Sample Category Title

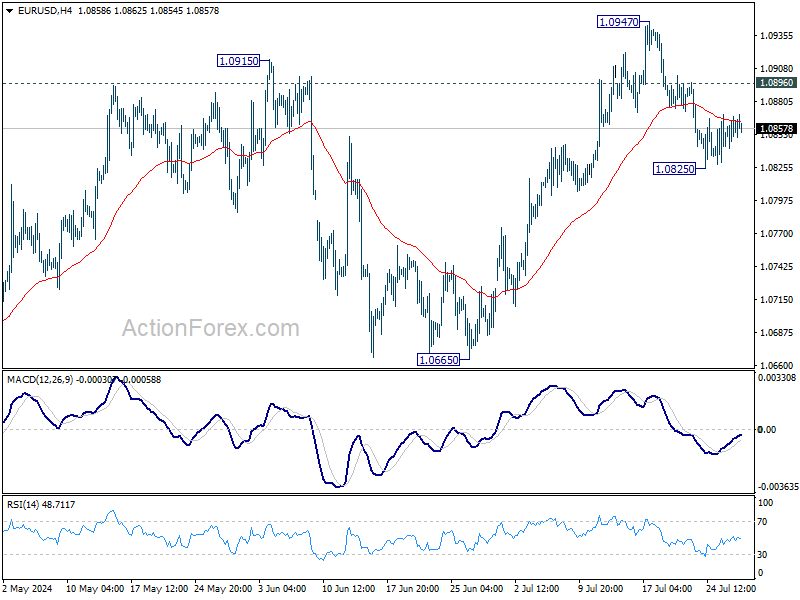

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0843; (P) 1.0855; (R1) 1.0869; More.....

Intraday bias in EUR/USD remains neutral for consolidations above 1.0825 temporary low. Further decline is expected as long as 1.0896 minor resistance holds. Below 1.0825 will target 55 D EMA (now at 1.0815). Sustained break there will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947, and target 1.0601/0665 support zone. Nevertheless, break of 1.0896 will bring retest of 1.0947 resistance instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

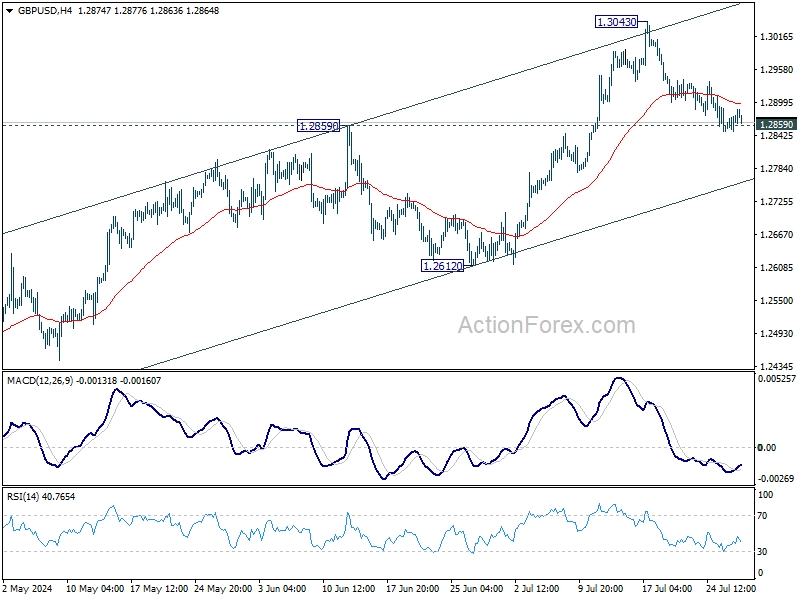

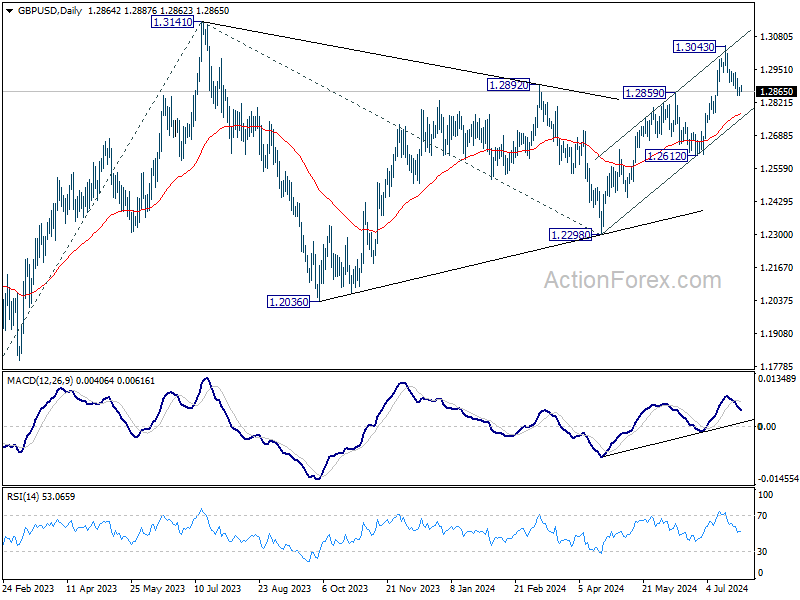

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2851; (P) 1.2866; (R1) 1.2883; More...

Intraday bias in GBP/USD remains neutral for the moment and outlook is unchanged. As long as 1.2859 resistance turned support holds, further rally is in favor. Break of 1.3043 will resume the rise from 1.2298. However, firm break of 1.2859 will turn bias to the downside for deeper decline to 55 D EMA (now at 1.2777).

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

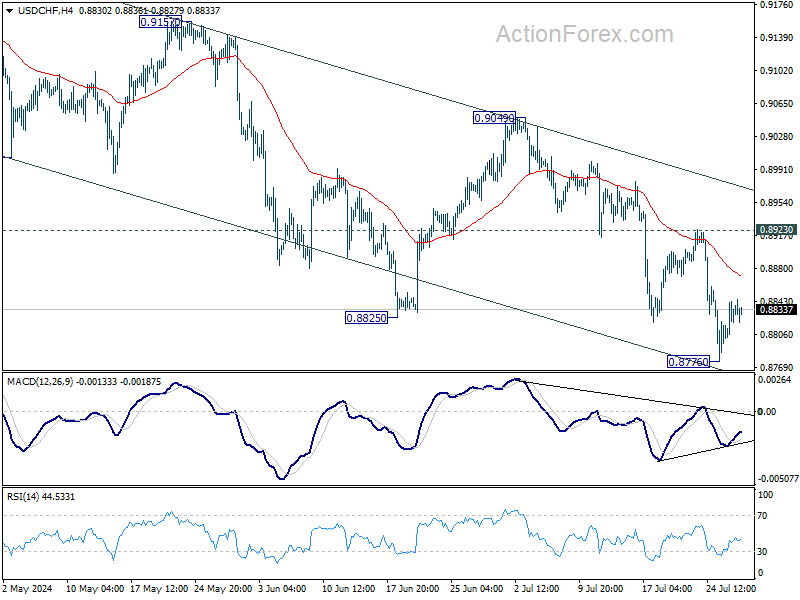

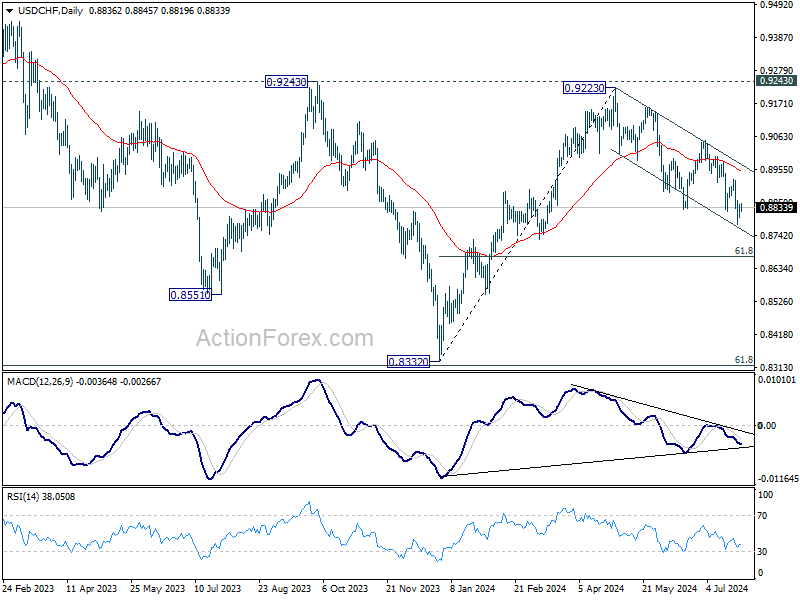

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8812; (P) 0.8828; (R1) 0.8853; More…

Intraday bias in USD/CHF remains neutral for consolidations above 0.8776 temporary low. Further decline is expected as long as 0.8923 resistance holds. On the downside, break of 0.8776 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. However, break of 0.8923 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

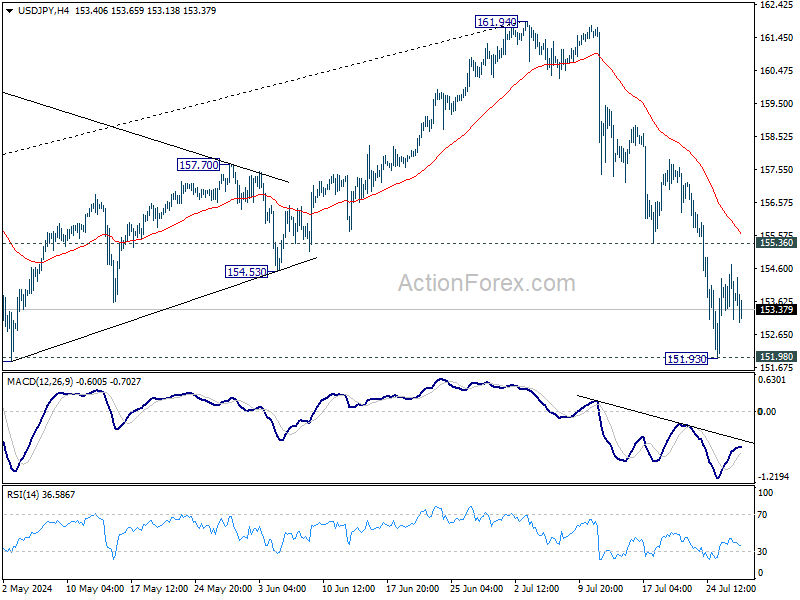

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.96; (P) 153.85; (R1) 154.59; More...

Intraday bias in USD/JPY remains neutral for consolidation above 151.93. Further decline is expected as long as 155.36 support turned resistance holds. On the downside, decisive break of 151.89 resistance turned support will argue that large scale correction is underway to 148.66 fibonacci level. Nevertheless, break of 155.36 will turn bias back to the upside for stronger rebound.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Break of 151.89 will pave the way to 38.2% retracement of 127.20 to 161.94 at 148.66. Risk will now stay on the downside as long as 55 D EMA (now at 157.04) holds, in case of rebound.

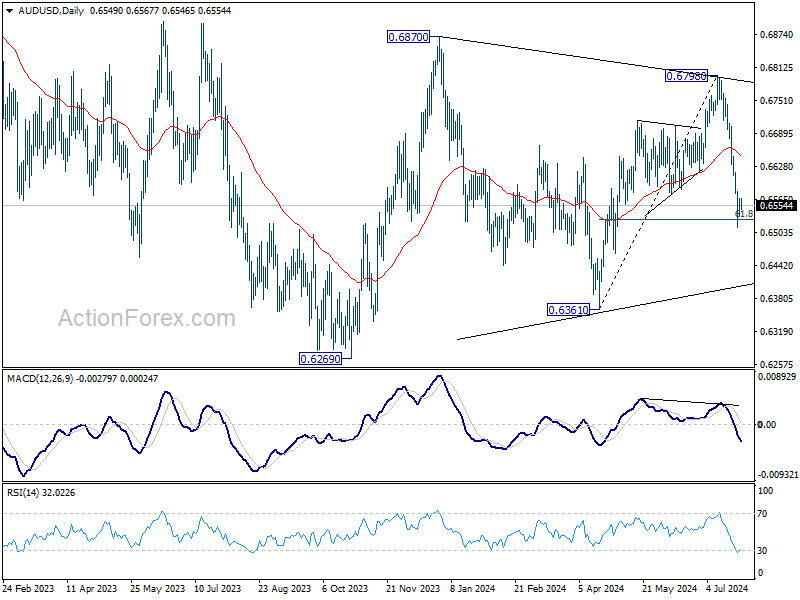

AUD/USD Daily Report

Daily Pivots: (S1) 0.6528; (P) 0.6548; (R1) 0.6568; More...

Intraday bias in AUD/USD remains neutral for consolidations above 0.6513 temporary low. Further decline is expected as long as 55 4H EMA (now at 0.6623) holds. On the downside, sustained break of 61.8% retracement of 0.6361 to 0.6798 at 0.6528 will resume the fall from 0.6798 to 0.6361 support next.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 0.6798 resistance holds, in case of rebound.

Asian Equity Markets Kick Off the week in Good Spirits

Markets

Core bonds finished higher last Friday. US Treasury yields were unable to build on Thursday’s Q2 GDP intraday rebound. The release of some economic data including personal income & spending and June PCE deflators wouldn’t call for a net daily yield decline between 3.1 and 5.6 bps but yet that’s exactly what happened. It suggests that going into a busy week and even after a sharp correction already, the downside in yields remained vulnerable. German yields ended the day marginally lower by less than 2 bps across the curve. Stock markets caught a breather. Technical support areas (5400 zone in S&P500, 4840 zone in EuroStoXX50) lived up to the name. Europe and Wall Street easily ended more than 1% higher. The US dollar traded mixed to slightly weaker. EUR/USD as a result finished a bit higher, into the northern 1.08-1.09 half. After an impressive comeback, Japan’s yen traded near the recent highs against the dollar (USD/JPY 153.76) and the euro (166.93). Sterling rebalanced after Thursday’s sharp drop lower. EUR/GBP tested 0.845 but eventually closed virtually unchanged around 0.8437. Cable (GBP/USD) snapped a three-day losing streak, eking out a slight gain to 1.2867. UK yields followed the global example south. The 2-yr yield hit a new YtD low ahead of the Bank of England meeting later this week.

Asian equity markets kick of the week in good spirits, following the US example end last week. Japan outperforms regional peers, rising more than 2%, unbothered by the Gaza war over the weekend escalating. Israel blamed Hezbollah for a rocket explosion in the Israeli-occupied Golan Heights that killed several youngers during a soccer game. Israel retaliated on Sunday but kept the door open for diplomacy. The eco calendar is a meagre one today and its backloaded nature could keep markets on the sidelines of the trading arena. Things get interesting from tomorrow on with European Q2 GDP and national (Germany, Spain, Belgium) inflation numbers due ahead of the European figure on Wednesday. Both the Bank of Japan and the Fed have their policy meeting on Wednesday with the Bank of England’s knife-edge decision due a day later. Friday is centered around US payrolls.

News & Views

Seeking to be better prepared for a potential next term, EU officials are developing a two-step trade strategy to deal with Donald Trump and the Republicans after the November elections. The former president has already floated the idea of a 10% minimum tariff on all imports, which the EU estimates could reduce exports to the US by around €150bn annually. The bloc’s negotiators plan to approach Trump and his team before he takes office and will discuss with US products the EU could buy in larger amounts. If that fails, the EC trade department is drawing up a list of imports on which it could smack 50% or more tariffs. The carrot-and-stick approach follows after Trump in his first presidency oversaw an import levy on €6.4bn of steel and aluminium, which was then countered by the EU by tariffs of a value of less than €3bn.

G20 finance chiefs last Friday concluded a two-day meeting with a joint statement expressing increasing hopes for a soft landing of the global economy. But there are a number of risks, including wars and escalating conflicts, that could endanger this outlook. It called for more global cooperation instead and to resist protectionism as well as stressed the need to reduce economic inequalities. The communique also first the time ever argued for cooperation to effectively tax the world’s largest fortunes though it has not been agreed on how to move further from this. The G20 chiefs assessed economic risks as broadly balanced with more economic cooperation, faster-than-expected disinflation and technological innovation including AI offsetting downside risks coming from the latter, as well as economic fragmentation, climate change, excessive debt and higher-for-longer rates.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Disappointing US and unconvincing EMU data, however, for now brings yields back to their post-French snap election low. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed indicated that it needs more evidence to lower its policy rate. June dots suggested one move in 2024 and four next year. Disappointing ISM and back-to-back downward CPI surprises put the US money market back on more than two rate cuts this year (September/December). The US 10-yr yield tests the recent lows and the downside of the downward trend channel in the 4.2% area.

EUR/USD

EUR/USD tested the topside of the 1.06-1.09 range as the dollar lost interest rate support at stealth pace. Markets consider a September rate cut a done deal and only need confirmation from high-ranked Fed officials. In the meantime, the euro got rid of the (French) political risk premium. EUR/USD recently evolved back to a more neutral positioning but is holding up rather well despite ongoing poor EMU data.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 support is being tested.

A Sense of Hope in the Market This Monday Morning

There is a sense of hope in the market this Monday morning after Friday’s PCE data boosted the expectation that the Federal Reserve (Fed) is getting very close to signaling its first rate cut in September. The core PCE came in slightly higher-than-expected – steady at 2.6% instead of a further easing to 2.5%, but the rest of the data was either in line or lower than expected. Personal income and spending for example showed easing and inflation-adjusted PCE fell to 0.2% on a monthly basis. All in all, the data was read as a green light for the Fed to confirm that September is a good time to start cutting the rates. The US 2-year yield sand below 4.40% after the data and remained under pressure in Asia this morning, the 10-year yield consolidation below 4.20%, activity on Fed funds futures gives a 100% chance for a September rate cut (with increasing pricing for a 50bp cut), and two more rate cuts are expected before the year ends. The Fed will start its two-day policy meeting tomorrow and will announce its policy decision on Wednesday. If all goes according to the plan, a strong signal for a September cut should not make a big difference – as it’s is already priced in. The risk is that we meet a slightly cautious Powell, in which case there could be some correction in dovish Fed bets. Also this week, the US jobs data will be closely watched. Due Friday, the NFP number is expected to show that the US added around 177K new nonfarm jobs in July, for steady wages growth of around 0.3% and an unemployment rate steady near 4.1%.

For now, the US dollar index remains under pressure near its 200-DMA and hovers around a key Fibonacci support – the major 38.5% retracement on this year’s rally – near 104.24. A decline below this level will – in theory – send the US dollar index into a medium term bearish consolidation zone and pave the way for a deeper downside correction. But one major hurdle to a further dollar weakness is the dovishness from the other central banks. A Fed cut will increase the probability of further rate cuts from the major central banks like the European Central Bank (ECB) and the Bank of England (BoE), which could, in return, slow down the weakening of the US dollar. In this context, the BoE could announce a 25bp rate cut when it meets on Thursday, while the ECB rate cut expectations mount on soft economic data and a disappointing earnings season.

In contrast with dovish expectations, the Bank of Japan (BoJ) is expected to announce QT this week and lower its policy rate by 10bp. The yen is in demand against most majors. If all goes according to the plan, the narrowing gap between Japan and the rest of the developed world should give the yen a further positive spin.

Focus on Big Tech

Friday was a better day for the Big Tech stocks in the US. Roundhill’s Magnificent Seven ETF rebounded 1%. But overall, last week saw accelerated rotation flows as capital moved out of Big Tech and into smaller and non-tech sectors of the market, driven by rising Fed cut bets and disappointing earnings from Google and Tesla. Nasdaq 100 slipped more than 2.50% last week and the S&P500 closed last week 0.8% down, while the equal weight index rebounded 0.8% over the week and the Russell 2000 stocks gained almost 3.5%. A dovish Fed and weak economic data could accelerate the rotation trend. As such, the Big Tech can only rely on their earnings to slow and – maybe – reverse the selloff. 4 of Magnificent Seven companies : Microsoft, Meta, Apple and Amazon are due to announce their Q2 earnings this week. Their results should not only meet but also beat the sky-high expectations.

Mounting Mid-East tensions give support to Oil

Crude oil is better bid this morning on mounting geopolitical tensions in the Middle East, after having slipped more than 2% on Friday. OPEC+ will meet this and expectations are mixed. OPEC is supposed to scale back their production restrictions next quarter, but the sluggish Chinese demand, the ample supply from Americas and the easing energy prices increase the odds of a delay of that move. Combined with boiling Mid-East, we could see oil prices in a better shape by the end of the week. Key resistance stands at $80pb.

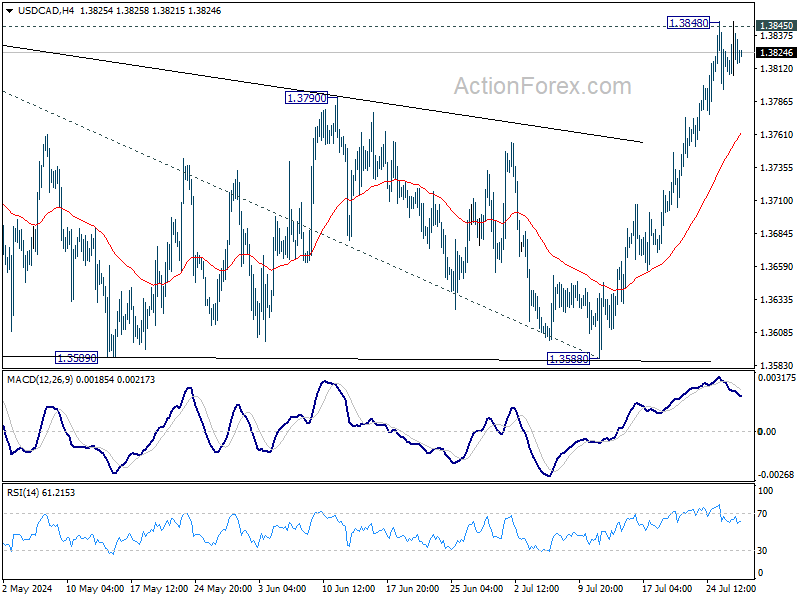

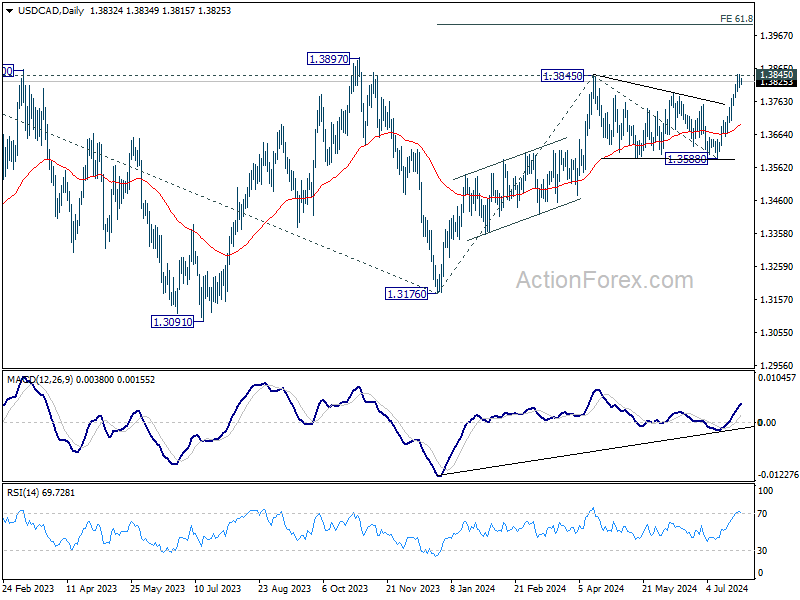

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3814; (P) 1.3831; (R1) 1.3856; More...

Intraday bias in USD/CAD remains neutral for consolidations below 1.3848 temporary top. Further rally is expected as long as 55 4H EMA (now at 1.3762) holds. Decisive break of 1.3845 will resume whole rally from 1.3176. Next target is 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

Quiet Forex Session Precedes Three Central Bank Meetings and High-Impact Data

Trading in the forex markets has been notably subdued during the Asian session today, even as major Asian stock indexes showed strong rebounds. This muted activity in currency trading is not surprising given that it's a typical Monday, coupled with an ultra light economic calendar. However, significant volatility is anticipated later in the week with a series of high-impact events on the horizon.

Three central banks are scheduled to hold meetings that could result in a rate hike, a hold, and a cut. Additionally, important economic data releases are expected, including CPI figures from Eurozone, Switzerland, and Australia, GDP data from Eurozone and Canada, and the highly anticipated non-farm payroll data from the US.

As July draws to a close, Yen remains the top performer among currencies, followed by Sterling and Swiss Franc. New Zealand Dollar is at the bottom, trailed by Australian and Canadian Dollars. Dollar and Euro are positioned in the middle. The overall picture reflects risk-off sentiment that may persist into August.

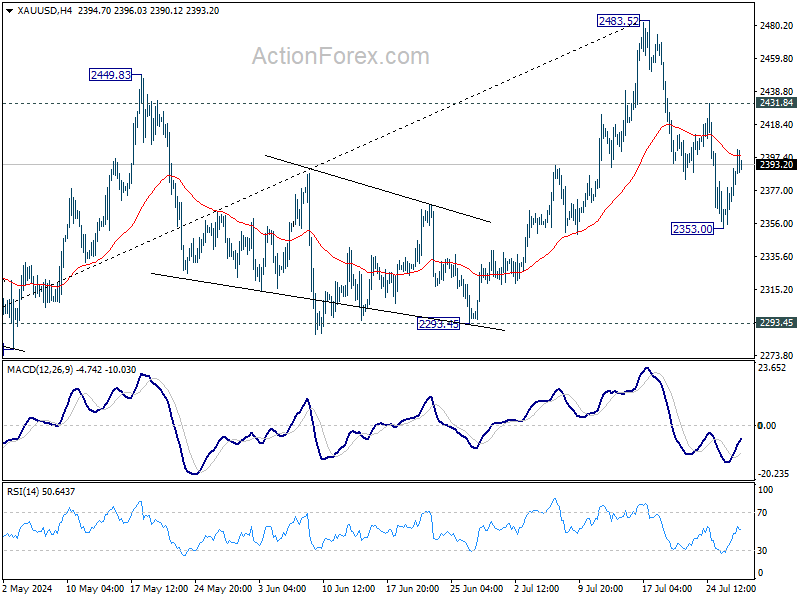

Technically, Gold is stuck in range without a clear direction for now. Prior support from rising 55 D EMA (now at 2356.89) somehow maintains its near term bullishness. Yet, rebound from 2353.00 is capped by falling 55 4H EMA (now at 2398.51). On the upside, firm break of 2431.84 resistance will suggest that the pull back from 2483.52 has completed, and larger up trend might be ready to resume. However, break of 2353.00 will extend the fall towards 2293.45 support, with risk of starting larger scale correction.

In Asia, at the time of writing, Nikkei is up 2.59%. Hong Kong HSI is up 1.85%. China Shanghai SSE is up 0.10%. Singapore Strait Times is up 0.60%. 10-year JGB yield is down -0.0327 at 1.029.

In Asia, at the time of writing, Nikkei is up 2.59%. Hong Kong HSI is up 1.85%. China Shanghai SSE is up 0.10%. Singapore Strait Times is up 0.60%. 10-year JGB yield is down -0.0327 at 1.029.

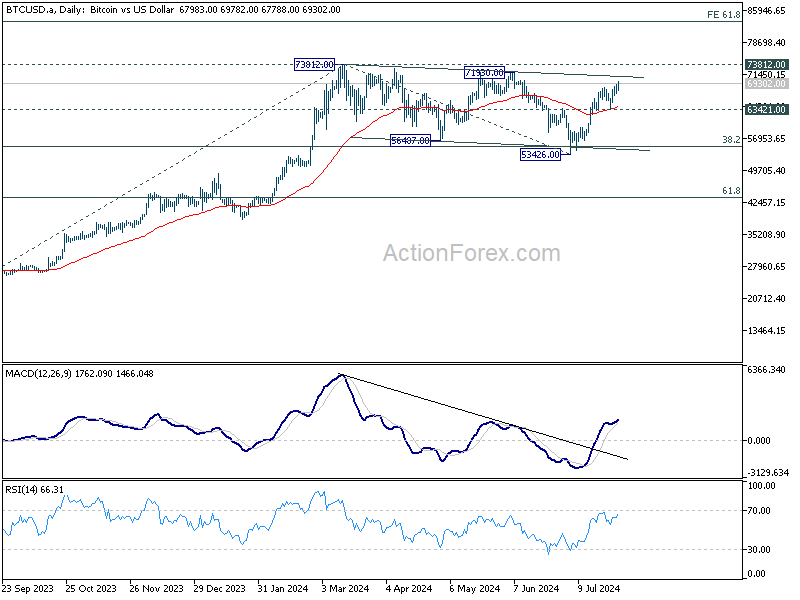

Bitcoin rises but struggles to break 70k handle

Bitcoin saw a modest rise at the beginning of this week, yet it remains below 70k mark, lacking the momentum to push past this psychological barrier. The cryptocurrency community had high hopes for Republican presidential nominee Donald Trump's keynote speech at the 2024 Bitcoin Conference over the weekend. However, the speech fell short of expectations, as Trump did not pledge to establish an official US bitcoin strategic reserve currency.

Instead, Trump promised to "keep 100% of all the bitcoin the US government currently holds or acquires into the future." He further emphasized the importance of embracing crypto technology, warning, "If we don't embrace crypto and bitcoin technology, China will, other countries will. They'll dominate, and we cannot let China dominate. They are making too much progress as it is."

Technically, Bitcoin's prior bounce from 55 D EMA is keeping the bullish outlook alive. That is, consolidation pattern from 73812 should have completed with three waves down to 53426. Near term outlook will now stay bullish as long as 63421 support holds, for retesting 73812 high first.

Decisive break of 73812 will resume larger up trend. Next target will be 61.8% projection of 24896 to 73812 from 533426 at 83656. Nevertheless, break of 63421 support will delay the bullish case, and extend the corrective pattern with another falling leg.

Fed, BoJ, BoE, and more top-tier events

The coming week promises to be exceptionally busy for financial markets with three central bank meetings and a slew of top-tier economic data on the agenda.

FOMC meeting is a relatively straight forward one. It is widely anticipated that interest rates will remain unchanged at 5.25-5.50%. The spotlight will be on any forward-looking statements, as Fed likely indicate that monetary policy is finally looming near, and pave the way for the first rate cut at next meeting in September.

While fed fund futures suggest a 64% probability of consecutive rate cuts in November and December, Chair Jerome Powell is unlikely to provide explicit hint during this meeting. Instead, Fed may defer to the forthcoming economic projections and dot plots in September for clearer guidance.

BoJ faces a tough decision, with uncertainty around whether to implement a second rate hike at this meeting. While postponing the decision to September or October is seen as feasible, the imminent meeting remains a "close call." It is more certain, however, that BoJ will outline plans to taper its bond purchases, potentially halving them in the coming years, fulfilling a commitment made at the last meeting.

BoE is also under significant scrutiny this week, with some market participants expecting a rate cut from 5.25% to 5.00%. A recent Reuters poll reflects a shift in sentiment, with 49 out of 60 economists surveyed anticipating the rate cut, a decrease in confidence from 97% in a previous June poll, showcasing growing uncertainty among economists.

BoE's history of surprising voting adds an element of unpredictability to this decision. Recent comments from BoE officials didn't suggest any consensus for a cut at this meeting. In addition to the rate decision, BoE will release new economic projections for markets to assess future monetary policy path.

Aside from central bank activities, top-tier economic data from around the globe will also play a crucial role in shaping market dynamics. In the US, consumer confidence, ADP employment, ISM manufacturing, and non-farm payrolls will be particularly influential, with the NFP report crucial for assessing the likelihood of multiple rate cuts by Fed this year. Eurozone GDP and CPI might help conclude the case for ECB to cut interest rate again in September. Likewise, Swiss CPI will also be an important piece of data for SNB to consider whether to cut interest rates again in September.

For Australia, Q2 CPI could be crucial for RBA to decide if another rate hike on August 6 to continue the inflation fight. Any significant upward surprises in CPI figures could compel RBA to act decisively, as failing to do so could impact its credibility. Ideally, RBA is hoping that both headline and underlying inflation are either continuing to decrease, or at least not accelerating. Additionally, Australian Dollar's movements will be influenced by upcoming official PMI data from China and Caixin PMI manufacturing report.

Here are some highlights for the week:

- Monday: UK M4 monthly supply, mortgage approvals;.

- Tuesday: Japan unemployment rate; Australia building approvals; Swiss KOF economic barometer; France GDP; Germany GDP; Eurozone GDP; US house price index, consumer confidence.

- Wednesday: Japan industrial production, retail sales, consumer confidence, BoJ rate decision; New Zealand ANZ business confidence; Australia CPI, retail sales; China official PMIs; Germany import prices, unemployment; Swiss UBC economic expectations; Canada GDP; US ADP employment, employment cost, Chicago PMI, pending home sales, FOMC rate decisions.

- Thursday: Japan PMI manufacturing final; Australia goods trade balance, import prices; China Caixin PMI manufacturing; Eurozone PMI manufacturing final, unemployment rate; UK PMI manufacturing final, BoE rate decision; US jobless claims, non-farm productivity, ISM manufacturing, construction spending; Canada PMI manufacturing.

- Friday: Japan monetary base; Australia PPI; Swiss CPI, PMI manufacturing; France industrial production; US non-farm payrolls, factory orders.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3814; (P) 1.3831; (R1) 1.3856; More...

Intraday bias in USD/CAD remains neutral for consolidations below 1.3848 temporary top. Further rally is expected as long as 55 4H EMA (now at 1.3762) holds. Decisive break of 1.3845 will resume whole rally from 1.3176. Next target is 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | GBP | M4 Money Supply M/M Jun | -0.10% | |||

| 08:30 | GBP | Mortgage Approvals Jun | 60K | 60K |

Bitcoin rises but struggles to break 70k handle

Bitcoin saw a modest rise at the beginning of this week, yet it remains below 70k mark, lacking the momentum to push past this psychological barrier. The cryptocurrency community had high hopes for Republican presidential nominee Donald Trump's keynote speech at the 2024 Bitcoin Conference over the weekend. However, the speech fell short of expectations, as Trump did not pledge to establish an official US bitcoin strategic reserve currency.

Instead, Trump promised to "keep 100% of all the bitcoin the US government currently holds or acquires into the future." He further emphasized the importance of embracing crypto technology, warning, "If we don't embrace crypto and bitcoin technology, China will, other countries will. They'll dominate, and we cannot let China dominate. They are making too much progress as it is."

Technically, Bitcoin's prior bounce from 55 D EMA is keeping the bullish outlook alive. That is, consolidation pattern from 73812 should have completed with three waves down to 53426. Near term outlook will now stay bullish as long as 63421 support holds, for retesting 73812 high first.

Decisive break of 73812 will resume larger up trend. Next target will be 61.8% projection of 24896 to 73812 from 533426 at 83656. Nevertheless, break of 63421 support will delay the bullish case, and extend the corrective pattern with another falling leg.