Sample Category Title

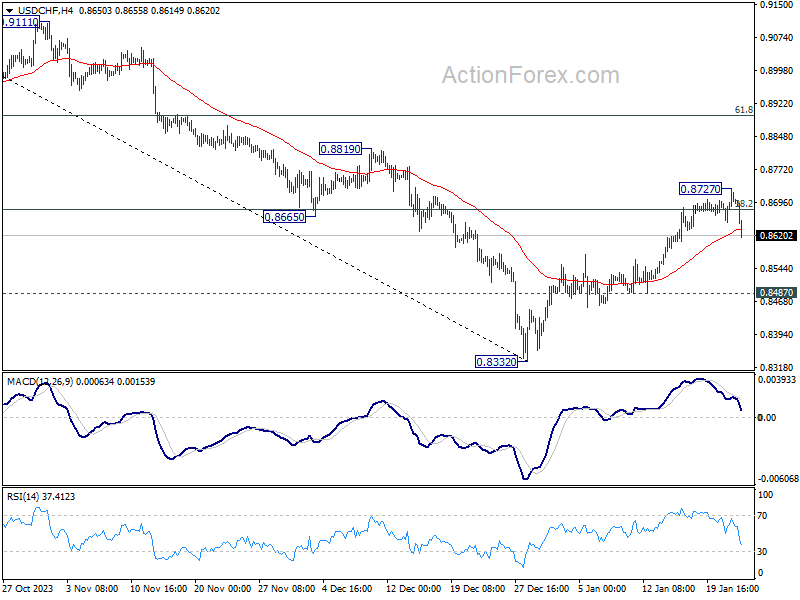

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8659; (P) 0.8694; (R1) 0.8737; More....

USD/CHF's break of 0.8632 minor support suggests initial rejection by 38.2% retracement of 0.9243 to 0.8332 at 0.8680 and 55 D EMA (now at 0.8686). Intraday bias is back on the downside for 0.8487 support. On the upside, though, break of 0.8727, and sustained trading above 0.8680 will turn near term outlook bullish for 61.8% retracement 0.8995.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

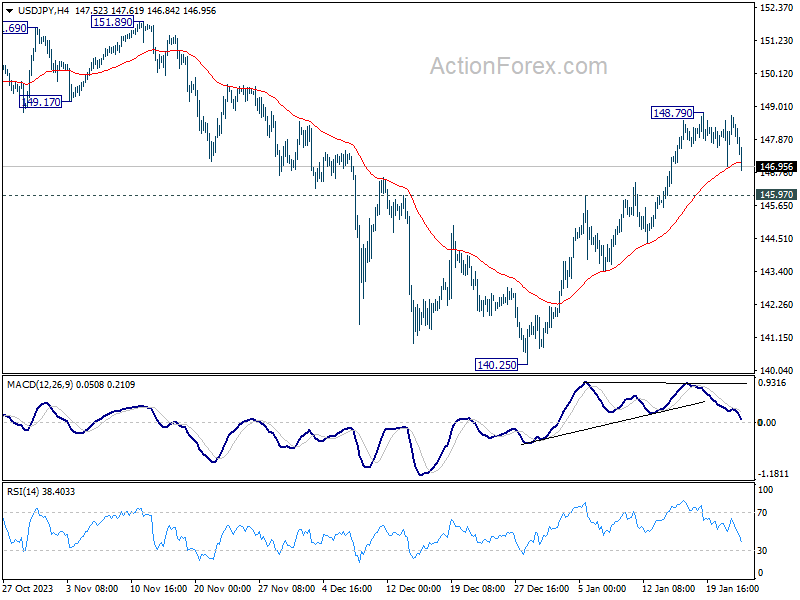

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.34; (P) 148.02; (R1) 149.05; More...

USD/JPY's retreat from 148.79 extends lower today but stays well above 145.97 resistance turned support. Intraday bias remains neutral at this point, and further rally remains in favor. Corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

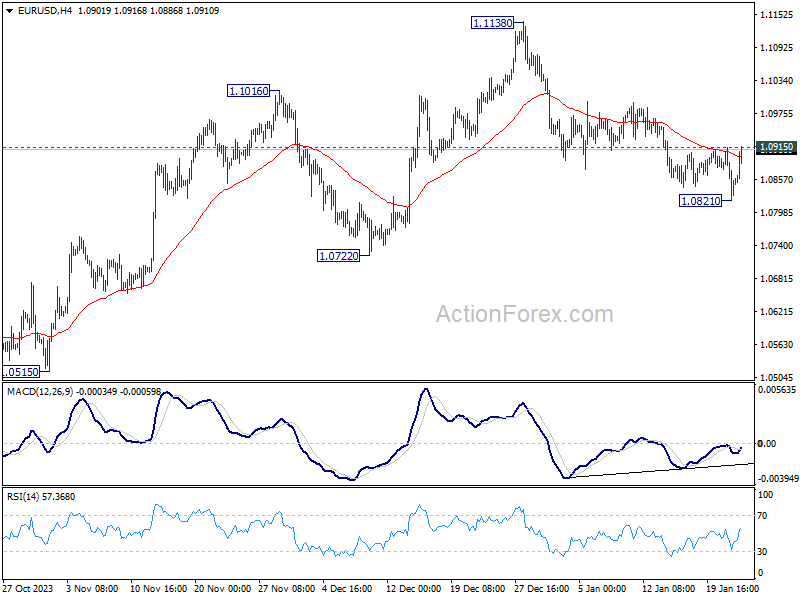

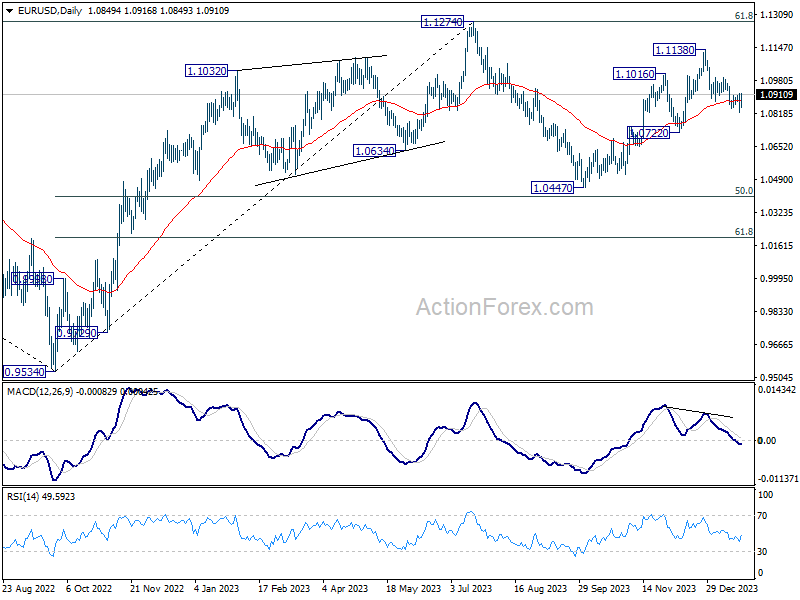

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0812; (P) 1.0864; (R1) 1.0906; More...

Intraday bias in EUR/USD is turned neutral with current recovery. On the upside, firm break of 1.0915 minor resistance will indicate short term bottom at 1.0821, on bullish convergence condition in 4H MACD. Intraday bias will be back on the upside for stronger rebound towards 1.1138 high. On the downside, though, below 1.0821 will resume the fall from 1.1138 to 1.0722 support next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

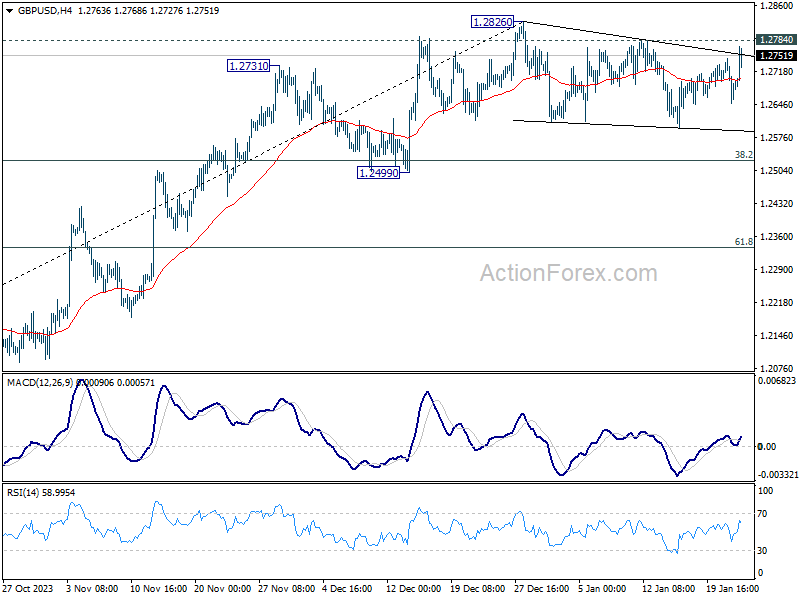

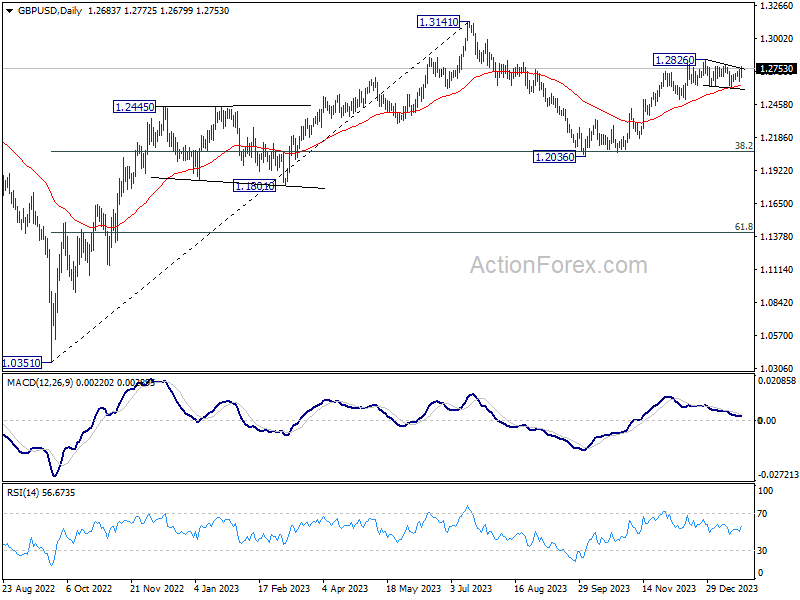

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2642; (P) 1.2694; (R1) 1.2740; More...

Immediate focus is now on 1.2784 minor resistance in GBP/USD. Decisive break there will suggest that consolidation pattern from 1.2826 has completed. Further rise should be seen through 1.2826 to resume the rise from 1.2036. Next target will be 1.3141 high. in case of another fall, downside should be contained above 1.2499 support to bring rebound.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Sterling Rises Following Encouraging UK PMI Data, Dollar Weakens Across the Board

Sterling rises notably against Euro and Dollar today, buoyed by encouraging UK PMI data that pointed to a strong start for the year with renewed growth momentum. More importantly, this data suggests that BoE might need to delay its rate cut plans, as inflationary pressures could potentially resurge due to supply disruptions in the Red Sea. Simultaneously, Eurozone's PMI data, while less optimistic, also supports ECB hawks' stance against premature rate cuts, with price indicators suggesting sustained inflationary pressures.

Conversely, Dollar softens broadly in the wake of slump in US 10-year yield. This decline comes amidst an uptick in market sentiment in Asia, following the People's Bank of China's decision to cut the reserve ratio requirement by 50 basis points. This move is set to inject approximately CNY 1T into the economy, aiming to bolster long-term capital. Nevertheless, Australian and New Zealand Dollars have not shown significant responses to this development. Meanwhile, Canadian Dollar is trading softly as market participants await BoC interest rate decision, where maintaining the current rate is widely anticipated.

From a technical perspective, a key focus for the remainder of the week will be the durability of the shift in sentiment in Hong Kong and China. The immediate point of interest lies at 15972.31 support-turned-resistance in HSI after today's 3.56% gain. Decisive break there will raise the chance of bottoming ahead of 14597.31 (2022 low). That would at least set up further rebound to 55 D EMA (now at 16571.05), or even further to channel resistance at around 18000 later in the quarter.

In Europe, at the time of writing, FTSE is up 0.35%. DAX is up 1.41%. CAC is up 0.88%. UK 10-year yield is up 0.0192 at 4.006. Germany 10-year yield is down -0.0247 at 2.330. Earlier in Asia, Nikkei fell -0.80%. Hong Kong HSI rose 3.56%. China Shanghai SSE rose 1.80%. Singapore Strait Times rose 0.58%. Japan 10-year JGB yield rose 0.0856 to 0.723.

UK PMI composite rises to 52.5, may delay BoE rate cut

UK PMI Manufacturing rose from 46.2 to 47.3 in January, a 9-month high. PMI Services rose from 53.4 to 53.8, an 8-month high. PMI Composite rose from 52.1 to 52.5, a 7-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, noted that UK business activity growth has "accelerated for a third straight month". He described this as a "promising start" to the year.

According to the survey data, UK economy is expected to grow at a quarterly rate of 0.2% after a flat fourth quarter, thereby "skirting recession and showing signs of renewed momentum".

However, Williamson highlighted a crucial implication of this unexpected growth strength in January, which could lead BoE to reconsider the timing of any anticipated interest rate cuts.

This reassessment is particularly pertinent in light of supply disruptions in the Red Sea, which have reignited inflationary pressures in the manufacturing sector. Williamson indicated that inflation is expected to remain stubbornly in the 3-4% range in the near term.

Bundesbank report warns of German economy's vulnerability to China's economic woes

In its latest monthly report, Bundesbank issued a cautionary message about China's current economic struggles and their potential impact on Germany. The report notes that China is grappling with "significant economic problems," and the relationship between China and Western industrial nations has "noticeably deteriorated recently." Such geopolitical risks, if they materialize, could have severe repercussions for the German economy.

The Bundesbank essay posits that "an economic crisis in China of the kind that has occurred in other countries in the past following a correction of excessive credit growth would probably be bearable for the German economy." However, the impact would not be negligible, with projections indicating that Germany's real GDP could be -0.7% lower in the first year of a potential crisis in China, and then -1% in the second year.

The report also highlights a more severe scenario: "However, an abrupt decoupling, for example as a result of a geopolitical crisis, would have a significantly greater impact on German industry in particular." In such an event, German companies with direct involvement in China could face considerable losses in sales and profit. Industries like automotive, mechanical engineering, electronics, and electrical engineering are particularly reliant on Chinese demand.

Moreover, Bundesbank emphasizes the broader risks associated with the close economic ties between Germany and China: "the close real economic ties between Germany and China also pose considerable risks for the German financial system."

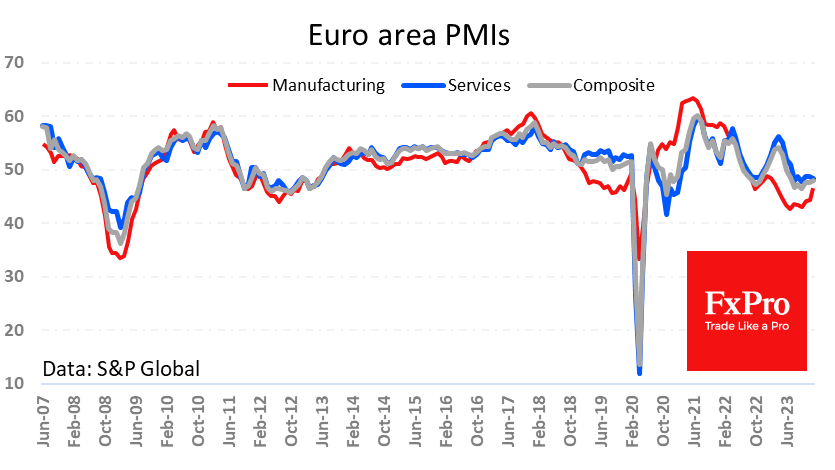

Eurozone's PMI composite climbs to 47.9, price data echo ECB hawks' caution

Eurozone PMI Manufacturing rose from 44.4 to 46.6 in January, a 10-month high. However, PMI services fell from 48.8 to 48.4. PMI Composite rose from 47.6 to 47.9, a 6-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that Eurozone's manufacturing sector is experiencing a "widespread easing of the downward trajectory witnessed in the past year". He highlights that this positive trend is "evident across key indicators such as output, employment, and new orders."

While the services sector is contracting, de la Rubia points out that the contraction is "currently moderate". He also notes a "silver lining," as there is an increase in companies expanding their workforce, which indicates a degree of optimism in the market.

De la Rubia's observation that PMI price indicators are in line with the sentiments of the hawks within ECB. He states they are "all about shouting 'hold your horses'", emphasizing a need for a measured approach and advising against rushing into early rate cuts.

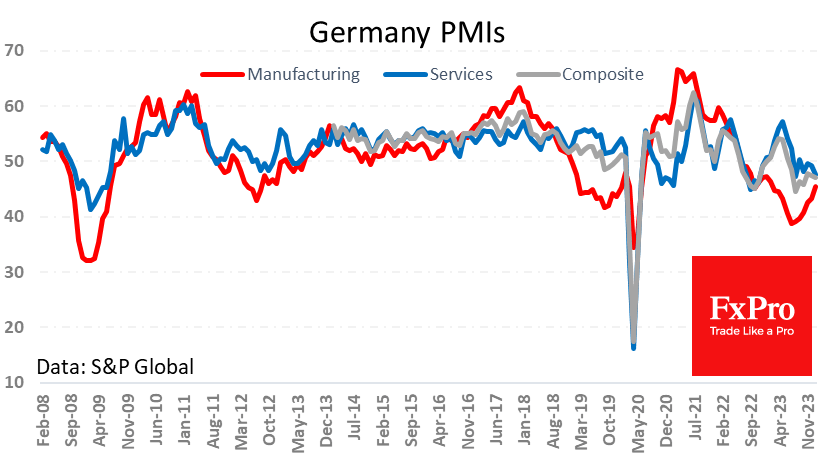

Germany PMI Manufacturing rose from 43.3 to 45.4 in January, an 11-month high. PMI Services fell from 49.3 to 47.6, a 5-month low. PMI Composite fell from 47.4 to 47.1, a 3-month low.

France PMI Manufacturing rose from 42.1 to 43.2 in January. PMI Services fell from 45.7 to 45.0. PMI Composite fell from 44.8 to 44.2.

Japan's PMI shows modest growth, manufacturing still in contraction

Japan's PMI Manufacturing rose fractionally from 47.9 to 48.0 in January, below expectation of 48.2. Manufacturing remained in contraction for the eighth consecutive months. PMI Services rose from 5.15 to 52.7. PMI Composite rose from 50.0 to 51.1.

Usamah Bhatti, Economist at S&P Global Market Intelligence, noted that while "modest" the private sector is having the strongest growth since September. However, there was disparity between the sectors, with services reaching a four-month high, while manufacturing marked its eighth consecutive month of contraction.

Regarding inflation, Bhatti said input price inflation "remains high historically". But output inflation eased to its "lowest since February 2022". This indicates that while input costs are still elevated, businesses are not passing these costs fully onto consumers.

Japan's exports exceed JPY 1T in 2023, US reclaims top export destination

Japan's exports rose 9.8% yoy to JPY 9648B in December, marking the biggest increase in a year. This boost was largely driven by 20.4% yoy jump in exports to US, predominantly from the automotive sector, while exports to Europe climbed by 10.3% yoy. Notably, shipments to China saw 9.6% yoy rise, registering their first growth in 13 months, primarily led by chip-making equipment. In contrast, imports declined -6.8% yoy to JPY 9586B. Consequently, trade balance turned positive, recording JPY 62.1B surplus.

Analyzing the whole year, Japan's trade deficit in 2023 more than halved to JPY -9.29T from the previous year. The country's total exports rose by 2.8% to reach JPY 100.89T , surpassing the JPY 100T mark for the first time ever. Meanwhile, total imports saw -7.0% decrease to JPY 110.18T.

A significant shift was observed in Japan's export destinations in 2023. US reclaimed its position as the largest recipient of Japanese exports by value for the first time in four years, surpassing China. Exports to US reached JPY 20.27T, showing 11.0% increase, while exports to China decreased by -6.5% to JPY 17.76T.

New Zealand CPI slows to 0.5% qoq, 4.7% yoy in Q4

New Zealand CPI rose 0.5% qoq in Q4, down from 1.8% qoq in Q3, matched expectations. Tradeable inflation turned negative to -0.2% qoq, from 1.8% qoq. Non-tradeable inflation slowed to 1.1% qoq, down from 1.7% qoq.

Annually, CPI slowed from 5.6% yoy to 4.7% yoy, matched expectations. Tradeable inflation slowed from 4.7% yoy to 3.0% yoy. non-tradeable inflation also slowed from 6.3% yoy to 5.9% yoy.

"While this is the smallest annual rise in the CPI in over two years, it remains above the Reserve Bank of New Zealand's target range of 1 to 3 percent," consumers prices senior manager Nicola Growden said.

Australia's PMI manufacturing Hits 11-month high, services Lagging

Australia PMI Manufacturing rose from 47.6 to 50.3 in January, back in expansion, and a 11-month high. PMI Services rose slightly from 47.1 to 47.9, a 3-month high. PMI Composite rose from 46.9 to 48.1, a 4-month high, but still in contraction.

Warren Hogan, Chief Economic Advisor at Judo Bank noted the PMI data indicates a that the economy remains on RBA's "narrow path" for soft landing. He highlights the manufacturing sector's rebound as a key factor in mitigating broader economic downturn risks.

Despite the general economic slowdown, Hogan observes that labor demand remains unexpectedly robust, differing from past economic cycles. However, he cautions that inflation pressures are still high, pointing out, "Input and output price indexes remain at levels suggesting CPI inflation is above the RBA's target range."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2642; (P) 1.2694; (R1) 1.2740; More...

Immediate focus is now on 1.2784 minor resistance in GBP/USD. Decisive break there will suggest that consolidation pattern from 1.2826 has completed. Further rise should be seen through 1.2826 to resume the rise from 1.2036. Next target will be 1.3141 high. in case of another fall, downside should be contained above 1.2499 support to bring rebound.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.50% | 0.50% | 1.80% | |

| 21:45 | NZD | CPI Y/Y Q4 | 4.70% | 4.70% | 5.60% | |

| 22:00 | AUD | Manufacturing PMI Jan P | 50.3 | 47.6 | ||

| 22:00 | AUD | Services PMI Jan P | 47.9 | 47.1 | ||

| 23:30 | AUD | Westpac Leading Index M/M Dec | 0.00% | 0.10% | ||

| 23:50 | JPY | Trade Balance (JPY) Dec | -0.41T | -0.45T | -0.41T | -0.35T |

| 00:30 | JPY | Manufacturing PMI Jan P | 48 | 48.2 | 47.9 | |

| 00:30 | JPY | Services PMI Jan P | 52.7 | 51.5 | ||

| 08:15 | EUR | France Manufacturing PMI Jan P | 43.2 | 42.5 | 42.1 | |

| 08:15 | EUR | France Services PMI Jan P | 45 | 46 | 45.7 | |

| 08:30 | EUR | Germany Manufacturing PMI Jan P | 45.4 | 43.7 | 43.3 | |

| 08:30 | EUR | Germany Services PMI Jan P | 47.6 | 49.5 | 49.3 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan P | 46.6 | 44.8 | 44.4 | |

| 09:00 | EUR | Eurozone Services PMI Jan P | 48.4 | 49.1 | 48.8 | |

| 09:30 | GBP | Manufacturing PMI Jan P | 47.3 | 46.7 | 46.2 | |

| 09:30 | GBP | Services PMI Jan P | 53.8 | 53.5 | 53.4 | |

| 14:45 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% | ||

| 14:45 | USD | Manufacturing PMI Jan P | 47.7 | 47.9 | ||

| 14:45 | USD | Services PMI Jan P | 51.1 | 51.4 | ||

| 15:30 | USD | Crude Oil Inventories | -1.2M | -2.5M | ||

| 15:30 | CAD | BoC Press Conference |

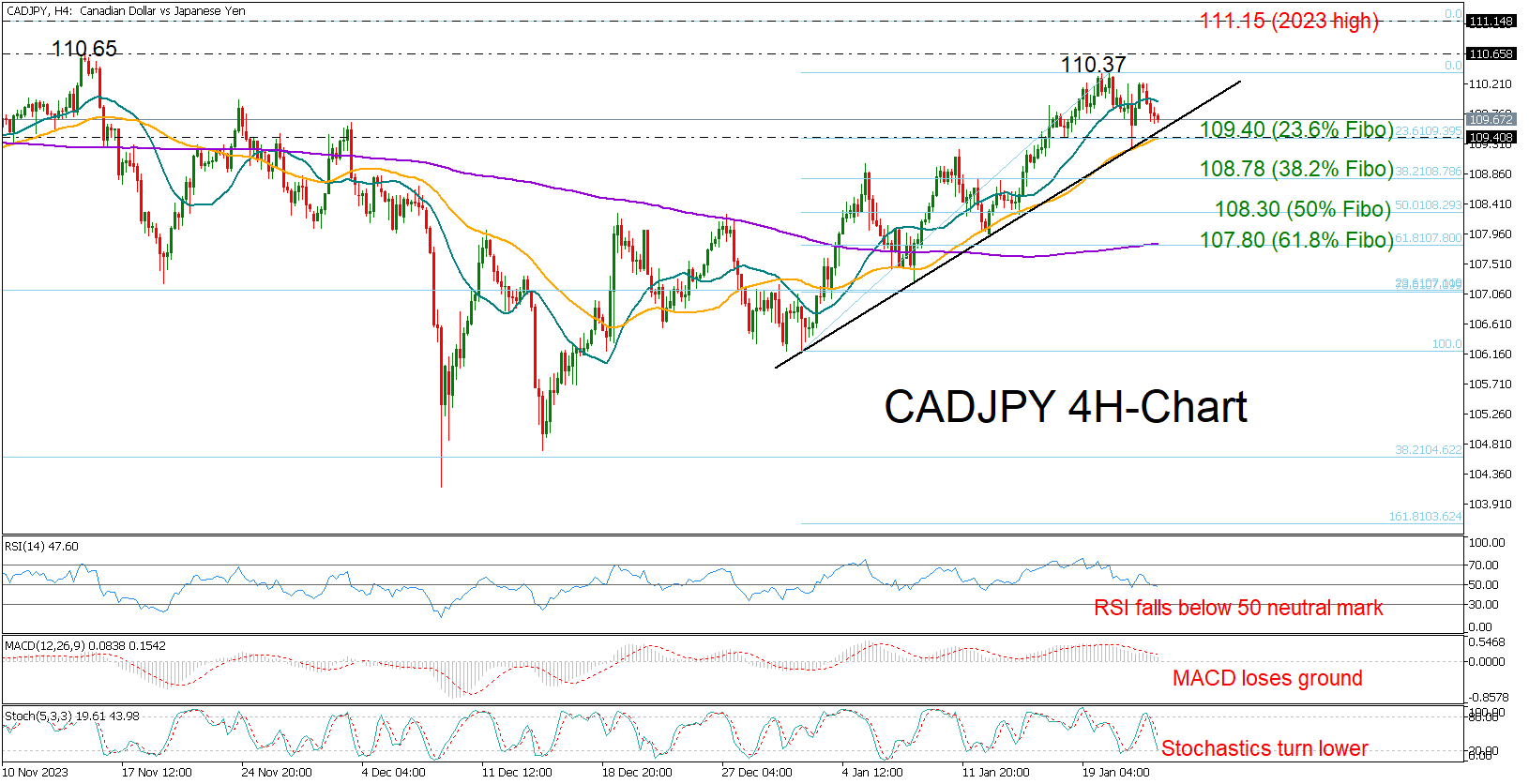

CADJPY Pulls Below 2-Month High Ahead of BoC Rate Decision

- CADJPY leans to the downside after two-month high

- 2024 uptrend remains intact above 109.50

- BoC policy announcement due at 15:00 GMT

CADJPY lost momentum after the peak at a two-month high of 110.37 on Monday, but January’s series of higher highs and higher lows on the four-hour chart remain intact and only a break below the 50-period simple moving average (SMA) and the support trendline at 109.40 would put the upward trajectory in doubt.

The technical indicators favor the bearish scenario as the RSI is crossing below its 50 neutral mark and the stochastic oscillator is shifting southwards. The MACD keeps decelerating below its red signal line, adding to the discouraging signals.

If the price drops below the ascending trendline and the 50-period SMA, which coincides with the 23.6% Fibonacci retracement of the 2024 uptrend, it could meet the 38.2% Fibonacci mark of 108.78. The 50% Fibonacci of 108.30 could next come into view ahead of the 61.8% Fibonacci of 107.80 and the 200-period SMA.

Should the upward pattern strengthen above November’s high of 110.65, the door will open for the 2023 top of 111.15. The 112.00-112.50 area last seen during 2007-2008 could be the next obstacle.

In summary, CADJPY is facing a weakening bias, but sellers may stay patient until they see a close below 109.40.

European PMIs weaker than analysts’ forecasts but didn’t disappoint markets

Preliminary January PMIs for Germany showed a worsening of the situation contrary to the expected improvement. The composite PMI in January was at 47.1 against 47.4 a month earlier, and there are forecasts of an increase to 47.8.

The reason for the deterioration was a dip in the services sector. The index of activity in this sector fell to 47.6 – the lowest since August – instead of the expected 49.3. Activity in Germany’s services sector has been contracting since August despite relatively low energy prices. And this could be an indication that the weight of interest rates is spreading through the economy.

Earlier, Germany’s Ifo Institute lowered its forecast for economic growth in 2024 from 0.9% to 0.7%. Some forecasters expect GDP to decline this year. These expectations and weak economic indicators reinforce expectations that the ECB will soon move to ease monetary policy, as weakness in the national economy may soften Germany’s traditionally very hawkish stance.

Indicators for the whole eurozone came out slightly weaker than expected. The composite PMI rose from 47.6 to 47.9 despite Germany’s failure. That said, the index remains in contractionary territory, i.e. below the 50 level.

The manufacturing sector, although presenting a relatively small share of the economy, acts as a reliable leading indicator. Both Germany and the Eurozone have seen a steady rise in Manufacturing PMI, setting the mood for an acceleration in the economy over the next couple of quarters.

The currency market was more influenced by the strength of the rest of the Eurozone data than by the disappointment with the German statistics. Optimism on the stock markets, also supported today by the positive dynamics of China, has played its role in the Euro’s purchases and return to 1.09.

Gold Not Out of the Woods Yet

- Gold below key barriers ahead of next week's FOMC policy announcement

- Technical signals cannot promise a meaningful rally

Gold has been in a tight range within the 2,016-2,030 region so far this week, struggling to find enough buyers to close successfully above its exponential moving averages (EMAs) on the four-hour chart and the broken support trendline from November.

The technical indicators point to a neutral-to-bullish bias, with the RSI maintaining a sideways trajectory above its 50 neutral mark and the MACD set to enter the positive region. That said, the current consolidation phase seems to be developing within a monthly bearish channel, which could also halt any potential bullish extensions near 2,040.

A successful close above 2,040 is required for a fast rally towards the 2,065 constraining zone. Even higher, the price could re-challenge December’s important 2,079-2,087 territory ahead of the 2,100 psychological mark. Should the bulls claim the latter, the spotlight will fall again to the record high of 2,144.

If the precious metal slides below the 2,016 support area instead, a new bearish wave could start towards the channel’s lower boundary seen at 1,990. Additional losses from there could retest December’s floor around 1,976.

Summing up, gold could remain exposed to downside risks unless it closes clearly above the bearish channel and the 2,040 level.

USDCAD: Key Levels to Consider for Further Upside or Deeper Correction

Bullish Scenario: Consider buying at levels 1.3428 or 1.3462 with take profit targets at 1.3990 (TP1), 135.00 (TP2), and 1.3510 in extension (TP3). It is recommended to set a stop loss (S.L.) below 1.3410 or at least 1% of the account capital**.

Bearish Scenario: Selling below 1.3460 (waiting for a retracement to the zone) with TP1 at 1.3430, TP2 at 1.3415, and TP3 at 1.34 in extension. It is advised to place a stop loss above 1.3477 or at least 1% of the account capital**. A trailing stop can be utilized.

Fundamental Analysis

Today, Wednesday, January 24, the Bank of Canada (BoC) issues its first policy statement of 2024 at 14:45. No change in the current interest rate of 5.00% is expected.

According to recent data, core inflation in Canada exceeded expectations in December, ruling out a significant shift in the dovish direction of the BoC in today's meeting. Despite this, some reports have highlighted the negative impact that high rates are having on other sectors of the economy.

The latest BoC Business Outlook Survey reported weakened demand and less favourable business conditions in the fourth quarter for investments, leading most companies to not plan new hires. However, lower inflation is still the primary goal of high rates and may soften in the coming months, favouring potential rate cuts starting in the second quarter, likely in April.

Daily Chart Analysis

The USDCAD pair has been in a macro bullish correction since the beginning of the month, reaching a peak at 1.3542 and forming a high-volume node that could be interpreted as a selling zone. From here, we evaluate key levels for two possible scenarios:

Bearish Scenario:

If quotes fall below the week's opening at 1.3426, sales towards the current Point of Control (POC) of the month (which may vary as the month has not ended) at 1.3355 can be expected. This level formed the last price buying zone and coincides with a Fibonacci retracement of 50%. This zone can act as a pivot defended by the bulls or be broken by bearish force.

Only a decisive breakout of the high-volume node forming the buying zone will indicate a continued downtrend with a target at the macro support of 1.3174.

Bullish Scenario:

After a 50% correction, a rebound from 1.3355 will offer an opportunity to activate a new upward impulse towards 1.3542, the next selling zone from December around 1.3592, and resistance at 1.3619, reversing the macro downtrend with a decisive or confirmed breakout with two rising highs.

Anticipated: An early rebound will occur with the failure of the price to break below the weekly opening of 1.3426 and the rapid surpassing of 1.35 and 1.3542, opening the door to further ascent towards 1.3619 and beyond into February.

H1 Chart Scenario:

The formation of a reversal pattern below the resistance at 1.3494 anticipates a short-term bearish scenario, especially with quotes below the uncovered POC* of the early sessions at 1.3462, near the day's opening.

1. The first intraday scenario: Aims for sales at Monday's uncovered POC* at 1.3428, converging with the weekly opening. This buying zone is expected to be defended by the bulls, causing a new price rebound towards 1.35 and the Average Daily Range (ADR) High at 1.3510, signalling an intraday sequence change.

2. The second intraday scenario: Will be activated after the decisive breakout (candle body) of the buying zone around 1.3428, with a possible breakdown of support at 1.3415, indicating greater bearish strength seeking the next buying liquidity zone around 1.3374, likely in the next day.

*Uncovered POC: POC = Point of Control: It is the level or zone where the highest volume concentration occurred. If there was a bearish move previously from it, it is considered a selling zone and forms a resistance area. Conversely, if there was a bullish impulse previously, it is considered a buying zone, usually located at lows, forming support zones.

**Consider this risk management suggestion

It is crucial that risk management is based on capital and traded volume. For this, a maximum risk of 1% of the capital is recommended. It is suggested to use risk management indicators such as the Easy Order.

Bundesbank report warns of German economy’s vulnerability to China’s economic woes

In its latest monthly report, Bundesbank issued a cautionary message about China's current economic struggles and their potential impact on Germany. The report notes that China is grappling with "significant economic problems," and the relationship between China and Western industrial nations has "noticeably deteriorated recently." Such geopolitical risks, if they materialize, could have severe repercussions for the German economy.

The Bundesbank essay posits that "an economic crisis in China of the kind that has occurred in other countries in the past following a correction of excessive credit growth would probably be bearable for the German economy." However, the impact would not be negligible, with projections indicating that Germany's real GDP could be -0.7% lower in the first year of a potential crisis in China, and then -1% in the second year.

The report also highlights a more severe scenario: "However, an abrupt decoupling, for example as a result of a geopolitical crisis, would have a significantly greater impact on German industry in particular." In such an event, German companies with direct involvement in China could face considerable losses in sales and profit. Industries like automotive, mechanical engineering, electronics, and electrical engineering are particularly reliant on Chinese demand.

Moreover, Bundesbank emphasizes the broader risks associated with the close economic ties between Germany and China: "the close real economic ties between Germany and China also pose considerable risks for the German financial system."