Sample Category Title

Canada: Inflation Accelerates in May

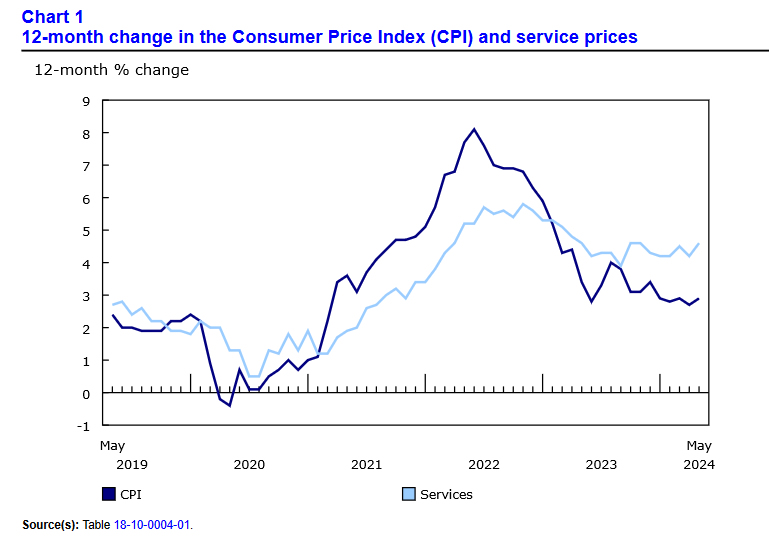

Headline CPI inflation edged higher in May to 2.9% year-on-year (y/y), above expectations for a 2.6% y/y print.

The acceleration was led by services, which were up 4.6% y/y, as Canadians were paying up for travel tours (+6.9% y/y) and flights (+4.5% y/y). This continues a trend where Canadians have been increasingly willing to spend on experiences rather than physical goods.

Shelter inflation also remained hot, coming in at 6.4% y/y (same as April). Rents were up an eyewatering 9.0% y/y, while mortgage interest cost inflation remained sky high at 23.3% y/y.

Goods inflation held steady at 1.0% y/y. This has been kept low by falling durable goods prices, which clocked in at -0.8% y/y (same as April). Discounting at furniture and home improvement stores continues to support easing price pressures.

In other disappointing news, the Bank of Canada's preferred "core" inflation measures rose to 2.9% y/y in May, up from 2.7% y/y in April. On a three-month annualized basis, the average moved from 1.6% in April to 2.5% in May. The BoC's former preferred measure, CPIX, went from 0.8% on the three-month basis to 2.1%. While these figures are still within the BoC's target range, they aren't moving in the right direction.

Key Implications

While this wasn't as big of a letdown as the Oilers' game last night, today's CPI print was a disappointment. Not only did the headline print unexpectedly rise, the average of the BoC's core inflation rates increased for the first time in 2024! This was driven by big price swings in a number of services categories. Big increases were seen in areas related to housing and travel – two sources of unrelenting price pressures over the last year.

Today's report won't instill any added confidence for the Bank of Canada. The central bank cut interest rates in early-June because it gained sufficient conviction that it had inflation under control. Just yesterday, Governor Macklem said in a speech, "since January, inflation has been below 3%, and our measures of underlying inflation have eased steadily. This has increased our confidence that inflation will continue to move closer to the 2% target this year." Now, one bad inflation print doesn't make a trend, and inflation remained below 3%. But it does speak to the unevenness of the path back to 2%. For this reason, we think the BoC will likely pause at its July meeting, before cutting rates again in September.

Sunset Market Commentary

Markets

US and EMU (interest rate) markets today are holding tight ranges with trading mostly technical in nature. If anything markets still err to rather dovish bias, with yields on both sides of the Atlantic hold with reach of recent lows. There were no data in EMU. In the US, the Philly Fed non-manufacturing index and the Chicago Fed national activity index printed on the better side of expectations. US S&P Corelogic house prices also were slightly stronger than expected. Fed’s Bowman, one of the hawkish members within the Fed FOMC, understandably still warned on upside inflation risks. She reiterated that rates will have to be kept high for some time. She still sees no room for interest rate cuts this year and as such shifted the expected cuts to next year. Amongst others, she also warned a fiscal stimulus and on a loosening of financial conditions as potential risks to the inflation outlook. The comments were no surprise. Still, US yields gradually reversed a tentative decline to currently add between 1.0 and 2.0 bps. Later today, the US consumer confidence (Conference Board) and a 2-yr $ 69 bln auction of US Treasuries still are worth looking at. Bunds slightly outperform Treasuries with yields easing about 1 bp across the curve. After some modest narrowing yesterday, spreads of France (10-yr +1 bp) and peripheral bond markets (Italy+3 bps) again widened slightly as investors are counting down the first round of the French elections this weekend. European equities couldn’t hold on to yesterday’s constructive start of the week. The EuroStoxx 50 is ceding about 0.5%. US indices, after yesterday’s setback in AI relates stocks today open mixed to marginally stronger (S&P + 0.15%). Recent rebound in oil shows tentative signs of running into resistance (Brent $ 85.75 p/b).

On FX markets, the dollar slightly outperforms today. DXY trades near 105.62. EUR/USD struggles not the fall back below the 1.07 handle (1.0705). The market focus remains on the USD/JPY cross rate. At 159.65, it still trades only a whisker away from the 160 area that trigger BoJ interventions end-April/early May. However, looking at the USD/JPY price pattern, markets apparently have little confidence that Japanese authorities will be able to change fortunes for the yen in a sustainable way. EUR/GBP also show no clear directional trend trading marginally weaker at 0.8445, probably due to euro softens rather sterling strength.

News & Views

Canadian inflation unexpectedly accelerated in May. Coming in at 0.6% m/m – double the 0.3% expected – the yearly figure increased from 2.7% to 2.9% (2.6% anticipated). Statistics Canada said the quickening was largely due to higher prices for services (4.6% y/y, up from 4.2%). Prices for goods (+1%) rose at the same rate as in April. The Bank of Canada’s core inflation gauges snapped a four-month y/y decline with the average picking up from 2.7% to 2.85%. The central bank earlier this month lowered the policy rate a first time to 4.75% amidst “continued evidence that underlying inflation is easing”, agreeing that monetary policy “no longer needs to be as restrictive” as it was. Today’s CPI reading is the first of two in total that the BoC will have at its disposal at the next policy meeting July 24. For now, though, they significantly raise the bar for a follow-up rate cut. Canadian money markets have pared odds for a July move from 62% to about 40%. The Canadian dollar quickly erased a kneejerk strengthening move with USD/CAD currently trading unchanged around 1.365.

Three people familiar with the Bank of Japan’s thinking said a rate hike would be on the table at each policy meeting, including July’s. One of the sources said that given what’s happening with inflation, interest rates are clearly too low. Governor Ueda in recent appearances also highlighted the possibility of that to happen, not surprisingly in the wake of recent JPY weakness. If the BoJ would indeed hike rates from 0-0.1% currently, it would come as a surprise to some 50% of the market. Moreover, it may come in tandem with a detailed plan on how the central bank plans to trim bond buying (currently JPY 6tn per month) and reduce the size of its $5tn balance sheet. Given the re-weakening of the Japanese yen to historical lows, any QT plan needs to be ambitious enough, creating the potential of the BoJ announcing bigger-than-expected buying cuts on July 31.

Graphs

USD/CAD: Loonie gains a few ticks as unexpected jump in inflation questions room for BOC follow-up rate cuts anytime soon.

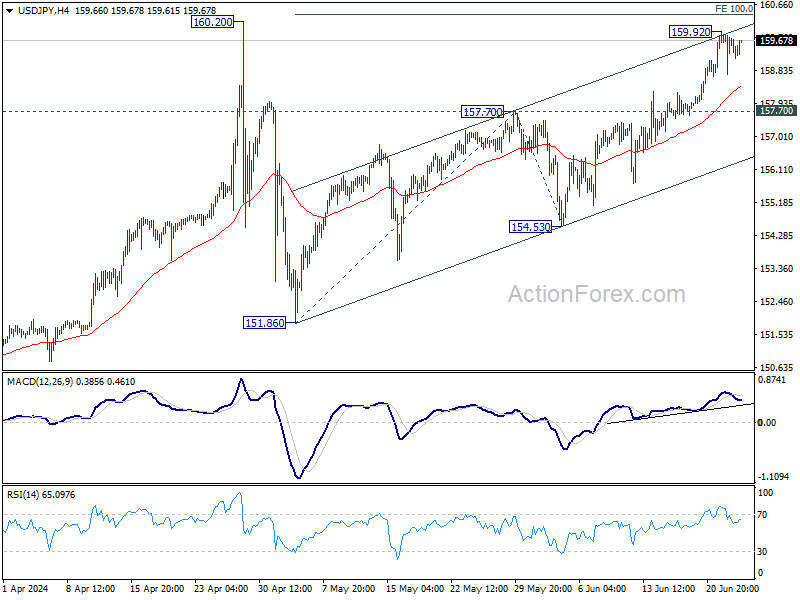

USD/JPY: markets testing Japanese authorities’ preparedness to stem the decline of the yen.

Cocoa prices extends decline on rumoured exit of long positions both of commercial parties and funds.

Brent oil ($ p/b): rebound running into resistance

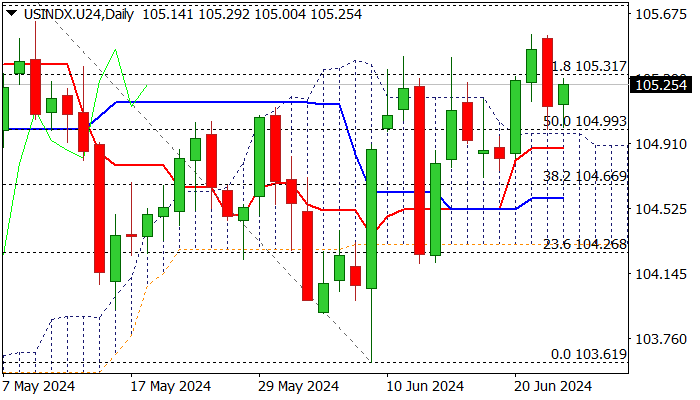

Dollar Index: Bullish Bias Above Daily Cloud, US Inflation Data in Focus

The dollar index regained traction on Tuesday and ticked higher after dropping 0.4% on Monday.

Pullback was contained by daily cloud top and marked a light correction of a larger uptrend, which remains intact.

Technical picture on daily chart remains bullish, as MA’s are in bullish setup, positive momentum is strong and price action underpinned by daily cloud.

Markets await release of US inflation data (PCE) on Friday, to get more clues about Fed’s rate path, which is expected to strongly influence dollar’s performance.

Focus will be also on the first debate of US presidential candidates, French election, as well as on geopolitics, especially after the latest signals that the conflict may spread on Lebanon.

Bullish near term bias is expected above 105.00 support (cloud top / 10DMA) for renewed attempt towards 105.71 (Fibo 76.4% of 106.36/103.61), while loss of 105 handle would weaken the structure and risk deeper drop towards 104.47/28 (100 / 200DMA’s respectively.

Res: 105.54; 105.71; 106.00; 106.36.

Sup: 105.00; 104.78; 104.47; 104.28.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.95; (P) 159.43; (R1) 160.11; More...

Intraday bias in USD/JPY remains neutral for the moment. Further rise will remain in favor as long as 157.70 resistance turned support holds. Sustained break of 106.20 and 100% projection of 151.86 to 157.70 from 154.53 at 160.37 will confirm long term up trend resumption, and pave the way to 161.8% projection at 163.97. Nevertheless, firm break of 157.70 will turn bias back to the downside for channel support (now at 156.26) first.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

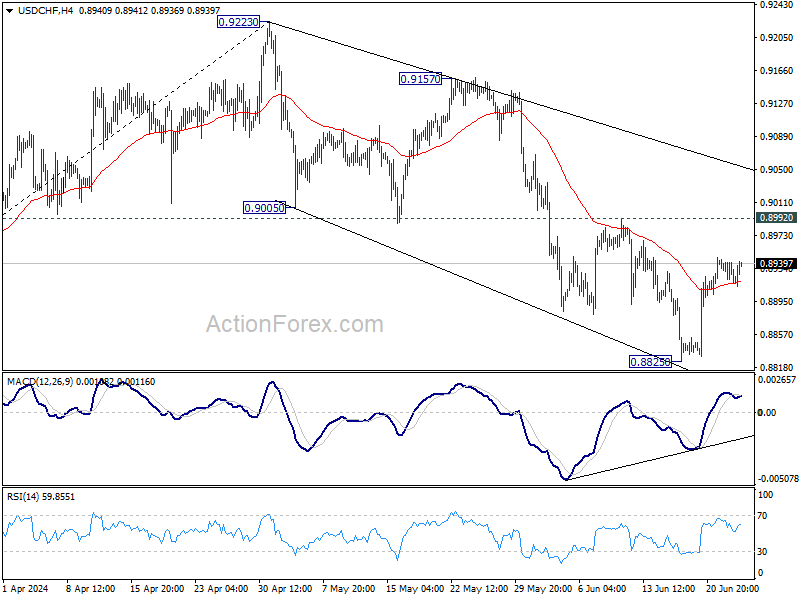

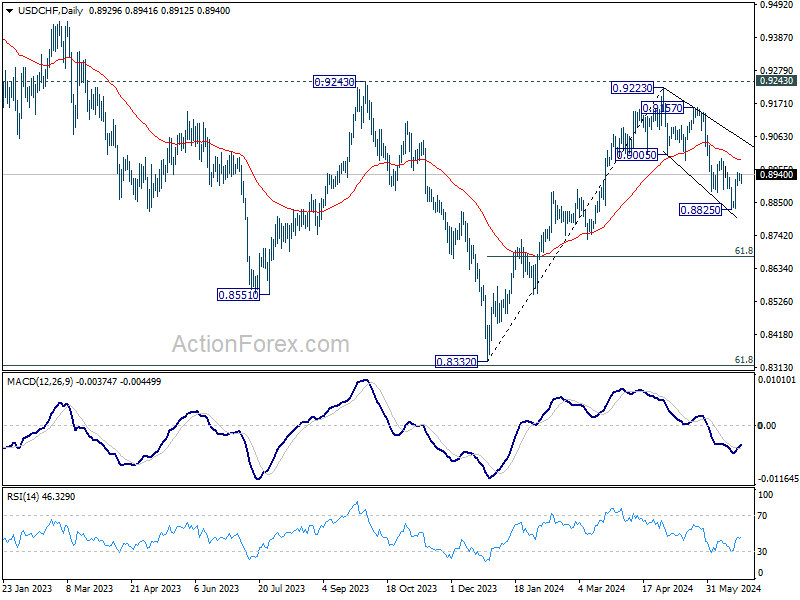

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8919; (P) 0.8932; (R1) 0.8943; More….

No change in USD/CHF's outlook as consolidation continues above 0.8825. Intraday bias stays neutral for the moment. Near term outlook remains bearish with 0.8992 resistance intact. Break of 0.8825 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

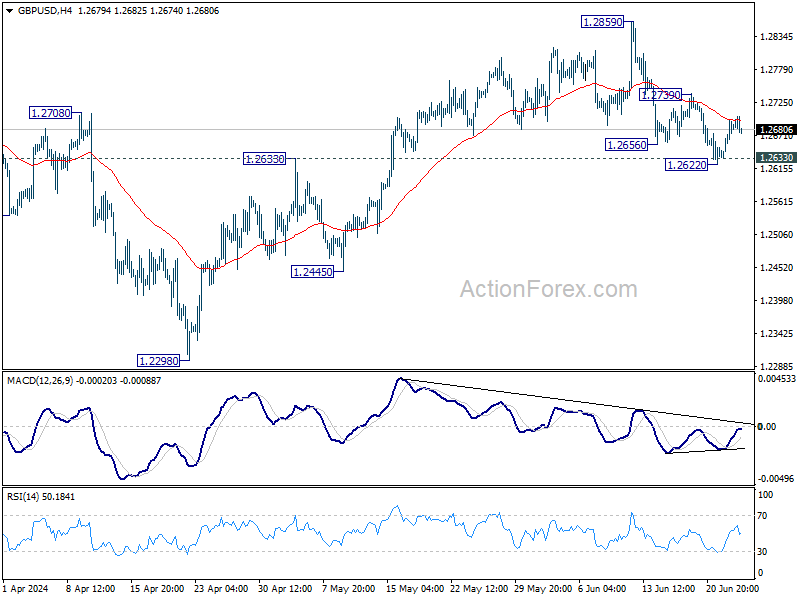

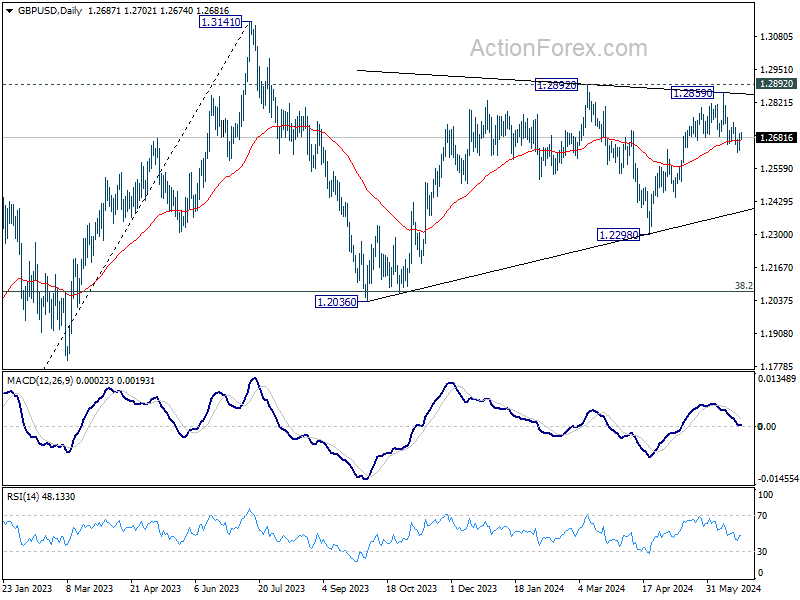

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2647; (P) 1.2672; (R1) 1.2712; More...

No change in GBP/USD's outlook and intraday bias stays neutral. Further decline is expected as long as 1.2739 resistance holds. Break of 1.2622, and sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. However, firm break of 1.2739 will argue that pull back from 1.2859 has completed, and bring retest of this high instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

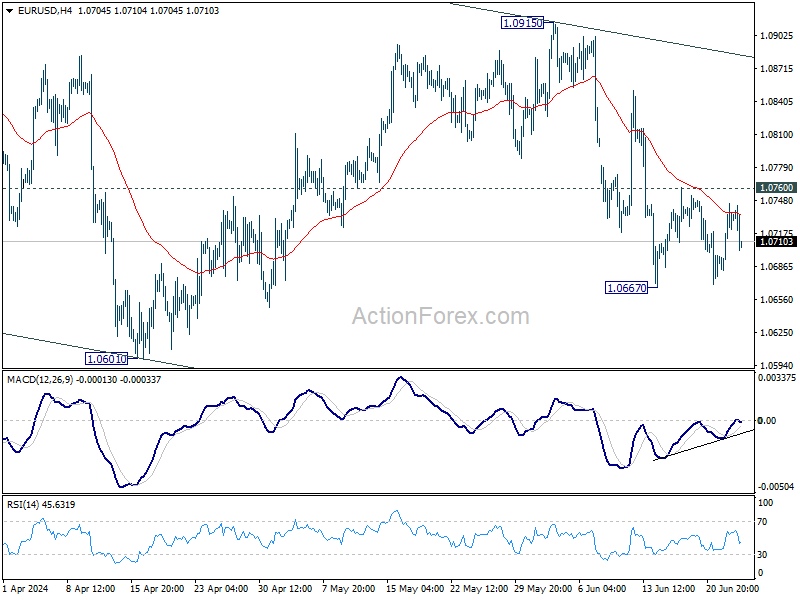

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0696; (P) 1.0721; (R1) 1.0760; More....

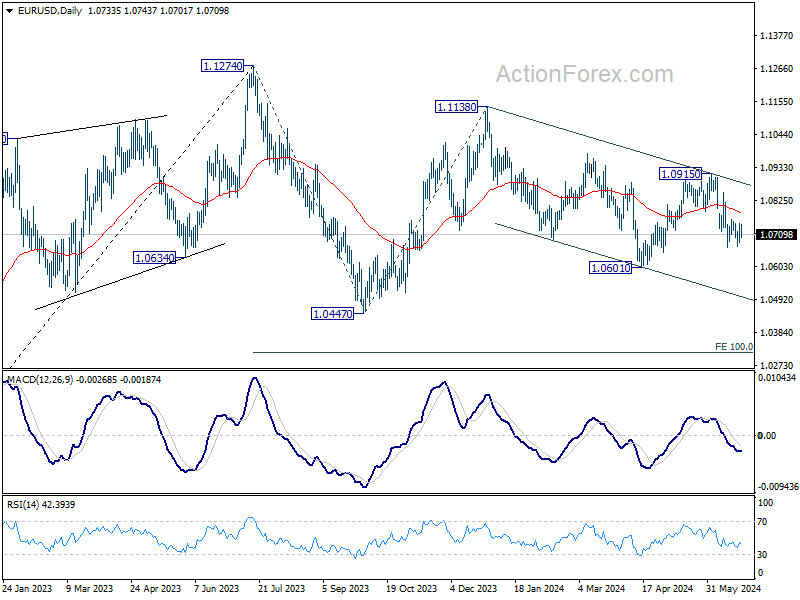

EUR/USD dips notably in early US session but stays in range above 1.0667. Intraday bias remains neutral at this point. Further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below. However, firm break of 1.0760 will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

Canadian Dollar Surges on Unexpected Inflation Rebound in May

Canadian Dollar jumps following after data showing that Canadian inflation unexpectedly accelerated in May. More importantly, the resurgence in price pressures was largely driven by significant increase in services inflation. The data aligns with BoC Governor Tiff Macklem's cautious stance that the central bank should not ease monetary policy "too quickly." Given this context, the likelihood of a back-to-back rate cut in July seems minimal. Attention will now shift to whether the Bank of Canada has room to cut interest rates at its September meeting, assuming no drastic economic surprises in the interim.

In broader currency markets, the Euro has turned broadly lower as its near term recovery momentum waned. The common currency remains overshadowed by uncertainties related to the French parliamentary elections, making a sustained bounce unlikely until the political situation clarifies. Australian and New Zealand Dollars, along with Swiss Franc, are among the weakest performers today too. In contrast, Dollar is showing strength, positioning as the second strongest currency after Canadian Dollar. Yen is also seeing some recovery, while British Pound is holding a middle ground.

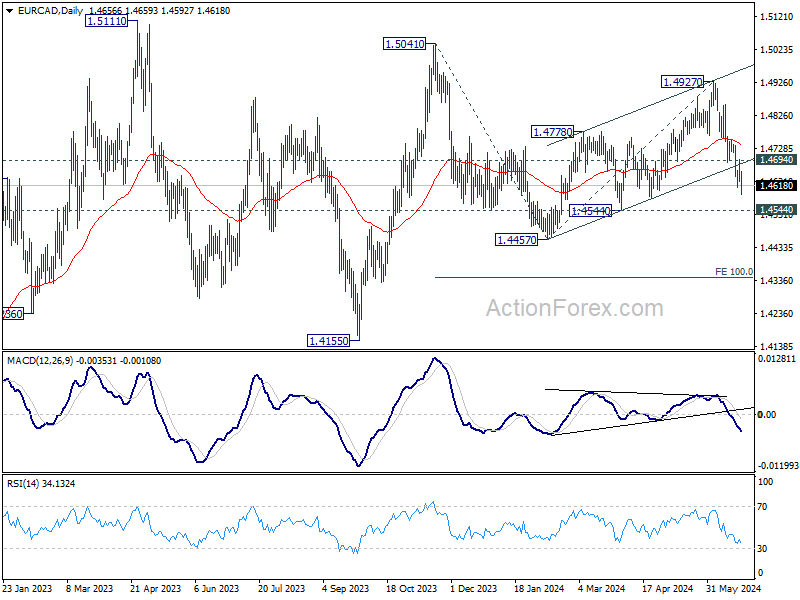

Technically, EUR/CAD's fall from 1.4927 resumed today after brief recovery. Corrective rise from 1.4457 should have completed with three waves up to 1.4927. Deeper decline is expected as long as 1.4694 resistance holds, to 1.4544 support. Decisive break there will argue that fall from 1.5041 is ready to resume through 1.4457 low.

In Europe, at the time of writing, FTSE is down -0.19%. DAX is down -0.99%. CAC is down -0.82%. UK 10-year yield is down -0.0129 at 4.071. Germany 10-year yield is down -0.017 at 2.405. Earlier in Asia, Nikkei rose 0.95%. Hong Kong HSI rose 0.25%. China Shanghai SSE fell -0.44%. Singapore Strait Times rose 0.37%. Japan 10-year JGB yield rose 0.0092 to 1.000.

Canada's CPI accelerates to 2.9% yoy, driven by service sector price hikes

Canada's CPI recorded a notable increase in May, climbing to 2.9% yoy from 2.7% yoy the previous month, surpassing the anticipated rate of 2.6%. This acceleration in headline CPI was primarily fueled by a significant uptick in service prices, which rose by 4.6% yoy in May, following a 4.2% yoy increase in April.

Diving deeper into the components, CPI median—which represents the midpoint of price changes—escalated from 2.6% yoy to 2.8% yoy, again outstripping the forecast of 2.6%. CPI trimmed, another measure that excludes extreme price movements, held steady at 2.9% yoy, also exceeding expectations of 2.8%. In contrast, CPI common, which reflects the common price changes across categories, slowed slightly from 2.6% yoy to 2.4% yoy, falling below the anticipated 2.6%.

On a monthly basis, the CPI rose by 0.6% mom in May, doubling the expected 0.3% mom increase. Similarly, the core CPI also increased by 0.6% mom, well above the forecast of 0.2%. This indicates a broader upward pressure on prices beyond just volatile categories.

Fed's Bowman: Inflation to remain elevated, rate hold necessary

Fed Governor Michelle Bowman, in a speech today, said her baseline outlook that US inflation will return to the 2% target, provided federal funds rate remains at its current level of 5.25-5.50% "for some time." She emphasized that Fed is "still not yet at the point" where it would be appropriate to lower the policy rate.

Bowman stressed the need for Fed to "consider a range of possible scenarios" as monetary policy decisions evolve. She remains "willing" to raise interest rates "should progress on inflation stall or even reverse."

Regarding inflation outlook, Bowman noted that since the beginning of 2024, there has been only "modest" progress on inflation. Core CPI has been running at 3.8% through May, which is significantly above the average inflation rate in the second half of last year. She expects inflation to "remain elevated for some time."

Bowman also highlighted several upside risks to inflation. She mentioned that it is unlikely that further supply-side improvements will continue to reduce inflation. Geopolitical developments could also pose additional risks. Furthermore, increased immigration and continued labor market tightness could lead to persistently high core services inflation.

Australia's Westpac consumer sentiment ticks up but still deeply pessimistic

Australia's Westpac Consumer Sentiment rose 1.7% mom to 83.6 in June. However, the index remains deeply pessimistic, well below neutral level of 100. Although assessments of personal finances and buyer sentiment have become less negative, concerns about inflation, interest rates, and economic growth continue to weigh heavily on consumers.

The sub-index tracking the 'economic outlook for the next 12 months' fell -5.7% mom to 78.5, marking its lowest level since last October. In contrast, the 'economic outlook for the next 5 years' sub-index saw a slight improvement, rising 2.1% mom to 94.1.

Regarding RBA monetary policy, Westpac noted that the upcoming Q2 CPI data, due on July 31, will be crucial. Westpac expects the update to confirm that weak demand is still exerting disinflationary pressure. This should provide RBA with sufficient confidence that upside risks are not materializing, reducing the likelihood of a rate hike.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0696; (P) 1.0721; (R1) 1.0760; More....

EUR/USD dips notably in early US session but stays in range above 1.0667. Intraday bias remains neutral at this point. Further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below. However, firm break of 1.0760 will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y May | 2.50% | 2.80% | 2.70% | |

| 00:30 | AUD | Westpac Consumer Confidence Jun | 1.70% | -0.30% | ||

| 12:30 | CAD | CPI M/M May | 0.60% | 0.30% | 0.50% | |

| 12:30 | CAD | CPI Y/Y May | 2.90% | 2.60% | 2.70% | |

| 12:30 | CAD | CPI Core M/M May | 0.60% | 0.20% | 0.20% | |

| 12:30 | CAD | CPI Median Y/Y May | 2.80% | 2.60% | 2.60% | |

| 12:30 | CAD | CPI Trimmed Y/Y May | 2.90% | 2.80% | 2.90% | |

| 12:30 | CAD | CPI Common Y/Y May | 2.40% | 2.60% | 2.60% | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | 7.00% | 7.40% | ||

| 13:00 | USD | Housing Price Index M/M Apr | 0.50% | 0.10% | ||

| 14:00 | USD | Consumer Confidence Jun | 100.2 | 102 |

Canada’s CPI accelerates to 2.9% yoy, driven by service sector price hikes

Canada's CPI recorded a notable increase in May, climbing to 2.9% yoy from 2.7% yoy the previous month, surpassing the anticipated rate of 2.6%. This acceleration in headline CPI was primarily fueled by a significant uptick in service prices, which rose by 4.6% yoy in May, following a 4.2% yoy increase in April.

Diving deeper into the components, CPI median—which represents the midpoint of price changes—escalated from 2.6% yoy to 2.8% yoy, again outstripping the forecast of 2.6%. CPI trimmed, another measure that excludes extreme price movements, held steady at 2.9% yoy, also exceeding expectations of 2.8%. In contrast, CPI common, which reflects the common price changes across categories, slowed slightly from 2.6% yoy to 2.4% yoy, falling below the anticipated 2.6%.

On a monthly basis, the CPI rose by 0.6% mom in May, doubling the expected 0.3% mom increase. Similarly, the core CPI also increased by 0.6% mom, well above the forecast of 0.2%. This indicates a broader upward pressure on prices beyond just volatile categories.

Canadian Dollar Eyes Inflation Release

The Canadian dollar is showing limited movement on Tuesday. USD/CAD is trading at 1.3675 in the European session, up 0.12% on the day at the time of writing. We could see some volatility in the North American session, when Canada releases the May CPI report. In the US, today’s highlights are the CB Consumer Confidence index and the Richmond Manufacturing index.

Canada’s inflation rate expected to fall

Canada’s annual inflation rate is projected to dip to 2.6% in May, compared to 2.7% in April, which was the lowest rate since March 2021. Monthly, inflation is expected to ease to 0.3%, down from 0.5% in April.

With inflation on a downward path, the markets are keeping a close eye on the Bank of Canada, which lowered rates earlier in June for the first time since its rate-hike cycle began in March 2022. The cut showed that the central bank was willing to make a major shift in policy and deliver a rate cut even with inflation above the BoC’s 2% target.

The BoC won’t cut for a second time, however, until it is convinced that inflation is on the decline, which makes today’s CPI release a key factor in the BoC’s rate plans. A decline in today’s inflation report could set the stage for a back-to-back rate cut at the July 18th meeting.

The central bank is taking a cautious approach to further rate cuts and has stressed that each rate decision will be taken one at a time, based on the data. Governor Macklem said earlier this week that he doesn’t want to lower rates too quickly and jeopardize the success that the BoC has made in bringing inflation down.

USD/CAD Technical

- USD/CAD is testing resistance at 1.3675. Above, there is resistance at 1.3695

- 1.3637 and 1.3614 are the next support levels