Sample Category Title

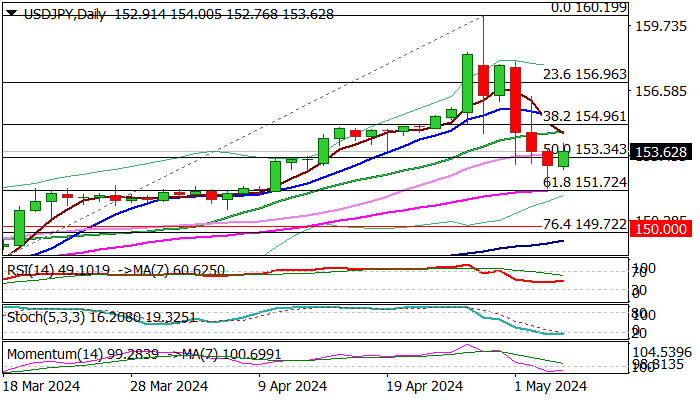

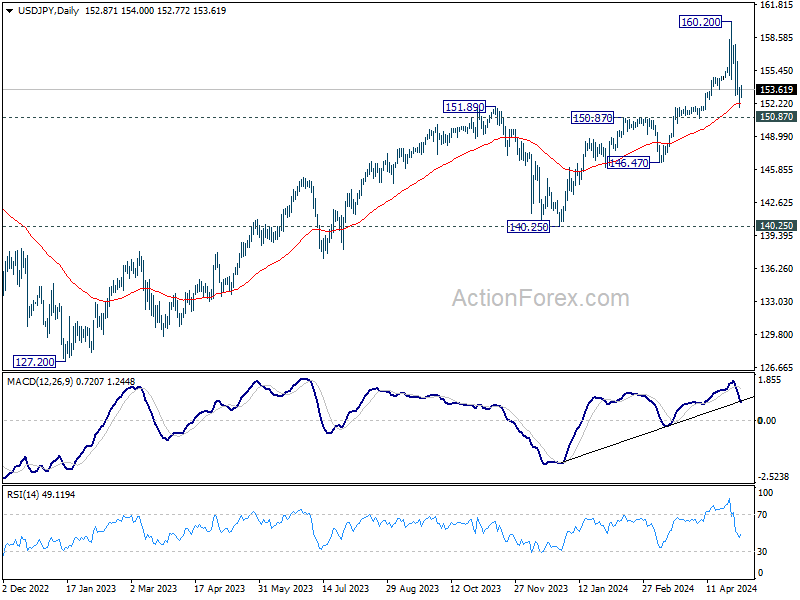

USDJPY – Initial Reversal Signal Requires More Work at the Upside for Confirmation

USDJPY edges higher on Monday after a pullback from new record high (160.19) was contained by strong Fibo support at 151.72 (61.8% retracement of 146.48/160.19 upleg, reinforced by 55DMA).

Strong rejection here left a Hammer candle on Friday, initial signal of reversal, which could be boosted if today’s bounce completes a bullish engulfing pattern.

However, more evidence is still required to generate reversal signal (break and close above 155.04 (Fibo 38.2% of 160.19/151.85 bear-leg).

Conflicting daily studies (negative momentum / mixed setup of MA’s / oversold stochastic) lack clearer direction signal for now.

Sustained break above 155.04/29 (Fibo / 10DMA) to firm near-term structure and signal bottom (151.72) and open prospects for further recovery.

Conversely, the downside will remain vulnerable if recovery fails to regain 155.04 pivot, with increased downside risk expected on rejection at initial Fibo barrier at 153.82 (23.6% of 160.19/151.85).

Res: 154.00; 155.04; 155.50; 156.02

Sup: 152.76; 151.72; 150.00; 149.72

Yen Rally Fizzles as US Dollar Climbs

The Japanese yen is sharply lower on Monday after stringing together a three-day rally. USD/JPY is trading at 153.92, up 0.62% at the time of writing.

The yen took traders on a roller-coaster ride last week. The Japanese yen fell below the 160 level on Monday, setting another 34-year record before recovering. On Wednesday, the yen climbed 2.1% and on Friday it strengthened to 151.85, a one-month high against the US dollar.

The sharp swings on Monday and Wednesday were likely caused by intervention from Japan’s Ministry of Finance (MoF). To no one’s surprise, the MoF wouldn’t comment on whether it had intervened. US Treasury Secretary Yellen also declined to say whether Tokyo had intervened, but Bank of Japan current account data indicated that the Japanese government may have bought up $60 billion to support the ailing yen.

Previous interventions by the MoF haven’t been effective, providing only a brief boost for the yen. With the Fed signaling that it won’t rush into cutting rates, the US/Japan rate differential isn’t narrowing and that will likely mean that the yen will resume its depreciation.

US nonfarm payrolls ease to 175,000

The US economy added 175,000 jobs in April, down from the upwardly revised 315, 000 in March and below of the market estimate of 240,000. This points to a slowdown from the strong job growth which marked the first quarter. Unemployment and wage growth were also down compared to March, and the somewhat soft employment report makes a September rate cut more likely.

The Fed’s rate path will be data-dependent, with a focus on inflation, consumer spending and GDP. At least week’s meeting, Fed Chair Powell said high inflation remained a concern but indicated that the Fed still planned to lower rates.

USD/JPY Technical

- USD/JPY is testing resistance at 153.92. Above, there is resistance at 154.87

- There is support at 152.90 and 151.95

Sunset Market Commentary

Markets

With Japanese and US markets closed, Europe stood on its own to look for direction after Friday’s yield decline in the wake of weaker than expected US payrolls and services ISM. US markets again considering two potential Fed rate cuts (Sept +/- 90% discounted, 2nd in December +/- 80% discounted) gives European investors some additional comfort on an early ECB rate cut (June almost fully discounted). Economic data were few. Still, a material upward revision of the French (services) PMI also filtered through into the EMU measure (EMU composite PMI upwardly revised from 51.4 to 51.7, best level in almost a year). Aside from better activity, the survey also signaled stronger inflationary pressures in April than in March, with both increases in input costs and output charges quickening and printing above historical series averages. However, with both headline and core EMU inflation in April having declined to the mid 2% area, this probably won’t prevent the ECB withdrawing some policy tightening before summer. This analysis of growing confidence of inflation moving toward 2% was confirmed by press comments of ECB Chief economist Lane this weekend. German yields are easing between 2.1 bps (2-y) and 3.7 bps (10-y). The German 2-y yield is testing intermediate support near 2.90%. The 10-y yield in last week’s move dropped back below the 2.50% barrier. US yields initially build on Friday’s easing momentum but declines are currently limited between 1-2 bps. The prospect/hope of some global central bank easing sooner or later this year, continues to provide some support for global equities. The EuroStoxx50 gains 0.6%. The S&P500 opens 0.35% stronger. Fed Powell’s rather soft assessment and Friday’s weaker data also discouraged dollar USD bulls. DXY struggles not to fall below the 105 barrier. EUR/USD remains well bid (1.0775) with first resistance at 1.0807 (38% retracement end-December/mid-April) within reach. USD/JPY is the exception to the rule with the pair rebounding north to currently trade in the 153.70 area. Even if the Fed were to start some gradually easing later this year, the interest rate gap between the Fed and the BOJ remains too wide to provide any lasting support the Japanese currency. The cat-and-mouse game of (verbal and/or real) interventions between Japanese officials and the market probably is far from over if the BOJ stays silent on the timing of further/protracted policy normalization. Later today, markets will keep an eye at the Fed’s Senior loan Officer Opinion Survey on bank lending. The report fur sure will contain some interesting features on how policy tightening has filtered through into the US economy, but it seldom had lasting market impact.

News & Views

The European Commission in a statement today announced to end a 6-year dispute with Poland over backsliding on democratic principles and the rule of law under the previous PiS government that came to power in 2015. EC president Von der Leyen said that the so-called Article 7 procedure can be closed following a plan that the pro-EU prime minister Tusk in February had presented. The plan back then also triggered the release of several billions locked-up cohesion funds. And last month the EU paid out the first instalment of EU recovery funds to Poland (€6.3bn), making today’s decision largely a formal one. The Polish zloty did frontrun the European-Polish détente a long time ago (since Tusk’s electoral victory), leading to a stoic response on the news today. EUR/PLN eases a few ticks towards 4.32.

John Swinney is poised to become Scotland’s first minister this week after being appointed leader of the Scottish National Party. Swinney’s predecessor Yousaf announced his resignation end of last month ahead of a no confidence vote he was about to lose. It was also week after collapsing the coalition with the Scottish Greens as Yousaf sought to move Scottish political needle from left to center again and face off a rising challenge from Scottish Labour in the upcoming general elections. Swinney is a veteran who led the party in the early 2000s and will face a vote in parliament as early as Tuesday. The SNP holds 63 seats compared with the 65 needed for a majority. Swinney thus needs to secure votes or abstentions from outside his party. The Scottish Greens hold seven seats and are willing to support Swinney provided he continues to pursue progressive policies.

Graphs

German 10-y yield eases back below 2.50% as hopes on global easing resurface post Friday’s US data.

USD-DXY TW index struggles to hold 105 barrier as global monetary conditions ease.

USD/CNY: yuan strengthens after May holidays on weaker dollar and hope for Chinese activity to improve.

EuroStoxx 50 tries to escape ST downtrend channel.

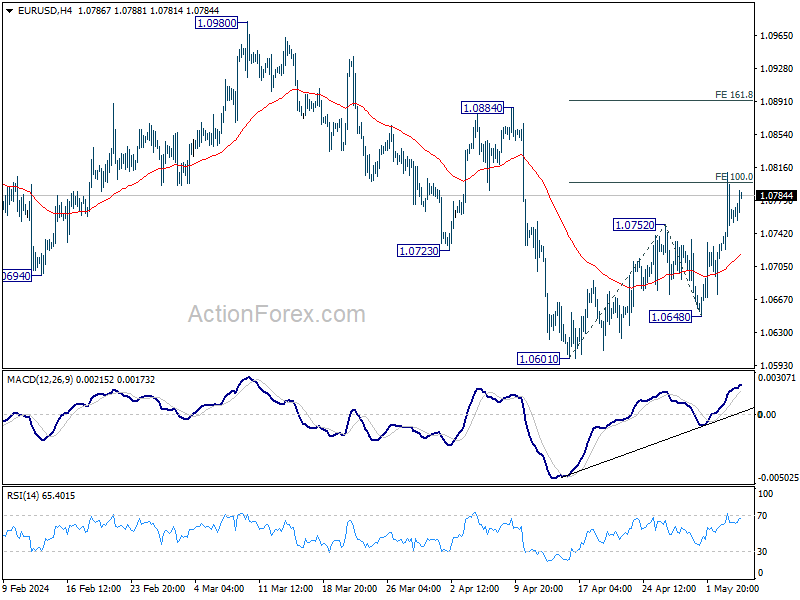

Euro Edges Higher as Eurozone Data Improves

The euro has started the new trading week quietly. EUR/USD is up 0.23%, trading at 1.0787 in the North American session at the time of trading.

Eurozone investor confidence shows slight improvement

The eurozone Sentix Investor Confidence index took a small step forward in May, rising to -3.6, up from -5.9 in April and was higher than expected. This was the seventh straight acceleration and the highest level since February 2022. The index, which has been in negative territory since February 2022, is creeping up to the zero level, which separates optimism from pessimism.

German and eurozone services PMIs showed slight growth in April, another indication that the eurozone economy is showing improvement. The German PMI came in at 53.2 and the eurozone at 53.3. After a prolonged decline in services, Germany has recorded three straight months of expansion and the eurozone two consecutive months.

The European Central Bank is widely expected to make an initial rate cut in June, as inflation has dropped to 2.4%. Inflation has proven difficult to push down to the 2% target, but ECB members are more confident that inflation will not rebound from one rate cut. Whether the ECB will embark on a series of rate cuts will depend on inflation and other key data.

US nonfarm payrolls ease to 175,000

The US economy added 175,000 jobs in April, a sharp drop from the upwardly revised 315, 000 in March and shy of the market estimate of 240,000. This points to a slowdown from the strong job growth which marked the first quarter. Unemployment and wage growth were also down compared to March, and the somewhat soft employment report makes a September rate cut more likely. The Fed’s rate path will be data-dependent, with a focus on inflation, consumer spending and GDP.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0766. Above, there is resistance at 1.0809

- There is support at 1.0720 and 1.0677

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0720; (P) 1.0766; (R1) 1.0809; More...

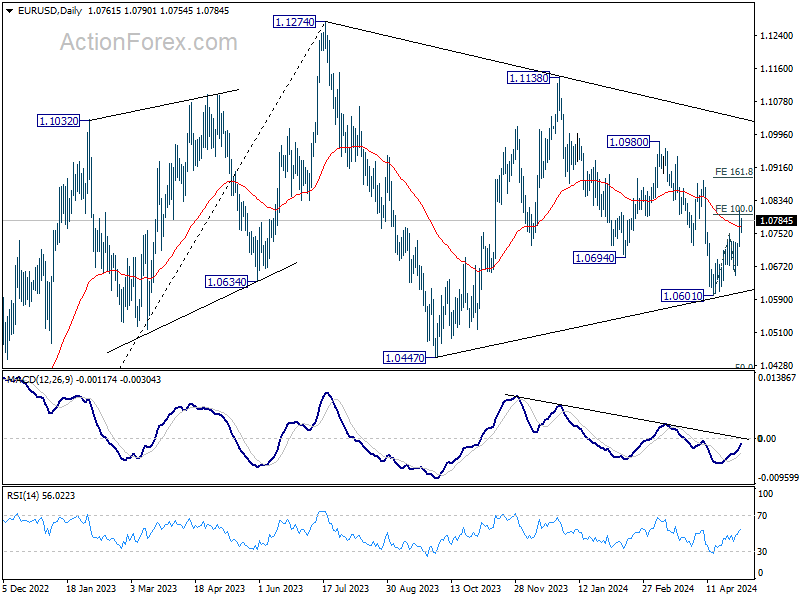

Intraday bias in EUR/USD stays on the upside at this point. Fall from 1.0980 could have completed with three waves down to 1.0601. Further rally is expected and firm break of 100% projection of 1.0601 to 1.0752 from 1.0648 at 1.0799 will pave the way to 161.8% projection at 1.0892. For now, risk will stay on the upside as long as 1.0648 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

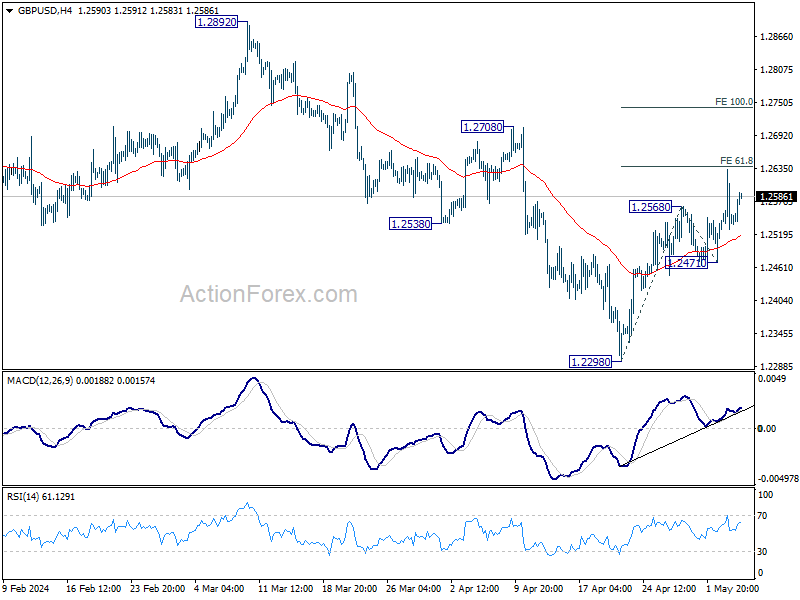

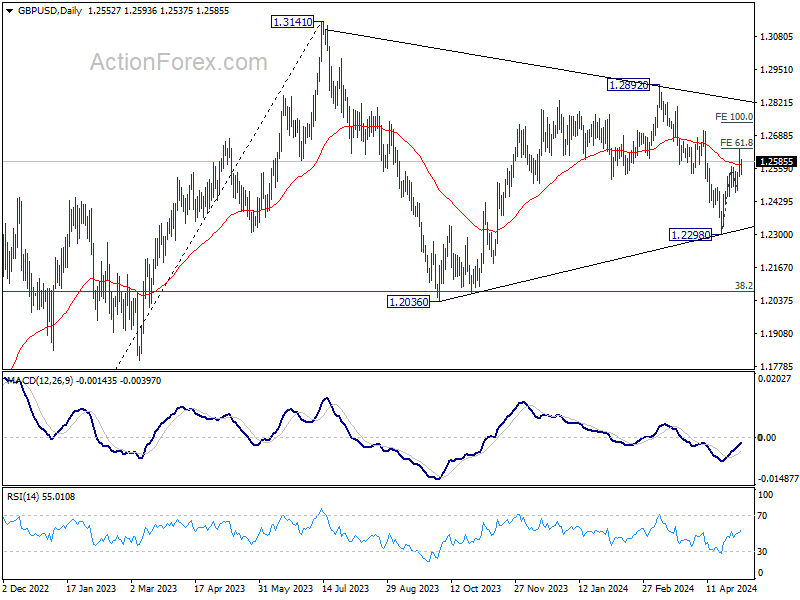

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2491; (P) 1.2564; (R1) 1.2619; More...

Intraday bias in GBP/USD remains mildly on the upside at this point. Fall from 1.2892 could have completed with three waves down to 1.2298. Further rise should be seen and break of 61.8% projection of 1.2298 to 1.2568 from 1.2471 will target 100% projection at 1.2741. For now, further rally will be expected as long as 1.2471 support holds, in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

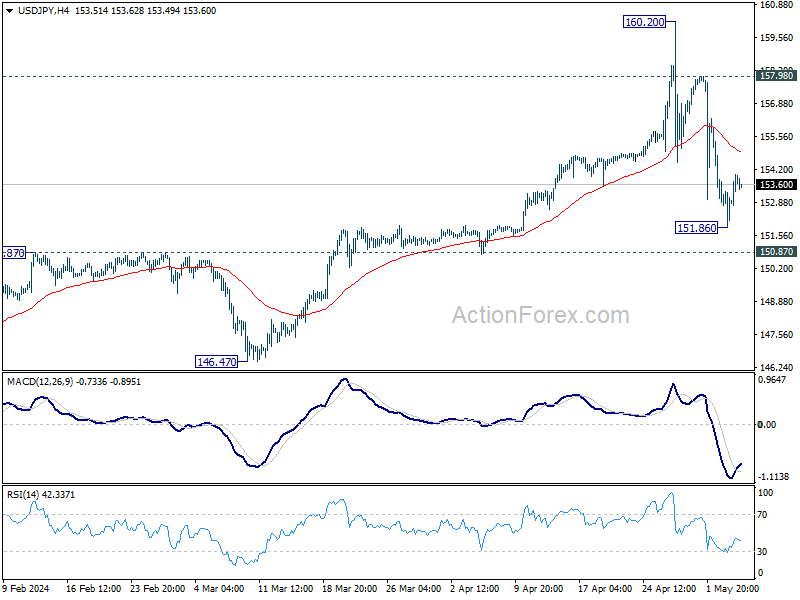

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.95; (P) 152.90; (R1) 153.92; More...

Intraday bias in USD/JPY remains neutral at this point. On the upside, firm break of 55 4H EMA (now at 154.95) will bring stronger rebound towards 157.98 resistance. On the downside, below 151.86 will resume the fall from 160.20. But strong support should be seen from 150.87 resistance turned support to bring rebound.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

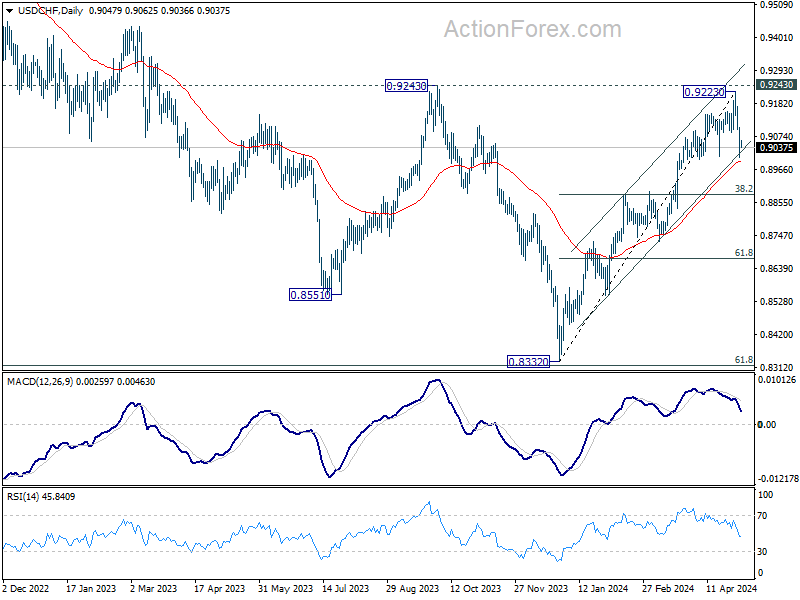

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9001; (P) 0.9055; (R1) 0.9104; More....

Outlook in USD/CHF is unchanged and intraday bias stays on the downside. Sustained break of 55 D EMA (now at 0.8993) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. On the upside, above 0.9087 minor resistance will turn intraday bias again first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Focus on RBA as Australian Dollar Maintains Strength

As the market transitions into US session, Australian Dollar maintains its position as the strongest currency of the day. While no significant economic data is expected from the US or Canada, the focus shifts to appearances by SNB Chair Thomas Jordan, as well as Fed officials Thomas Barkin and John Williams. However, traders are expected to look through these events, anticipating insights from the RBA's decision.

Expectations are widespread that RBA will maintain its policy rate unchanged at 4.35%. Attention will be directed towards the new economic forecasts and the post-meeting press conference. The key question revolves around whether Governor Michele Bullock will shift her stance from a neutral position of "no ruling anything in or out" to a "tightening bias" stance.

Any shift in Bullock's tone could indicate the central bank's future direction, whether it's on track for either a rate cut as some economists expect in November. Or a hike as forecasted by Judo Bank chief economic adviser Warren Hogan, top economic forecaster in the Australian Financial Review's first annual ranking of economists in 2023.

In the broader currency markets, Sterling and Kiwi are also displaying strength. Yen trails as the weakest currency, followed by Swiss Franc and the Dollar. Euro and the Canadian Dollar occupy middle positions. This picture reflects a prevailing risk-on sentiment mirrored in the rally in major European indexes and US futures.

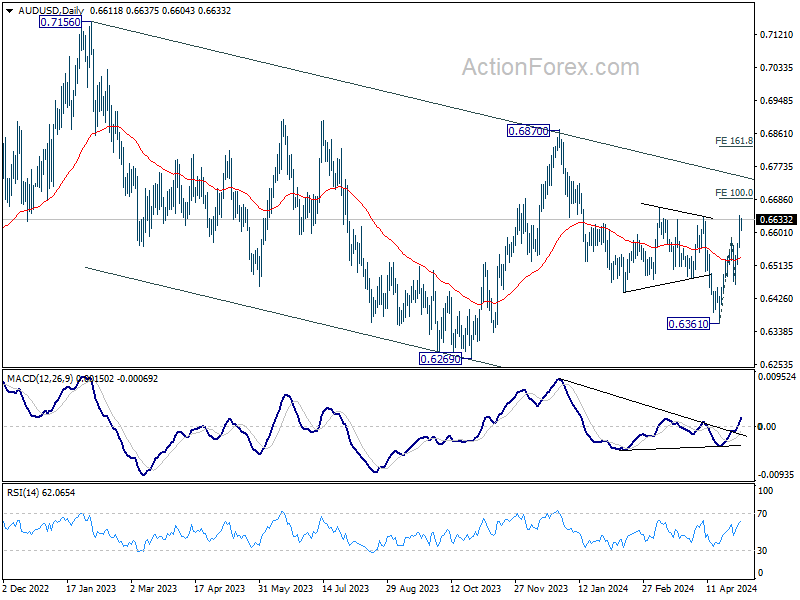

Technically, a major focus now is on AUD/USD. Current rise from 0.6361 is in progress for 100% projection of 0.6361 to 0.6585 from 0.6464 at 0.6688. Decisive break there could prompt upside acceleration, which would bolster the case that it's indeed resuming the rally from 0.6269. That would in turn shift favor to the case that whole corrective fall from 0.7156 has completed at 0.6269 already. Let's see how it goes.

In Europe, at the time of writing, UK is on holiday. DAX is up 0.99%. CAC is up 0.79%. Germany 10-year yield is down -0.0483 at 2.450. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.55%. China Shanghai SSE rose 1.16%. Singapore Strait Times rose 0.31%.

Eurozone PPI falls -0.4% mom, -7.8% yoy in Mar

Eurozone PPI fell -0.4% mom, -7.8% yoy in March. For the month, industrial producer prices increased by 0.1% for intermediate goods, 0.1% for capital goods, 0.1% for durable consumer goods, and 0.4% for non-durable consumer goods. Prices decreased by -1.8% for energy.

EU PPI fell -0.5% mom, -7.6% yoy. Among Member States for which data are available, the largest monthly decreases in industrial producer prices were recorded in Bulgaria (-3.4%), Denmark and Greece (both -2.3%) and Spain (-2.2%). Increases were observed in Ireland and Sweden (both +0.9%) as well as in Germany and Croatia (both +0.2%).

Eurozone Sentix rises to -3.6, window for ECB rate cut limited

Eurozone Sentix Investor Confidence rose from -5.9 to -3.6 in May, above expectation of -4.8. This marks the seventh consecutive increase and the highest level since February 2022. Additionally, Current Situation Index climbed from -16.3 to -14.3, marking seven consecutive increases and reaching its highest point since May 2023. Expectations Index also saw growth, rising from 5.0 to 7.8, marking eight consecutive increases and reaching its highest level since February 2022.

Sentix noted that while the data presents an encouraging picture, indicating a gradual recovery from the economic challenges of the past two years, underlying weaknesses in momentum persist. The rise in expectations, though positive, is described as "very sluggish" and has yet to substantially impact the situation values.

As for ECB, Sentix said the window for cutting interest rate "does not appear to be very large". Despite improvements in the economy, a deteriorating inflation environment adds pressure to bond markets.

Eurozone PMI services finalized at 53.3, highest in 11 months

Eurozone's PMI services index was finalized at to 53.3 in April, marking a notable improvement from March's 51.5. PMI Composite was finalized at 51.7, up from the previous month's 50.3 Both reached the highest levels in 11 months.

Notable country-level performances on PMI Composite include Spain reaching a 12-month high at 55.7, Germany achieving a 10-month high at 50.6, and France hitting an 11-month high at 50.5. However, Italy recorded a two-month low at 52.6, and Ireland saw a six-month low at 50.4.

Chief Economist at Hamburg Commercial Bank, Cyrus de la Rubia, highlighted the positive momentum, noting that service providers have witnessed growth for the third consecutive month, signaling an end to the lackluster performance observed in the latter half of the previous year. He emphasized the uptick in employment, new business, and order book growth, which reached its strongest expansion in eleven months.

However, concerns regarding operating costs persist, with PMI index for operating costs in the service sector continuing to rise rapidly over the past year. De la Rubia cautioned that ECB is likely to adopt a cautious approach regarding potential rate cuts, given this trend. Despite this, service companies have managed to offset some of the cost increases by passing them on to consumers, reflecting improving demand conditions.

China's Caixin PMI services dips to 52.5, weak expectations a major hurdle

China's Caixin PMI Services for April, while dipping slightly from 52.7 to 52.5 as expected, maintains a growth streak for the 16th consecutive month. The sector sees robust expansion in new business, marking its fastest pace in nearly a year. Business confidence also reaches its peak for the year so far. PMI Composite, which edged up from 52.7 to 52.8, reached its highest level since May 2023

"The growth in supply and demand in the manufacturing and services sectors picked up pace, with outstanding export growth," notes Wang Zhe, Senior Economist at Caixin Insight Group. However, Wang cautions, "the pressure on the job market should not be overlooked," with employment metrics experiencing a sharper decline compared to the previous month.

Furthermore, Wang highlights the persistent challenges in pricing dynamics, stating that "input and output prices remained relatively low, particularly due to the drag from manufacturing factory gate prices."

Wang noted, "Weak expectations remain one of the major hurdles facing economic development, leading to increasing pressure on employment and a greater risk of deflation."

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9001; (P) 0.9055; (R1) 0.9104; More....

Outlook in USD/CHF is unchanged and intraday bias stays on the downside. Sustained break of 55 D EMA (now at 0.8993) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. On the upside, above 0.9087 minor resistance will turn intraday bias again first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | TD Securities Inflation M/M Apr | 0.10% | 0.10% | ||

| 01:45 | CNY | Caixin Services PMI Apr | 52.5 | 52.5 | 52.7 | |

| 07:45 | EUR | Italy Services PMI Apr | 54.3 | 54.7 | 54.6 | |

| 07:50 | EUR | France Services PMI Apr | 51.3 | 50.5 | 50.5 | |

| 07:55 | EUR | Germany Services PMI Apr F | 53.2 | 53.3 | 53.3 | |

| 08:00 | EUR | Eurozone Services PMI Apr F | 53.3 | 52.9 | 52.9 | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence May | -3.6 | -4.8 | -5.9 | |

| 09:00 | EUR | Eurozone PPI M/M Mar | -0.40% | -0.70% | -1.00% | -1.10% |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | -7.8% | -8.30% | -8.50% |

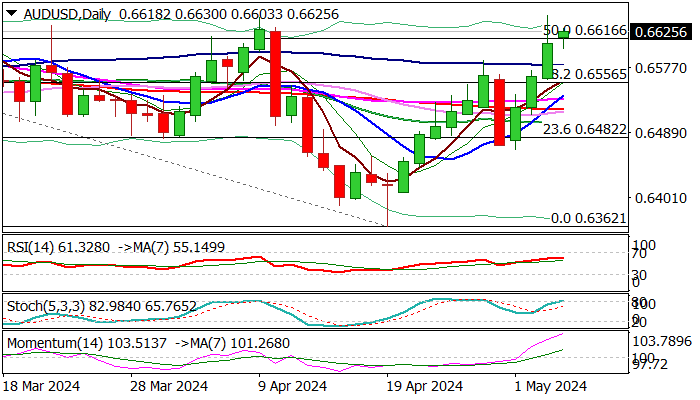

AUD/USD: Bulls Hold Grip Ahead of RBA Policy Meeting on Tuesday

AUDUSD keeps firm tone on Monday, despite Friday’s spike and subsequent pullback, though with initial warning that traders may opt for a partial profit taking after strong rally in past two days, when the pair advanced 2%.

Stretched daily studies add to signals of correction, but dips are likely to be shallow and ideally contained by 100DMA (0.6579) to position for fresh attack at key 0.6660/70 zone (multiple tops of Mar/Apr /May, also near Fibo 61.8% of 0.6871/0.6362) violation of which to spark acceleration towards 0.6750 zone.

The action is also supported by two large consecutive bullish weekly candles, with expectations that Australia’s policymakers may show more hawkishness in Tuesday’s RBA policy meeting (rate hike is still on the table) expected to further underpin Aussie dollar.

Res: 0.6644; 0.6667; 0.6676; 0.6750.

Sup: 0.6600; 0.6579; 0.6556; 0.6520.