Sample Category Title

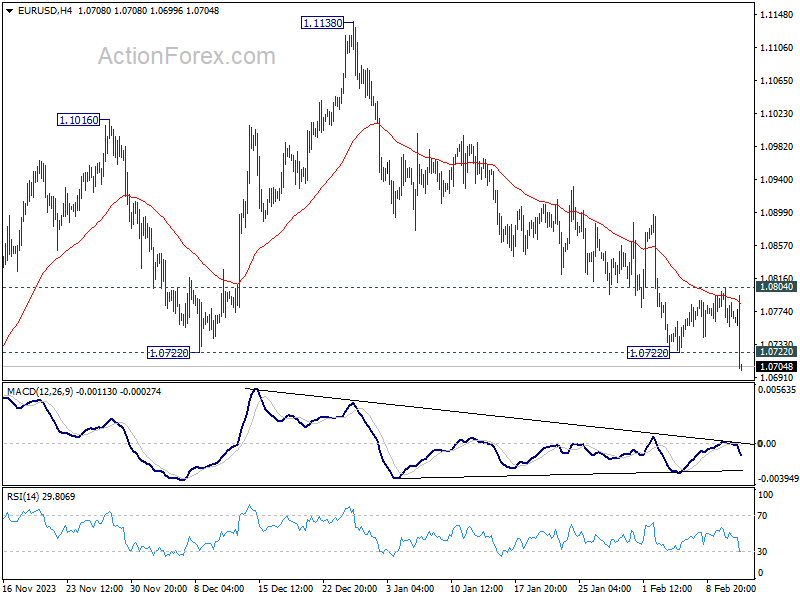

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0750; (P) 1.0778; (R1) 1.0800; More...

EUR/USD's fall from 1.1138 resumed by breaking 1.0722 support today. More importantly, current development argues that whole rise from 1.0477 has already finished. Intraday bias is back on the downside for 1.0447. On the upside, break of 1.0804 resistance is needed to signal short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

Core Inflation Slowdown Hits a Snag, Dollar Rises Amid Fed Cut Uncertainties

Dollar rises significantly in early US session supported by the latest consumer inflation data, which also triggers a marked in DOW futures, dropping by over -300 points. Concurrently, 10-year Treasury yield is soaring near 4.3% mark. Most critically, the inflation data revealed that core CPI remained unchanged at 3.9% in January. This stagnation in core CPI—previously at 4% just three months ago and 4.3% six months back—sparked debates on whether disinflationary trends are stalling. This development would likely delaying any immediate Fed rate cut. Now, the May timeline for initiating rate reductions appears increasingly doubtful.

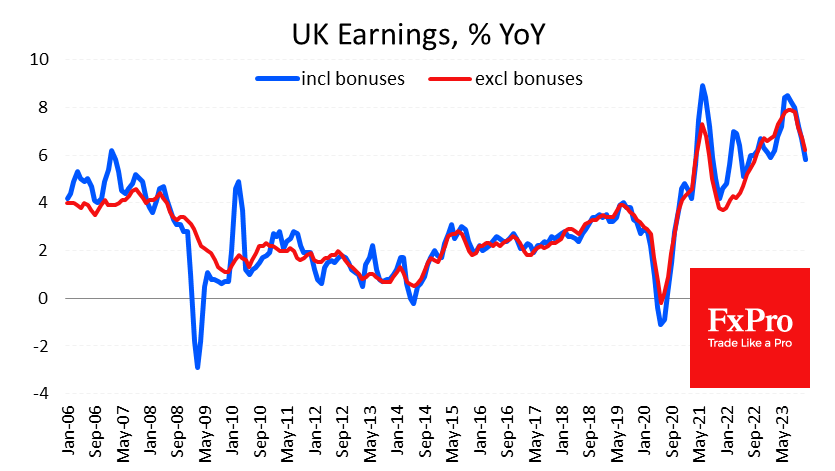

Meanwhile, Sterling, currently as a distant second best performer after Dollar, was supported by robust UK employment data. Although the data revealed gradual easing of wage pressures, they are not decelerating as quickly as BoE had hoped. Additionally, the decline in the unemployment rate underscores a persistently tight labor market, likely to sustain wage inflation. Attention is now keenly directed towards wage settlements expected by April, with some financial analysts adjusting their forecasts for BoE's initial rate cut from May to later in the summer. However, Pound's robustness will still be tested by the forthcoming UK CPI tomorrow and Thursday's GDP data.

Conversely, Swiss Franc found itself at the bottom of today's currency performance, affected by Switzerland's lower-than-expected January CPI data and a significant slowdown in core CPI. These developments have fueled speculation among investors that SNB might advance its timeline for the initial rate cut, moving from September to a possible June action. The next set of CPI data due in early March could critically influence the SNB's decision-making process in its March 21 meeting. A further surprise on the downside could prompt SNB to take preemptive action in March, potentially marking it as the first G10 central bank to commence easing in the current economic cycle.

Elsewhere, New Zealand Dollar and Australian Dollar trailed behind, with the former particularly impacted by RBNZ's survey indicating a further easing of inflation expectations. Canadian Dollar, however, secured its position as the third strongest performer of the day, while Euro is mixed.

In Europe, at the time of writing, FTSE is down -0.41%. DAX is down -0.92%. CAC is down -0.79%. UK 10-year yield is up 0.076 at 4.134. Germany 10-year yield is up 0.040 at 2.406. Earlier in Asia, Nikkei rose sharply by 2.89% to new 34-year high. Japan 10-year JGB yield rose 0.0052 to 0.730. Singapore Strait Times rose 0.11%.

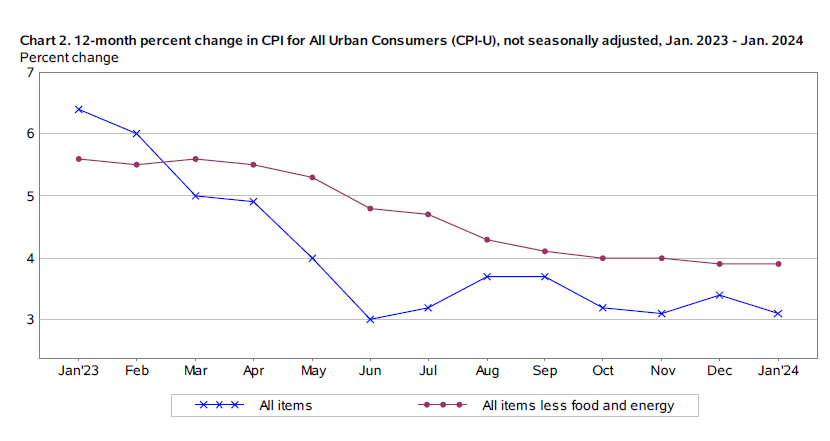

US CPI slows to 3.1% yoy in Jan, but core CPI unchanged at 3.9% yoy

US CPI rises 0.3% mom in January, above expectation of 0.2% mom. CPI core (all items less food and energy) rise 0.4% mom, above expectation of 0.3% mom. Index for shelter rose 0.6% mom, contributing over two thirds of the monthly all item increase. Food index rose 0.4% mom while energy index fell -0.9% mom.

For the 12-month period, CPI slowed from 3.4% yoy to 3.1% yoy, above expectation of 2.9% yoy. CPI core was unchanged at 3.9% yoy, above expectation of 3.8% yoy. Energy index fell -4.6% yoy while food index rose 2.6% yoy.

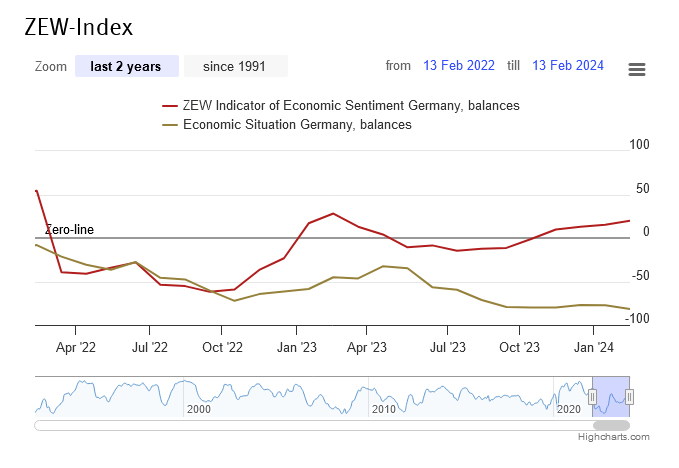

German ZEW sentiment rises to 19.9, anticipating rate cuts

German ZEW Economic Sentiment rose from 15.2 to 19.9 in February, above expectation of 17.5. Current Situation Index, however, fell from -77.3 to -79.0, below expectation of -81.7.

Eurozone ZEW Economic Sentiment rose from 22.7 to 25.0, above expectation of 20.1. Current Situation Index increased 5.9 to -53.4.

ZEW President Achim Wambach said: "The German economy is in a bad place. The assessment of the current economic situation by the respondents has deteriorated to the lowest level since June 2020. In contrast, economic expectations for Germany have improved again."

"Accordingly, more than two-thirds of the respondents expect the ECB to make interest rate cuts over the next six months in light of falling inflation rates. Almost three-quarters of respondents expect imminent interest rate cuts by the American central bank."

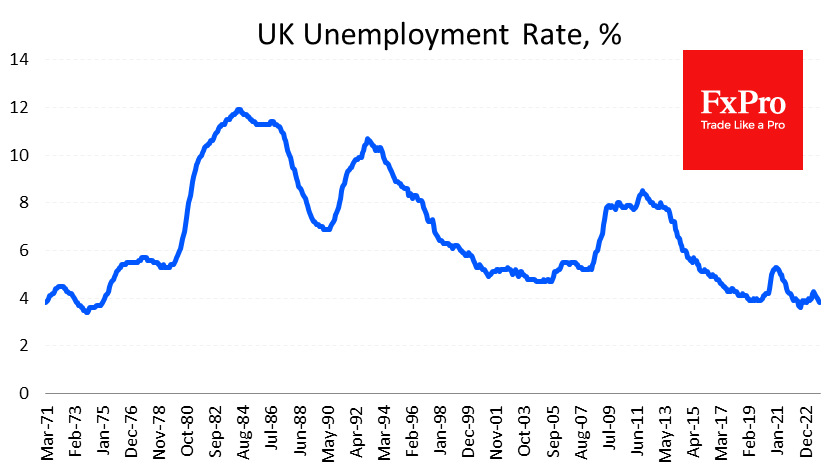

UK unemployment rate falls to 3.8%, wages growth slows but beat expectations

UK payrolled employment rose 48k or 0.2% mom in January. Over the 12-month period, payrolled employment grew 413k or 1.4% yoy. Median month pay rose 6.4% yoy, ticked up from December's 6.3% yoy. Claimant count rose 14.1k, below expectation of 15.2k.

In the three months to December, employment rate rose 0.2% (quarterly change) to 75.0%. Unemployment rate fell -0.2% to 3.8%. Inactivity rate was unchanged at 21.9%. Average earnings including bonus rose 5.8% yoy, down from prior month's 6.7% yoy, but above expectation of 5.7% yoy. Average earnings excluding bonus rose 6.2% yoy, down from prior 6.7% yoy, above expectation of 6.0% yoy.

Swiss CPI down to 1.3% yoy in Jan, below expectation 1.6% yoy

Swiss CPI rose 0.2% mom in January, well below expectation of 0.6% mom. Core CPI (excluding fresh and seasonal products, energy and fuel), fell -0.3% mom. Domestic products prices rose 0.6% mom. Imported products prices fell -1.3% mom.

Annually, CPI slowed sharply from 1.7% yoy to 1.3% yoy, below expectation of 1.6% yoy. Core CPI slowed from 1.5% yoy to 1.2% yoy. Domestic products prices growth slowed from 2.3% yoy to 2.0% yoy. Imported products prices fell deeper, down from -0.2% yoy to -0.9% yoy.

RBA's Kohler points to slightly faster than expected inflation decline

Marion Kohler, RBA's Head of Economic Analysis, noted in a speech that inflation is "still high" but acknowledged a welcome trend: it's decreasing "at a slightly faster rate" than what RBA had forecasted three months prior.

Looking ahead, RBA's expectation is for inflation to settle back into its 2-3% target range by 2025 and reach the midpoint by the following year. However, Kohler underscored the "substantial uncertainty" surrounding these long-term predictions.

A notable aspect of Australia's inflation dynamics, as Kohler pointed out, is the "divergence in the path of core goods and services price inflation."

The primary driver behind the recent dip in inflation rates is the decrease in goods price inflation, whereas services price inflation remains "high and broadly based." This sector's inflation is predicted to "only gradually" diminish as a more equitable demand-supply relationship is established and domestic cost pressures begin to ease.

Kohler also touched on labor costs, particularly significant in the labor-intensive services sector, as a crucial factor influencing the pricing strategies of businesses. RBA believes wage growth is "around its peak" and anticipates a gradual reduction in line with improvements in the labor market. Signs of "easing wage pressures" are already evident in specific industries, notably within business services.

Australia NAB business conditions down to 6, price pressures easing

Australia NAB Business Confidence improved slightly form 0 to 1 in January. Despite this marginal improvement, Business Conditions dropped from 8 to 6, with notable decreases in trading conditions from 11 to 8, profitability conditions from 7 to 5, and employment conditions also falling from 7 to 5.

In terms of cost pressures, labour cost growth remained steady at 2.0% in quarterly equivalent terms, while purchase cost growth saw a slight increase to 1.8% from 1.7%. Product price growth experienced a pickup, moving to 1.2% in quarterly terms from 0.9%, reflecting a broader trend of easing price pressures. Specifically, retail price growth rose to 0.9% from 0.5%, and the growth rate for recreation & personal services prices increased to 1.2% from 0.9%.

NAB Chief Economist Alan Oster commented on the findings, stating, " Capacity utilisation remains high, despite the slowing in growth over the second half of 2023, and price pressures are easing, with hopes they settle well below where they are now."

Australian Westpac consumer sentiment hits 20-Month high, but still pessimistic

Australia Westpac Consumer Sentiment Index surged by 6.2% mom to 86 in February, marking the highest level since June 2022. This increase also represents the largest monthly gain since April of the previous year, which conincided with a period when RBA temporarily halted its tightening cycle.

According to Westpac, the surge in consumer sentiment was notably propelled by improved sentiment towards major purchases, which climbed 11.3% to 86.8, and more optimistic outlook for the economy over the next year, rising 8.8% to 88.9—the highest since May 2022. Additionally, five-year economic outlook rose 4.4% to 93.

The cooling inflation and more favorable perspective on interest rates are believed to be the primary factors behind this uplift. However, despite the recent gains, consumer mood remains in the pessimistic territory.

A notable "sharp turnaround" in sentiment was observed following RBA's decision in February to maintain the cash rate steady, with sentiment dropping from 94.1 to just 80 post-meeting. While the decision to keep rates unchanged aligned with general expectations, the decline in sentiment suggests consumers were anticipating a "clearer indication" that interest rates might begin to decrease.

Looking forward, Westpac anticipates the RBA will maintain the current interest rate in March, contingent on inflation continuing to align with expectations.

RBNZ survey reveals easing inflation expectationss

According to RBNZ's latest Survey of Expectations, one-year inflation expectation fell by 38 basis points from 3.60% to 3.22%, marking its lowest point since September 2021. The survey also indicates a growing consensus, with more than half of respondents expecting that CPI inflation will fall back to RBNZ's target range of 1-3% by the end of 2024

Furthermore, the survey pointed to a decrease in inflation expectations over the longer term, with two-year-ahead predictions dropping from 2.76% to 2.50%, and expectations for five and ten years ahead also seeing decline to 2.25% (from 2.43%) and 2.16% (from 2.28%), respectively.

In terms of interest rates, survey participants anticipate OCR to average at 5.46% by the end of March, with projected decrease to 4.74% by the end of the year. The OCR currently stands at 5.50%.

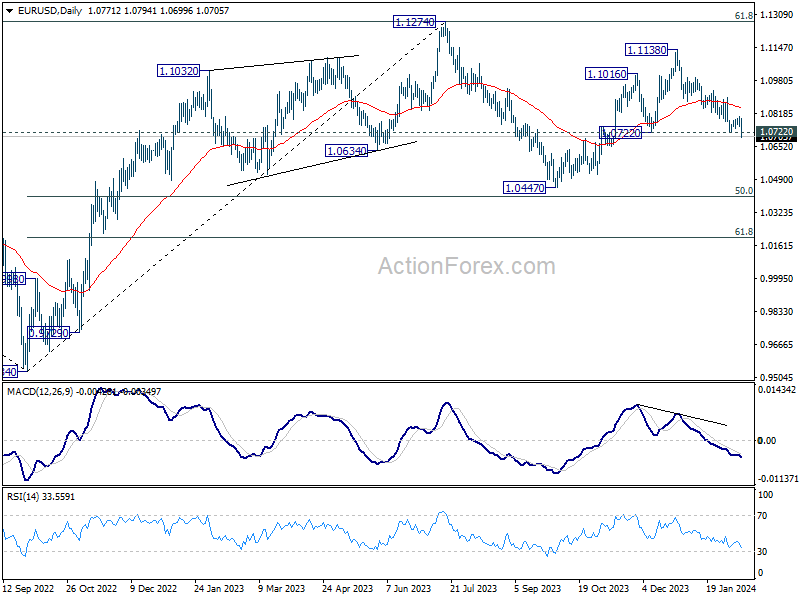

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0750; (P) 1.0778; (R1) 1.0800; More...

EUR/USD's fall from 1.1138 resumed by breaking 1.0722 support today. More importantly, current development argues that whole rise from 1.0477 has already finished. Intraday bias is back on the downside for 1.0447. On the upside, break of 1.0804 resistance is needed to signal short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Feb | 6.20% | -1.30% | ||

| 23:50 | JPY | PPI Y/Y Jan | 0.20% | 0.10% | 0.00% | 0.20% |

| 00:30 | AUD | NAB Business Confidence Jan | 1 | -1 | ||

| 00:30 | AUD | NAB Business Conditions Jan | 6 | 7 | ||

| 02:00 | NZD | RBNZ Inflation Expectations Q1 | 2.50% | 2.76% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jan | -9.90% | |||

| 07:00 | GBP | Claimant Count Change Jan | 14.1K | 15.2K | 11.7K | 5.5K |

| 07:00 | GBP | Unemployment rate Dec | 3.80% | 4.00% | 4.20% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | 5.80% | 5.70% | 6.50% | 6.70% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | 6.20% | 6.00% | 6.60% | 6.70% |

| 07:30 | CHF | CPI M/M Jan | 0.20% | 0.60% | 0.00% | |

| 07:30 | CHF | CPI Y/Y Jan | 1.30% | 1.60% | 1.70% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Feb | 19.9 | 17.5 | 15.2 | |

| 10:00 | EUR | Germany ZEW Current Situation Feb | -81.7 | -79 | -77.3 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | 25 | 20.1 | 22.7 | |

| 11:00 | USD | NFIB Business Optimism Index Jan | 89.9 | 91.1 | 91.9 | |

| 13:30 | USD | CPI M/M Jan | 0.30% | 0.20% | 0.30% | |

| 13:30 | USD | CPI Y/Y Jan | 3.10% | 2.90% | 3.40% | |

| 13:30 | USD | CPI Core M/M Jan | 0.40% | 0.30% | 0.30% | |

| 13:30 | USD | CPI Core Y/Y Jan | 3.90% | 3.80% | 3.90% |

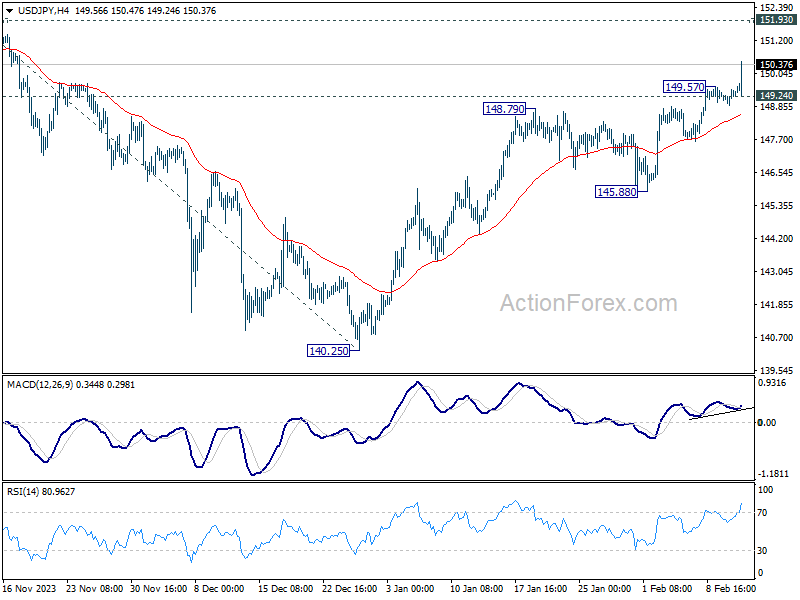

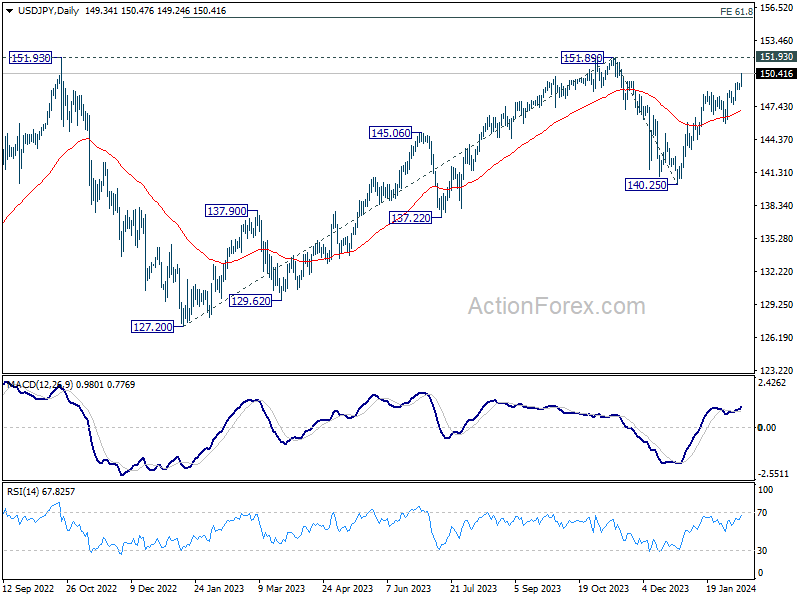

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.03; (P) 149.25; (R1) 149.58; More...

USD/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Further rally should now be seen to retest 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. On the downside, below 149.24 minor support will turn bias neutral and bring consolidations, before staging another rally.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

US CPI slows to 3.1% yoy in Jan, but core CPI unchanged at 3.9% yoy

US CPI rises 0.3% mom in January, above expectation of 0.2% mom. CPI core (all items less food and energy) rise 0.4% mom, above expectation of 0.3% mom. Index for shelter rose 0.6% mom, contributing over two thirds of the monthly all item increase. Food index rose 0.4% mom while energy index fell -0.9% mom.

For the 12-month period, CPI slowed from 3.4% yoy to 3.1% yoy, above expectation of 2.9% yoy. CPI core was unchanged at 3.9% yoy, above expectation of 3.8% yoy. Energy index fell -4.6% yoy while food index rose 2.6% yoy.

New Zealand Dollar Slips After Inflation Expectations Ease

The New Zealand dollar has declined after New Zealand inflation expectations decelerated in the fourth quarter. In the European session, NZD/USD is trading at 0.6114, down 0.25%. The New Zealand dollar declined by 0.40% after the inflation expectations release but has pared these losses.

New Zealand inflation expectations ease to 2.5%

Inflation expectations are a key component of inflation trends, as entrenched expectations can result in higher inflation. On Tuesday, New Zealand inflation expectations fell to 2.5% in Q4, its lowest level in over two years and down from 2.76% in the third quarter.

The release should be an encouraging sign for the Reserve Bank of New Zealand, which has made the battle of inflation its top priority. Inflation is currently running at a 4.7% clip, well above the upper band of the one to three per cent target range. The RBNZ is concerned that inflationary pressures remain sticky and has signaled that it could raise interest rates.

The markets had priced in a rate cut the second half of the year, but “RBNZ speak” has pushed back against these expectations and a stronger-than-expected employment report last week have dampened these expectations. Investors have responded by pricing in a rate hike at 45% at the February 28th meeting and an 80% likelihood at the May meeting. Today’s inflation expectations release could ease pressure on the RBNZ to raise rates, and instead continue the pause in rates which has lasted since May.

In the US, the Federal Reserve has been pushing back against market expectations for a rate cut, and a March cut is now unlikely. On Monday, Richmond Fed President Thomas Barkin reiterated his concerns about lowering interest rates too soon, saying that there was a real risk of inflation moving higher.

NZD/USD Technical

- NZD/USD is testing support at 0.6116. Below, there is support at 0.6072

- 0.6193 and 0.6237 are the next resistance lines

January US CPI and Its Impact on EURUSD

Fundamental Outlook

Today, Tuesday, February 13th, at 8:30 am New York time, the Bureau of Labor Statistics (BLS) releases US inflation data related to the Consumer Price Index (CPI). This high-impact data could generate significant changes in the perception of the Federal Reserve's (Fed) monetary policy, likely triggering extreme volatility around the US dollar (USD).

Market Expectations

Expectations surrounding the upcoming report are clear: overall inflation in the United States is expected to increase at an annual rate of 2.9% in January, a slight deceleration compared to the 3.4% rise recorded in December. At the same time, the core CPI inflation rate, which excludes food and energy prices, is projected to decrease to 3.7% from 3.9% the previous month. On a monthly basis, a 0.2% increase is expected for the overall CPI and a 0.3% increase for the core CPI.

Adjustment of Previous Monthly Figures

The BLS also reported that it revised downward the December monthly increase in the CPI to 0.2% from 0.3%. On the other hand, the November CPI was revised upward to 0.2% from 0.1%, while October's growth remained unchanged at 0.1%. These revisions, according to the BLS, reflect new seasonal adjustment factors.

Factors That Could Affect the Figures

Richmond Federal Reserve Bank President Thomas Barkin warned on Monday that US companies accustomed to raising prices in recent years could continue to fuel inflation. Among other factors that could influence the inflation report, the 6% increase in oil prices due to concerns about a possible supply shock from the crisis in the Red Sea stands out.

Market Impact

Following solid labour market data in January, markets have adjusted their expectations regarding a possible change in Fed policy. Currently, at FBS, we estimate that the Fed will only make 3 or 4 rate cuts starting in the summer, considering bank officials' statements, leaving room for unexpectedly high CPI data to be released.

This implies that a higher outcome than analysts' estimates will trigger an aggressive rise in the USD, suggesting that the Fed will comfortably remain with higher rates. On the other hand, lower-than-expected data will lead to USD selling, as it implies that the Fed may adjust to anticipate the cut to May or June, thereby affecting US Treasury bond yields and consequently the US dollar.

EURUSD

Trading below the weekly opening at 1.0777, just above what is considered buying zones with the Point of Control (POC) located at 1.0778, a rebound towards yesterday's high volume node at 1.0792 is expected. This is very close to the resistance at 1.0805, a breakthrough which will extend the ascent towards the daily bullish average range at 1.0822, especially with lower-than-expected figures indicating the extension of the current bullish correction.

However, this publication often generates volatile movements in both directions before the pair renews its technical downtrend sequence. This will be possible if quotes fail to break the local resistance at 1.0805 and resume selling towards 1.0741, 1.0723, and the bearish average range at 1.0714 near last week's buying zone between 1.0696 and 1.0688. This could happen with a more volatile reaction to unexpectedly higher-than-expected data.

Stronger Labour Market Continues to Boost Pound

Economic data continues to be on the Pound’s side, with another set of better-than-expected figures, this time from the labour market. The unemployment rate fell from 4.2% to 3.8% against expectations of 4.0%.

A fall in the number of active job seekers in the labour market increases competition among employers, helping to keep wages growing at a higher rate. Wages rose by 5.8% in the three months to December. That’s a solid decline from 6.7% the previous month and a peak of 8.5% six months earlier, but more robust than the 5.8% expected.

The annual rate of wage growth has been above the rate of consumer inflation for half a year, narrowing the gap that had built up in previous years as prices had risen sharply. The slowdown in wage growth and the uptrend in the unemployment rate create an expectation that the Bank of England’s next move will be to cut interest rates. However, more potent labour market data, especially if complemented by a further acceleration in inflation on Wednesday, will push back the expected date for policy easing.

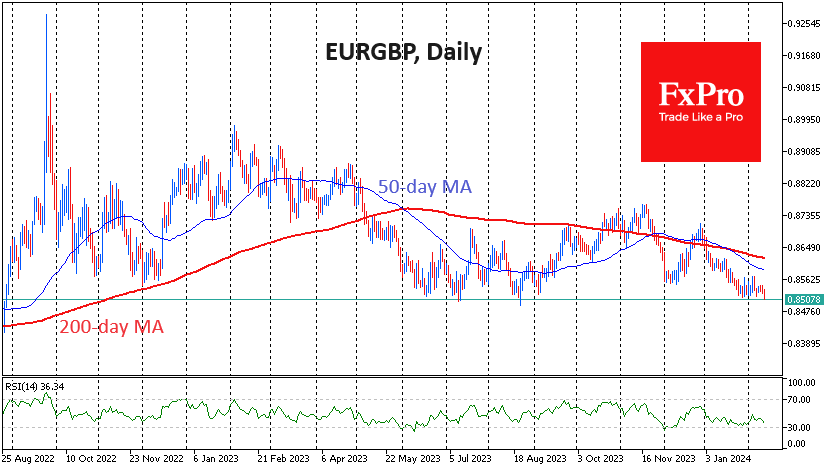

Better-than-expected employment figures have supported the Pound’s gains, especially against the Euro and the Franc. The GBPUSD has primarily traded in a very tight range of 1.26-1.2650 over the past week. EURGBP is down 0.3% at 0.8510, the June-August 2023 pivot area, following the release. The pair’s active bearish trend, which began earlier this year, suggests a renewal of multi-month lows with the potential for a drop to 0.83-0.84 before the end of the current quarter.

A Step in the Right Direction for the UK But BoE Will Remain Cautious

The UK is continuing to make progress toward being able to cut interest rates but as has been the case throughout the last couple of years, the process is far from straightforward.

The good news is that wage growth is slowing at a good pace after peaking last summer and near-term trends are very promising. The bad news is that the labor market remains very tight and it's still highly uncertain whether wage growth will fall to a level consistent with 2% inflation soon.

Then there's the unemployment rate which fell to 3.8% but is no longer reliable as a sole indicator. At a time when the BoE would like absolute clarity on the labor market, it's left to piece together a variety of data and surveys to form a judgment. Not ideal when central banks everywhere are petrified to move too early and risk stoking inflationary pressures again.

This is the first major economic release for the UK this week with inflation to come tomorrow, GDP on Thursday, and retail sales on Friday. Ultimately the CPI data is what matters most but it would be handy if wage growth continues to slide between now and the May meeting if that is to be the live decision many expect it will.

The pound is trading higher on the back of the release on the belief that today's data is a small setback - wage growth not falling as much as expected and unemployment falling further. I don't think today changes a great deal, wage growth is still cooling at a decent rate and the data over the next couple of months is arguably more important.

The MPC will only have data up to March in time for the May meeting which is perhaps why markets are currently favoring a summer start for rate cuts.

Oil continues to drift higher

Oil prices are up almost 8% from last week's lows but remain a little shy of the peak hit in late January. The market remains very volatile, with events in the Middle East creating upside risks. Then there's the global economy and interest rates, the expectations of which are forever changing. Interest rate expectations have been pared back more recently but traders remain upbeat on the economic outlook. Of course, the further back the first rate cuts are pushed, the less confident people will be which could weigh on oil prices.

Gold choppy ahead of US CPI

Gold remains rangebound following quite a choppy start to the year. The yellow metal has remained above $2,000 during this time which suggests traders are committed to the prospect of many rate cuts this year. But in the absence of that first move or even a hint toward it, we haven't seen a breakout in either direction. Perhaps the US CPI data later could tip the balance.

A psychologically important milestone

The post-ETF sell-off in bitcoin didn't last very long and a break above $50,000 will be widely viewed as a significant milestone in its comeback. It's been a rough couple of years but the ETF approvals were an important achievement that's helped propel the price higher. Many will now be hoping it goes from strength to strength, perhaps buoyed by the halving event in April.

German ZEW sentiment rises to 19.9, anticipating rate cuts

German ZEW Economic Sentiment rose from 15.2 to 19.9 in February, above expectation of 17.5. Current Situation Index, however, fell from -77.3 to -79.0, below expectation of -81.7.

Eurozone ZEW Economic Sentiment rose from 22.7 to 25.0, above expectation of 20.1. Current Situation Index increased 5.9 to -53.4.

ZEW President Achim Wambach said: "The German economy is in a bad place. The assessment of the current economic situation by the respondents has deteriorated to the lowest level since June 2020. In contrast, economic expectations for Germany have improved again."

"Accordingly, more than two-thirds of the respondents expect the ECB to make interest rate cuts over the next six months in light of falling inflation rates. Almost three-quarters of respondents expect imminent interest rate cuts by the American central bank."

USD: Critical Levels To Watch Ahead of CPI

The US Dollar Index (DXY) has been in a consolidation phase since early February, displaying minor signs of weakening last week. Despite this, the USD continues to find support around the 104.00 mark on dips, indicating a general resilience. Analysis suggests that the USD may currently be overvalued in the short term when considering various factors such as spreads. Moreover, US yields have remained relatively stagnant, limiting the potential for the USD to strengthen without significant economic data improvements. Market sentiment is awaiting the release of the US January CPI report, which is expected to influence the USD's short-term trajectory. Depending on whether inflation is slower or sticks close to expectations, the USD's direction could vary, potentially impacting market expectations regarding future Federal Reserve actions. In essence, while the USD remains somewhat stable, its near-term movement hinges on upcoming economic data releases.

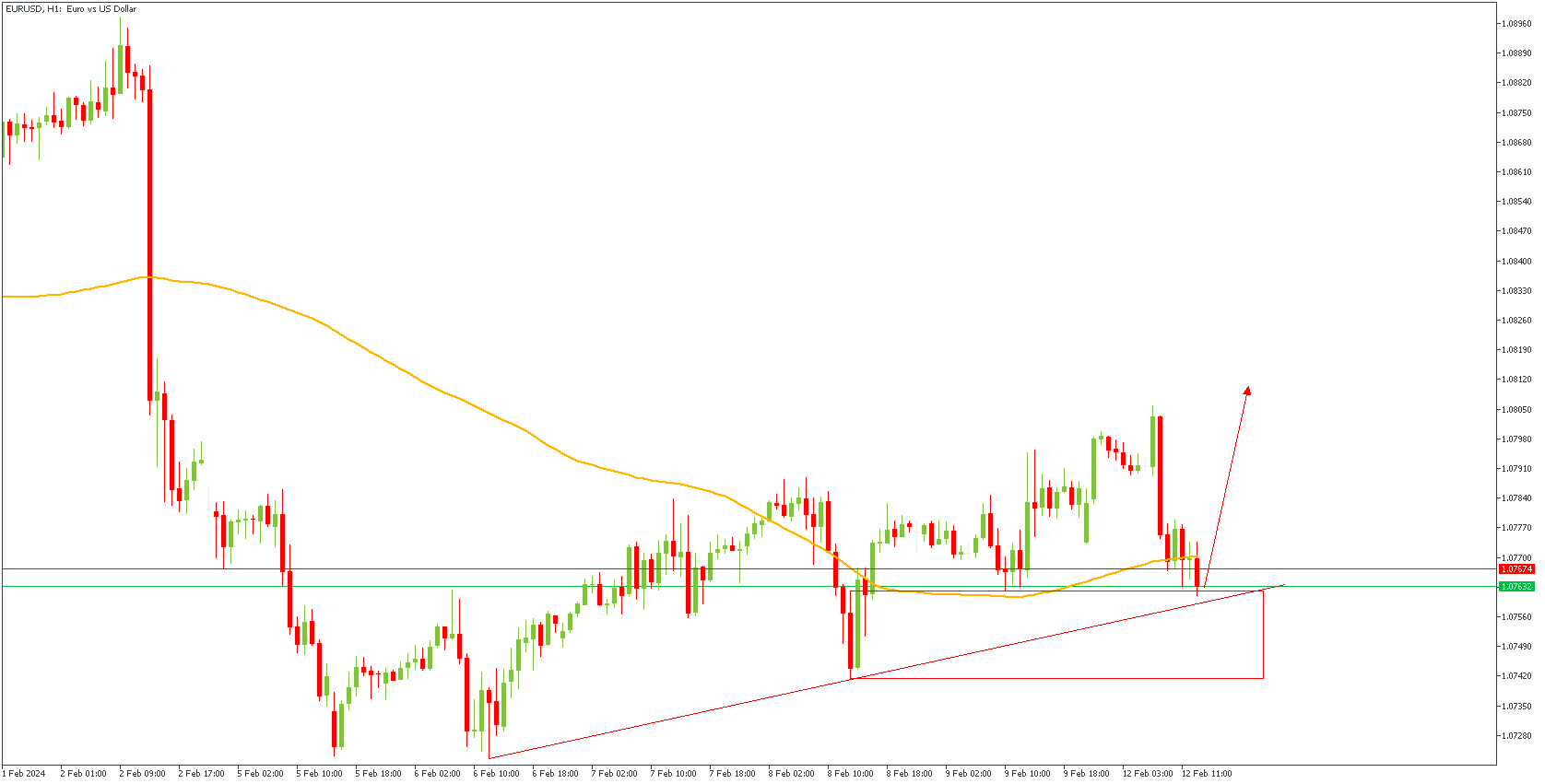

EURUSD - H1 Timeframe

On the 1-hour timeframe, EURUSD is currently being supported by the trendline, 100-period moving average,as well as the demand zone - all of which indicate the possibility of a bullish continuation from the current zone.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.07997

- Invalidation: 1.07408

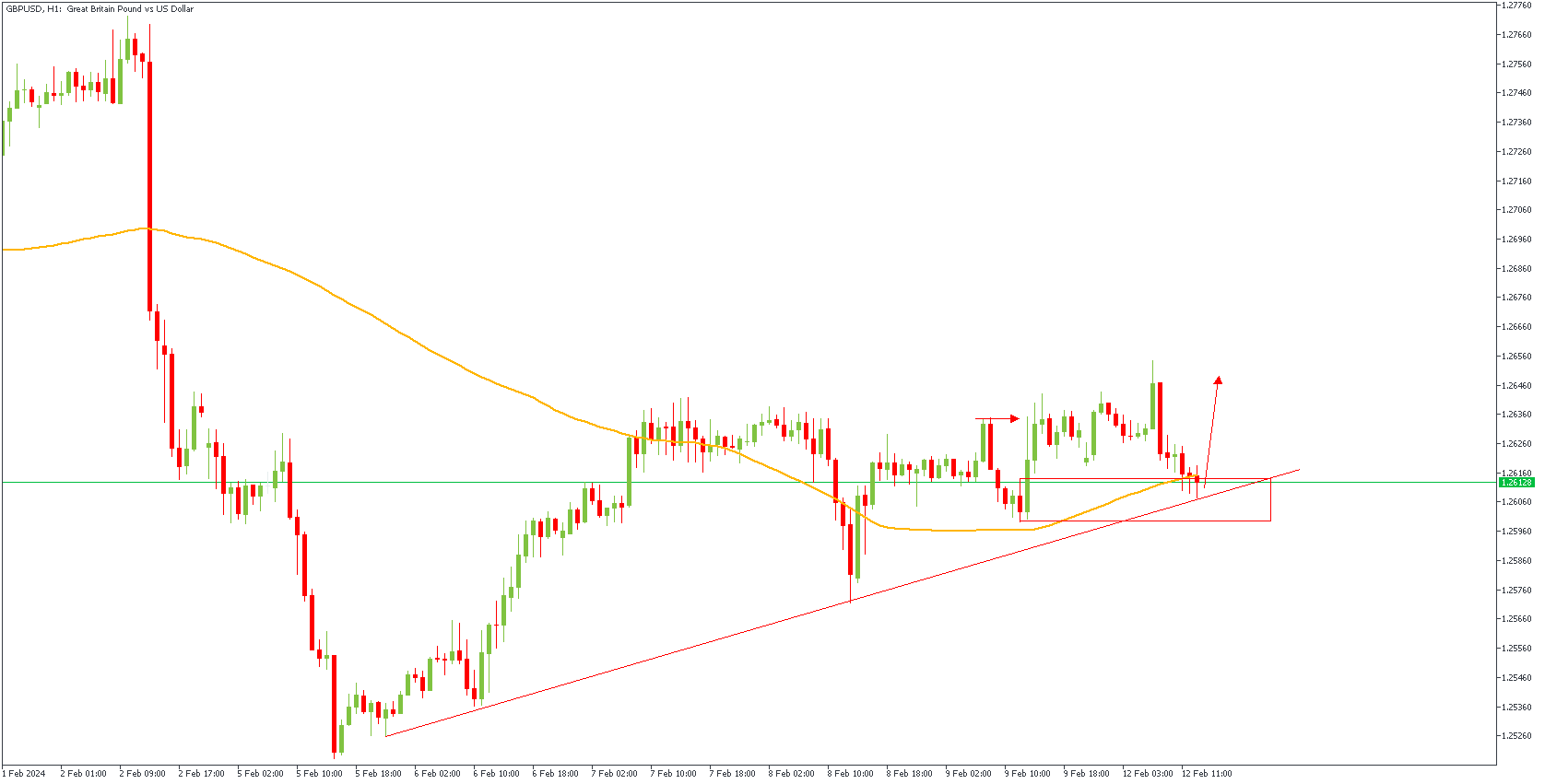

GBPUSD - H1 Timeframe

In a similar manner to what we already analyzed on the EURUSD chart, the hourly timeframe chart of GBPUSD is also trading within the demand zone at the moment with crucial support from the trendline, 100-period moving average, and the demand zone as well.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.26456

- Invalidation: 1.25989

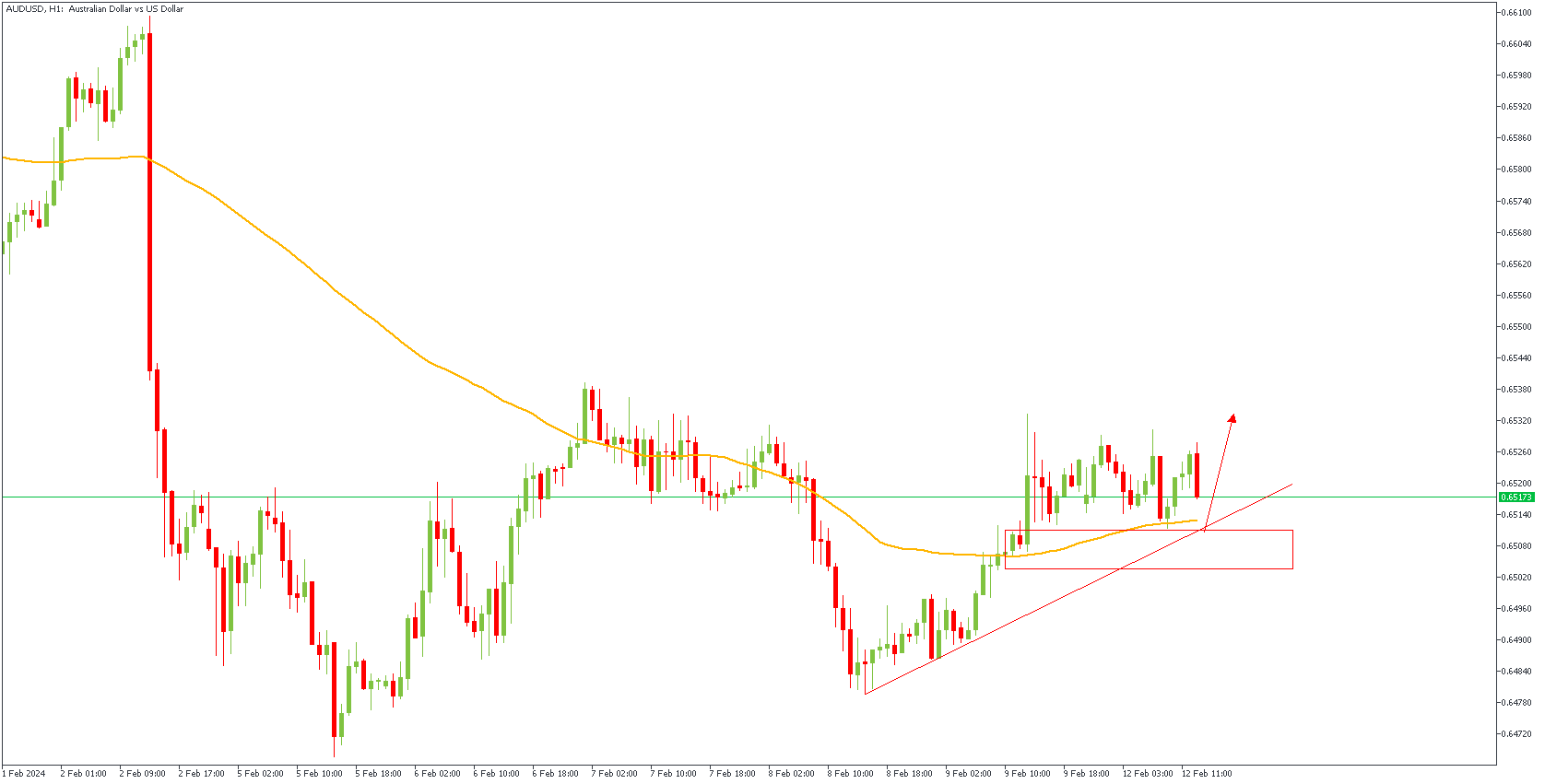

AUDUSD - H1 Timeframe

AUDUSD is in alignment with the views on GBPUSD and EURUSD as afore-mentioned. I see the likelihood of price bouncing off the trendline support, moving average support, and the demand zone.

Analyst’s Expectations:

- Direction: Bullish

- Target: 0.65270

- Invalidation: 0.65032

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.