Sample Category Title

US ISM Services Misses as Prices Jump to 2022 High, Jobs Contract on Iran Oil Shock

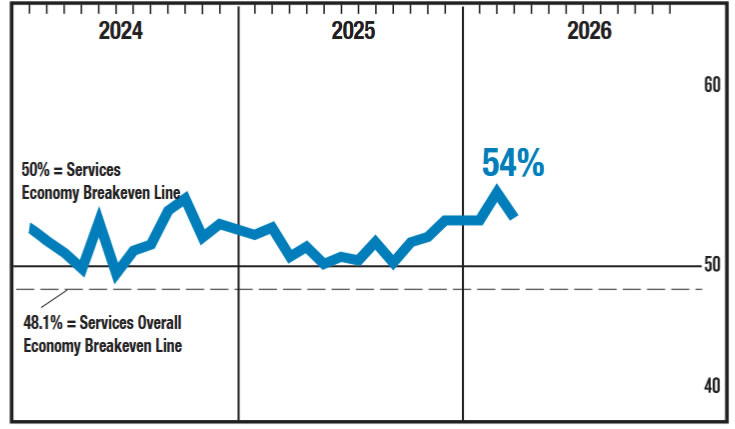

US ISM Services PMI slowed in March, but the bigger signal came from inflation, with prices surging to the highest level since 2022 as the Iran-driven oil shock feeds through the economy. The headline index fell from 56.1 to 54.0, missing expectations of 55.0, pointing to moderating growth even as cost pressures intensify.

Under the hood, activity softened notably. Business Activity/Production dropped from 59.9 to 53.9, its lowest level since September 2025. Employment fell from 51.8 to 45.2, slipping back into contraction for the first time in four months. This suggests firms are becoming more cautious on hiring even as demand conditions remain mixed.

At the same time, demand has yet to roll over. New Orders rose from 58.6 to 60.6, indicating resilience in underlying consumption. However, the divergence between strong orders and weakening employment highlights growing uncertainty among businesses as cost pressures rise.

The inflation side was the standout. Prices jumped sharply from 63.0 to 70.7, the highest reading since October 2022, driven by rising fuel and transportation costs linked to the Middle East conflict. ISM noted that “the predominant commentary this month was about impacts and adjustments due to the conflict with Iran,” with companies reporting higher gas and diesel prices and building inventories to guard against disruptions.

Supply chains are also feeling the strain. Supplier Deliveries rose from 53.9 to 56.2, reflecting slower deliveries amid shipping disruptions and flight issues.

Overall, while the index still points to around 1.9% annualized GDP growth, the mix of cooling activity and surging prices reinforces a stagflation signal.

Silver Flushes Weak Hands, Finds Floor at 70, But 80 Remains Out of Reach

Silver didn’t just survive last Thursday’s selloff—it revealed something important. The nearly 9% plunge was a stress test, and the market’s response—holding firmly above 70—signals that the defense of 70 is more than technical noise. It may mark the point where control shifted from weak to strong hands.

The selloff could have delivered a clean positioning reset. Leveraged longs were forced out in size, with weak hands flushed out in a single session. But what followed was just as critical: strong hands stepping in quickly, absorbing supply and preventing a deeper breakdown.

Crucially, the market refused to wait for 60. That level remains the most important value zone, yet buyers chose to act early, stepping in at 70 instead. This behavior reflects a change in mindset—less patience, more urgency—as participants position ahead of tightening supply conditions and persistent geopolitical uncertainty.

Those structural factors are still in play. With supply deficits extending into a fifth consecutive year, Silver has a fundamental cushion underneath it. This doesn’t guarantee a rally, but it strengthens the case that the downside is increasingly supported, especially after such a sharp flush lower.

However, the upside story remains incomplete. Silver continues to face yield-driven pressure, with its non-yielding asset sensitivity limiting gains in a high-rate environment. A move toward 80 will need yield relief, likely through falling US 10 yield from the current 4.3% towards 4.2%. Until that happens, rallies—while possible—are likely to stall below key resistance, leaving 80 just out of reach for now.

Technically, for now, further rise is expected as long as 66.70 support holds. Break of 76.29 will resume the rebound from 60.97 towards 38.2% retracement of 121.83 to 60.97 at 84.21. However, break of 66.70 will likely bring another test of 60.97, or probably even a brief breach of 60 psychological level, before Silver forms a durable bottom.

Chart Alert: WTI Crude Oil Whipsawed Above 20-day MA Ahead of Trump’s Speech and US-Iran Ceasefire Hopes

Key takeaways

- Volatility driven by ceasefire uncertainty: WTI crude surged above $102.25 to as high as $116 before reversing sharply, with an intraday whipsaw driven by conflicting signals around a potential US–Iran ceasefire and Trump’s rhetoric.

- Ceasefire expectations skewed to June: Prediction market assigns low odds of a ceasefire by end-April (~22.5%) but sees a higher probability (~51.5%) by end-June, keeping near-term geopolitical risk elevated.

- WTI bullish trend intact but key levels critical: The breakout above $102.25 signals a continuing bullish sequence, with upside toward $124–$132 if momentum holds, while a break below $102.25 risks a pullback toward $96–$93.

The West Texas oil CFD (a proxy of the WTI crude oil futures) has staged the expected bullish move, where it cleared above $102.25 per barrel and hit a closing level of $112.84 last Thursday, 2 April 2026, before the Easter holiday.

Market participants continue to discount the “optimism of a ceasefire deal” between the US and Iran from US President Trump’s social media posts and public speeches made in the past week.

In today’s early Asian session (Monday, 6 April 2026), the price actions of the West Texas oil CFD gapped up by 2.9% to print a current intraday high of $116.17, just shy of its 4-year high of $119.54 recorded on 9 March 2026, as the market digested the possibilities of further hostilities between US and Iran where Trump posted a social media with foul language, warning Iran’s power infrastructure will be destroyed if Tehran does not open the Strait of Hormuz by Tuesday, 7 April 2026 8.00 p.m. Eastern Time (an extension of an earlier Monday deadline).

Interestingly, the earlier gains of the West Texas oil CFD were all wiped out as it declined by 2.3% at $110.27 at the time of writing.

Ceasefire hopes are the primary driver of the current intraday whipsawing in oil prices. An Axios report stated that the US, Iran, and a group of regional mediators are discussing terms for a potential 45-day ceasefire that may lead to a permanent end to the war. In addition, US President Trump said he plans a news conference on Monday at 1.00 p.m. Eastern Time.

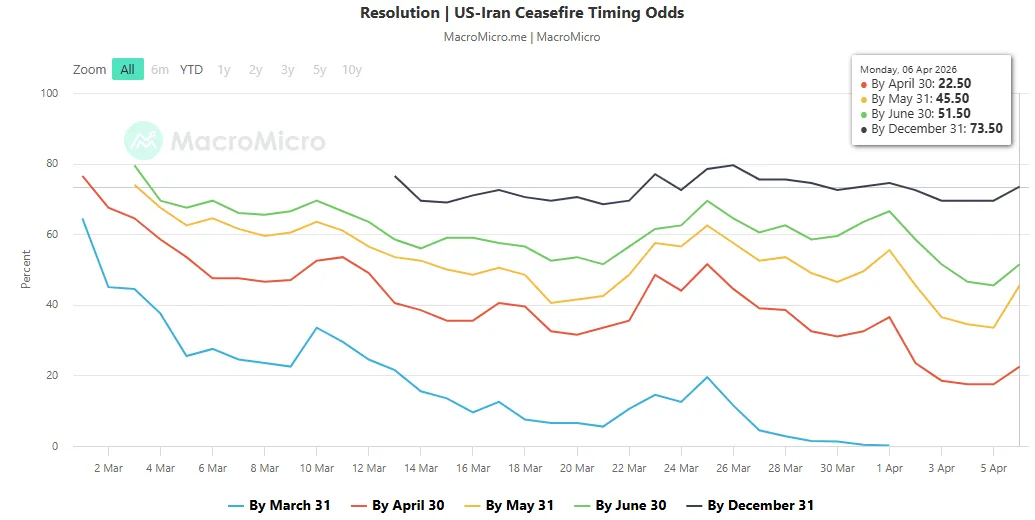

Prediction market is still expecting a US-Iran ceasefire in June 2026

Fig. 1: Polymarket US-Iran ceasefire timing odds as of 6 Apr 2026 (Source: MacroMicro).

The above chart reflects the market-implied probability of an official ceasefire agreement between the US and Iran on various specific dates from the prediction market platform, Polymarket, where participants trade contracts based on the probability of future events.

As of Monday, 6 April 2026, the probability of a ceasefire by 30 April remains low at 22.5%, while the likelihood rises significantly to 51.5% by 30 June (see Fig. 1).

Let’s now focus on the potential short-term trajectory (1 to 3 days) of WTI crude oil from a technical analysis perspective

WTI Crude Oil – Minor bullish impulsive up sequence from 23 March 2026 low remains intact

Fig. 2: West Texas Oil CFD minor trend as of 27 Mar 2026 (Source: TradingView).

The West Texas oil CFD (a proxy of the WTI crude oil futures) managed to stage a bullish breakout last Thursday, 2 April 2026, from a three-week sideways range configuration

Hence, a potential minor bullish impulsive up move sequence has kick-started from its 23 March 2026 low (see Fig. 2).

Watch the $102.25 short-term pivotal support to maintain the near-term bullish bias. A clearance above $116.56/119.54 sees the next intermediate resistances to come in at $124.40 and $131.30/132.67(also close to a Fibonacci extension cluster).

However, failure to hold at $102.25 and an hourly close below it negates the bullish tone for another round of minor corrective pull-back to retest the next intermediate support zone at $96.44/93.70 (also the 20-day moving average).

Key elements to support the near-term bearish bias on WTI crude oil

- The price actions have continued to oscillate within a minor ascending channel in place since the 23 March 2026 low, with its channel support coming in at around $102.25

- The hourly RSI momentum indicator is still holding above its pull-back support at around the 50 level.

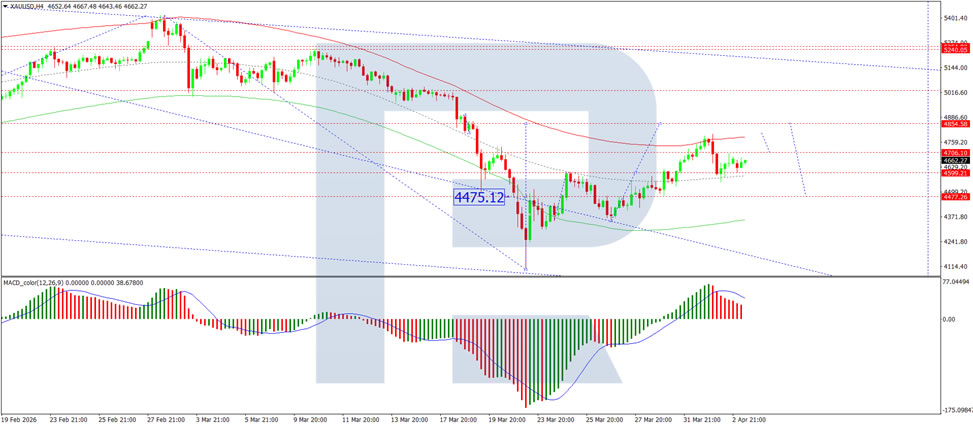

Gold – 12% Decline Since Middle East Conflict Began: This May Not Be the Limit

Gold declined to 4,600 USD per troy ounce on Monday, extending losses from the previous session. Pressure intensified after Donald Trump issued a new ultimatum to Iran, threatening strikes on energy and civilian infrastructure unless the Strait of Hormuz is reopened.

Trump signalled his readiness to sharply increase pressure and set a new deadline, further heightening tensions in financial markets. Tehran has rejected the demands and continues to target energy facilities in the region.

Since the onset of the conflict, gold has lost approximately 12% of its value. Rising energy prices are amplifying inflation risks and reinforcing expectations of higher interest rates, which limit demand for the metal.

Moreover, gold is not fully fulfilling its traditional role as a safe-haven asset. Some investors are being forced to unwind positions to cover losses in other market segments, adding further downward pressure on prices.

Technical Analysis

On the H4 XAU/USD chart, the market is forming a consolidation range around 4,599 USD. An upside breakout would open the way for a correction towards 4,854 USD, while a downside breakout could mark the beginning of a new downward wave towards 4,477 USD. The MACD indicator confirms the current momentum, with its signal line above the zero line and pointing firmly upwards.

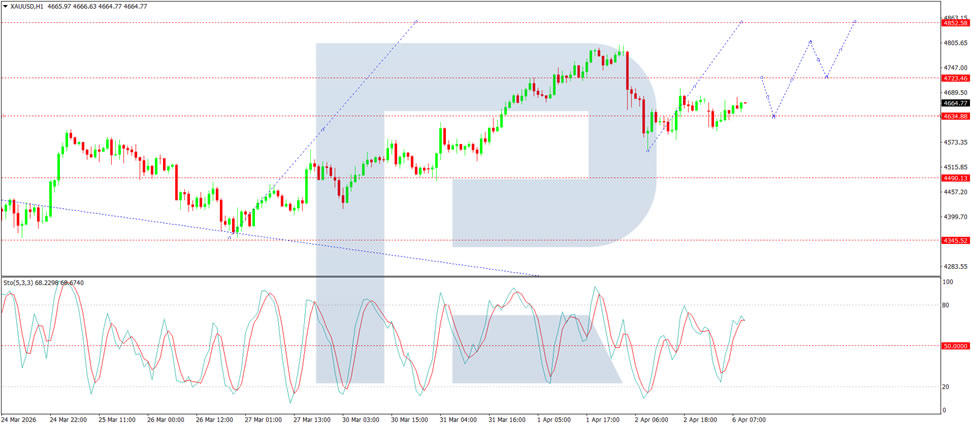

On the H1 chart, the market has broken above 4,636 USD and is forming a wave towards 4,737 USD. Looking ahead, a corrective move back to 4,636 USD is likely, followed by a renewed advance towards 4,852 USD. The Stochastic oscillator supports this scenario, with its signal line above 50 and pointing towards 80.

Conclusion

Gold’s 12% decline since the start of the Middle East conflict highlights a market paradox: escalating geopolitical tensions have failed to support the traditional safe-haven asset. Instead, surging energy prices have intensified inflation concerns, pushing interest rate expectations higher and weighing on the non-yielding metal. Forced liquidation by investors covering losses elsewhere has added to the selling pressure. With Trump issuing a new ultimatum and Tehran rejecting the demands, the conflict shows no signs of easing. While technical indicators suggest scope for a short-term rebound, gold’s broader trajectory remains vulnerable, and further downside cannot be ruled out.

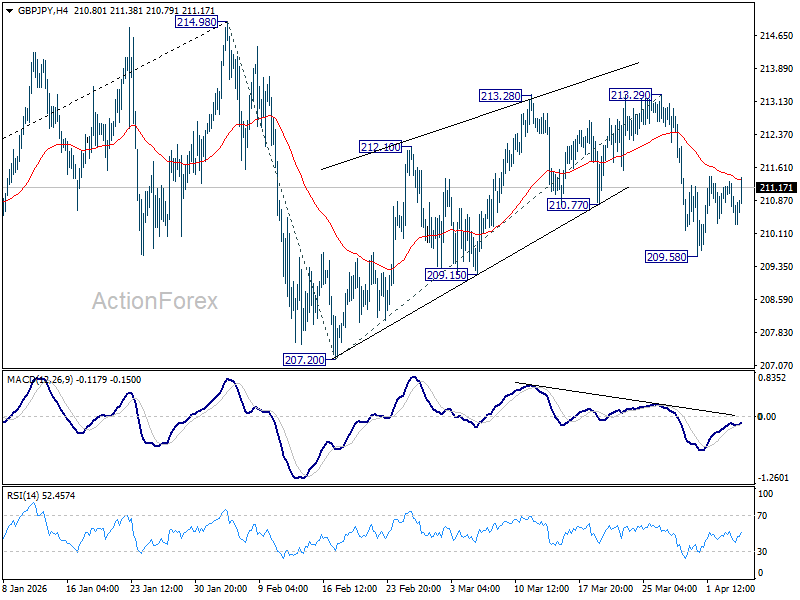

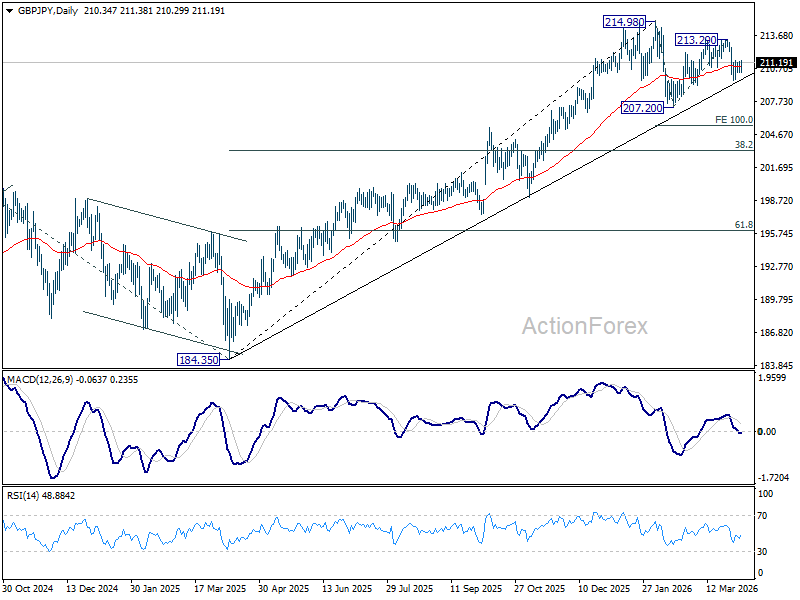

GBP/JPY Daily Outlook

Daily Pivots: (S1) 210.38; (P) 210.85; (R1) 211.29; More...

Intraday bias in GBP/JPY stays neutral first, and risk remains on the downside with 213.29 resistance intact. Corrective pattern from 214.98 should be in the third leg. Break of 209.58 will target 207.20 and below.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

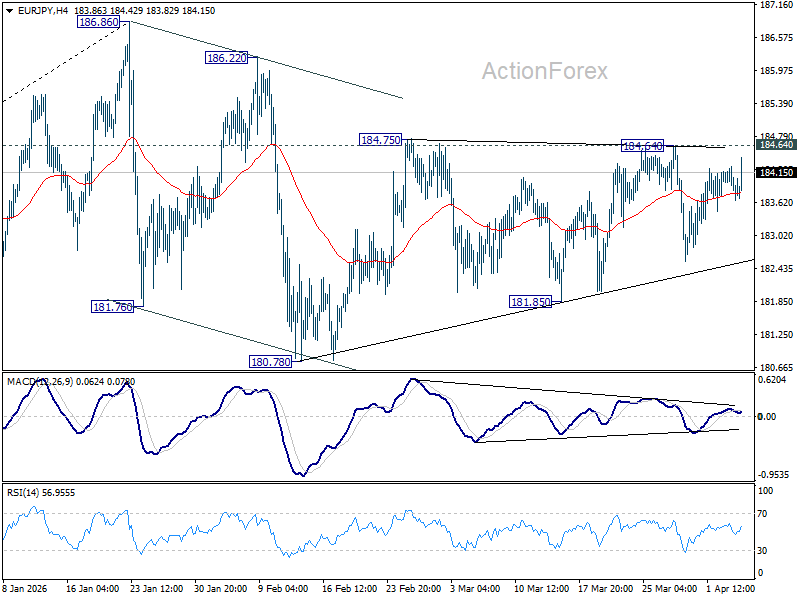

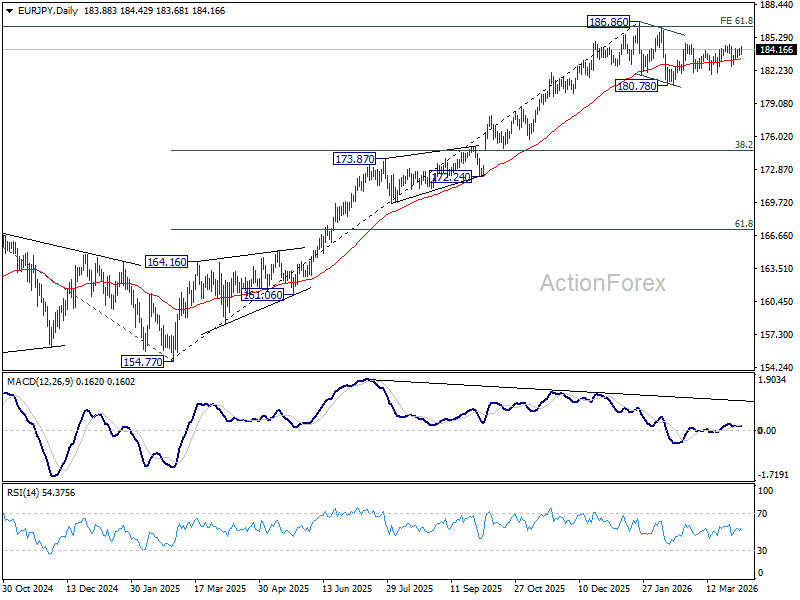

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.61; (P) 183.95; (R1) 184.24; More...

Range trading continues in EUR/JPY and intraday bias remains neutral. On the downside, firm break of 181.85 support should confirm that the correction from 186.86 is already in the third leg. Deeper fall should be seen to 180.78 and below. However, break of 184.75 resistance will bring stronger rally to retest 186.86 high instead.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 176.21) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

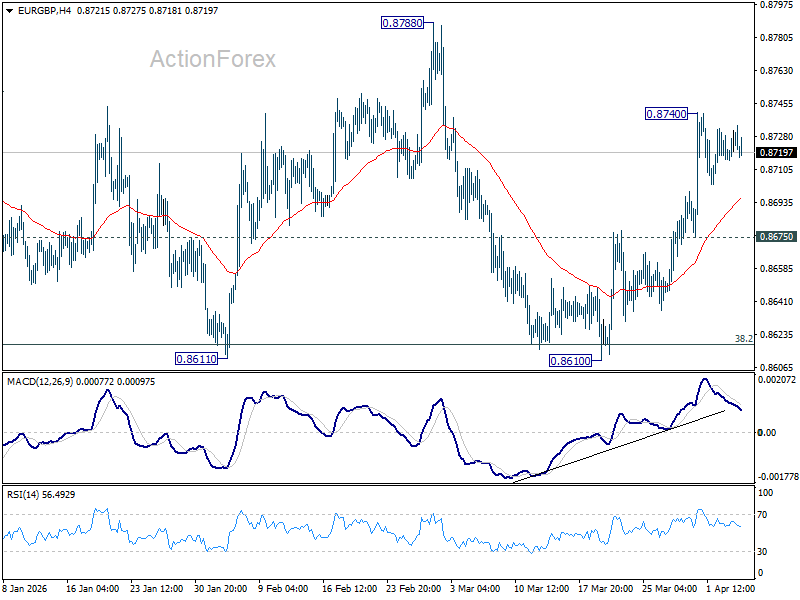

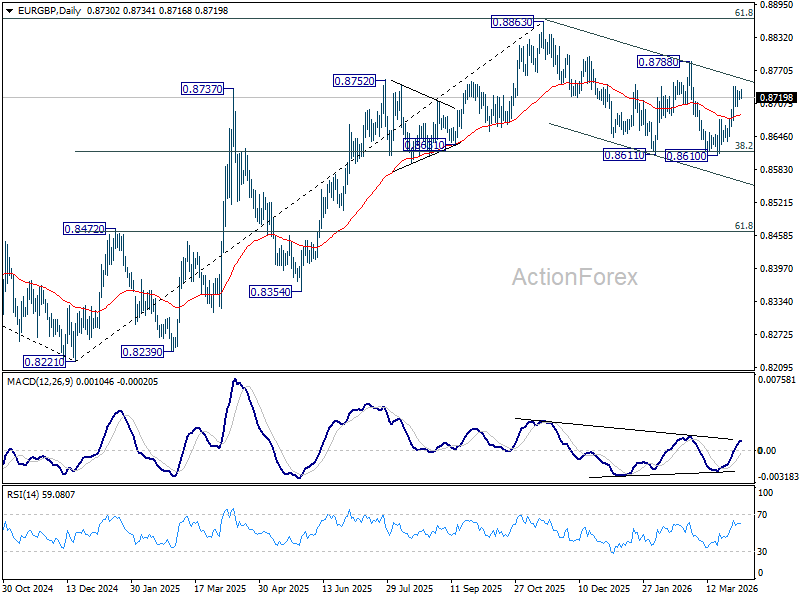

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8717; (P) 0.8725; (R1) 0.8734; More…

EUR/GBP is staying in consolidations below 0.8740 and intraday bias stays neutral. On the upside, above 0.8740 will resume the rebound from 0.8610 short term bottom to 0.8788 resistance next. However, break of 0.8675 will bring retest of 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be resume to resume through 0.8863. Nevertheless, sustained trading below 0.8618 should confirm reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

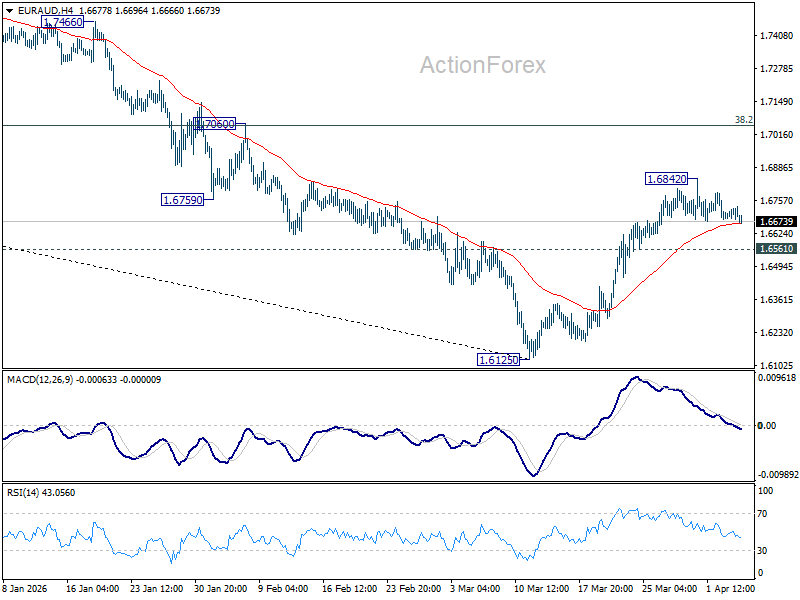

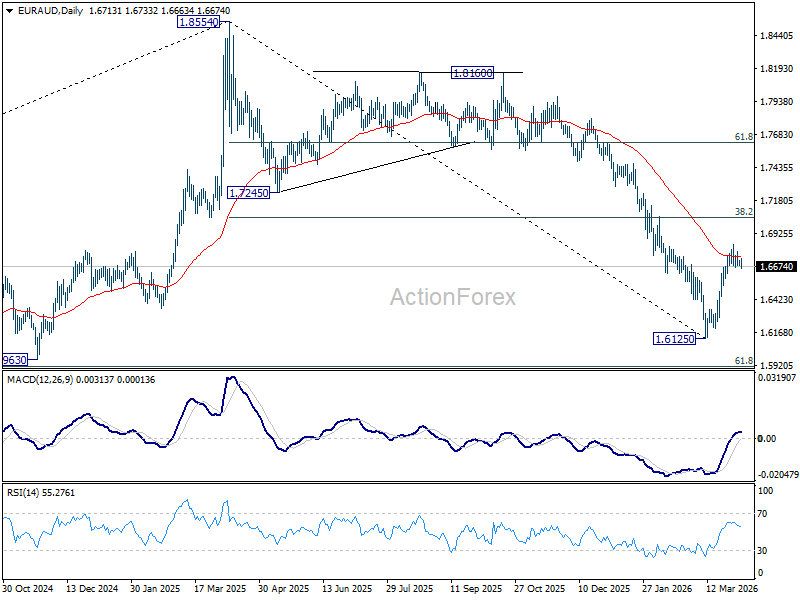

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6688; (P) 1.6709; (R1) 1.6730; More...

EUR/AUD is extending consolidations below 1.6842 and intraday bias remains neutral. On the upside, above 1.6842 will resume the rebound from 1.6125 to 38.2% retracement of 1.8554 to 1.6125 at 1.7053. However, break of 1.6561 minor support will argue that the rebound fro 1.6125 has completed, after rejection by 55 D EMA (now at 1.6745). Retest of 1.6125 low should be seen next.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7207) holds, even in case of strong rebound.

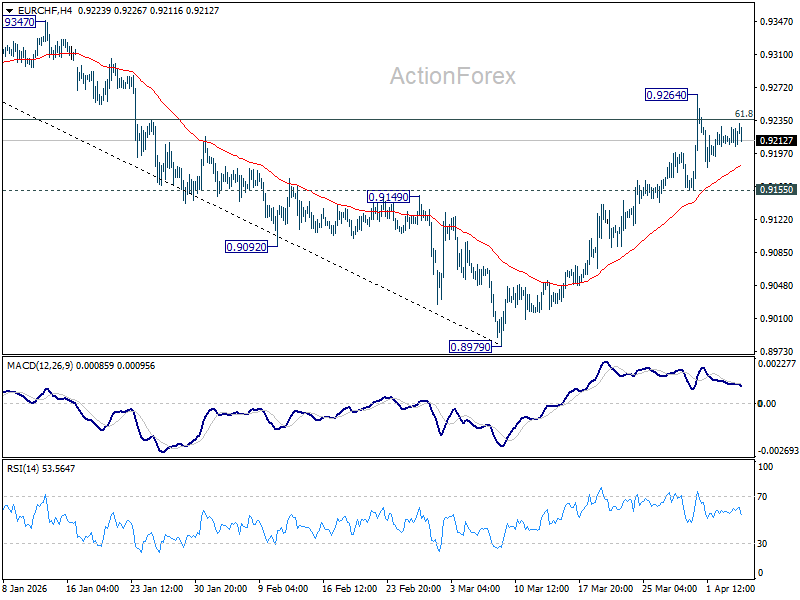

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9206; (P) 0.9218; (R1) 0.9228; More....

Intraday bias in EUR/CHF remains neutral and more sideway trading could be seen below 0.9264. On the upside, sustained trading above 61.8% retracement of 0.9394 to 0.8979 at 0.9235 will pave the way to 0.9394 key resistance next. However, break of 0.9155 support will turn bias back to the downside for 0.8979 low.

In the bigger picture, as long as 55 W EMA (now at 0.9281) holds, the larger down trend from 0.9928 (2024 high) is still expected to continue through 0.8979 at a later stage. However, sustained break of 55 W EMA should confirm medium term bottoming, and bring stronger rise through 0.9394 resistance, even as a corrective move.

Gold Price Slips Back, WTI Crude Oil Rally Gains Fresh Strength

Gold price rallied above $4,750 before correcting lower. Crude oil prices are rising and could climb further higher toward $110.00.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price gained pace for a move toward $4,800 and recently corrected lower against the US Dollar.

- A key bullish trend line is forming with support at $4,630 on the hourly chart of gold at FXOpen.

- WTI Crude oil prices are moving higher above the $100.00 resistance zone.

- There was a break above a bearish trend line with resistance at $97.00 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price was able to climb above $4,500. The price even surpassed $4,750 before the bears appeared.

The price traded close to $4,800 before there was a downside correction. There was a move below $4,750 and $4,700. The price settled below the 50-hour simple moving average, and RSI dipped below 50. There was a move below the 38.2% Fib retracement level of the upward move from the $4,351 swing low to the $4,800 high.

However, the bulls are active above $4,575 and the 50% Fib retracement. There is also a key bullish trend line forming with support at $4,630.

Immediate hurdle on the upside is $4,695 and the 50-hour simple moving average. The next major breakout level is $4,750. An upside break above $4,750 could send Gold price toward $4,800. Any more gains may perhaps set the pace for an increase toward $4,880.

If there is no fresh increase, the price could continue to move down. Initial support on the downside is near $4,630 and the trend line. The first key breakdown zone could be $4,520. If there is a downside break below $4,520, the price might decline further. In the stated case, the price might drop to $4,350.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a steady increase against the US Dollar. The price gained bullish momentum after it settled above $96.40.

The bulls pushed the price above the 50-hour simple moving average, and the RSI climbed toward 75. Besides, there was a break above a bearish trend line with resistance at $97.00. The price tested the $105.85 zone and is currently consolidating gains.

There was a minor pullback below $103 and the 23.6% Fib retracement level of the upward move from the $92.78 swing low to the $105.86 low.

If there is a fresh increase, the price could struggle near $105.85. A close above $106.85 could send the price toward $108. The next key area of interest might be $110. Any more gains might send the price toward $112.

Conversely, the price might correct gains and test $100.85. The main bid area on the WTI crude oil chart could be $99.30, the 50% Fib retracement level, and the 50-hour simple moving average. If there is a downside break, the price might decline toward $96.40. Any more losses may perhaps open the doors for a move to $92.80.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.