Sample Category Title

Markets Will Keep a Close Eye on Developments in Middle East

Markets

Markets on Friday were captured by a risk-off correction as headlines/rumours suggested an upcoming, direct strike of Iran against Israel. Especially US equities were hit, closing up to 1.62% lower (Nasdaq). For once, bonds also played their role as safe haven going into an uncertain weekend, reversing some short positioning that occurred after stickier than expected US March CPI data early last week. US yields declined between 4.9 bps (30-y) and 7.3 bps (5-y). The consumer confidence report from the University of Michigan painted a mixed picture with the headline sentiment index easing slightly from 79.4 to 77.9. At the same time, both the 1-year ahead (3.1% from 2.9%) and LT inflation expectations in the survey (3.0% from 2.8%) only confirmed the narrative of stubbornly high inflation expectations. Several Fed governors including Susan Collins, Mary Daly, Raphael Bostic and Jeffrey Schmid in one way or another reiterated that the Fed has every reason to stay cautious as long as activity remains strong while at the same time the Fed doesn’t get the additional confidence needed to comfortably start an easing cycle. Bunds outperformed Treasuries after the ECB on Thursday signaled it likely will start cutting rates in June. German yields declined between 11 bps (5-y) and 8.0 bps (30-y). The combination of an ever more obvious policy divergence between the Fed and the likes of the ECB, together with a risk-off sentiment catapulted the dollar. EUR/USD easily dropped below the 1.0695 YTD low to close at 1.0643. Cable slipped below the 1.25 barrier/range bottom (close 1.2452). USD/JPY set a new multi-year top (close 153.23).

Investors this morning try to assess the fall-out from the attack of Iran against Israel. Asian equities mostly trade in red (e.g. Nikkei -0.85%), but declines remain orderly. Markets apparently consider a scenario where any reaction from Israel won’t cause a major escalation. The oil price even eases slightly with Brent returning near $90 p/b. Bonds show little additional safe haven demand with US yields rising 2-3 bps. The dollar maintains most of Friday’s gains (EUR/USD 1.0655, DXY 105.96). The yen underperforms with USD/JPY breaking higher to currently trade near 153.8.

Later today, markets evidently will keep a close eye on the developments in the Middle East. This might lead to a more cautious sentiment on risk. However, it’s far from sure that a less positive sentiment will automatically translate into lower bond yields. Higher commodity prices and potential supply disruptions (shipping) don’t help the disinflationary process. Regarding the data, we look out for US retail sales and the Empire manufacturing survey. The latter is expected to improve from -20.9 to -5.0. Retail sales still are expected to grow a solid 0.4% M/M. Strong US activity/demand data only will reinforce the idea that there is no reason for the Fed to rush to rate cuts anytime soon. On FX markets, the dollar end last week succeeded a technically significant break. The EUR/USD decline below 1.0695 opens the way for the pair to return to the 2023 low at 1.0448.

News & Views

Fitch on Friday warned that recent fiscal slippage adds to uncertainty over Hungary’s ability to keep debt to GDP on a gradual downward path. Last year’s government deficit of 6.7% was well above the original target of 3.9% and October’s revised target of 5.2%. This year’s running deficit at HUF 2.3tn at the end of Q1 is already 58% of the 2024 annual target, largely due to higher spending. The 2024 goal post was already moved from 2.9% to 4.5%, a target Fitch considers challenging still given the weak growth prospects, high interest costs and social spending. The rating agency believes Hungary will be placed under the EU’s excessive debt procedure this year as a result. Fitch’s baseline scenario sees public debt rising to 73.9% this year before easing back to 72.5% in 2025.

China kept the rates on the seven-day reverse repo and one-year medium term lending facility unchanged this morning. The latter stands at 2.5% and serves as a guide to the commercial banks’ loan prime rates (LPRs). While the Chinese economy and inflation (a mere 0.1% y/y in March) could use some monetary support, the central bank is walking a tightrope, keeping one eye at the weak yuan as well. With the Fed unlikely to cut rates anytime soon, lowering rates in China would increase pressure on an already weak yuan. USD/CNY has been trending higher all year and Chinese authorities have recently given up defending the 7.20 figure. The pair is currently hovering north towards 7.24 in a gradual manner authorities seem to be comfortable with.

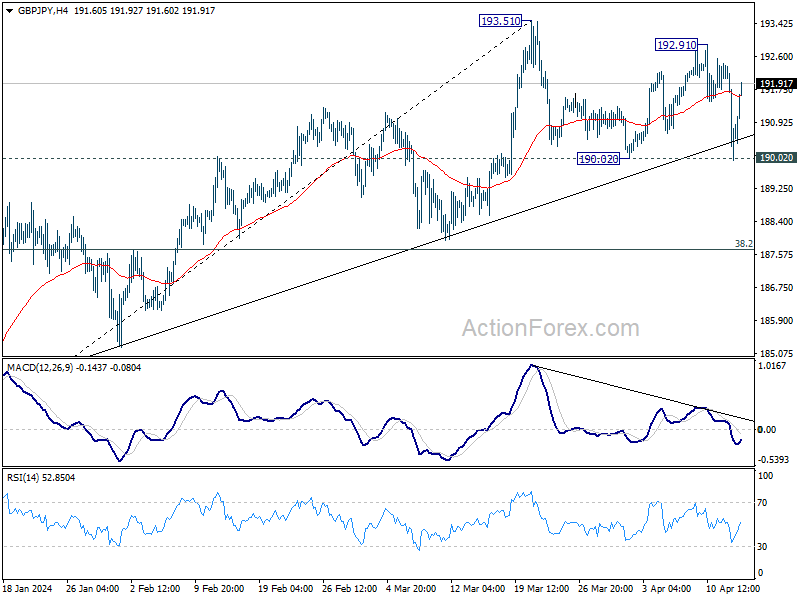

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.67; (P) 191.07; (R1) 192.15; More..

Intraday bias in GBP/JPY remains neutral for the moment. On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. Nevertheless, decisive break of 190.02 will indicate that it's at least correcting the rise from 178.32, and target 38.2% retracement of 178.32 to 193.51 at 187.70.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

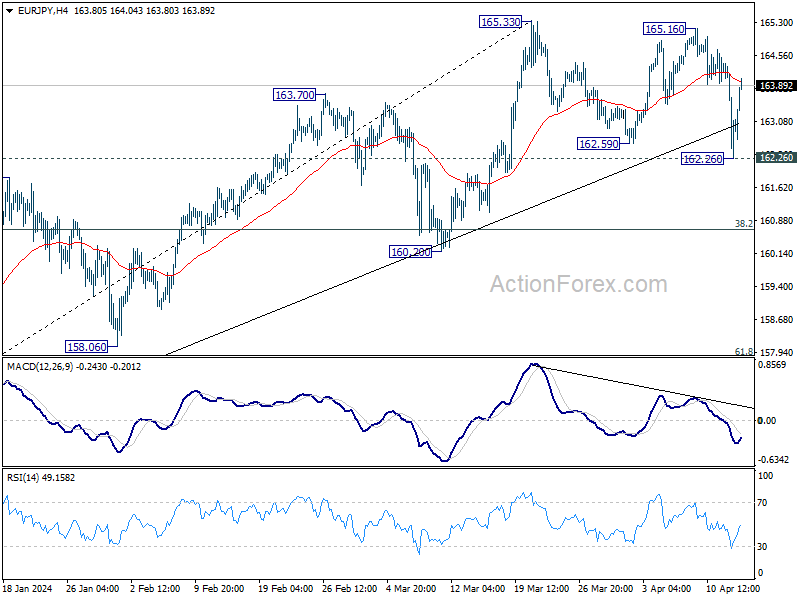

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.08; (P) 163.31; (R1) 164.36; More...

Intraday bias in EUR/JPY remains neutral first. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. However, decisive break of 162.26 support will argue that it's at least correcting the rise from 153.15, and target 38.2% retracement of 153.15 to 165.33 at 160.67.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

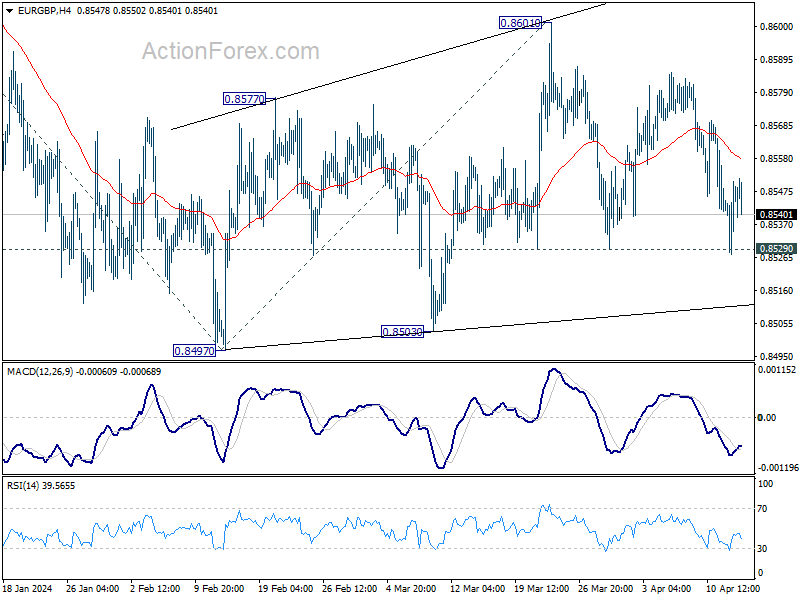

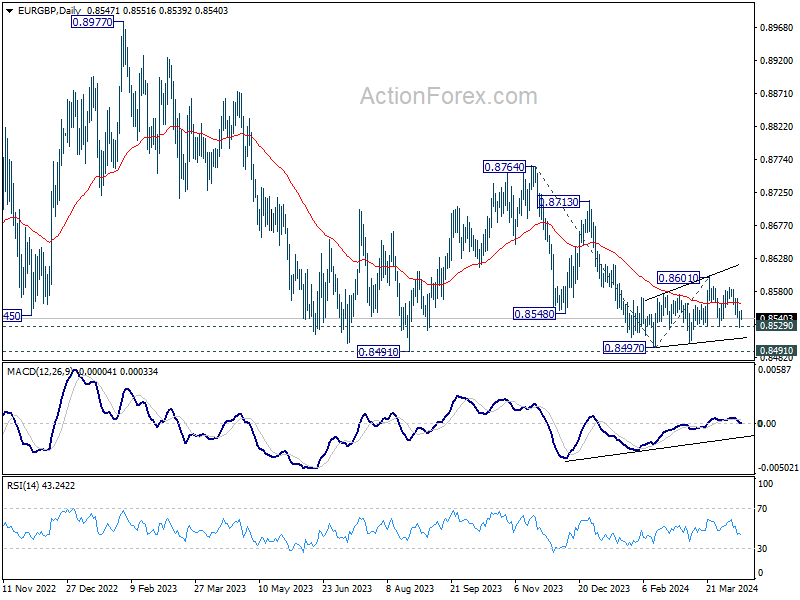

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8533; (P) 0.8542; (R1) 0.8557; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8601 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

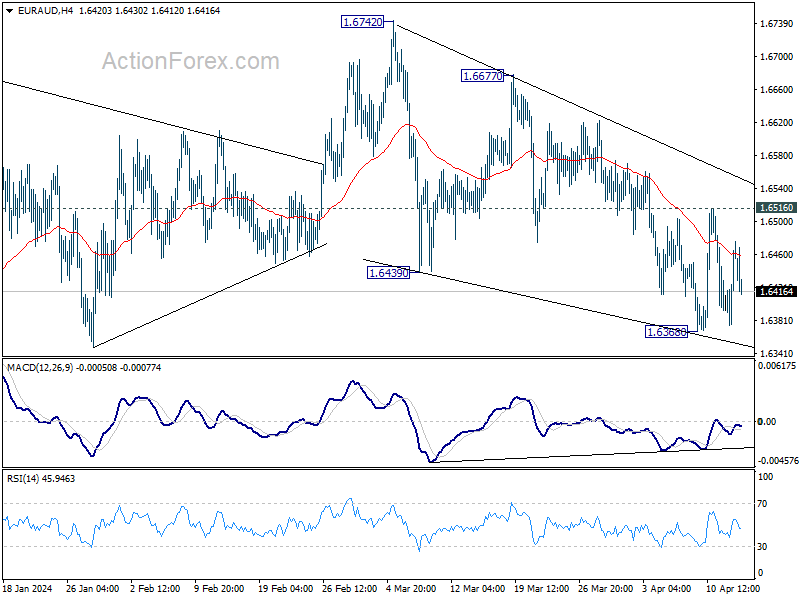

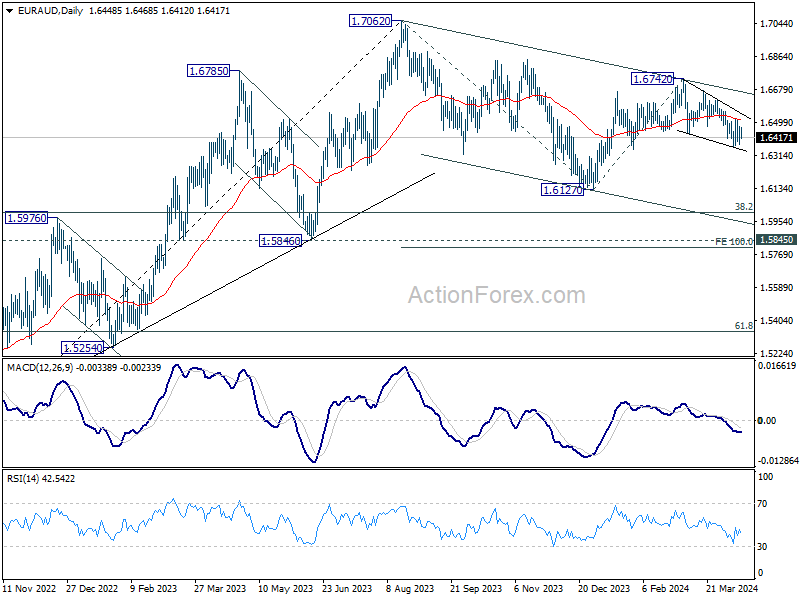

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6403; (P) 1.6442; (R1) 1.6505; More...

Intraday bias in EUR/AUD remains neutral for the moment. Risk will stay on the downside as long as 1.6516 resistance holds. On the downside, below 1.6368 will resume the fall from 1.6742 towards 1.6127 low. Nevertheless, break of 1.6516 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). The correction is probably still in progress with fall from 1.6742 as the third leg. Strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

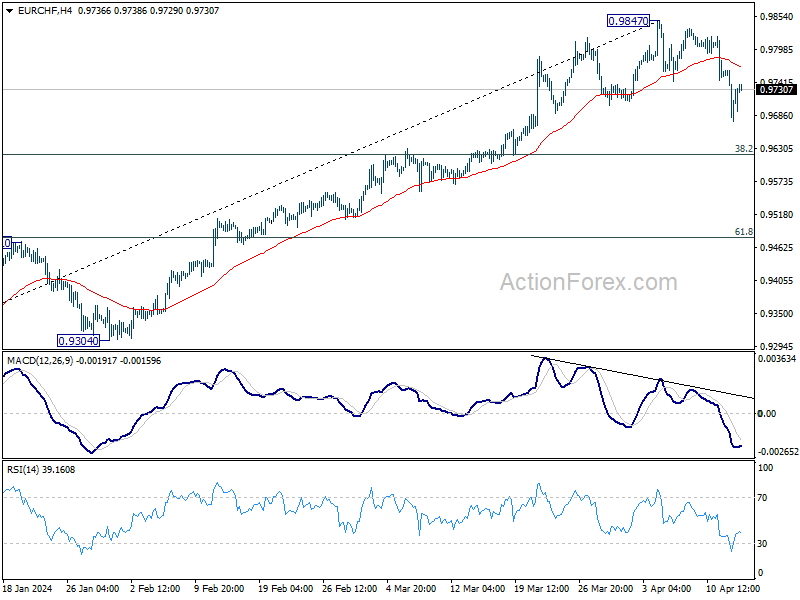

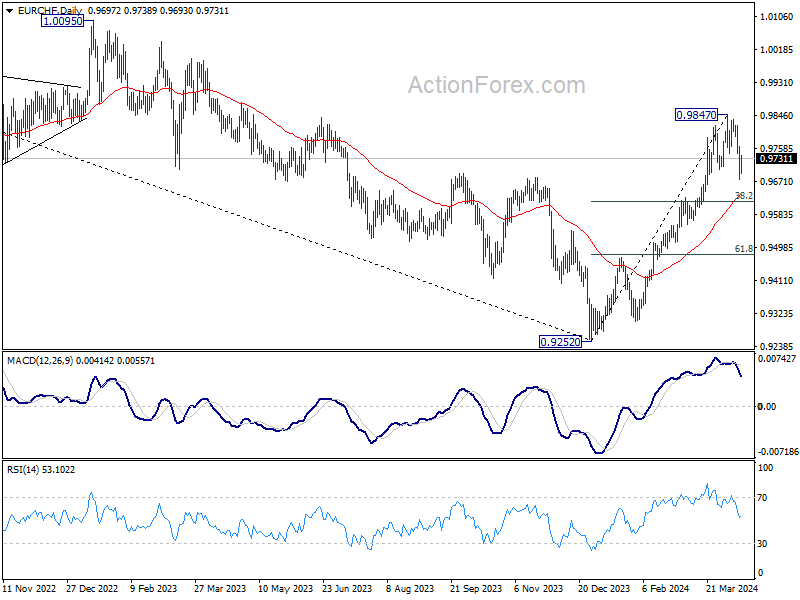

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9684; (P) 0.9724; (R1) 0.9770; More...

Intraday bias in EUR/CHF remains mildly on the downside for 38.2% retracement of 0.9252 to 0.9847 at 0.9620. But strong support is expected from there to contain downside to bring rebound, and set the range for the consolidation pattern from 0.9847. Nevertheless, for now, risk will stay on the downside as long as 0.9847 resistance holds, in case of recovery.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9633) holds.

Iranian Drone Strike on Israel Escalates Middle East Tensions

In focus today

The key focus today will be the escalation of the Middle Eastern conflict following the Iranian strike on Israel and signals on the extent of Israeli retaliation, see more below.

In the euro area, we receive industrial production data for February. The industry has been weak the past years, but we are currently receiving tentative signs of a bottoming out of activity. German industrial production rose 2.1% in February, so we could be in for a decent monthly increase in the euro area today.

In the US, focus will be on March retail sales. Control group sales are likely to recover after weak prints in January and February. Unusually low seasonal adjustment factor weighed on sales growth at the start of the year, but the effect will fade from March. Besides technicalities, higher oil prices, recent upticks in immigration and the early timing of Easter may have all lifted sales towards spring.

In Sweden, the government presents its Spring Fiscal Policy Bill and amending budget bill for the current budget year. As the government already announced that the additional reforms will amount to only SEK 16.8bn it is fair to say that they maintain their restrictive fiscal policy. The number of additional reforms can be set into comparison of a SEK 33bn better than expected central government budget outcome of the last two months, or the fact that it amounts to only roughly 0.3% of the current Swedish GDP.

Overnight China will release GDP for Q1 on top of the monthly data dump across sectors. GDP is expected to rise 4.9% y/y in Q1 down from 5.2% y/y in Q4. However, it reflects a tough comparison with the high Q1 level last year after the covid reopening. On a q/q basis we look for around 1.5% growth corresponding to 6% annualised growth. Focus will also be on the data on retail sales and home sales. Consumers may hold back a bit on spending now after signals from the government that a trade-in scheme is coming, where people can trade in old durable goods and get a discount on new goods. Home sales and housing prices will provide key information on the state of the housing crisis.

Later in the week, focus will be on German ZEW data for April (Tuesday), final euro area inflation for March (Wednesday), and nation-wide March CPI from Japan (early Friday).

Economic and market news

What happened over the weekend

Tensions in the Middle East escalated as Iran attacked Israel with drones and missiles Saturday night, in retaliation for the alleged Israeli killing of military personnel at the Syrian embassy of Iran earlier this month. Damage was modest as the IDF reported to have shot down most of the weaponry. The attack was to some extent anticipated as Iran had vowed to retaliate, but both the US and several regional powers had urged restraint. The market reaction has so far been somewhat muted as markets weigh the probability of further escalation, though gold was slightly up this morning and oil slightly down. Iran says it considers 'the matter concluded' but could use greater force if Israel responds in kind while the Israeli war cabinet said on Sunday it was 'unclear when and how big' the response should be, FT reports. The US has urged Israel to show restraint. Iran has previously threatened it could close the Strait of Hormuz, through which 20% of the volume of the world's oil consumption passes through as well as a significant share of gas.

China kept a key policy rate unchanged, even after Chinese credit data surprised to the soft side on Friday suggesting China is still 'muddling through' with no bust but no strong recovery either. Despite this, the MLF rate remained unchanged on Monday as there has been pressure on the Chinese currency lately due to expectations of higher US rates for longer. Going forward, we think the PBOC stays put for a while and waits for clearer signals that the Fed is cutting as it gives them more space to lower rates without adding depreciation pressure on the currency.

In an effort to reduce Russian metals' production revenue, the US and UK expanded sanctions by banning aluminium, copper and nickel produced by Russia from being imported to the two countries, as well as banning metal exchanges (LME and CME) from accepting new contracts trading Russian-produced metals.

What happened Friday

EUR/USD continued to decline during the day as the ECB has indicated rate cuts are near while recent upside US macro surprises have lowered market expectations of rate cuts from the Fed, the latest example of this being the University of Michigan consumer sentiment showing both 1Y and 5Y inflation expectations have risen with the former showing 3.1% (+0.2).

Swedish inflation surprised to the downside with the CPIF printing at 2.2% y/y (cons: 2.6%) and core at 2.9% (cons: 3.2%) which gave further merit to a May rate cut from the Riksbank, for which markets are currently pricing 20bp. The SEK was initially weaker, then erased some losses but closed weaker with EUR/SEK up 0.68%.

Equities: Global equities were lower on Friday and lower for the week, dragged down by the US. Despite the leg lower in equities cyclicals still outperformed last week, which shows how equity investors are more nervous for overheating than recession. On Friday we saw big banks in the US massively underperforming led by JPM as their earnings and not least guidance failed to impress. In the US on Friday Dow -1.2%, S&P 500 -1.5%, Nasdaq -1.6% and Russell 2000 -1.9%. Asian markets are mostly lower this morning following Friday session on Wall Street. US and European futures are higher which might be slightly surprising for some given the Iranian attack on Israel.

FI: There was a solid decline in primary European government bond yields on Friday, where the Bund rallied some 10bp and US 10Y Treasuries rallied 6bp after the negative sentiment had dominated the bond market after the higher-than-expected US CPI-data released earlier last week. Initially, the decline in the was bigger, but at the end of the day there was a minor rebound in bond yields. If we look at the 10Y BTPS-Bund spread the spread has widened since mid-March but has now stabilised around 130bp. Furthermore, the Bund ASW-spread has also stabilised and is now trading above 30bp.

FX: The Iranian attack on Israel and raised tensions in the Middle East have weighed on Asian equities and the JPY. Muted response in oil so far with Brent at just above USD 90/bbl. EUR/USD tumbled more than 2% last week following the US CPI and the ECB news but is stable around 1.065 this morning. EUR/SEK starts the week around 11.56 and EUR/NOK 11.58, both with their eyes on the next leg for risk sentiment and oil.

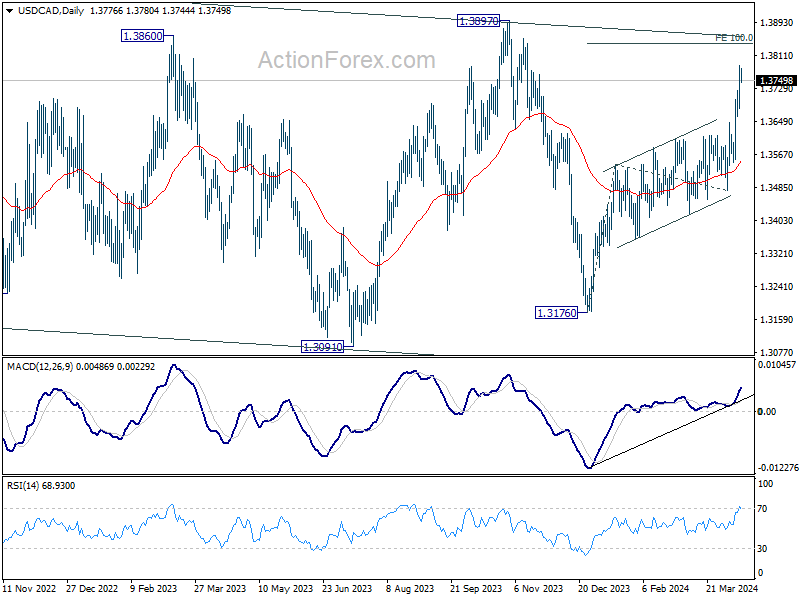

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3708; (P) 1.3748; (R1) 1.3813; More...

Intraday bias in USD/CAD remain son the upside at this point. Current rise from 1.3176 should target 100% projection of 1.3176 to 1.3540 from 1.3477 at 1.3841. On the downside, below 1.3724 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

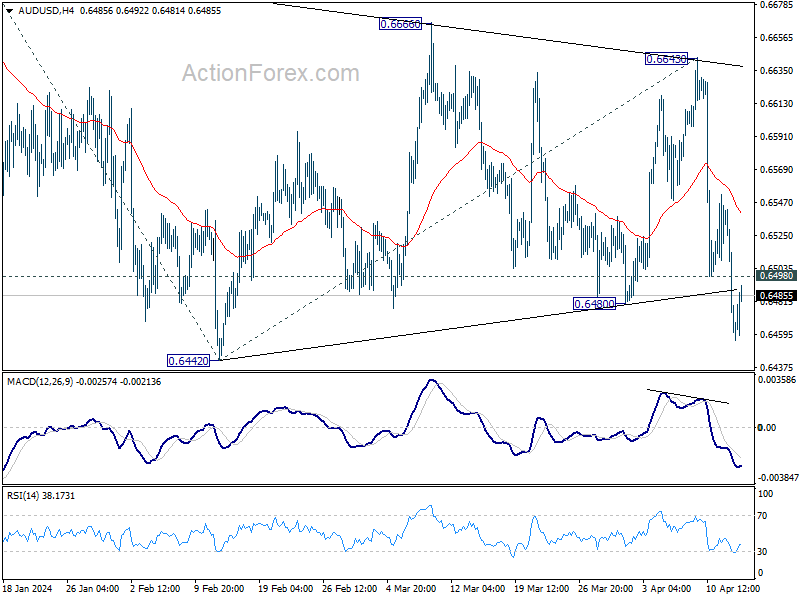

AUD/USD Daily Report

Daily Pivots: (S1) 0.6430; (P) 0.6488; (R1) 0.6520; More...

Intraday bias in AUD/USD remains on the downside for 0.6442 support. Decisive break there confirm resumption of the fall from 0.6870 and target 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378. On the upside, above 0.6498 resistance will turn intraday bias and bring consolidations. But risk will stay mildly on the downside as long as 0.6643 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

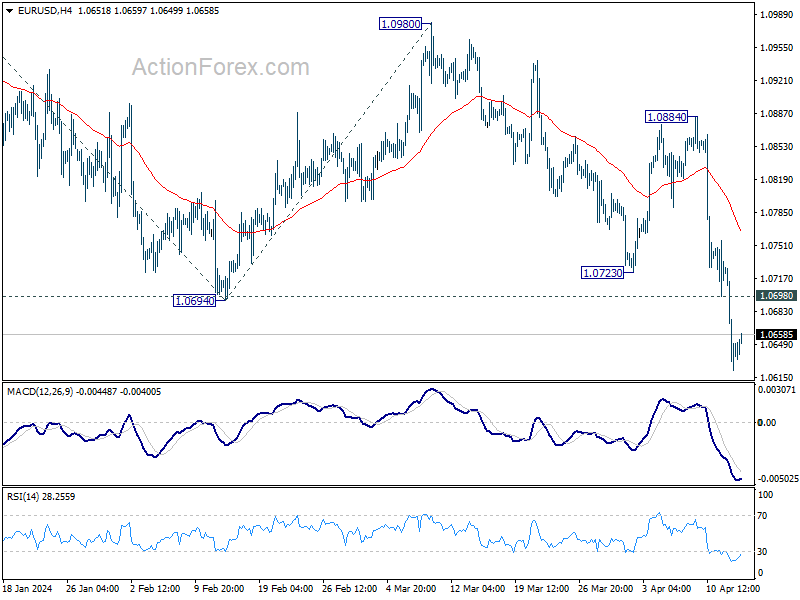

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0599; (P) 1.0665; (R1) 1.0708; More...

Intraday bias in EUR/USD remains on the downside at this point. Current is part of the decline from 1.1138. Next target is 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. On the upside, above 1.0723 support turned resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.