Sample Category Title

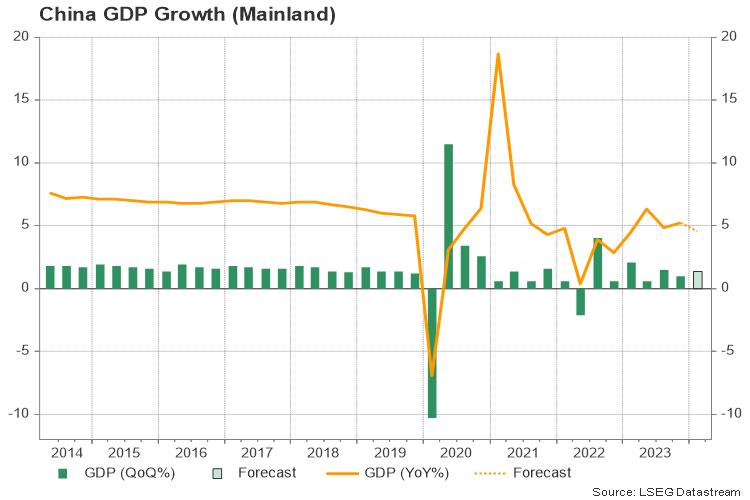

China’s Q1 GDP Growth Next on Asian Calendar

- China’s Q1 GDP expected to fall below 5.0% on Tuesday at 02:00 GMT

- Expansion to remain solid but unlikely to quell stimulus calls

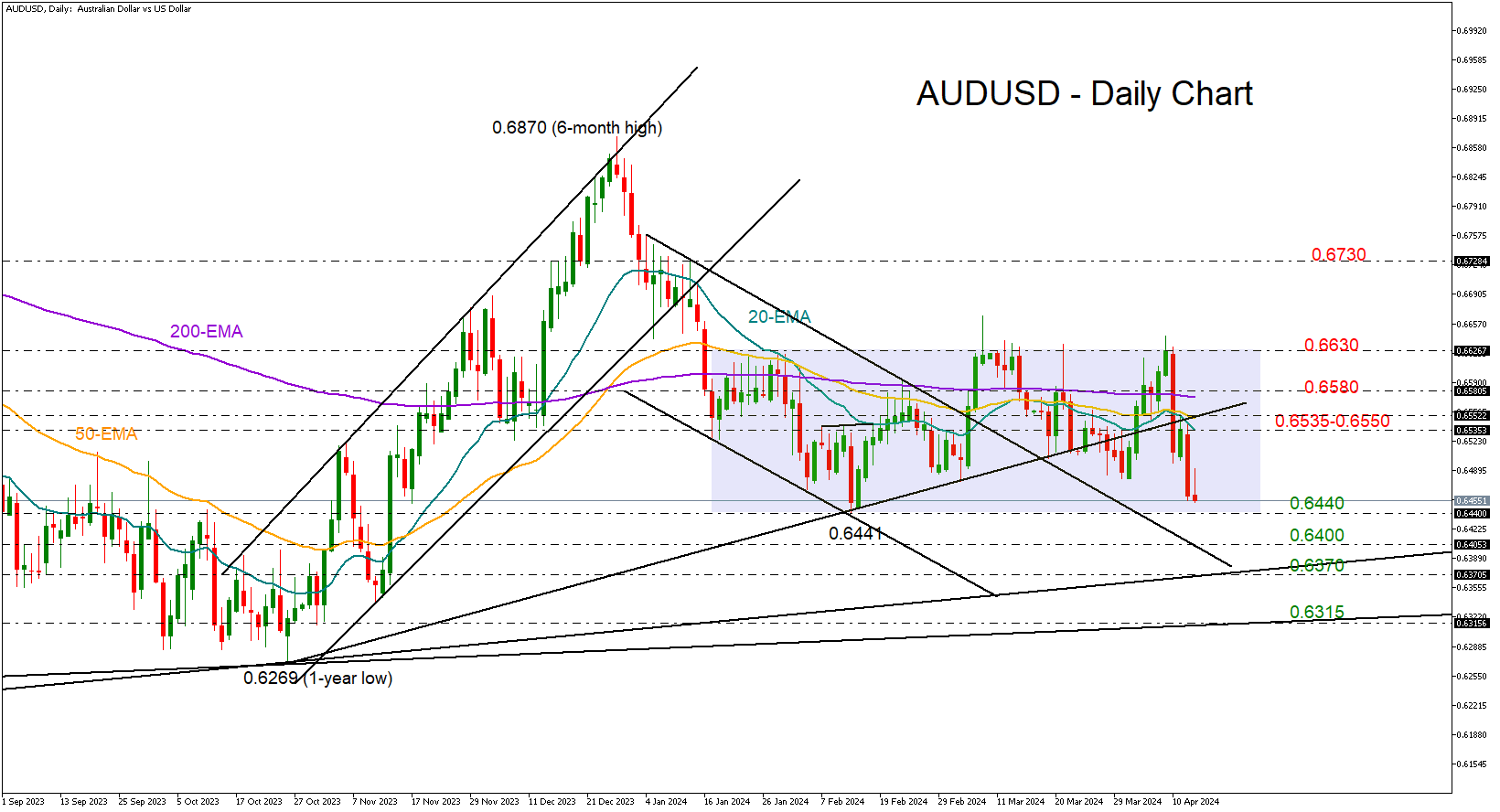

- AUDUSD tests lower boundary of the 2024 range

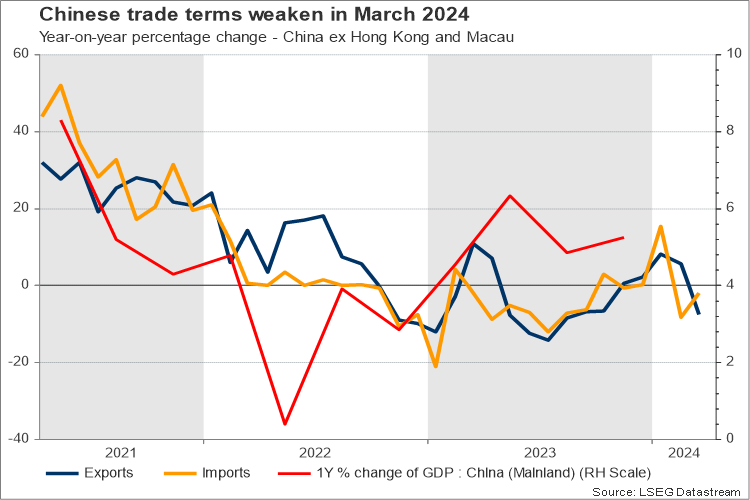

China to report weaker GDP after disappointing trade data

China remains a major trade partner for advanced economies such as the US and Europe, especially in the manufacturing sector, where its global dominance in terms of production and value added surpasses its peers by a large margin. Therefore, although the West has toughened its stance against Beijing’s trade practices in industrial areas, demand from China will remain vital for global markets.

China’s GDP data scheduled for release on Tuesday will give an insight into how the economy performed in the first three months of the year. Forecasts point to a slowdown to 4.6% y/y in Q1 from 5.2% y/y previously - the lowest in a year - but the sharp decline might be an outcome of the annual comparison effects as China’s delayed reopening at the end of 2022 unleashed a surge in consumption and production in the same period last year.

The unexpected steep 7.5% drop in the value of exports and the almost 2.0% decline in imports in March has already warned traders over an economic deceleration in Q1, but if the quarter-on-quarter GDP reading shows a stronger rebound of 1.4% in Q1 compared to 1.0% in Q4, investors may not sell aggressively the yuan and the aussie. Note that the manufacturing sector returned to expansion in March for the first time in a year, according to the PMI data.

Economic outlook remains blurry

Nevertheless, the economy might have a tough time in boosting investors’ sentiment. The problematic real estate sector, which remains vulnerable to delayed projects, excessive borrowing, and bankruptcy jitters, will keep weighing on the economic outlook. Recent headlines suggest that credit support from banks is well below the amount needed to secure the completion of pre-sold houses, while the previous stimulus measures are already losing power in the new homes market. Funds raising in the Mainland's capital markets is not optimistic either, hitting multi-year lows recently in a sign of broken confidence.

As regards to consumption, the latest inflation figures underlined persisting challenges on the demand front. Consumer prices rose by a marginal rate of 0.1% y/y in March after a 0.7% surge on the back of the Lunar new year celebrations in February, remaining worlds apart as inflation in other major economies is showing some stickiness above central banks’ targets. Producer prices faced stronger headwinds, dipping for the 16th consecutive month by 2.5% y/y.

Hence, given the problematic old growth drivers, such as infrastructure, and the geopolitical and policy risks, which threaten China’s competitiveness in clean energy products, the government might be under pressure to release more stimulus if Tuesday’s GDP data miss expectations.

AUDUSD levels to watch

Looking at AUDUSD, the pair is currently trading at the lower boundary of the 2024 range of 0.6440-0.6630, and in the absence of any positive technical signals, there is little optimism for a rebound. Although the negative surprise in China’s trade data did not cause any serious reaction in the market last week, investors will look for a break below the 0.6440 floor and towards 0.6400 if China’s GDP misses forecasts by a large margin. Slightly lower, the 0.6315-0.6370 support trendline area could be another important pivot area.

Alternatively, for the price to reach the upper band of the range around 0.6630, the bulls will have to overcome the 0.6535-0.65680 zone, where the exponential moving averages (EMAs) are placed. If the pair breaks its horizontal move on the upside, resistance could next emerge near the 0.6730 territory.

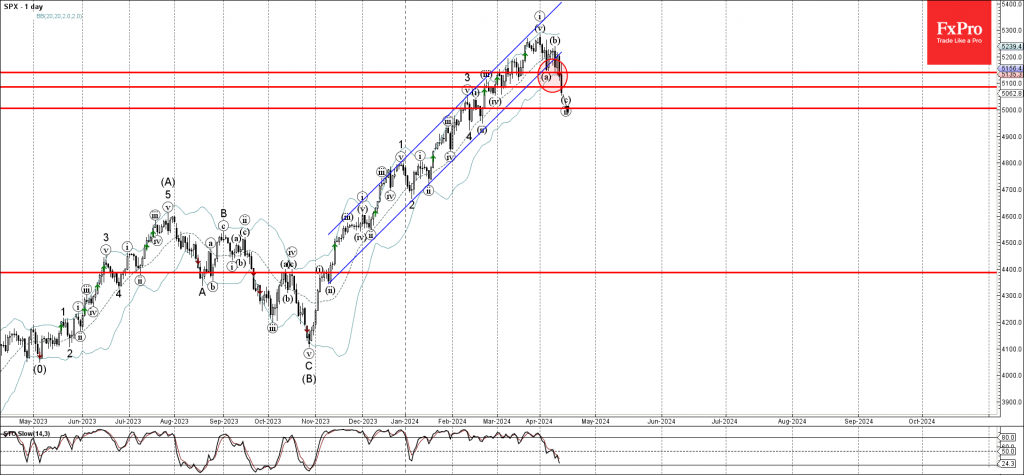

S&P 500 Wave Analysis

- S&P 500 falling inside sharp c-wave

- Likely to fall to support level 5000.00

S&P 500 index continues to fall inside the sharp c-wave of the minor ABC correction ii from the end of last month.

The price earlier broke the support levels 5100.00 and 5140.00, which strengthened the bearish pressure on these index .

Given the worsening sentiment seen across the USA equity, S&P 500 index can be expected to fall further to the next round support level 5000.00.

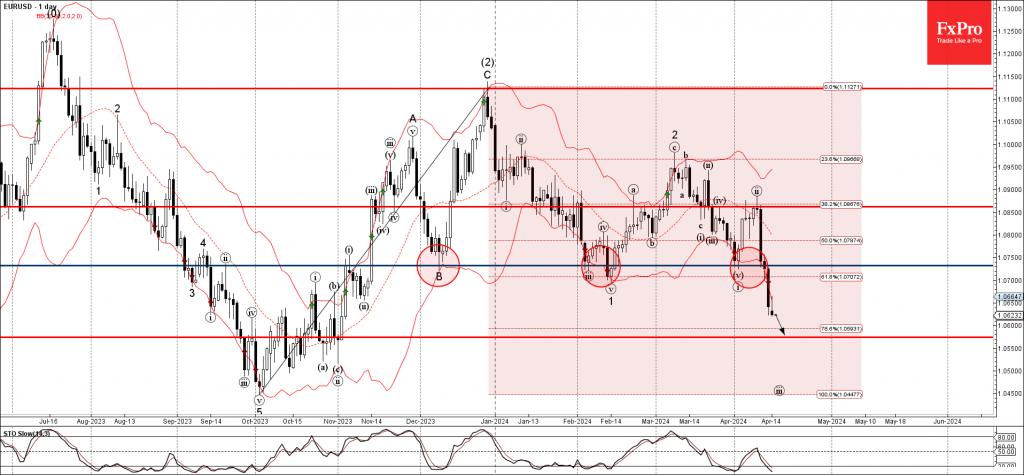

EURUSD Wave Analysis

- EURUSD broke support level 1.0730

- Likely to fall to support level 1.0570

EURUSD currency pair fall after the earlier breakout of the key support level 1.0730 (which has been reversing the price from December) intersecting with the 61.8% Fibonacci correction of the ABC correction (2) from October.

The breakout of the support level 1.0730 accelerated the iii-wave of the active impulse waves 3 and (3) .

Given the continuing bullish USD sentiment, EURUSD can be expected to fall further to the next support level 1.0570.

UK Inflation Report Could Shift Market’s Focus Away from Geopolitics

- BoE’s determination could be tested if this week’s CPI prints surprise on the upside

- Pound could benefit from a strong set of data this week

- Employment data will be released on Tuesday; the inflation report on Wednesday

Inflation in the spotlight

At the last Bank of England meeting, which is still relatively fresh in the market’s mind, the Committee maintained its balanced approach. The UK economy is navigating through rough waters with the upcoming general elections expected to add further fuel to the fire. Interestingly, the UK appears to exhibit signs both from the US and euro area economies.

It is experiencing the strong inflation seen in the former and the weak growth present in the latter. BoE’s inherited dovishness has not been openly expressed yet, but this week’s data could tip the balance in favour of the doves. In the meantime, at least six members are scheduled to be on the wires including Governor Bailey and known hawk Haskel.

Labour market data on Tuesday

On Tuesday, labour market statistics and average earnings data for February will be published. The latter has been a real headache for the BoE doves as, despite the deceleration seen from the 2023 highs, the yearly growth in average earnings remains incompatible with a central bank willing to cut rates. The market forecasts point to a small easing to 5.8% for the excluding bonuses indicator, which would be another positive sign for the doves.

The main reason for the elevated earnings prints is the tightness of the labour market. The official unemployment is expected to climb to 4%, just a tad above its recent all-time low level, with the market paying more attention to the more up-to-date claimant count change. A large jump in March could tentatively show an easing in labour demand. However, this progress is very gradual and might not pick up considerable speed due to the post-Brexit restrictions imposed by the UK government.

Could inflation surprise on the upside?

At 06:00 GMT on Wednesday the March inflation report will be released. Progress has been made on this front as headline CPI dropped in February to its lowest rate since October 2021 with the core indicator proving much stickier. The market is looking for another easing to 3.1% and 4.2% respectively but there might be some sizeable upside risks following last Wednesday’s strong US inflation report.

Confirmation of the market forecasts would appease the BoE doves and bring forward the chances of the first rate cut from September to August. This move could pick up speed if Wednesday’s producer price index results surprise on the downside and thus point to further easing in inflationary pressure during the rest of 2024.

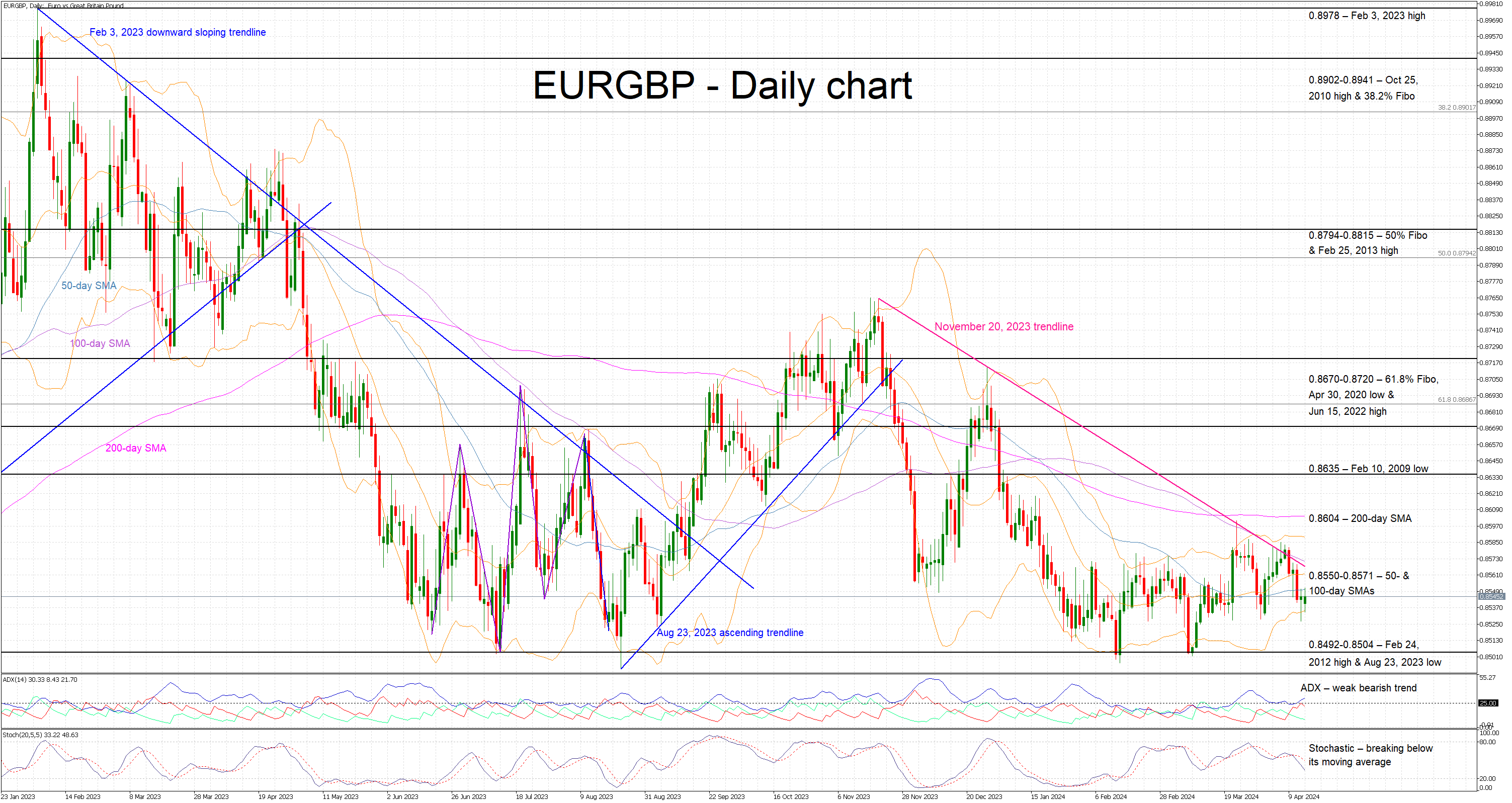

Pound could benefit from a stronger inflation report

The pound has been anxiously trying to take advantage of developments elsewhere, but it has failed to make any concrete gains lately. The ongoing dollar strength has pushed the pound/dollar pair to the lowest level since mid-December 2023 while euro/pound is still hovering close to its recent 2024 lows.

With the ECB seen ready to announce a rate cut in June, a strong set of data this week could push the euro/pound pair towards the 0.8492-0.8504 area and potentially open the door to a new 20-month low level.

On the flip side, weakening inflationary pressure and as loosening labour market could convince the market that a BoE rate cut is closer than currently anticipated and hence allow pound bears to push the euro/pound pair towards the November 23, 2023 downward sloping trendline at 0.8566.

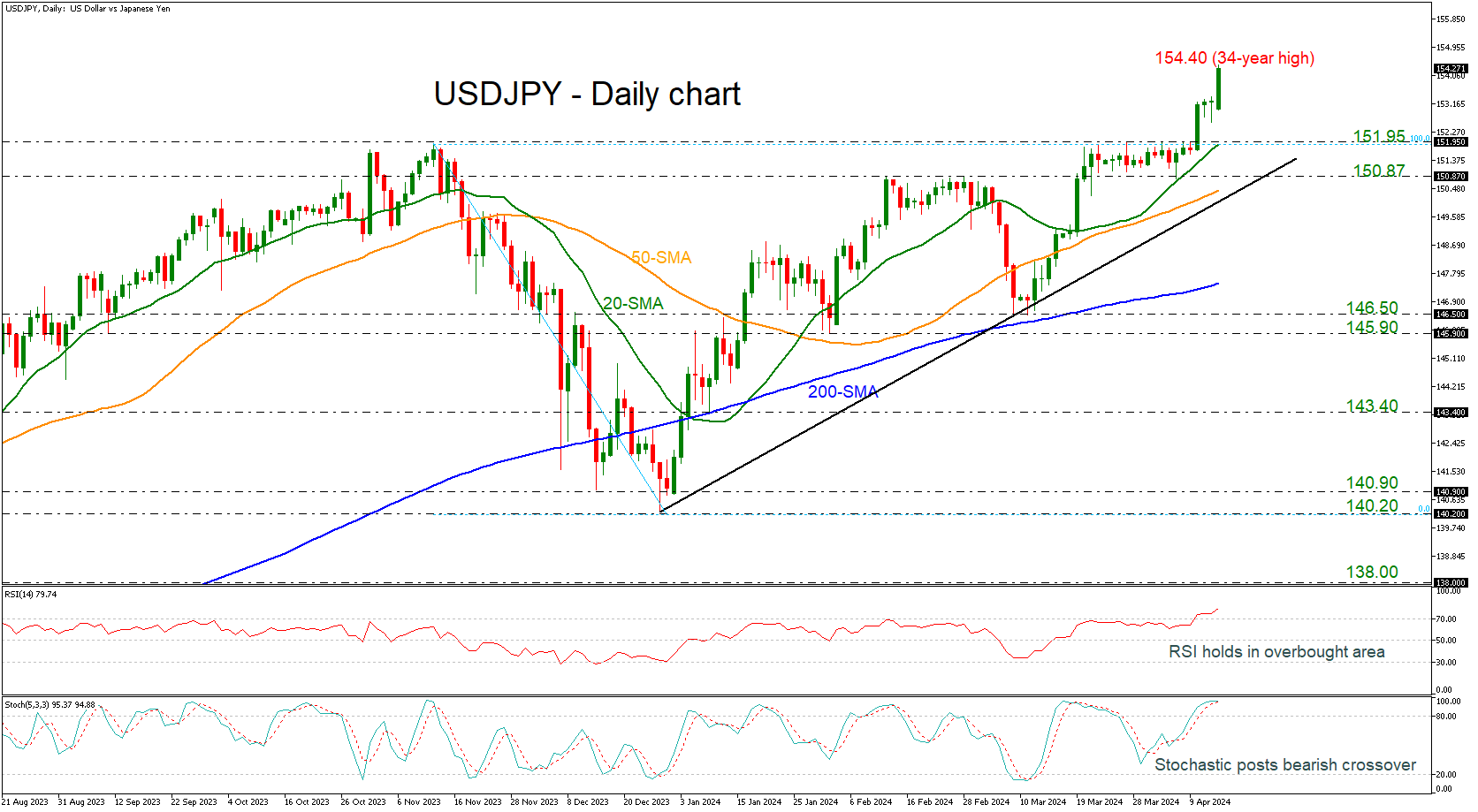

USDJPY Rallies to Another Fresh 34-Year High

- USDJPY surpasses 154.00

- Round numbers to be watched

- Stochastics indicate overstretched market

USDJPY is surging to another multi-year high above the 154.00 round number, adding 0.8% so far today. The technical oscillators are holding in overbought regions. The RSI is suggesting that more gains may be on cards; however, the stochastic oscillator is indicating an overstretched market as it is creating a bearish crossover within its %K and %D lines above the 80 level, hinting that a potential negative retracement is near.

Should the pair manage to strengthen its positive momentum, the next resistance could come near the next handles such as 155.00 and 156.00 before the market rallies towards the 161.8% Fibonacci extension level of the down leg from 151.95 to 140.20 at 159.15.

However, if prices begin a bearish correction, immediate support could come from the 151.95 obstacle, which overlaps with the 20-day simple moving average (SMA) ahead of the 150.87 barrier. The next key support to watch lower down is the 150.87 region ahead of the 50-day SMA at 150.45 before testing the medium-term ascending trend line at 150.00.

To sum up, USDJPY remains positive since prices are continuing the steep upward rally and only a decrease beneath the 200-day SMA may change the outlook to neutral.

Fed’s Williams foresees interest rate normalization starting this year

In an interview with BloombergTV. New York Fed President John Williams suggested that Fed is still on track to start cutting interest rates within the year.

"We will need to start a process at some point to bring interest rates back to more normal levels, and my own view is that process will likely start this year," Williams stated.

Regarding the recent inflation data, Williams did not regard it as a decisive shift in economic trends but acknowledged its impact on his assessments and future forecasts.

Williams also touched on the topic of the Federal Reserve's balance sheet management, specifically the ongoing quantitative tightening process. He advocated for a more measured pace in reducing the Fed's balance sheet, a strategy aimed at allowing more room for evaluation and adjustment.

Sunset Market Commentary

Markets

Geopolitics as a market theme tend to have a limited shelf life but investors this time really took it to the next level. Except for some minor bourse losses in Asia, Iran’s retaliatory attacks against Israel didn’t trigger the slightest risk aversion in Europe, quite the contrary. The EuroStoxx50 adds 1.5% and Wall Street rises 0.5-1%. Core bonds slipped. Yields gapped higher at the open with gains boosted by exceptionally strong US retail sales. The March edition crushed the bar, whatever the gauge, while the February readings were revised higher. Headline sales rose 0.7% m/m and core measures rose between 1 and 1.1%. 8 out of the 13 categories printed gains. The control group (excluding food, gas, building materials and car dealers) rose the most since February 2023 (1.1% m/m), boding well for the private consumption component in Q1 GDP growth. US yields jump between 7 and 9.5 bps across the curve with the likes of the 10y on track for a new YtD closing high. The 2y came less than 1 bp short of testing the 5% again. German yields add 6.6-7.2 bps. The Japanese yen greatly underperforms on currency markets with the risk-on mood and rising core bond yields bashing JPY to a new 34y low against the dollar. USD/JPY tops the 154 big figure. EUR/USD temporarily gave up all earlier gains after the retails sales were released. The pair hit an intraday low around 1.063, just shy of Friday’s YtD (intraday) low of 1.0623 before recovering marginally to 1.064 currently. Sterling strengthens against most peers in the run-up to an economic update that entails labour market data tomorrow, inflation figures Wednesday and retail sales Friday. EUR/GBP drops to 0.8534. Oil prices eased back below $90, suggesting few Middle East related supply concerns. Metal prices including aluminum do rise about 5% following the UK and US sanctioning Russian exports but that’s about half of the initial surge in Asian dealings.

More ECB speakers hit the wires today in the wake of the policy meeting last Thursday. Governing Council member Simkus sees a more than 50% of more than 3 rate cuts this year with a follow-up move in July after June. Slovakia’s Kazimir opened the door for a cut in June but didn’t want to commit on a path after June. Chief Economist Lane noted that the further inflation path is going to be bumpy. He expressed confidence inflation is heading back to 2% but added wage gains and services inflation remains elevated. Their comments had no intraday impact on markets.

News & Views

The Swedish government presented its 2024 Spring Budget today against the background of significantly falling inflation while the Swedish economy is in recession, with low GDP growth and rising unemployment. CPIF inflation is expected to average 2.1% this year, followed by 1.7% next year and 2% in 2026. GDP growth is set to accelerate from 0.7% this year, to 2.5% next year and 3.2% in 2026. Against this background and given fiscal leeway, Minister of Finance Svantesson presented an additional spending budget of SEK 17.3bn. The proposals are meant to navigate Sweden through the recession and safeguarding the welfare system, improve law enforcement and safety and security and stronger defense and crisis preparedness. The government forecasts a 1.2% of GDP budget shortfall this and a small 0.3% deficit in 2025 before returning to budget surpluses. The debt to GDP ratio is expected to peak at 31.8% this year, before falling back to 31.5% and 30% over the next two years. The Swedish krona recovers somewhat today in a better risk environment after testing the EUR/SEK YTD high just above 11.60 last week.

Rating agency Fitch commented on the Belgian pensions reform bill, approved by Federal Parliament earlier this month. Fitch judges that reforms (introduction of pension bonus, increased requirement to obtain the minimum pension, cap on the growth of some pensions to civil servants,…) are insufficient to alleviate the increasing cost pressures of an ageing population on public finances. Their positive impact is largely offset by an earlier increase in the minimum pension. Political fragmentation continues to complicate fiscal adjustment efforts in the face of high and rising public debt. This is also reflected in Fitch’s negative outlook on the AA- rating. A parliamentary monitoring committee suggested that the fiscal deficit would rise to 5.6% of GDP by 2027 (from 4.3% last year) in a no-policy change scenario. Inflation indexation is also having a negative net impact on the budget balance with general election and a potential political standstill looming as the next risk factor.

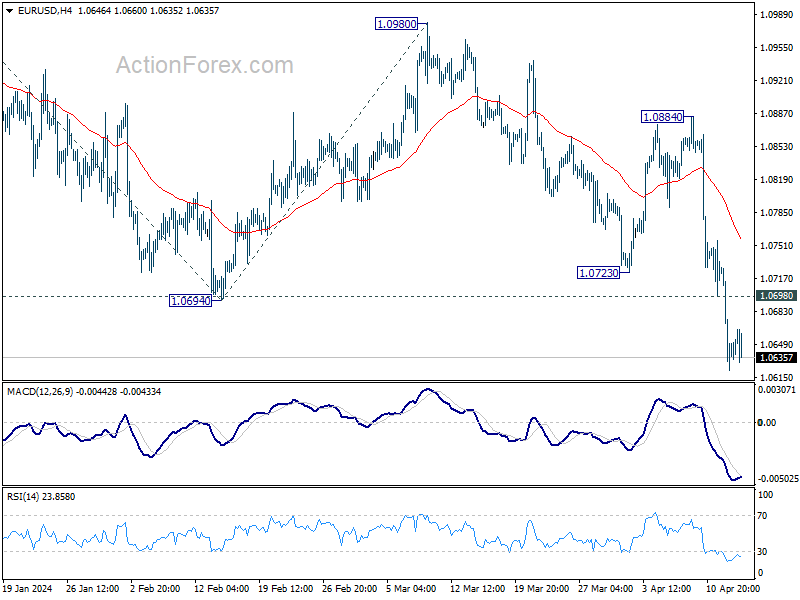

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0599; (P) 1.0665; (R1) 1.0708; More...

No change in EUR/USD's outlook and intraday bias stays on the downside. Current fall is part of the decline from 1.1138. Next target is 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. On the upside, above 1.0723 support turned resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

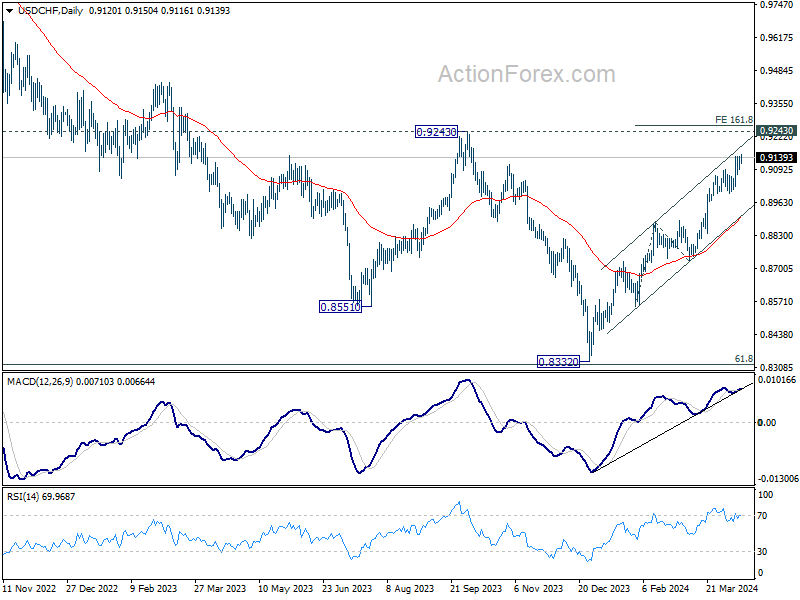

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9105; (P) 0.9126; (R1) 0.9164; More....

Intraday bias in USD/CHF stays neutral first. Consolidation from 0.9146 might still extend further. But further rally is expected as long as 0.8996 support holds. Firm break of 0.9146 will target 161.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.9268.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.