Sample Category Title

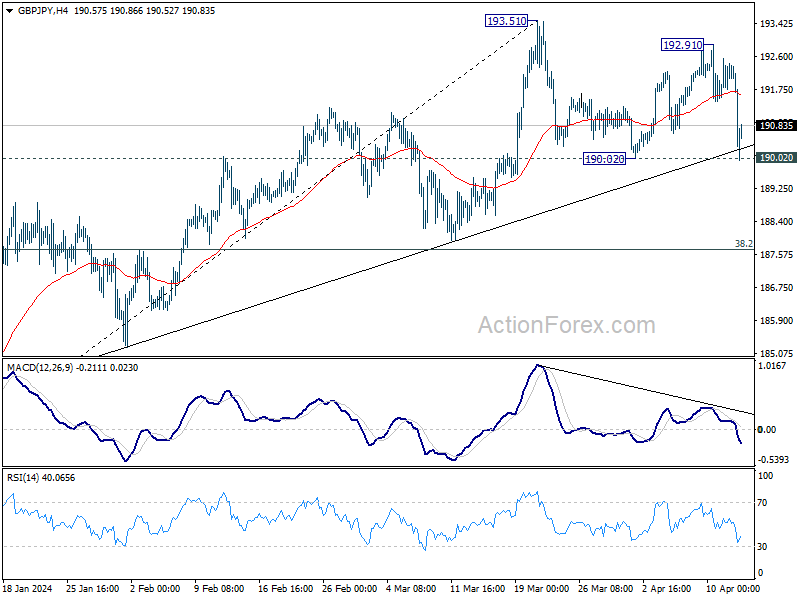

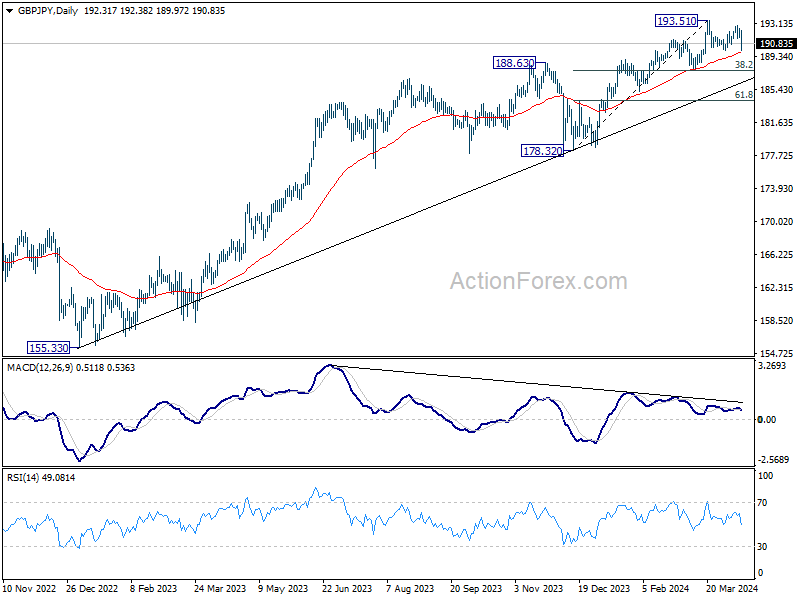

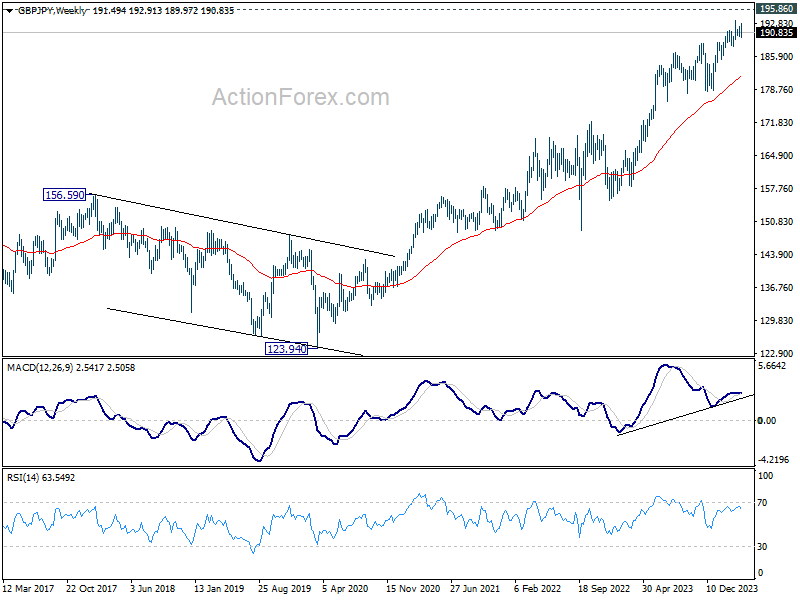

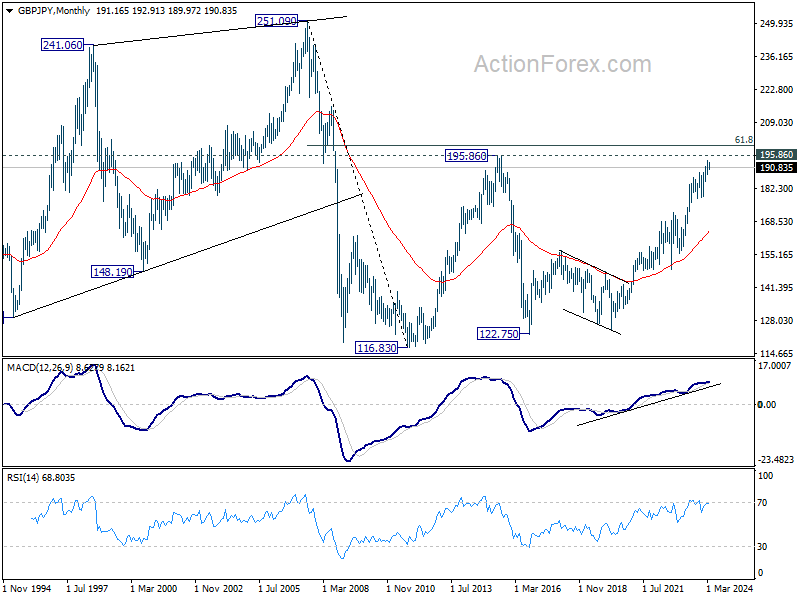

GBP/JPY Weekly Outlook

GBP/JPY retreated deeply after failing to break through 193.51 resistance, but recovered after breaching 190.02 support. Initial bias remains neutral this week first. On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. Nevertheless, decisive break of 190.02 will indicate that it's at least correcting the rise from 178.32, and target 38.2% retracement of 178.32 to 193.51 at 187.70.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Further rally will remain in favor as long as 178.32 support holds. Break of 195.86 (2015 high) is possible. But strong resistance could be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80 to limit upside, at least on first attempt.

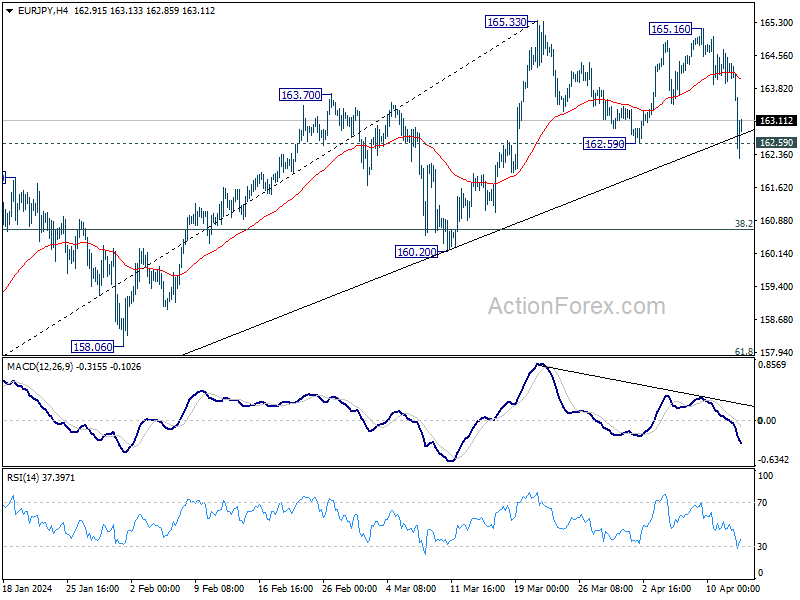

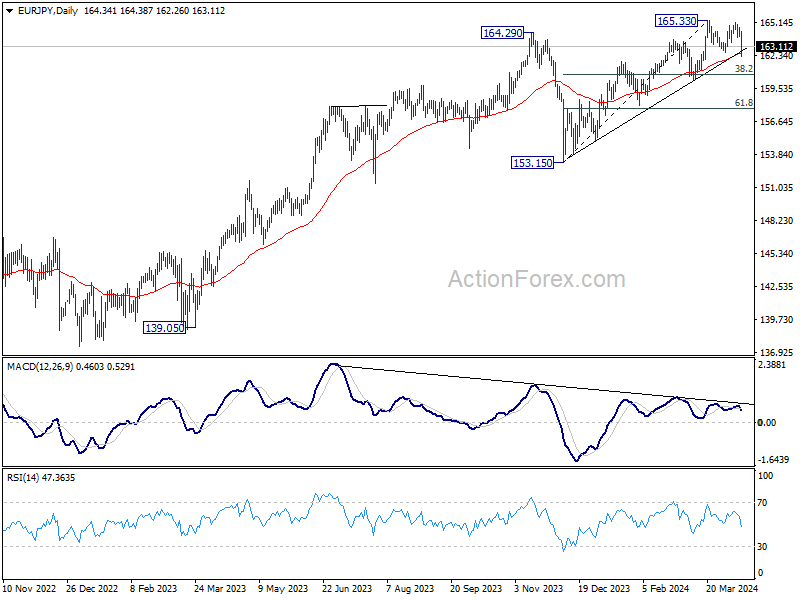

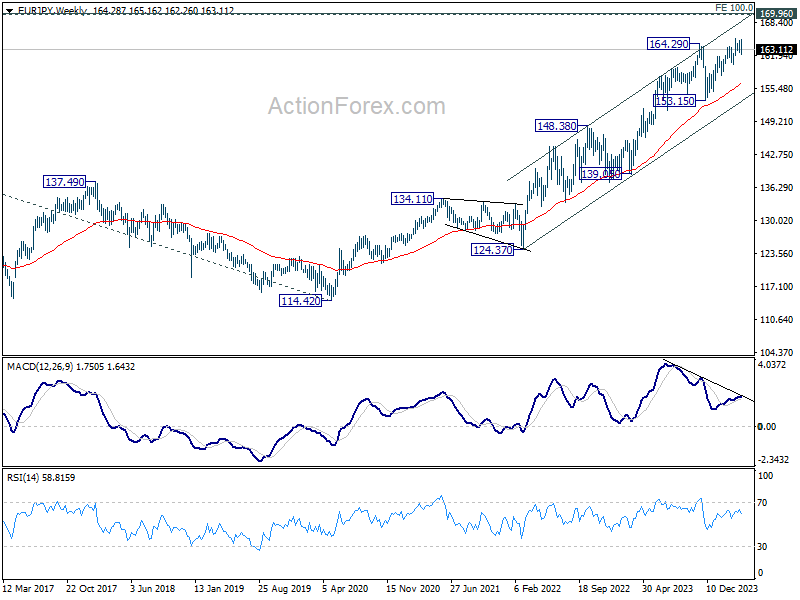

EUR/JPY Weekly Outlook

EUR/JPY failed to break through 165.33 last week and retreated sharply since then. Despite brief breach of 162.59 support, it recovered quickly. Initial bias remains neutral this week first. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. However, decisive break of 162.59 will argue that it's at least correcting the rise from 153.15, and target 38.2% retracement of 153.15 to 165.33 at 160.67.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 153.15 support holds.

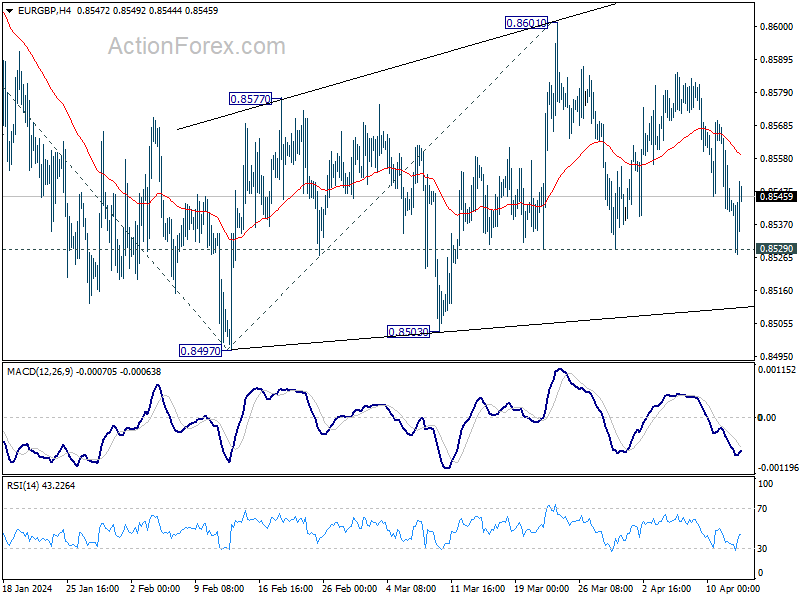

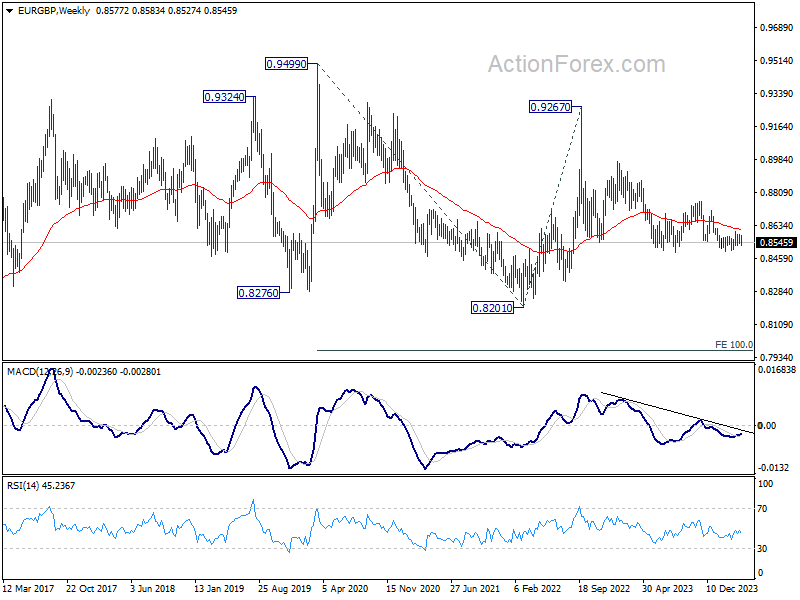

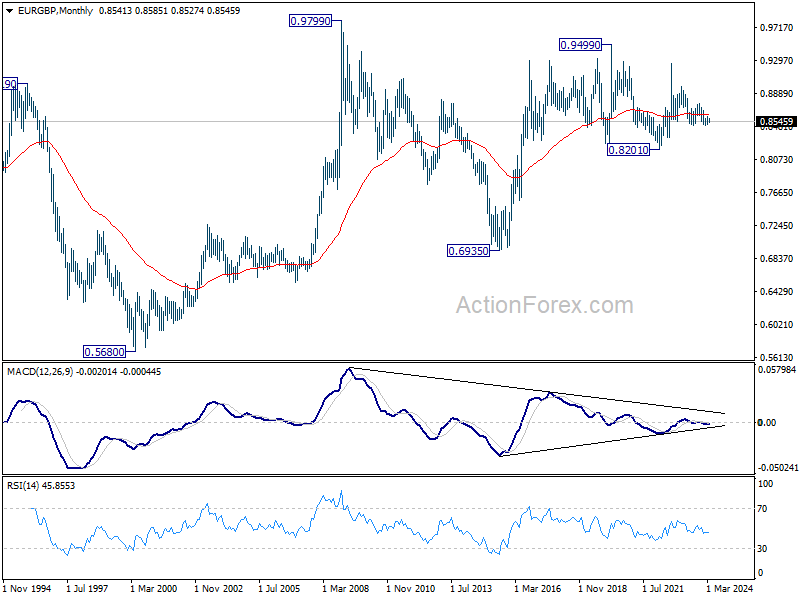

EUR/GBP Weekly Outlook

EUR/GBP stays in established range last week and outlook is unchanged. Initial bias remains neutral this week first. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8601 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

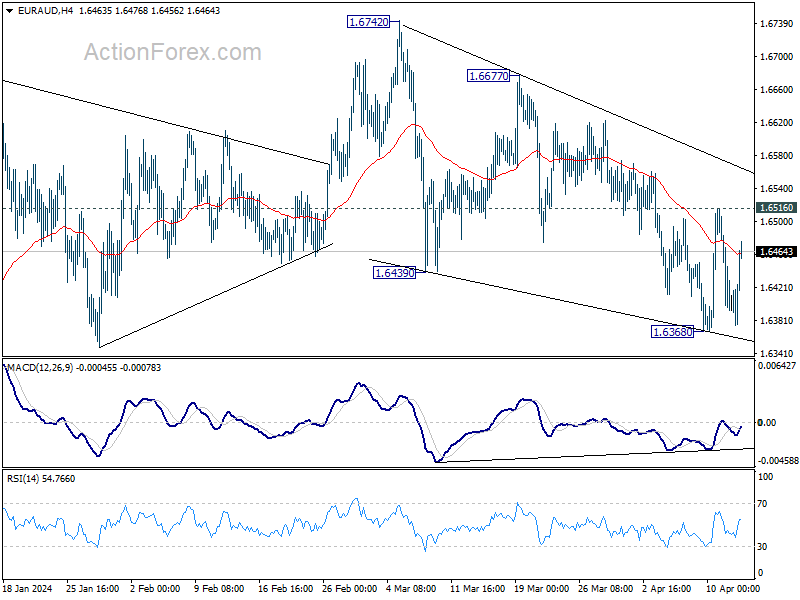

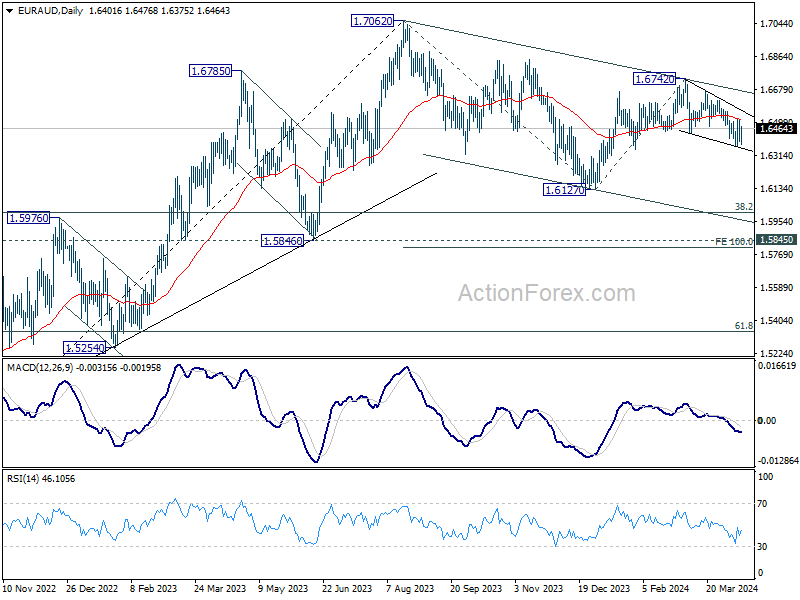

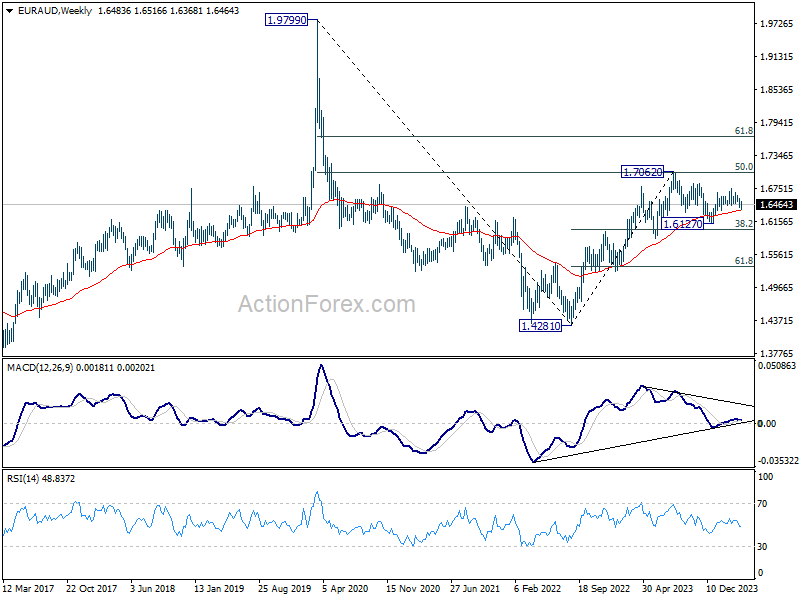

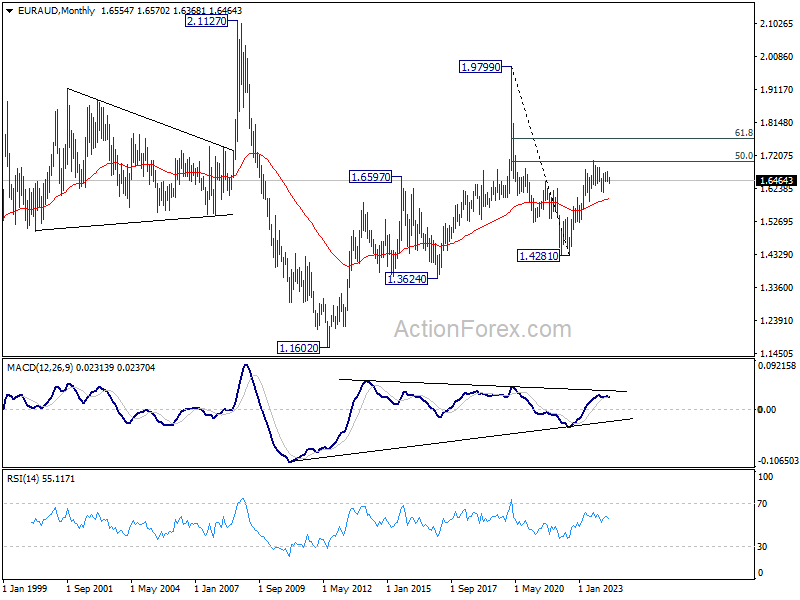

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.6742 extended to 1.6368 last week before turning sideway. Initial bias stays neutral this week first, but risk will stay on the downside as long as 1.6516 resistance holds. On the downside, below 1.6368 will resume the fall from 1.6742 towards 1.6127 low. Nevertheless, break of 1.6516 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). The correction is probably still in progress with fall from 1.6742 as the third leg. Strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5950) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

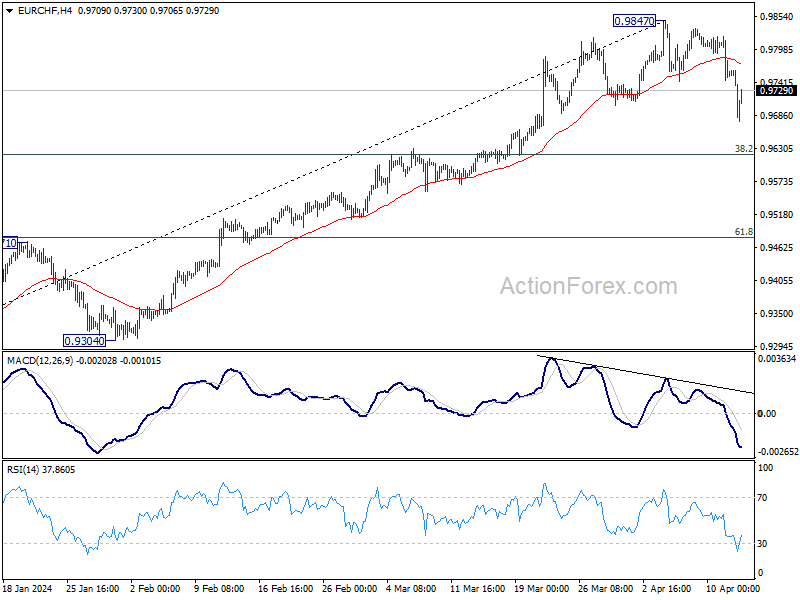

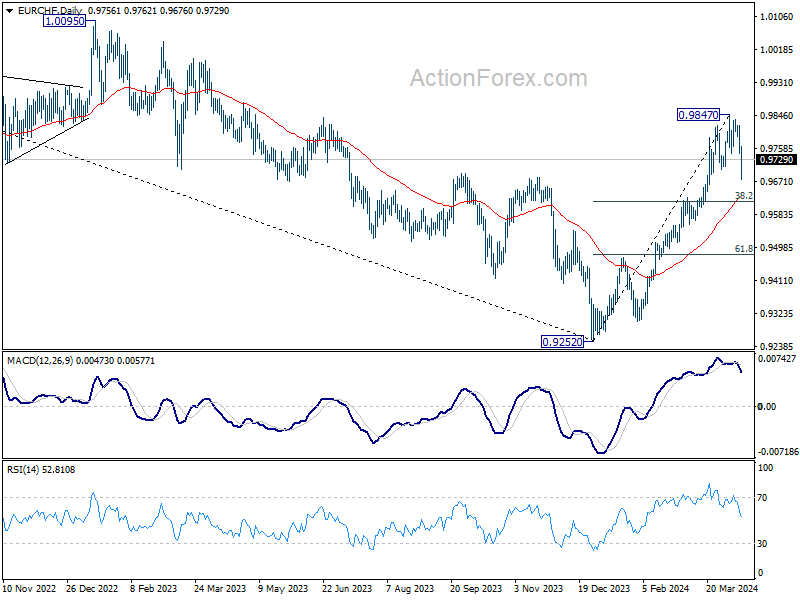

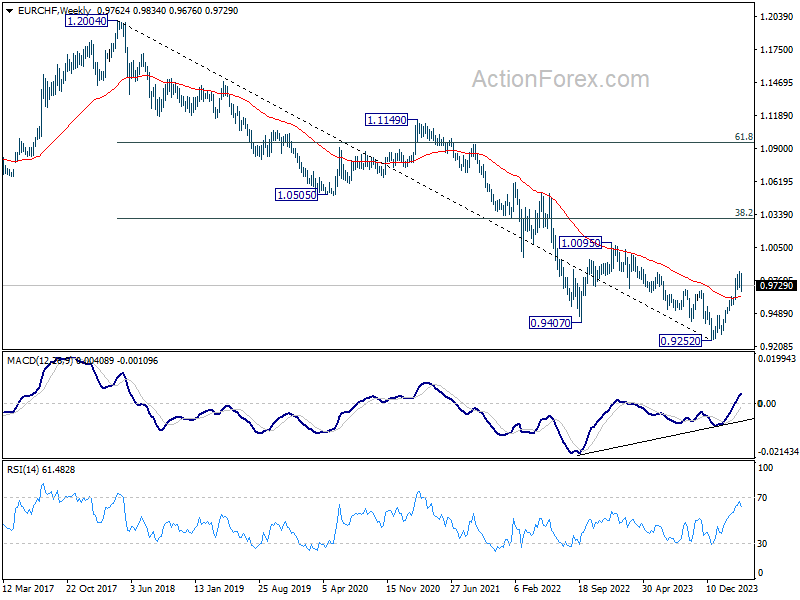

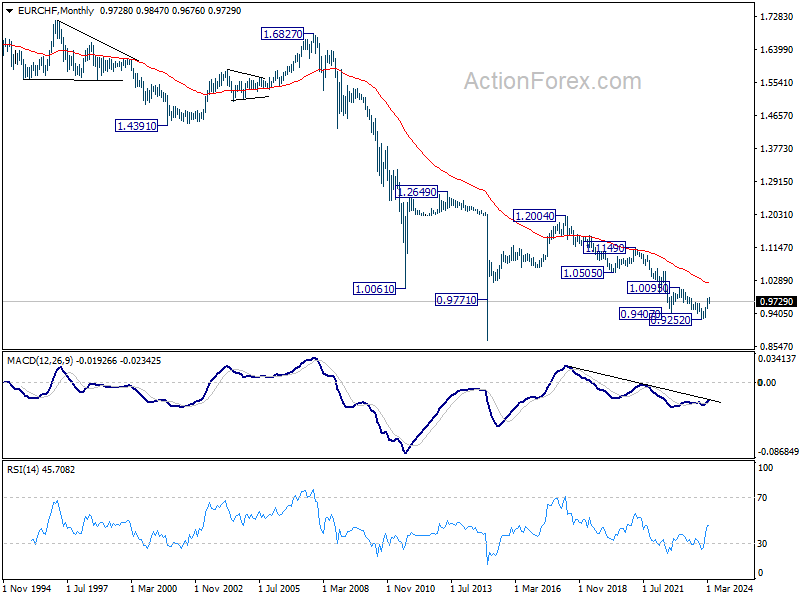

EUR/CHF Weekly Outlook

EUR/CHF's decline last week indicates short term topping at 0.9847, on bearish divergence condition in 4H MACD. Initial bias is mildly on the downside for 38.2% retracement of 0.9252 to 0.9847 at 0.9620. But strong support is expected from there to contain downside to bring rebound, and set the range for sideway trading. Nevertheless, for now, risk will stay on the downside as long as 0.9847 resistance holds, in case of recovery.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9633) holds.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 4/15 – 4/19

Monday, Apr 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Mar | 53 | |

| 23:50 | JPY | Machinery Orders M/M Feb | 0.80% | -1.70% |

| 06:30 | CHF | Producer and Import Prices M/M Mar | 0.20% | 0.10% |

| 06:30 | CHF | Producer and Import Prices Y/Y Mar | -2% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | 0.80% | -3.20% |

| 12:30 | CAD | Manufacturing Sales M/M Feb | 0.70% | 0.20% |

| 12:30 | CAD | Wholesale Sales M/M Feb | 0.80% | 0.10% |

| 12:30 | USD | Empire State Manufacturing Index Apr | -9 | -20.9 |

| 12:30 | USD | Retail Sales M/M Mar | 0.40% | 0.60% |

| 12:30 | USD | Retail Sales ex Autos M/M Mar | 0.50% | 0.30% |

| 14:00 | USD | Business Inventories Feb | 0.30% | 0.00% |

| 14:00 | USD | NAHB Housing Market Index Apr | 52 | 51 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Mar | |

| Forecast: | Previous: 53 | ||

| 23:50 | JPY | Machinery Orders M/M Feb | |

| Forecast: 0.80% | Previous: -1.70% | ||

| 06:30 | CHF | Producer and Import Prices M/M Mar | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Mar | |

| Forecast: | Previous: -2% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | |

| Forecast: 0.80% | Previous: -3.20% | ||

| 12:30 | CAD | Manufacturing Sales M/M Feb | |

| Forecast: 0.70% | Previous: 0.20% | ||

| 12:30 | CAD | Wholesale Sales M/M Feb | |

| Forecast: 0.80% | Previous: 0.10% | ||

| 12:30 | USD | Empire State Manufacturing Index Apr | |

| Forecast: -9 | Previous: -20.9 | ||

| 12:30 | USD | Retail Sales M/M Mar | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Mar | |

| Forecast: 0.50% | Previous: 0.30% | ||

| 14:00 | USD | Business Inventories Feb | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 14:00 | USD | NAHB Housing Market Index Apr | |

| Forecast: 52 | Previous: 51 | ||

Tuesday, Apr 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q1 | 5.00% | 5.20% |

| 02:00 | CNY | Retail Sales Y/Y Mar | 5.10% | 5.50% |

| 02:00 | CNY | Industrial Production Y/Y Mar | 6.00% | 7.00% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Mar | 4.30% | 4.20% |

| 06:00 | GBP | Claimant Count Change Mar | 17.2K | 16.8K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | 4.00% | 3.90% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Feb | 5.50% | 5.60% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Feb | 6.10% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Feb | 27.3B | 28.1B |

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | 35.1 | 31.7 |

| 09:00 | EUR | Germany ZEW Current Situation Apr | -80.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | 37.2 | 33.5 |

| 12:30 | CAD | CPI M/M Mar | 0.70% | 0.30% |

| 12:30 | CAD | CPI Y/Y Mar | 2.80% | |

| 12:30 | CAD | CPI Median Y/Y Mar | 3.00% | 3.10% |

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 3.20% | 3.20% |

| 12:30 | CAD | CPI Common Y/Y Mar | 3.10% | 3.10% |

| 12:30 | USD | Building Permits Mar | 1.51M | 1.52M |

| 12:30 | USD | Housing Starts Mar | 1.48M | 1.52M |

| 13:15 | USD | Industrial Production M/M Mar | 0.40% | 0.10% |

| 13:15 | USD | Capacity Utilization Mar | 78.50% | 78.30% |

| 22:45 | NZD | CPI Q/Q Q1 | 0.60% | 0.50% |

| 22:45 | NZD | CPI Y/Y Q1 | 4.70% | |

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.28T | -0.45T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q1 | |

| Forecast: 5.00% | Previous: 5.20% | ||

| 02:00 | CNY | Retail Sales Y/Y Mar | |

| Forecast: 5.10% | Previous: 5.50% | ||

| 02:00 | CNY | Industrial Production Y/Y Mar | |

| Forecast: 6.00% | Previous: 7.00% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Mar | |

| Forecast: 4.30% | Previous: 4.20% | ||

| 06:00 | GBP | Claimant Count Change Mar | |

| Forecast: 17.2K | Previous: 16.8K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | |

| Forecast: 4.00% | Previous: 3.90% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Feb | |

| Forecast: 5.50% | Previous: 5.60% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Feb | |

| Forecast: | Previous: 6.10% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Feb | |

| Forecast: 27.3B | Previous: 28.1B | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | |

| Forecast: 35.1 | Previous: 31.7 | ||

| 09:00 | EUR | Germany ZEW Current Situation Apr | |

| Forecast: | Previous: -80.5 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | |

| Forecast: 37.2 | Previous: 33.5 | ||

| 12:30 | CAD | CPI M/M Mar | |

| Forecast: 0.70% | Previous: 0.30% | ||

| 12:30 | CAD | CPI Y/Y Mar | |

| Forecast: | Previous: 2.80% | ||

| 12:30 | CAD | CPI Median Y/Y Mar | |

| Forecast: 3.00% | Previous: 3.10% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Mar | |

| Forecast: 3.20% | Previous: 3.20% | ||

| 12:30 | CAD | CPI Common Y/Y Mar | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 12:30 | USD | Building Permits Mar | |

| Forecast: 1.51M | Previous: 1.52M | ||

| 12:30 | USD | Housing Starts Mar | |

| Forecast: 1.48M | Previous: 1.52M | ||

| 13:15 | USD | Industrial Production M/M Mar | |

| Forecast: 0.40% | Previous: 0.10% | ||

| 13:15 | USD | Capacity Utilization Mar | |

| Forecast: 78.50% | Previous: 78.30% | ||

| 22:45 | NZD | CPI Q/Q Q1 | |

| Forecast: 0.60% | Previous: 0.50% | ||

| 22:45 | NZD | CPI Y/Y Q1 | |

| Forecast: | Previous: 4.70% | ||

| 23:50 | JPY | Trade Balance (JPY) Mar | |

| Forecast: -0.28T | Previous: -0.45T | ||

Wednesday, Apr 17, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Mar | 0.10% | |

| 06:00 | GBP | CPI M/M Mar | 0.60% | |

| 06:00 | GBP | CPI Y/Y Mar | 3.10% | 3.40% |

| 06:00 | GBP | CPI Core Y/Y Mar | 4.10% | 4.50% |

| 06:00 | GBP | RPI M/M Mar | 0.80% | |

| 06:00 | GBP | RPI Y/Y Mar | 4.50% | |

| 06:00 | GBP | PPI Input M/M Mar | 0.00% | -0.40% |

| 06:00 | GBP | PPI Input Y/Y Mar | -2.70% | |

| 06:00 | GBP | PPI Output M/M Mar | 0.20% | 0.30% |

| 06:00 | GBP | PPI Output Y/Y Mar | 0.40% | |

| 06:00 | GBP | PPI Core Output M/M Mar | 0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y Mar | 0.30% | |

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 2.90% | 2.90% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 2.40% | 2.40% |

| 14:30 | USD | Crude Oil Inventories | 5.8M | |

| 18:00 | USD | Fed's Beige Book |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Mar | |

| Forecast: | Previous: 0.10% | ||

| 06:00 | GBP | CPI M/M Mar | |

| Forecast: | Previous: 0.60% | ||

| 06:00 | GBP | CPI Y/Y Mar | |

| Forecast: 3.10% | Previous: 3.40% | ||

| 06:00 | GBP | CPI Core Y/Y Mar | |

| Forecast: 4.10% | Previous: 4.50% | ||

| 06:00 | GBP | RPI M/M Mar | |

| Forecast: | Previous: 0.80% | ||

| 06:00 | GBP | RPI Y/Y Mar | |

| Forecast: | Previous: 4.50% | ||

| 06:00 | GBP | PPI Input M/M Mar | |

| Forecast: 0.00% | Previous: -0.40% | ||

| 06:00 | GBP | PPI Input Y/Y Mar | |

| Forecast: | Previous: -2.70% | ||

| 06:00 | GBP | PPI Output M/M Mar | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 06:00 | GBP | PPI Output Y/Y Mar | |

| Forecast: | Previous: 0.40% | ||

| 06:00 | GBP | PPI Core Output M/M Mar | |

| Forecast: | Previous: 0.20% | ||

| 06:00 | GBP | PPI Core Output Y/Y Mar | |

| Forecast: | Previous: 0.30% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 5.8M | ||

| 18:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

Thursday, Apr 18, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | -6 | |

| 01:30 | AUD | Employment Change Mar | 7.2K | 116.5K |

| 01:30 | AUD | Unemployment Rate Mar | 3.90% | 3.70% |

| 01:30 | AUD | RBA Bulletin Q1 | ||

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 0.80% | 0.30% |

| 06:00 | CHF | Trade Balance (CHF) Mar | 3.22B | 3.66B |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 45.2B | 39.4B |

| 12:30 | USD | Initial Jobless Claims (Apr 12) | 214K | 211K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | 0.8 | 3.2 |

| 14:00 | USD | Existing Home Sales Mar | 4.20M | 4.38M |

| 14:30 | USD | Natural Gas Storage | 24B | |

| 23:30 | JPY | National CPI Y/Y Mar | 2.80% | |

| 23:30 | JPY | National CPI core Y/Y Mar | 2.70% | 2.80% |

| 23:30 | JPY | National CPI core-core Y/Y Mar | 3.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | |

| Forecast: | Previous: -6 | ||

| 01:30 | AUD | Employment Change Mar | |

| Forecast: 7.2K | Previous: 116.5K | ||

| 01:30 | AUD | Unemployment Rate Mar | |

| Forecast: 3.90% | Previous: 3.70% | ||

| 01:30 | AUD | RBA Bulletin Q1 | |

| Forecast: | Previous: | ||

| 04:30 | JPY | Tertiary Industry Index M/M Feb | |

| Forecast: 0.80% | Previous: 0.30% | ||

| 06:00 | CHF | Trade Balance (CHF) Mar | |

| Forecast: 3.22B | Previous: 3.66B | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | |

| Forecast: 45.2B | Previous: 39.4B | ||

| 12:30 | USD | Initial Jobless Claims (Apr 12) | |

| Forecast: 214K | Previous: 211K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | |

| Forecast: 0.8 | Previous: 3.2 | ||

| 14:00 | USD | Existing Home Sales Mar | |

| Forecast: 4.20M | Previous: 4.38M | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 24B | ||

| 23:30 | JPY | National CPI Y/Y Mar | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | National CPI core Y/Y Mar | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 23:30 | JPY | National CPI core-core Y/Y Mar | |

| Forecast: | Previous: 3.20% | ||

Friday, Apr 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Mar | 0.30% | 0.00% |

| 06:00 | EUR | Germany PPI M/M Mar | 0.00% | -0.40% |

| 06:00 | EUR | Germany PPI Y/Y Mar | -4.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Mar | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 06:00 | EUR | Germany PPI M/M Mar | |

| Forecast: 0.00% | Previous: -0.40% | ||

| 06:00 | EUR | Germany PPI Y/Y Mar | |

| Forecast: | Previous: -4.10% | ||

The Weekly Bottom Line: One Hundred Days into 2024, Rate Cuts Remain on the Horizon

U.S. Highlights

- Inflation, as measured by the Consumer Price Index, accelerated to 3.5% year-on-year in March – the highest reading in six months.

- Minutes from the Federal Reserve meeting in March showed that officials remained in favor of exercising patience amid persistent inflationary pressures.

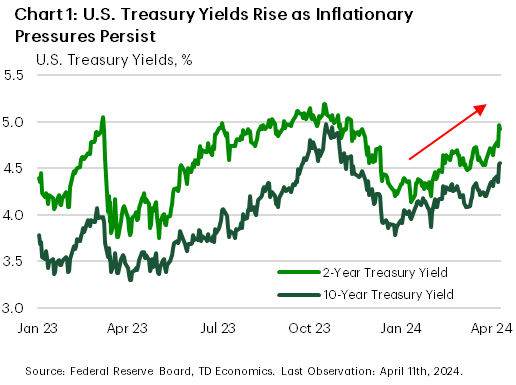

- U.S. Treasury yields spiked roughly 15 basis-points as market expectations for lower interest rates were pushed back into the second half of the year.

Canadian Highlights

- The Bank of Canada held its policy rate at 5%, while comments from Governor Macklem indicated that a rate cut is “within the realm of possibilities” at the June meeting.

- Canadian Government bond yields moved higher in tandem with U.S. Treasuries. This may slow the Canadian housing market, reducing the extent of relief from expected rate cuts.

- The Federal government’s housing plan will increase the Home Buyers Plan withdrawal limit and extend amortization for some borrowers but will likely have a limited impact on the housing market.

U.S. – One Hundred Days into 2024, Rate Cuts Remain on the Horizon

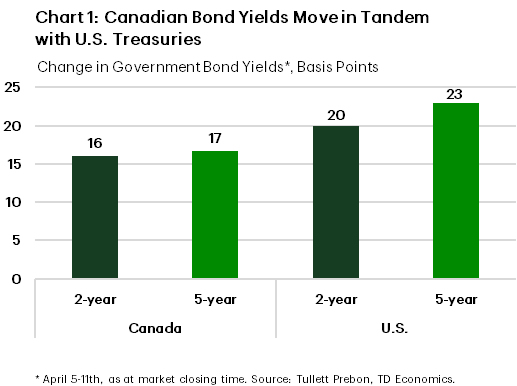

Financial markets were caught off-guard this week as slightly hotter than expected inflation data prompted a spike in U.S. Treasury yields and a modest retreat in equity prices. As of the time of writing, the ten- and two-year Treasury yields finished the week up roughly 15 basis-points (Chart 1), while the S&P 500 fell 0.9%. While the deviation relative to expectations for the March Consumer Price Index (CPI) inflation was marginal, the underlying details proved to be more concerning.

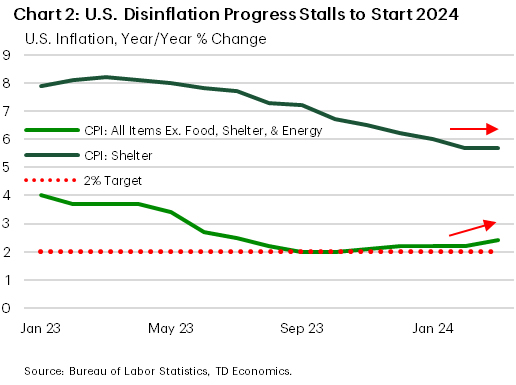

Headline inflation in March jumped to 3.5% year-on-year, with energy prices seeing positive price growth in annual terms for the first time in over a year. Excluding energy and food prices, core inflation remained unchanged relative to February at 3.8%. The reason why the disinflation process stalled in the first quarter is related to two factors. The first is that disinflation in the heavily weighted shelter subcategory moderated relative to the previous quarter. While this offered less support to the Fed’s mission to reattain price stability, the measurement of shelter prices is lagged relative to market trends by several months, and thus the direction of shelter inflation is still expected to be downward moving forward.

The second factor keeping inflation elevated was the acceleration in price growth for categories excluding food, energy, and shelter – aggregately referred to as supercore inflation. Inflation pressures within this subcategory were broad-based in the first quarter (Chart 2) which has not gone unnoticed by the Federal Reserve. In the March meeting minutes released this week, FOMC participants noted they were reluctant to discount the inflation data of the first quarter and emphasized that they would require greater confidence that inflation was on a sustainable trajectory back to the 2% target before considering less restrictive policy options.

This lined up with the even-toned statements made by Federal Reserve officials this week, including Vice Chair and New York Fed President John Williams who stated that he expects “inflation to continue its gradual return to 2 percent, although there will likely be bumps along the way, as we’ve seen in some recent inflation readings”. In a speech this week, Boston Fed President Susan Collins also stated “Overall, the recent data have not materially changed my outlook, but they do highlight uncertainties related to timing, and the need for patience”. Market pricing for the first Federal Reserve cut this year shifted from June to July this week, although market confidence remains weak with the balance of risks skewed towards the potential for a later commencement date.

Looking to next week, we receive an update on retail sales for March on Monday, which are expected to show slower growth relative to the prior month, in part owing to a moderation in auto sales. Next week also marks the start of the Spring IMF meetings, which will include meetings between the Fed and the U.S. Treasury and their international counterparts, in addition to the publication of the IMF’s updated World Economic Outlook.

Canada – A Week of Celestial Events

Two events garnered widespread attention in Canada this week: the solar eclipse and the Bank of Canada’s (BoC) monetary policy meeting. Both have implications for the economy – the former by boosting demand for astro-tourism, the latter by capping demand for almost everything else. As widely anticipated, the Bank held its policy rate at 5%, while comments from Governor Macklem indicated that a rate cut is “within the realm of possibilities” at the June meeting. This had no major impact on the market expectations, where a full rate cut remains priced for the July meeting.

Several takeaways emerged from the Monetary Policy Report – a fresh set of forecasts, accompanying the BoC’s announcement. Namely, the near-term GDP forecast was upgraded reflecting higher population growth and some recovery in consumer spending. Despite the upgrade to the growth outlook, the BoC marked down its inflation forecast by two tenths of a percentage point and now expects its measure of core inflation to reach 2.2% by year-end. In his speech following the announcement, Governor Macklem maintained a cautious tone, stating he would rather err on the side of over-tightening policy to avoid any setbacks in lowering inflation.

Another ‘celestial’ announcement was a 25-basis point (bp) increase in the estimated neutral rate – the policy rate consistent with the economy operating at its full capacity with stable inflation. The Bank justified this increase by citing a higher global neutral rate (using the U.S. as a proxy) and “key Canadian domestic factors” like growth in total hours worked and a younger population of savers. Simply put, the Bank signaled the end point of its upcoming easing cycle will likely be a bit higher than previously thought.

While hard to quantify, an increase in neutral rate likely had only a marginal effect on long-term rates this week. A stronger gravitational pull was exerted by the sharp rise in U.S. Treasury yields following another higher-than-expected inflation reading which resulted in one of the largest weekly moves in yields over the past two years (Chart 1).

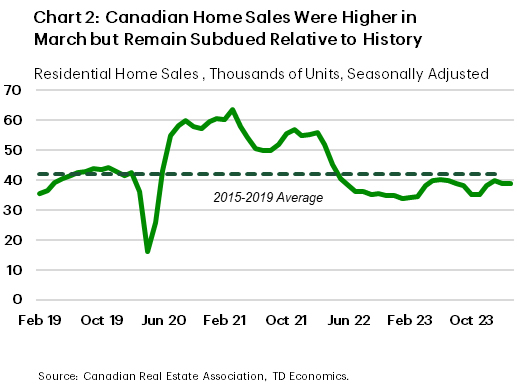

This backup in yields casts a shadow over the Canadian housing market. On the one hand, existing home sales for March were up 0.5% on the month, and, according to CREA, new listings for April are tracking stronger, which could support higher sales activity this month. On the other hand, sales remain below their historical average while higher bond yields will exert additional pressure on affordability, signaling a period of slower activity in the months ahead (Chart 2).

From that perspective, today’s release of the government’s housing plan is timely. Based on Chrystia Freeland’s speech, the government will be increasing the Home Buyers Plan withdrawal limit from $35k to $60k and lifting amortization for insured mortgages from 25 to 30 years for newly built homes and first-time buyers. Our initial assessment suggests that these measures will have a limited impact on the housing market but stay tuned for our comprehensive analysis of the Federal Government Budget next week.

Weekly Economic & Financial Commentary: No, No, After You

Summary

United States: Are We There Yet?

- The March consumer price data dominated the economic discussion this week and are the latest to support that the timing and degree of Fed easing will be later and smaller than many of us previously expected. We're not yet there. We now expect the FOMC won't begin to ease policy until its Sept. 18 meeting.

- Next week: Retail Sales (Mon.), Industrial Production (Tue.), Existing Home Sales (Thu.)

International: Major Central Banks Readying Markets for Rate Cuts

- The European Central Bank (ECB) held monetary policy steady this week, though we view the accompanying statement as laying the groundwork for easing in June. We expect the ECB to deliver an initial 25 bps rate cut at its June meeting. The Bank of Canada (BoC) also held steady and said “we are seeing what we need to see” to lower policy interest rates, but that “we need to see it for longer.” We also lean toward an initial 25 bps policy rate cut from the BoC at its June meeting.

- Next week: China GDP (Tue.), Canada CPI (Tue.), U.K. CPI (Wed.)

Interest Rate Watch: No, No, After You

- The not-quite synchronized actions of the world's central banks came into better focus this week. We explore how that is impacting the rates market in the United States and abroad, particularly as expectations shift in the foreign exchange market.

Credit Market Insights: Consumer Fear of Delinquency on the Rise

- Earlier this week, the New York Fed released its Survey of Consumer Expectations for March. While inflation expectations were largely stable, cracks in household financial well-being were evident in consumers’ responses.

Topic of the Week: Biden Unveils New Plan to Cancel Student Debt

- The Biden administration moved this week to propose new student loan debt relief that would affect millions of Americans. The new proposal would cancel up to $20,000 in debt for borrowers whose balances have grown as a result of unpaid interest. Overall, the macroeconomic impact looks to be muted for the policy, even if the impact could be significant for affected households.

Canadian Inflation to Tick Higher as BoC Considers Rate Cuts

The Bank of Canada will be focused on the March Canadian consumer price index report next Tuesday after another upward surprise in U.S. price growth created doubt about the U.S. Federal Reserve’s rate-cutting plans this year.

Slower price growth in Canada in recent months and a sharply underperforming Canadian economy have “increased confidence” among BoC policymakers that inflation will continue to slow. But the central bank wants to see more evidence before shifting to interest rate cuts.

We expect year-over-year price growth in March to tick higher to 3% from 2.8% in February largely due to higher gasoline prices pushing energy costs further above year-ago levels. Food price growth should be little changed—still above 3% but slower than the 10% plus peak increases in late 2022.

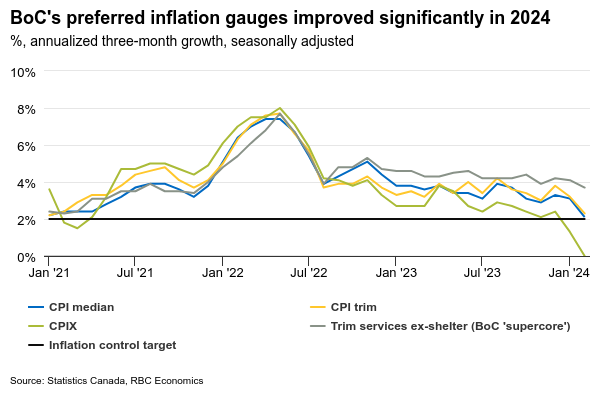

The CPI data is often volatile and clothing prices, in particular, could rebound in the spring after milder-than-usual temperatures slowed demand and prices over the winter. The BoC will be more focused on its preferred list of core measures—which are designed to look through volatility in any one subcomponent—for signs that broader inflation pressures continue to ease. We look for growth in the BoC’s preferred trim and median measures to hold close to the February pace both on a year-over-year and three-month rolling average basis. The latter slowed to a 2.2% average annualized rate in February.

Week ahead data watch

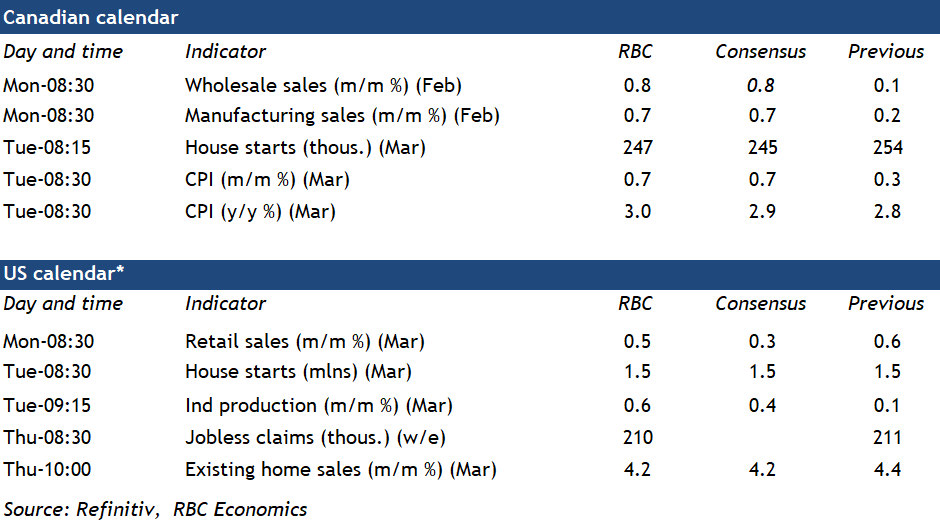

We expect Canadian manufacturing sales to tick up 0.7% in February in line with Statistics Canada’s advance indicator. Much of that growth was driven by higher sales in the petroleum and coal subsector. Sales volumes likely dipped given the industrial product price index edged up 0.7% in February.

StatCan’s early estimate of “core” wholesale sales increased by 0.8% in February with sales in machinery, equipment and supplies, motor vehicles and parts and accessories and building material and supplies subsectors going up during that month.

March housing starts likely stood at 247,000, given that building permits grew at a slower pace (8%) in February, down from 13% in January.

U.S. retail sales likely ticked up 0.5% in March, following 0.6% growth in February led by price-related sales increase at gas stations. But auto sales dipped during that month, partially offsetting some of the growth.

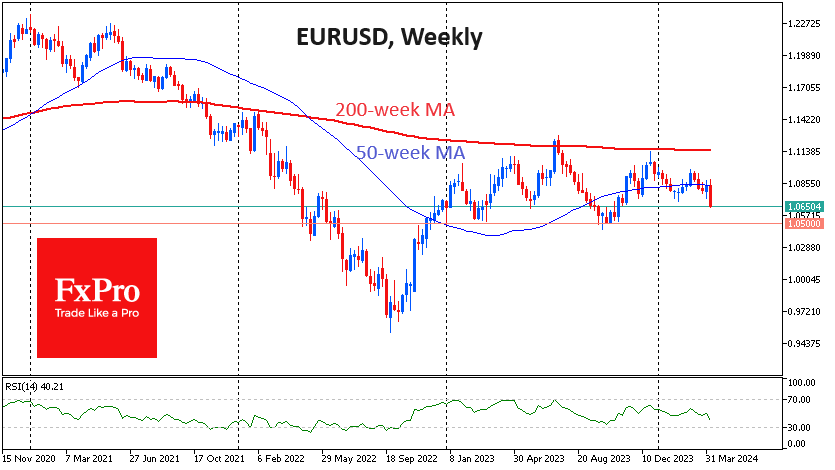

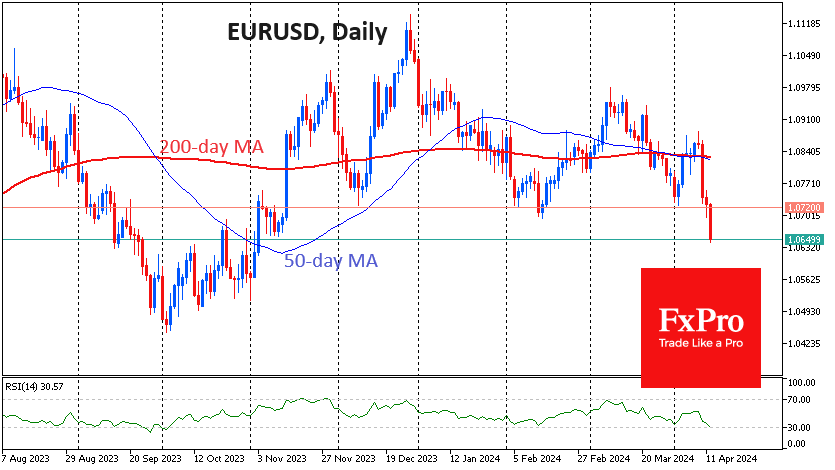

EURUSD Has Bucked the Trend, Threatening to Fall Below Parity

EURUSD is losing 1.9% from Wednesday’s peak to a five-month low at 1.0650. US inflation data and ECB comments highlight the divergence of Fed and ECB monetary policy.

Wednesday’s US inflation report appears to have set the trend for the dollar, taking it out of a more than four-month wander around its 200-day moving average. And the biggest contributor to this pullback is the EURUSD dynamics.

The pressure on the key currency market pair comes from several directions at once. On the US side, markets have continued to receive pro-inflationary data since the beginning of the month: acceleration in manufacturing activity, strong new job growth, and stronger CPI acceleration than expected. This data continued to push back the date of the expected Fed’s rate cut and the number of these moves.

On the European side, by contrast, data releases and comments from ECB officials are supporting the sentiment for the first cut in June. And this is a divergence that markets can no longer ignore.

The EURUSD dynamics during this week emphasise the serious bearish bias in the pair. The pair crossed the 50- and 200-day moving averages in a sharp move on Wednesday and closed well below them. Neither on Thursday nor on Friday did the Euro make any noticeable attempts to rebound.

Moreover, we don’t even see the typical Friday thrust of short-term profit-taking with an ongoing sell-off. EURUSD slid to 1.0650, having fallen out of its trading range since late December.

EURUSD has been receiving support on dips towards 1.05 in 2023, spending only a few days below that level. The pair will likely test the strength of this support again very soon, and the accumulating difference in Fed and ECB policy reinforces the chances that the pair will not stop there this time.

If indeed EURUSD falls below 1.05 in April, the pair could fall to the next leg, finding support only near 0.95.