Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0830; (P) 1.0886; (R1) 1.0917; More...

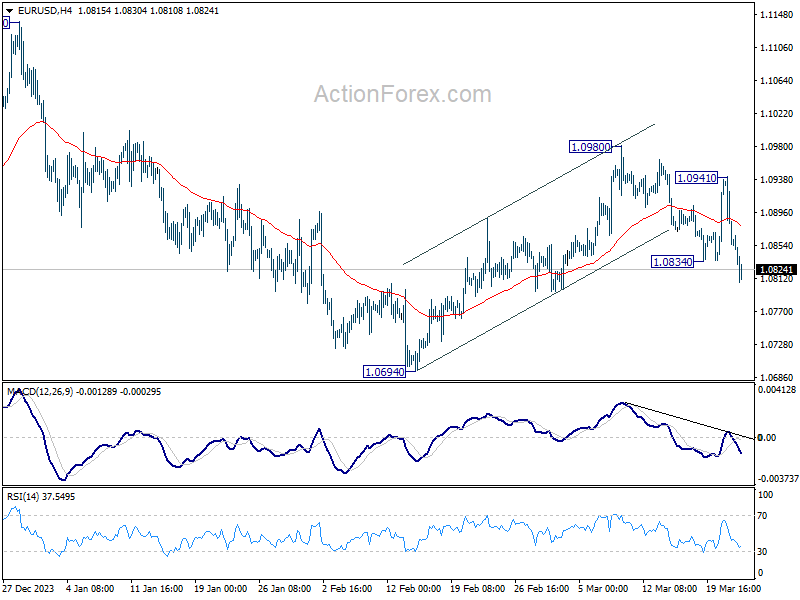

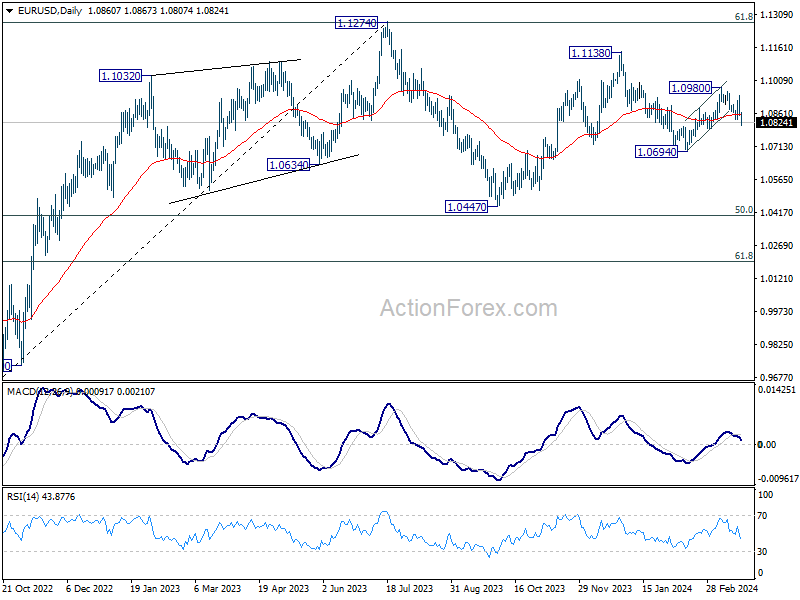

Intraday bias in EUR/USD remains on the downside at this point. Current development argues that corrective recovery from 1.0694 has completed at 1.0980 already. Deeper fall is expected to retest 1.0694 next. For now, risk will stay on the downside as long as 1.0941 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Yen Rebounds Amid Short-Covering, Dollar Rally Eases

Japanese Yen rebounds broadly today, likely driven by traders taking profits on short positions after a significant week of sell-off following BoJ's rate hike. This stabilization comes amidst speculations stirred by Japan's latest inflation data, raising the prospect of a second hike by BoJ in the second half of the year. Nevertheless, such predictions seem premature at this juncture. Additionally, the decline in benchmark yields from Germany and the UK has provided some support to Yen.

Meanwhile, Dollar is trading as the second strongest currency for the day, albeit with signs of losing momentum as the week draws to a close. This slight pullback could be attributed to profit-taking activities as well. In contrast, Australian Dollar and New Zealand Dollar are facing downward pressure, trading up as the day's underperformers. Both currencies face additional pressure due to the sharp decline in Chinese Yuan, which hit a four-month low. European majors present a mixed picture, with Sterling notably underperforming compared to its counterparts.

In Europe, at the time of writing, FTSE is up 0.46%. DAX is up 0.07%. CAC is down -044%. UK 10-year yield is down -0.075 at 4.039. Germany 10-year yield is down -0.067 at 2.344. Earlier in Asia, Nikkei rose 0.18%> Hong Kong HSI fell -2.16%. China Shanghai SSE rose 0.26%. Singapore Strait Times fell -0.07%. Japan 10-year JGB yield rose 0.0037 to 0.744.

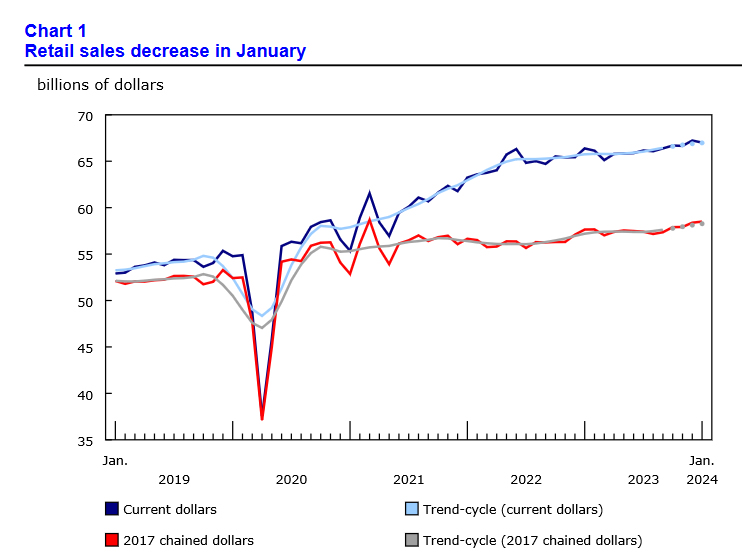

Canada's retail sales falls -0.3% mom in Jan, led by motor vehicle and parts dealers

Canada's retail value fell -0.3% mom to CAD 67.0B in January, smaller than expectation of -0.4% mom decline. Sales were down in three of nine subsectors and were led by decreases at motor vehicle and parts dealers (-2.4% mom)

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were up 0.4% mom.

In volume terms, retail sales increased 0.2% mom.

Advance estimate suggests that sales increased 0.1% mom in February.

ECB's Nagel: June cut increasingly likely, but no automatism afterwards

In a webcast today, ECB Governing Council member Joachim Nagel indicated that the chance is increasing for a first rate cut "before the summer break" in August. However, he cautioned that afterwards, ECB will maintain a data-dependent approach and policy loosening wouldn't be on autopilot. "I do not see that there is a kind of automatism," he remarked. "It is data dependent and it is not a done deal that everything is going smoothly for the rest of the year or maybe for next year. So we have to be vigilant, we have to be cautious."

The ECB official flagged several "open issues" that warrant cautions, including the volatility in energy prices and the ongoing uncertainties surrounding wage growth and profit margins. "This meeting-to-meeting approach is the best way to address the current situation," he added.

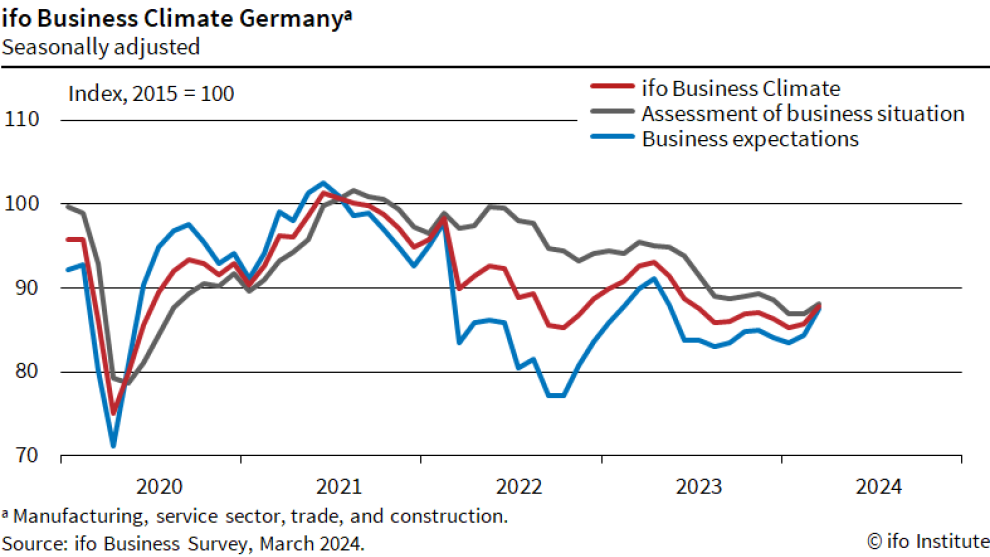

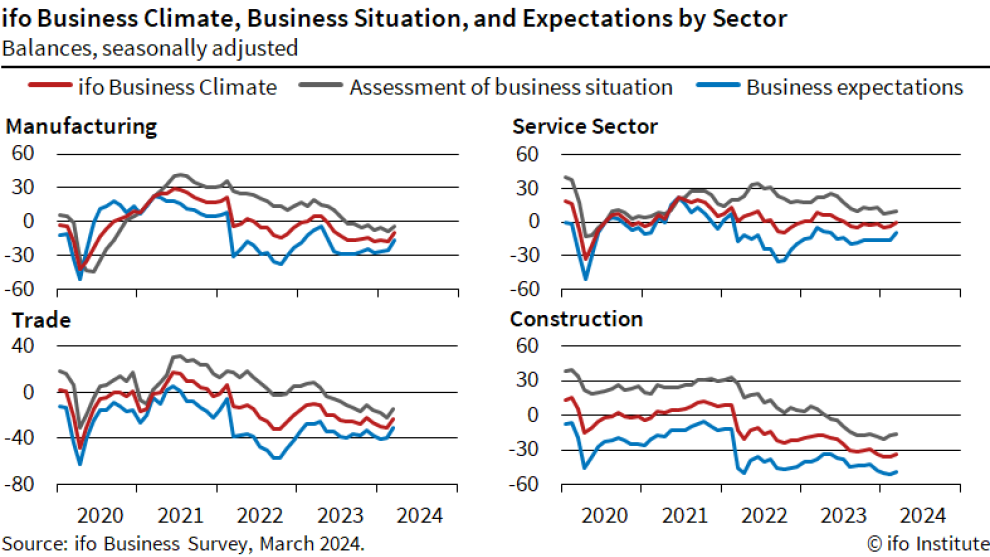

German Ifo business climate rises to 87.8, glimpses light on the horizon

Germany's Ifo Business Climate Index rose to 87.8 in March, from the previous 85.7, surpassing anticipated 86.2. This uplift is mirrored in both Current Assessment Index, which advanced from 86.9 to 88.1 against expectations of 86.8. Expectations Index, which climbed from 84.1 to 87.5, outstripping the forecasted 84.7.

A closer look at sector-specific changes reveals significant variances: Manufacturing sector saw a substantial leap from -17.1 to -10.0. Services sector marked a positive turn, moving from -4.0 to 0.3. Meanwhile, the trade sector saw an improvement as its index rose from -30.8 to -22.9. However, the construction sector observed a slight decrease from -35.4 to -33.5,.

Ifo President Clemens Fuest encapsulated the sentiment by stating, "The German economy glimpses light on the horizon," highlighting a renewed sense of optimism among businesses.

UK retail sales volumes flat in Feb, sales value down -0.1% mom

In February 2024, UK's retail sales volumes remained unchanged month-over-month, a performance that's better than expectation of -0.3% mom decline. Meanwhile, sales value slightly dipped by a -0.1% mom.

A broader examination reveals -0.4% decline in sales volumes over the three months leading up to February, compared to the preceding three-month period. Additionally, a year-over-year comparison with the three months to February 2023 shows -1.0% decrease.

Japan CPI core rises to 2.8% in Feb, above BoJ's target for 23rd month

Japan's CPI core (ex-fresh food) rises from 2.0% yoy to 2.8% yoy in February, matched expectations. This increase marks the first acceleration in four months and maintains the index above BoJ's 2% target for the 23rd consecutive month.

The uptick in the core CPI was primarily due to a less pronounced decline in energy prices, reflecting diminishing impact of government subsidies introduced to mitigate energy costs. Specifically, energy prices saw a decrease of -1.7% yoy, a significant moderation from -12.1% yoy drop recorded in January.

The overall headline CPI also showed an uptick, accelerating from 2.2% yoy to 2.8%yoy. However, when examining CPI core-core, which excludes both food and energy, there was a slight slowdown from 3.5% yoy to 3.2% yoy.

New Zealand's goods exports rises 16% yoy in Feb, imports up 3.3% yoy

In February, New Zealand's goods exports leaped by 16% yoy to NZD 5.9B. This surge contrasts with a more modest 3.3% yoy increase in goods imports, totaling NZD 6.1B. Consequently, monthly trade deficit narrowed significantly to NZD -218m, far exceeding market expectations of a shortfall of NZD -825m.

Exports to China, New Zealand's largest trading partner, increased by 10% yoy, contributing an additional NZD 154m. US saw a remarkable 52% yoy jump in exports, adding NZD 305m, while EU and Australia also recorded increases in New Zealand exports by 7.9% yoy and 5.9% yoy, respectively. However, trade with Japan contracted, with exports declining by -10% yoy.

On the import front, China and South Korea marked significant increases of 7.1% yoy and 42% yoy, respectively, indicating robust demand for goods from these economies. Conversely, imports from US and EU saw downturns, declining by 20% yoy and 7% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0830; (P) 1.0886; (R1) 1.0917; More...

Intraday bias in EUR/USD remains on the downside at this point. Current development argues that corrective recovery from 1.0694 has completed at 1.0980 already. Deeper fall is expected to retest 1.0694 next. For now, risk will stay on the downside as long as 1.0941 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (MZD) Feb | -218M | -825M | -976M | -1089M |

| 23:30 | JPY | National CPI Y/Y Feb | 2.80% | 2.20% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Feb | 2.80% | 2.80% | 2.00% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Feb | 3.20% | 3.50% | ||

| 00:01 | GBP | GfK Consumer Confidence Mar | -21 | -20 | -21 | |

| 07:00 | GBP | Retail Sales M/M Feb | 0.00% | -0.30% | 3.40% | 3.60% |

| 09:00 | EUR | Germany IFO Business Climate Mar | 87.8 | 86.2 | 85.5 | 85.7 |

| 09:00 | EUR | Germany IFO Current Assessment Mar | 88.1 | 86.8 | 86.9 | |

| 09:00 | EUR | Germany IFO Expectations Mar | 87.5 | 84.7 | 84.1 | |

| 12:30 | CAD | Retail Sales M/M Jan | -0.30% | -0.40% | 0.90% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Jan | 0.50% | -0.50% | 0.60% |

Canada’s retail sales falls -0.3% mom in Jan, led by motor vehicle and parts dealers

Canada's retail value fell -0.3% mom to CAD 67.0B in January, smaller than expectation of -0.4% mom decline. Sales were down in three of nine subsectors and were led by decreases at motor vehicle and parts dealers (-2.4% mom)

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were up 0.4% mom.

In volume terms, retail sales increased 0.2% mom.

Advance estimate suggests that sales increased 0.1% mom in February.

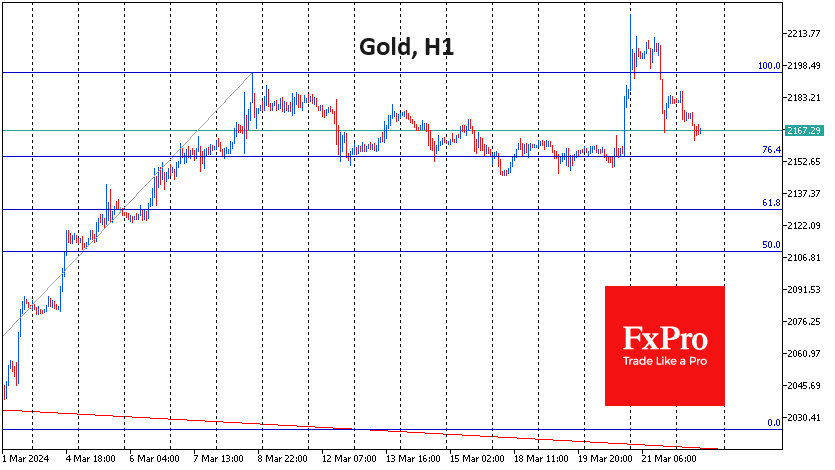

Gold’s Retreat Not Yet a Reversal

The Fed’s comments led to a 3% rise in gold, but the dollar’s recovery in the second half of Thursday reduced this gain to just 0.5%. Technically, the outlook is unclear, but fundamentally, things are still on the side of the bulls.

In early trading on Thursday, gold slipped to $2222 on thin liquidity and the triggering of stop orders, which washed short positions out of the market. Throughout the day on Thursday, a stabilisation above $2200 looked attractive for many to take money off the table.

The technical analysis so far gives a mixed picture on the daily timeframes.

On the bullish side, gold’s ability to break above previous highs confirmed the Fibonacci extension scenario to 2300 (161.8% of the rally in the last days of February) after a corrective consolidation of 76.4%. The ability to make new highs after a pause is also a bullish signal.

On the bearish side, fatigue after the rise is temporarily evident: the price update of the highs has not been confirmed by the RSI. Moreover, the index left the overbought territory (>70) in the first half of Friday’s trading.

Cautious traders may want to wait for a break above the $2155-2190 area, as the chances of further movement in the direction of the break are higher.

In our view, gold’s failure on Thursday and the first half of Friday does not look like a reversal, as the push into the dollar in recent hours is the result of speculation that other central banks will be even softer than the Fed. This is a supportive environment for risk assets, including gold. Still, the impressive rally in gold since the second half of February and the recent surge have left the market somewhat overheated and in need of a pause.

ECB’s Nagel: June cut increasingly likely, but no automatism afterwards

In a webcast today, ECB Governing Council member Joachim Nagel indicated that the chance is increasing for a first rate cut "before the summer break" in August. However, he cautioned that afterwards, ECB will maintain a data-dependent approach and policy loosening wouldn't be on autopilot.

"I do not see that there is a kind of automatism," he remarked. "It is data dependent and it is not a done deal that everything is going smoothly for the rest of the year or maybe for next year. So we have to be vigilant, we have to be cautious."

The ECB official flagged several "open issues" that warrant cautions, including the volatility in energy prices and the ongoing uncertainties surrounding wage growth and profit margins. "This meeting-to-meeting approach is the best way to address the current situation," he added.

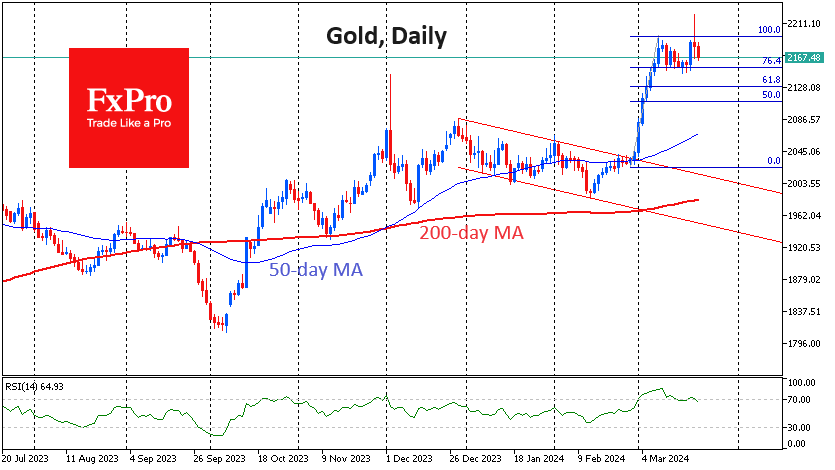

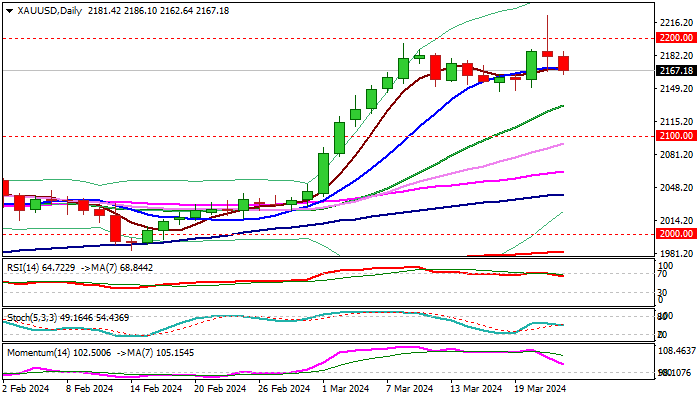

XAU/USD: Gold Eases from New Record High

Gold price eases further on Friday, extending pullback from new record high $2222 (posted on Thursday) after a strong upside rejection on probe above psychological $2200 barrier.

The yellow metal came under increased pressure from stronger dollar after Fed kept the policy unchanged and signaled that high borrowing cost may stay elevated as the US economy is in good condition, which cooled talks about rate cuts from June.

However, the US central bank remains on track towards policy easing this year, which will continue to underpin gold price in the longer run.

Significant supports at $2146/41 (this week’s low / former record high of Dec 4) are exposed and should ideally contain and keep the price action within limited consolidation range, guarding lower pivot at $2131 (Fibo 38.2% of $1984/$2222, reinforced by rising 20DMA), where extended dips should find firm ground to mark a healthy correction of a larger rally from $1984).

Technical picture is mixed on daily chart as MA’s are in bullish setup, but momentum and RSI indicators are heading south after diverging from the price action in earlier sessions, which requires caution.

Res: 2186; 2200; 2222; 2250.

Sup: 2160; 2146; 2141; 2131.

Pound Drops to 1-Month Low After Flat Retail Sales

The British pound has extended its losses on Friday. In the European session, GBP/USD is trading at 1.2600, down 0.45%. Earlier, the pound fell as low as 1.2584, its lowest level since March 20.

UK retail sales unchanged in February

UK retail sales were flat in February, after a revised 3.6% gain (m/m) in January. This was better than the market estimate of -0.3%. On an annualized basis, retail sales fell by 0.4%, erasing most of the 0.5% gain in January. Britain’s weather was unusually wet in February which dampened retail trade.

Dovish BoE sends pound tumbling

The Bank of England maintained the cash rate at 5.25% at Wednesday’s meeting. The pause was widely expected and marked the sixth straight time that the BoE has kept rates unchanged.

Perhaps the most significant development at the meeting was the Monetary Policy Committee vote. The MPC voted 8-1 to keep rates unchanged, with one member voting for a quarter-point cut. This was the first time in the current tightening cycle that no members voted for a hike – at the previous meeting, two members voted to raise rates by a quarter-point.

The markets pounced on the vote as evidence of a dovish shift in the Bank’s stance and the British pound sank 1% on Wednesday, its worst one-day performance since October 2023.

It looks like rates have peaked, but when can we expect the BoE to start cutting rates? Governor Bailey said after the meeting that inflation is not “yet at the point where we can cut interest rates, but things are moving in the right direction”. The markets are looking at an initial cut in June, with an outside possibility in May.

GBP/USD Technical

- GBP/USD is testing support at 1.2605. Below, there is support at 1.2552

- There is resistance at 1.2704 and 1.2757

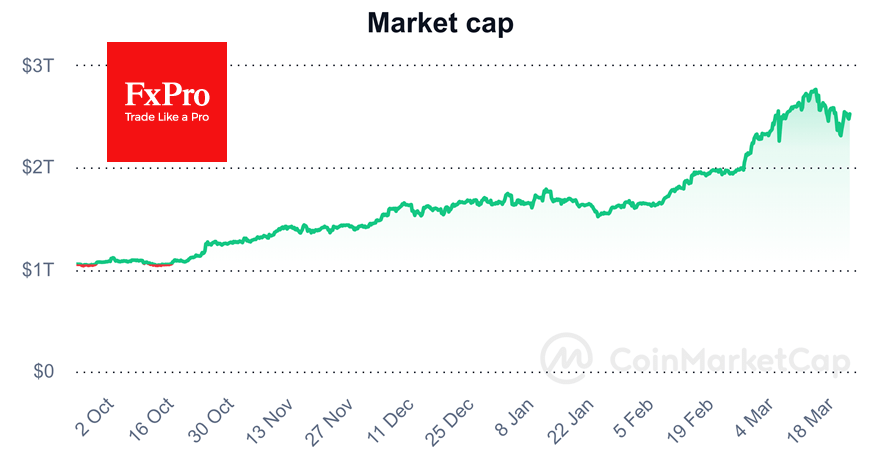

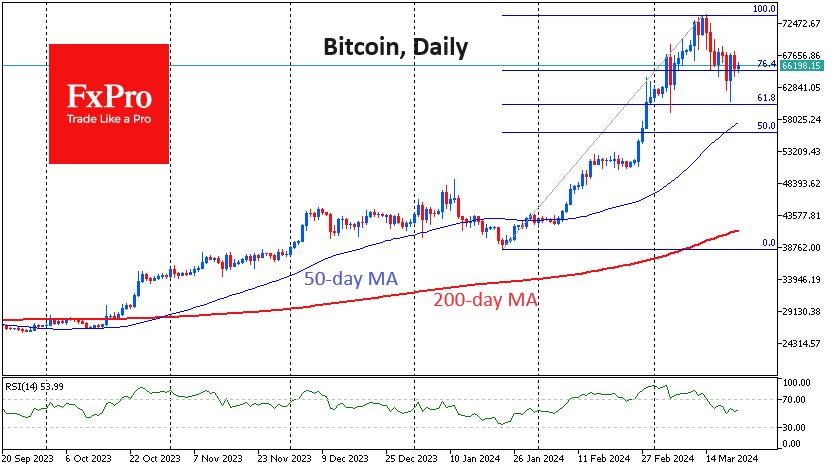

Rising Dollar Spooked Bitcoin, But Not the Entire Crypto Market

Market picture

The cryptocurrency market closed lower on Thursday, but little changed from the $2.53 trillion market cap over 24 hours. However, the internal dynamics are mixed. Bitcoin loses 1.5% and retreats to $66K, while Ethereum hovers around $3500 (-0.25%), BNB and DOGE are up over 5%, and XRP is up around 4%.

It’s as if the cryptocurrencies haven’t chosen their shepherd: should they follow negative from the strengthening dollar or positive after new heights of US indices? We lean towards the latter, believing that the dollar strengthens against even weaker peers whose central banks are more dovish.

Overall, G10 central banks’ dovishness eases a liquidity drain, which is positive for cryptocurrencies that are sensitive to it.

News background

Bitcoin’s current pullback is a temporary correction, according to CryptoQuant. Judging by the low level of inflows from new investors, BTC’s bull cycle is far from over.

BTC could fall to $52K in the coming weeks, warned 10xResearch. However, there will be a further rise to at least $106K due to the upcoming halving in April.

The SEC has no good reason to reject applications to launch an Ethereum ETF, said Coinbase General Counsel Paul Grewal. For years, the commission has treated the world’s second-largest cryptocurrency as an exchange-traded commodity rather than a security, he said.

Former US CFTC commissioner Brian Quintenz criticised the SEC’s stance on Ethereum, saying the agency was creating confusion in the law.

Solana is attracting the most investor interest. Solana accounts for 49.3% of global investor interest in blockchain ecosystems in 2024, CoinGecko calculated based on internet search data. The leadership is fuelled by SOL’s rise to highs from 2021, the development of ecosystem projects such as Pyth and the popularity of meme tokens such as dogwifhat.

Ethereum co-founder Vitalik Buterin said the main challenge for the network’s PoS mechanism was the centralisation involved in staking services. Lido, Coinbase and Binance have gained “excessive market share”, he said.

German Ifo business climate rises to 87.8, glimpses light on the horizon

Germany's Ifo Business Climate Index rose to 87.8 in March, from the previous 85.7, surpassing anticipated 86.2. This uplift is mirrored in both Current Assessment Index, which advanced from 86.9 to 88.1 against expectations of 86.8. Expectations Index, which climbed from 84.1 to 87.5, outstripping the forecasted 84.7.

A closer look at sector-specific changes reveals significant variances: Manufacturing sector saw a substantial leap from -17.1 to -10.0. Services sector marked a positive turn, moving from -4.0 to 0.3. Meanwhile, the trade sector saw an improvement as its index rose from -30.8 to -22.9. However, the construction sector observed a slight decrease from -35.4 to -33.5,.

Ifo President Clemens Fuest encapsulated the sentiment by stating, "The German economy glimpses light on the horizon," highlighting a renewed sense of optimism among businesses.

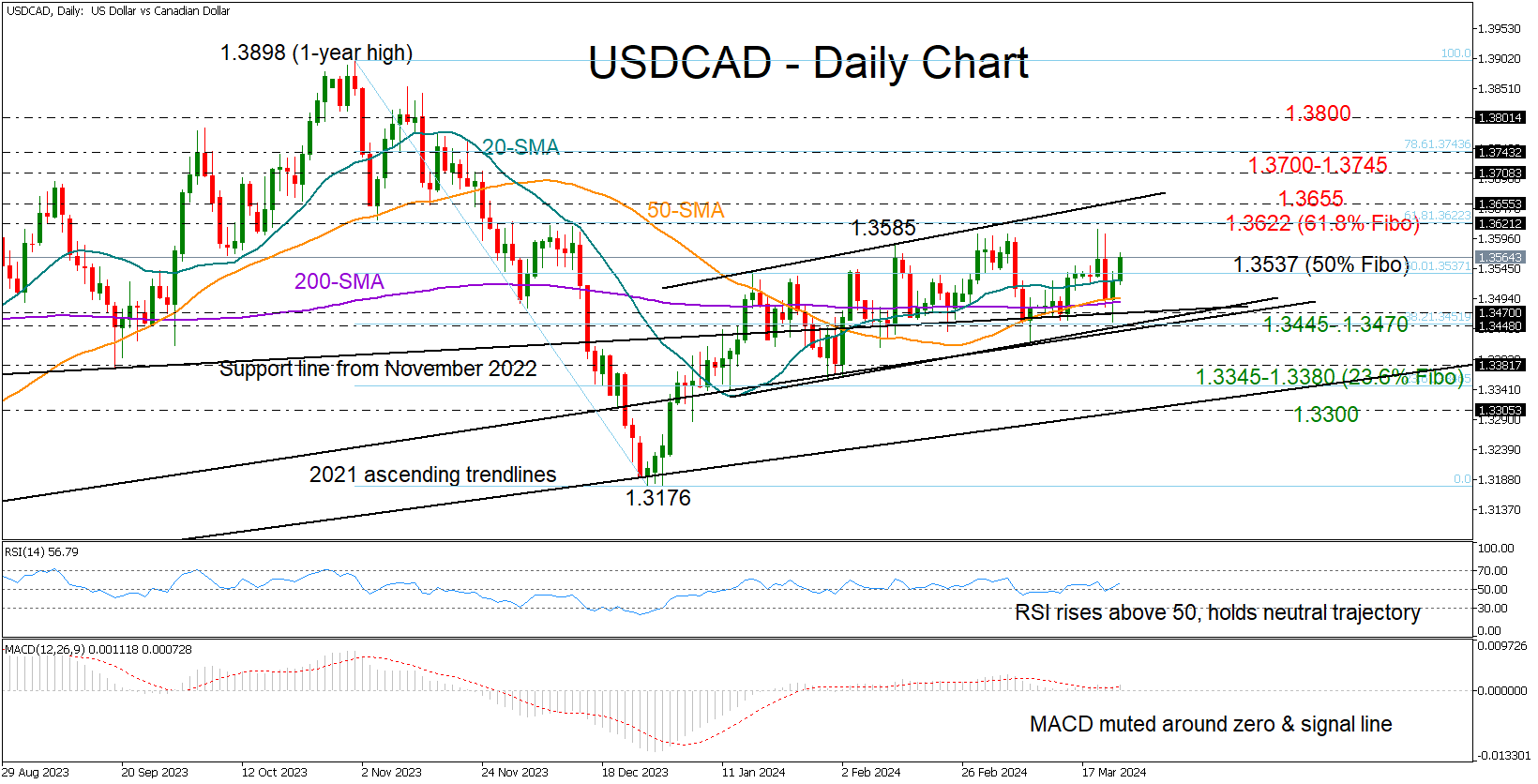

Is There Stronger Bullish Trend for USDCAD?

- USDCAD switches back to gains, surpasses SMAs

- Technical signals cannot warrant a bullish channel breakout

USDCAD successfully recovered from a flash drop to 1.3454 and closed Thursday’s session above the 50- and 200-day SMAs, maintaining its position within the short-term bullish channel. Consequently, the bulls piled in on Friday to drive the pair above the 20-day SMA and the 50% Fibonacci retracement of the November-December downtrend, which has been a key resistance zone since the start of the year.

The recent bullish accomplishments have raised expectations for further progress towards the upper boundary of the channel at 1.3655. However, the current neutral trend in the RSI and MACD does not inspire confidence. Prior to a channel breakout, the bulls will have to overcome the 61.8% Fibonacci mark of 1.3622. Should they exit the channel on the upside, resistance could initially develop somewhere within the 1.3700-1.3745 region, and then around 1.3800.

Conversely, if the pair sinks below the important 1.3445-1.3470 support area, it could seek shelter within the 1.3345-1.3380 territory, where the 23.6% Fibonacci number is placed. Even lower, the bears might push towards the ascending trendline, which connects the 2021 and 2022 lows at 1.3300.

Overall, the recent rise in USDCAD doesn’t provide enough technical evidence for an immediate extension towards the upper boundary of the channel.