Sample Category Title

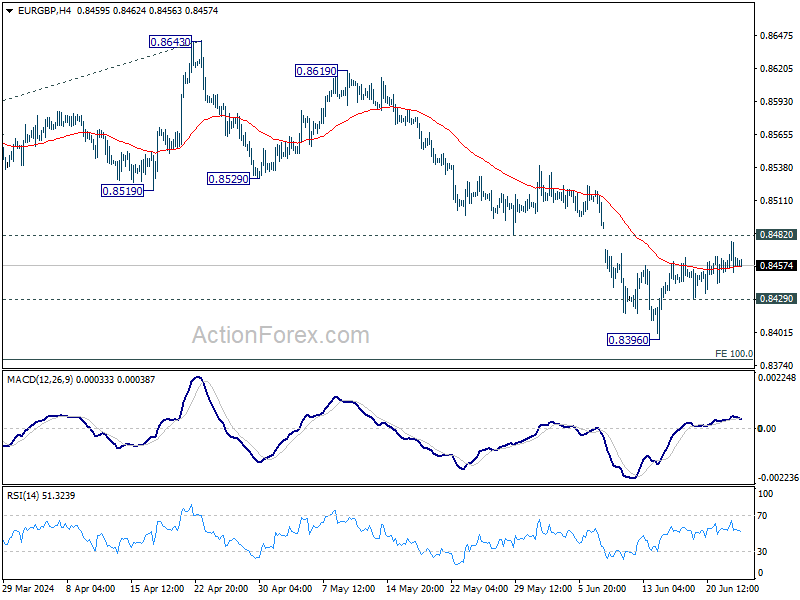

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8450; (P) 0.8464; (R1) 0.8476; More...

EUR/GBP is still extending the consolidation pattern from 0.8396 and intraday bias stays neutral. Outlook will stay bearish as long as 0.8482 support turned resistance holds. On the downside, below 0.8429 minor support will bring retest of 0.8396 low first. Further break there will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

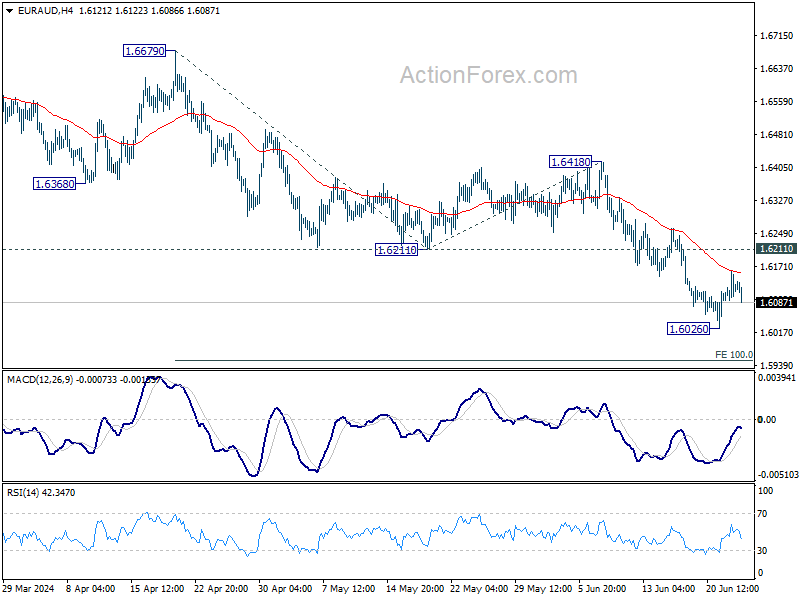

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6090; (P) 1.6125; (R1) 1.6161; More...

Intraday bias in EUR/AUD stays neutral at this point. Consolidation from 1.6026 could extend further, but upside should be limited by 1.6211 support turned resistance to bring another fall. Below 1.6026 will turn bias back to the downside for 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

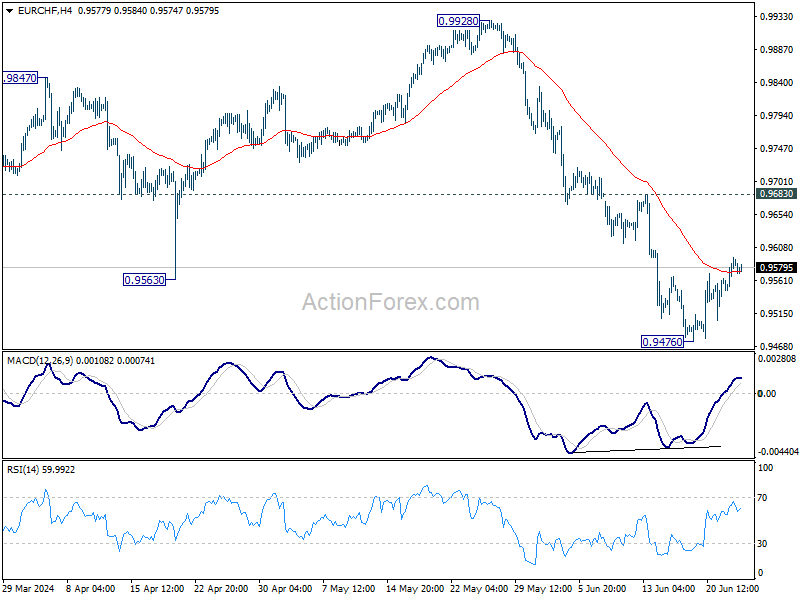

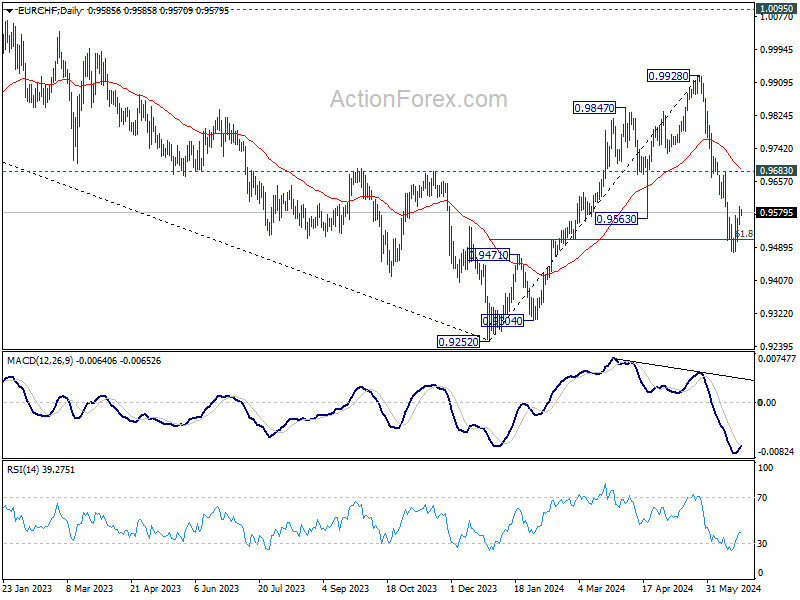

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9553; (P) 0.9574; (R1) 0.9606; More....

Intraday bias in EUR/CHF remains neutral for the moment and outlook is unchanged. Consolidation from 0.9476 could extend with stronger recovery. But outlook will remain bearish as long as 0.9683 resistance holds. On the downside, break of 0.9476, and sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will bring retest of 0.9252 low next.

In the bigger picture, rebound from 0.9252 should have completed at 0.9228. Medium term outlook remains bearish with 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

EUR/USD Has Little Upward/Rebound Potential

Markets

Fuss about potential Japanese FX interventions (USD/JPY 160) and more French political scenario’s dominated headlines yesterday, but failed to inspire trading. European risk sentiment improved with key indices rising by 0.5% to 1.5%. Safe haven assets like core bonds and the dollar travelled the other direction, resulting in marginally higher German yields and EUR/USD reconquering 1.07 (close 1.0733). Sentiment soured after European close with AI-darlings correcting from recent record races. The S&P 500 (-0.3%) and Nasdaq (-1.1%) ended with losses, fueling a late bid in US Treasuries. Comments by San Francisco Fed Daly (voter this year) were interesting. She stressed that at this point, inflation is not the only risk that the Fed faces. Daly admits that the labour market so far adjusted slowly with the unemployment rate only edging up. She fears though that we are getting nearer to a point where that benign outcome could be less likely. “Future labour market slowing could translate into higher unemployment, as firms need to adjust not just vacancies, but actual jobs”. Daly urged policy makers to remain vigilant to both inflation and labour market risks. If inflation falls more slowly than expected, Daly said it would be appropriate to hold interest rates higher for longer. If inflation falls quickly or the labor market cools more than expected, cutting rates would be necessary. From a risk/positioning point of view, we follow Daly’s reasoning. The bumpy inflation path ahead certifies the June FOMC dot plot calling for only one policy rate cut this year. A sudden weakening of the labour market is a bigger risk to this scenario that the inflation path.

Today’s eco calendar is empty in Europe. Some ECB members speak, but the focus gradually turns to next week’s Sintra symposium, the ECB’s equivalent of the end of August Jackson Hole meeting by the Fed. The US calendar is more interesting with house prices, Richmond Fed manufacturing index and especially consumer confidence. Speeches by Fed Bowman and Cook and the start of the US Treasury’s end-of-month refinancing operation serve as a wildcard. Going into Friday’s PCE deflators and with the end of quarter looming, we err on the side of a decent bid for US Treasuries. A bigger correction in (US) tech stocks would also fit this view. Together with this weekend’s French elections is why we stick to the view that EUR/USD has little upward/rebound potential even in case of softer US data. Intervention bells in USD/JPY (159.42) are still ringing.

News & Views

Australian consumer confidence as measured by the Westpac-Melbourne Institute improved modestly in June rising from 82.2 to 83.6, but remains well below the 100 level that signals the balance between pessimists and optimists. According to comments from Westpac, “the survey detail suggests positives from fiscal support measures are being negated by increased concerns about inflation and the outlook for interest rates”. Fiscal support measures made consumers turning more positive on current and future family finances. They also showed more preparedness to buy major household items. At the same time, consumers turned much more negative on the economy for the next year (-5.7%). Also intentions to buy a dwelling declined substantially. The survey comes as the Reserve bank of Australia at its June 19 meeting indicated that inflation has been easing more slowly than expected and that it remains prepared to do what is necessary to bring inflation back to target. The Aussie dollar continues trading in a tight range between 0.6575 and 0.6715 (currently 0.6665).

Argentina entered a technical recession in the first quarter of this year. Activity contracted 2.6% Q/Q after a decline of 2.5% in the final quarter of last year. Activity in Q1 was 5.1% lower compared to the same period last year. The recession comes as president Milei tries to restore public finances via aggressive spending cuts. Private consumption declined 6.7% Y/Y. Also public consumption was 5% lower. Imports shrank by 20.1% while exports rose 26.1%. Due to the contraction in activity the unemployment rate rose from 5.7% in Q4 2023 to 7.7%.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative (France) dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. This might cap further sterling gains. At the same time, the euro remains vulnerable to political event risk going into the French elections. EUR/GBP 0.84 is becoming solid support.

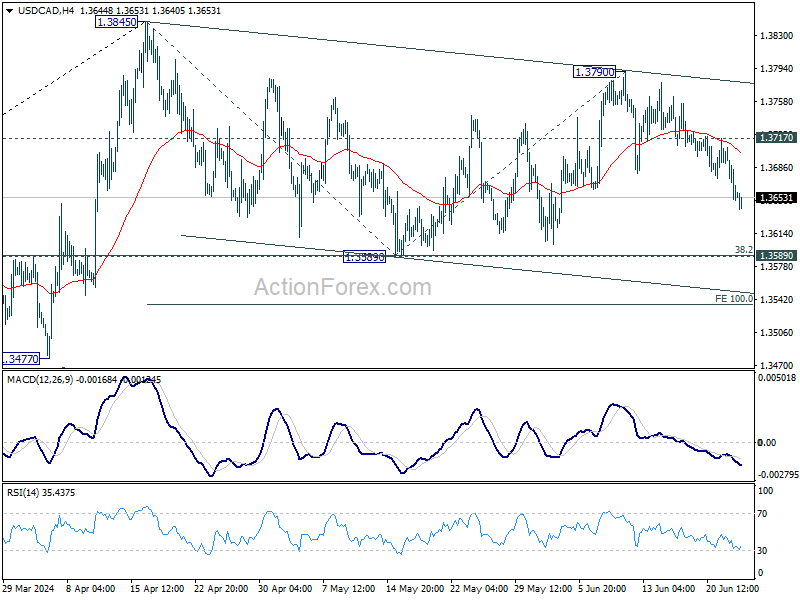

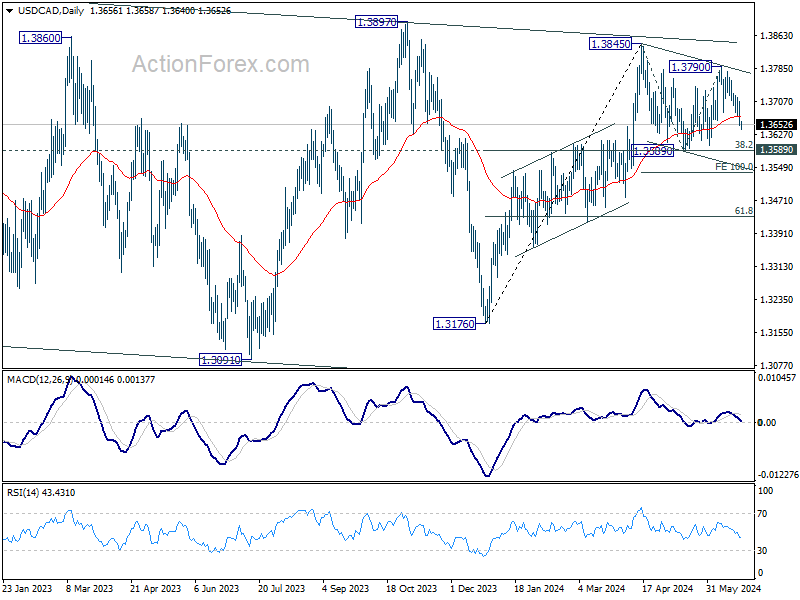

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3637; (P) 1.3672; (R1) 1.3695; More...

USD/CAD's extended fall from 1.3790 suggests that rebound form 1.3589 has completed. Corrective pattern from 1.3845 is now in the third leg. Intraday bias is back on the downside for 1.3589 support. Break there will target 100% projection of 1.3845 to 1.3589 from 1.3790 at 1.3534. On the upside, above 1.3717 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

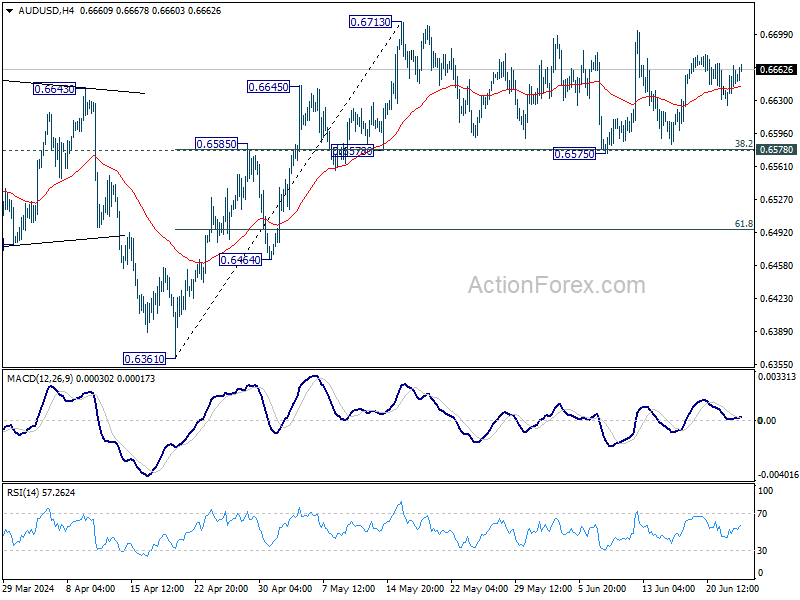

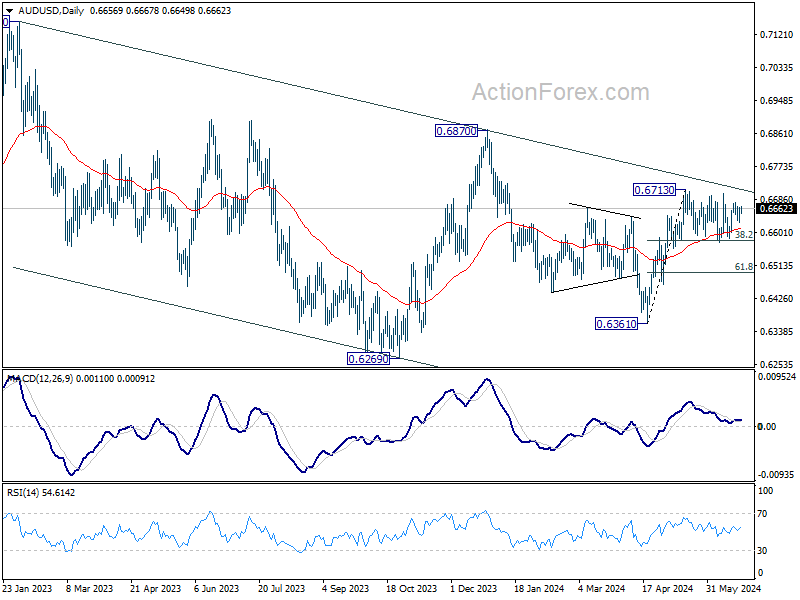

AUD/USD Daily Report

Daily Pivots: (S1) 0.6633; (P) 0.6650; (R1) 0.6675; More...

AUD/USD is still bounded in consolidation from 0.6713 and intraday bias stays neutral. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

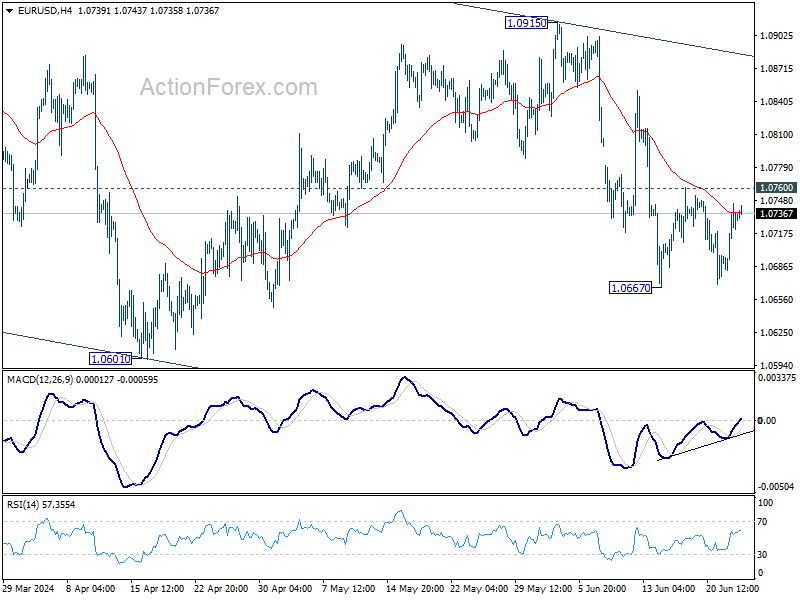

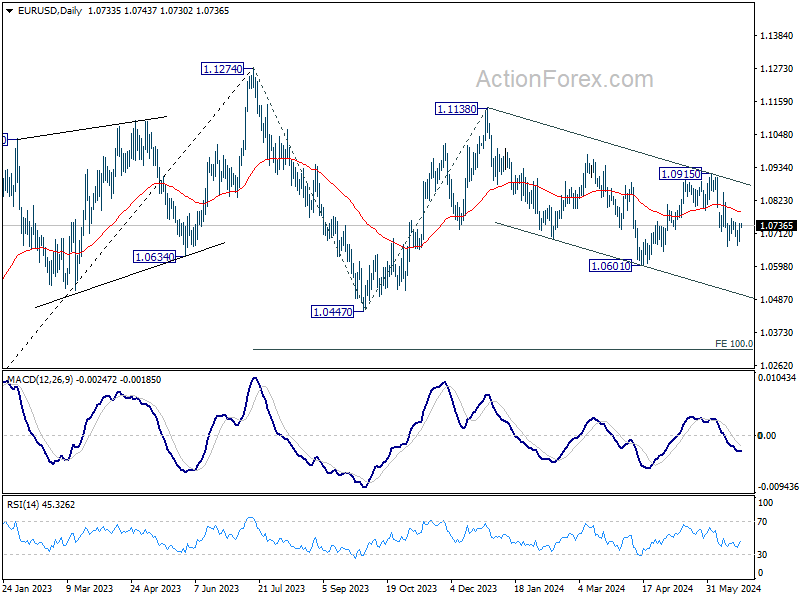

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0696; (P) 1.0721; (R1) 1.0760; More....

EUR/USD is extending the consolidations from 1.0667 and intraday bias stays neutral. Further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below. However, firm break of 1.0760 will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

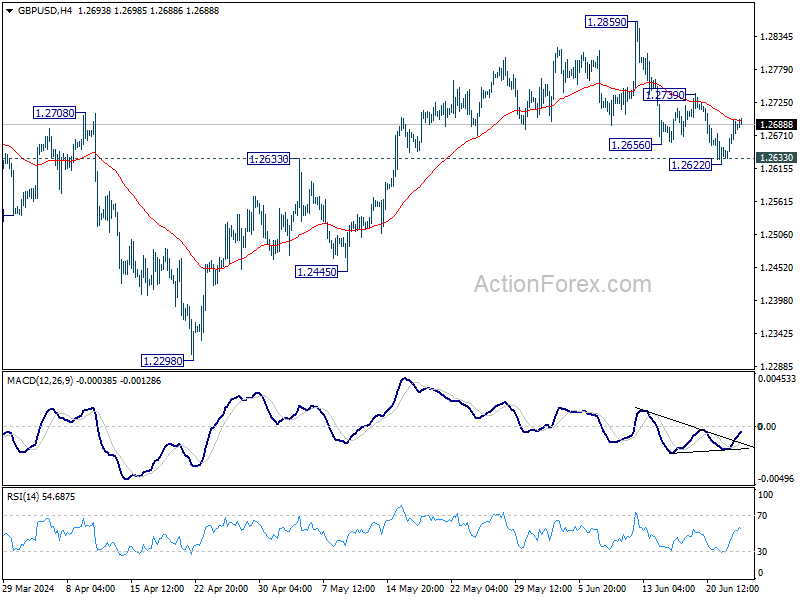

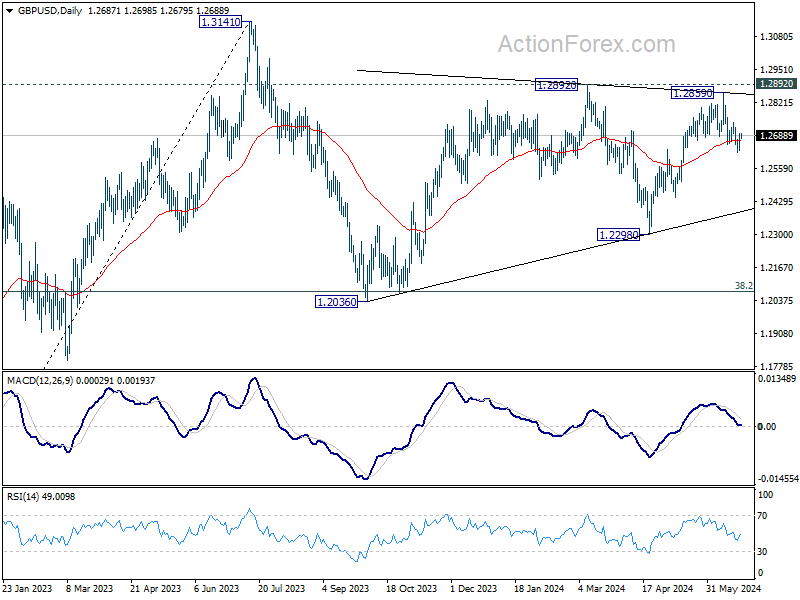

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2647; (P) 1.2672; (R1) 1.2712; More...

Intraday bias in GBP/USD remains neutral for the moment. Further decline is expected as long as 1.2739 resistance holds. Break of 1.2622, and sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. However, firm break of 1.2739 will argue that pull back from 1.2859 has completed, and bring retest of this high instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8919; (P) 0.8932; (R1) 0.8943; More….

USD/CHF is still bounded in consolidation from 0.8825 and intraday bias stays neutral at this point. Near term outlook remains bearish with 0.8992 resistance intact. Break of 0.8825 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

Tech Down, Energy Up

The selloff in Nvidia deepened yesterday and sent the shares into the correction territory following a 10% selloff. Nvidia shares erased around $430 bn in market cap over the past three sessions. The selloff hit suddenly, right after the company stole the status of the world’s most valuable company from Microsoft last week. There has been no bad news regarding the company’s fundamentals on the newswire, no analyst downgrades, no soft forecasts, no rumours of slowing sales. It’s just that the end of last quarter and the first half may have brought some investors to take some profit and go to the sidelines.

One question that everyone asks is, whether last week’s good news marked the finale of the Nvidia’s surge to the top, and if the past three-day selloff is the beginning of a sharper downside correction. I don’t have the answer to that question, the time will tell. Yes, there has certainly been strong speculation in Nvidia’s exponential surge since the beginning of last year. And yes, strong rallies were often followed by sharp selloffs. In this context, Nvidia probably has ways to correct before finding a more reasonable valuation.

From a technical perspective, the first support is seen near $110 a share, the minor 23.6% Fibonacci retracement on the AI rally that started at the beginning of last year with the launch of OpenAI’s ChatGTP. The 50-DMA, just above the $100 psychological support presently, could act as another support and finally, the major support to the AI rally is the $92 per share level, the major 38.2% Fibonacci retracement should, in theory, distinguish between the actual AI rally and a medium term bearish reversal.

The other question in minds is if the price pullback a good opportunity to strengthe long position at a better price before Nvidia announces its Q2 earnings, where it’s expected to reveal a monstruous $28bn sales, which is more than the double of money is made the same time last year.

In all cases, it’s too early to call the end of the Nvidia-mania, but given the high amount of speculation around the stock, we shall see the price action gets worse before it gets better.

Elsewhere, fortunes for Apple are improving as the company – who have lagged its peers in the AI rally – found an opportunity window to bring investors back on board and that opportunity window is offering the AI tools developed by others on their iPhones – with free partnerships – to see if people would buy the latest AI-boosted models. In this context, Apple announced that it would integrate Meta’s Llama 3 AI to its products, after it announced earlier that it would also offer OpenAI’s ChatGPT on iPhones. It’s a genius move, let’s see if it could make the AI rally change hands!

Energy smiles

Yesterday’s 6.68% plunge in Nvidia shares didn’t do good to mood in Nasdaq 100. The index dropped more than 1% whereas losses in the S&P500 remained limited to 0.31%, as the financials gained 0.63% while energy sector rallied 1.70% on the back of a rebound in crude oil to retest the $82pb level resistance, the major 61.8% level on the latest selloff. If this level is cleared, oil bulls will have a higher conviction on the sustainability of the rally and the gains could extend toward the $85pb level. The question is, do the soft economic data around the world justify a further rise in oil prices? Chinese growth is still not as strong as it should be, German business expectations unexpectedly declined for the first time in five months and the latest data from the US hinted at a faster-than-anticipated slowdown in the US economy. On the other hand, the central banks expectations aren’t easing enough to compensate for the slowing Western economies. So I’m wondering if we could see enough conviction above the $82pb level to carry this rally higher. And also, I’m wondering whether higher oil prices wouldn’t boost inflation expectations and jeopardize soft central bank expectations and limit the upside.

In the FX

The US dollar index eased yesterday, as the weekend euro bears scaled back their positions after the weekend. The EURUSD rebounded to near 1.0750. We could see the euro recover against the greenback in the first half of the year but I would expect the bears to come back in charge before the weekend, as the first round of the French legislative elections are due this weekend and political risks remain high as Marine Le Pen’s National Rally is seen getting more than a third of the votes. Elsewhere, the USDJPY trades a touch below the critical 160 level as the yen bears are testing the nerves of the Japanese officials to see what level will trigger an FX intervention. In Canada, the Loonie benefits from a rise in oil prices. Due today, data is expected to show a further slowdown in Canadian inflation and could fuel the expectation that the Bank of Canada (BoC) could continue pulling its rates lower. But we could see oil prices weigh heavier in the balance than rate cut expectations if crude prices break above a key resistance.