 1/3 probability to an unchanged policy rate scenario. Updated projections show a clear intentions to trim the policy rate further this year, unlike previous May projections which hinted at a potential final rate hike. The OCR rate is set to average 4.92% in Q4 2024 (from 5.65%), 3.85% in Q4 2025 (from 5.14%) and 3.13% in Q4 2026 (from 3.7%). The RBNZ continues to see a 3% policy rate at the end of the forecasting horizon. In its policy statement, the MPC for the first time indicates that annual CPI is returning to within the 1%-3% target band. Surveyed inflation expectations, firms’ pricing behavior, headline inflation, and a variety of core inflation measures are moving consistent with low and stable inflation. Services inflation remains elevated but is also expected to continue to decline, both at home and abroad, in line with increased spare economic capacity. Updated annual CPI forecasts show a 2.3%-2.3%-2% path for the 2024-2026 period from 2.9%-2.2%-2% in May. In the meantime, economic growth remains below trend with a broad range of indicators suggesting that the economy is contracting faster than anticipated. On top, further downside risks to output and employment have become more apparent. At the press conference, RBNZ governor Orr indicated that the MPC contemplated to option of a 50 bps rate cut but eventually settled on a low-risk start to the easing cycle as they feel in a strong position to move calmly. NZD swap rates dropped by 5 bps (30-yr) to 11 bps (2-yr) after the decision with NZD money markets discounting a cumulative 75 bps of additional policy rate cuts at this year’s remaining two meetings. The kiwi dollar reversed yesterday’s gains, dropping back from 0.6080 to 0.60.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU data rolled in, dragging the long end of the curve down. After breaking below 2.34%-2.4% eyes now turn to 2.12-2.16%.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is continuing to move better in to balance. There was no pushback against market pricing back then (75 bps cuts in 2024, 100 bps in 2025). The pivot weakened the technical picture in US yields with another batch of weak eco data pushing the 10-yr sub 4%.

EUR/USD

EUR/USD tested the topside of the 1.06-1.09 range as the dollar lost interest rate support at stealth pace. A September rate cut is highly likely and markets increase bets on future easing on incoming weak US data. The risk-off these data trigger (sharper than expected slowdown?) offset the interest rate losses for USD. EUR/USD is moving south within the 1.07-1.09 range.

EUR/GBP

The Bank of England delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually and on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Risk-off proved a more important driver of GBP recently. We may see a return to the 0.85-0.86 sideways trading range that dominated 2024H1.

Three Times CPI on the Menu

In focus today

Today we get CPI numbers out of the US, UK, and Sweden.

In the US, we expect both headline and core CPI to come in at 0.2% m/m seasonally adjusted. The release is the second to last before the next FOMC meeting in September, and the Fed will undoubtedly keep close watch of the figures. The inflation data are released at 14.30 CET.

In Sweden, we get July inflation data at 8.00 CET. We expect July inflation to continue to print below the Riksbank's current inflation forecast as per the June Monetary Policy Report (MPR), with our forecasts of CPIF at 1.4% y/y and CPIF excl. Energy at 2.0% y/y being 0.4 p.p. and 0.2p.p. below the MPR, respectively.

We expect CPIF excl. Energy to print below 2.0% for the remainder of the year, which adds pressure on the Riksbank to continue cutting its policy rate. Today's figure will be important input ahead of next week's meeting, where markets are pricing 28bp of cuts, whereas we forecast a 25bp cut down to 3.50%. After that, we expect two more cuts for 2024 but note that markets are discounting 25bp cuts at each remaining meeting this year (September, November and December).

In the UK CPI inflation is due at 8.00 CET, where analysts expect headline to come in at 2.3% y/y (prior 2.0% y/y), whereas core inflation is expected to stand at 3.4% y/y (prior 3.5% y/y).

Overnight the Q2 Japanese national accounts will be released. It shall be interesting to see if growth has come back on track following three weak quarters. Preliminary data suggests it has, although private spending has likely remained weak.

Economic and market news

What happened yesterday

In the US, yields across the curve dropped and equities gained with the technology heavy Nasdaq leading the way, as markets viewed a softer-than-expected PPI print as dovish ahead of today's CPI print.

Market pricing for the coming September FOMC meeting also changed slightly, with markets now seeing a marginally larger probability of a 50bp cut in September than a 25bp cut. However, it is worth noting, that pricing has been very volatile lately given last week's surge in recession-fears.

What happened overnight

The Reserve Bank of New Zealand cut its cash rate by 25bp to 5.25%. Market pricing was pointing towards a cut, whereas consensus amongst analysts had been more divided and leaning towards an unchanged cash rate decision. As such the New Zealand dollar is trading lower this morning against the US dollar (NZD/USD), down around 1% at 0.602.

In Japan, Prime Minister Fumio Kishida announced he would step down, as he will not seek re-election this September as president of the Liberal Democratic Party (LDP). As the LDP is by far the dominant party in the current two-party coalition government, the next leader of the party looks set to become the country's next Prime Minister.

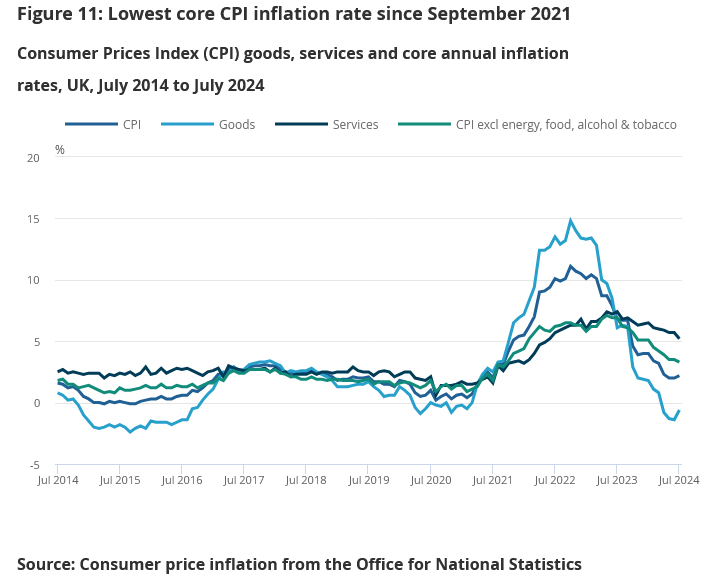

UK CPI rises to 2.2% in Jul, core down to 3.3%, both below expectations

UK CPI rose from 2.0% yoy to 2.2% yoy in July, below expectation of 2.3% yoy. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.5% yoy to 3.3% yoy, below expectation of 3.4% yoy. Core CPI reading was the lowest since September 2021.

CPI goods annual rate rose from -1.4% yoy to negative 0.6% yoy. CPI services annual rate fell from 5.7% yoy to 5.2% yoy.

On a monthly basis, CPI fell by -0.2% mom.

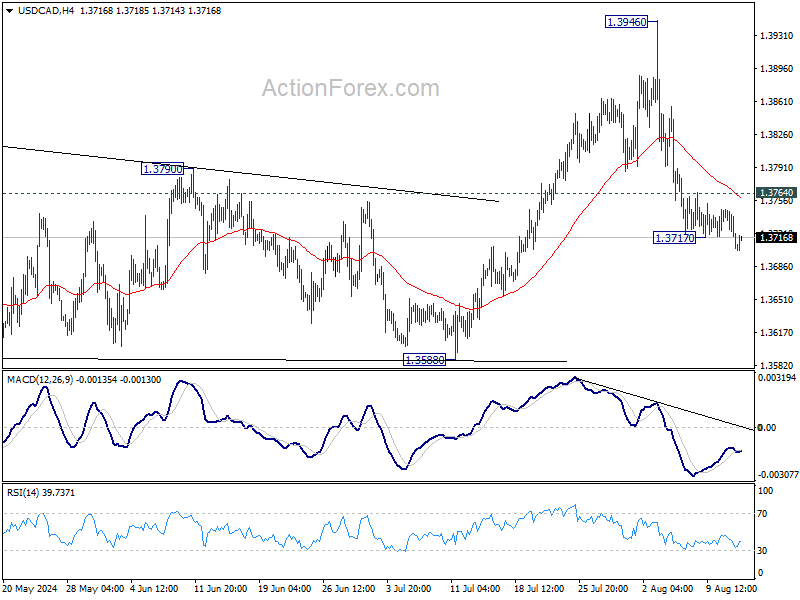

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3725; (P) 1.3737; (R1) 1.3754; More...

USD/CAD's fall from 1.3946 resumed after brief consolidations and intraday bias is back on the downside sustained trading below 55 D EMA (now at 1.3726) will dampen the original bullish view and bring deeper decline back towards 1.3588 support. On the upside, above 1.3764 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

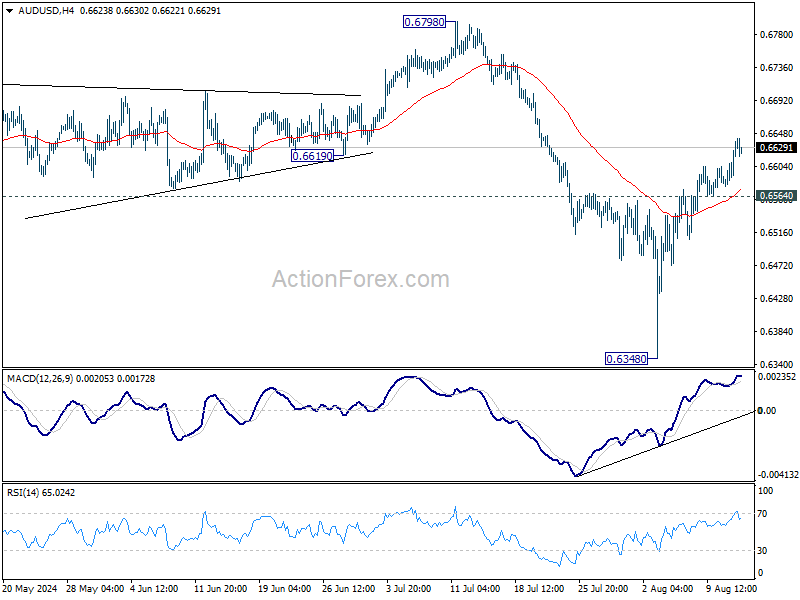

AUD/USD Daily Report

Daily Pivots: (S1) 0.6596; (P) 0.6617; (R1) 0.6655; More...

AUD/USD's rally from 0.6438 is still in progress and intraday bias stays on the upside. With break of 55 D EMA (now at 0.6612), next target is 0.6798 resistance. On the downside, below 0.6564 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. Meanwhile, break of 0.6798 will target upper side of the range at 0.7156.

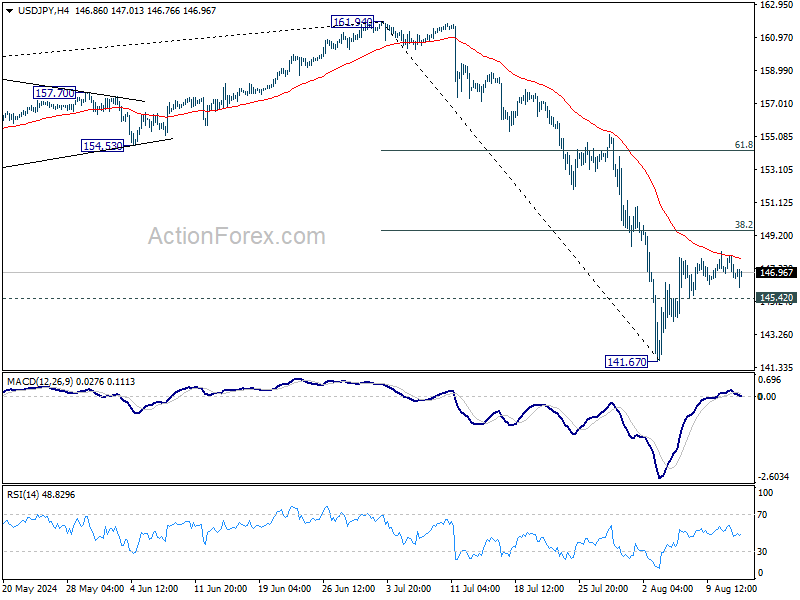

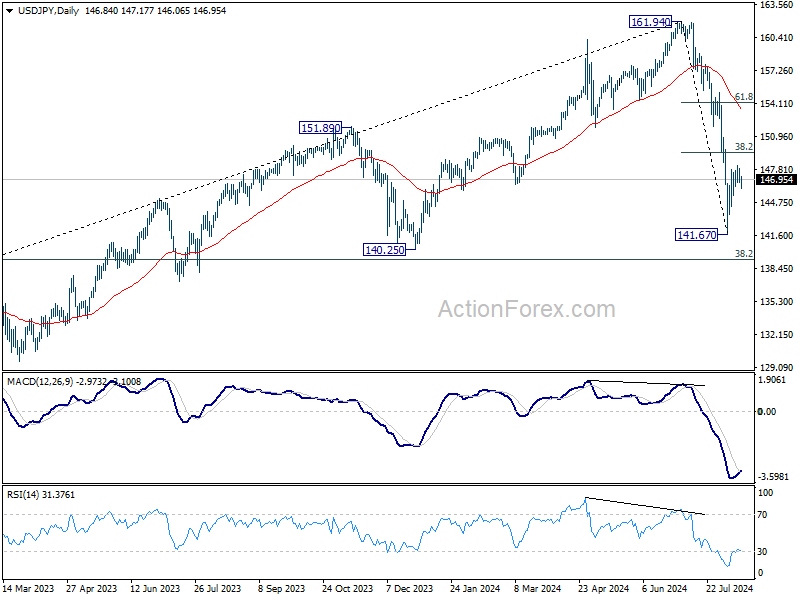

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.31; (P) 147.13; (R1) 147.66; More...

Intraday bias in USD/JPY remains neutral for the moment. Outlook stays bearish with 38.2% retracement of 161.94 to 141.67 at 149.41 intact and intraday bias stays neutral. Below 145.42 minor support will turn bias to the downside for 141.67. Break there will resume the fall from 161.94 to 140.25 support next. Nevertheless, decisive break of 149.41 will bring stronger rally to 61.8% retracement at 154.19, even as a corrective move.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.77) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

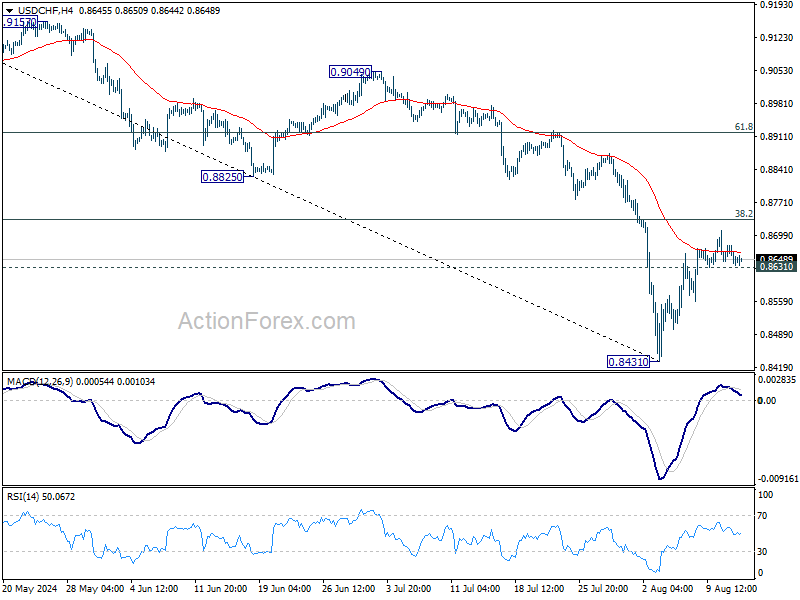

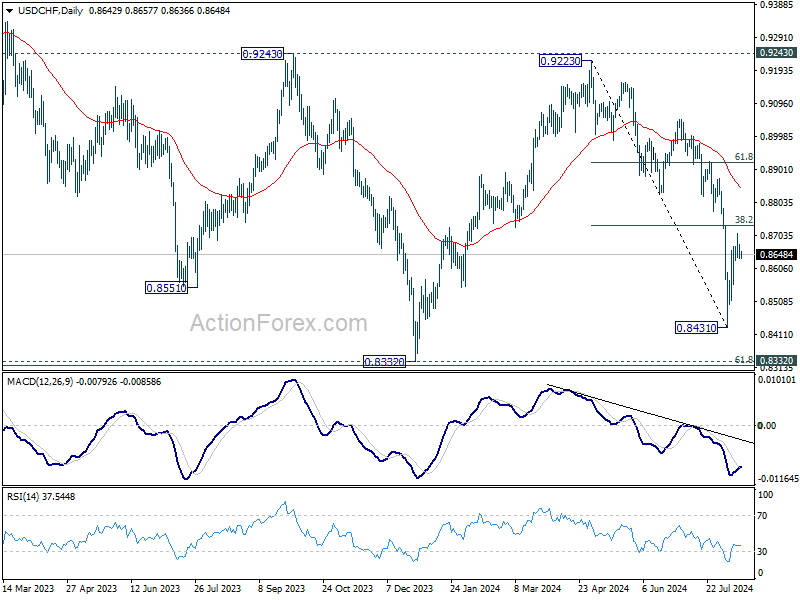

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8630; (P) 0.8655; (R1) 0.8673; More….

Intraday bias in USD/CHF stays neutral and outlook remains bearish with 38.2% retracement of 0.9223 to 0.8431 at 0.8734 intact. On the downside, below 0.8631 minor support will bring retest of 0.8431 first. Break there will resume the fall from 0.9223 to 0.8332 low. Nevertheless, firm break of 0.8734 will bring stronger rally to 61.8% retracement at 0.8920, even as a corrective move.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

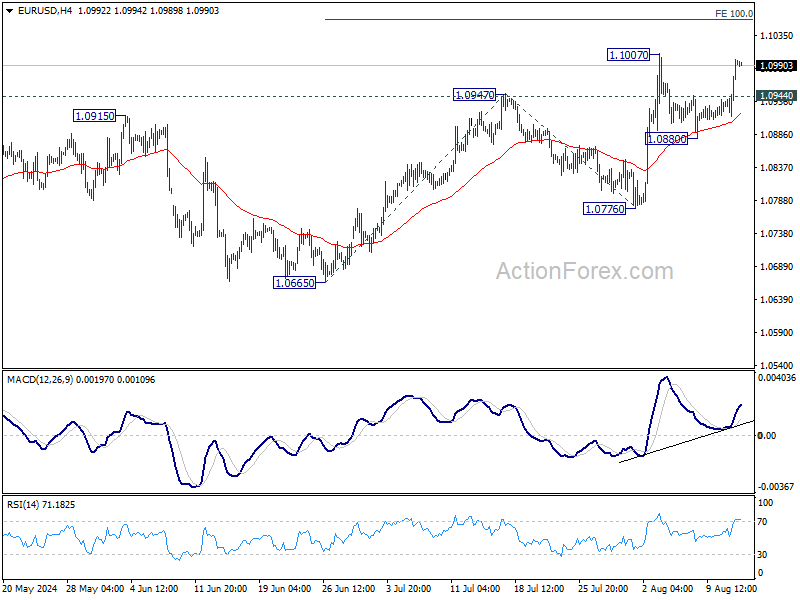

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0938; (P) 1.0969; (R1) 1.1024; More.....

EUR/USD's break of 1.0944 minor resistance suggests that pull back from 1.1007 has completed at 1.0880 already. Intraday bias is back on the upside for 1.1007. Firm break there will resume larger rise from 1.0665. Next target is 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1056. For now, outlook will stay bullish as long as 1.0880 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

RBNZ August 2024 MPS Review: Ready… Steady… Go!

- The RBNZ cut the OCR to 5.25% at its August policy meeting by unanimous decision.

- We think the RBNZ only seriously considered the option of cutting the OCR by 25bps at this point. The Governor noted that there are further meetings this year where further adjustments can be made.

- The revised projections lowered the OCR track significantly. The track implies that the next easing will occur at the October Monetary Policy Review, and a total of 75bp of cuts are forecast by end 2024.

- The track implies the RBNZ's monetary policy strategy is to more quickly ease policy over the next 6-12 months. The RBNZ aims to reach neutral OCR levels of around 3% by 2027 as previously expected – but reaches there more quickly.

- The RBNZ's near-term forecasts for economic growth have been revised down significantly. A wider output gap and looser labour market gives them confidence that inflation will ultimately fall.

- Inflation is forecast to fall back inside the 1-3% band in the September quarter of this year and is still not projected to return to 2% until Q2 2026.

- The RBNZ assesses the risk profile for inflation as balanced – and now two sided. We think the risk profile is decidedly to the upside for non-tradables inflation pressures.

- Today's RBNZ update leaves us comfortable with our forecast of two further 25bp cuts in October and November. We will review our forecasts beyond then in coming days.

Key take out: OCR cut 25bps and further easing seems likely this year

The RBNZ unexpectedly cut the OCR to 5.25%. The decision to cut by 25bps today was reached by consensus and so no vote was taken.

As widely expected, the RBNZ's projected track for the OCR was revised significantly lower from that seen in the May MPS.

- The projected average OCR in Q4 this year was revised down 73bps to 4.92%, at face value implying three 25bps rate cuts by the end of this year.

- The projected OCR for Q4 2025 was revised down 129bps to 3.85%, implying a further around 100 bps of rate cuts next year.

- The forecast for Q4 2026 was revised down 57bps to 3.12%, implying around three 25bps cuts in that year.

- The RBNZ assumes the OCR reaches around 3% in Q3 2027 (the final quarter of the forecast).

According to the RBNZ, the most important driver of the revised view were a significant downgrade in the near-term growth outlook (as we had foreshadowed in our recent Economic Overview). This weaker growth profile and resultant weaker output gap has increased the MPC's confidence that inflation will continue to fall to the mid-point of the 1-3% target range over a similar timeframe as previously expected. Indications of weaker price intentions and inflation expectations have further buttressed the RBNZ's confidence that domestic inflation pressures will ultimately normalize.

Risks

We think the RBNZ's revised growth forecasts are well balanced in the short term. The RBNZ has included a relatively firm bounce back in the economy over 2025 compared to our forecasts. Having said that, the much easier interest rate profile compared to our more conservative OCR forecast assumptions explains some of that relative optimism. Interestingly, the RBNZ does not see the front-loaded easing profile impacting on house prices significantly in the next year. There could be some upside risks there in coming quarters given the generally strong inverse relationship between interest rates and house prices.

The risks around their short-term inflation projections also look well balanced, although from early 2025 the RBNZ has an optimistic view on how quickly non-tradable inflation will fall. We are not so sure about that, and it will be up to the data to confirm this is going to occur.

Westpac's OCR call

We remain comfortable with the previous forecast of two further 25 bp cuts to the OCR over the balance of the year (from the lower 5.25% starting point). Hence, we expect the OCR to end 2024 at 4.75%. Beyond that we will make a full assessment in coming days.

CPI inflation to fall below 3% sooner than expected

Underlying the downward revision to the RBNZ's interest rate projection is a better contained outlook for inflation. Inflation surprised the RBNZ to the downside in the June quarter and it's now expected to fall below 3% in the September quarter. That's sooner than the RBNZ had assumed in May, and in line with our own forecasts for inflation over the remainder of this year.

Further ahead, the RBNZ is sounding increasingly confident that inflation will settle close to the 2% midpoint of their target band (though this still isn't expected to be reached until mid-2026). We're also expecting to see inflation trending back towards 2%. However, there are some key areas where we think the RBNZ might be surprised.

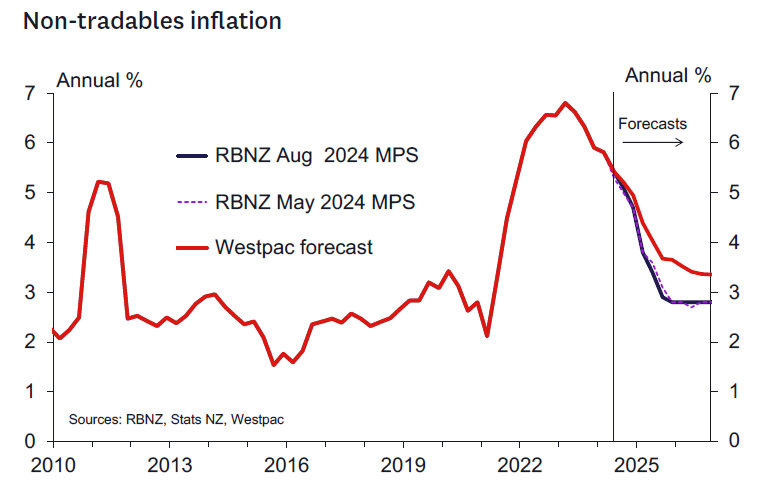

First, and most importantly, is the 'stickiness' in domestic inflation. The RBNZ expects that domestic inflation will drop back sharply over 2025 as capacity pressures ease. They've also allowed for a faster easing in price setting behaviour (i.e. inflation expectations) and more moderate increases in the prices for items like insurance. We're less optimistic about how quickly domestic inflation will ease and expect that it will continue to surprise the RBNZ to the upside (as it has done over the past year).

Balanced against that risk of persistent domestic inflation, imported inflation (i.e. tradables) has fallen well short of the RBNZ's forecasts. The RBNZ is projecting a reacceleration in imported inflation next year after some sharp falls recently. In contrast, we expect that it will remain soft for some time. That will help to keep overall inflation and inflation expectations contained.

Near-term GDP growth forecasts revised down

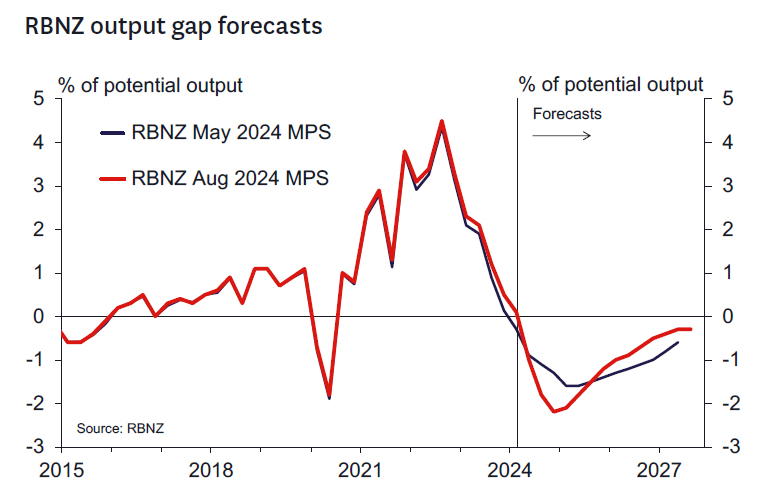

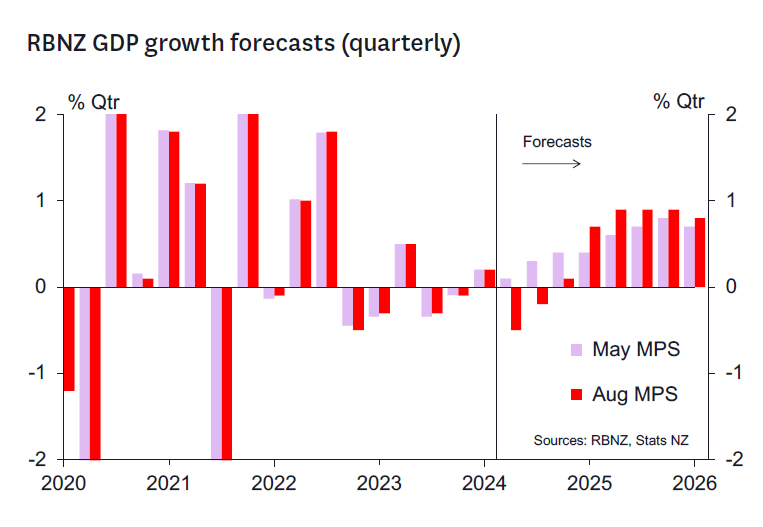

A key driver of today's decision was a sharply downgraded view of the near-term outlook for activity, with crucial implications for the labour market (see below) and the output gap. Indeed, the RBNZ's forecasts for GDP growth in Q2 and Q3 were revised down by a cumulative 1.1ppts and at -0.5%q/q and -0.2%q/q respectively are nearly identical to the estimates that we included in our recent updated Economic Overview. As a result, while the RBNZ has again revised down its estimate of the economy's potential growth rate, the RBNZ now expects the output gap to turn more negative over the coming year, troughing at -2.2% of GDP in Q4 this year, rather than a trough of -1.6% of GDP in Q1 next year.

Given the much easier monetary conditions included in these projections, the RBNZ's forecasts also build in a much stronger cyclical rebound in activity next year. Indeed, the RBNZ now expects GDP to grow 3.3% over the 2025 calendar year up from 2.4% in the May MPS. As a result, the output gap is expected to shrink to -1.2% of GDP by the end of next year, which is slightly smaller than the -1.4% of GDP output gap projected in the May MPS. It is worth noting that this rebound is quite a bit stronger than forecast in our recent Economic Overview, albeit with our forecasts based on firmer monetary conditions than implied by the RBNZ's revised projections.

The RBNZ's labour market view

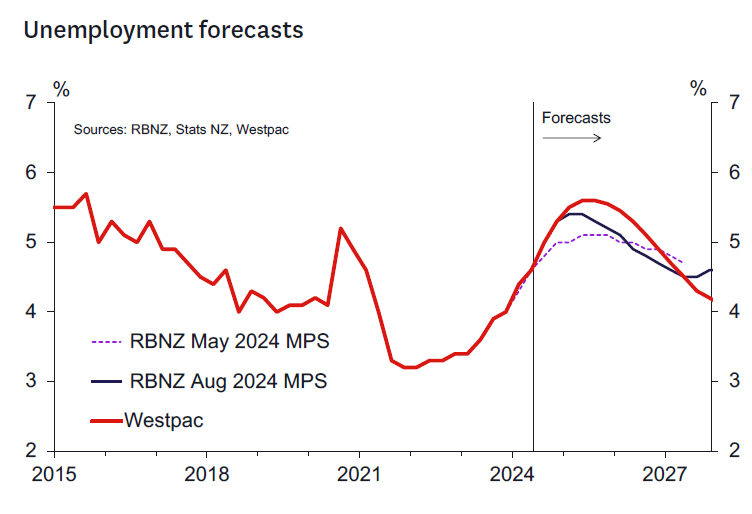

The RBNZ acknowledged the softening in the labour market, particularly in the near term – the sharp slowdown in job vacancies and the fall in filled jobs in the last few months were among the high-frequency activity indicators that the RBNZ highlighted in its Statement. They expect the unemployment rate to rise further in the coming quarters, reaching a peak of 5.4% in early 2025. That's higher than their previous forecast of a 5.1% peak, though it's within the range of forecasts that the RBNZ has produced over the last couple of years. Along with that increasing slack in the labour market, the RBNZ expects a faster moderation in wage growth.

RBNZ takes relatively sanguine view on impact of Budget 2024

The August MPS is the first to be released since Budget 2024 was unveiled in late May, and so the first to fully incorporate an estimate of the full impact of the new Government's policies. The RBNZ's view on the impact of fiscal policy is set out on Box B of the MPS. The RBNZ notes that spending reductions in the public sector will reduce inflationary pressure, and income tax threshold changes will increase inflationary pressure. A fiscal multiplier of 0.5 is assumed to apply to both spending reductions and tax revenue reductions – in line with estimates derived from past research in New Zealand, but this assumption is recognised as a source of uncertainty. The RBNZ also noted that tax cuts can also increase labour supply and affect wage bargaining, which may partially offset the inflationary pressure from higher spending.

Given that the May MPS had already implicitly accounted for a share of the lower government spending, the RBNZ's updated assumptions about fiscal policy have added slightly to medium-term inflationary pressure. However, those effects have clearly been swamped by other economic developments. Overall, the RBNZ concluded that the net impact for monetary policy is expected to be small and is highly uncertain. Over coming months, the RBNZ will refine its estimates in light of the emerging data.

Key domestic data to watch ahead of the RBNZ's October Review

The next RBNZ policy review will take place on 9 October. In addition to any important economic or financial developments offshore, there are several domestic economic data releases that will have a significant bearing on the outcome of that meeting. The most important are:

- The Q2 GDP report (19 September): The outcome of this report will be compared to the RBNZ's estimate, with any deviation having implications for the RBNZ's estimate of the output gap and perhaps also its view on near-term growth momentum.

- The Q3 QSBO survey (1 October): The focus will be on indicators of spare capacity and cost/ inflation pressures. It will also be interesting to see if confidence, hiring and investment indicators are lifting from low levels as monetary conditions ease.

- Selected price indexes for July/August (15 August/12 September): These indexes will cast light on some of the most volatile components of the CPI and thus on the certainty that the Q3 CPI (16 October) will show inflation back inside the 1-3% target band.

- Employment indicators for July/August (28 August/30 September): Developments in the labour market will remain a key focus for the RBNZ and these indicators will provide insight into the likely outcome of the Q3 labour surveys (released 6 November).

- The August Electronic Card Transactions report (12 September): This release will capture the first month of retail spending since the personal tax cuts took effect.

In addition to the above, key monthly activity indicators such as the Business NZ manufacturing and services indexes and the ANZ Business Outlook survey will also be of interest.