Sample Category Title

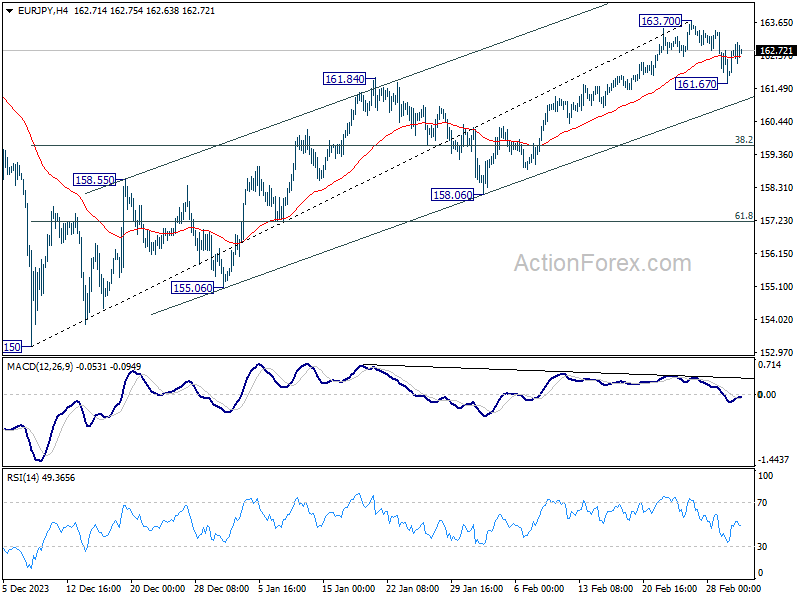

EUR/JPY Weekly Outlook

EUR/JPY dipped to 161.67 last week but recovered since then. Initial bias is turned neutral this week first. Another decline is mildly in favor as long as 163.70 resistance holds. Below 161.67 will target channel support (now at 161.11). However, firm break of 163.70 will resume the rally from 153.15 to retest 164.29 high.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 148.38 resistance turned support holds.

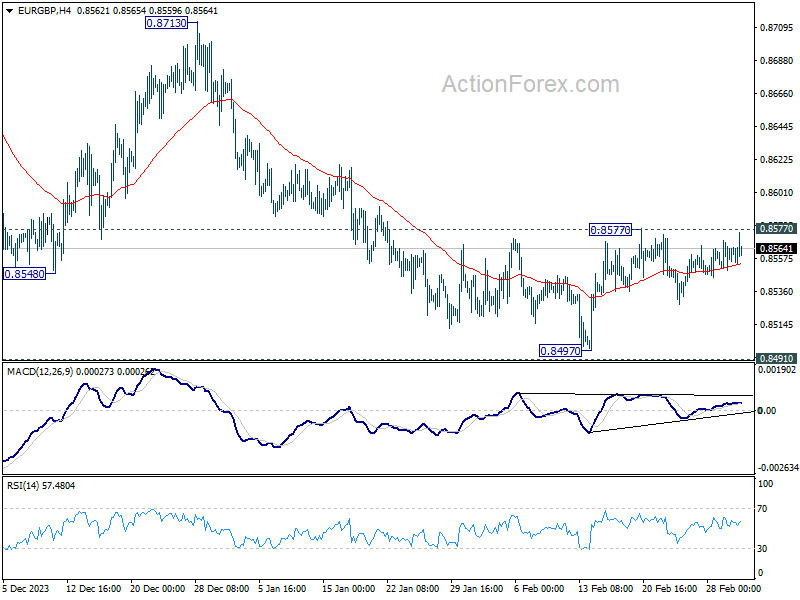

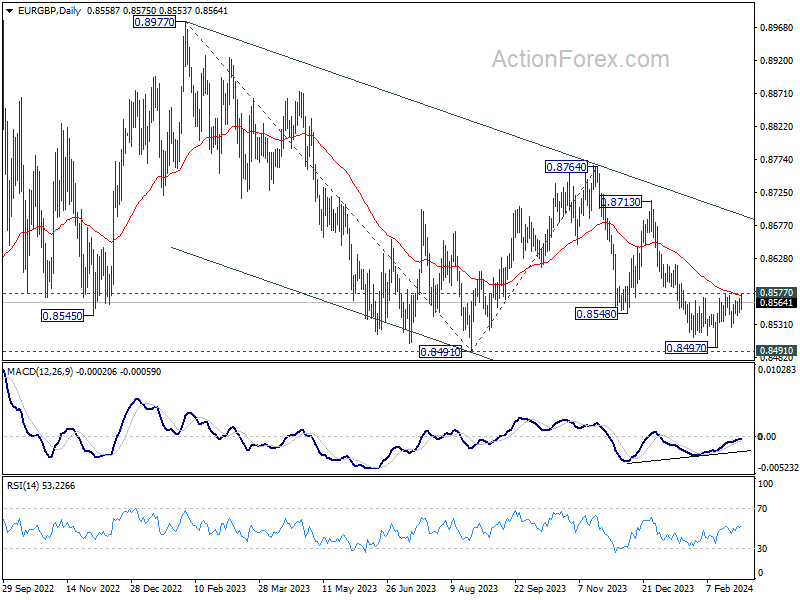

EUR/GBP Weekly Outlook

EUR/GBP recovered last week but failed to break through 0.8577 so far. Initial bias remains neutral this week first. Considering bullish convergence condition in D MACD, decisive break of 0.8577 and 55 D EMA (now at 0.8574) will argue that fall from 0.8764 has completed. Intraday bias will be back on the upside for rebound towards 0.8713 resistance. Nevertheless, firm break of 0.8491/7 support zone will confirm larger down trend resumption.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

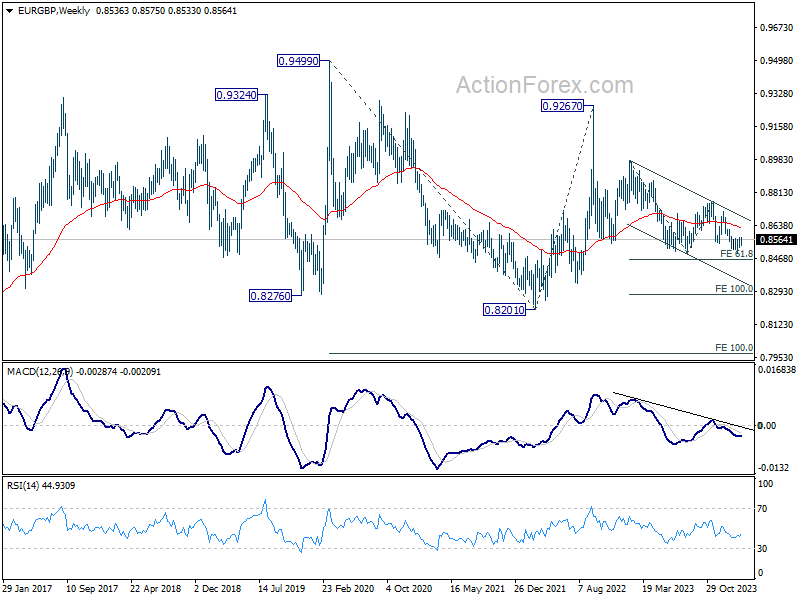

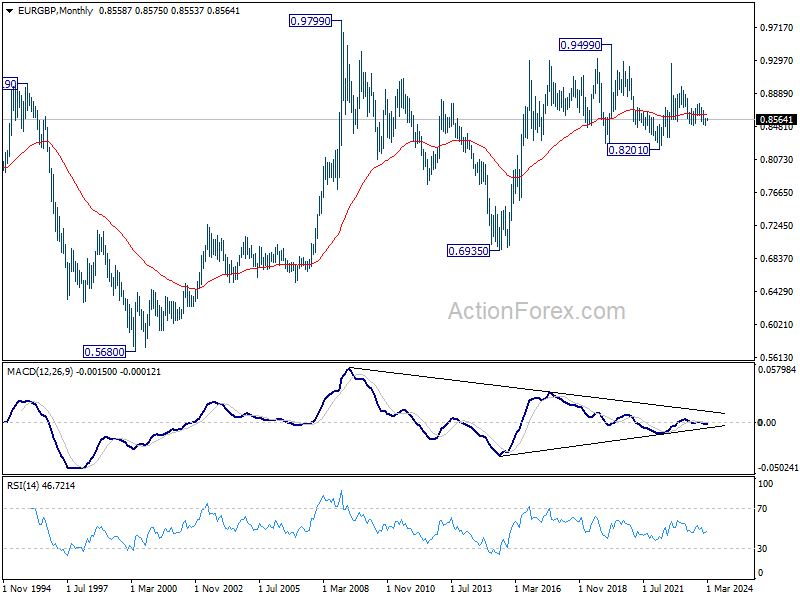

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

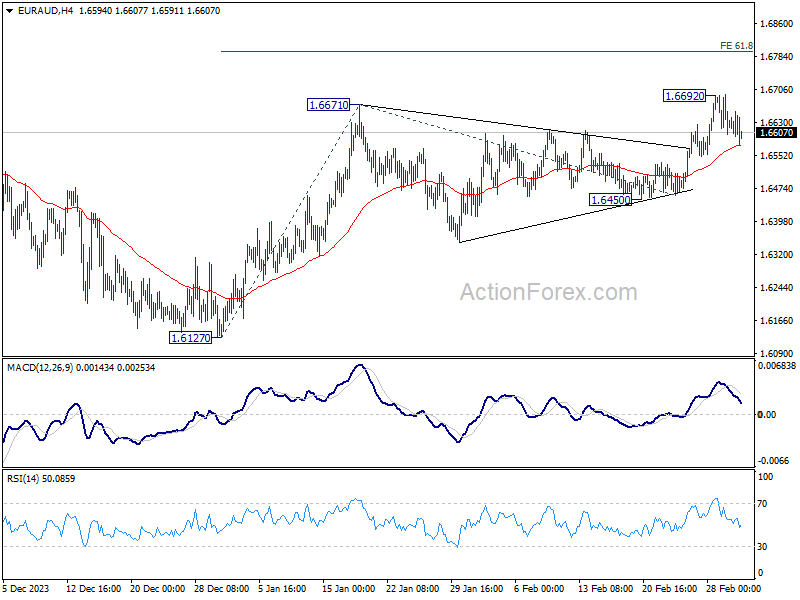

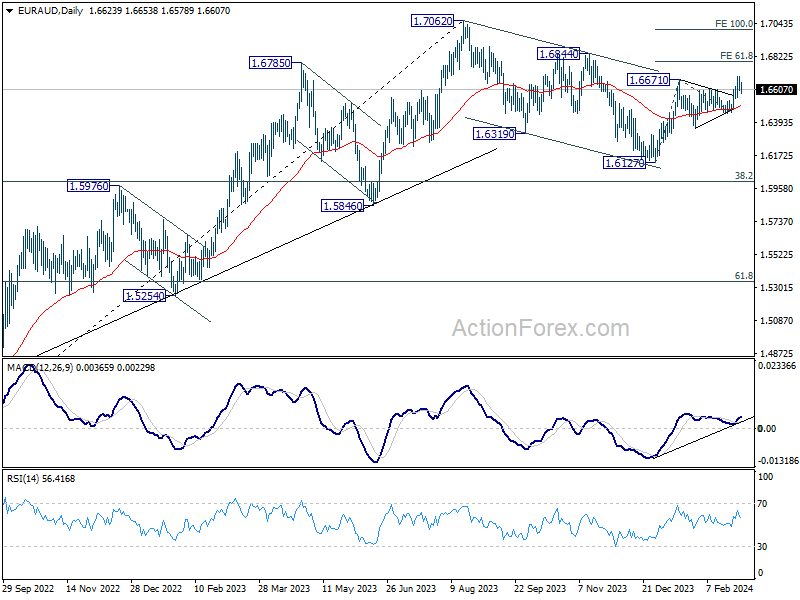

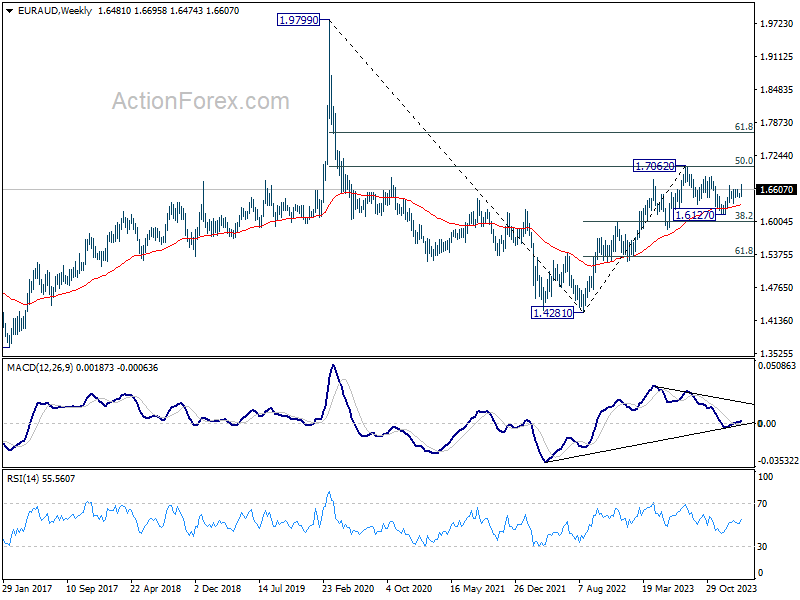

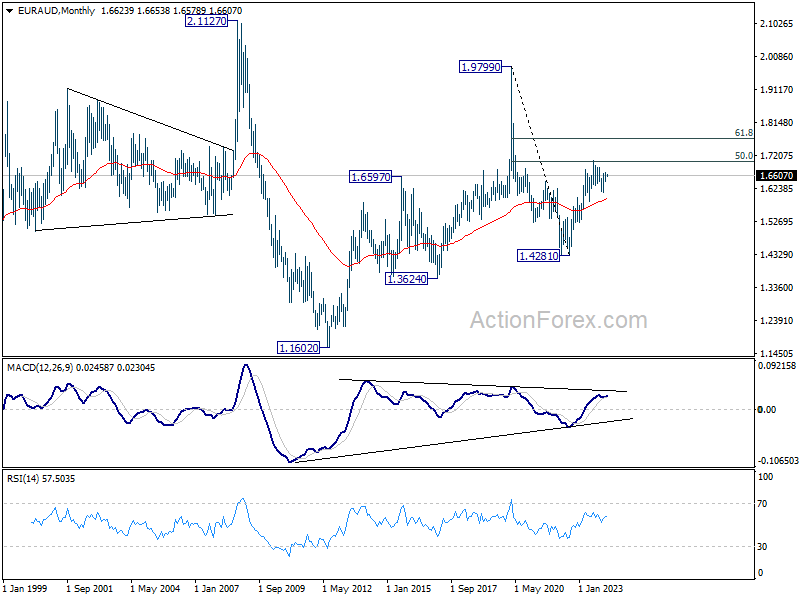

EUR/AUD Weekly Outlook

EUR/AUD's rebound from 1.6127 resumed last week and edged higher to 1.6692, but retreated since then. Initial bias stays neutral this week first. Current development suggests that whole correction from 1.7062 should have completed with three waves down to 1.6127. Further rally is expected as long as 1.6450 support holds. Above 1.6692 will target 61.8% projection of 1.6127 to 1.6671 from 1.6450 at 1.6786 next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5932) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

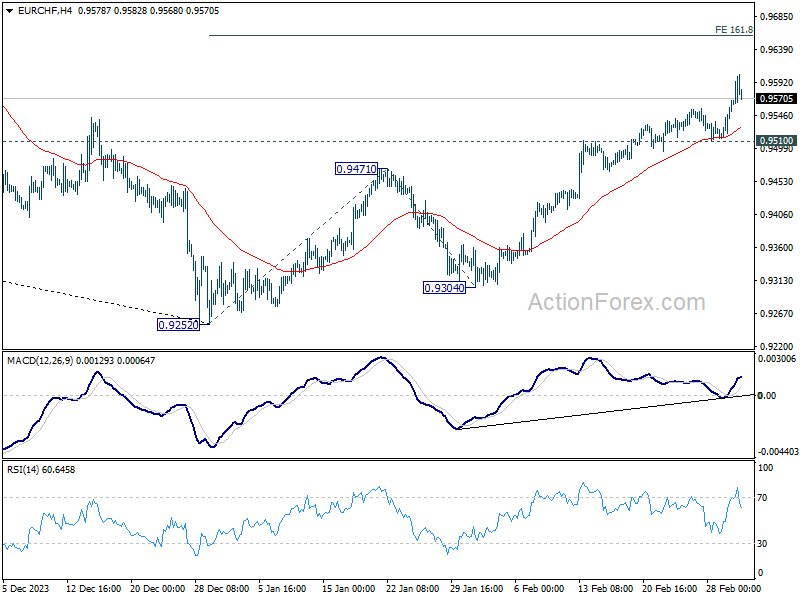

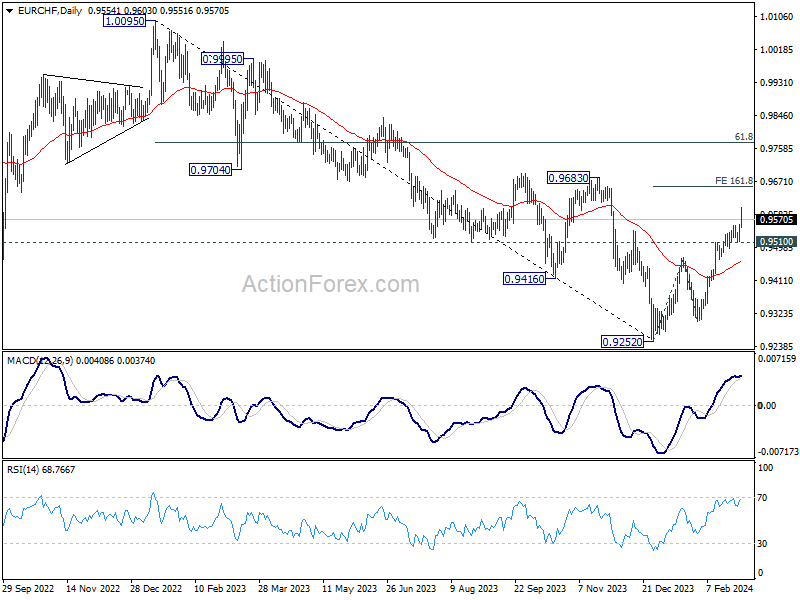

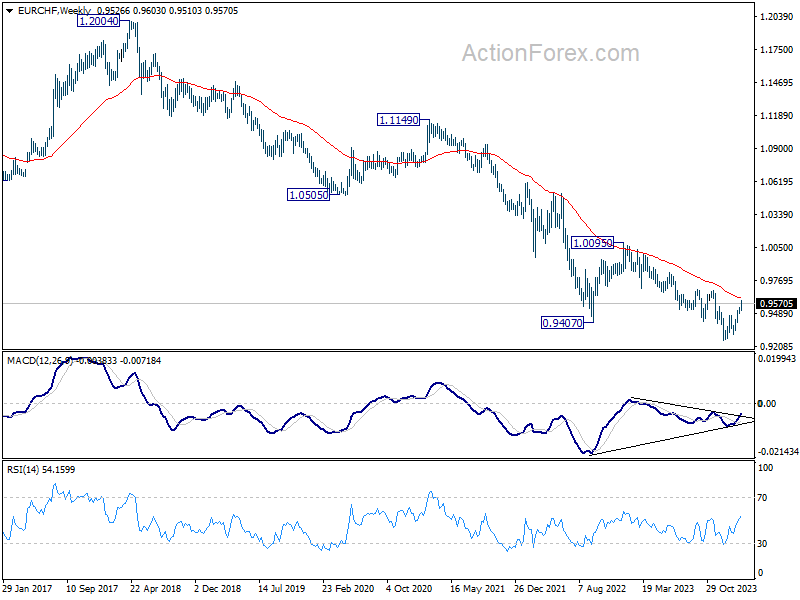

EUR/CHF Weekly Outlook

EUR/CHF's rally from 0.9252 continued last week and hit as high as 0.9603. Initial bias stays on the upside this week for 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. For now, further rally is expected as long as 0.9510 support holds, in case of retreat.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9622) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.9% retracement of 1.0095 to 0.9252 at 0.9773 and above.

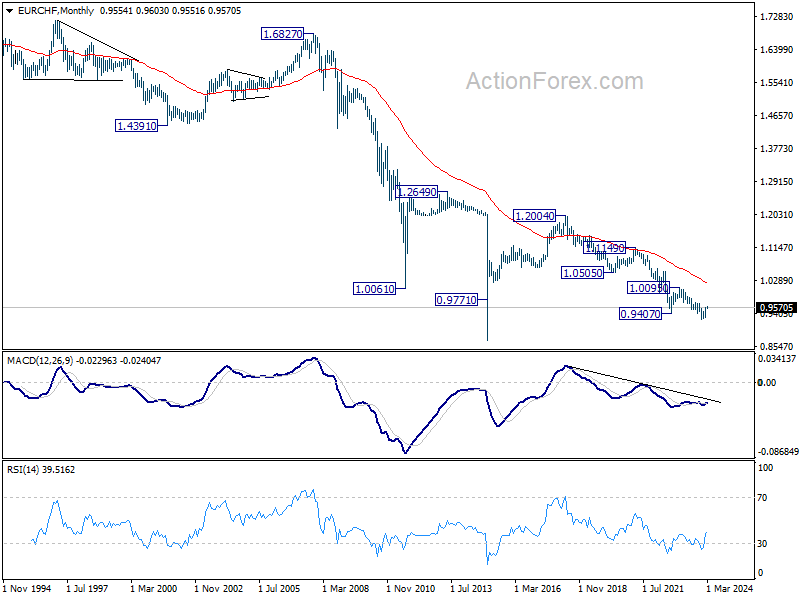

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 3/4 – 3/8

Monday, Mar 4, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q4 | -0.20% | -0.60% |

| 23:50 | JPY | Capital Spending Q4 | 2.90% | 3.40% |

| 23:50 | JPY | Monetary Base Y/Y Feb | 4.70% | 4.80% |

| 00:00 | AUD | TD Securities Inflation M/M Feb | 0.30% | |

| 00:30 | AUD | Building Permits M/M Jan | 4.00% | -9.50% |

| 07:30 | CHF | CPI M/M Feb | 0.50% | 0.20% |

| 07:30 | CHF | CPI Y/Y Feb | 1.10% | 1.30% |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | -10.8 | -12.9 |

| 23:30 | JPY | Tokyo CPI Y/Y Feb | 1.60% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Feb | 2.50% | 1.60% |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Feb | 3.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q4 | |

| Forecast: -0.20% | Previous: -0.60% | ||

| 23:50 | JPY | Capital Spending Q4 | |

| Forecast: 2.90% | Previous: 3.40% | ||

| 23:50 | JPY | Monetary Base Y/Y Feb | |

| Forecast: 4.70% | Previous: 4.80% | ||

| 00:00 | AUD | TD Securities Inflation M/M Feb | |

| Forecast: | Previous: 0.30% | ||

| 00:30 | AUD | Building Permits M/M Jan | |

| Forecast: 4.00% | Previous: -9.50% | ||

| 07:30 | CHF | CPI M/M Feb | |

| Forecast: 0.50% | Previous: 0.20% | ||

| 07:30 | CHF | CPI Y/Y Feb | |

| Forecast: 1.10% | Previous: 1.30% | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | |

| Forecast: -10.8 | Previous: -12.9 | ||

| 23:30 | JPY | Tokyo CPI Y/Y Feb | |

| Forecast: | Previous: 1.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Feb | |

| Forecast: 2.50% | Previous: 1.60% | ||

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Feb | |

| Forecast: | Previous: 3.10% | ||

Tuesday, Mar 5, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Feb | 1.40% | |

| 00:30 | AUD | Current Account Balance (AUD) Q4 | 5.0B | -0.2B |

| 01:45 | CNY | Caixin Services PMI Feb | 52.9 | 52.7 |

| 07:45 | EUR | France Industrial Output M/M Jan | -0.10% | 1.10% |

| 08:45 | EUR | Italy Services PMI Feb | 52.3 | 51.2 |

| 08:50 | EUR | France Services PMI Feb F | 48 | 48 |

| 08:55 | EUR | Germany Services PMI Feb F | 48.2 | 48.2 |

| 09:00 | EUR | Eurozone Services PMI Feb F | 50 | 50 |

| 09:30 | GBP | Services PMI Feb F | 54.3 | 54.3 |

| 10:00 | EUR | Eurozone PPI M/M Jan | -0.10% | -0.80% |

| 10:00 | EUR | Eurozone PPI Y/Y Jan | -10.60% | |

| 14:45 | USD | Services PMI Feb F | 51.3 | 51.3 |

| 15:00 | USD | ISM Services PMI Feb | 0.30% | 53.4 |

| 15:00 | USD | Factory Orders M/M Jan | -2.80% | 0.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Feb | |

| Forecast: | Previous: 1.40% | ||

| 00:30 | AUD | Current Account Balance (AUD) Q4 | |

| Forecast: 5.0B | Previous: -0.2B | ||

| 01:45 | CNY | Caixin Services PMI Feb | |

| Forecast: 52.9 | Previous: 52.7 | ||

| 07:45 | EUR | France Industrial Output M/M Jan | |

| Forecast: -0.10% | Previous: 1.10% | ||

| 08:45 | EUR | Italy Services PMI Feb | |

| Forecast: 52.3 | Previous: 51.2 | ||

| 08:50 | EUR | France Services PMI Feb F | |

| Forecast: 48 | Previous: 48 | ||

| 08:55 | EUR | Germany Services PMI Feb F | |

| Forecast: 48.2 | Previous: 48.2 | ||

| 09:00 | EUR | Eurozone Services PMI Feb F | |

| Forecast: 50 | Previous: 50 | ||

| 09:30 | GBP | Services PMI Feb F | |

| Forecast: 54.3 | Previous: 54.3 | ||

| 10:00 | EUR | Eurozone PPI M/M Jan | |

| Forecast: -0.10% | Previous: -0.80% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Jan | |

| Forecast: | Previous: -10.60% | ||

| 14:45 | USD | Services PMI Feb F | |

| Forecast: 51.3 | Previous: 51.3 | ||

| 15:00 | USD | ISM Services PMI Feb | |

| Forecast: 0.30% | Previous: 53.4 | ||

| 15:00 | USD | Factory Orders M/M Jan | |

| Forecast: -2.80% | Previous: 0.20% | ||

Wednesday, Mar 6, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q4 | 0.30% | 0.20% |

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | 21.0B | 22.2B |

| 09:30 | GBP | Construction PMI Feb | 49.2 | 48.8 |

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | 0.10% | -1.10% |

| 13:15 | USD | ADP Employment Change Feb | 150K | 107K |

| 13:30 | CAD | Labor Productivity Q/Q Q4 | -0.10% | -0.80% |

| 14:45 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% |

| 15:00 | USD | Fed's Chair Powell testifies | ||

| 15:00 | USD | Wholesale Inventories Jan F | -0.10% | -0.10% |

| 15:00 | CAD | Ivey PMI Feb | 54.4 | |

| 15:30 | USD | Crude Oil Inventories | 4.2M | |

| 19:00 | USD | Fed's Beige Book | ||

| 21:45 | NZD | Manufacturing Sales Q4 | -2.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q4 | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | |

| Forecast: 21.0B | Previous: 22.2B | ||

| 09:30 | GBP | Construction PMI Feb | |

| Forecast: 49.2 | Previous: 48.8 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | |

| Forecast: 0.10% | Previous: -1.10% | ||

| 13:15 | USD | ADP Employment Change Feb | |

| Forecast: 150K | Previous: 107K | ||

| 13:30 | CAD | Labor Productivity Q/Q Q4 | |

| Forecast: -0.10% | Previous: -0.80% | ||

| 14:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 15:00 | USD | Fed's Chair Powell testifies | |

| Forecast: | Previous: | ||

| 15:00 | USD | Wholesale Inventories Jan F | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 15:00 | CAD | Ivey PMI Feb | |

| Forecast: | Previous: 54.4 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 4.2M | ||

| 19:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Manufacturing Sales Q4 | |

| Forecast: | Previous: -2.70% | ||

Thursday, Mar 7, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Feb | 11.50B | 10.96B |

| 03:00 | CNY | Trade Balance (USD) Feb | 110.3B | 75.3B |

| 03:00 | CNY | Trade Balance (CNY) Feb | 620B | 541B |

| 06:45 | CHF | Unemployment Rate Feb | 2.20% | 2.20% |

| 07:00 | EUR | Germany Factory Orders M/M Jan | -6.00% | 8.90% |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Feb | 662B | |

| 13:15 | EUR | ECB Main Refinancing Rate | 4.50% | 4.50% |

| 13:30 | CAD | Trade Balance (CAD) Jan | 0.3B | -0.3B |

| 13:30 | CAD | Building Permits M/M Jan | 2.10% | -14% |

| 13:30 | USD | Initial Jobless Claims (Mar 1) | 212K | 215K |

| 13:30 | USD | Trade Balance (USD) Jan | -63.2B | -62.2B |

| 13:30 | USD | Nonfarm Productivity Q4 | 3.20% | 3.20% |

| 13:30 | USD | Unit Labor Costs Q4 | 0.50% | 0.50% |

| 13:45 | EUR | ECB Press Conference | ||

| 15:00 | USD | Fed's Chair Powell testifies | ||

| 15:30 | USD | Natural Gas Storage | -96B | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | 1% | |

| 23:30 | JPY | Overall Household Spending Y/Y Jan | -4.30% | -2.50% |

| 23:50 | JPY | Bank Lending Y/Y Feb | 3.10% | |

| 23:50 | JPY | Current Account (JPY) Jan | 2.07T | 1.81T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Feb | |

| Forecast: 11.50B | Previous: 10.96B | ||

| 03:00 | CNY | Trade Balance (USD) Feb | |

| Forecast: 110.3B | Previous: 75.3B | ||

| 03:00 | CNY | Trade Balance (CNY) Feb | |

| Forecast: 620B | Previous: 541B | ||

| 06:45 | CHF | Unemployment Rate Feb | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 07:00 | EUR | Germany Factory Orders M/M Jan | |

| Forecast: -6.00% | Previous: 8.90% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Feb | |

| Forecast: | Previous: 662B | ||

| 13:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 13:30 | CAD | Trade Balance (CAD) Jan | |

| Forecast: 0.3B | Previous: -0.3B | ||

| 13:30 | CAD | Building Permits M/M Jan | |

| Forecast: 2.10% | Previous: -14% | ||

| 13:30 | USD | Initial Jobless Claims (Mar 1) | |

| Forecast: 212K | Previous: 215K | ||

| 13:30 | USD | Trade Balance (USD) Jan | |

| Forecast: -63.2B | Previous: -62.2B | ||

| 13:30 | USD | Nonfarm Productivity Q4 | |

| Forecast: 3.20% | Previous: 3.20% | ||

| 13:30 | USD | Unit Labor Costs Q4 | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 13:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 15:00 | USD | Fed's Chair Powell testifies | |

| Forecast: | Previous: | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -96B | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | |

| Forecast: | Previous: 1% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Jan | |

| Forecast: -4.30% | Previous: -2.50% | ||

| 23:50 | JPY | Bank Lending Y/Y Feb | |

| Forecast: | Previous: 3.10% | ||

| 23:50 | JPY | Current Account (JPY) Jan | |

| Forecast: 2.07T | Previous: 1.81T | ||

Friday, Mar 8, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Jan P | 110.2 | |

| 05:00 | JPY | Eco Watchers Survey: Current Feb | 50.6 | 50.2 |

| 07:00 | EUR | Germany Industrial Production M/M Jan | 0.50% | -1.60% |

| 07:00 | EUR | Germany PPI M/M Jan | -0.10% | -1.20% |

| 07:00 | EUR | Germany PPI Y/Y Jan | -8.60% | |

| 07:45 | EUR | France Trade Balance (EUR) Jan | -6.5B | -6.8B |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 | 0.00% | 0.00% |

| 13:30 | USD | Nonfarm Payrolls Feb | 200K | 353K |

| 13:30 | USD | Unemployment Rate Feb | 3.70% | 3.70% |

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.20% | 0.60% |

| 13:30 | CAD | Capacity Utilization Q4 | 79.90% | 79.70% |

| 13:30 | CAD | Net Change in Employment Feb | 20.0K | 37.3K |

| 13:30 | CAD | Unemployment Rate Feb | 5.80% | 5.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Jan P | |

| Forecast: | Previous: 110.2 | ||

| 05:00 | JPY | Eco Watchers Survey: Current Feb | |

| Forecast: 50.6 | Previous: 50.2 | ||

| 07:00 | EUR | Germany Industrial Production M/M Jan | |

| Forecast: 0.50% | Previous: -1.60% | ||

| 07:00 | EUR | Germany PPI M/M Jan | |

| Forecast: -0.10% | Previous: -1.20% | ||

| 07:00 | EUR | Germany PPI Y/Y Jan | |

| Forecast: | Previous: -8.60% | ||

| 07:45 | EUR | France Trade Balance (EUR) Jan | |

| Forecast: -6.5B | Previous: -6.8B | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 13:30 | USD | Nonfarm Payrolls Feb | |

| Forecast: 200K | Previous: 353K | ||

| 13:30 | USD | Unemployment Rate Feb | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 13:30 | USD | Average Hourly Earnings M/M Feb | |

| Forecast: 0.20% | Previous: 0.60% | ||

| 13:30 | CAD | Capacity Utilization Q4 | |

| Forecast: 79.90% | Previous: 79.70% | ||

| 13:30 | CAD | Net Change in Employment Feb | |

| Forecast: 20.0K | Previous: 37.3K | ||

| 13:30 | CAD | Unemployment Rate Feb | |

| Forecast: 5.80% | Previous: 5.70% | ||

The Weekly Bottom Line: Coming Off the Boil?

U.S. Highlights

- January’s personal and income spending report landed just where it was expected to, with the only surprise coming from a bigger than expected lift from nominal personal income growth.

- The Fed’s preferred measure of inflation, core personal consumption expenditure prices, cooled to 2.8% year-on-year, with near-term trends suggesting it has room to fall.

- A weaker-than-expected ISM manufacturing report helped support the notion that demand is cooling.

Canadian Highlights

- If the Bank of Canada (BoC) needed another signal that its past rate hikes were working, it got it this week with the release of fourth quarter GDP.

- The economy returned to growth, but the pace remained in the doldrums for a country whose population grew by more than 3%.

- This below-trend pace of growth is exactly what the BoC wants to see for it to be convinced that inflation will continue to decelerate toward its 2% target.

U.S. – Coming Off the Boil?

January’s personal and income spending report landed just where it was expected to, with the only surprise coming from a bigger lift from nominal personal income growth. The as-expected print comes on the heels of updated GDP data that showed consumer spending closed out last year at an even better pace than originally thought. Most importantly, an upside inflation surprise was averted in January, allowing markets to let out a sigh of relief. After the data release Treasury yields tumbled and equities rallied. The data showed that price pressures continue to cool off. However, for a cautious Fed more progress will have to be made, leaving the first policy rate cuts a ways away.

First and foremost, this week’s personal income and spending report showed real personal consumption expenditures (PCE) pulled back 0.1% in January after healthy gains in November and December. Not a big surprise after January’s retail sales report showed a significant pullback. With some weather related factors weighing on demand it’s likely that this was more of a one-off than a new trend and February will likely show some bounce back.

Stronger-than- expected growth in personal income was largely a result of a larger cost of living adjustment in social security payments (and other government transfers), and the inflation adjusted real personal disposable income (PDI) measure showed no growth. Looking forward, this is what we’re interested in, as the downbeat month shaved two percentage points off of annual real PDI growth, bringing it down to 2.1% year-on-year. A deceleration in total real income growth is going to be part of the formula that cools the relentless consumer demand we’ve seen from the U.S. since the pandemic.

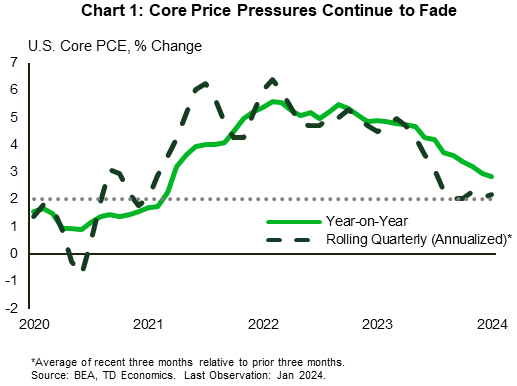

Of course, the Fed isn’t after just slowing the economy, but bringing demand and supply into better balance to tame inflation. On this front, yesterday’s report brought welcome news. The Fed’s preferred measure of inflation (core PCE) cooled to 2.8% year-on-year. Yes, still above the Fed’s target, but this is owing to base-effects from last year. Take a closer look at any near-term metrics and inflation is looking a lot closer to target. The three-month and six-month rates are at 2.6% and 2.5% (annualized), respectively. Smooth out some of the month-to-month noise in the series by taking a rolling quarterly rate of change, and core PCE prices have been advancing between 2% and 2.3% (annualized) since last September (Chart 1).

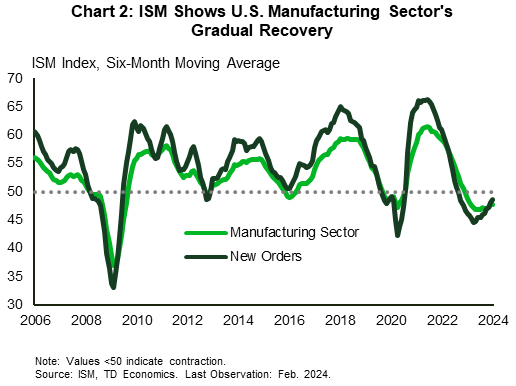

February’s ISM manufacturing report closed out the week, and supported the notion that demand is coming off a boil. With a 47.8 print for the month, the reading fell well short of market expectations and signaled that the recovery in the manufacturing sector is progressing rather slowly (Chart 2). Moreover, new manufacturing orders show that demand remains tepid.

For the Fed, these indicators come as signs that the relentless demand that powered the U.S. economy in late-2023 might be cooling off. Next Tuesday’s February ISM services report should shed light on the much larger services sector, while Fed Chair Jerome Powell’s testimony on Wednesday will hopefully give us a better sense of how the Fed is viewing these latest numbers.

Canada – Another Quarter of Weak Growth

If the Bank of Canada (BoC) needed another signal that its rate hikes were working, it got it this week. Fourth quarter GDP posted yet another quarter of sub-trend economic growth. That makes it three quarters in a row. Can it go for one more? Markets seem to think so, as firmer pricing around a June/July rate cut imply little hope for any forthcoming economic acceleration.

The details of the GDP report left little room for optimism. Yes, real GDP did increase by +1% quarter-on-quarter annualized (q/q) in the fourth quarter, after posting a negative print over the summer of 2023. And yes, this was above the BoC's expectation for no growth. But, the pace of growth is still not much to write home about, coming in well below the trend pace for an economy that saw its population grow by +3% during the quarter.

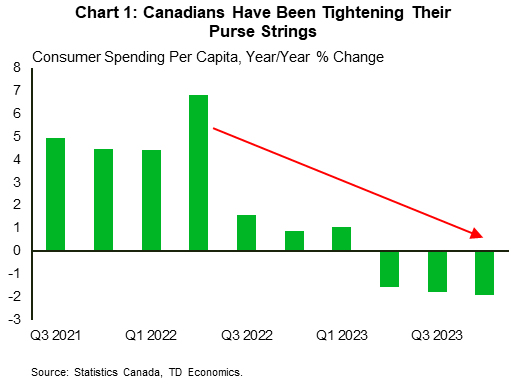

Consumer spending was tepid once again. If it wasn't for the slow loosening of automotive supply chains, which has delayed the delivery of past car purchases, consumer spending would have shown effectively no growth over the last six months. Even worse, spending per capita contracted for the fifth time in the past six quarters, keeping the annual pace of growth firmly in the doldrums (Chart 1).

The only real positive in the report came from exports, which were by far, the biggest contributor to economic growth in the fourth quarter. Canada has benefitted from its trade linkages with the U.S., which has grown three times faster than Canada over 2023. Strong American demand for Canadian exports has provided a nice offset to our domestic economic slowdown. This could have some staying power as well. Energy exports have been in demand, and with new pipelines coming online soon, this new capacity appears to be arriving at just the right time.

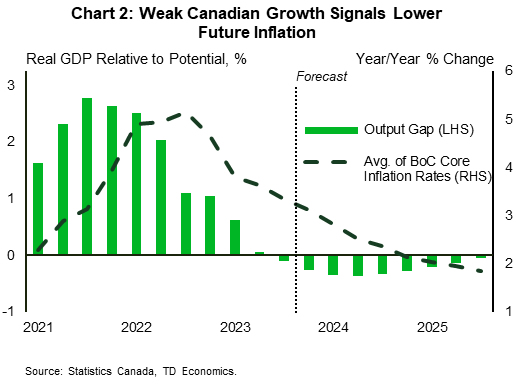

How does all this impact the BoC, which is set to make its next interest rate decision next week? The short answer is, not much. Outside of the one-off surge in spending in early 2023, Canadian economic growth has been abysmal ever since the BoC started raising rates in 2022. This period of below-trend growth is exactly what the BoC was hoping for. The central bank has been able to steer the economy from a state of excess demand – where consumer demand outpaced supply – to a state of greater balance. In economics jargon, the BoC has closed the output gap. Now, economic theory would tell you that when the output gap closes, and goes negative like it did six months ago, inflation will decelerate (Chart 2). From this lens, the wheels are in motion for inflation to move further towards the BoC's 2% target. It is just a matter of time.

Luckily for the BoC, it has been gifted a little more time before it needs to cut rates. The fact that the economy has eked out modest, but still positive gains, means that a soft landing is still the base-case scenario. This allows the BoC to sit back over the next couple of months and ensure that inflation continues to grind lower. We think it will, which will allow the BoC to make its first rate cut in June.

Weekly Economic & Financial Commentary: Economic Growth Continues Despite Downbeat Data

Summary

United States: Economic Growth Continues Despite Downbeat Data

- Economic data were downbeat this week, as downward revisions took some of the shine out of the marquee headline numbers. Durable goods orders declined, consumer confidence took a dip and the PCE deflator accelerated, bringing real personal spending into the red. Despite the somewhat weak start to Q1, economic growth continues to trek along.

- Next week: ISM Services (Tue.), Trade Balance (Thu.), Employment (Fri.)

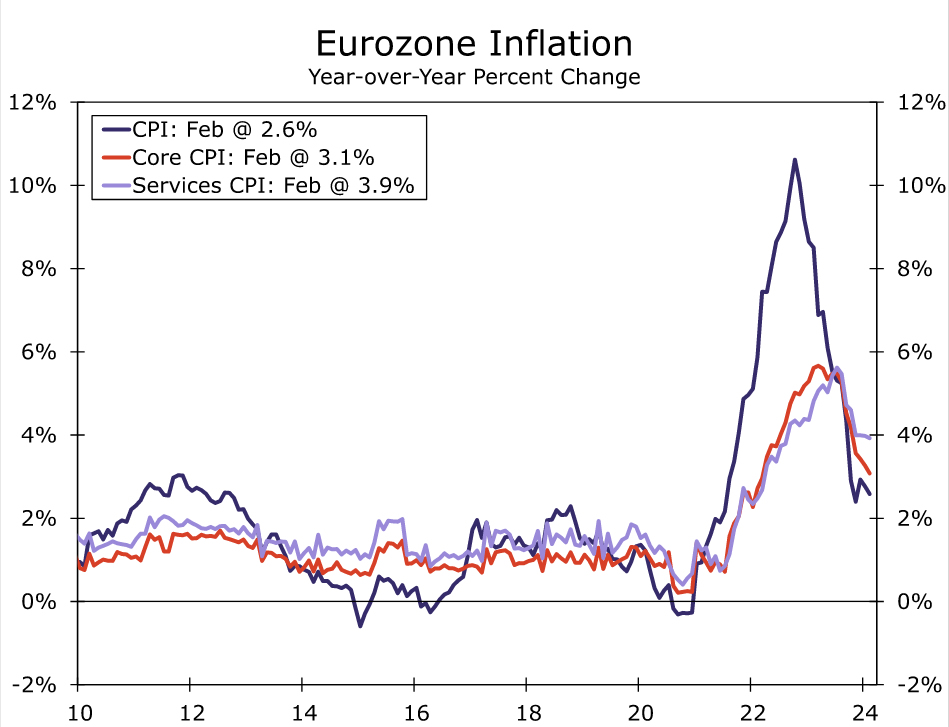

International: Eurozone Inflation Stays Sticky

- Eurozone disinflation continued in February; however, CPI surprised to the upside last month, leaving markets questioning when the ECB will shift to rate cuts. Sticky inflation and elevated wage growth, in our view, is now likely to keep the ECB on the sidelines until the middle of 2024.

- Next week: Bank of Canada (Wed.), European Central Bank (Thu.), Mexico CPI (Thu.)

Credit Market Insights: Mostly Good in the Neighborhood

- Earlier this month, the Federal Reserve Bank of New York released its Quarterly Report on Household Debt and Credit encompassing the fourth quarter of 2023. The level of household debt outstanding sits $3.4 trillion above where it stood prior to the COVID-19 pandemic, or about 24% higher. Households have by and large been able to service their debt obligations even as the Fed’s tightening cycle has raised interest expenses on households.

Topic of the Week: “Super Core”: The Inflation Measure du Jour

- For much of this cycle, “super core” inflation was the talk of the town. Since its introduction, however, attention on the "super core" from Fed officials, analysts and market participants has seemed to dwindle. Why did “super core” ascend into the limelight and then fade from view? This week, we chronicle the rise and fall of interest in the "super core" and provide an update to its current run-rate.

BoC to Deliver Another Dovish Hold, Unemployment Rate to Tick Higher

The Bank of Canada is widely expected to maintain the overnight rate steady again at its meeting on Wednesday. An announcement on the ending of quantitative tightening is unlikely but we expect that to follow later in April. Over past meetings, the BoC has been gradually and cautiously moving towards a more dovish stance. Language around the need to hike rates further was already dropped in January and is unlikely to reappear in the statement next week. The central bank will instead continue to highlight softening in aggregate demand while reiterating that inflation pressures, although easing are still a risk.

Economic data since the last monetary policy meeting in January largely confirmed the weakening of the Canadian economy. The 1% annualized increase in gross domestic product in Q4 2023 was above the flat reading that the BoC expected. But details were much softer with growth in Q4 coming almost entirely from net exports. Domestic consumers and businesses on the other hand continued to pull back spending and investment activities. GDP growth was, again, slower on a per capita basis as population growth outpaced output for a sixth consecutive quarter.

We expect February labour market data released on Friday after the BoC’s decision to show another gain in employment. It will however not be large enough to prevent an increase in the unemployment rate to 5.9% as hiring demand keeps falling short of the rising supply of workers. Labour market numbers for January were firmer than expected with wage growth remaining high. But lower job openings continue to highlight slowing labour demand. Other Statistics Canada estimates of wage growth derived from business payrolls submissions have slowed more significantly. The silver lining of all the softening in the economy is that inflation pressures will likely continue to ease rather than reaccelerate. Our base case continues to assume the BoC will start moving the overnight rate lower in June after more data confirming easing inflation back towards target.

Week ahead data watch:

January’s Canadian trade data is likely to show monthly declines in both export and exports with rail carloadings (-7.7%)— contracting sharply that month. Oil prices went up 2.8%, and that will impact the value of energy exports and imports. Overall, we expect the trade deficit ($700 million) to widen from the prior month.

The U.S. trade balance (US$-63.8B) likely widened in January given the goods deficits from the advance trade report increased by US$2.3B. Much of that was driven by higher imports of autos, and capital goods.

We expect February U.S. payroll numbers to show another solid employment gain, with growth mainly coming from the leisure and hospitality, health care, and government sectors. We expect the unemployment rate to hold steady at 3.7%.

European Central Bank Gravitating Toward A Mid-Year Rate Cut

Summary

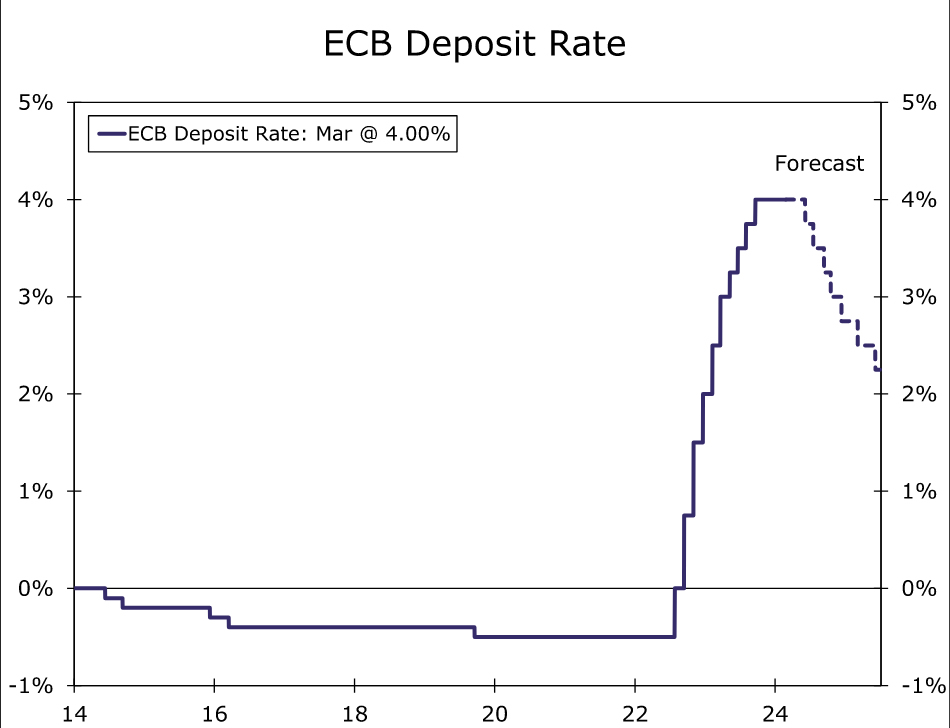

The Eurozone economy faced a particularly challenging period during the second half of 2023, with the region only narrowly avoiding a technical recession. Given the challenging growth environment, the European Central Bank (ECB) ended its tightening cycle with a final 25 bps rate hike in September last year and has, since early 2024, indicated the next move is likely to be a rate cut. The outlook for ECB monetary easing has been fluid, with expectations for an initial ECB rate cut at times fluctuating between April and June. That said, firmer Eurozone PMI surveys, a still-gradual disinflation process, and the weight of ECB policy rhetoric have seen expected rate cut timing shift more solidly towards June. In that context, we now also expect the ECB will begin its easing cycle with a 25 bps Deposit rate cut to 3.75% at its June monetary policy announcement.

Eurozone Economy Shows Tentative Signs of Stabilization

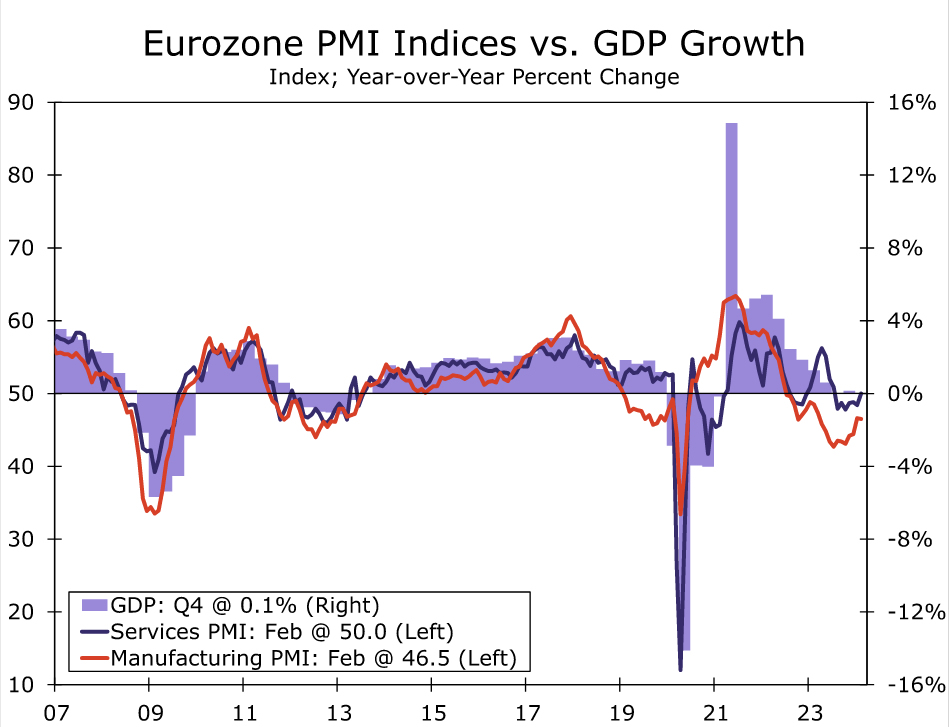

One of the most significant data releases since the European Central Bank's (ECB) most recent policy announcement was the Eurozone PMI surveys for February. Of particular note, the February service sector PMI rose more than expected to 50.0, from 48.4 in January. That saw the services PMI exit contraction territory for the first time since July of last year. Service sector sentiment for the region's largest economies was also favorable, as Germany's services PMI rose to 48.2 and France's services PMI rose to 48.0. The news from the Eurozone manufacturing PMI was not as upbeat, as that index unexpectedly eased to 46.5 in February from 46.6 in January, driven by weakness in German manufacturing. Still, with the service sector a much more sizable portion of the overall economy, the Eurozone composite PMI also rose to 48.9 in February, from 47.9 the prior month. Although not as significant as these headline figures, the details of the February PMI survey also hinted at lingering inflation pressures. The report noted that growth of average input costs across producers of goods and providers of services accelerated for a second successive month to reach the highest level since last May. The report also said that selling price inflation likewise accelerated, up for a fourth month running in February to also hit the highest level since last May.

Other confidence surveys since the ECB's latest announcement are more mixed. At a national level, Germany's February IFO business confidence index rose to 85.5, but French business confidence and Italian economic sentiment both fell in February. Meanwhile, the European Commission's Economic Sentiment Indicator for the Eurozone also fell to 95.4 in February, but that same survey showed the Employment Expectations Indicator edging up to 102.5 in February, a level historically consistent with positive jobs growth. That suggests steady Eurozone labor market trends can continue. In recent weeks, labor market indicators have shown continued employment growth in Q4 of 0.3% quarter-over-quarter and 1.3% year-over-year, and a January unemployment rate that fell to 6.4%, a record low. Taken together, the firming in the PMI indices and mixed readings from other sentiment surveys, along with steady labor market trends, offer early—albeit tentative—signs the Eurozone economy is stabilizing. At the margin, we think tentative economic stability has reduced the urgency for ECB monetary easing, and is a contributing factor to expectations for an initial ECB rate cut getting pushed back to mid-year.

Eurozone Inflation News Still Favorable, But How Long Will It Continue?

The other key pieces of Eurozone economic news since the ECB's latest policy announcement were inflation data for January and February. Those figures revealed some further progress on the disinflation front, albeit at a gradual pace. For the February CPI, headline inflation slowed to 2.6% year-over-year and core inflation slowed to 3.1% year-over-year. Service sector inflation remained somewhat sticky, easing only slightly to 3.9%. To be sure, the deceleration in annual inflation was flattered by base effects related to the large price increases that were seen in early 2023. Taking a closer and more granular look and price trends over the past six months, we note that the CPI excluding food and energy—which is close to but not identical to the official core CPI measure—has advanced at a 2.3% annualized pace. Thus even over this shorter time period, underlying inflation trends have moved closer to, but not yet converged, to the ECB's 2% inflation target. And likely of concern to ECB policymakers, services inflation has persisted over the past six months, rising at a 3.4% annualized pace during that period.

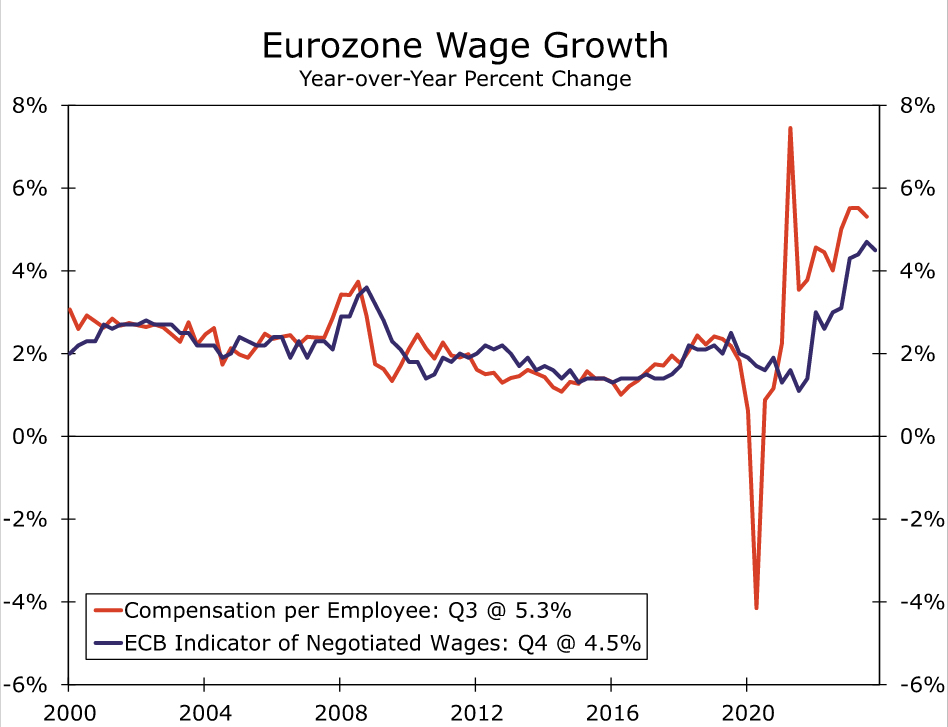

Another reservation regarding the inflation outlook, and one cited by several ECB policymakers, is the still-elevated pace of wage growth. The most up-to-date wage figures available on a Eurozone-wide basis is the ECB's indicator of negotiated wages. The negotiated wage index decelerated slightly to 4.5% year-over-year in Q4 from 4.7% in Q3 but, at least for now, suggests wage growth is at a level that is probably still too high to achieve the 2% inflation target on a sustained basis. The fact that the unemployment rate is at a record low perhaps reinforces concerns that wage growth may decelerate only gradually. It is against this backdrop, and despite the improving inflation trends of the past several months, that ECB policymakers have been wary of moving too aggressively in lowering interest rates, and have indicated an increasingly clear preference to see wage trends from early 2024 before making a decision to adjust interest rates. Those wage data for early 2024 will only be available in time for the ECB's June monetary policy announcement, and not for the ECB's April monetary policy announcement.

Chief among comments from policymakers have been those of ECB President Lagarde. Among her more recent comments, she said the ECB must be convinced that disinflation is sustainable and that Q1 wage data will be important for the ECB's assessment. Some other policymakers (Nagel, Holzmann, Schnabel) have cautioned against early rate cuts, while others have indicated a desire to see more wage data or even cited June as more likely timing for initial ECB easing. In the wake of these comments, market participants are now pricing in just 6 bps of rate cuts for the April meeting, and 24 bps of rate cuts for the June meeting.

Given current market pricing, it would likely take a proactive effort from ECB policymakers to accelerate the market's easing expectations and to allow for an April rate cut to become a more realistic possibility. That proactive guidance from ECB policymakers is something we view as a low probability outcome. Indeed, for those hoping for dovish elements from the ECB monetary policy announcement on 7 March, at best we expect the ECB to repeat it is “not there yet” on inflation, to perhaps caution against premature monetary easing, and to repeat that its preference is to see more wage data before adjusting its policy interest rate. At worst, we would not completely rule out more aggressive guidance in which the ECB takes the possibility of an April rate hike off the table. The other key element of the ECB's March monetary policy announcement to watch will be the central bank's updated economic projections. In the absence of a significant downward revision to its inflation forecast (in December, the ECB projected CPI inflation ex food and energy at 2.3% in 2025 and 2.1% in 2026), there would also be little reason for market participants to pull forward their expected rate cut timing. Since we view dovish policy guidance and/or a sharp downward revision to inflation forecasts as unlikely at the ECB's March announcement, and at the risk of adjusting our own forecasts with 'perfectly imperfect' timing, we now view an initial 25 bps Deposit Rate cut to 3.75% at the ECB June's monetary policy announcement as the most likely outcome.

Beyond the initial June move, we expect the ECB will keep lowering interest rates in steady 25 bps rate cut increments at the following meetings. We expect Eurozone economic growth to improve, but remain moderate overall. Meanwhile, we expect wage growth in particular, and price inflation to a lesser extent, to decelerate further as the year progresses. Should those economic trends transpire, we forecast the ECB will follow up with 25 bps rate cuts at the July, September, October and December meetings, which would see the Deposit Rate end 2024 at 2.75%. As the ECB's policy rate moves somewhat closer to a more neutral level and economic activity firms further in 2025, we expect a step down in the pace of ECB rate cuts to once per quarter next year. We forecast 25 bps Deposit Rate cuts in March, June and September 2025, which would see the ECB's policy rate reach a terminal level of 2.00% by late next year.

Week Ahead – ECB Decision and US Payrolls to Steal the Show

- Nonfarm payrolls and Powell’s testimony will be crucial for US dollar

- European Central Bank could set the stage for summer rate cuts

- Bank of Canada decision and UK budget announcement also in focus

Dollar braces for US payrolls

Riding high on a wave of US economic resilience, the dollar is currently the best-performing major currency this year, having gained nearly 3% against a basket of currencies in a couple of months.

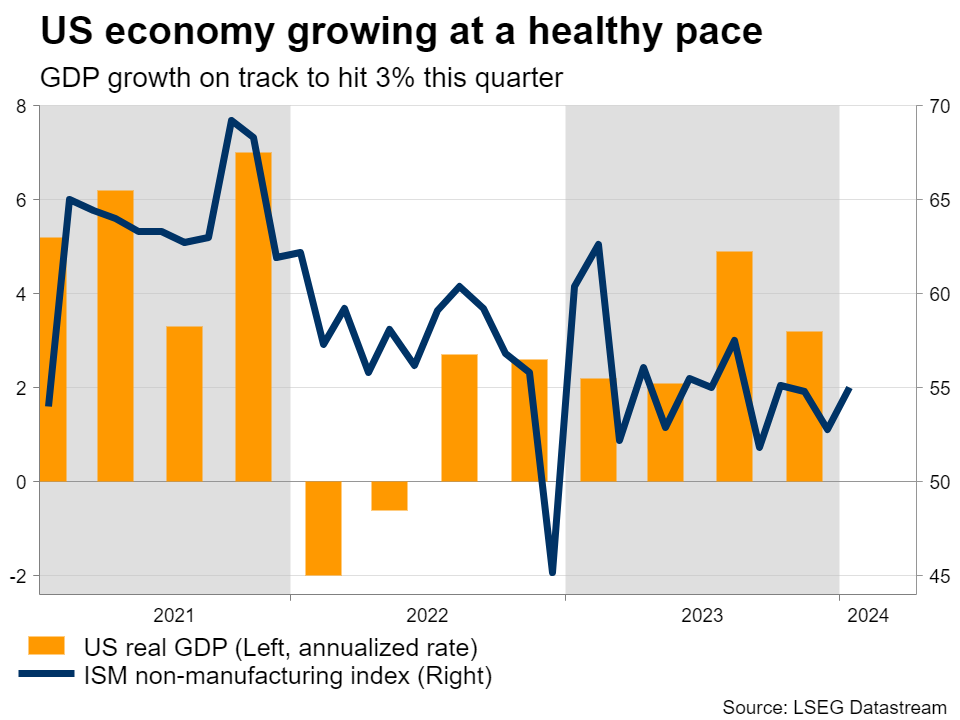

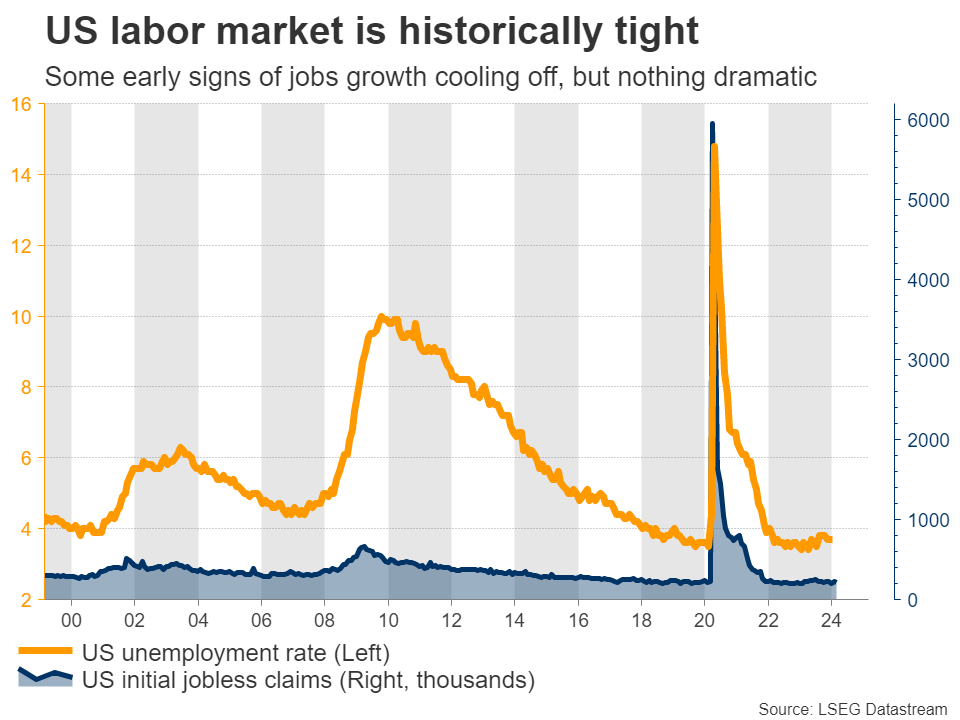

This stellar performance reflects an impressive US economy. Economic growth is running at a solid pace, the labor market remains historically tight, and inflation is not cooling as rapidly as investors had hoped.

With the economy still hot, traders have been forced to unwind bets of imminent Fed rate cuts. Markets are currently pricing just three rate cuts for this year, down from six cuts a few months ago. Hence, investors expect US interest rates to stay at higher levels for a while longer.

Grim economic prospects in the rest of the world have also benefited the dollar. The United Kingdom and Japan have fallen into technical recessions, the Eurozone is haunted by stagnant growth, and China is still dealing with the fallout in its property sector. As such, the alternatives to the dollar are not very attractive at this stage.

Next week’s events will help shape this narrative. The ball will get rolling on Tuesday with the release of the ISM services index for February, ahead of the private ADP employment data on Wednesday.

Meanwhile, Fed Chairman Powell will appear before Congress both on Wednesday and Thursday for his semiannual testimony. Investors usually focus on the Q&A session with lawmakers, where the Fed chief will be grilled on the economic outlook.

Of course, the main event will come on Friday, when the latest US employment report hits the markets. Economists expect another round of solid jobs numbers, which would reaffirm that the labor market remains in good shape. Some early indicators pointed to a slowdown in employment growth in February, but nothing dramatic.

Has the ECB fallen behind the curve?

In the Eurozone, the central bank is widely expected to keep rates steady on Thursday, so the spotlight will fall mostly on the updated economic projections and any signals by President Lagarde on the timing of rate cuts.

The euro area economy hit a wall last year, as high interest rates started to bite demand and governments dialed back their spending. Germany has been hit particularly hard, with a slowdown in global trade crippling its export-heavy business model.

Mirroring this economic slowdown, inflation has lost steam, falling to an annual rate of just 2.6% in February. Wage growth has started to lose speed as well, although it remains at high levels.

Despite this loss of momentum, ECB officials have stressed that it’s still too early to cut rates, as doing so prematurely could fuel a second round of inflation. Most officials have circled June as the most likely month for a rate cut, which would give them access to updated wage numbers.

This meeting will probably be used as a ‘stepping stone’ towards June, with the central bank reaffirming it will be patient with rates until it is certain inflation has been crushed.

Normally, this would be a positive message for the euro. However, this time may be different. The Eurozone economy is already staring down the barrel of a recession and the longer the ECB waits to cut rates, the more painful the downturn might be. In turn, that could force the central bank to cut even deeper later on.

The ECB is laser-focused on wage growth, which unfortunately is one of the most lagging economic indicators. Waiting too long to act could inflict unnecessary damage on the economy and lead to a situation where rates are ultimately slashed with brute force. That paints a gloomy picture for the euro, even if the ECB preaches patience next week.

UK budget and Canadian rate decision coming up

Crossing into the United Kingdom, the government will unveil its latest budget on Wednesday. The Chancellor has made it clear he wants to cut taxes for workers, in a last-ditch attempt to win back voters before a general election that will almost certainly be a disaster for the ruling party.

In the markets, the action will depend on which taxes are cut and how deeply. Meaningful cuts to income tax or national insurance could spell good news for the pound, as that would fuel spending and inflation, adding pressure on the Bank of England to keep rates high for longer. That said, there isn’t much scope for drastic tax changes, so any reaction might be relatively small.

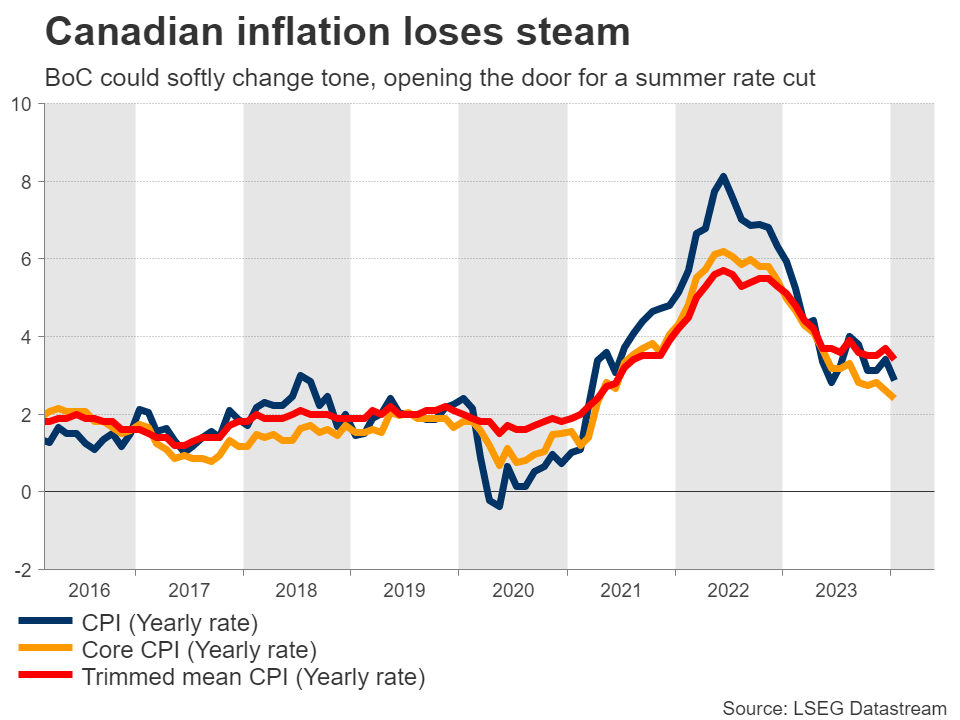

Over in Canada, the central bank will conclude its meeting on Wednesday. Markets are pricing in a 15% probability of an immediate rate cut, but that is highly unlikely considering that the economy is still in decent shape. The housing market in particular is extremely hot, boosted by record levels of migration.

That said, it’s only a matter of time until the Bank of Canada does cut, as inflation has slowed sharply. Markets are pricing in the first rate cut during the summer. Hence, this meeting may bring a soft change in tone, whereby the Bank lays the groundwork for such a move. The nation’s employment data will follow on Friday.

Finally, some data releases from Japan, China, and Australia could attract attention. Starting on Tuesday, the latest inflation stats from Tokyo will give investors a sense of whether the Bank of Japan will raise rates this year. Australia’s GDP data for Q4 will be released on the same day, alongside China’s services PMI for February.