Sample Category Title

Can Rate Cuts and Geopolitics Propel Gold to Fresh Record Highs?

- Gold’s uptrend hits a snag; 2024 characterized by consolidation phase

- But ingredients for a rally are still there

- Geopolitical risks and Fed rate cuts hold key to rekindling the bulls

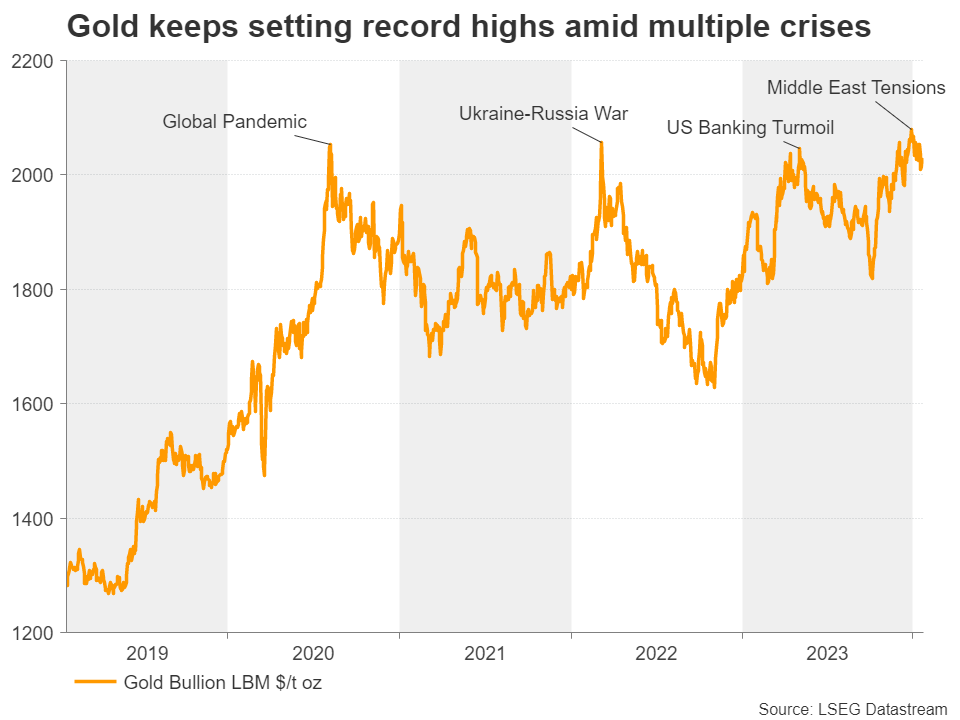

Scaling new heights as world goes from crisis to crisis

Since 2020, the world has been stumbling from one crisis onto another, creating the perfect ground for a massive rally in gold prices. From the Covid pandemic in 2020, to the Russia-Ukraine war in 2022, to the mini-banking crisis in the US in 2023, there’s been no shortage of turmoil over the past few years to boost demand for the world’s traditional safe haven.

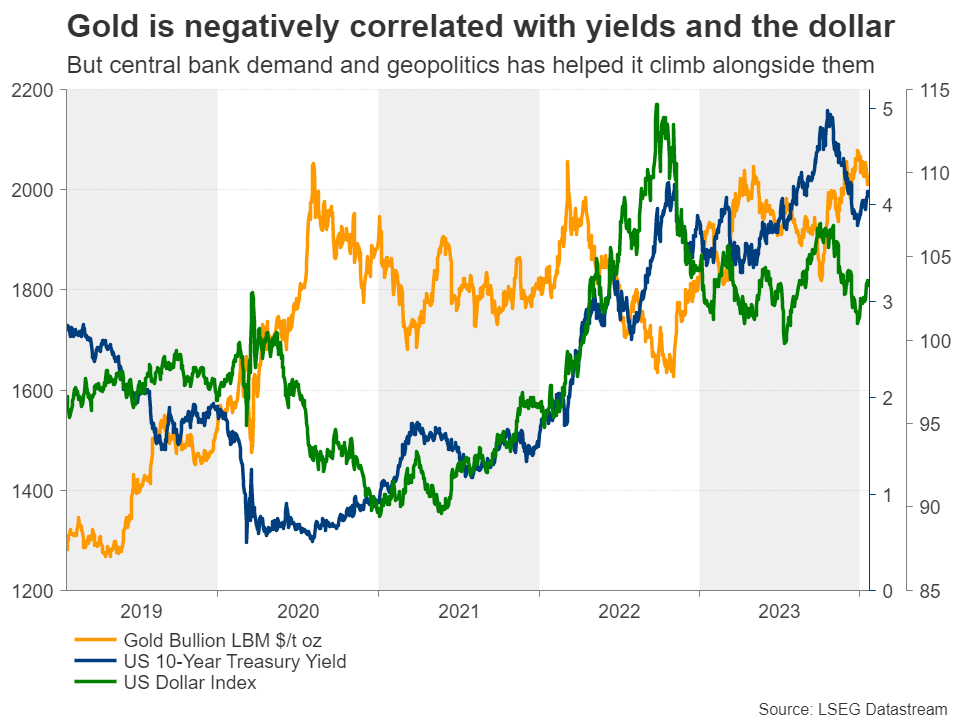

Gold is the world’s oldest store of value as well as one of the safest assets to own, which is why investors rush to gold whenever financial markets are overrun by uncertainty. However, aside from geopolitical events and panic in financial markets, gold also has a long-established relationship with government bonds and the US dollar. Both are also considered to be safe havens so are in direct competition with gold.

Are gold and yields still inversely related?

When bond yields rise, this makes investing in government bonds more attractive, and thus, negatively impacting the price of gold. But rising yields, specifically US Treasury yields, can be a double whammy for the precious metal because not only does gold lose out due to its a non-yielding attribute, but higher bond yields also increase the attractiveness of the US dollar.

As gold is priced in US dollars, it becomes more expensive for non-US investors whenever the greenback appreciates, which is why gold has such a strong negative correlation with the currency.

Whilst these relationships have always been the primary drivers for gold, they’ve become more prominent than ever now that geopolitical risks and interest rate speculation are both so elevated. After all, it is not often that gold climbs to record highs at the same time as US yields are rallying to multi-year peaks.

The geopolitical risk premium

When gold first soared above $2,000/oz in the aftermath of the pandemic in 2020, interest rates and yields were at rock bottom as central banks around the world were engaged in money printing. In the last rally when bullion hit a new all-time high of $2,135.40, borrowing costs had surged by around 500 basis points during this period, completely disobeying the negative correlation rule between the two.

This goes to show the scale at which the geopolitical risk premium has risen amid multiple hotspots around the world that could erupt at any moment. However, there is an additional element that’s also been lifting gold prices lately.

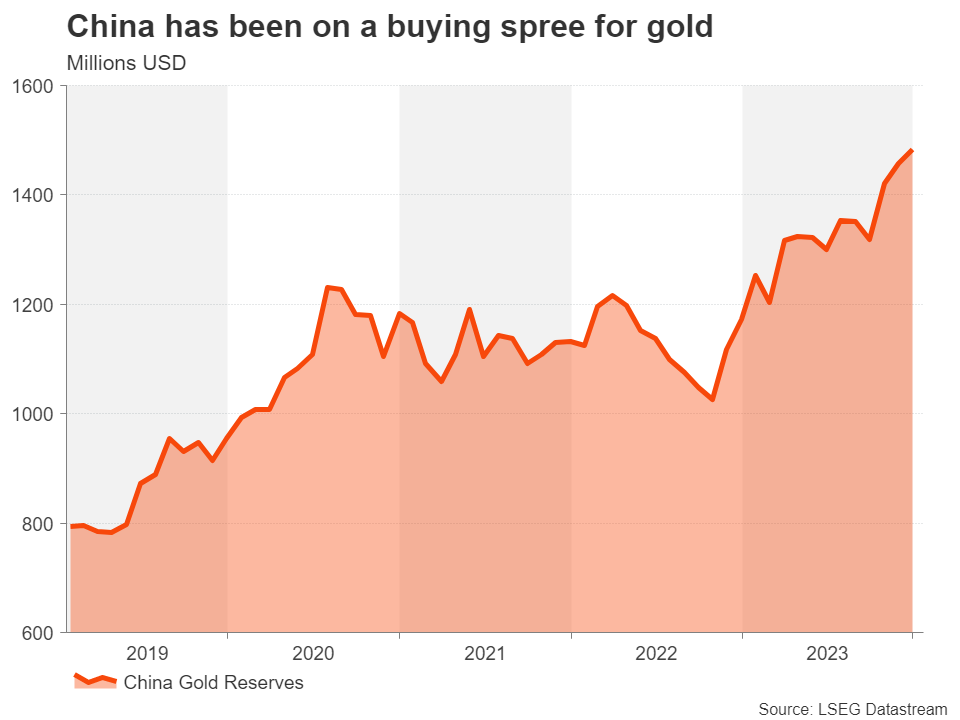

Soaring demand by central banks

Central banks have been purchasing gold in record amounts over the last few years - a trend that’s been primarily driven by China and is motivated by the desire to reduce reliance on the US dollar.

Both geopolitics and the ‘de-dollarization’ trend are expected to remain major contributors of demand in 2024, supporting the bulls’ side of the story. But the bears may not be so fortunate this year as central banks like the Fed are highly anticipated to embark on a rate-cutting cycle within the next few months, potentially leading to a substantial pullback in yields and a weaker dollar.

How risky is the inflation bet?

So does this mean that it is only a win-win scenario for gold? Not necessarily. Although there can be no disputing that the bullish case for the yellow metal is quite strong at the moment, there are risks attached to the dovish outlook for the Fed.

Neither the rhetoric from Fed officials nor the economic data support the argument for hefty rate cuts in 2024. Whilst a recession cannot be totally ruled out, all the evidence indicates a soft landing for the US economy, diminishing the need for a large reduction in borrowing costs. Those pointing to the drop in inflation as the main reason why the Fed will slash rates are right, but only to an extent.

Fed vs the markets

As long as growth stays positive and the labour market remains tight, the Fed will have limited scope to cut rates as looser policy under such conditions can easily overstimulate the economy. Markets have already scaled back some of their dovish bets for the Fed but still anticipate at least five 25-bps rate cuts versus the three projected by FOMC members. Subsequently, Treasury yields have reversed some of their decline, with the halt in the slide of oil prices underpinning the rebound.

With central bank easing fully priced in and the possibility of more dialling back of expectations, the prospect of gold receiving a further boost from lower yields and a weaker dollar doesn’t look particularly great as things stand now. What could change this picture, however, is a deterioration in the labour market.

Is the US outlook too rosy?

So far, despite the surge in layoffs in 2023, there’s been no notable jump in unemployment. But there is a danger that businesses will step up layoffs this year to safeguard their profit margins in a low growth environment. Senior Fed policymakers have already signalled that with inflation falling, the focus in 2024 will likely shift to the central bank’s employment mandate.

But there’s the possibility that inflation even surprises to the upside, especially following the latest developments in the Middle East. The threat of a major flare-up has risen following the attacks on Red Sea shipping by Houthi rebels in Yemen as well as the recent cross-border missile strikes by both Israel and Iran.

No let-up in geopolitical frictions

An escalation would not only push up energy prices, but additionally create a permanent pause in Red Sea journeys, sparking a broader supply chain shock for the global economy. This would have a two-way effect on gold prices as higher inflation would boost interest rates, while heightened tensions would increase safe-haven demand for gold.

Another positive risk for gold is the dollar side of the equation acting independently of bond yields. This could occur in a scenario where the outlook for the major economies improves, bolstering currencies like the euro and yen, lessening the appeal for the greenback.

In a nutshell, there seem to be an equal number of factors that can go right as well as wrong for gold in 2024, with a Fed repricing being the biggest downside risk and a new geopolitical crisis being the largest upside risk. The thing to note here is that investors are probably less prepared for the former than the latter, but nevertheless, there has been some caution brewing in the market lately.

Gold appears to be in wait-and-see mode

Gold prices have been consolidating after spiking to a record high in December. There seems to be ample support around the 50-day moving average (MA) for the time being but should this support weaken and the focus shifts to the $2,000 mark, it will then be up to the 200-day MA to defend gold’s bullish structure.

If the bulls successfully hold onto to the 50-day MA, a revisit of the all-time peak of $2,135.40 could be on the cards, although there may be a battle between the late December high of $2,088.29 and the $2,100 level to get there.

Either way, a fresh attempt into uncharted territory is probably sometime away as investors will want to tread carefully until the Fed has laid out a clearer path for interest rates, something that is unlikely to happen before the spring.

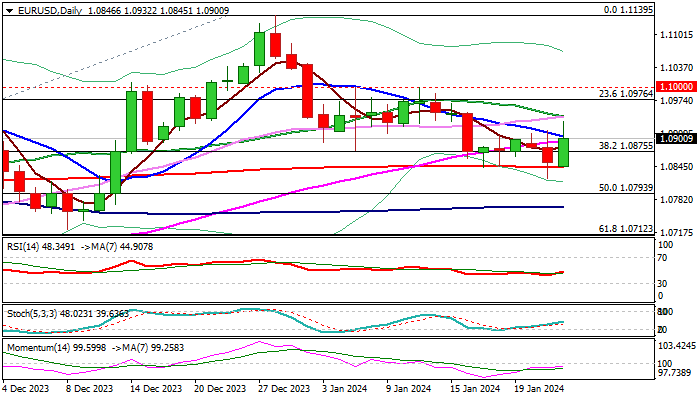

EUR/USD Outlook: Rises to One-Week Gigh on Renewed Risk Appetite

Fresh bulls emerged after top of rising daily cloud and 200DMA (1.0851/43) contained dips for the fourth consecutive day, leaving a higher base at this zone and generating an initial signal that pullback from 1.1139 (Dec 28 peak) has bottomed.

Renewed strength requires sustained break above 1.0943 pivot (20DMA/Fibo 38.2% of 1.1139/1.0821) to sideline downside risk and open way for attack at key 1.10 resistance zone (Jan 11 lower top/psychological.

Also, repeated weekly close above cracked Fibo support at 1.0875 (Fibo 38.2% retracement of 1.0448/1.1139) would add to the upside prospects.

Only violation of 200DMA/cloud top, would negate and shift near-term focus to the downside.

Res: 1.0943; 1.0967; 1.0980; 1.1000.

Sup: 1.0875; 1.0843; 1.0821; 1.0793.

Bank of Canada Holds Steady, Recognizing that Shelter Inflation is the Issue

- The Bank of Canada maintained the overnight rate at 5.0%, while stating that it will continue with quantitative tightening (QT).

- The Bank highlighted the slowing in economic momentum stating, "the economy has stalled since the middle of 2023 and growth will likely remain close to zero through the first quarter of 2024". The Bank also noted that the labour market has cooled, "with job vacancies returning to near pre-pandemic levels and new jobs being created at a slower rate than population growth."

- On the inflation outlook, it "expects inflation to remain close to 3% during the first half of this year before gradually easing, returning to the 2% target in 2025." It highlighted that "while the slowdown in demand is reducing price pressures in a broader number of CPI components and corporate pricing behaviour continues to normalize, core measures of inflation are not showing sustained declines."

- On the future path of policy, the Bank is still concerned about the "persistence in underlying inflation (and the) Governing Council wants to see further and sustained easing in core inflation."

Key Implications

- The Bank of Canada held the line today, but is starting to shift its tone in stronger acknowledgement of the problematic forces of shelter costs. Since the spring, BoC rhetoric has focused on the clear signs of weakness within the economy and this was feeling long in the tooth, now complemented by the dichotomy occurring between shelter costs and the opposing price dynamics elsewhere in the economy. What we know is that Canadians have cut spending over the last year (on a per person basis) as high rates have tightened consumers’ purse strings. Normally this would cause inflation to decelerate quickly, but structural imbalances in the real estate sector are keeping the BoC’s preferred inflation gauges elevated. Importantly, this factor was a big focus of today's policy statement and had its own section in the MPR – an issue we called out in our early-January report.

- While the Bank isn’t yet ready to signal a change in policy, markets are taking the lead. Odds are pointing to the first rate cut happening in April/June. We echo this sentiment. The BoC’s tight policy has caused the economy to flatline since last summer, which has quickly pushed the job market back into balance. Even the BoC's quantitative tightening policy looks to have potentially gone too far with market overnight rates continuing to drift from the Bank's target rate. With this alongside the realization that the BoC can't set policy just based on elevated shelter inflation, it is clear that the central bank is getting ready to signal a rate cut in the coming months.

Sunset Market Commentary

Markets

European January PMI surveys failed to really inspire trading. A disappointing outcome for the French services PMI – releases ahead of German and aggregate EMU data – caused a spike higher in German Bunds, but lack of follow-through buying rapidly pulled German bonds back to opening levels. The EMU composite PMI improved marginally from 47.6 to 47.9, broadly in line with expectations (48). A sectoral breakdown showed a less dire situation in the export-oriented manufacturing sector (46.4 from 44.4 vs 44.7 forecast) while the malaise in the domestic services sector again became a little worse (48.4 from 48.8 vs 49 forecast). The composite PMI points to (mild) recession since June 2023 though this month’s figure is the best since July 2023, suggesting a bottoming out process. The manufacturing PMI recorded the best level since March 2023, but remains sub-50 for an 18th consecutive month now. The services PMI is going nowhere (47.8-48.8 range) for 6 months now. Details strengthened the feeling of a moderating downturn at the start of the new year, but price pressures intensified. The overall contraction of new orders was the smallest recorded since last June, helping stabilise employment levels and lift business optimism about the year ahead to an eight-month high. Companies still relied on backlogs of work to help sustain current operating levels though. Disruptions to shipping in the Red Sea caused supply chains to lengthen for the first time in a year, but manufacturing input costs still fell on average. Service sector cost growth accelerated in January, contributing to the steepest overall rise in prices charged for goods and services since last May. The latter sharply contrasts with markets pricing aggressive rate cuts by the ECB; a view which we expect to be shared by ECB President Lagarde at tomorrow’s press conference. Daily changes on the German yield curve range between -3.5 bps and -4 bps across the curve. US Treasury yields slip slightly more (up to 5 bps). EUR/USD advances (1.0930), but that’s mainly because of the bullish sentiment on stock markets. European bourses arise by up to 2% for EuroStoxx50 with US gauges opening up to 0.75% higher. Chinese stimulus (see below) and strong Q4 corporate earnings are at play. Sterling attacked EUR/GBP 0.8550 support on Gilt underperformance, but the move failed. UK PMI’s showed the recovery in private sector output gaining momentum, but the Red Sea crisis hit manufacturing supply chains and pushed up input costs. The latter adds to evidence (together with sticky inflation) that the BoE isn’t in the position to even start contemplating rate cuts yet. US PMI’s – just released – beat consensus, boosting the goldilocks feeling. Output grew at the fastest pace for seven months while prices charged rose at the slowest rate since May 2020. US Treasuries and EUR/USD lose some ground in a first reaction.

News & Views

Chinese assets roar today. Bourses ended between 1.25-1.8% higher in China and even added 3.50% in Hong Kong. USD/CNY eases to 7.15 compared to 7.20 two days ago. The rally follows a Bloomberg report that Chinese authorities are considering the creation of a state-baked stabilization fund to prop up a slumping stock market. Policymakers are seeking to mobilize some CNY 2tn, or $278bn. That news was followed by additional monetary easing. PBOC governor Pan this morning said the central bank will cut the reserve requirement ratio for banks within two weeks while hinting at more support to come. The cut would amount to 50 bps, unleashing about CNY 1tn of extra liquidity in the market. Both the size as well as the fact that Pan pre-announced the rate cut is very unusual and suggests there’s a growing sense of urgency with policymakers to help the economy and property market to stabilize as well as to stem the market rout. Because even as Chinese assets bounce back today, the likes of the CSI 300 index are still down 45% from the post-pandemic high while the yuan is trading less than 3% above a 15y low.

January bond sales hit a new record in Europe today. Total sales already grew to €300bn. Apart from corporations, the huge offering is concentrated in the SSA debt segment. The likes of Italy and Spain each raised €15bn in their first syndicated sale of the year. Belgium already amassed a lofty €7bn two weeks ago while the EU just yesterday tapped €8bn. January is typically a busy month but this time additional factors are at play. Borrowers across the spectrum seek to profit from big investor demand who want to lock in higher rates now before major central banks starts cutting rates. The end-2023 yield correction is providing countries and companies alike an excellent moment to enter the market. Borrowers are also trying to get ahead of (geo)political events, including US presidential elections.

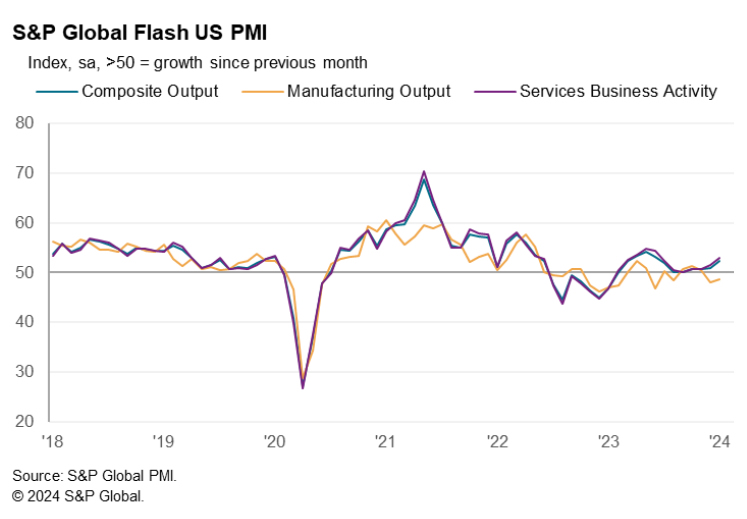

US PMI composite rises to 52.3, marked growth acceleration and sharp inflation cooling

US PMI Manufacturing rises from 47.9 to 50.3 in January, back in expansion, and the highest level in 15 months. PMI Services rose from 51.4 to 52.9, a 7-month high. PMI Composite rose from 50.9 to 52.3, a 7-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, highlights this as an "encouraging start" to the year, with companies reporting "marked acceleration of growth" alongside "sharp cooling of inflation pressures".

Growth momentum has notably intensified, driven by improved demand conditions and steady increase in new orders over the past three months, which has in turn enhanced business confidence to its most optimistic level since May 2022.

Furthermore, there's an air of optimism regarding lower inflation in 2024, anticipated to ease the cost of living pressures and potentially pave the way for lower interest rates.

Notably, the rate of price increases has slowed to its lowest since the early pandemic lockdowns of 2020. Companies report that the current pace of selling price inflation has fallen to "below the pre-pandemic average," aligning with projections of consumer price inflation descending below Fed's 2% target.

BoC hold rates steady, still concerned about risks to inflation outlook

BoC kept overnight rate unchanged at 5.00% as widely expected. In the accompanying statement, BoC expressed that it's "still concerned about risks to the outlook for inflation", in particular the "persistence in underlying inflation". The central bank's focus remains squarely on the equilibrium between demand and supply within the economy, closely monitoring inflation expectations, wage growth, and corporate pricing behaviors.

BoC's assessment of the economy suggests a phase of stagnation, projecting growth to "likely remain close to zero" through Q1. However, gradual strengthening in growth is anticipated around mid-year, predicated on the expectations of pickup in household spending and boost in exports and business investment, spurred by a recovery in foreign demand. Government spending is also expected to play a significant role.

For 2024, BoC forecasts GDP growth at 0.8%, a figure that aligns with its October projection. Looking further ahead, the bank anticipates a more robust growth rate of 2.4% in 2025.

Inflation, a critical concern for the BoC, ended the year at 3.4%. Shelter costs continue to be a significant factor in driving inflation above the target. The central bank's projections indicate that inflation will hover around 3% during the first half of the year, with expectations of a gradual decline, ultimately returning to the 2% target by 2025.

(BOC) Bank of Canada maintains policy rate, continues quantitative tightening

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

Global economic growth continues to slow, with inflation easing gradually across most economies. While growth in the United States has been stronger than expected, it is anticipated to slow in 2024, with weakening consumer spending and business investment. In the euro area, the economy looks to be in a mild contraction. In China, low consumer confidence and policy uncertainty will likely restrain activity. Meanwhile, oil prices are about $10 per barrel lower than was assumed in the October Monetary Policy Report (MPR). Financial conditions have eased, largely reversing the tightening that occurred last autumn.

The Bank now forecasts global GDP growth of 2½% in 2024 and 2¾% in 2025, following 2023's 3% pace. With softer growth this year, inflation rates in most advanced economies are expected to come down slowly, reaching central bank targets in 2025.

In Canada, the economy has stalled since the middle of 2023 and growth will likely remain close to zero through the first quarter of 2024. Consumers have pulled back their spending in response to higher prices and interest rates, and business investment has contracted. With weak growth, supply has caught up with demand and the economy now looks to be operating in modest excess supply. Labour market conditions have eased, with job vacancies returning to near pre-pandemic levels and new jobs being created at a slower rate than population growth. However, wages are still rising around 4% to 5%.

Economic growth is expected to strengthen gradually around the middle of 2024. In the second half of 2024, household spending will likely pick up and exports and business investment should get a boost from recovering foreign demand. Spending by governments contributes materially to growth through the year. Overall, the Bank forecasts GDP growth of 0.8% in 2024 and 2.4% in 2025, roughly unchanged from its October projection.

CPI inflation ended the year at 3.4%. Shelter costs remain the biggest contributor to above-target inflation. The Bank expects inflation to remain close to 3% during the first half of this year before gradually easing, returning to the 2% target in 2025. While the slowdown in demand is reducing price pressures in a broader number of CPI components and corporate pricing behaviour continues to normalize, core measures of inflation are not showing sustained declines.

Given the outlook, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank's balance sheet. The Council is still concerned about risks to the outlook for inflation, particularly the persistence in underlying inflation. Governing Council wants to see further and sustained easing in core inflation and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is March 6, 2024. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR on April 10, 2024.

EUR/USD – Rallies Despite Continued Weakness in Eurozone PMIs

- Eurozone data remains recessionary

- EURUSD rebounds after surveys

- Is it just a corrective rally?

The data from the eurozone isn’t improving early in the new year, with the latest PMI surveys all remaining firmly in contraction territory.

While we’re continuing to see improvements in the manufacturing survey, that comes from a very low base and still some way from the 50 threshold that separates growth from contraction. And it doesn’t appear on course to breach that threshold any time soon.

The services sector is arguably more problematic as it’s a far more important segment of the economy and it’s showing little sign of recovering. This may aid the case for the ECB to consider cutting rates in the coming months if demand remains soft and the economy is either in or on the brink of recession but we’ll need to see more evidence of that over the next six weeks to make March a live prospect. Assuming, of course, inflation doesn’t enable that all on its own.

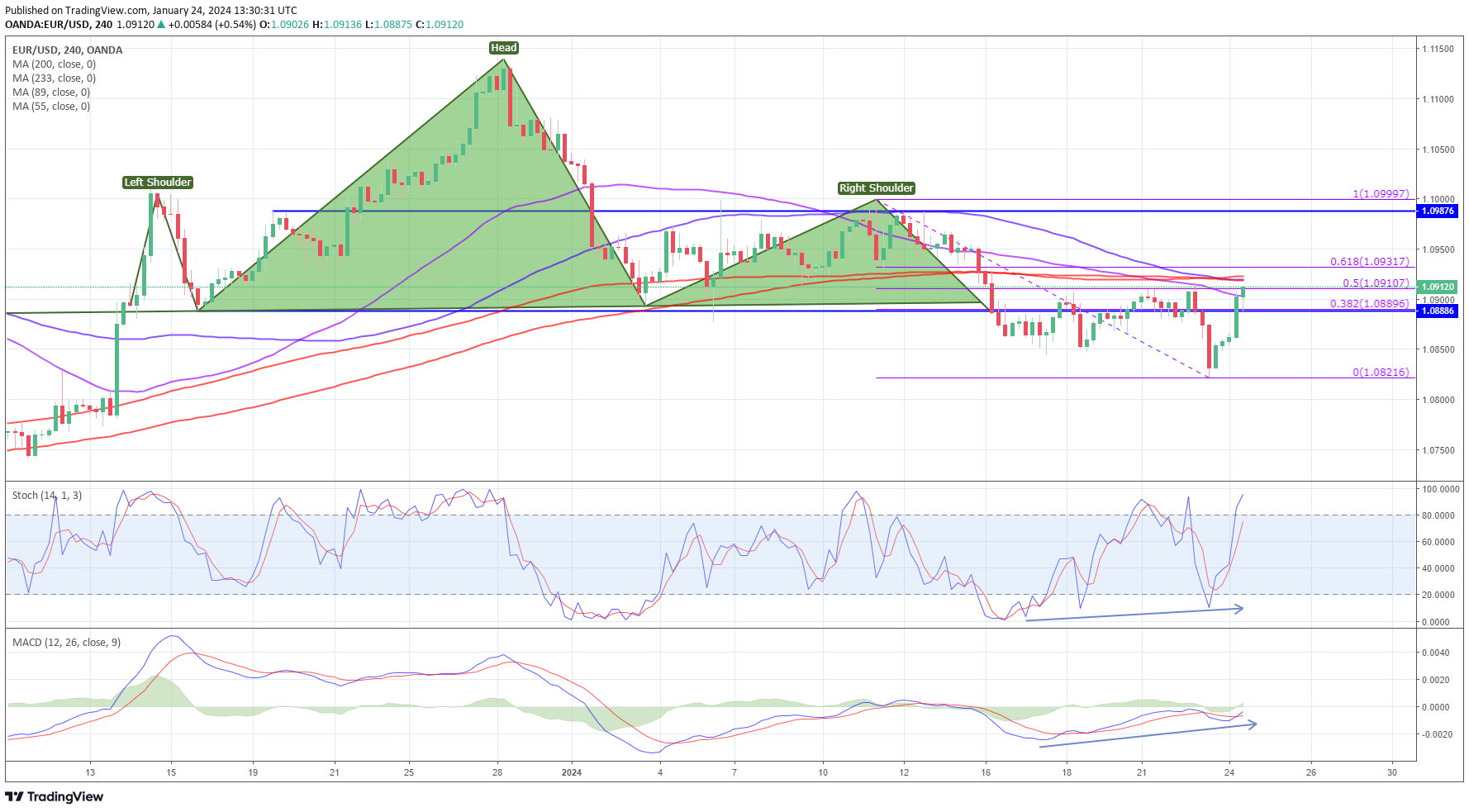

EURUSD rebounds after brief divergence

Despite this morning’s data, the euro is rallying against the dollar today but is there more to come?

EURUSD Daily

Source – OANDA

Before today’s move, the pair had been falling in the opening weeks of the year but in recent days, momentum had been waning. That was evident in the stochastic which clearly made higher lows on the most recent descent in price. But it’s clearer again on the 4-hour chart below on both the stochastic and MACD.

EURUSD 4-Hour

What’s also clear though is that we’ve only seen a small decline since the break of the head and shoulders neckline a week ago. So either this rally is corrective, something Fib levels could help identify, or something has fundamentally changed in that time.

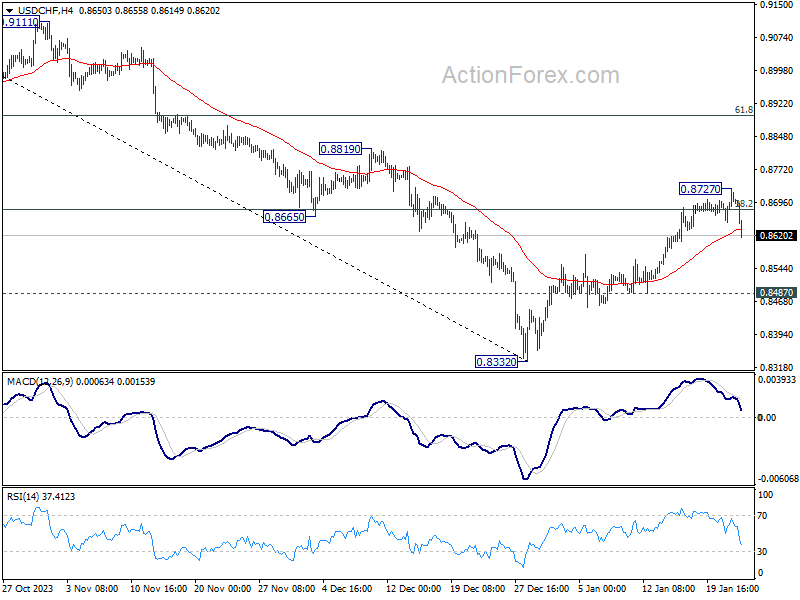

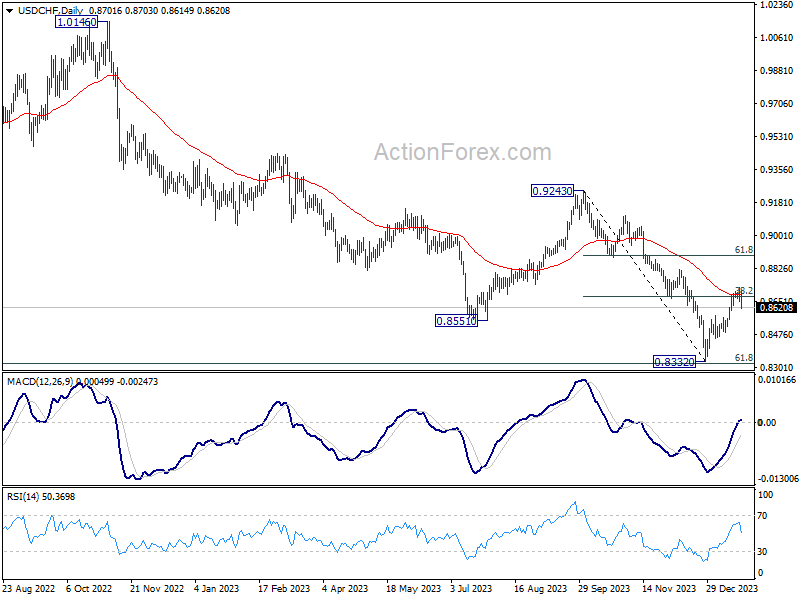

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8659; (P) 0.8694; (R1) 0.8737; More....

USD/CHF's break of 0.8632 minor support suggests initial rejection by 38.2% retracement of 0.9243 to 0.8332 at 0.8680 and 55 D EMA (now at 0.8686). Intraday bias is back on the downside for 0.8487 support. On the upside, though, break of 0.8727, and sustained trading above 0.8680 will turn near term outlook bullish for 61.8% retracement 0.8995.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

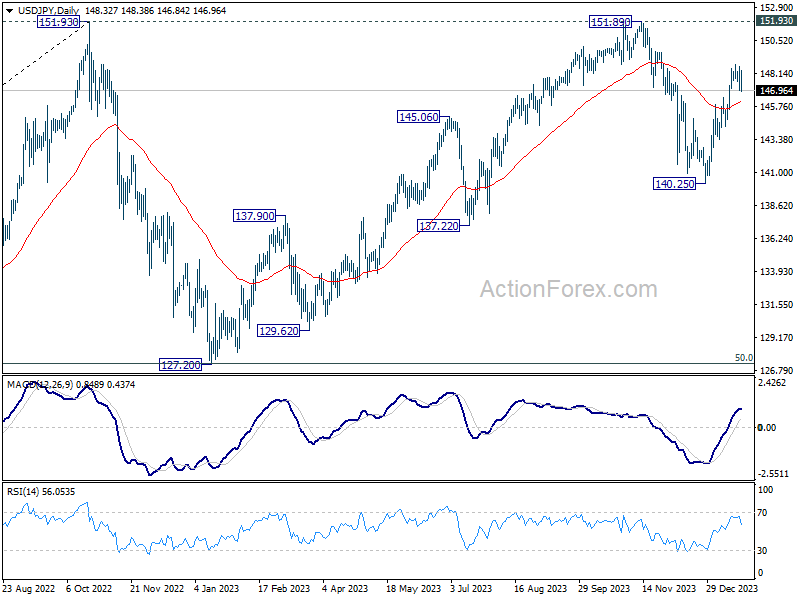

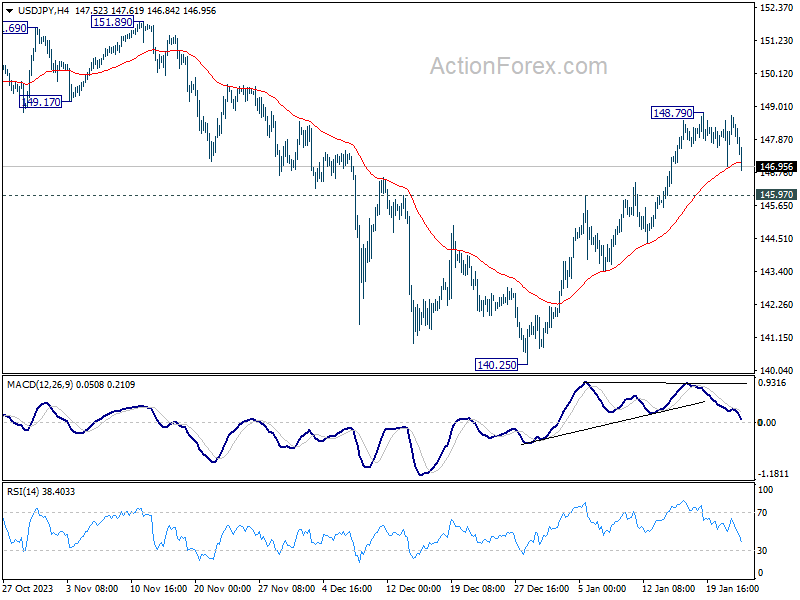

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.34; (P) 148.02; (R1) 149.05; More...

USD/JPY's retreat from 148.79 extends lower today but stays well above 145.97 resistance turned support. Intraday bias remains neutral at this point, and further rally remains in favor. Corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.