Sample Category Title

RBA’s Lack of Hawkishness Weakens Aussie, Yen’s Retreat Continues

In the aftermath of RBA's decision to maintain interest rates unchanged and the absence of explicit hawkish signals, Australian Dollar weakens mildly. Despite notable upgrades in inflation forecasts, the central bank opted for a cautious approach, refraining from signaling imminent rate hikes and maintaining a stance of "not ruling anything in or out." Recent stronger-than-expected inflation data did not push RBA closer to resume monetary tightening, at least for the time being.

Meanwhile, Japanese Yen displayed continued weakness, retracing last week's strong gains. Japan's top currency diplomat, Masato Kanda, chose not to comment US Treasury Secretary Janet Yellen's recent assertion that currency intervention is permissible only in exceptional circumstances. Kanda's posture led markets to believe that last week's alleged intervention may have been unilateral rather than coordinated.

Overall in the currency markets, Dollar is the strongest one for today at this point, followed by Euro and Kiwi. Canadian Dollar and Swiss Franc are on the softer side while Sterling is mixed.

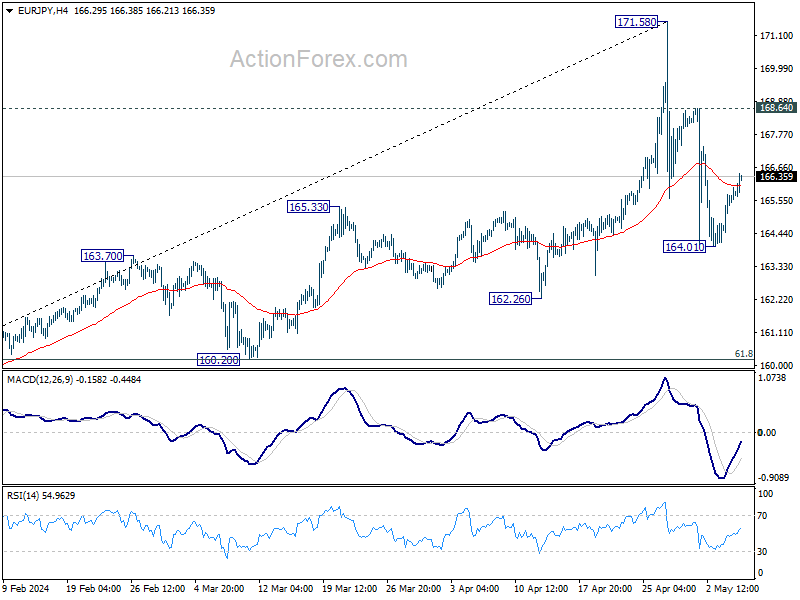

Technically, EUR/JPY's break of 55 4H EMA suggests that fall from 171.68 could have completed at 164.01 already. Rise from there is seen as the second leg of the corrective pattern from 171.68 and could extend towards 168.64 resistance. Attention is now on whether USD/JPY and GBP/JPY would break through their respective 55 4H EMA to align and solidify this outlook.

In Asia, at the time of writing, Nikkei is up 1.29%. Hong Kong HSI is down -0.74%. China Shanghai SSE is up 0.01%. Singapore Strait Times is up 0.08%. Japan 10-year JGB yield is down -0.0311 at 0.875. Overnight, DOW rose 0.46%. S&P 500 rose 1.03%. NASDAQ rose 1.19%. 10-year yield fell -0.0110 to 4.489.

RBA stands pat, upgrades inflation forecasts, not ruling anything in or out

RBA left cash rate target unchanged at 4.35% as widely expected. The central bank maintained that it's "not ruling anything in or out" regarding the next move in monetary policy because of uncertainty surround inflation outlook.

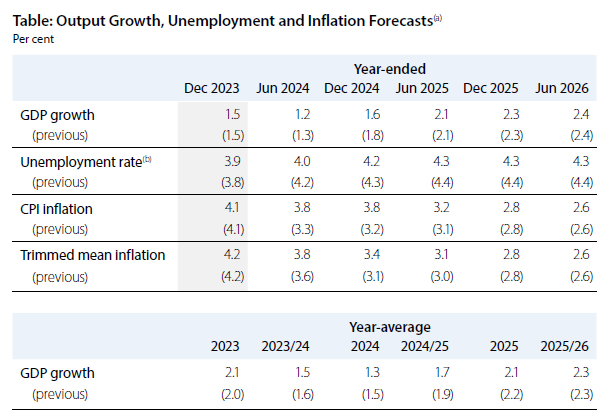

In the new economic forecasts, both headline and core inflation forecasts for 2024 are upgraded substantially. Meanwhile, growth forecasts were downgraded slightly for both 2024 and 2025.

Year-average GDP growth:

- For 2024 downgraded from 1.5% to 1.3%

- For 2025 downgraded from 2.2% to 2.1%.

Year-ended CPI inflation:

- For Dec 2024 upgraded from 3.2% to 3.8%.

- For Dec 2025 unchanged at 2.8%.

- For June 2026 at 2.6% (new).

Year-ended trimmed mean inflation:

- For Dec 2024 upgraded from 3.1% to 3.4%.

- For Dec 2025 unchanged at 2.8%.

- For June 2026 at 2.6% (new)

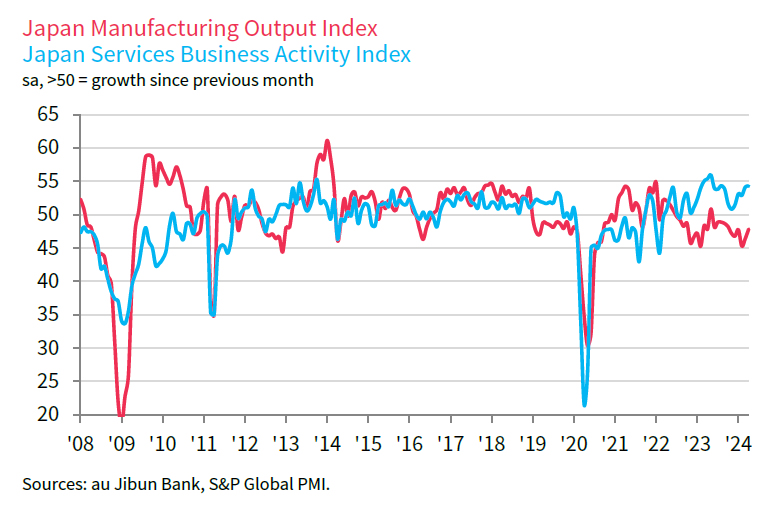

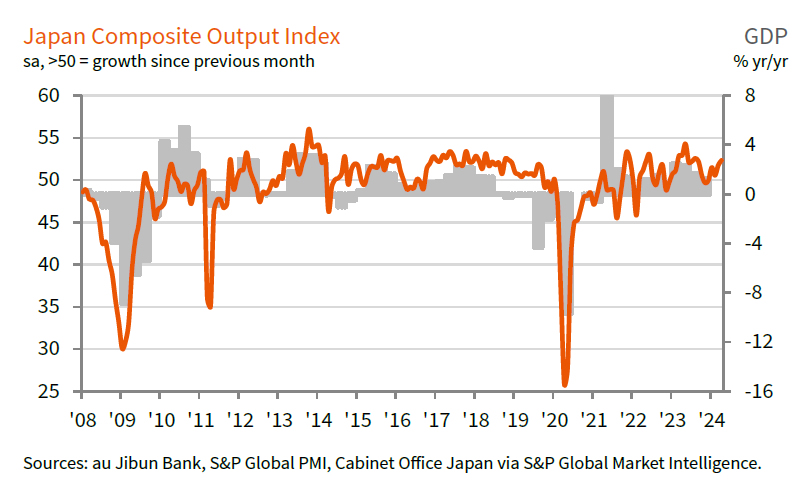

Japan's PMI services finalized at 54.3, strong demand and rising costs

Japan's PMI Services for April finalized at 54.3, slightly up from March's 54.1. PMI Composite also saw an uptick, reaching 52.3, the highest level since August 2023.

According to Tim Moore, Economics Director at S&P Global Market Intelligence, April showcased "another strong month" for the service sector, driven by increasing business and consumer spending. This momentum resulted in the fastest upturn in business activity since August 2023. Despite challenges such as shortages of candidates hindering recruitment, positivity regarding the longer-term business outlook contributed to solid employment growth.

However, rising wage costs have emerged as a significant concern, leading to the sharpest increase in average cost burdens in eight months. Service providers are responding to elevated cost pressures by seeking higher prices from clients, with the latest survey indicating the fastest pace of price increases since the sales tax hike in April 2014.

Fed's Barkin: More demand moderation needed

Richmond Fed President Thomas Barkin's said overnight that the pace of disinflation has possibly stalled. "We're going to need a little more edge off of demand to get all the way" back to target, he added. Despite these challenges, he expressed optimism regarding the current level of the benchmark policy rate, indicating confidence that it will effectively address inflation.

"I still have the weight going toward inflation," Barkin said. "It's a stubborn road back...It doesn't mean you won't get it back. It just means it takes a while...to corral price setters into believing they don't really have a chance" for aggressive increases.

Separately, New York Fed President John Williams affirmed that "eventually we'll have rate cuts". But for now, monetary policy is in a "very good place." He refrained from providing a specific timetable for rate adjustments but noted that the economy is gradually returning to better balance amid a shift to a slower rate of growth. He anticipates GDP growth in the range of 2-2.5% for the year.

Looking ahead

Swiss unemployment rate and foreign currency reserves, Germany factor orders and trade balance, France trade balance, UK PMI construction, and Eurozone retail sales will be released in European session. Later in the day, Canada will release Ivey PMI.

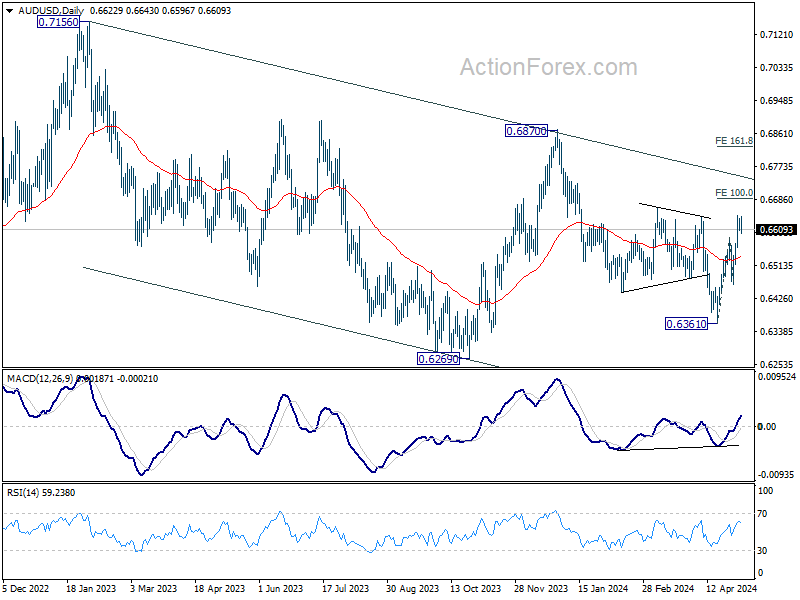

AUD/USD Daily Report

Daily Pivots: (S1) 0.6608; (P) 0.6623; (R1) 0.6642; More...

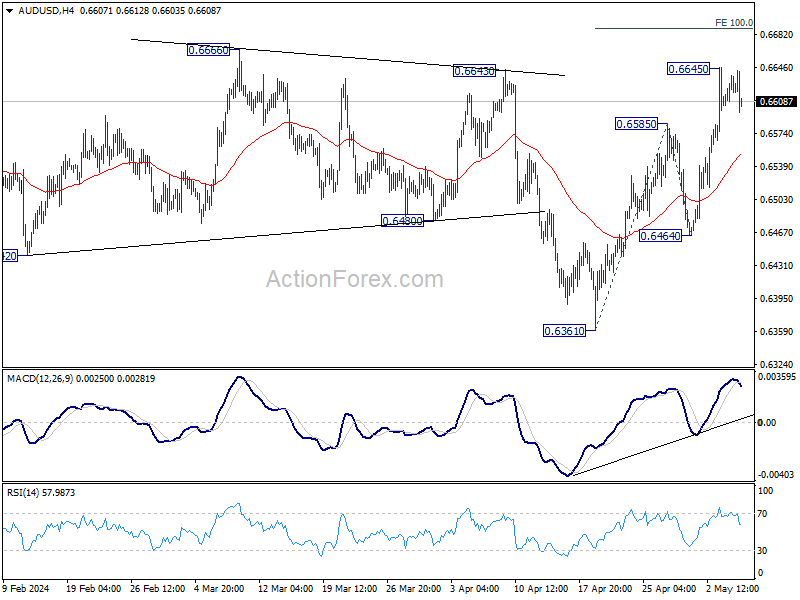

Intraday bias in AUD/USD is turned neutral with current retreat. Some consolidations could be seen but further rally is expected as long as 0.6464 support holds. As noted before, fall from 0.6870 could have completed with three waves down to 0.6361. Above 0.6645 will target 100% projection of 0.6361 to 0.6585 from 0.6464 at 0.6688 next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Services PMI Apr F | 54.3 | 54.6 | 54.6 | |

| 04:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 05:30 | AUD | RBA Press Conference | ||||

| 05:45 | CHF | Unemployment Rate M/M Apr | 2.30% | 2.30% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | 22.4B | 21.4B | ||

| 06:00 | EUR | Germany Factory Orders M/M Mar | 0.40% | 0.20% | ||

| 06:45 | EUR | France Trade Balance (EUR) Mar | -5.0B | -5.2B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Apr | 715B | |||

| 08:30 | GBP | Construction PMI Apr | 51.1 | 50.2 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Mar | 0.60% | -0.50% | ||

| 14:00 | CAD | Ivey PMI Apr | 58.1 | 57.5 |

RBA stands pat, upgrades inflation forecasts, not ruling anything in or out

RBA left cash rate target unchanged at 4.35% as widely expected. The central bank maintained that it's "not ruling anything in or out" regarding the next move in monetary policy because of uncertainty surround inflation outlook.

In the new economic forecasts, both headline and core inflation forecasts for 2024 are upgraded substantially. Meanwhile, growth forecasts were downgraded slightly for both 2024 and 2025.

Year-average GDP growth:

- For 2024 downgraded from 1.5% to 1.3%

- For 2025 downgraded from 2.2% to 2.1%.

Year-ended CPI inflation:

- For Dec 2024 upgraded from 3.2% to 3.8%.

- For Dec 2025 unchanged at 2.8%.

- For June 2026 at 2.6% (new).

Year-ended trimmed mean inflation:

- For Dec 2024 upgraded from 3.1% to 3.4%.

- For Dec 2025 unchanged at 2.8%.

- For June 2026 at 2.6% (new)

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.25 per cent.

Inflation remains high and is falling more gradually than expected.

Recent information indicates that inflation continues to moderate, but is declining more slowly than expected. The CPI grew by 3.6 per cent over the year to the March quarter, down from 4.1 per cent over the year to December. Underlying inflation was higher than headline inflation and declined by less. This was due in large part to services inflation, which remains high and is moderating only gradually.

Higher interest rates have been working to bring aggregate demand and supply somewhat closer towards balance. But the data indicate continuing excess demand in the economy, coupled with strong domestic cost pressures, both for labour and non-labour inputs. Conditions in the labour market have eased over the past year, but remain tighter than is consistent with sustained full employment and inflation at target. Wages growth appears to have peaked but is still above the level that can be sustained given trend productivity growth. Meanwhile, inflation is still weighing on people's real incomes and output growth has been subdued, reflecting weak household consumption growth.

The outlook remains highly uncertain.

The economic outlook remains uncertain and recent data have demonstrated that the process of returning inflation to target is unlikely to be smooth.

The central forecasts, based on the assumption that the cash rate follows market expectations, are for inflation to return to the target range of 2–3 per cent in the second half of 2025, and to the midpoint in 2026. In the near term, inflation is forecast to be higher because of the recent rise in domestic petrol prices, and higher than expected services price inflation, which is now forecast to decline more slowly over the rest of the year. Inflation is, however, expected to decline over 2025 and 2026.

The persistence of services inflation is a key uncertainty. It is expected to ease more slowly than previously forecast, reflecting stronger labour market conditions including a more gradual increase in the unemployment rate and the broader underutilisation rate. Growth in unit labour costs also remains very high. It has begun to moderate slightly as measured productivity growth picked up in the second half of last year. This trend needs to be sustained over time if inflation is to continue to decline.

At the same time, household consumption growth has been particularly weak as high inflation and the earlier rises in interest rates have affected real disposable income. In response, households have been curbing discretionary spending and maintaining their saving. Real incomes have now stabilised and are expected to grow later in the year, supporting growth in consumption. But there is a risk that household consumption picks up more slowly than expected, resulting in continued subdued output growth and a noticeable deterioration in the labour market.

More broadly, there are uncertainties regarding the lags in the effect of monetary policy and how firms' pricing decisions and wages will respond to the slower growth in the economy at a time of excess demand, and while the labour market remains tight.

There also remains a high level of uncertainty about the overseas outlook. While there has been improvement in the outlook for the Chinese and US economies, and many global commodity prices have picked up, geopolitical uncertainties, including those related to the conflicts in the Middle East and Ukraine, remain elevated.

Returning inflation to target is the priority.

Returning inflation to target within a reasonable timeframe remains the Board's highest priority. This is consistent with the RBA's mandate for price stability and full employment. The Board needs to be confident that inflation is moving sustainably towards the target range. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

Recent data indicate that, while inflation is easing, it is doing so more slowly than previously expected and it remains high. The Board expects that it will be some time yet before inflation is sustainably in the target range and will remain vigilant to upside risks. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe remains uncertain and the Board is not ruling anything in or out. The Board will rely upon the data and the evolving assessment of risks. In doing so, it will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target.

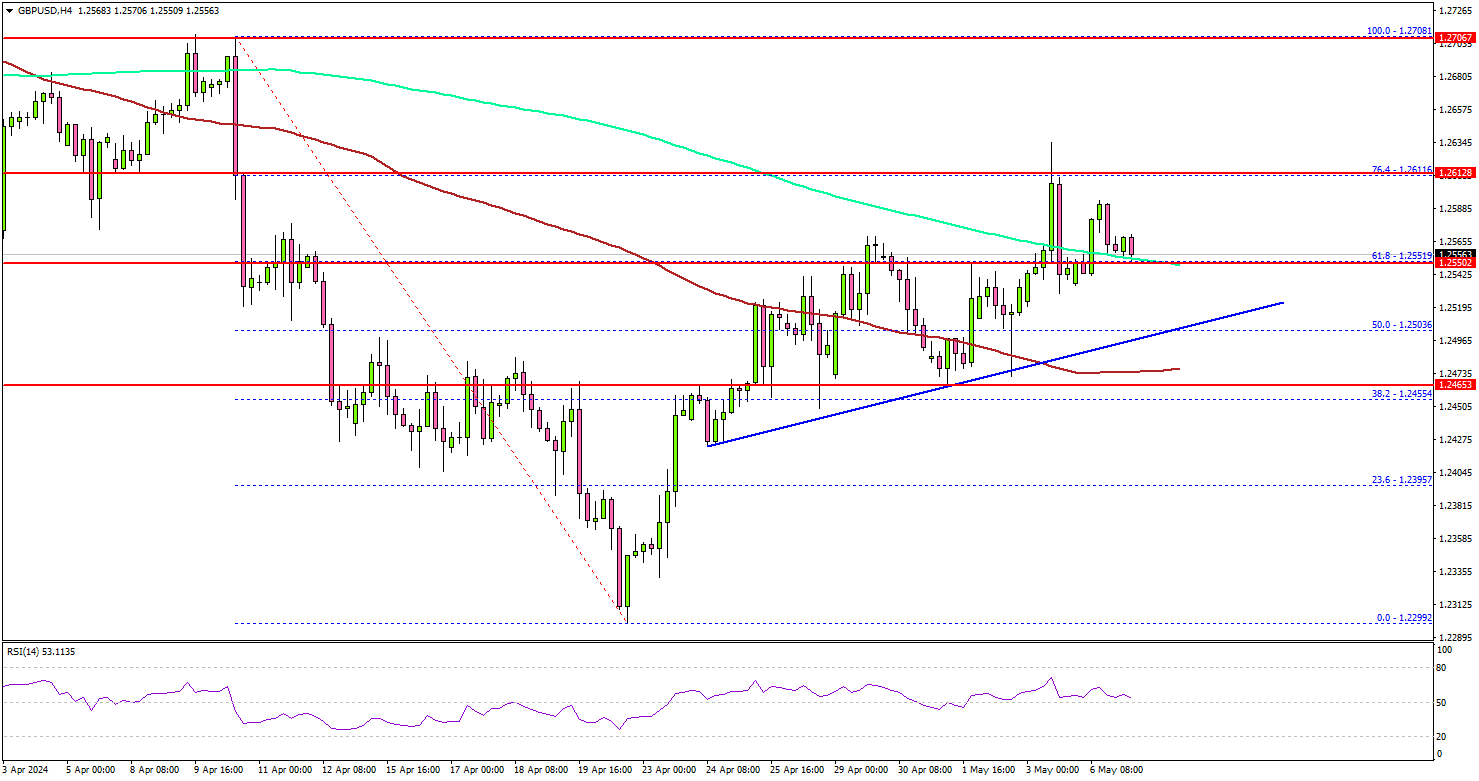

GBP/USD Aims Higher As Dollar Signals Weakness

Key Highlights

- GBP/USD started a recovery wave above the 1.2500 resistance.

- A connecting bullish trend line is forming with support at 1.2500 on the 4-hour chart.

- Gold prices are attempting a fresh increase above the $2,300 resistance.

- Bitcoin recovered losses and was able to retest the $65,000 resistance zone.

GBP/USD Technical Analysis

The British Pound found support near 1.2300 against the US Dollar. GBP/USD started a decent increase and was able to clear the 1.2450 resistance.

Looking at the 4-hour chart, the pair climbed above the 50% Fib retracement level of the downward move from the 1.2708 swing high to the 1.2299 low. It also settled above the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour).

However, the bears were active near the 1.2620 resistance. They prevented a close above the 76.4% Fib retracement level of the downward move from the 1.2708 swing high to the 1.2299 low.

A clear move above the 1.2620 resistance might send it toward the 1.2700 level. Any more gains might call for a move toward the 1.2800 level in the near term.

Immediate support is near the 1.2550 level and the 200 simple moving average (green, 4-hour). The next major support is at 1.2520. There is also a connecting bullish trend line forming with support at 1.2500 on the same chart.

If there is a downside break below the 1.2520 support, the pair might test 1.2465 and the 100 simple moving average (red, 4-hour). Any more losses might send the pair toward 1.2420.

Looking at Bitcoin, the price gained bullish momentum and was able to test the key resistance at $65,000 and $65,200.

Economic Releases

- UK’s Construction PMI for April 2024 – Forecast 50.4, versus 50.2 previous.

- Euro Zone Retail Sales for April 2024 (MoM) - Forecast +0.6%, versus -0.5% previous.

Japan’s PMI services finalized at 54.3, strong demand and rising costs

Japan's PMI Services for April finalized at 54.3, slightly up from March's 54.1. PMI Composite also saw an uptick, reaching 52.3, the highest level since August 2023.

According to Tim Moore, Economics Director at S&P Global Market Intelligence, April showcased "another strong month" for the service sector, driven by increasing business and consumer spending. This momentum resulted in the fastest upturn in business activity since August 2023. Despite challenges such as shortages of candidates hindering recruitment, positivity regarding the longer-term business outlook contributed to solid employment growth.

However, rising wage costs have emerged as a significant concern, leading to the sharpest increase in average cost burdens in eight months. Service providers are responding to elevated cost pressures by seeking higher prices from clients, with the latest survey indicating the fastest pace of price increases since the sales tax hike in April 2014.

Fed’s Barkin: More demand moderation needed

Richmond Fed President Thomas Barkin's said overnight that the pace of disinflation has possibly stalled. "We're going to need a little more edge off of demand to get all the way" back to target, he added. Despite these challenges, he expressed optimism regarding the current level of the benchmark policy rate, indicating confidence that it will effectively address inflation.

"I still have the weight going toward inflation," Barkin said. "It's a stubborn road back...It doesn't mean you won't get it back. It just means it takes a while...to corral price setters into believing they don't really have a chance" for aggressive increases.

Separately, New York Fed President John Williams affirmed that "eventually we'll have rate cuts". But for now, monetary policy is in a "very good place." He refrained from providing a specific timetable for rate adjustments but noted that the economy is gradually returning to better balance amid a shift to a slower rate of growth. He anticipates GDP growth in the range of 2-2.5% for the year.

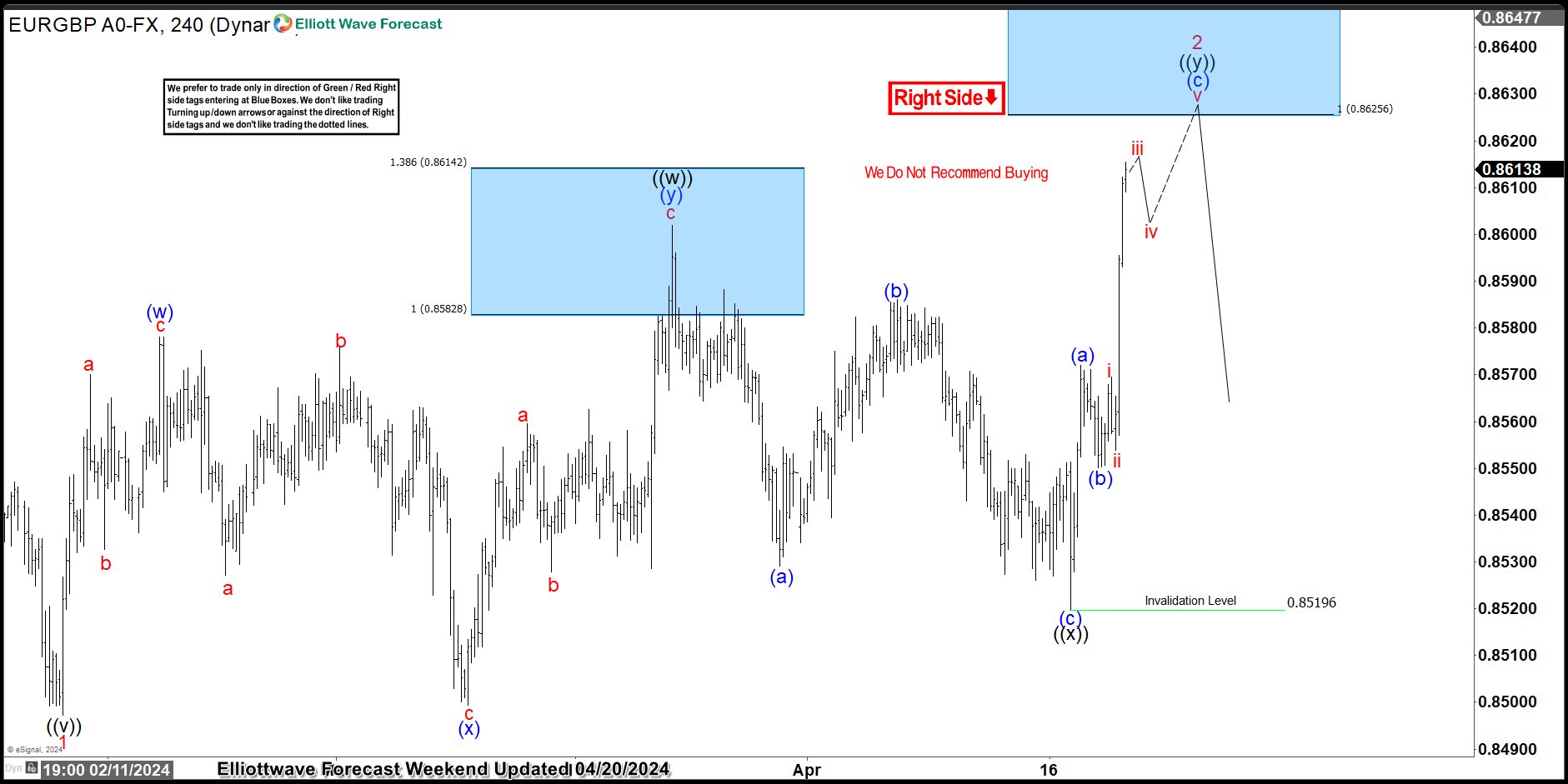

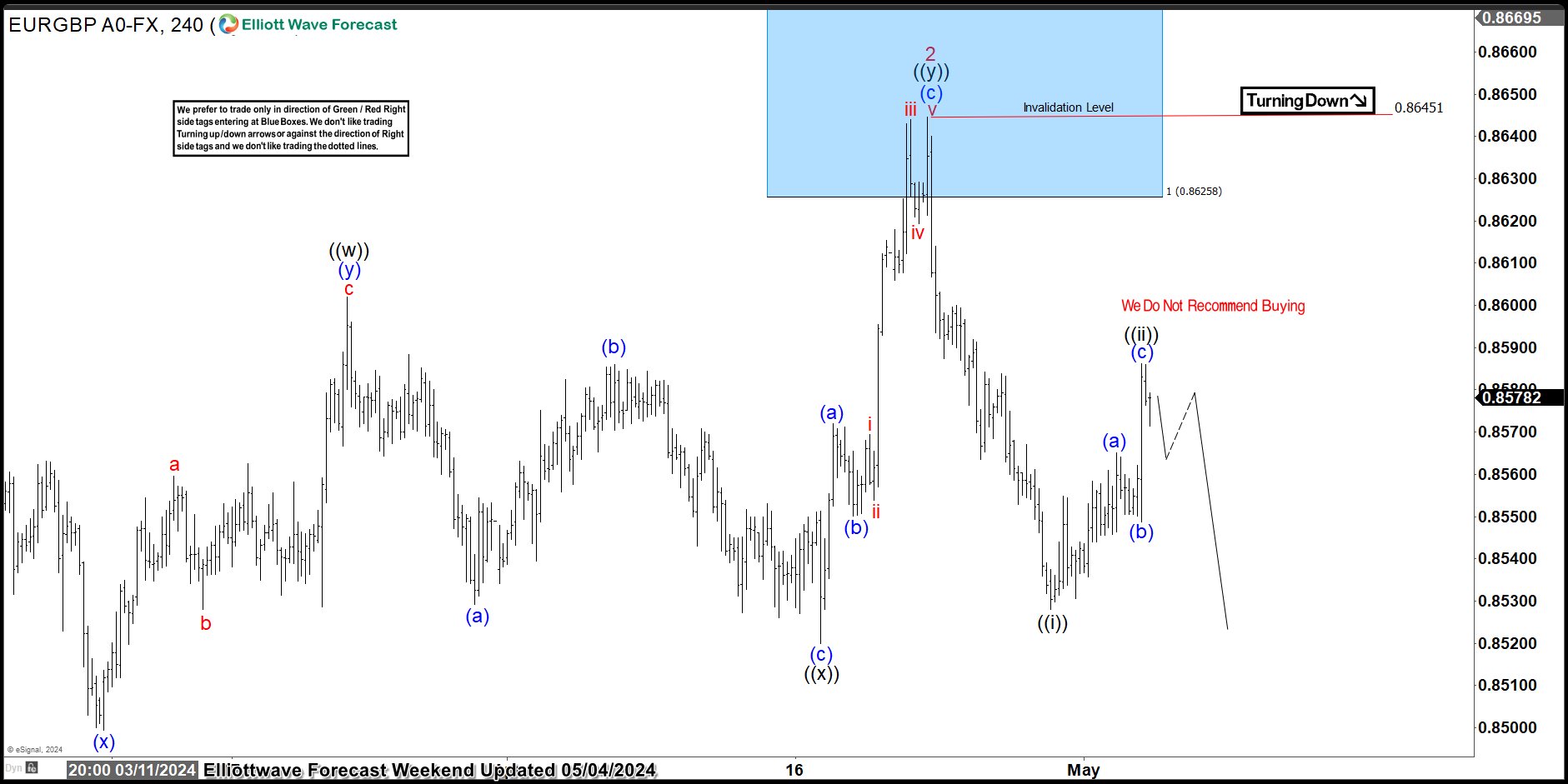

EURGBP Perfectly Reacting Lower From Blue Box Area

In this technical blog, we are going to take a look at the past performance of EURGBP 4-Hour Elliott wave Charts that we presented to our members. In which, the decline to 2/14/2024 low took place as an impulsive structure and showed a lower sequence with a bearish right side tag calling for more downside to happen. Therefore, our members knew that selling the bounces in the direction of the right side tag remained the preferred path. We will explain the Elliott wave structure & selling opportunity our members took below:

EURGBP 4-Hour Elliott Wave Chart From 4.20.2024

EURGBP 4-Hour Elliott Wave Chart from 4/20/2024 Weekend update. In which the decline to 0.8497 low ended wave 1 as an impulse sequence. Up from there, the pair made a bounce in wave 2. The internals of that bounce unfolded as a double three structure where wave ((w)) ended at 0.8602 high. Wave ((x)) pullback ended at 0.8519 low. And wave ((y)) was expected to reach the blue box area. From there, sellers were expected to appear looking for further downside or a minimum 3-wave reaction lower.

EURGBP Latest 4-Hour Elliott Wave Chart From

This is the latest 4-Hour view from the 5/04/2024 Weekend update. In which the pair is showing a reaction lower taking place from the blue box area. Allowing shorts to get into a risk-free position shortly after taking the position. But a break below the 0.8497 low remains to be seen to confirm the next extension lower towards the 0.8376- 0.8210 area & avoid double correction higher.

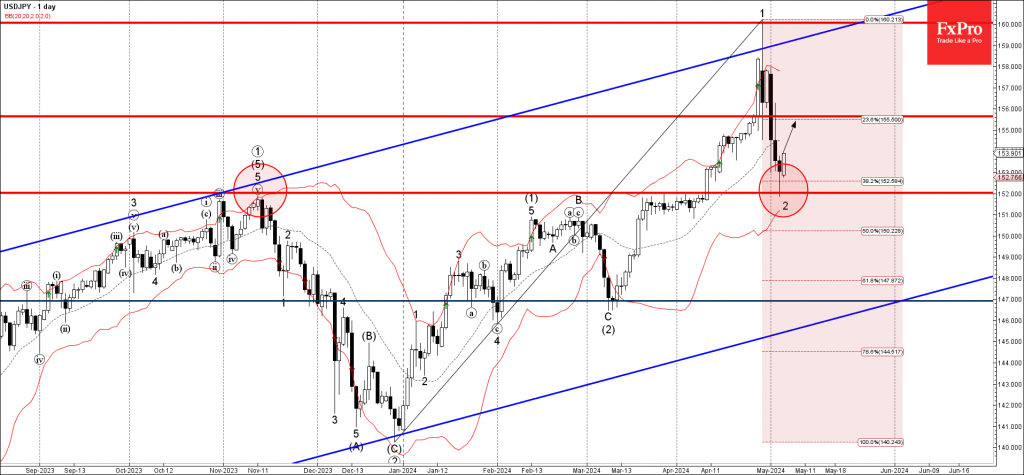

USDJPY Wave Analysis

- USDJPY reversed from support zone

- Likely to rise to resistance level 155.65

USDJPY currency pair recently reversed up from the support zone lying between the strong support level 152.00 (former multi-month high from November) and the 38.2% Fibonacci correction of the upward impulse from December.

The upward reversal from the support level 152.00 stopped the previous short-term correction 2.

Given the predominant daily uptrend and the strongly bullish US dollar sentiment seen across the FX markets today, USDJPY can be expected to rise further to the next resistance level 155.65.

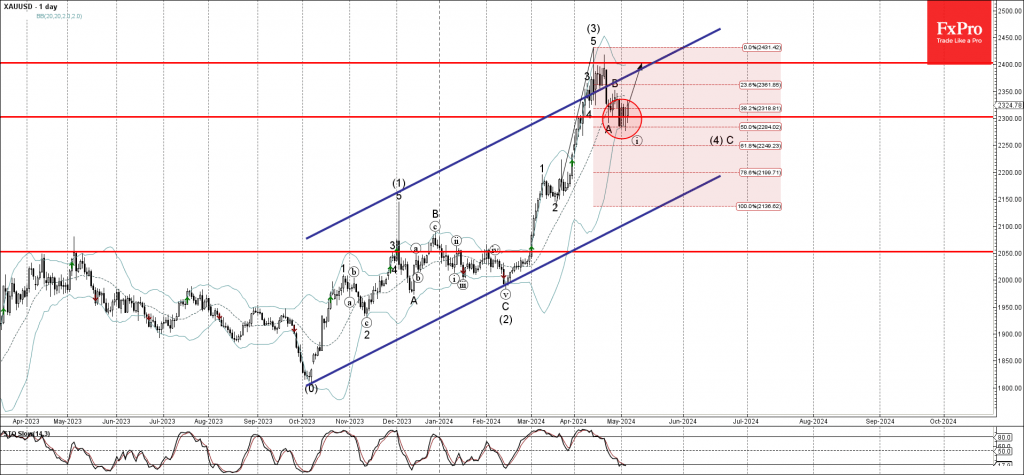

Gold Wave Analysis

- Gold reversed from support zone

- Likely to rise to resistance level 2400.00

Gold recently reversed up from the support zone lying between the support level 2300.00, lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from March.

The upward reversal from the support level 2300.00 stopped the previous intermediate ABC correction (4).

Given the clear daily uptrend, Gold can be expected to rise further to the next resistance level 2400.00, which reversed the price twice in April.