Sample Category Title

Sunrise Market Commentary

Markets

A violent sell-off hit UK Gilts as local markets reopened following Monday’s Spring Bank Holiday. In a catch-up move to weakness in core bonds on Monday, UK yields jumped 9 to 10 bps across the curve. Contrary to the move in the EU and the US, the curve move was a parallel shift rather than bear flattening. The UK 30-yr yield hit its highest level since May 1998 (5.78%). The UK 10-yr yield moved back above 5% and came within 2 bps from the highest level since June 2008. This set-up suggests that Bank of England governor Bailey better avoids being too complacent on the need to tighten monetary policy in the face of looming inflation risks. Especially given the fragile political situation with the ruling Labour party set to lose big in tomorrow’s UK local elections. It might be the straw that breaks PM Starmer’s back while also raising questions around Chancellor Reeves’ authority to pursue fiscal discipline. Sterling didn’t suffer from rising UK risk premia with a new bullish shift in risk sentiment adding some counterweight.

Key European and US benchmarks gained 1-2% as oil prices erased Monday’s increase. Brent crude is back at where it started the week ($108/b). Markets took comfort from US comments that the ceasefire was still in place despite a day of clashes around Hormuz after US President Trump announced the start of “Project Freedom”. Iran’s foreign minister immediately labeled it “Project Deadlock”. The US didn’t walk its talk that any new Iranian violence would be met with great US fury. It’s also telling that President Trump after two days already said that he would pause the project to guide ships through the Straight, boasting “great progress” toward “a complete and final agreement with representatives in Iran”. The latter not being confirmed from the Iranian side. High-level talks between Iran and China suggest something might be brewing when US President Trump and Chinese President Xi Jinping meet next week.

Asian stock markets extend their rally this morning with South Korea significantly outperforming thanks to Samsung. The company hit the $1tn valuation mark on the memory chip boom. Japanese markets remain closed for holidays, but that didn’t stop officials from more FX interventions. They pushed USD/JPY from 158 to 155 as the current JPY-valuation remains out of line with fundamentals. As long as oil prices stay this high, we fear Japanese officials to fight an uphill battle. Today’s eco calendar contains the monthly ADP employment report. Weekly data suggest another solid outcome which could trigger more repositioning on US money markets. Since last week’s Fed meeting, they went from erring on the side of a rate cut as the next central bank move to erring on the side of a hike. The US quarterly refunding announcement might draw some attention too in light of huge and still rising US budget deficits. In line with the situation in the UK, watch out for any vulnerability at the (very) long end of the curve. The US 30-yr yield at the end of last week briefly moved beyond the psychological 5% barrier.

News & Views

South Korean inflation accelerated in April to 0.5% M/M and 2.6% Y/Y, the fastest pace since July 2024 (from 0.3% M/M and 2.2% Y/Y). Core inflation was unchanged at 2.2%. Transportation costs rose 3.4% M/M. Prices for recreation and culture added 1.5%. Food prices declined by 0.9% M/M to slow to 0.3% Y/Y. Inflationary tendencies were slowed by government measures to cap the rise in fuel prices. The Bank of Korea (BoK) indicated that it expects inflation to rise further in May as higher oil price might feed through to other products. Yesterday, the deputy governor of the BoK suggested that the combination of ongoing resilience in economic activity and higher inflation might cause it to consider raising rates. The BoK kept its policy rate unchanged at 2.5% since May 2025. It meets next on May 28.

Over the previous session, the NOK/SEK cross rate challenged the psychological parity barrier and touched the highest levels since end may 2024. The NOK outperformance over the SEK comes as both central banks will announce results of their regular policy meetings tomorrow. At its March meeting, the Norges Bank indicated that the inflation outlook might make It appropriate to raise the policy rate at one of the forthcoming meetings. Money markets see a 50% chance for a 25 bps move tomorrow, with a hike fully discounted by June. A high oil price also supports NOK outperformance. Regarding the Riksbank, expectations that it might give in to rate hike pressures are much more modest. The central bank at its previous meeting signaled that it expected the policy rate to stay at 1.75% for some time to come, even as uncertainty is high. This assessment was supported by modest March CPI figures. April CPI figures will be published today.

Flip Flop

The Project Freedom was paused, meaning that the US abandons the idea to escort ships out of the Strait of Hormuz – as the initiative didn’t fare well with Iran. And the lack of further escalation in the Middle East was enough to divert investors’ attention back to earnings. The rally that paused for a few hours resumed.

The S&P 500 and Nasdaq pushed to fresh record highs, while the Stoxx 600 rebounded from its 50-DMA. Gains were led by technology stocks on both sides of the Atlantic. VanEck’s Semiconductor ETF traded at a fresh record, ASML rebounded 3.5%, and Infineon Technologies, a German chipmaker and one of Europe’s largest semiconductor companies, rose more than 8% to a record high before announcing earnings.

Today, the Kospi index confirms that optimism with more than a 6.5% jump at the time of writing.

So the market mood now flip-flops between AI optimism and Middle East headlines, with geopolitical worries having a smaller and shorter-lived impact as investors become used to the war headlines. I believe there is a certain underpricing of the risks here, but the reality is that the perfect calm for entering a position doesn’t exist. We are either confronted with geopolitical crises, trade wars or high valuations.

Today, it’s a mixture of all three, yet the major indices are doing well, including EM. MSCI’s EM index also hit a record high yesterday. The stock rally itself is serving as a hedge against inflation, though the risk of a sharp reversal cannot be ruled out given the uncertainties. Oh well.

Trade, war and tech worries haven’t really shown up in earnings so far. More than 80% of S&P500 companies have reported better-than-expected revenue so far. In Europe, around 45% of Stoxx600 companies surpassed revenue expectations. The gap is certainly due to the differing tech exposure of the two continents.

Again yesterday, AMD delivered a strong earnings beat, with Q1 revenue rising 38% YoY to $10.3 billion and data-centre sales surging 57% thanks to booming AI infrastructure demand. The company also guided Q2 revenue above expectations, reinforcing optimism around its AI accelerator and server CPU businesses. The market reaction was equally positive: AMD shares jumped 16% in after-hours trading as investors cheered the strong AI-driven growth outlook and improving visibility on future demand.

Super Micro Computer also jumped around 18% in after-hours trading after delivering mixed results: earnings beat expectations comfortably, helped by improving margins and strong AI server demand, but revenue missed estimates as some customer deployments were delayed. The company nevertheless issued upbeat guidance for the current quarter, signalling confidence that AI infrastructure spending remains robust. Investors focused on the stronger profitability and guidance rather than the revenue miss, as confirmation of the strength of the renewed AI-led optimism.

So this morning, with no further escalation in the Middle East and falling oil prices, US and European futures point to a positive start.

That relief is also notable in the US dollar index, which is trading lower this morning against most major currencies. The EURUSD is pushing above the 1.17 mark, while the USDJPY eased back toward 155.

On the data front, US figures were mixed yesterday. ISM data pointed to softer activity in March, while job openings fell less than expected in March and new home sales rose compared with a month earlier. Today, eyes will be on the ADP report, where expectations are that the US economy may have added around 118K private jobs in April.

What’s interesting is that predictions diverge. On one hand, the thousands of job cuts announced by big (and smaller!) tech companies due to AI replacement weigh on estimates. On the other hand, these same companies are spending hundreds of billions of dollars building massive AI infrastructure that also creates jobs — but those investments don’t hit headlines as hard as Big Tech layoffs do. So the question is whether job losses are stronger or softer than the job gains. I guess we will see.

The way the market processes the news will certainly be impacted by the positive vibes of the moment. Softer-than-expected jobs data could revive Federal Reserve (Fed) dovishness, pull yields lower and support a further equity rally. Meanwhile, stronger-than-expected figures could confirm that the US economy is not doing that badly after all, cement optimism and push equities to fresh highs.

Given the market’s resilience to bad news and enthusiasm around good news, I certainly don’t see the bears taking the upper hand for now. But selloffs happen suddenly.

One interesting point, though: some analysts note that the positive reaction to earnings beats is smaller than the negative reaction to earnings misses. That is confirmation that valuations are high and US equities remain expensive.

The question is whether this optimism could spread to other markets. The answer is: it depends. Middle East tensions have clearly shifted capital flows toward technology names, both inside and outside the US. European and UK stocks lagged behind tech-heavy indices like the Kospi and Taiex. Rising energy costs initially hit Asian indices harder, but the negative impact on market sentiment tends to last longer in Europe.

Given investors’ appetite for hiding from the war under the tech roof, the underperformance of European indices will likely remain in play until there is more clarity in the Middle East and, ideally, a notable retreat in energy prices. Otherwise, European economies could also face higher interest rates alongside a slowing economic outlook — and for cyclical European indices, that is not good news.

Trump Pauses Hormuz Mission, Signalling Progress in Negotiations

In focus today

In Sweden, flash CPI figures are set for release, with a decline expected due to the VAT reduction on food from 12% to 6%. CPIF excluding energy is forecast to fall to 0.3% y/y, down from 1.1% in March, reflecting the tax impact. CPI and CPIF are affected in the same way, but high fuel prices keep CPIF at 1.2%. More indicators suggest rising prices, while tax effects may mask higher underlying inflation over the coming year.

In the US, ADP will release its monthly estimate of private-sector employment growth for May. Weekly 'pulse' estimates from ADP suggest a strong rebound in job growth during the reference period, despite ongoing uncertainties around energy supply.

In the euro area, the final services and composite PMI are revealed today. The preliminary composite PMI stood at 48.6, with the services sector acting as the main drag as its PMI fell further to 47.4. The manufacturing PMI, released on Monday, held steady at 52.7, matching the preliminary figure.

In Poland, the National Bank of Poland (NBP) is set to announce its policy rate decision, with consensus anticipating that the NBP base rate will remain unchanged at 3.75%.

Today at 10.00-10.30 CEST, we will host a webinar on the Strait of Hormuz closure and its implications for markets. Topics include the severity of the energy supply shock, prospects for recovery, and the broader economic impact.

Economic and market news

What happened overnight

In the US-Iran conflict, Iranian Foreign Minister Abbas Araghchi met with China's Foreign Minister Wang Yi in Beijing to discuss bilateral relations and regional developments, amid Iran's diplomatic efforts to rally international support. Meanwhile, Trump announced a temporary pause to "Project Freedom," a naval operation in the Strait of Hormuz, indicating a potential de-escalation. Oil prices declined following the announcement and continued to fall overnight, driven by expectations of progress toward a peace deal with Iran, as hinted by Trump. Trump's upcoming visit to China adds further complexity, given Beijing's close ties with Tehran and its economic reliance on oil transit through the strait.

What happened yesterday

In the US, March JOLTs and April ISM Services came in close to expectations, with limited market impact expected. JOLTs figures were mixed, as hiring increased to 5.6M while layoffs rose to 1.9M, and the job openings-to-unemployed ratio remained steady at 0.95, indicating little change in labour market balance over the past six months. ISM Services also delivered mixed signals, with unchanged prices, weaker new orders, and improved business activity and employment indices. Overall, the releases offer no clear directional signals.

In Switzerland, April CPI aligned with expectations, as headline inflation climbed to 0.6% y/y from 0.3% in March, driven by increased prices for petrol, diesel, and heating oil. Core inflation softened to 0.3% y/y, below the consensus forecast of 0.5%. With domestic inflation pressures remaining muted, this outcome is unlikely to influence the SNB's policy stance, and we anticipate the central bank will keep the policy rate unchanged at 0%.

Equities: Equities rebounded on Tuesday. S&P 500 0.8% and small cap Russell 2000 1.8%. Tech continued to lead the market, but preference shifted from software to semis. Intel, Qualcomm and Micron all surged, up 11-13%. Semi heavy Korea is surging 6% this morning (70% ytd, 180% LTM) and Shenzhen 2.5%, following the holiday yesterday. While Stoxx 600 gained 2% the last month, S&P 500 rallied 10%. Sector composition explains this underperformance, not energy prices alone.

So, tech continued in jaw dropping speed, with Asia and US the prime beneficiaries. However, general cyclicals also rebounded yesterday, along with small caps, following reassuring comments about the ceasefire from the US admin. Regional banks, materials and industrials were up between 1-2%. Stoxx 600 gained 0.7%

FI and FX: There was a modest rebound in the global bond market as the oil price declined yesterday. The truce between US and Iran seems to be holding up and the risk of an escalation seems to be diminished, and we have seen a combination of rising equity prices and decline in bond yields. Hence, the 30Y Treasury yield is trading around the 5% level. However, in UK government yields continue to increase given the higher energy costs as well as the political uncertainty with the upcoming local elections. Here the level for the 30Y government bond yield is at 5.78%, which is the highest level since 1998. The dollar has been range-trading around the 117-level versus the Euro and moved above the 157-level versus the JPY.

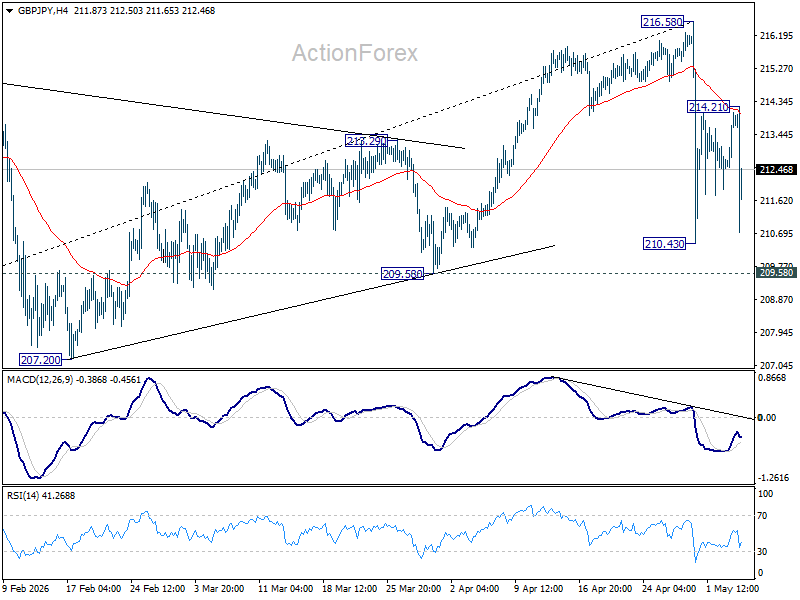

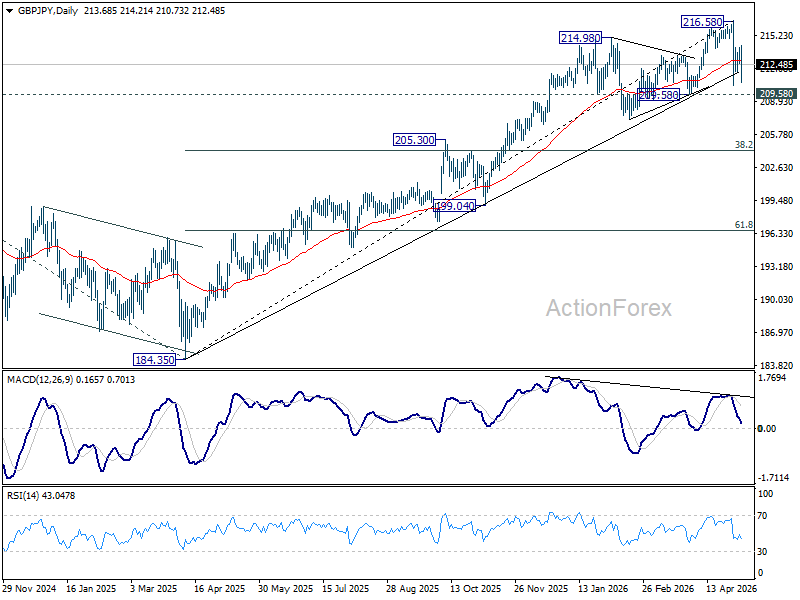

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.85; (P) 213.46; (R1) 214.39; More...

GBP/JPY fell sharply after rejection by 55 4H EMA but stays above 210.43. Intraday bias remains neutral first. Further decline is expected as long as 214.21 holds. Below 210.43 will target 209.58 support first. Break will target 38.2% retracement of 184.35 to 216.58 at 204.28.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.45) will argue that it's already in medium term down trend for 184.35 support.

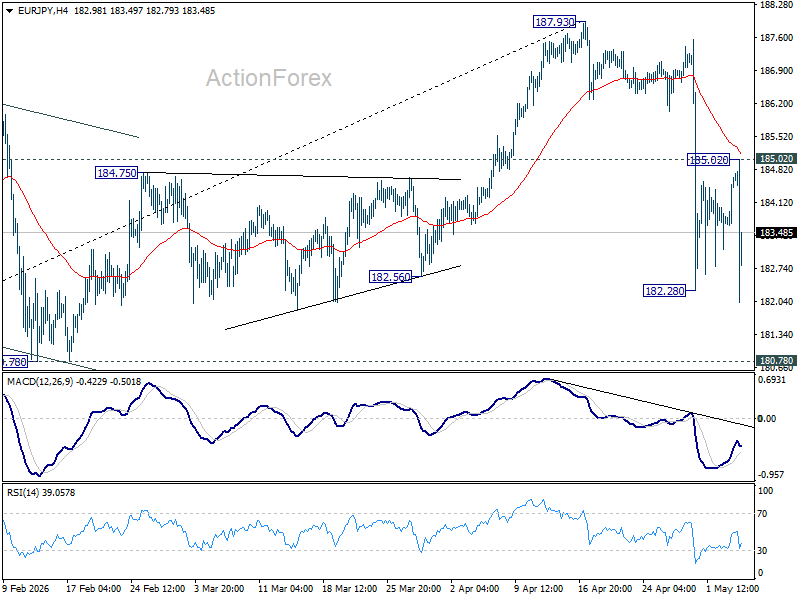

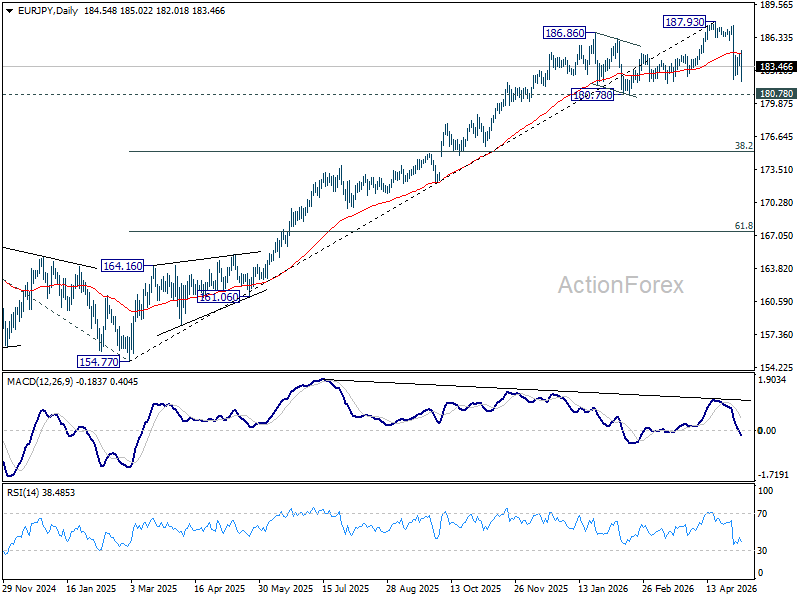

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.92; (P) 184.35; (R1) 185.04; More...

EUR/JPY's breach of 182.28 suggests that consolidation from there has completed at 185.02, and fall from 187.93 is resuming. Intraday bias is back on the downside for 180.78 support next. For now, risk will stay on the downside as long as 185.02 resistance holds, in case of recovery.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 177.76) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

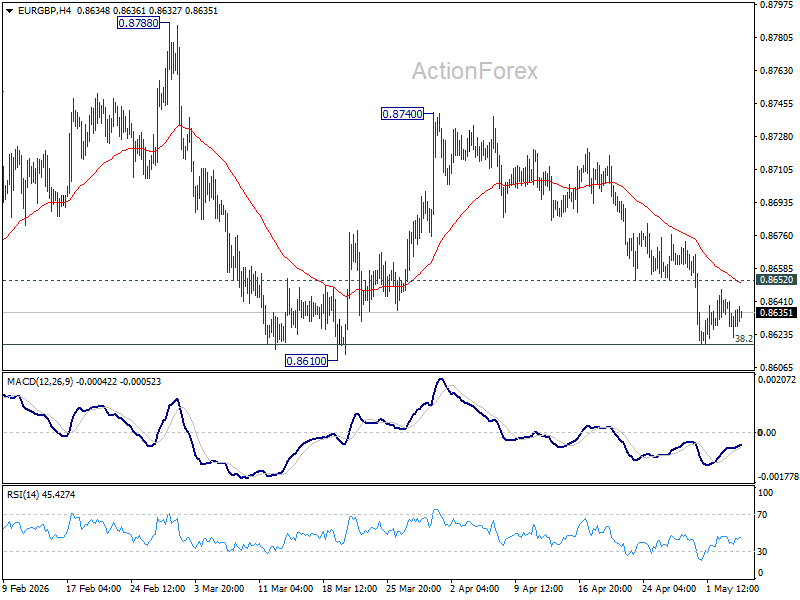

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8625; (P) 0.8635; (R1) 0.8648; More…

Intraday bias in EUR/GBP remains neutral for the moment, and further fall is expected with 0.8652 support turned resistance intact. . On the downside, decisive break of 0.8610 key support carry larger bearish implications and pave the way to 0.8466 fibonacci level next. However, firm break of 0.8652 will turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.8677) and above.

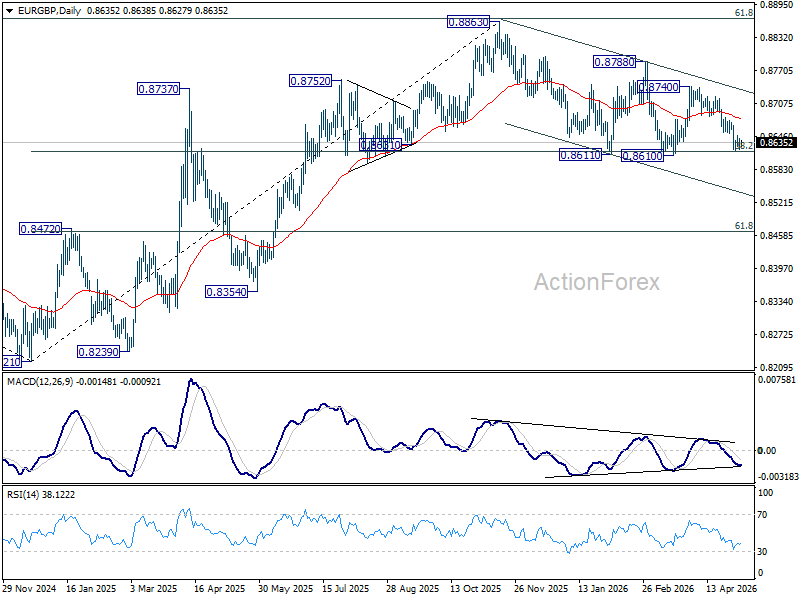

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Sustained break there will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least. For now, risk will stay mildly on the downside as long as 55 D EMA (now at 0.8680) holds, in case of recovery.

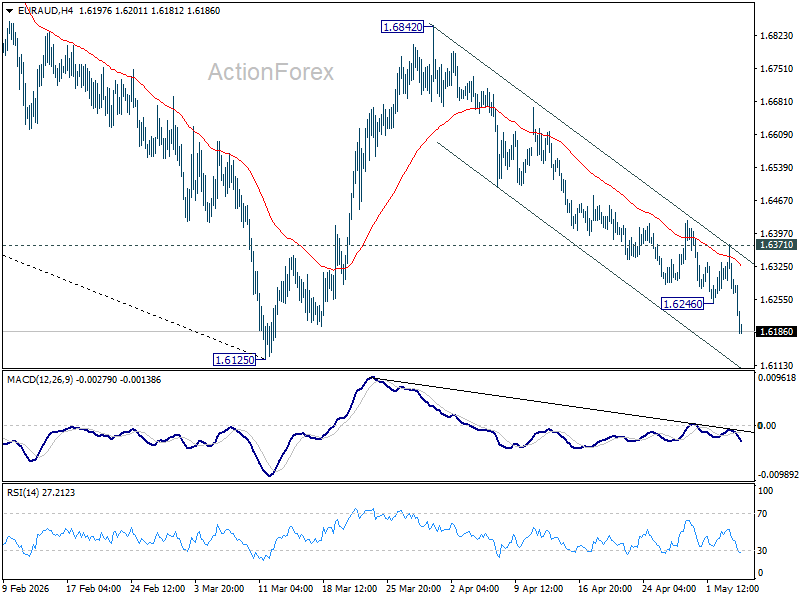

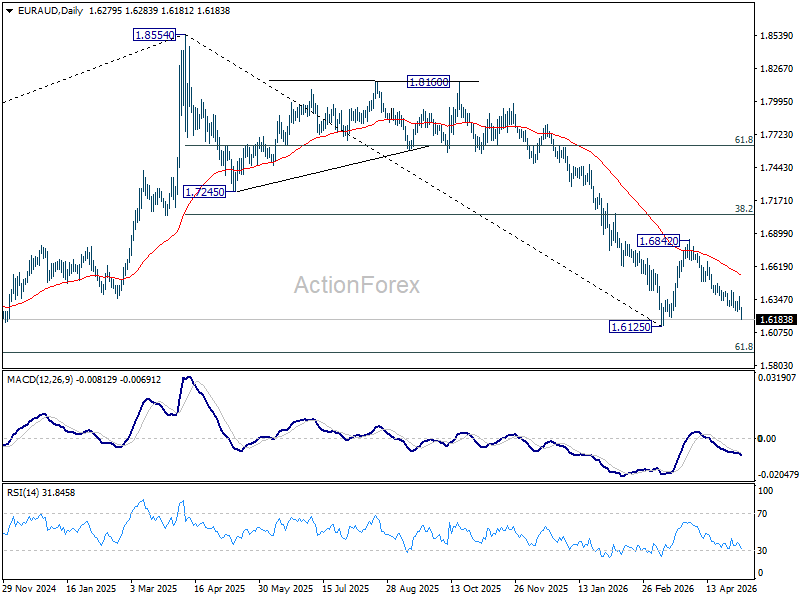

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6240; (P) 1.6307; (R1) 1.6347; More...

EUR/AUD's fall from 1.6824 resumed after brief consolidations and intraday bias is back on the downside. Decisive break of 1.6125 low will confirm resumption of whole down trend from 1.8554. For now, risk will stay on the downside as long as 1.6371 resistance holds, in case of recovery.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7069) holds, even in case of strong rebound.

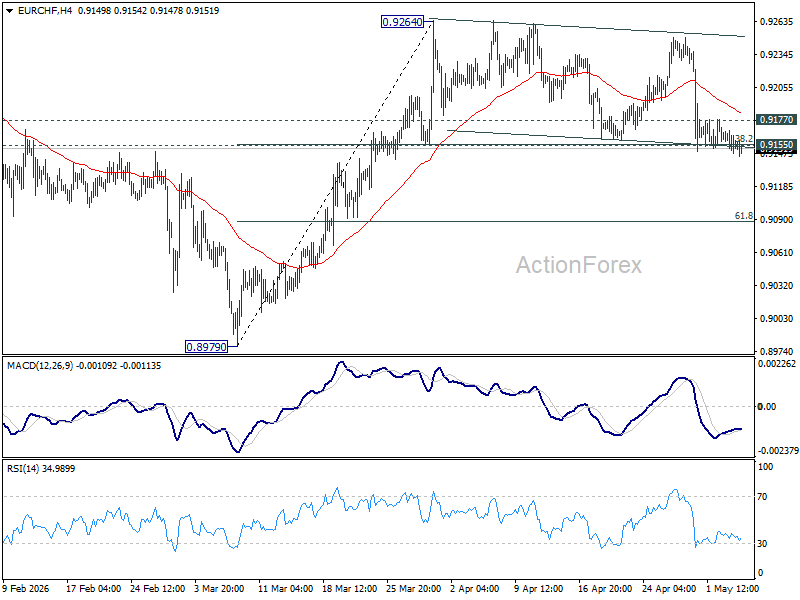

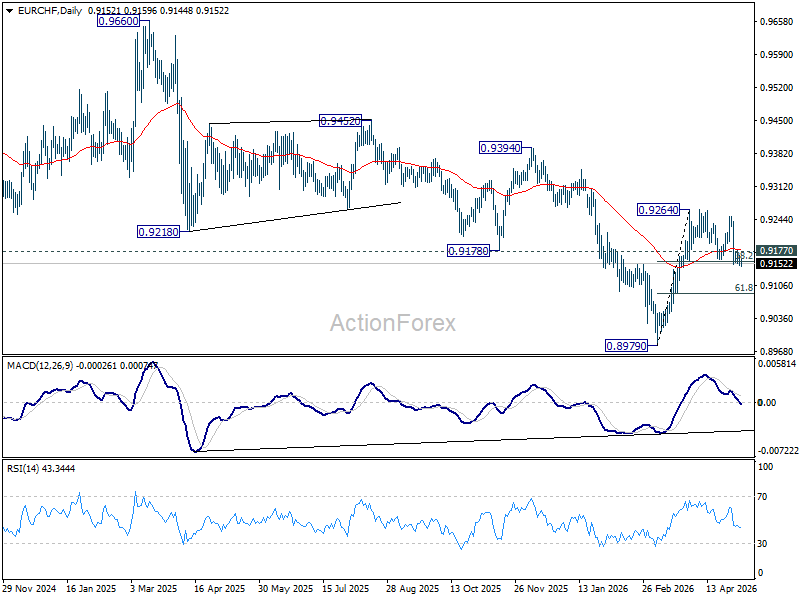

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9148; (P) 0.9160; (R1) 0.9171; More....

Intraday bias in EUR/CHF remains neutral first. On the upside, above 0.9177 minor resistance will bring stronger rebound back to 0.9264 resistance. However, sustained break of 0.9155 cluster support (38.2% retracement of 0.8979 to 0.9264 at 0.9155) break of 0.9155 will turn bias back to the downside for deeper pullback to 61.8% retracement at 0.9088 and possibly below.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9268) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

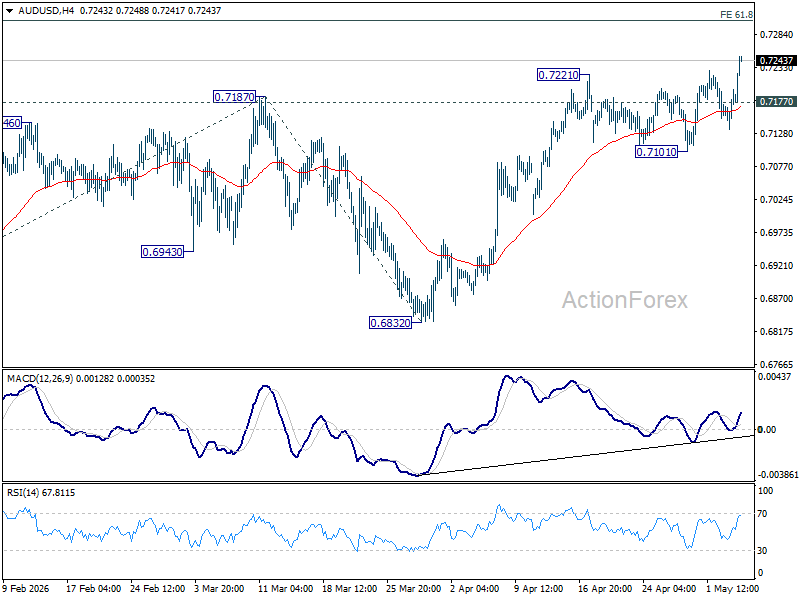

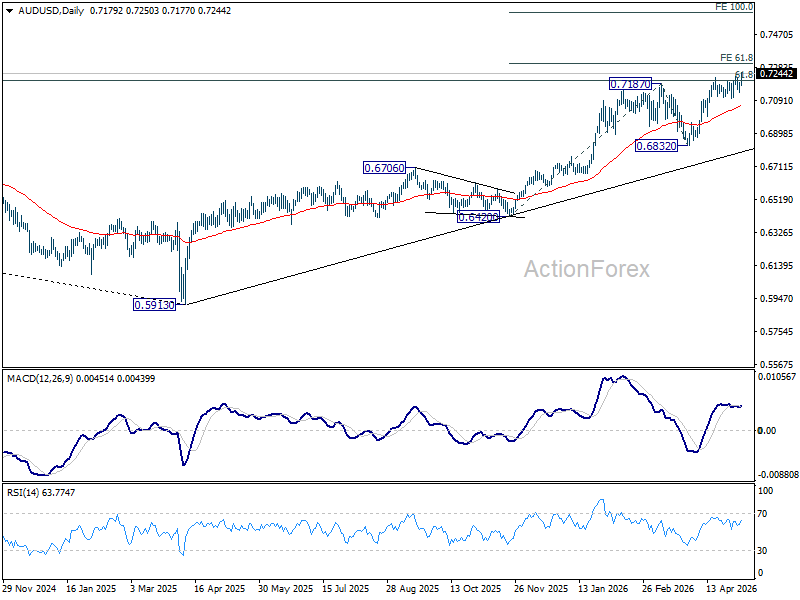

AUD/USD Daily Report

Daily Pivots: (S1) 0.7146; (P) 0.7172; (R1) 0.7210; More...

AUD/USD's rally resumed after brief consolidations and intraday bias is back on the upside. Next target is 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. On the downside, below 0.7177 minor support will turn intraday bias neutral again. But outlook will remain bullish as long as 0.7101 support holds, in case of retreat.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

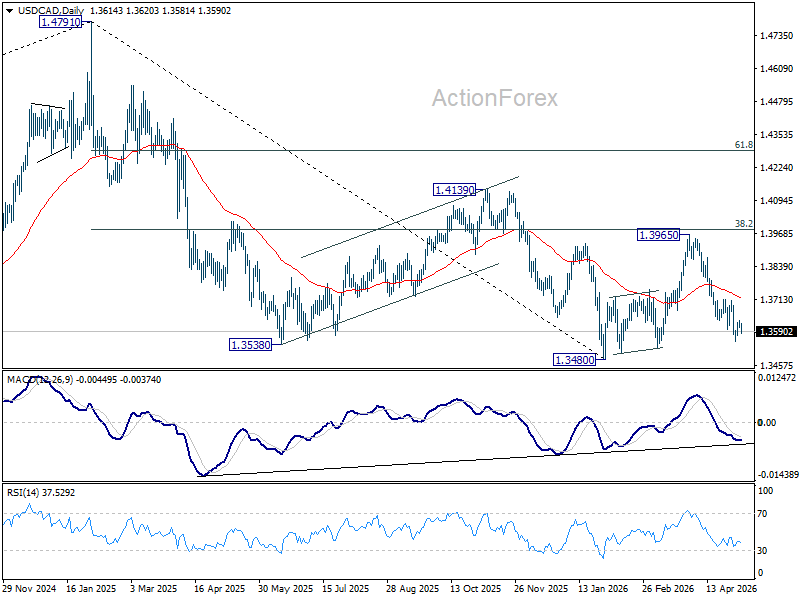

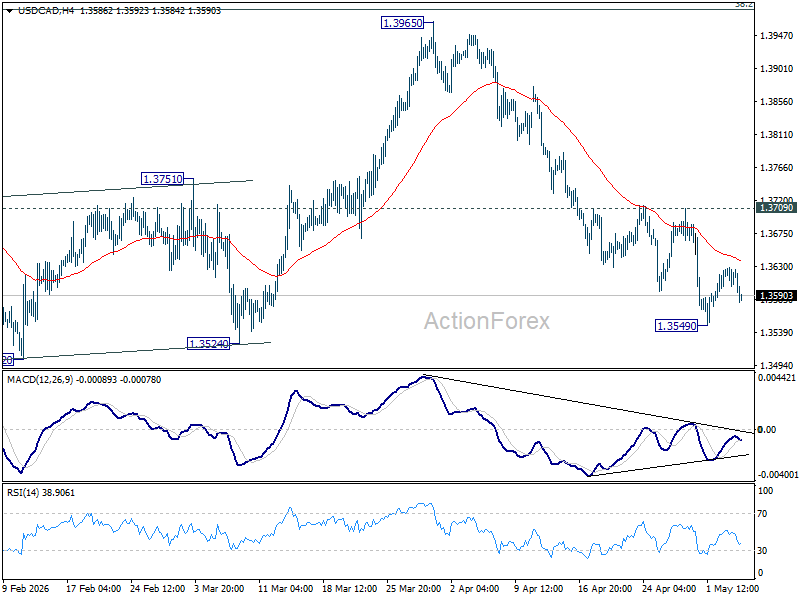

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3606; (P) 1.3618; (R1) 1.3633; More...

Intraday bias in USD/CAD remains neutral for consolidations above 1.3549. Further decline is expected as long as 1.3709 resistance holds. Below 1.3549 will resume the fall from 1.3965 to retest 1.3480 low. Decisive break there will resume whole down trend from 1.4791. However, firm break of 1.3709 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.