Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0804; (R1) 1.0842; More...

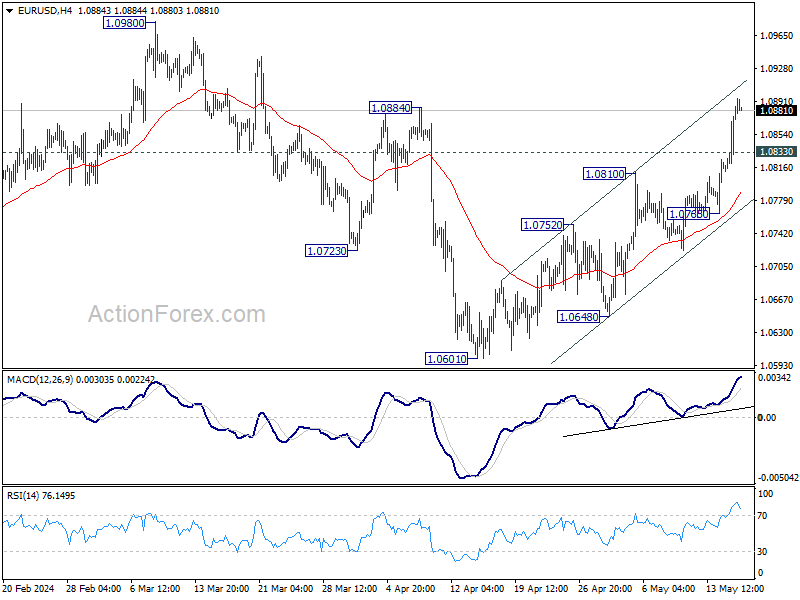

EUR/USD's rally from 1.0601 continues today and intraday bias stays on the upside. Next target is 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed already. On the downside, below 1.0833 minor support will turn intraday bias neutral first. But further rally is expected as long as 1.0765 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

Dollar Selloff Continues as Risk-On Sentiment Drives US Stocks to New Highs

Dollar faced broad sell-offs overnight and continued to weaken in Asian session. Investors breathed a sigh of relief after US CPI data indicated that disinflation is progressing, which has reignited speculation about near-term rate cuts by Fed. Or at least, another rate hike is now highly unlikely, as repeated by Chair Jerome Powell. Fed fund futures now show nearly 74% chance of a rate cut in September. Additionally, the probability of two total cuts this year has risen to around 70%. This optimism propelled NASDAQ to lead major US stock indexes to new record closes, while 10-year Treasury yield plummeted, breaking below 4.4% mark.

In the currency markets, New Zealand Dollar emerged as the strongest performer for now, further boosted by its rebound against Australian Dollar. Although Aussie also saw notable gains, its upside was capped by mixed employment data that revealed a rise in unemployment rate. British Pound is currently the second strongest currency, supported by robust wage growth data released yesterday. On the other hand, Canadian Dollar is the second weakest, following the greenback. Swiss Franc is also weak, ranking as the third worst performer. currency. Meanwhile, Euro and the Japanese Yen are positioned in the middle of the pack.

Technically, NZD/USD's strong break of falling channel resistance suggests that corrective fall from 0.6368 has completed with three waves down to 0.5851. Rise from 0.5851 is probably the third leg of the pattern from 0.5771. For now, further rise is expected as long as 55 D EMA (now at 0.6019) holds. Firm break of 0.6125 resistance will reinforce this view and should pave the way through 0.6368 to 100% projection of 0.5771 to 0.6368 from 0.5851 at 0.6448.

In Asia, at the time of writing, Nikkei is up 0.90%. Hong Kong HSI is up 1.68%. China Shanghai SSE is up 0.48%. Singapore Strait Times is up 0.82%. Japan 10-year JGB yield is down -0.030 at 0.924. Overnight, DOW rose 0.88%. S&P 500 rose 1.17%. NASDAQ rose 1.40%. 10-year yield fell -0.0890 to 4.356.

Fed's Kashkari: Current rates might be one foot on the brake, not two

Minneapolis Fed President Neel Kashkari stated overnight that Fed likely needs to keep interest rates at the current level for "a while longer," raising questions about how much they are restraining the US economy.

He highlighted that the "biggest uncertainty" is understanding the exact amount of "downward pressure" monetary policy is putting on the economy. This uncertainty means Fed "probably need[s] to sit here for a while longer" until there is more clarity on where "underlying inflation is headed" before drawing any conclusions.

He remarked on the surprising "resilience" of the economy, suggesting that current interest rates might mean "we're putting one foot on the brake and not two."

Fed's Goolsbee stresses need for housing inflation drop to reach 2% target

Chicago Fed President Austan Goolsbee, in a Marketplace interview, emphasized the importance of a significant decline in housing inflation to achieve the Fed's 2% overall target.

"It would be hard for me to see that we could get to the 2% overall target unless house prices, inflation comes down substantially from where it is right now," Goolsbee stated.

Despite the current challenges, Goolsbee remains optimistic, noting, "I'm still both optimistic and my read of the evidence is that that is going to happen." He pointed to yesterday's CPI numbers, which show some decrease in housing costs, as a positive sign.

However, he cautioned that if this trend does not continue, Fed will need to delve deeper to understand the underlying issues.

Japan's Q1 GDP contracts -0.5% qoq, weak consumption and capital spending

Japan's GDP contracted by -0.5% qoq in Q1, slightly worse than the expected -0.4% qoq decline. On annualized basis, GDP fell by -2.0%, missing forecast of -1.5% drop.

Private consumption, which makes up over half of the Japanese economy, decreased by -0.7%, exceeding anticipated -0.2% decline. This marks the fourth consecutive quarter of decline, the longest streak since 2009.

Capital spending fell by -0.8%, slightly more than the expected -0.7% decrease. This was the first decline in two quarters.

Exports declined by -5.0%, despite ongoing support from inbound tourism, while imports fell by -3.4% amid reduction in energy imports. The trade figures reflect a broader slowdown in global demand, which is impacting Japan's export-driven economy.

Australia's employment grows 38.5k in Apr, unemployment rate rises to 4.1%

Australia employment grew 38.5k in April, well above expectation of 25.3k. Full-time jobs fell -6.1k while part-time jobs rose 44.6k. Unemployment rate rose from 3.9% to 4.1%, above expectation of 3.9%. participation rate rose from 66.6% to 66.7%. Monthly hours worked was unchanged. Number of unemployed rose 30.3k or 5.3% mom.

Looking ahead

Italy's trade balance is a feature in European session. Later in the day, US will release jobless claims, building permits and housing starts, import price, Philly Fed survey, and industrial production.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0804; (R1) 1.0842; More...

EUR/USD's rally from 1.0601 continues today and intraday bias stays on the upside. Next target is 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed already. On the downside, below 1.0833 minor support will turn intraday bias neutral first. But further rally is expected as long as 1.0765 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q1 P | -0.50% | -0.40% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | 3.60% | 3.30% | 3.90% | |

| 01:30 | AUD | Employment Change Apr | 38.5K | 25.3K | -6.6K | |

| 01:30 | AUD | Unemployment Rate Apr | 4.10% | 3.90% | 3.80% | 3.90% |

| 04:30 | JPY | Industrial Production M/M Mar F | 3.40% | 3.80% | ||

| 09:00 | EUR | Italy Trade Balance (EUR) Mar | 4.77B | 6.03B | ||

| 12:30 | USD | Initial Jobless Claims (May 10) | 219K | 231K | ||

| 12:30 | USD | Building Permits Apr | 1.48M | 1.46M | ||

| 12:30 | USD | Housing Starts Apr | 1.43M | 1.32M | ||

| 12:30 | USD | Import Price Index Y/Y Apr | 0.20% | 0.40% | ||

| 12:30 | USD | Philadelphia Fed Survey May | 7.7 | 15.5 | ||

| 13:15 | USD | Industrial Production M/M Apr | 0.20% | 0.40% | ||

| 13:15 | USD | Capacity Utilization Apr | 78.40% | 78.40% | ||

| 14:30 | USD | Natural Gas Storage | 76B | 79B |

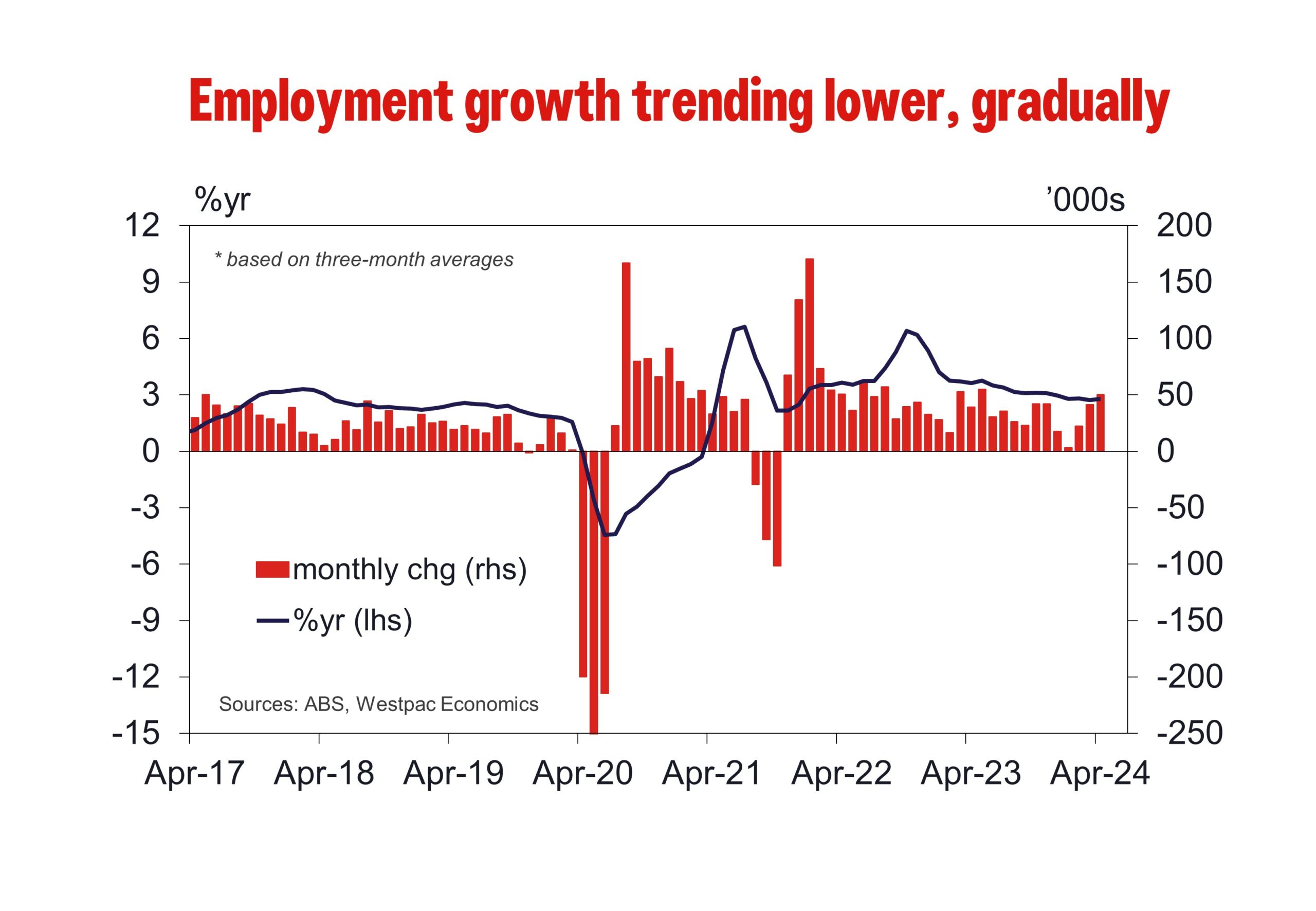

Australia April Labour Force: Gradual Softening Persists

Employment: +38.5k (from –5.9k). Unemployment Rate: 4.1% (from 3.9%). Participation Rate: 66.7% (from 66.6%).

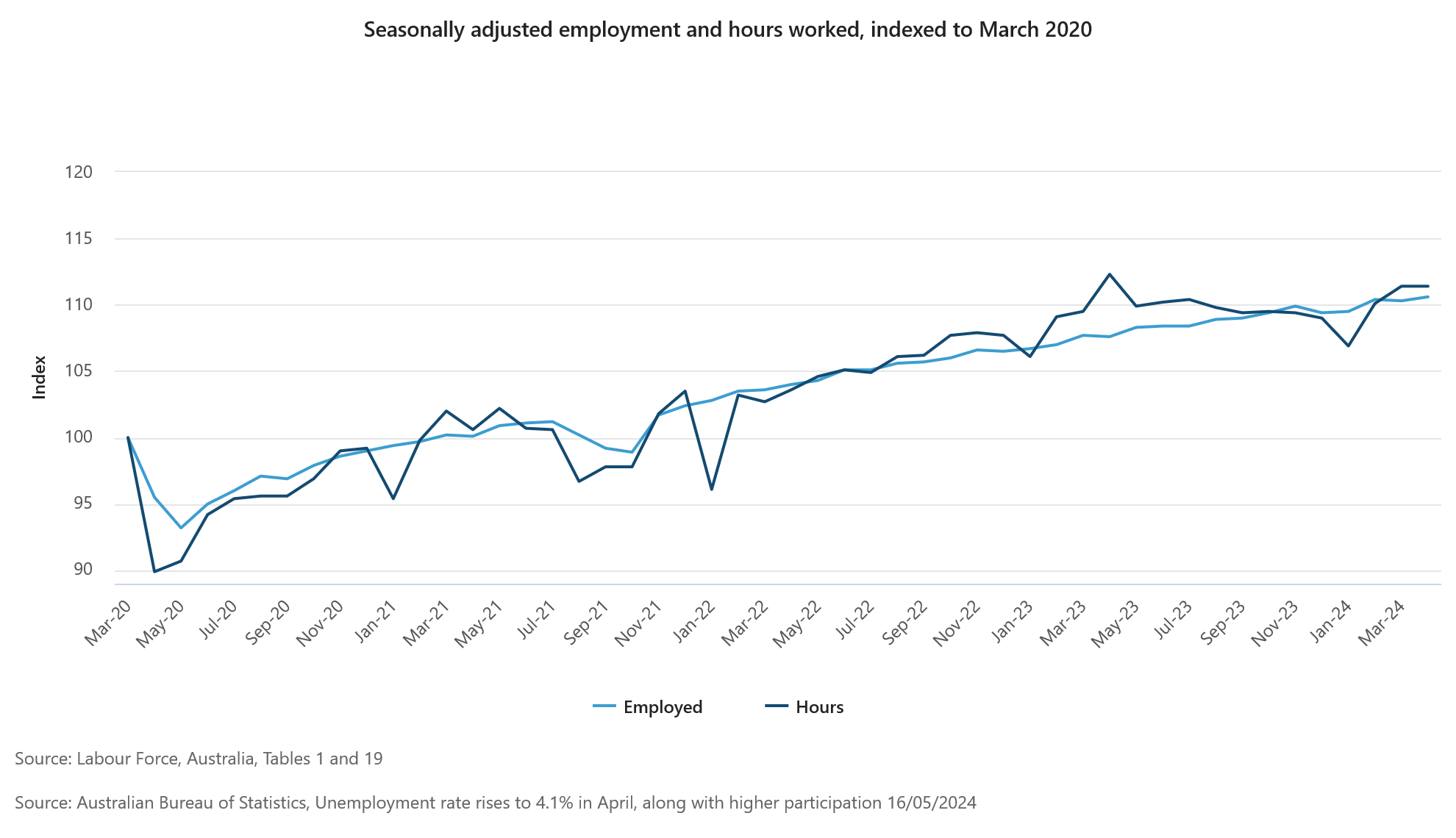

In April, the level of employment rose by +38.5k (0.3%), stronger than Westpac’s forecast for +20k and the market consensus for +23.7k. That follows a fairly volatile opening quarter, with gains ranging from +11.6k in January, to +118.2k in February and –5.9k in March. On a three-month average basis, annual employment growth has held broadly steady at 2.8%yr over the past four months. Still, employment’s current pace remains stronger than 2.0%yr to 2.5%yr ‘norm’ observed in the years prior to the pandemic.

Labour demand has certainly cooled over the past year, but it has only translated into a gradual softening in employment growth. Easing labour demand appeared more clearly in average hours worked over the second half of last year. Since then, it has shown few signs of extended weakness.

In the month, growth in the working age population kept pace with that of employment, seeing the employment-to-population ratio hold steady at 64.0%. While we anticipate growth across both the working age population and employment to moderate over the remainder of the year, the former will likely continue to outstrip the latter, which will see the employment-to-population ratio gradually fall over 2024 after having moved broadly sideways near historic highs over much of 2023.

It is also worth highlighting that the ABS have provided more information around the recent behaviour of seasonally adjusted estimates in the Labour Force Survey. The main takeaway is that recent volatility is likely to be temporary, reflecting changes in the dynamics and behaviours of people and businesses within the context of a historically tight labour market. Elements of that was seen in today’s results with respect to unemployment (below) and was certainly present in many estimates around the beginning of the year. With more data over time, the nature of the changes in underlying dynamics will be better understood.

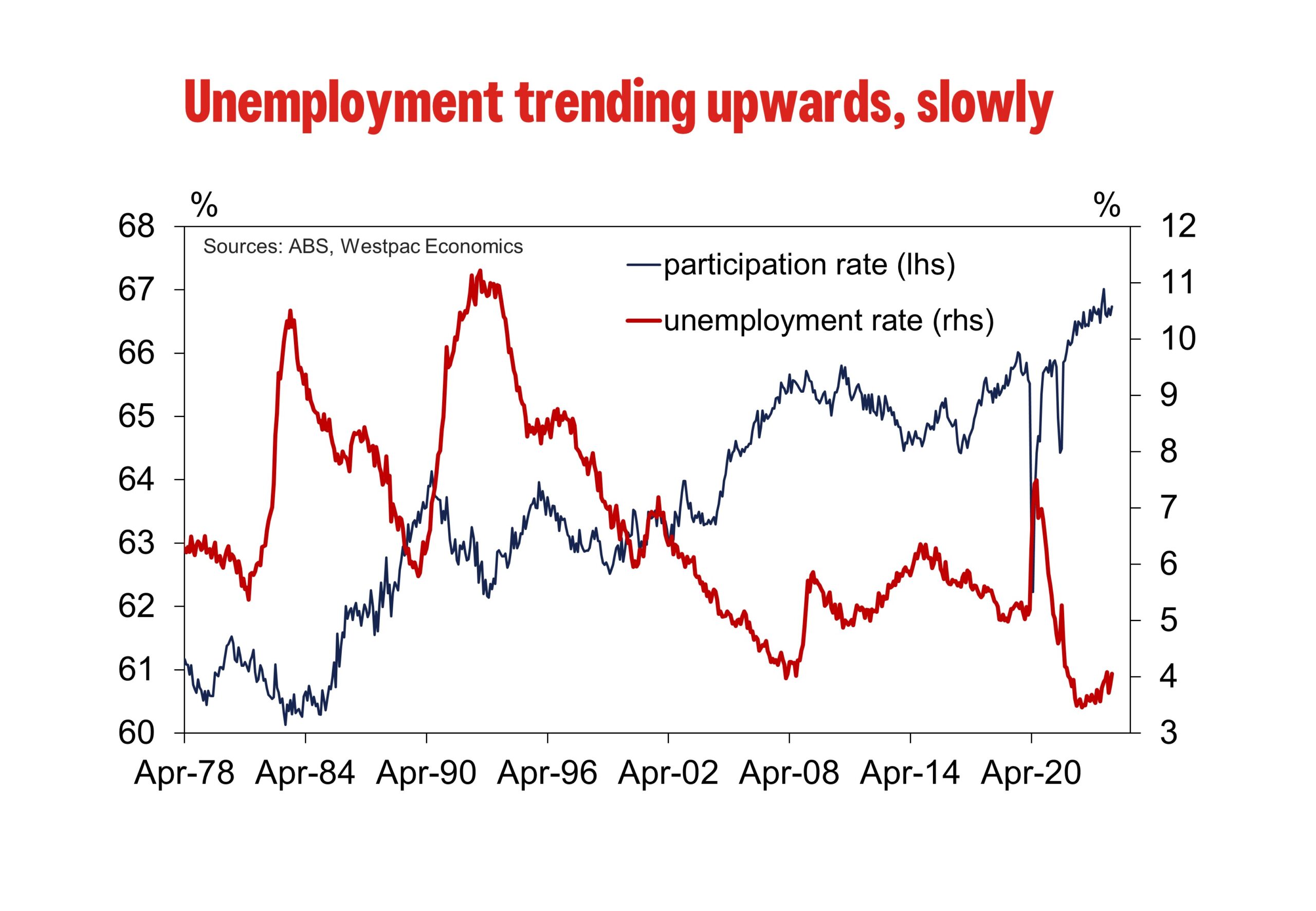

Unemployment Rate

Labour force participation was a little stronger than expected, with the participation rate moving higher from 66.6% in March to 66.7% in April. That implies an appreciable lift in the size of the labour force, up +68.8k. Given the +38.5k lift in employment, that means there was a rise in the number of unemployed persons (+30.3k), which saw the unemployment rate move from 3.9% to 4.1% (4.05% to two decimal places).

The ABS noted that the increase in the number of employed persons partly reflected more people than usual indicating they had a job that they were waiting to start. This is a dynamic that has appeared more prominently in ‘holiday’ months since the reopening and has had an influence in driving month-to-month swings in the unemployment rate. Should these individuals move into employment next month, there is room for the unemployment rate to round back down in May.

Given the upward revision to March (from 3.8% to 3.9%), the impact of the above seasonal dynamics, and the strong round-up in April (4.05% reported at 4.1%), the overall change in unemployment in the month does not represent a material surprise to expectations for the month alone.

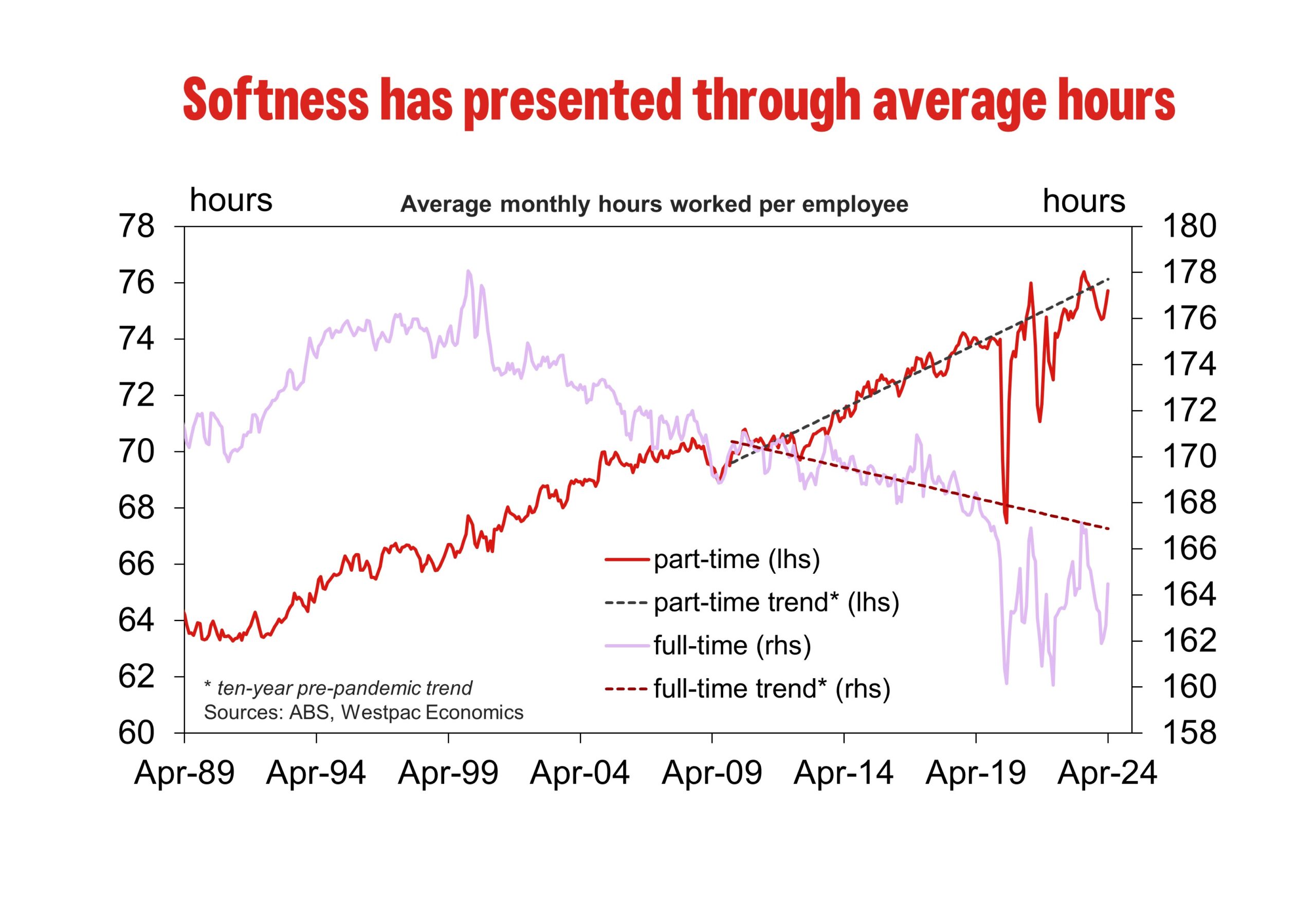

Hours Worked

The total number of hours worked has been soft over the last year, notwithstanding the increase in the number of people employed. This continued in April, with the number of hours worked remaining unchanged compared with March. In annual terms, hours worked declined by 0.1%. This was the first annual decline since the pandemic (February 2021).

Hours worked can be volatile from month to month, particularly now given the shift in seasonality. ABS trend data tries to remove this volatility and provide an estimate of the underlying trend. This shows that hours worked declined from June 2023 and started to turn in November 2023. It has now surpassed the June 2023 level. Over this same period employment has increased by around 1.8%.

Robust employment growth coupled with soft hours worked outcomes implies that the average number of hours worked has declined. This is indeed what we have observed but again, this started to turn since November 2023. Average number of hours worked have returned to pre-pandemic levels (January 2020). These dynamics suggests that the labour market went through a significant adjustment in the second half of 2023 and has now started to normalise.

The change in the number of hours worked over April differed across the states. Strong increases were recorded in Tasmania (+5.8%) and Queensland (+1.6), with declines were recorded in Western Australia (-1.8%), South Australia (-0.8%), Victoria (-0.3%) and NSW (-0.2%).

Potential Labour Supply

The bounce back in international students and immigrants returning to Australia when borders reopened was larger than anyone expected. As a result, the working age population grew at a record pace for most of last year. This now looks to have peaked, in the month of September 2023 when looking at the annual growth rate. Despite this, the change in the working age population continues to outpace employment. We expect this will continue to occur going forward. This is consistent with a loosening in labour market conditions – with the unemployment rate drifting higher and the employment to population ratio moving lower.

Other Labour Market Measures

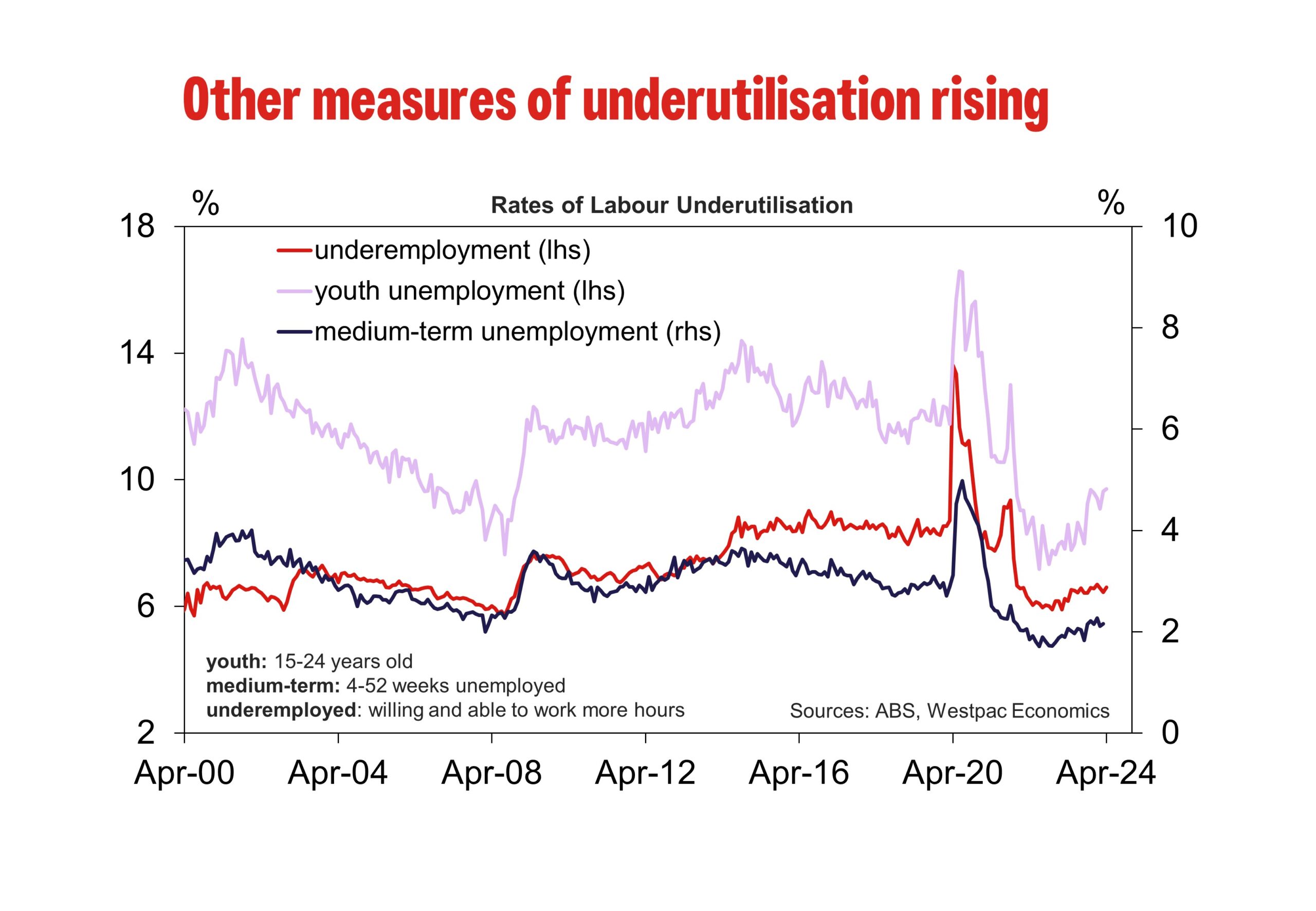

Consistent with the soft hours worked outcome some other labour market indicators also softened over the month of April.

The underemployment rate, which measures the share of employed workers who are willing and able to work more hours, ticked up to 6.6% in April. Over 2023 the underemployment rate has drifted higher in trends terms, coinciding with the slowdown in economic activity.

The underutilisation rate, which combines the unemployment and underemployment rates, jumped to 10.7% - the highest rate since January. Consistent with the underemployment rate, the underutilisation rate has drifted higher in trends terms, from 9.5% in late 2022 to 10.3% in March 2024 (trend terms).

Outlook

The tone of today’s survey, in relation to its implications on the outlook, is not materially different from last month. The dynamics which drove a clear softening in conditions over the second half of last year – namely the ‘correction’ in average hours from elevated levels and a slowdown in employment growth – have not been as strong recently. Looking past the considerable month-to-month volatility, the labour market has generally held in robust health with signs of emerging slack being gradual at best.

As we have emphasised before, the extent to which labour demand will continue to cool over the near-term will critically depend on the interplay between headcount and hours. We continue to anticipate that conditions will gradually soften over the course of this year, as employment growth continues to soften and the unemployment rate ticks up to a quarter-average of 4.3% by year-end.

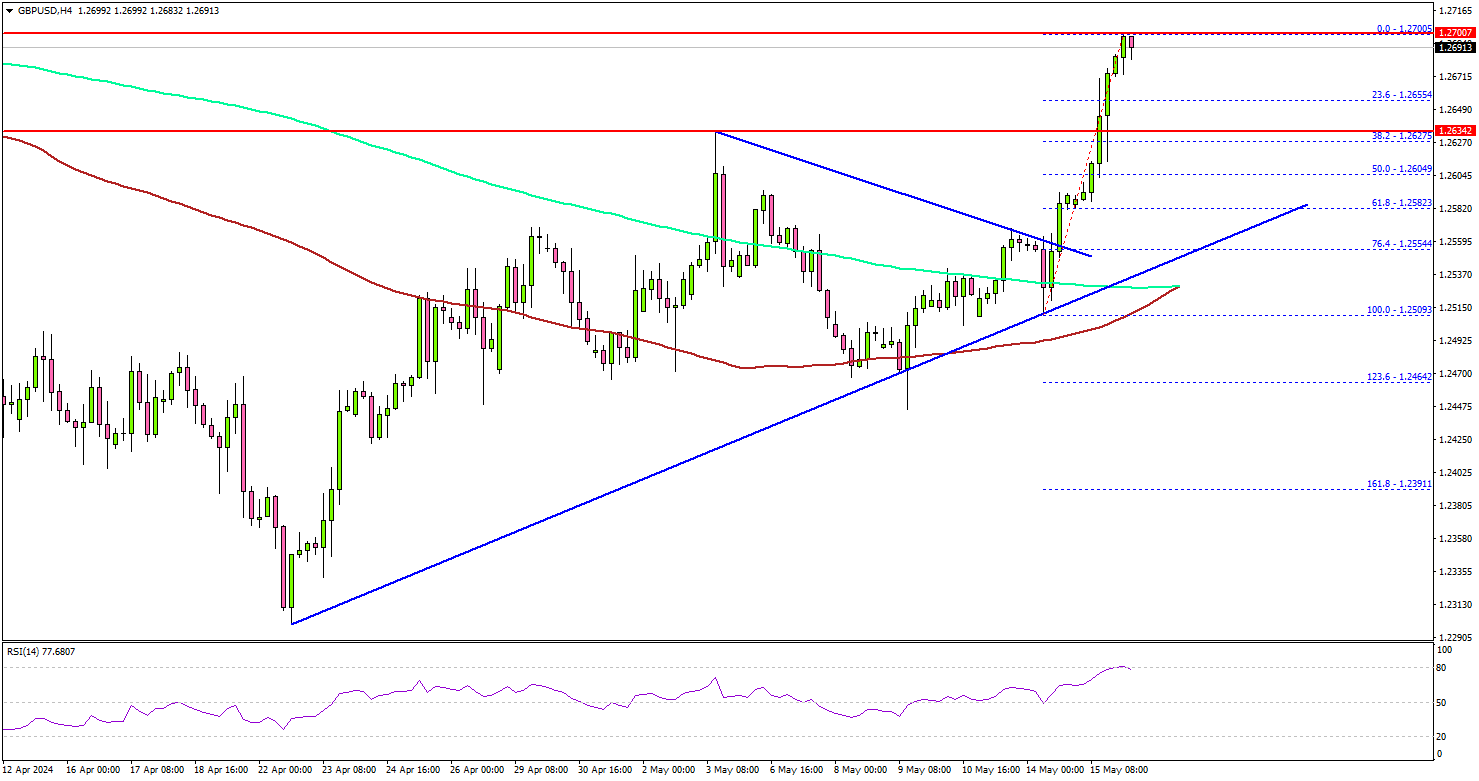

GBP/USD Kickstarts Fresh Surge Amid Sharp Decline In Dollar Value

Key Highlights

- GBP/USD started a decent increase and climbed above 1.2600.

- A key bullish trend line is forming with support at 1.2580 on the 4-hour chart.

- Gold prices cleared the $2,375 resistance to move into a positive zone.

- USD/JPY dipped again and traded below the 155.00 level.

EUR/USD Technical Analysis

The British Pound started a decent increase above the 1.2550 resistance against the US Dollar. GBP/USD cleared the 1.2600 resistance to move into a positive zone.

Looking at the 4-hour chart, the pair even settled above the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour). There was a move toward the 1.2700 level.

A high was formed at 1.2700 and the pair is now consolidating gains. The first major resistance is near 1.2720. A clear move above the 1.2720 resistance might send it toward the 1.2750 level. Any more gains might call for a move toward the 1.2880 level in the near term.

Conversely, GBP/USD might correct gains. Immediate support is near the 1.2665 level. The first major support is near the 1.2620 level. The next major support is at 1.2600.

There is also a key bullish trend line forming with support at 1.2580 on the same chart. If there is a downside break below the 1.2580 support, the pair might test 1.2535 or the 100 simple moving average (red, 4-hour). Any more losses might send the pair toward 1.2450.

Looking at Gold, the bulls came into action and they were able to push prices toward the $2,400 resistance zone.

Economic Releases

- US Initial Jobless Claims - Forecast 220K, versus 231K previous.

- US Industrial Production for April 2024 (MoM) – Forecast 0.1%, versus 0.4% previous.

Australia’s employment grows 38.5k in Apr, unemployment rate rises to 4.1%

Australia employment grew 38.5k in April, well above expectation of 25.3k. Full-time jobs fell -6.1k while part-time jobs rose 44.6k. Unemployment rate rose from 3.9% to 4.1%, above expectation of 3.9%. participation rate rose from 66.6% to 66.7%. Monthly hours worked was unchanged. Number of unemployed rose 30.3k or 5.3% mom.

Japan’s Q1 GDP contracts -0.5% qoq, weak consumption and capital spending

Japan's GDP contracted by -0.5% qoq in Q1, slightly worse than the expected -0.4% qoq decline. On annualized basis, GDP fell by -2.0%, missing forecast of -1.5% drop.

Private consumption, which makes up over half of the Japanese economy, decreased by -0.7%, exceeding anticipated -0.2% decline. This marks the fourth consecutive quarter of decline, the longest streak since 2009.

Capital spending fell by -0.8%, slightly more than the expected -0.7% decrease. This was the first decline in two quarters.

Exports declined by -5.0%, despite ongoing support from inbound tourism, while imports fell by -3.4% amid reduction in energy imports. The trade figures reflect a broader slowdown in global demand, which is impacting Japan's export-driven economy.

Fed’s Goolsbee stresses need for housing inflation drop to reach 2% target

Chicago Fed President Austan Goolsbee, in a Marketplace interview, emphasized the importance of a significant decline in housing inflation to achieve the Fed's 2% overall target.

"It would be hard for me to see that we could get to the 2% overall target unless house prices, inflation comes down substantially from where it is right now," Goolsbee stated.

Despite the current challenges, Goolsbee remains optimistic, noting, "I'm still both optimistic and my read of the evidence is that that is going to happen." He pointed to yesterday's CPI numbers, which show some decrease in housing costs, as a positive sign.

However, he cautioned that if this trend does not continue, Fed will need to delve deeper to understand the underlying issues.

Fed’s Kashkari: Current rates might be one foot on the brake, not two

Minneapolis Fed President Neel Kashkari stated overnight that Fed likely needs to keep interest rates at the current level for "a while longer," raising questions about how much they are restraining the US economy.

He highlighted that the "biggest uncertainty" is understanding the exact amount of "downward pressure" monetary policy is putting on the economy. This uncertainty means Fed "probably need[s] to sit here for a while longer" until there is more clarity on where "underlying inflation is headed" before drawing any conclusions.

He remarked on the surprising "resilience" of the economy, suggesting that current interest rates might mean "we're putting one foot on the brake and not two."

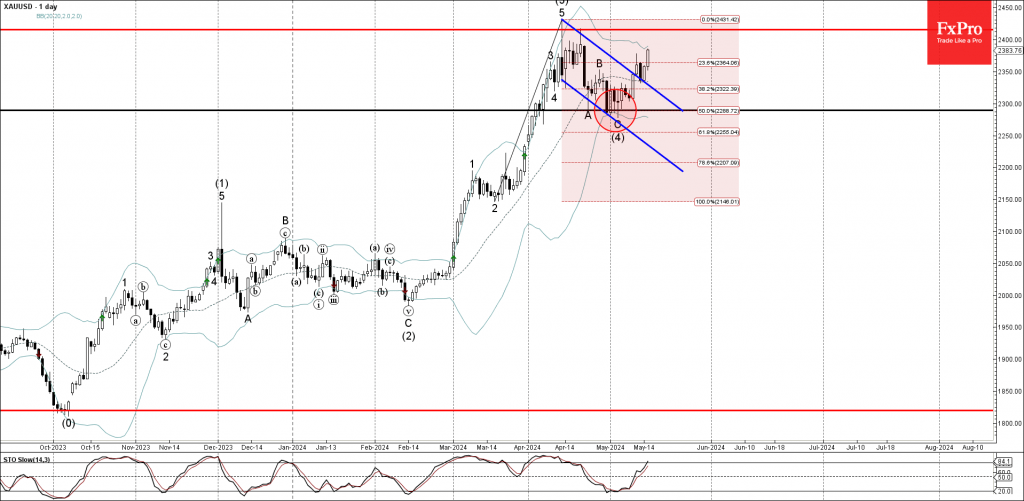

Gold Wave Analysis

- Gold broke daily down channel

- Likely to reach resistance level 2415.00

Gold recently broke the resistance trendline of the narrow daily down channel from April, which enclosed the previous ABC correction (4).

The breakout of this down channel accelerated the active intermediate impulse wave (5) – which belongs to the higher order impulse sequence from October.

Given the predominant daily uptrend, Gold can be expected to rise further toward the next resistance level 2415.00, which reversed the price twice in April.

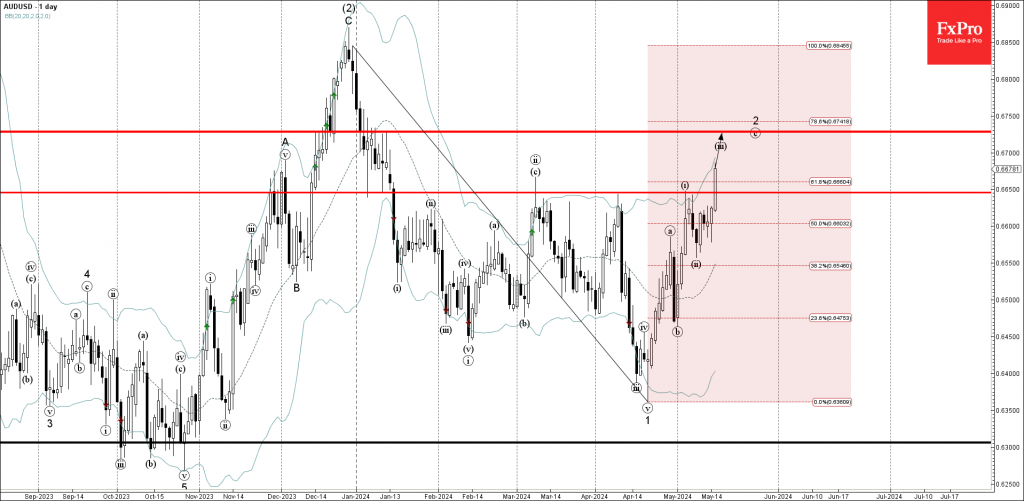

AUDUSD Wave Analysis

- AUDUSD broke key resistance level 0.6650

- Likely to reach resistance level 0.6760

AUDUSD currency pair recently broke the key resistance level 0.6650, which has been reversing the pair from the start of March.

The breakout of the resistance level 0.6650 coincided with the breakout of the 61.8% Fibonacci correction of the downward correction from the end of December – which accelerated the active impulse wave 3.

Given the strongly bearish USD sentiment, AUDUSD currency pair can be expected to rise further toward the next resistance level 0.6760, former resistance from January and the target for the completion of the active wave 2.