Sample Category Title

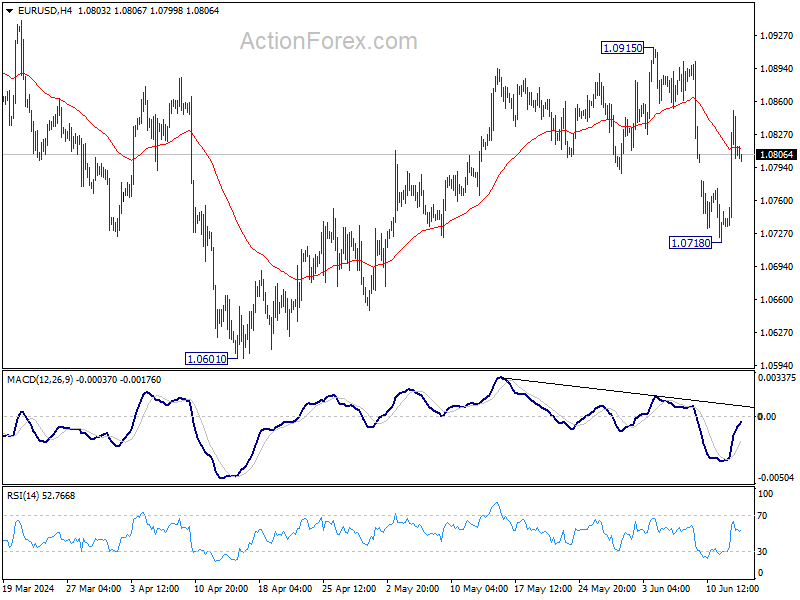

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0745; (P) 1.0799; (R1) 1.0862; More....

Intraday bias in EUR/USD is turned neutral again first with current retreat. On the upside, firm break of 1.0915 will resume whole rise from 1.0601. On the downside, break of 1.0718 will resume the fall from 1.0915 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, which might still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. Nevertheless, on the upside, firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2733; (P) 1.2796; (R1) 1.2862; More...

Near term outlook in GBP/USD will stay bullish as long as 1.2687 support holds. Rise from 1.2298 should target 1.2892 resistance. Decisive break there will strengthen the case that correction from 1.3141 has completed, and bring further rally to retest this high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

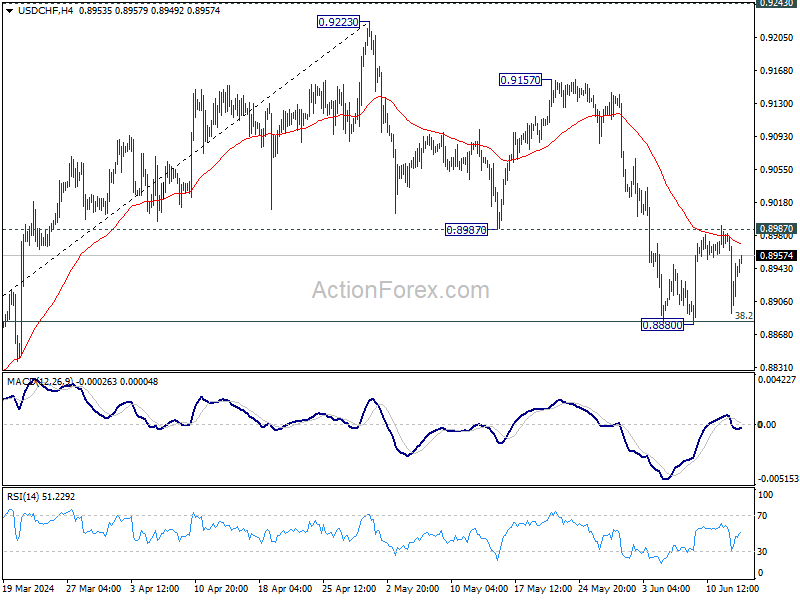

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8897; (P) 0.8940; (R1) 0.8988; More….

Intraday bias in USD/CHF remains neutral as range trading continues between 0.8880/8987On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

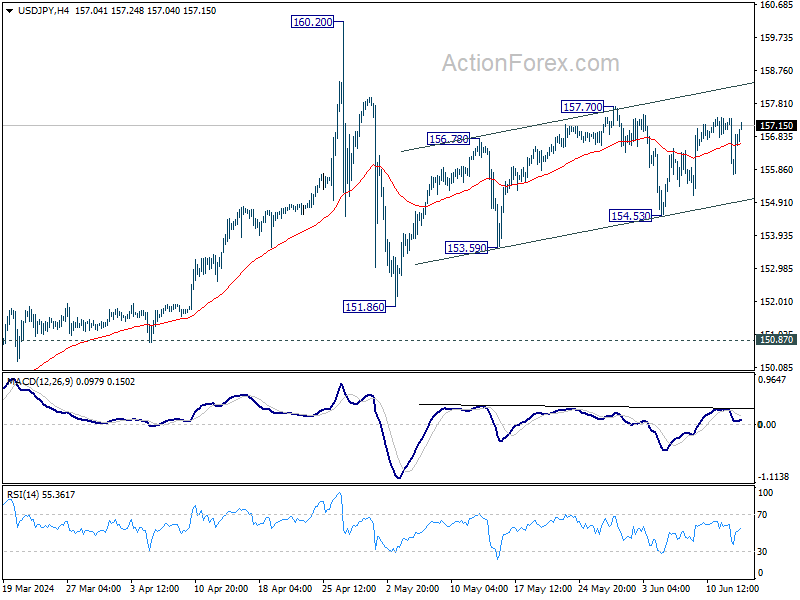

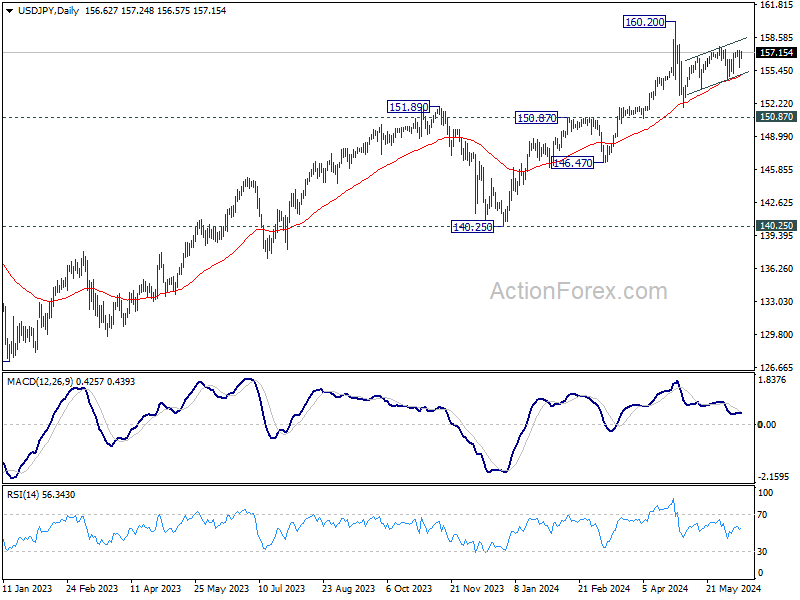

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.84; (P) 156.61; (R1) 157.49; More...

Intraday bias in USD/JPY remains neutral first as range trading continues inside 154.53/157.70.On the downside, break of 154.53 will turn bias to the downside for 151.86 support and possibly below, as the third leg of the corrective pattern from 160.20. On the upside, break of 157.70 will resume the whole rise from 151.86 and target 160.20 high.

In the bigger picture, a medium term top should be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

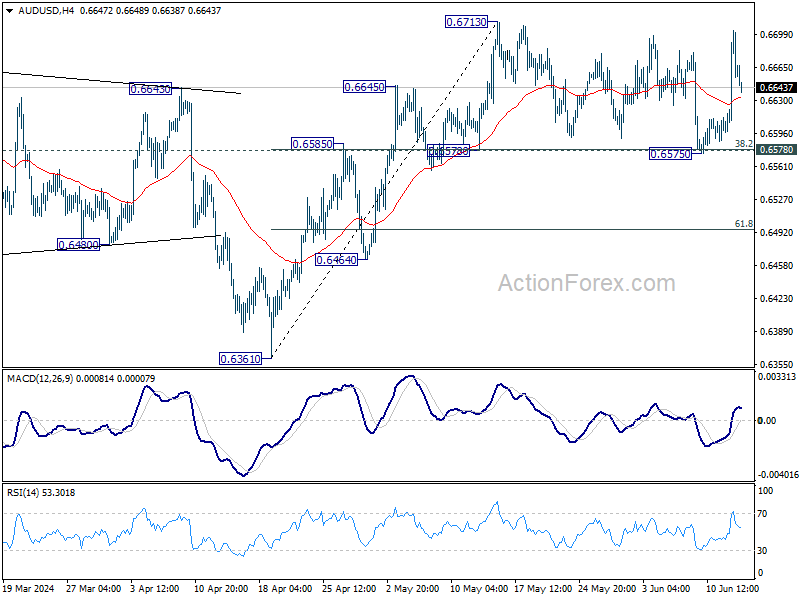

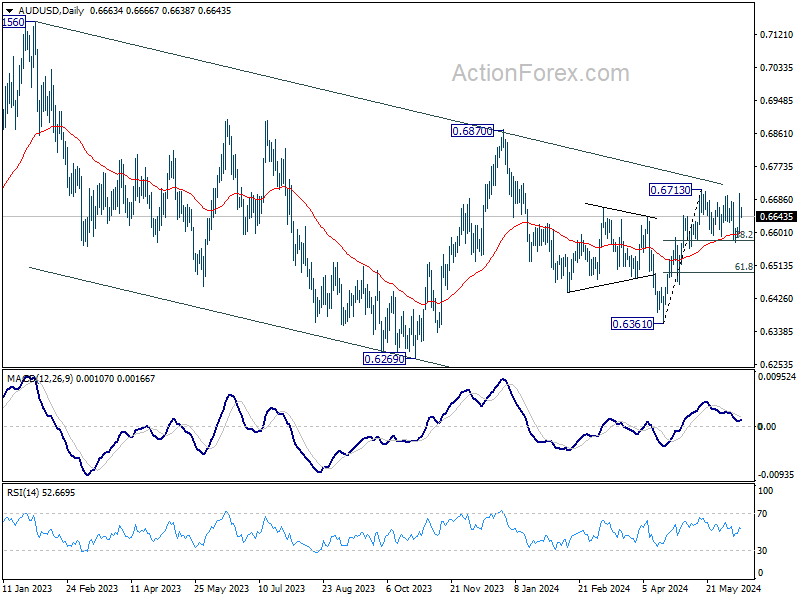

AUD/USD Daily Report

Daily Pivots: (S1) 0.6605; (P) 0.6655; (R1) 0.6713; More...

Despite strong rebound, AUD/USD failed to break through 0.6713 resistance and retreated sharply. Intraday bias remains neutral at this point. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) will bring deeper fall to 61.8% retracement at 0.6495 instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Dollar Pared Some of Sharp Losses in Wake of Fed

Markets

The Fed kept the policy rate unchanged at 5.25-5.5% yesterday. The expected decision was accompanied by a statement that mentioned “modest” further progress towards the 2% inflation objective instead of the “lack” of it in the May edition. It’s the only change and feels like a post-CPI addition. The dot plot entailed bigger changes though and moved from three cuts to just one this year – be it narrowly. The 2025 median forecast shifted from three to four (to 4-4.25%) with the 2026 prediction at an unchanged 3-3.25%. The neutral rate shifted further north from 2.56% to 2.75%. It takes just one more participant to adjust his/her view to 3% to tilt the general balance towards this level. That would surely have drawn more market attention than yesterday’s upgrade did. Inflation forecasts were revised higher for 2024 (2.6% headline, 2.8% core) and 2025 (both 2.3%), reflecting in part the negative surprises from Q1. Chair Powell during the presser referred to the predictions as being conservative. They changed little to nothing to growth and unemployment forecasts. Based on the dots and Powell’s comments, the first rate cut and follow-ups are more than anything else just a matter of timing. Demand is cooling and the labour market has moved back towards a pre-Covid state. But the chair said the inaugural move is a consequential one and before deciding on it they want to gain more confidence first. US yields jumped in the wake of the Fed but that had more to do with the low starting point, caused by slower-than-expected CPI numbers (0.0% m/m headline, 0.2% core) hours earlier. Net daily changes eventually amounted to losses of -6.2 (30-yr) to -10.2 bps (5-yr). Given current market pricing for 2024 & 2025 and with few important economic data in the next two weeks or so, we think US rates are likely to trade sideways for the time being. Yesterday’s intraday lows (front end and back end) mark a solid bottom. The dollar pared some of the sharp losses in the wake of the Fed. EUR/USD returned from a high around 1.085 to 1.081, still up from the 1.074 at the open. DXY opened at 105.27, found support at 104.26 and finished at 104.64 from an 105.27. Today’s PPI’s and weekly jobless claims in the US may trigger some volatility but are unlikely to move the needle permanently. The 30-yr USD 22bn bond auction tonight follows Tuesday’s strong 10-yr one. The dust seems to have settled a bit in Europe after the elections and Macron’s political gamble. But uncertainty will continue to linger in coming weeks. We continue to keep a close eye on peripheral and (semi-) core swap spreads which continued to increase slightly in the case of France yesterday. The euro’s upside is capped short term, allowing for some correction lower within the 1.06-1.09 trading range. EUR/GBP is trying to recoup some of the heavy losses incurred over the previous days. Technically, though, the picture remains challenging.

News & Views

Solid Australian labour market data for the month May bolster the Reserve Bank of Australia’s case for its higher-for-longer strategy. The economy added 39.7k jobs (vs +37.4k in April). While close to consensus, it’s interesting to see that full time occupations accounted for a 41.7k increase, with part-time jobs sliding by 2.1k. Last month it was the other way around. The unemployment rate ticked lower, from 4.1% to 4% with a stable (following upward revision to April figures) participation rate of 66.8%. The head of the Australian Bureau of Statistics said that "The employment-to-population ratio and participation rate both continue to be much higher than their pre-pandemic levels. Together with elevated levels of job vacancies, this suggests the labour market remains relatively tight, though less than in late 2022 and early 2023”. The Aussie dollar failed to profit from the numbers with AUD/USD currently changing hands around 0.6650 after yesterday’s volatile session (including test of YTD top near 0.67).

The UK RICS’s monthly net balance of house prices fell to -17 in May, the lowest level since January, from a downwardly revised -7 in April. The gauge of new buyer enquiries fell to the lowest since November (-8 from -1). New instructions (16 from 25) and agreed sales (-13 from 4) also recorded steep drops. RICS commented that the recent recovery across the UK housing market appears to have slipped into reverse of late, with buyer demand losing momentum slightly on the back of the upward moves seen in mortgage rates over the past couple of months. Nevertheless, expectations point to this delaying, rather than derailing, a modest improvement going forward. Sales expectations indeed rose from 0 to 6 with price expectations broadly unchanged at -12.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. The German 10y yield set a new YtD top at 2.7%.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield remains stuck in the 4.3/4.7% trading range.

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.

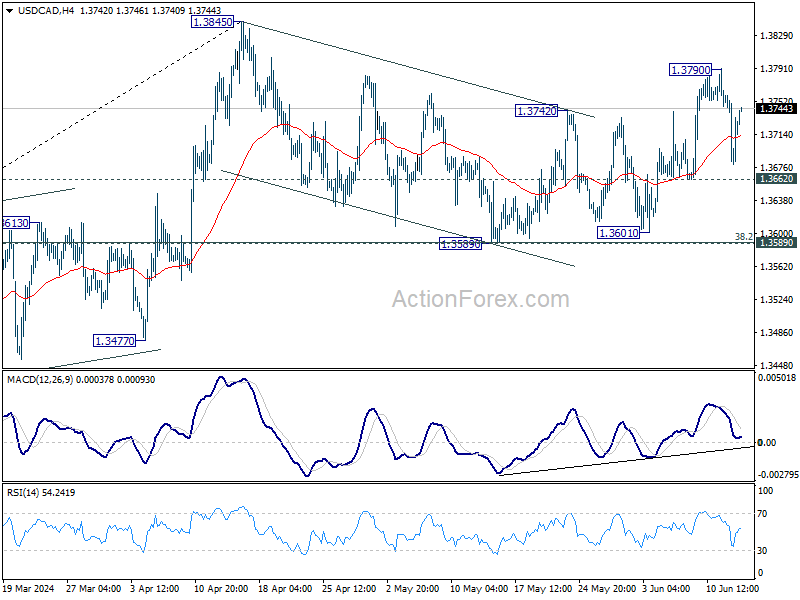

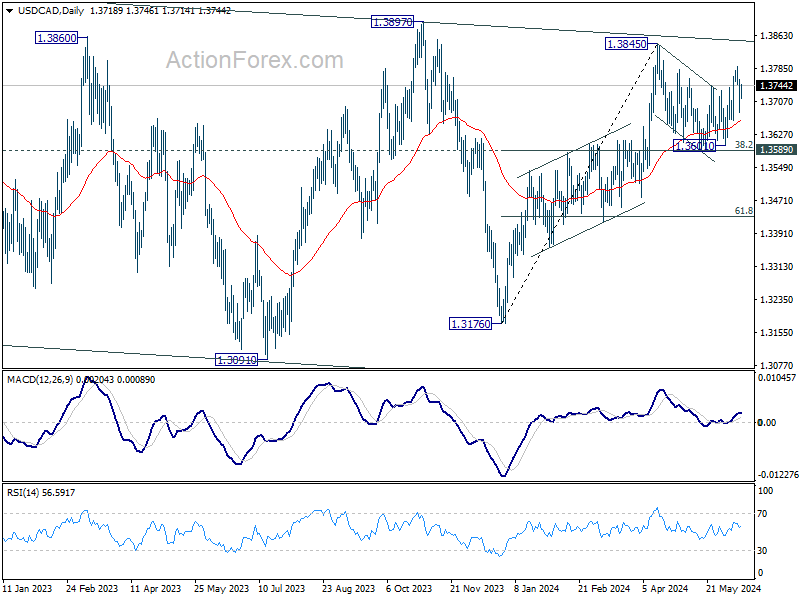

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3682; (P) 1.3722; (R1) 1.3764; More...

Despite steep retreat, USD/CAD recovered strongly ahead of 1.2662 support. Intraday bias stays neutral first. On the upside, above 1.3790 will resume the rebound from 1.3589 to retest 1.3845 high. Firm break there will resume larger rally. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Dollar Stabilizes After FOMC Projections, Eyes on US PPI and Jobless Claims

While Dollar had a sharp decline following US consumer inflation data overnight, the selloff was short-lived. The greenback stabilized and recovered after FOMC projections indicated that only one rate cut is likely this year. Stock and bond markets showed little reaction to Fed's announcement. Attention now turns to upcoming US PPI and jobless claims data for further market direction.

In the broader forex market, Japanese Yen remains the weakest currency of the week. BoJ's policy decision tomorrow is unlikely to offer much support. However, Yen's selloff is somewhat contained as traders remain cautious about risks of intervention. Dollar is the second weakest, followed by Euro, which continues to grapple with political instability in France and the EU.

On the other hand, New Zealand Dollar is the strongest performer this week. Australian Dollar is the second strongest, but showed little reaction to slightly better-than-expected employment data. British Pound ranks third, benefiting additionally from Euro's weakness. Swiss Franc and Canadian Dollar are positioned in the middle.

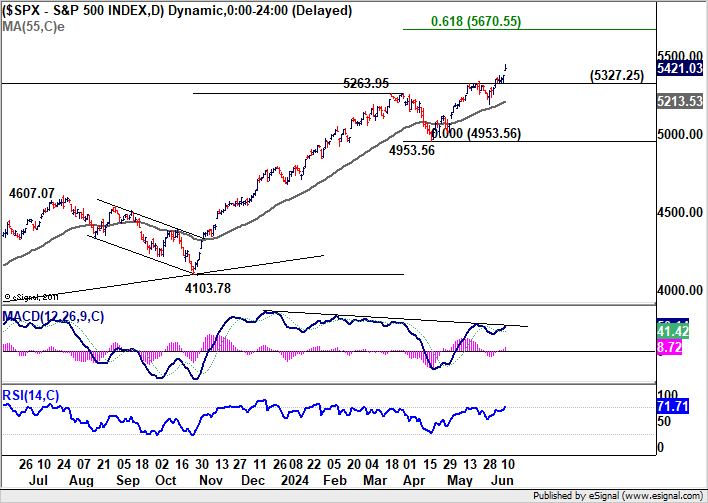

Technically, S&P 500's up trend appears to be finally picking up momentum with yesterday's post-CPI rise. Further rally is now expected as long as 5327.25 support holds. Next target is 61.8% projection of 4103.78 to 5263.95 from 4953.56 at 5670.55. On the downside, break of 5327.25 will bring consolidations first before staging another upmove.

In Asia, Nikkei fell -0.44%. Hong Kong HSI is up 0.40%. China Shanghai SSE is down -0.21%. Singapore Strait Times is up 0.54%. Japan 10-year JGB yield is down -0.0133 at 0.976. Overnight, DOW fell -0.09%. S&P 500 rose 0.85%. NASDAQ rose 1.53%. 10-year yield fell -0.109 to 4.295.

Fed's balanced projections have something for both hawks and doves

S&P 500 and NASDAQ extended their record runs overnight, but that was mainly fueled by softer-than-expected May US CPI data. Market reaction to FOMC's rate decision was indeed subdued, reflecting the balanced nature of the new economic projections and dot plot, which offered something for both hawks and doves.

On the hawkish side, the median projection now indicates only one rate cut this year, a sharp shift from the three cuts anticipated back in March. The balance of the dot plot showed 11 members favoring one or no cuts versus 8 members advocating for two cuts, indicating a significant hurdle for those seeking more aggressive rate reductions.

Although some argue that not all FOMC members vote on policy decisions, potentially making the actual voting balance more dovish, it's clear that Fed will require further encouraging inflation data, similar to the yesterday's May CPI figures, before considering any policy easing.

Another hawkish signal was the increase in the long-run "neutral" rate from 2.6% to 2.8%. This rate has now risen by more than a quarter of a percentage point over Fed's last two sets of projections. That suggests officials believe inflation will be more challenging to control in the future. However, Fed Chair Jerome Powell downplayed the significance of this increase, noting that it does not necessarily influence short-term rate projections.

On the dovish side, no FOMC members projected another rate hike, compared to two who had previously indicated the possibility of one more hike. This consensus suggests that all policymakers prefer to maintain the current interest rate level to combat inflation rather than tightening further, which should reassure most investors.

Going forward, Powell emphasized that Fed would make decisions based on the totality of incoming data rather than pre-determining future actions. He elaborated, "it's going to be not just the inflation readings. It's going to be the totality of the data, what's happening in the labor market, what's happening with the balance of risks, what's happening with the forecasts, what's happening with growth."

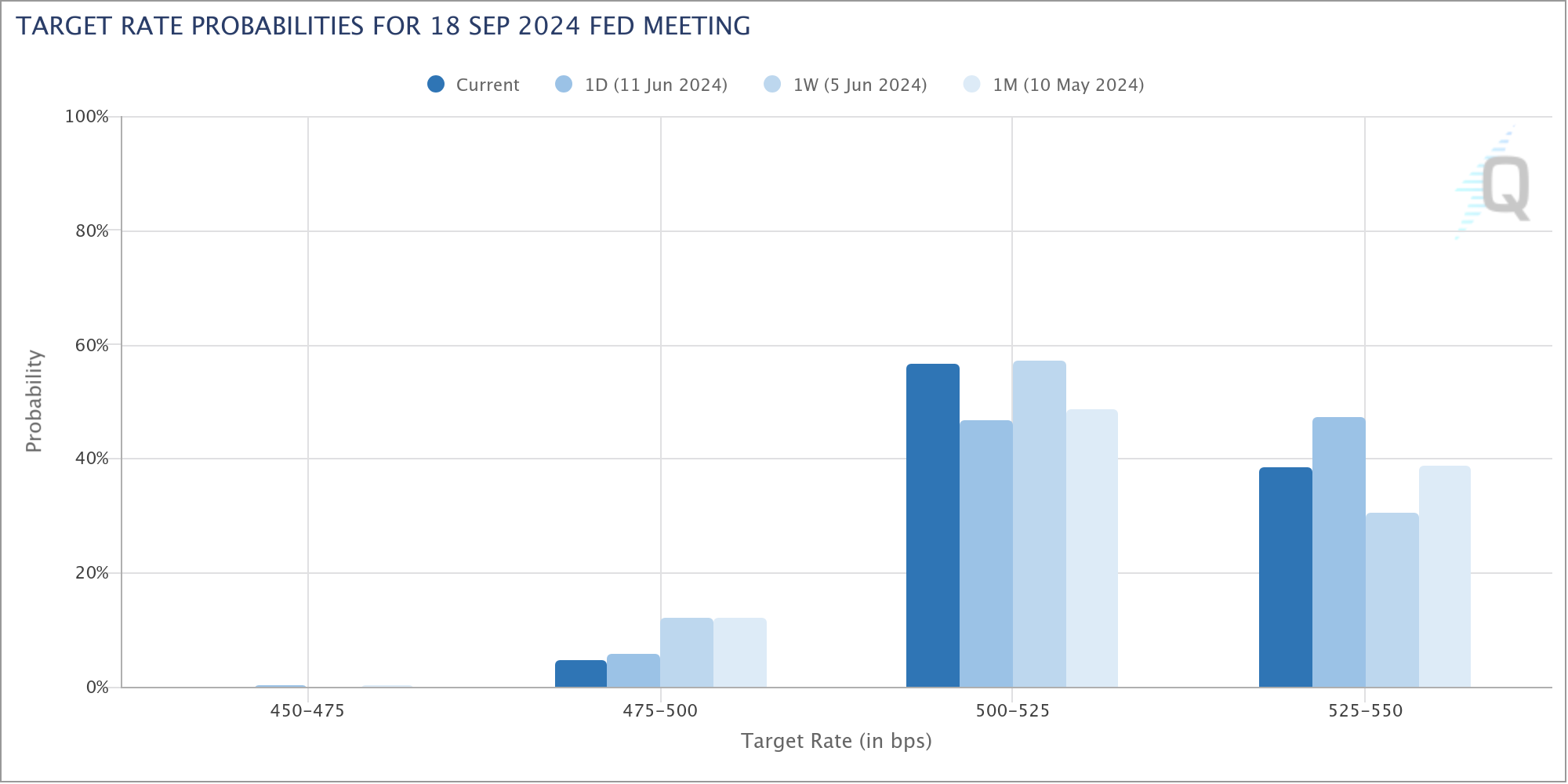

Currently, Fed funds futures indicate a 61% chance of a rate cut in September, even lower than the 69% chance a week ago before the release of strong non-farm payroll data. The odds would likely continue to fluctuate in the current range until significant progress is seen in disinflation.

Australia's employment rises 39.7k, labor market remains relatively tight

Australia's labor market demonstrated resilience in May, with employment increasing by 39.7k, slightly surpassing expectations of 39.0k. Full-time jobs saw a significant rise of 41.7k, while part-time jobs experienced a slight decline of -2.1k.

Unemployment rate decreased from 4.1% to 4.0%, aligning with market forecasts. Key labor metrics, such as the employment-to-population ratio and the participation rate, remained steady at 64.1% and 66.8%, respectively. However, monthly hours worked dipped by -0.5% on a month-over-month basis.

Bjorn Jarvis, ABS head of labor statistics, highlighted that the number of unemployed people, though nearing 600k, is still about 110k fewer than in March 2020, before the pandemic.

Additionally, both the employment-to-population ratio and participation rate are significantly higher than pre-pandemic levels. Jarvis pointed out that these factors, along with sustained high job vacancy levels, indicate that the labor market "remains relatively tight, though less so than in late 2022 and early 2023."

Looking ahead

Swiss PPI and Eurozone industrial production will be released in European session. Later in the day, US will publish PPI and jobless claims.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3682; (P) 1.3722; (R1) 1.3764; More...

Despite steep retreat, USD/CAD recovered strongly ahead of 1.2662 support. Intraday bias stays neutral first. On the upside, above 1.3790 will resume the rebound from 1.3589 to retest 1.3845 high. Firm break there will resume larger rally. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance May | -17% | -5% | -5% | -7% |

| 23:50 | JPY | BSI Large Manufacturing Index Q2 | -1 | -5.2 | -6.7 | |

| 01:30 | AUD | Employment Change May | 39.7K | 39.0K | 38.5K | 37.4K |

| 01:30 | AUD | Unemployment Rate May | 4.00% | 4.00% | 4.10% | |

| 06:30 | CHF | PPI M/M May | 0.50% | 0.60% | ||

| 06:30 | CHF | PPI Y/Y May | -1.80% | |||

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 0.10% | 0.60% | ||

| 12:30 | USD | PPI M/M May | 0.20% | 0.50% | ||

| 12:30 | USD | PPI Y/Y May | 2.20% | 2.20% | ||

| 12:30 | USD | PPI Core M/M May | 0.30% | 0.50% | ||

| 12:30 | USD | PPI Core Y/Y May | 2.30% | 2.40% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 7) | 227K | 229K | ||

| 14:30 | USD | Natural Gas Storage | 75B | 98B |

Fantastic, Then

The Federal Reserve’s (Fed) dot plot plotted one rate cut for 2024, down from three in March and the Fed revised its inflation forecasts higher. But the Fed’s announcement didn’t get more hawkish than this because the distribution of the dots was much narrower than in March; 7 members plotted a one-cut preference while 8 members favoured two cuts, and 4 suggested that the Fed should not cut rates this year but hey… As a result, the distribution of the dots between those who voted for one and two rate cuts was more dovish than I expected. Plus, the dots also suggested 4 rate cuts in 2025 instead of 3, so one rate cut just jumped over to the next calendar year. And finally, we heard the Fed tweak its communication slightly: they no longer think that there is a ‘lack’ of progress in inflation toward the 2% goal but a ‘modest further progress’ instead. And that’s a big deal for the doves obviously because a progress is a progress even if it’s small. And the cherry on top, the CPI update that came in a few hours before the policy announcement was softer-than-expected. Both headline and core CPI printed a weaker-than-expected figure in May on both monthly and yearly basis, and core inflation even cooled to the slowest pace in more than 3 years. Fantastic.

The US 2-year yield tipped a toe below 4.70% but has rebounded above 4.75% this morning, the 10-year yield hit 4.25% before rebounding, the S&P500 and Nasdaq took advantage of the dovish vibes to extend gains toward a fresh record. Even the Stoxx 600 could cheer up a little. If inflation data shows further ‘modest’ progress, there is no reason we see the equity rally abate this summer.

In the FX, the US dollar index took a sharp dive below the 50-DMA yesterday on the back of a softer-than-expected CPI report and a sufficiently dovish Fed statement. The EURUSD rebounded past its 50, 100 and 200-DMA, traded as high as 1.0850 before easing to 1.08 – this is where the pair consolidates this morning. I maintain a neutral outlook as a further USD weakness should be countered by sustained downside pressure on the euro due to the chaotic political scene in France. Investors are most likely recovering from the kneejerk shock, the French 10-year yield eased yesterday on Macron’s announcement that he won’t quit his presidential seat even if he loses majority at the upcoming legislative elections. The latest polls suggests that Le Pen could win 31% of the first round votes while Macron is seen securing only 18%. But some think that the chaos that Mr Ciotto caused among Republicans could help consolidate power around a more balanced group than Le Pen’s National Rally, and Macron could offer that balanced harbour. In all cases, whatever it is, the outlook for the EURUSD remains neutral to slightly positive. The political shenanigans are still a short-term downside risk for the single currency but a sustainably softer US dollar should help the euro hold ground against the greenback.

Across the channel, Cable is preparing to test the March peak despite election jitters as a likely Labour victory in the UK is unusually seen as being a positive outcome for both sterling and the British assets. Here in Switzerland, a further dollar weakness could prevent the franc from extending losses – which wouldn’t be a bad news per se for the Swiss National Bank’s (SNB) fight against inflation that also picked up a certain momentum in the past few readings. On the flip side of the globe, the USDJPY barely reacts to the Fed decision and to the dollar’s broad-based weakness, as the Bank of Japan (BoJ) is not expected to throw fireworks at its scheduled meeting tomorrow, and finally in Australia, the Aussie-dollar gained the right to remain in the bullish trend, after having successfully held ground above a major 38.2% retracement on April to May rebound. The pair could extend gains to 68 cents.

In the energy space, US crude made an attempt on the $79pb level yesterday, fueled by dovish Fed expectations and the reflation flows, but the latest EIA data showed an unexpected 3.7-mio barrel build in the US inventories last week and the IEA said yesterday that global oil market faces a ‘major’ surplus this decade due to the shift away from fossil fuels. They predict that oil demand will level off around 105.6 mio barrels per day and that there will be around 8 mio barrel gap with the supply: the supply being higher than the demand by end of the decade. But the end of the decade is still a ways off, and the current reflation trade could help oil bulls make an educated attempt at the $80 per barrel resistance.

US CPI Lower Than Expected, While FOMC Signals Only One Rate Cut in 2024

In focus today

Today Norges Bank (NB) will publish the regional survey for Q2, where we expect that the respondents (corporates) will be somewhat more optimistic than in February. The aggregated production index for both the current (Q2) and the next quarter (Q3) will probably end up in the range of 0.2-0.3%, which will be somewhat higher than NB assumed in the PPR in March (0.0 % in Q2).

In Sweden, we get Prospera's big quarterly Q2 survey which includes not only inflation but also wage expectations, not least among social partners. However, all price/inflation expectations are more or less aligned around 2% at all horizons so it is unlikely to show any surprises.

In the US, May PPI is due for release today. In the evening, Fed's Williams moderates a discussion at the Economic Club of New York, potentially sharing some fresh views after the Fed's rate decision yesterday.

In Japan, the policy board convenes in the Bank of Japan (BoJ) today and wraps up the meeting with a policy decision early Friday. We expect no rate change, but we do expect the BoJ to signal tapering of its bond purchases. BoJ has kept the bond purchase pace unchanged at about JPY6 trillion a month after ending negative rates and yield curve control in March. It is a natural next step to cut purchases and Governor Ueda has also communicated that this is a priority. We think the BoJ will move slowly ahead, and thus getting started now with small steps seems like a good way forward.

Economic and market news

What happened yesterday

In the US, consumer prices rose 3.3% y/y in May (Cons: 3.4%; Prior: 3.4%) and were unchanged in the seasonally adjusted monthly measure of the same. Likewise, core CPI came in lower than expected as well at 0.2%|3.4% m/m|y/y (Cons: 0.3%|3.5%; Prior: 0.3%|3.6%). This was a positive surprise for the Fed in its battle against inflation, since the 0.2% m/m core inflation print rhymes with Fed's 2% target. However, the print follows 4 months straight with higher price pressures, so there is still some way to go before we expect the Fed to be confident enough about inflation to start cutting rates. 10y US treasuries dropped around 15bp in the hours after the print. EUR/USD increased initially from 1.076 to around 1.083.

The Fed maintained its monetary policy unchanged as widely anticipated, keeping the interval for the Fed funds rate at 5.25-5.50%. The most important news is the change in the dots, which signalled delayed cuts, with median pencilling in only 1 reduction for 2024 (prev. 3) but 4 for both 2025 and 2026 (prev. 3), so 25 bp higher end of 2025 but unchanged end of 2026. 2024 core PCE forecast was adjusted to 2.8% (prev. 2.6%) while other forecasts were largely unchanged. UST yields retracted part of the earlier CPI-driven decline and USD regained strength. We make no changes to our Fed call and still expect two 25bp rate cuts this year (starting September) followed by four more in 2025.

In Europe, the EU BEV car tariffs on Chinese brands will be increased from 10% to around 20% depending on the brand. The weight of new cars in euro area HICP is 3.2%, but we do not expect this to affect inflation significantly - and thereby ECB policy rates. The Chinese government urged the EU to reconsider the tariffs on Chinese electric vehicles overnight. We see it as most likely that China will not escalate this to a trade war. China is already pressured on the trade front with the US, so they need a tolerable relationship with the EU.

ECB Vice President De Guindos spoke about monetary policy, where he stated that the ECB should move very slowly when reducing interest rates due to continued high uncertainty about the inflation outlook. De Guindos stated that he was very certain that inflation will eventually fall to 2%. However, the next few months will likely be bumpy while service inflation remains a cause for caution, he added. We still expect the next rate cut to come at the final meeting of 2024 in December.

In France, president Macron said that he would not resign if his party suffered a poor result in the upcoming snap election in June.

In the UK, GDP was unchanged in April compared to March as expected, sending the economy back in low growth territory after a strong first three months in 2024. Financial markets showed little reaction to the print, while markets still see it as highly unlikely that we will see a rate cut at next week's policy meeting.

Market movements

Equities: Global equities saw a significant rise yesterday, not due to robust demand data, but rather softer-than-expected CPI data from the US. While it superficially appeared as a classic risk-on day with equities rising across regions and cyclicals outperforming, value still underperformed growth by 1% as yields dropped like a stone. Hence, this shows how important inflation still is for investors and we cannot fully allow ourselves to think about a negative correlation between bonds and equities. Part of the rotation yesterday also relates to the high and still growing appetite for tech stocks, which is also evident in today's futures where tech is leading significantly. In the US yesterday, Dow fell by 0.1%, while S&P 500 rose by 0.9%, Nasdaq by 1.5%, and Russell 2000 by 1.6%. Asian markets are mostly higher this morning, with (again) a noticeable appetite for tech in South Korea and Taiwan leading the advances. European futures are lower while US futures are higher this morning.

FI: Yields rose on the back of the slightly hawkish revisions to the FOM'’s dots, though the move was not sufficient to counterbalance the strong market reaction following the soft CPI figures. The market pricing of cuts this year dropped from 50bp to 45bp in response to the statement/SEP release, and Powell managed to maintain that level throughout the press conference. 10Y UST yields are trading 8bp lower relative to yesterday morning, while the 10Y Bund yield is down 9bp. Peripherals saw big tailwinds with 10Y BTP yields declining 15bp through the day. The Bund ASW-spread widened for the third consecutive day with the level now trading slightly above 29bp.

FX: EUR/USD bounced back yesterday after US CPI inflation was lower than expected. That further spurred a rally in Scandi currencies where EUR/SEK fell briefly below 11.20. JPY also found some relief - USD/JPY dipped below 156.