Sample Category Title

Holiday-Thinned Trade Keeps FX Locked in Ranges

Trading in Asian markets was subdued at the start of the week, with activity dampened by the U.S. holiday and the approach of Lunar New Year. Many regional desks are already lightly staffed, leaving liquidity thin and conviction limited. The holiday mood has kept volatility compressed.

Major currency pairs and crosses are confined within Friday’s ranges, with little appetite to initiate fresh positions ahead of key catalysts. Dollar, Yen, and Euro are all holding steady, while commodity currencies are drifting modestly but without follow-through.

The week ahead, however, offers potential triggers. RBNZ policy decision, FOMC minutes from January meeting, and a heavy slate of UK data including inflation and employment could inject direction back into markets.

Beyond scheduled events, geopolitical developments may prove more consequential. The second round of U.S.–Iran talks in Geneva on Tuesday is drawing attention. The discussions aim to de-escalate tensions over Tehran’s nuclear programme and avert renewed military confrontation.

According to reports, Iran is pursuing an agreement that would provide economic benefits for both sides, including energy and mining investments as well as aircraft purchases. Progress would signal easing geopolitical risk in Middle East.

Any meaningful breakthrough could weigh on oil prices by reducing supply risk premium. In turn, that may spill over into Gold, which has recently been vulnerable after sharp technical selloff. Conversely, stalled negotiations could revive safe-haven demand.

In currency markets, relative performance remains fluid. Aussie is currently the strongest, followed by Loonie and Dollar, while Yen is lagging alongside Swiss Franc and Sterling. Euro and Kiwi are positioned mid-pack. Given the low-liquidity backdrop, these rankings could shift quickly once participation normalizes.

In Asia, at the time of writing, Nikkei is up 0.07%. Hong Kong HSI is up 0.52%. China is on holiday. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is up 0.001 at 2.214.

Japan sidesteps technical recession as Q4 growth barely grows by 0.1% qoq

Japan’s economy narrowly avoided a technical recession in Q4, but the rebound fell short of expectations. GDP rose just 0.1% qoq, below the 0.4% forecast, though an improvement from Q3’s -0.6% contraction. On an annualized basis, growth came in at 0.2%, recovering from -2.6% but well under the expected 1.6%.

Private consumption, which accounts for more than half of output, edged up 0.1%. Demand for mobile phones provided support, though spending on food and autos declined. External demand was weak, with exports falling -0.3% qoq, dragged down by soft automobile shipments.

Investment provided modest offsets. Business spending rose 0.2%, supported by strong demand for semiconductor-manufacturing equipment, while housing investment jumped 4.8%.

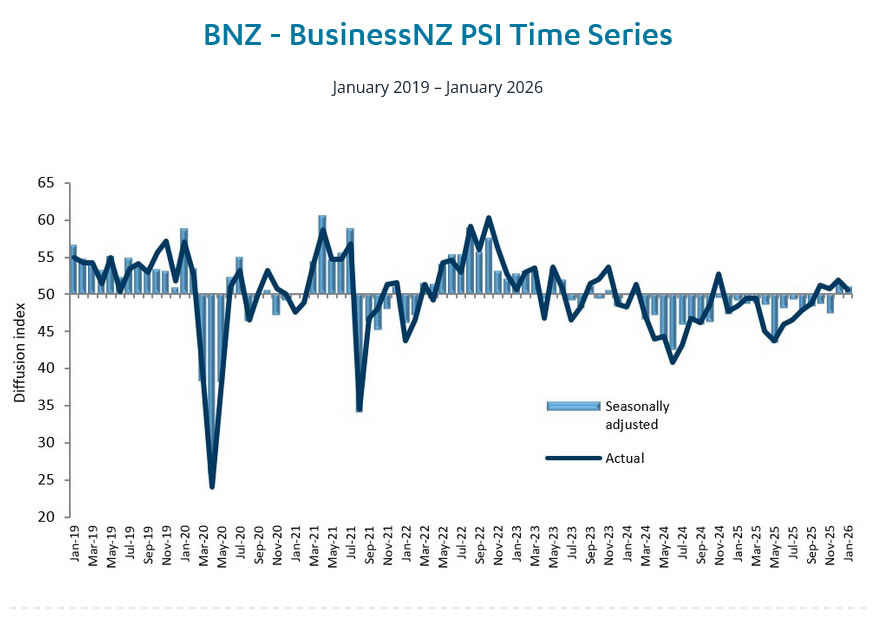

NZ BNZ services falls to 50.9, employment weakness offsets sales strength

New Zealand’s BusinessNZ Performance of Services Index eased from 51.7 to 50.9 in January, slipping further below the survey’s historical average of 52.8. While the index remains marginally in expansion territory, the details reveal a mixed picture. Activity and sales improved from 52.5 to 54.2, but employment deteriorated from 49.6 to 49.1, staying firmly in contraction. New orders edged lower from 52.1 to 51.8, suggesting demand momentum is softening at the margin.

Sentiment remains subdued. The proportion of negative comments rose sharply to 58.7%, up from 50.4% in December and 52.9% in November. Respondents cited seasonal disruptions from Christmas–New Year holidays, fewer enquiries, and a prolonged post-holiday lull. Elevated living and operating costs continue to weigh on business confidence, underscoring fragile recovery conditions.

Still, BNZ Senior Economist Doug Steel struck a more constructive tone, noting that data since late 2025 has reinforced confidence that positive momentum can be sustained. While services growth is hardly robust, the economy appears to be expanding gradually.

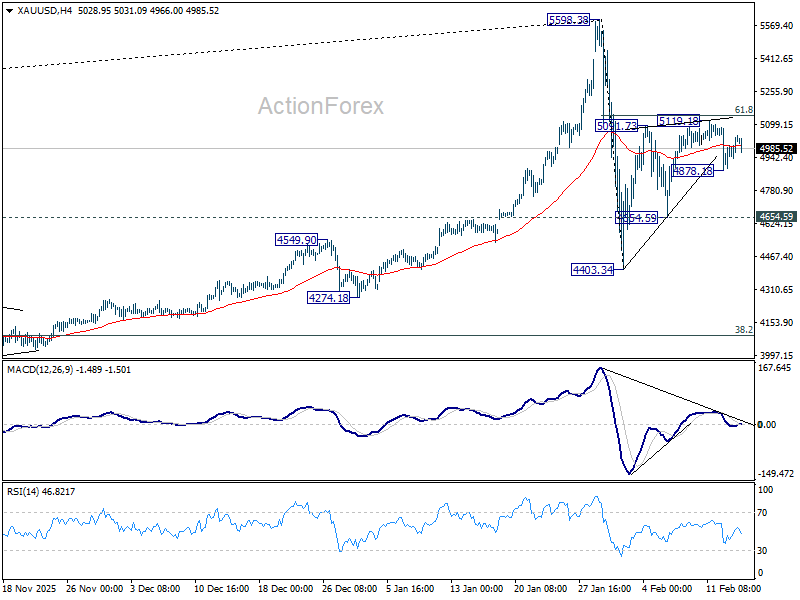

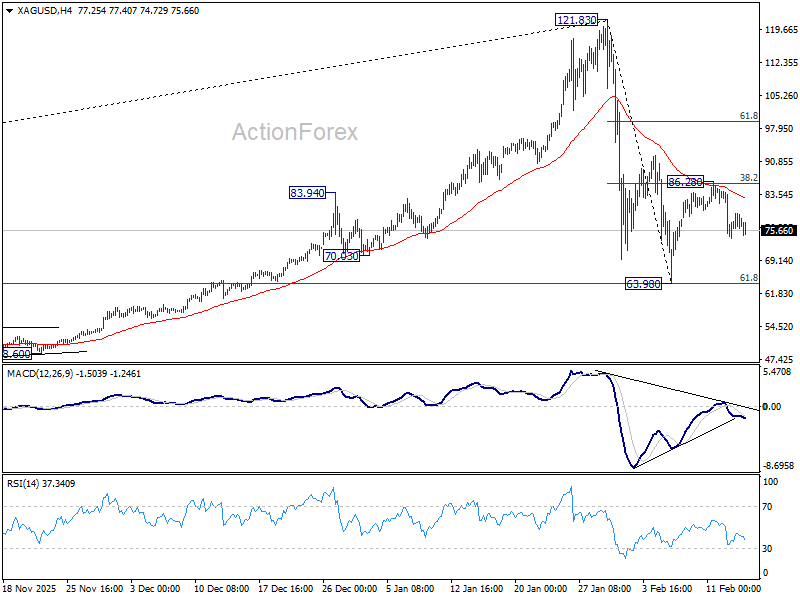

Gold and Silver risk revisiting February lows as corrective rebound fade

Gold and Silver are technically fragile after last week’s sharp mid-week selloff. The subsequent recoveries have lacked conviction, with momentum indicators failing to show meaningful upside traction. Price action suggests sellers remain in control in the near term. A retest of the early February lows now looks increasingly likely, particularly if Dollar stages a more notable rebound.

In broader context, both metals have transitioned into medium-term corrective phases. The powerful, unified macro narrative that fueled last year’s record-breaking rally is no longer present. Instead of a dominant theme like geopolitics or central bank policies, price movements are now more technical and intermarket-driven.

Technically, Gold’s break below its near-term rising trend line raises the risk that rebound from 4,403.34 has already completed at 5,119.18 in a three-wave corrective structure. As long as 5119.18 caps upside, near-term risks remain mildly skewed lower. Break below 4,878.18 temporary low could trigger acceleration toward 4654.59 support. A firm move through that level would open the door for retest of 4,403.34.

Silver shows similar vulnerability. Strong rejection at the 85 resistance zone — where 55 4H MACD rolled over and 38.2% retracement of 121.83 to 63.98 at 85.46 converged — suggests rebound from 63.98 has likely completed at 86.28. Deeper fall would be seen back to retest 63.98. But an immediate break there is not expected. Range trading between 63.98 and 86.28 may dominate in near term before broader decline from 121.83 resumes.

The week ahead: RBNZ hold, Fed minutes, UK CPI, and AU employment

This week’s macro calendar lacks a blockbuster event, but central bank communication and key inflation prints could still shift rate expectations at the margin. RBNZ stands as the only policy meeting, while FOMC minutes, UK CPI, and Australian employment data provide additional catalysts.

RBNZ is widely expected to hold OCR at 2.25%. After an aggressive easing cycle, policymakers are now in prolonged pause mode, allowing prior rate cuts to filter through economy. Growth has shown tentative stabilization, but recovery remains uneven. Inflation rebounded to 3.1% in Q4 from prior quarter, while one-year inflation expectations rose to 2.59%. Although uptick grabbed attention, with spare capacity lingering and unemployment still above average, RBNZ has little urgency to reverse course.

Late 2026 or early 2027 remains base case for an RBNZ rate hike. Guidance on tightening remains premature. However, tone matters. If policymakers sound increasingly confident that recovery is taking hold, markets could begin to price earlier normalization. That would offer near-term support to NZD, particularly against soft Dollar backdrop.

In US, focus shifts to FOMC minutes from January meeting. Rates were left unchanged at 3.50–3.75%, with only Governors Christopher Waller and Stephen Miran dissenting in favor of a cut. Both are well-known doves, so attention will center on broader committee debate.

The key question is whether majority views easing cycle as completed, or merely paused. March hold is effectively locked in, but nuance in discussion could shift June pricing slightly. Markets will parse language around inflation progress and labor market resilience for clues.

UK data calendar is heavier. Employment, wage growth, CPI, and retail sales all arrive as markets increasingly price March rate cut following dovish hold by BoE. Inflation dynamics remain decisive. Any faster-than-expected slowdown would cement expectations for imminent easing. Conversely, sticky wage growth would complicate picture and limit downside for Sterling. Political instability continues to weigh on GBP sentiment, leaving currency sensitive to macro surprises.

Australia’s employment data is another focal point. RBA surprised markets earlier this year by returning to rate hike stance amid renewed inflation pressure. While Q1 CPI remains critical for determining May decision, solid job and wage data would keep tightening bias alive.

Beyond that, Japan GDP, Canada CPI, and flash PMIs from major economies round out calendar.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Japan GDP; Eurozone industrial production; Canada housing starts, manufacturing sales.

- Tuesday: RBA minutes; Japan tertiary industry index; Germany CPI final; UK employment; Germany ZEW; Canada CPI; US Empire state manufacturing.

- Wednesday: New Zealand PPI; RBNZ rate decision; Japan trade balance; UK CPI, PPI; US durable goods orders; industrial production, FOMC minutes.

- Thursday: Australia employment; Eurozone current account; Canada new housing price index, trade balance; US jobless claims, Philly Fed survey, trade balance.

- Friday: Australia PMIs; Japan PMIs; UK retail sales, PMIs; Eurozone PMIs; Canada retail sales; US GDP revision, personal income and spending, PCE inflation, PMIs.

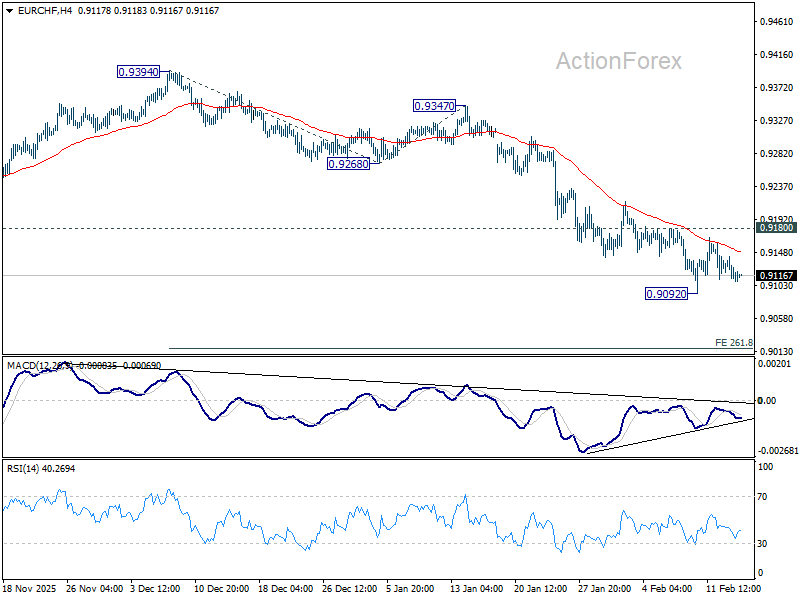

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9099; (P) 0.9122; (R1) 0.9135; More....

EUR/CHF is staying in consolidations above 0.9092 and intraday bias remains neutral. Further decline is expected as long as long as 0.9180 resistance holds. Firm break of 0.9092 will resume larger down trend and target 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143. However, considering bullish convergence condition in 4H MACD, decisive break of 0.9180 will indicate short term bottoming, and bring stronger rebound towards 55 D EMA (now at 0.9236).

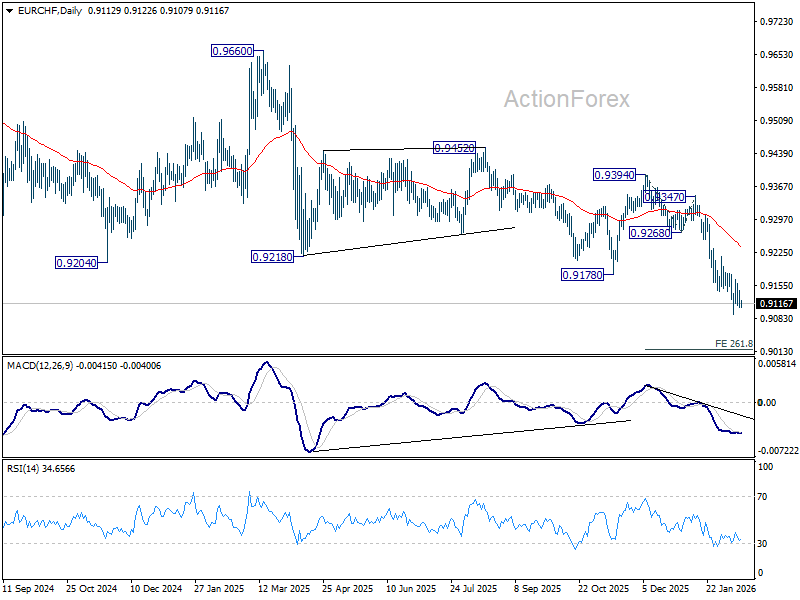

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9258) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

Gold and Silver risk revisiting February lows as corrective rebound fade

Gold and Silver are technically fragile after last week’s sharp mid-week selloff. The subsequent recoveries have lacked conviction, with momentum indicators failing to show meaningful upside traction. Price action suggests sellers remain in control in the near term. A retest of the early February lows now looks increasingly likely, particularly if Dollar stages a more notable rebound.

In broader context, both metals have transitioned into medium-term corrective phases. The powerful, unified macro narrative that fueled last year’s record-breaking rally is no longer present. Instead of a dominant theme like geopolitics or central bank policies, price movements are now more technical and intermarket-driven.

Technically, Gold’s break below its near-term rising trend line raises the risk that rebound from 4,403.34 has already completed at 5,119.18 in a three-wave corrective structure. As long as 5119.18 caps upside, near-term risks remain mildly skewed lower. Break below 4,878.18 temporary low could trigger acceleration toward 4654.59 support. A firm move through that level would open the door for retest of 4,403.34.

Silver shows similar vulnerability. Strong rejection at the 85 resistance zone — where 55 4H MACD rolled over and 38.2% retracement of 121.83 to 63.98 at 85.46 converged — suggests rebound from 63.98 has likely completed at 86.28. Deeper fall would be seen back to retest 63.98. But an immediate break there is not expected. Range trading between 63.98 and 86.28 may dominate in near term before broader decline from 121.83 resumes.

USD/JPY Falls to Key Support as AI Concerns Pressure Stocks

Last week, USD/JPY started higher after Sanae Takaichi’s strong election win. However, as the result was largely expected, selling soon entered the market. Even though U.S. employment data came in stronger than expected, adding 130,000 jobs and lowering the chances of a near-term U.S. rate cut, USD/JPY still ended the week lower.

U.S. stocks also fell over the week, with technology shares leading the decline. Investors are increasingly concerned about how artificial intelligence could affect existing business models. Weaker-than-expected U.S. Retail Sales added further pressure, although lower CPI data helped ease some inflation worries.

Bitcoin remained under pressure, with sellers continuing to dominate and concerns growing about its longer-term outlook. Gold, on the other hand, continued its steady rise as investors looked for stability.

Markets This Week

U.S. Stocks

Concerns about the impact of AI continued to dominate markets last week, a theme we have seen throughout 2026. After hitting record highs earlier in the week, the Dow turned lower as negative sentiment spread. The move below the 10-day moving average suggests the recent uptrend may be over for now. With AI concerns unlikely to disappear soon, selling into rallies may offer better trading opportunities this week. Resistance is at 50,500, 51,000, and 51,500, while support is at 49,500, 49,000, 48,500, and 48,000.

Japanese Stocks

The Nikkei started the week higher as markets viewed Takaichi’s victory as positive for Japanese stocks. However, weakness in U.S. equities and a stronger yen limited further gains. Although the recent uptrend remains strong, the market may move lower in the short term, especially if U.S. stocks stay under pressure. Without fresh positive news, gains may be difficult to sustain, so sideways to slightly lower movement is possible this week. Resistance is seen at 58,000円, 59,000円, and 60,000円, while support is at 56,000円, 55,000円, 54,000円, and 53,000円.

USD/JPY

USD/JPY moved lower as traders took profit after Takaichi’s victory. Attention has shifted to the narrowing interest rate gap between the U.S. and Japan, as the Bank of Japan continues to signal that further rate hikes are possible. The pair is still holding above key support at 152 and is trading well below the 10-day moving average, so a short-term bounce at the start of the week is possible. However, weaker-than-expected U.S. data could quickly push the pair lower again. Resistance is at 155, 156, 158, and 159, while support is at 152, 151, and 150.

Gold

Gold had a relatively quiet week, trading around the key $5,000 level. Prices moved lower at times, but strong buying interest remained, showing that gold is still in demand. Buying opportunities may offer the better strategy overall, but with the chart pointing to sideways movement near $5,000, buying on dips rather than chasing rallies may be the smarter short-term approach. Resistance is seen at $5,100, $5,200, $5,500, and $5,600, while support is at $4,900, $4,800, and $4,650.

Crude Oil

WTI crude traded sideways last week and failed to break above recent resistance, as tensions in Iran did not escalate further and the technical picture weakened. With prices now below the 10-day moving average, the market appears to be in a range, with slightly lower levels more likely in the short term. Resistance remains at $66.50, $70, and $75, while support is at $60, $55, and $50.

Bitcoin

Bitcoin traded sideways last week as investors reviewed the recent sharp fall and continued to question its long-term future. The price has moved back above the 10-day moving average, which is now flat, suggesting that another large drop is less likely in the short term. For now, range trading may offer the best opportunities as the market waits for clearer direction. Resistance is at $70,000, $75,000, $80,000, and $85,000, while support is at $65,000, $60,000, and $55,000.

This Week’s Focus

- Monday: Japan GDP and Industrial Production, E.U. Industrial Production

- Tuesday: E.U. German CPI and ZEW Economic Sentiment, U.K. Unemployment Rate

- Wednesday: Japan Trade Balance, U.K. CPI, U.S. Durable Goods, Housing Starts, Industrial Production and FOMC Meeting Minutes

- Thursday: Australia Unemployment Rate, U.S. Trade Balance

- Friday: Japan National CPI, U.K. Retail Sales and S&P Global Manufacturing PMI, E.U. HCOB Eurozone Manufacturing PMI, U.S. PCE Price index, S&P Global Manufacturing PMI, New Home Sales and Michigan Consumer Sentiment

Although the week may begin quietly due to the U.S. holiday, it could become more interesting as markets focus on Wednesday’s key economic announcements and the Fed minutes. Investors will be watching closely to see whether U.S. stocks come under further pressure. USD/JPY is approaching an important support level and is likely to see increased volatility. Meanwhile, Bitcoin has consolidated at lower levels and is worth monitoring closely for potential trading opportunities.

Japan sidesteps technical recession as Q4 growth barely grows by 0.1% qoq

Japan’s economy narrowly avoided a technical recession in Q4, but the rebound fell short of expectations. GDP rose just 0.1% qoq, below the 0.4% forecast, though an improvement from Q3’s -0.6% contraction. On an annualized basis, growth came in at 0.2%, recovering from -2.6% but well under the expected 1.6%.

Private consumption, which accounts for more than half of output, edged up 0.1%. Demand for mobile phones provided support, though spending on food and autos declined. External demand was weak, with exports falling -0.3% qoq, dragged down by soft automobile shipments.

Investment provided modest offsets. Business spending rose 0.2%, supported by strong demand for semiconductor-manufacturing equipment, while housing investment jumped 4.8%.

NZ BNZ services falls to 50.9, employment weakness offsets sales strength

New Zealand’s BusinessNZ Performance of Services Index eased from 51.7 to 50.9 in January, slipping further below the survey’s historical average of 52.8. While the index remains marginally in expansion territory, the details reveal a mixed picture. Activity and sales improved from 52.5 to 54.2, but employment deteriorated from 49.6 to 49.1, staying firmly in contraction. New orders edged lower from 52.1 to 51.8, suggesting demand momentum is softening at the margin.

Sentiment remains subdued. The proportion of negative comments rose sharply to 58.7%, up from 50.4% in December and 52.9% in November. Respondents cited seasonal disruptions from Christmas–New Year holidays, fewer enquiries, and a prolonged post-holiday lull. Elevated living and operating costs continue to weigh on business confidence, underscoring fragile recovery conditions.

Still, BNZ Senior Economist Doug Steel struck a more constructive tone, noting that data since late 2025 has reinforced confidence that positive momentum can be sustained. While services growth is hardly robust, the economy appears to be expanding gradually.

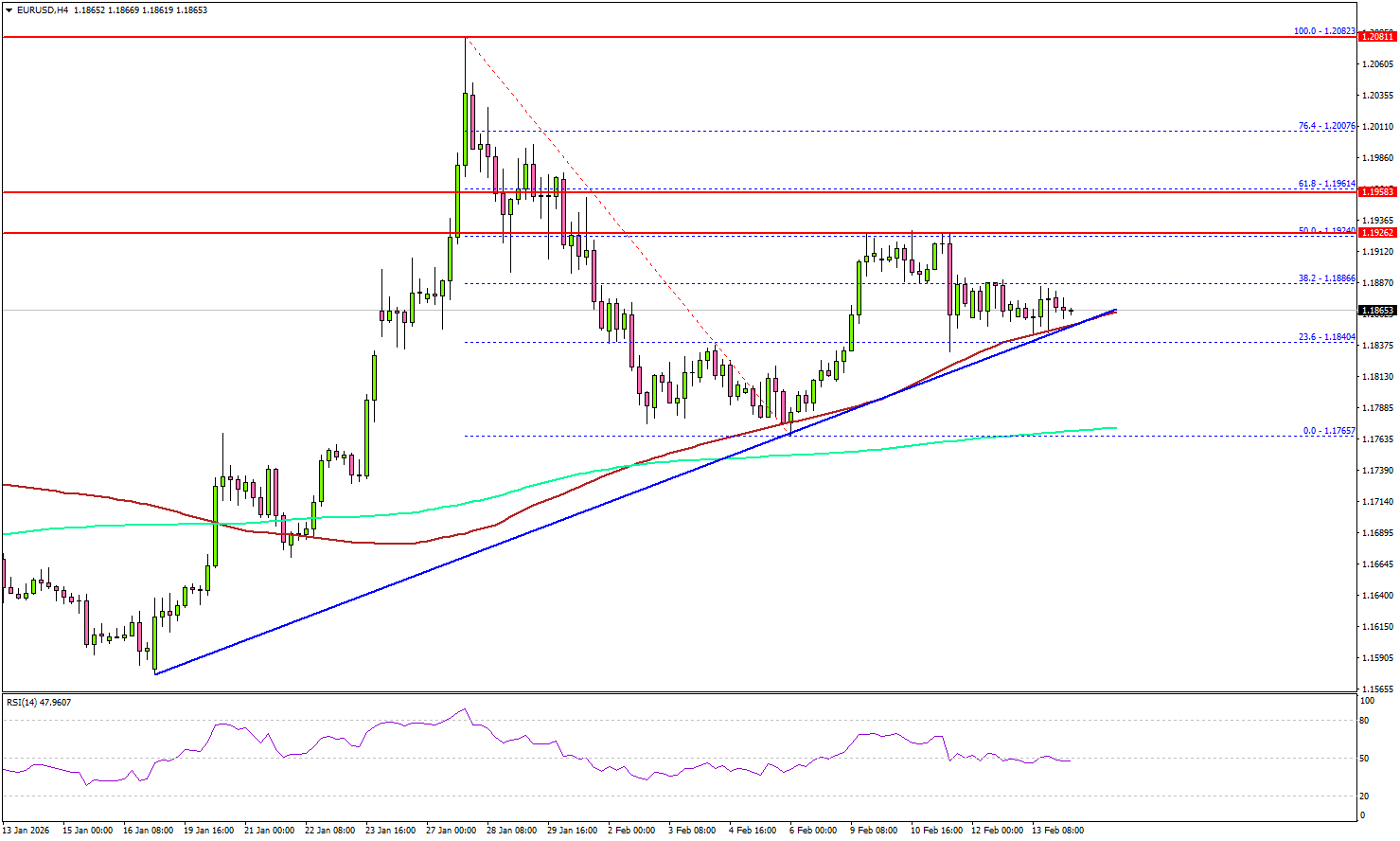

EUR/USD At Pivotal Juncture As Sellers Guard Resistance

Key Highlights

- EUR/USD found support at 1.1765 and corrected some losses.

- A key bullish trend line is forming with support at 1.1850 on the 4-hour chart.

- GBP/USD is consolidating above the 1.3600 support.

- Gold prices could resume upside if there is a move above $5,150.

EUR/USD Technical Analysis

The Euro dipped below 1.1800 against the US Dollar before the bulls appeared. EUR/USD found support near 1.1765 and recently started a recovery wave.

Looking at the 4-hour chart, the pair climbed above 1.1800 and the 38.2% Fib retracement level of the downward move from the 1.2082 swing high to the 1.1765 low. The pair even settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

On the upside, the pair is now facing hurdles near 1.1920 and the 50% Fib retracement level of the downward move from the 1.2082 swing high to the 1.1765 low.

The next stop for the bulls might be 1.1960. A close above 1.1960 could open the doors for more gains. In the stated case, the bulls could aim for a move to 1.2000 or even 1.2050. The main resistance sits near 1.2080.

Immediate support could be 1.1850 and the trend line. The first major area for the bulls might be near 1.1800. The main support sits at 1.1765, below which the pair might gain bearish momentum. In the stated case, it could even revisit 1.1660.

Looking at GBP/USD, the pair is slowly moving higher from 1.3520 but faces hurdles near 1.3680 and 1.3720.

Upcoming Key Economic Events:

- Euro Zone Industrial Production for Dec 2025 (MoM) - Forecast -1.5%, versus +0.7% previous.

FOMC to Remain Constrained by Inflation in 2026

The growth outlook is sanguine, but for inflation risks are clear.

The US economy continued to perform strongly through the turn of the year despite acute uncertainty. According to the latest Atlanta Fed GDPnow nowcast, not even the longest Federal Government shutdown on record was enough to slow GDP growth to trend, let alone below it. In 2026, growth is likely to normalise towards trend after five years of outperformance, but the prospect of a sustained period of disappointing momentum currently seems remote. Despite the Administration’s preference for lower rates, there is little cause for the FOMC to continue cut materially from here.

Now available to January, nonfarm payrolls growth looks to be forming a base, having edged backwards during the six months to October but averaging monthly gains of 73k since. The unemployment rate has also oscillated between 4.2% to 4.4% since February 2025 – evidence of stabilisation not an upward trend.

Other labour market indicators also point to a fully employed labour force and balance between new entrants and job listings. Most notably, the Employment Cost Index and hourly earnings from the establishment survey both continue to point to robust nominal income gains, and the ISM employment indexes have recently bounced back from depressed levels.

US household wealth is meanwhile at record highs and continuing to grow thanks to broad-based gains across equities and real estate, albeit with the latter tracking a modest pace. Established households are benefiting from comparatively low debt levels and the historically low interest rates locked in following the pandemic. Marginal borrowers are also beginning to see adjustable rates edge lower – a 5-year fixed rate which then converts to a variable rate versus the traditional standard 30-year fixed rate.

Household cash flows and wealth therefore stand ready to offer robust support to renovation activity, new home purchases and discretionary consumption from 2026. Sentiment is the risk, however, with households still acutely aware of the cost to real incomes brought by sustained elevated inflation.

On that front, the latest readings are a concern, with the University of Michigan measure of sentiment 13% below its 5-year average and 32% below its full history average as at February. That is in large part due to backward-looking perceptions of household finances, despite the aforementioned nominal gains.

While there is less hard evidence, many businesses are arguably similarly placed to households, benefiting from robust conditions but concerned over what tomorrow may bring. For companies, the risk is two-sided, being exposed to supply constraints related to tariffs and reduced labour supply on the one and with consumers’ financial anxiety limiting their ability to reprice on the other. We therefore expect to see firms invest for efficiency and productivity through 2026 but, in aggregate, to eschew expanding capacity – the hyperscalers being an obvious exception.

This backdrop highlights a concern of ours not only for 2026 but also 2027 and into the medium term. Put simply: if consumption remains above trend, the labour market fully employed and businesses (in aggregate) capacity-constrained, it will be extremely difficult for the FOMC to bring inflation sustainably back to their 2.0%yr target from circa 2.5%yr pace in January. Indeed, given the persistent weakness seen in business investment since the GFC, an acceleration in inflation pressures remains a distinct possibility – annual core services inflation was 2.9%yr in January, and close to 5.0% on an annualised basis.

In light of the above, we have pushed out the last cut forecast for the FOMC this cycle from March to June 2026. We also must make clear that we have low conviction in this call, believing the economy is more likely to outperform than disappoint on activity and / or prices, in which case the FOMC would be justified to remain on hold for the foreseeable future.

We recognise this view deviates considerably from market pricing, which currently has two cuts by year-end and a high chance of another by June 2027, much of this reflecting expectations of a shift in approach once Kevin Warsh takes over from Jerome Powell as FOMC Chair in May. But, for the data to warrant such a course by the FOMC, we would need to see a material deterioration in the labour market, or the rapid abating of inflation pressures and associated risks. These outcomes are possible but, at present, seem unlikely.

This analysis first appeared in Westpac Economics’ February Market Outlook which also includes our latest forecasts for Australia, the global economy and financial markets.

Dollar Set to Test Multi-Decade Levels

Key themes for the US dollar and global FX markets.

The US dollar initially rallied from 97.9 in late-December to 99.4 mid-January. However, it then lost its way, falling back to a near 4-year low of 96.2, now 97.0. At the current level, the US dollar is around 15% below its mid-2022 peak and circa 1.5% under its 10-year average. Our baseline expectation is that the dollar will settle between its current level and the 20-year average over the coming 12-18 months, but risks are arguably skewed to the downside.

It is not as though we have a pessimistic view on the US economy, however. Indeed, quite the opposite. As detailed on page 16 of the February Market Outlook (linked below), our baseline expectation for 2026 is another year of above-trend growth, led by the consumer and tech infrastructure investment. Underlying this expectation is the view that the labour market will remain fully employed and wage growth ahead of inflation.

Along with the lagged effect of tariffs and evidence of capacity constraints across a number of key sectors such as housing, transport, energy and health, there is therefore good reason to believe that inflation will remain above the FOMC’s 2.0%yr target and risks skewed to the upside. The above views on growth and inflation are why we hold the expectation of one more cut from the FOMC loosely against market pricing for at least two cuts this year.

Why then do we expect the US dollar to fall further and risks to remain skewed to the downside? It is because of the opportunities elsewhere.

Regarding financial opportunities, the strong run for US equities limits the chance of further outperformance, the global dominance of US technology firms notwithstanding. Also, unlike the years immediately following the pandemic, the narratives around both Europe and Asia’s economies are increasingly focused on growth and economic development rather than trade risks, and investors have been taking note of these themes.

As important as the trends themselves are their likely persistence, with economic growth in Europe and Asia to continue receiving support over the coming decade and potentially beyond. This is a striking contrast to the US’ current situation where the upcycle in infrastructure spending is likely at or very near its peak, and the dividend from it likely to come in the form of distributed efficiency wins across the economy and for profits, more so than an outright surge in production and national income.

Considering recent developments by each bilateral exchange rate within the DXY group, euro and sterling have clearly been the big winners. Since mid-January, EUR/USD has risen from USD1.16 to USD1.19, which is materially above the average of the past decade, USD1.12. Sterling has followed suit, GBP/USD rising from USD1.30 in November (also its decade average) to USD1.36 today.

The Canadian dollar’s recent gain has been more modest, USD/CAD only falling from CAD1.39 in mid-January to CAD1.36, above the decade average of CAD1.33 (i.e. the Canadian dollar is still below its 10-year average versus the US dollar). Meanwhile, Japan’s yen has been little changed on net since mid-December, albeit with considerable volatility day-to-day amid a myriad of political and geopolitical developments.

Ahead, amongst the DXY pairs, relative changes are likely to follow a similar pattern, with euro and sterling most likely to show strength – we believe to respective peaks of USD1.22 and USD1.41 by mid-2027. The Canadian dollar is also expected to rally materially, but likely not until late-2027 and 2028 once growth has strengthened and trade uncertainties have been put to rest. At June 2027, we expect USD/CAD to only be marginally lower at CAD1.34. But by June 2028, we forecast USD/CAD to have fallen to CAD1.30. For each currency, there is clear upside against the US dollar, but likely only if downside US economic and / or policy risks assert.

A similar logic can be laid out for the yen. Prime Minister Sanae Takaichi and the LDP’s historic win in February’s lower house election will provide considerable scope for fiscal policy to aid growth and confidence amongst businesses and consumers – the latter group particularly if the suspension of the consumer tax on food goes ahead. Still, the stance of monetary policy is unlikely to change materially in the near term, and so yield support for the yen should hold at current levels, not increase. Yen appreciation is therefore only seen gaining momentum as growth sustains and persistent inflation gives the Bank of Japan cause to act. Global investment flows are also important for the yen’s outlook. We continue to look for USD/JPY to slowly track down to JPY145 at end-2026, then JPY139 come mid-2028, still well above 2019’s JPY109 level.

While not a constituent of the DXY index, China’s renminbi is evidence of participants growing belief in Asia. From a peak of CNY7.35 last April, USD/CNY has declined to CNY6.90 at present, a 6% appreciation for the renminbi. Ahead, we expect a similar sized appreciation against the US dollar, albeit spread across the next 18 months to CNY6.35 at mid-2028. If China’s Central Government can reset the domestic economy decisively, then additional strength could be seen over a short period. The investment China has undertaken across Asia and its underlying development prospects are likely to see gains in the renminbi spread to other regional currencies over time.

This analysis first appeared in Westpac Economics’ February Market Outlook which also includes our latest forecasts for Australia and the global economy.

Eco Data 2/16/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Jan | 50.9 | 51.5 | 51.7 | |

| 23:50 | JPY | GDP Q/Q Q4 P | 0.10% | 0.40% | -0.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | 3.40% | 3.20% | 3.40% | |

| 04:30 | JPY | Industrial Production M/M Dec F | -0.10% | -0.10% | -0.10% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | -1.40% | -1.50% | 0.70% | |

| 13:15 | CAD | Housing Starts Y/Y Jan | 238K | 265K | 282K | 281K |

| 13:30 | CAD | Manufacturing Sales M/M Dec | 0.60% | 0.50% | -1.20% | -1.30% |

| 21:30 | NZD |

| Business NZ PSI Jan | |

| Actual | 50.9 |

| Consensus | |

| Previous | 51.5 |

| Revised | 51.7 |

| 23:50 | JPY |

| GDP Q/Q Q4 P | |

| Actual | 0.10% |

| Consensus | 0.40% |

| Previous | -0.60% |

| 23:50 | JPY |

| GDP Deflator Y/Y Q4 P | |

| Actual | 3.40% |

| Consensus | 3.20% |

| Previous | 3.40% |

| 04:30 | JPY |

| Industrial Production M/M Dec F | |

| Actual | -0.10% |

| Consensus | -0.10% |

| Previous | -0.10% |

| 10:00 | EUR |

| Eurozone Industrial Production M/M Dec | |

| Actual | -1.40% |

| Consensus | -1.50% |

| Previous | 0.70% |

| 13:15 | CAD |

| Housing Starts Y/Y Jan | |

| Actual | 238K |

| Consensus | 265K |

| Previous | 282K |

| Revised | 281K |

| 13:30 | CAD |

| Manufacturing Sales M/M Dec | |

| Actual | 0.60% |

| Consensus | 0.50% |

| Previous | -1.20% |

| Revised | -1.30% |

The Under-Appreciated Effects of FX Appreciation

The USD sell-off has caused the AUD to appreciate beyond what the recent shift in the rates outlook would imply.

- Geopolitics and AI-generated investor nervousness have contributed to a growing pivot out of the USD since the beginning of the year, if not out of US-domiciled assets necessarily. The result has been compressed credit spreads elsewhere and vibrant activity in non-US credit markets, including Australia.

- The USD has therefore depreciated noticeably in recent weeks but remains overvalued on standard metrics, though less so than a year ago. The AUD has appreciated even more, with a bit more than half the shift in the TWI since the beginning of 2025 being an arithmetic consequence of the USD move. The rest is attributable to other factors, including but not limited to the shift in the rates outlook over the past couple of months.

- Normally, the AUD moves in ways that offset other shocks rather than being a shock in its own right. However, the nature of the USD sell-off and shifts in hedging suggest that the appreciation could dampen imported inflation by more than is implied by rate moves alone.

If the procession of geopolitical events in the year’s opening weeks wasn’t enough, global markets have been buffeted by a growing pivot out of USD-denominated assets. Some of that pivot has involved investors retaining exposure to the underlying US assets but hedging the exchange rate exposure, while in other cases, portfolios are being reallocated outright.

This ‘de-dollarisation’ pivot has in part been driven by the various geopolitical events of recent weeks, many of which are seen as US-negative and USD-negative, but there is more to it than that. Compounding the nervousness has been ongoing uncertainty about the implications of the AI technology and investment boom. The major players’ investment plans are of such enormous scale that digesting the resulting issuance will inevitably affect the market more broadly. This is especially so when we are already seeing cases where investment with an economic life of less than a decade is being funded by a 100-year bond issue.

Another element of this nervousness has been seen in negative equity market reactions to recent releases of new AI products that are seen as potentially disrupting incumbent industries. We remain of the view that these new technologies will not destroy jobs and industries in the way some fear. After all, the intellectual property of a software firm is less that they have people who know how to code, and more that they have people who know what makes a good payroll system, or drawing software, or whatever it may be. That design knowledge is harder to ‘vibe’ than the code. But for now, the rate of change is so rapid that the first reaction will be fear, until the broader implications can be worked through.

An intense appetite to invest in credit products means that neither the shift out of USD or the boom in AI investment funding has materially shifted fixed-interest pricing in the large US and other major markets. For example, 10-year government bond yields are little changed over the past couple of months. Rather, we see the impact in compressed credit spreads, and in smaller debt markets such as Australia’s, where issuance volumes have expanded to take advantage of strong investor demand. New participants have entered both sides of the Australian credit market and activity broadly has been vibrant.

The pivot out of USD assets has materially contributed to a sell-off of the USD in recent weeks. Over the past month, DXY is down around 2%, and it touched even lower levels in late January. Despite this, standard metrics still show the USD as moderately overvalued, with the real effective exchange rate around 12% above its long-run average. This overvaluation was even more pronounced at the beginning of 2025 and has progressively unwound in fits and starts.

Meanwhile, because the Chinese currency is closely managed to maintain its USD exchange rate, it has moved relatively little in trade-weighted terms. But because inflation has been much lower there than in the US and many other major industrialised economies, its real effective exchange rate is around 15% below its peak in early 2022. The resulting increased competitiveness is one reason why China has been able to meet its growth targets by increasing exports.

Domestically, the main result of these developments is that the AUD has appreciated noticeably. In trade-weighted terms, it is up 5% since the beginning of the year and 10% since the start of 2025. These are large shifts that cannot be entirely attributed to the higher rates outlook in Australia recently.

To be fair, the rates environment has contributed: yields on Australian 10-year sovereign bonds are now around 65bp above their US equivalents, despite the Australian sovereign being more highly rated, after being closer to flat in the middle of last year. This has made Australian assets particularly attractive to global investors, within the broader pivot away from USD-denominated assets. But if shifts in domestic rates alone had been the driver, cross-rates against other currencies would have risen by more than they have done; in particular, AUD/EUR would not be below where it was at the beginning of 2025.

At least some of the AUD’s appreciation instead stems from other factors, including higher prices for some key commodities and the previously mentioned sell-off in the USD. Many of the entities increasing their hedging or reallocating new flows are Australian superannuation funds, so the impact on the AUD/USD exchange rate can be expected to be pronounced.

The AUD/USD bilateral rate is up nearly 15% since the beginning of last year, versus 10% on the TWI. The USD and CNY together have a roughly 40% weight in the trade-weighted index, and slightly less than that in the RBA’s import-weighted index. A crude way of thinking about this is that the USD bilateral move, and accompanying CNY move, accounts for 6ppt of the 10ppt move in TWI since the beginning of 2025. Since the AUD/USD rate would have moved anyway with the higher Australian rates outlook, not all of this relates to the USD sell-off. Again, though, movements against other major currencies imply that most of it was USD-driven.

Another way of thinking about the appreciation is through the lens of the real effective AUD exchange rate (using the IMF monthly real effective exchange rate data supplemented with nominal TWI movements, given the RBA’s quarterly index only goes to the December quarter). The 5½% lift in this measure in February to date compared with December is considerably larger than the impact of the roughly 100bp shift in the interest rate path implied by the RBA’s own models.

If the AUD remains at this level or appreciates further, some downward pressure on inflation in imported items can be expected over the next year or two. While estimates are necessarily imprecise, there are good reasons to think that size of the effect will not be fully captured in the impulse response from interest rate shock to inflation in a whole-economy model. Our assessment is that – partly for timing reasons – the RBA might not have fully incorporated this possibility into its February forecasts or assessment of risks.

In this week’s Market Outlook publication, we highlighted several reasons to expect that the current elevated inflation rate will unwind over time. Some of them, like the conclusion of public infrastructure projects and their impetus to demand, are purely domestic developments. The exchange rate appreciation, on the other hand, depends a lot on how attractive US markets remain to global investors or whether the sell-off continues.

This is quite a different dynamic to how policymakers usually think about the exchange rate. Normally, the AUD is seen as a shock absorber, the depreciation that cushions the effect of a global downturn, or the appreciation that absorbs and widely distributes the benefits of a commodity boom. Policymakers in Australia remember the difficulties their NZ and Canadian counterparts got into back in the 1990s by treating the exchange rate as an independent factor in a Monetary Conditions Index. It is therefore understandable that they might downplay a move that happened at the same time as the rates outlook moved a lot.

This time round, though, it will pay to keep a weather eye on the implications of global asset reallocation and Australian hedging patterns for AUD, and what this might do to the cost base for imported goods.