Sample Category Title

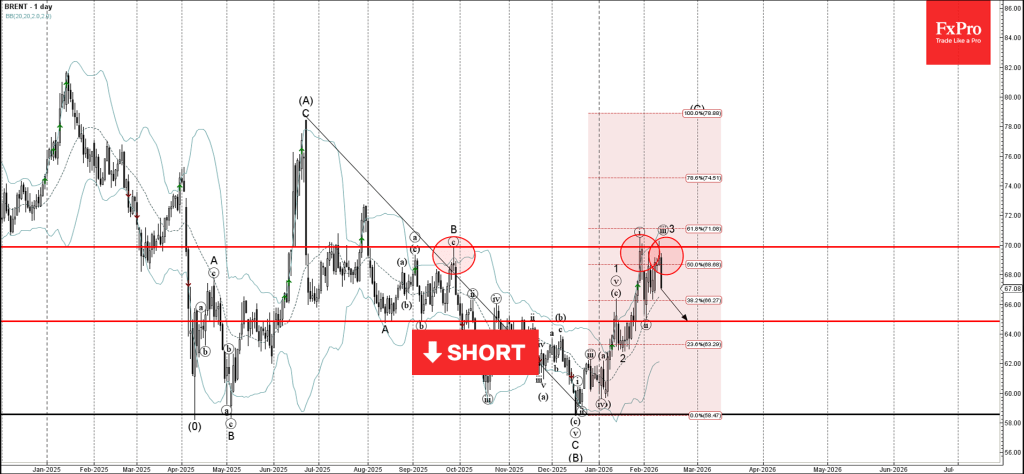

Brent Crude Oil Wave Analysis

Brent Crude Oil: ⬇️ Sell

- Brent Crude Oil reversed from resistance zone

- Likely to fall to support level 64.85

Brent Crude Oil recently reversed down from the resistance zone between the round resistance level 70.00 (which has been reversing the price from September), upper daily Bollinger Band and the 61.8% Fibonacci correction of the downward impulse from June.

The downward reversal from this resistance zone created the daily Shooting Star, which stopped the earlier impulse waves iii and (3).

Brent Crude Oil can be expected to fall to the next support level 64.85 (low of the previous minor correction ii).

Eco Data 2/13/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Jan | 55.2 | 56.1 | ||

| 07:30 | CHF | CPI M/M Jan | -0.10% | 0.00% | 0.00% | |

| 07:30 | CHF | CPI Y/Y Jan | 0.10% | 0.10% | 0.10% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | 11.6B | 10.2B | 10.7B | 10.2B |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.30% | 0.30% | 0.30% | |

| 13:30 | USD | CPI M/M Jan | 0.20% | 0.30% | 0.30% | |

| 13:30 | USD | CPI Y/Y Jan | 2.40% | 2.50% | 2.70% | |

| 13:30 | USD | CPI Core M/M Jan | 0.30% | 0.30% | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Jan | 2.50% | 2.50% | 2.60% |

| 21:30 | NZD |

| Business NZ PMI Jan | |

| Actual | 55.2 |

| Consensus | |

| Previous | 56.1 |

| 07:30 | CHF |

| CPI M/M Jan | |

| Actual | -0.10% |

| Consensus | 0.00% |

| Previous | 0.00% |

| 07:30 | CHF |

| CPI Y/Y Jan | |

| Actual | 0.10% |

| Consensus | 0.10% |

| Previous | 0.10% |

| 10:00 | EUR |

| Eurozone Trade Balance (EUR) Dec | |

| Actual | 11.6B |

| Consensus | 10.2B |

| Previous | 10.7B |

| Revised | 10.2B |

| 10:00 | EUR |

| Eurozone GDP Q/Q Q4 P | |

| Actual | 0.30% |

| Consensus | 0.30% |

| Previous | 0.30% |

| 13:30 | USD |

| CPI M/M Jan | |

| Actual | 0.20% |

| Consensus | 0.30% |

| Previous | 0.30% |

| 13:30 | USD |

| CPI Y/Y Jan | |

| Actual | 2.40% |

| Consensus | 2.50% |

| Previous | 2.70% |

| 13:30 | USD |

| CPI Core M/M Jan | |

| Actual | 0.30% |

| Consensus | 0.30% |

| Previous | 0.20% |

| 13:30 | USD |

| CPI Core Y/Y Jan | |

| Actual | 2.50% |

| Consensus | 2.50% |

| Previous | 2.60% |

Sunset Market Commentary

Markets

UK Q4 2025 growth and December production this morning again painted a sluggish picture on activity at the end of 2025. The UK economy ‘expanded’ 0.1% Q/Q, equal to the Q2 pace. Consensus expected 0.2%. Household consumption (0.2% Q/Q) and government spending (0.4%) contributed positively to growth. Gross Fixed capital investment declined (-0.1% Q/Q) with especially a 2.7% Q/Q decline in business investment catching the eye. Net exports (exports -0.6% Q/Q, imports +0.8%) also contributed negatively. In 2025 as a whole, the UK economy grew by 1.3% Y/Y. From a production point of view, manufacturing grew a solid 0.9%, agriculture added 0.3%. Construction activity contracted (-1.2%) while services stagnated. The monthly December GDP indicator stranded at a 0.1% monthly gain. The market reaction was as lackluster as the data. UK yield are easing 1-2.5 bps across the curve. The UK currency over the previous two days tried two brief attempts to rebound as uncertainty on the political fate of PM Starmer eased. However, for now this tentative rebound soon met sterling selling interest. EUR/GBP struggles sustainably settle below the 0.87. barrier (currently 0.8705).

US trading was captured in some kind of interlude between yesterday’s payrolls release with the yearly revision and tomorrow’s January US CPI report. Stronger than expected January job growth (130k) and the unemployment rate declining to 4.3% eased building pressures for the Fed to frontload further easing. That said, average monthly job growth last year slowing to 15k keeps the debate alive on the Fed’s reaction function in a context of ‘jobless growth’. The weekly jobless claims published today did little to bring any clarity (decline to 227k from a high 232k last week, but above 223k consensus). Bond yields yesterday soon reversed part of the initial post-payrolls rise and today are further ceding between 1 bp (2-y) and 3.5 bps (30-y). The 2-y yield struggles to regain the 3.5% level. The 10-y (4.16%) holds below the 4.2% reference. Later today, the US Treasury will sell $25 bln of 30-y notes. German yields are changing less than 1 bp across the curve. The dollar is going nowhere. DXY trades marginally lower near 96.8. EUR/USD gains a few ticks (1.1885). The yen rally is taking a breather. USD/JPY came within reach of the YTD low just above 152 (rumours at that time on the US and Japan discussing coordinated interventions), but the finally some consolidation kicked in (currently 153.3). The little news/low volatility environment today again supports equities. The EuroStoxx 50 (+0.8%) intraday touched a new all-time top just below 6100. In the US, the Dow Jones is only a whisker away from an all-time record (currently 50400; +0.55 %).

News & Views

Hungarian inflation quickened less than expected in January. Monthly price growth amounted to 0.3%, up from 0.1% in December but halve the pace expected. The annual reading plunged to 2.1% from 3.3%, below the central bank’s (MNB) 3% midpoint target for the first time in five years as well as the slowest since 2018. The MNB’s core measures also showed some (steep) declines with core CPI ex. indirect taxes falling to a similar multiyear year low of 2.6%. Services inflation, a focal point of the central bank, decelerated to 5% from 6.8%. CPI is kept artificially lower through the government’s profit curbs though, which have been extended to end-May as per ministerial decision today. Either way, MNB governor Varga at last month’s post-meeting press conference said that annual corporate repricing at the start of the year would be “decisive” for the central bank whether or not to restart its easing cycle (from 6.5% currently). Today’s numbers make such a rate cut at the February meeting ever more likely, particularly against the backdrop of a resilient forint. The HUF is showcasing that again today with losing only marginal ground both after the CPI release and after an EU court opinion suggested to scrap the release of more than €10bn in funds for the country. EUR/HUF trades around the 380 barrier. Swap yields tumbled up to 7 bps.

ECB board member Piero Cipollone today said that the central bank is preparing to broaden access to its euro backstop facility to more central banks outside the euro zone. Today just eight national banks have access to these repo lines, called Eurep. By expanding access, the ECB aims to reduce euro funding market disruption in times of stress. But it’s also a tool long favoured by ECB president Lagarde to boost the common currency’s global reach, particularly in the current circumstances where the US dollar’s status is being reassessed by investors.

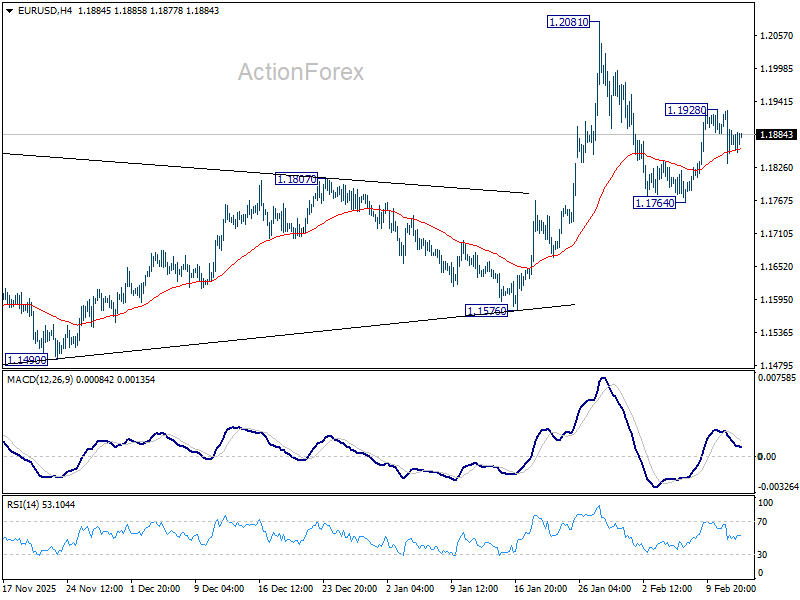

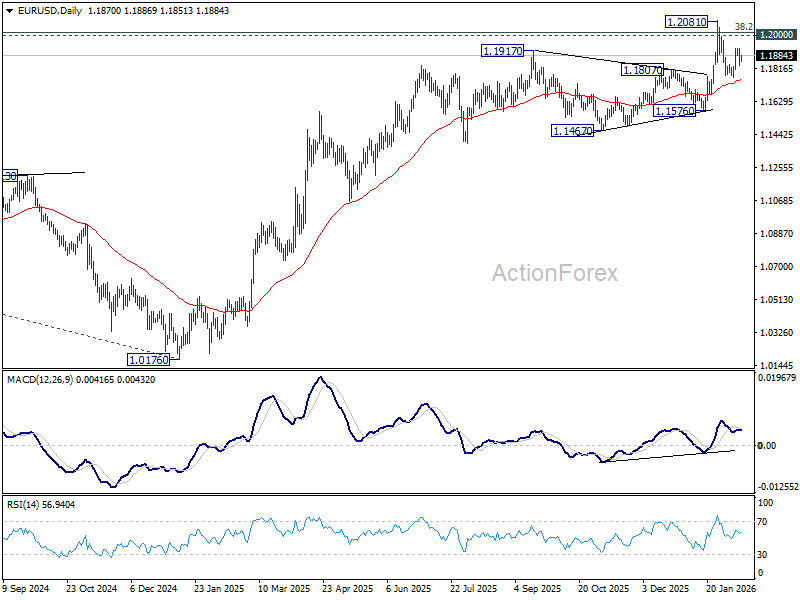

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1828; (P) 1.1877; (R1) 1.1921; More….

Intraday bias in EUR/USD stays neutral for the moment. On the upside, above 1.1928 will target a retest on 1.2081 high. Decisive break there and sustained trading above 1.2 psychological level will carry larger bullish implications. On the downside, however, sustained trading below 55 D EMA (now at 1.1752) will raise the chance of reversal on rejection by 1.2, and target 1.1576 support for confirmation.

In the bigger picture, as long as 55 W EMA (now at 1.1470) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7668; (P) 0.7699; (R1) 0.7750; More….

Intraday bias in USD/CHF remains neutral. Consolidations from 0.7603 is extending and stronger rebound could be seen to 0.7816 resistance. But upside should be limited by 55 D EMA (now at 0.7874). On the downside, firm break of 0.7603 will resume larger down trend to 0.7382 projection level next.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8152) holds.

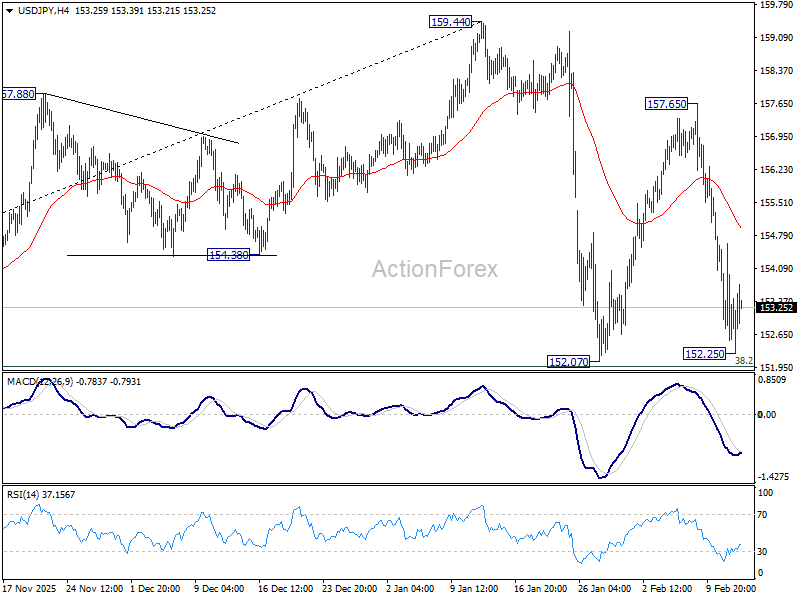

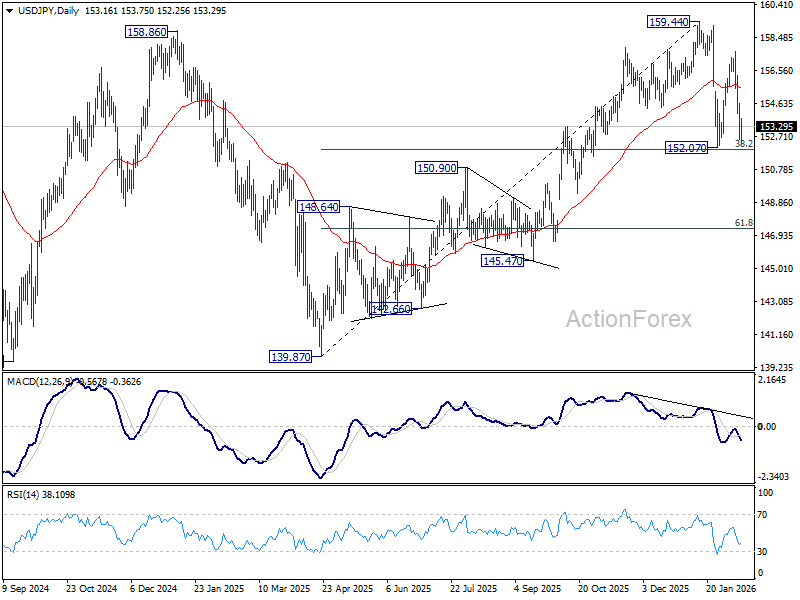

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.34; (P) 153.49; (R1) 154.43; More...

No change in USD/JPY's outlook and intraday bias remains neutral. While another fall cannot be ruled out, strong support should be seen from 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound. On the upside, sustained break of 55 4H EMA (now at 154.96) will bring stronger rebound towards 157.65. However, sustained break of 151.96 will argue that it's reversing the rise from 139.87 already.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.68) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

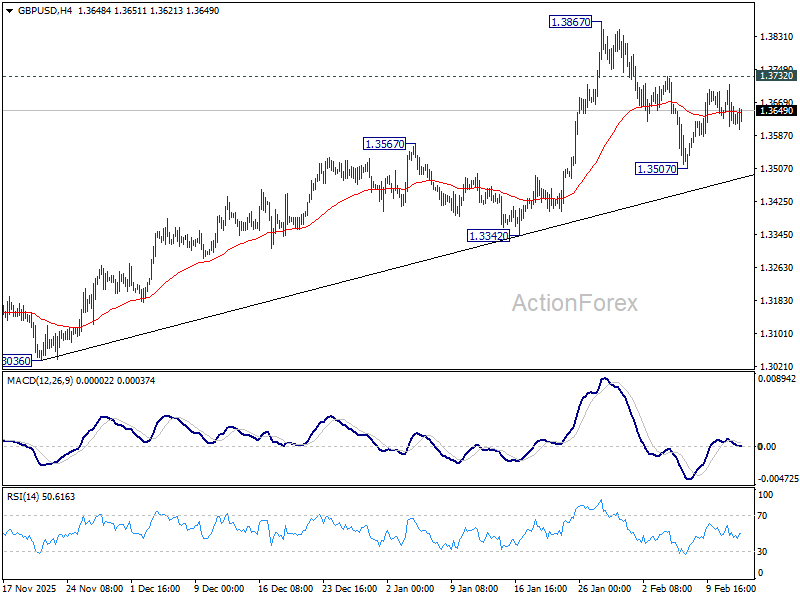

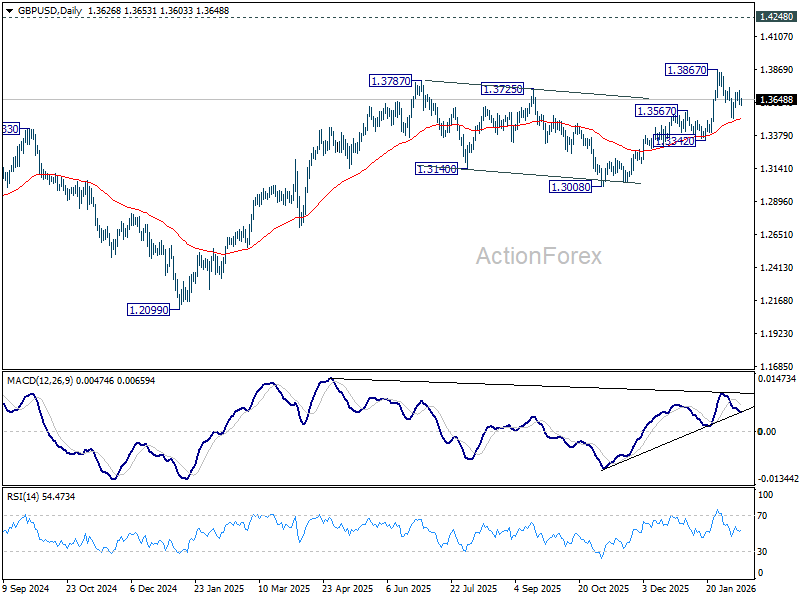

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3588; (P) 1.3650; (R1) 1.3691; More...

GBP/USD is still gyrating in tight range below 1.3732 resistance and intraday bias remains neutral. On the upside, firm break of 1.3732 will suggest that pullback from 1.3867 has completed as a correction at 1.3507. Retest of 1.3867 should be seen first. Firm break there will resume larger up trend towards 1.4284 key resistance. On the downside, however, sustained trading below 55 D EMA (now at 1.3505) will raise the chance of larger scale correction, and target 1.3342 support for confirmation.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

FX Stalls as Sterling Shrugs Off GDP Miss, Yen Rally Pauses

Forex markets are relatively subdued today, with most major pairs and crosses confined within yesterday’s ranges. After recent volatility, positioning appears balanced as traders await a stronger catalyst to drive the next move.

Sterling is modestly firmer despite weaker-than-expected UK GDP data. December growth came in soft and the fourth quarter barely managed a positive reading, yet the currency’s resilience suggests markets are focusing on stabilization rather than disappointment.

Some economists argue that the latest figures point to an economy that has bottomed out rather than one sliding into contraction. Surveys indicate a pickup in manufacturing activity in January and early signs of revival in services, supporting hopes that growth momentum could improve as 2026 unfolds.

The National Institute of Economic and Social Research expects UK GDP to expand by 0.3% in the Q1. Associate economist Fergus Jimenez-England noted that while 2025 growth of 1.3% slightly undershot expectations and Q4 services were weak, business sentiment has improved after months of uncertainty surrounding the Autumn Budget.

Policy expectations are also lending support. BoE Monetary Policy Committee member Sarah Breeden said it is “reasonable to expect” another quarter-point rate cut by the end of April. Her comments that it is time to “take the foot off the monetary brake” reinforced expectations that easing could resume soon.

Elsewhere, Yen’s rally appears to be losing some immediate momentum. Technical resistance levels in key crosses may be limiting further gains for now, although the pullback remains shallow. The sustainability of Yen’s move will likely depend on broader market sentiment, particularly developments in Japan’s domestic equity market. The Nikkei continued its record run today, but signs of exhaustion are emerging after an extended rally.

Political optimism has been a key driver. Investors have embraced Prime Minister Sanae Takaichi’s strong electoral mandate and the prospect of higher spending, tax relief and a more assertive economic agenda. However, questions remain over how new fiscal initiatives will be funded. A shift in domestic risk appetite could help underpin a more durable Yen reversal.

For the week so far, Dollar remains the weakest performer, followed by Sterling and Euro. Yen leads gains, with Aussie and Kiwi also firm. Swiss Franc and Loonie are trading in the middle of the pack as markets wait for the next catalyst.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is up 1.38%. CAC is up 1.00%. UK 10-year yield is down -0.018 at 4.463. Germany 10-year yield is flat at 2.797. Earlier in Asia, Nikkei fell -0.02%. Hong Kong HSI fell -0.86%. China Shanghai SSE rose 0.05%. Singapore Strait Times rose 0.65%. Japan 10-year JGB yield fell -0.002 to 2.235.

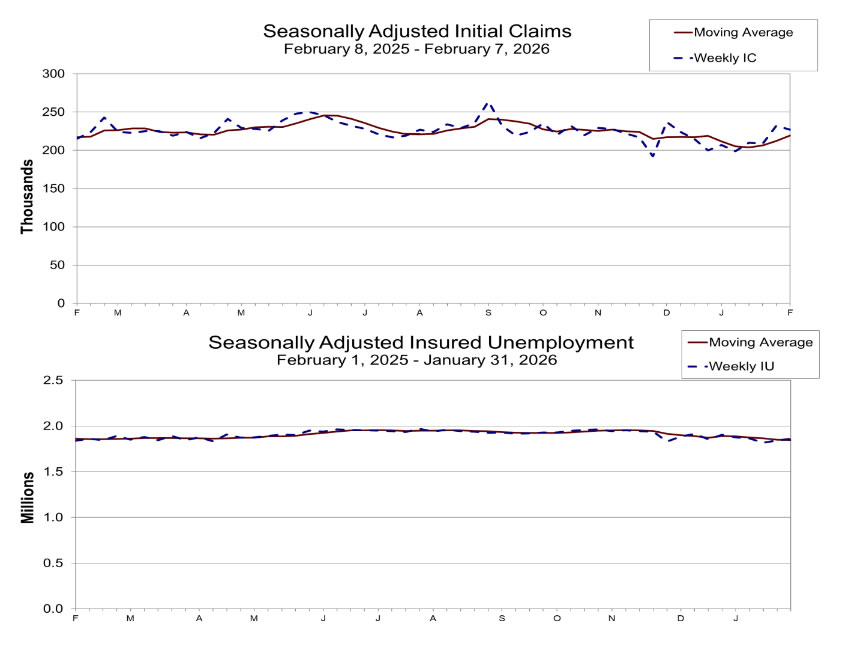

US initial jobless claims fall to 227k, above exp 222k

US initial jobless claims fell -5k to 227k in the week ending February 7, above expectation of 222k. Four-week moving average of initial claims rose 7k to 219.5k.

Continuing claims rose 21k to 1,862, in the week ending January 31. Four-week moving average of continuing claims fell -3k to 1,847k, lowest since October 5, 2024.

UK GDP misses at 0.1% mom growth, production and construction drag

UK GDP rose just 0.1% mom in December, undershooting expectations for a 0.2% gain and pointing to a subdued end to 2025. While services output expanded by 0.3% on the month, weakness in production, which fell -0.9%, and construction, down -0.5%, capped overall growth.

For the fourth quarter as a whole, GDP grew 0.1% quarter-on-quarter compared with Q3. Production output provided the largest positive contribution, rising 1.2%, while services showed no growth and construction contracted sharply by -2.1%.

On a broader basis, GDP expanded 1.0% in the three months to December 2025 compared with a year earlier, with services and production both up 1.0%. Annual GDP growth for 2025 came in at 1.3%, driven primarily by 1.4% growth in services, while production posted its first annual increase since 2021 at 0.2%. Construction grew 1.8%.

Japan PPI eases to 2.3%, but import costs accelerate

Japan’s producer price index slowed slightly to 2.3% year-on-year in January from 2.4%, matching expectations and suggesting pipeline price pressures are stabilizing. The moderation came despite sharp divergences across components.

Fuel prices dropped -12.9% yoy, providing a significant drag on overall wholesale inflation. In contrast, nonferrous metal prices surged 33%, while agricultural goods rose 22.4%. Food and beverage prices also remained elevated, increasing 4.7% from a year earlier, highlighting persistent cost pressures in parts of the supply chain.

Meanwhile, Yen-based import prices climbed 0.5% yoy, up from a 0.2% gain in December. Despite a recent rebound in the currency, Yen’s broader weakness over recent months has raised the cost of imported energy and raw materials.

RBA’s Bullock says inflation above 3% “unacceptable,” keeps door open to more hikes

RBA Governor Michele Bullock reinforced the hawkish stance at a Senate estimates hearing today, making clear that further tightening remains on the table. “If we need to go up further because inflation is entrenched, the board will do so,” she said, stressing that returning inflation to target remains the central bank’s primary mandate.

Bullock said inflation running “with a three in front of it” is unacceptable. She noted that, at present, total demand is judged to be exceeding the economy’s capacity to supply, helping to explain ongoing inflation pressures. At the same time, she struck a more balanced tone on growth, pointing to the labour market as a key "positive". While productivity remains weak and limits how fast the economy can expand, employment conditions are holding up. “We’re in this position because the economy is actually doing okay,” Bullock said,.

The RBA raised the cash rate by 25 bps last week to 3.85%, reversing one of last year’s cuts, after underlying inflation accelerated to 3.4% in the latest quarter. With forecasts pointing to inflation reaching 3.7% this year, markets now price roughly a 75% chance of another hike to 4.10% at the May meeting.

RBA’s Hunter: Job market tightness consistent with inflation pressure

RBA Assistant Governor Sarah Hunter signalled that Australia’s labour market remains tight despite signs of moderation elsewhere in the economy. In a speech today, she said the RBA’s full employment and NAIRU frameworks indicate that conditions have stabilized and remain “a bit tight,” consistent with "some inflationary pressure in the economy."

She described the relationship between labour tightness and inflation as “like the entwined double helix,” arguing that persistent capacity constraints continue to underpin price pressures. Recent data support that view, with unemployment unexpectedly falling to a seven-month low of 4.1% in December, raising the possibility that the labor market may be tightening again.

Hunter noted that the slowdown over the past few years has occurred primarily through fewer vacancies, reduced job switching, and slower hiring rather than a material rise in unemployment.

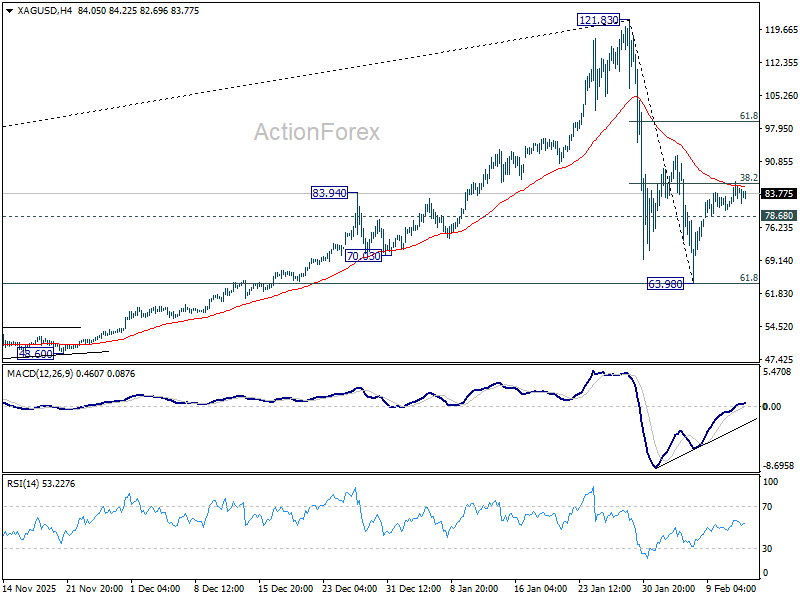

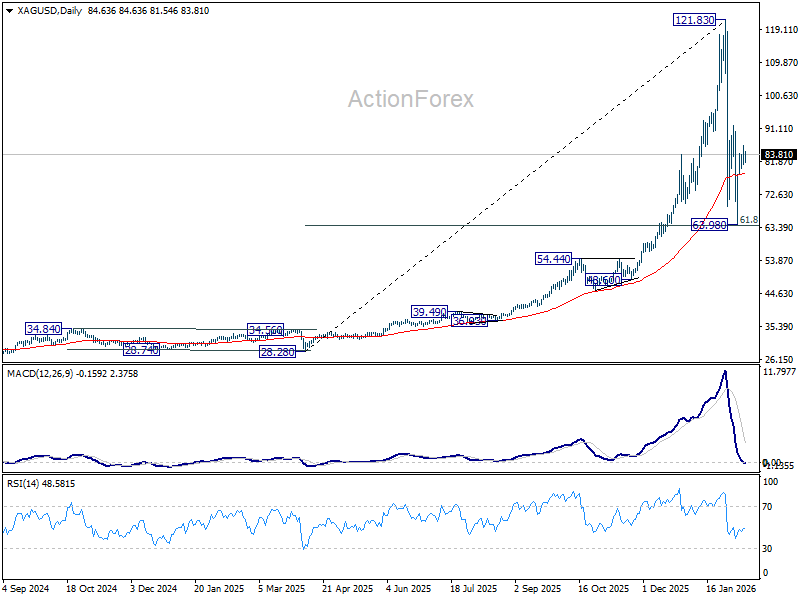

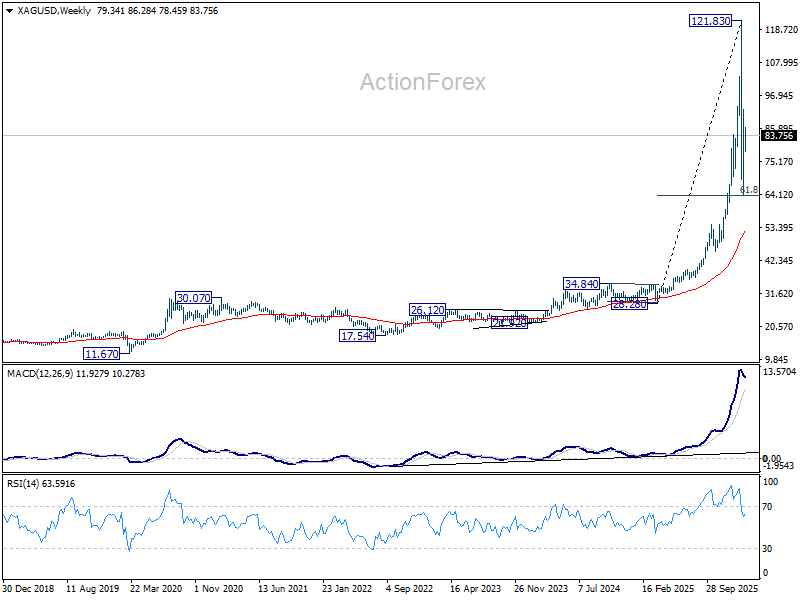

Silver push toward 100 hinges on 85/86 key barrier break

Silver is now pressing into a critical near-term resistance cluster around 85–86, a zone that could determine whether the sharp selloff from 121.82 has already bottomed at 63.98 or whether another leg lower is still ahead. The area combines 55 4H EMA (now at 85.27) and 38.2% retracement of 121.83 to 63.98 at 86.07, creating a technically dense barrier. Price reaction here is likely to set the tone for the next multi-week move.

Stepping back briefly, strong support emerged at 63.98, around 61.8% retracement of 28.28 to 121.83 at 64.04. That the decline from 121.82 is a correction to the up trend from 28.28 only. While the larger picture still points to prolonged medium-term consolidation, the immediate question is whether the next short-term upswing is about to unfold.

If Silver can sustain trading above the 85/86 zone, it would solidify the case that the first corrective leg completed at 63.98 and that a second leg higher is underway. In that scenario, further rise should be seen to 61.8% retracement of 121.83 to 63.98 at 99.73. However, the psychological 100 level sits just above that target and is likely to cap upside.

Conversely, rejection at 85/86 followed by a break below 78.68 support would shift the bias back to the downside. That would put 63.98 back in view and raise the probability that the correction is deeper than initially thought. In that case, the pullback could extend into a broader correction of the uptrend from 17.54 (2022 low), or even the larger advance from 11.69 (2020 low), before a durable base forms.

For now, the technical picture argues for patience rather than conviction. Silver is sitting at a clear decision point, and clarity should emerge within days. A confirmed break above 86 would favor positioning for a push toward 100, while failure at resistance would suggest waiting for another dip before considering fresh long positions.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3588; (P) 1.3650; (R1) 1.3691; More...

GBP/USD is still gyrating in tight range below 1.3732 resistance and intraday bias remains neutral. On the upside, firm break of 1.3732 will suggest that pullback from 1.3867 has completed as a correction at 1.3507. Retest of 1.3867 should be seen first. Firm break there will resume larger up trend towards 1.4284 key resistance. On the downside, however, sustained trading below 55 D EMA (now at 1.3505) will raise the chance of larger scale correction, and target 1.3342 support for confirmation.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

US initial jobless claims fall to 227k, above exp 222k

US initial jobless claims fell -5k to 227k in the week ending February 7, above expectation of 222k. Four-week moving average of initial claims rose 7k to 219.5k.

Continuing claims rose 21k to 1,862, in the week ending January 31. Four-week moving average of continuing claims fell -3k to 1,847k, lowest since October 5, 2024.

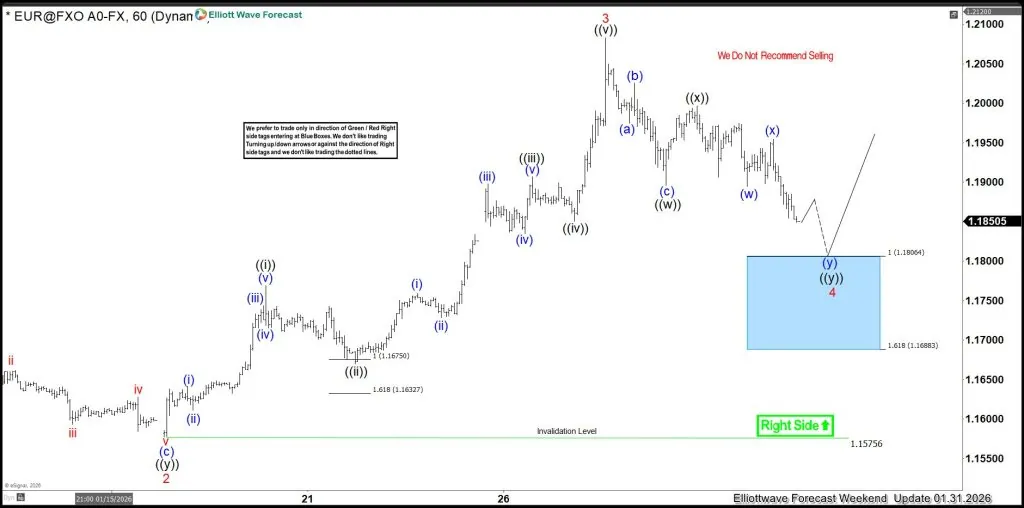

EURUSD Validates Elliott Wave with Perfect Blue Box Reaction

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of EURUSD. In which, the rally from 05 November 2025 low is unfolding as a diagonal & showed a higher high sequence therefore, called for an extension higher to take place. We knew that the structure in EURUSD should remain supported & extend higher. So, we advised members not to sell the pair & buy the dips in 3, 7, or 11 swings at the blue box areas. We will explain the structure & forecast below:

EURUSD 1-Hour Elliott Wave Chart From 1.31.2026

Here’s the 1- hour Elliott wave Chart from the 1.31.2026 Weekend update. In which, the rally to $1.2082 high completed wave 3 & made a pullback in wave 4. The internals of that pullback unfolded as Elliott wave double three correction where wave ((w)) ended at $1.1895 low. A rally to $1.1996 high-ended wave ((x)). Then started the next leg lower in wave ((y)) towards $1.1806- $1.1688 blue box area. From there, buyers were expected to appear looking for new highs ideally or for a 3-wave bounce minimum.

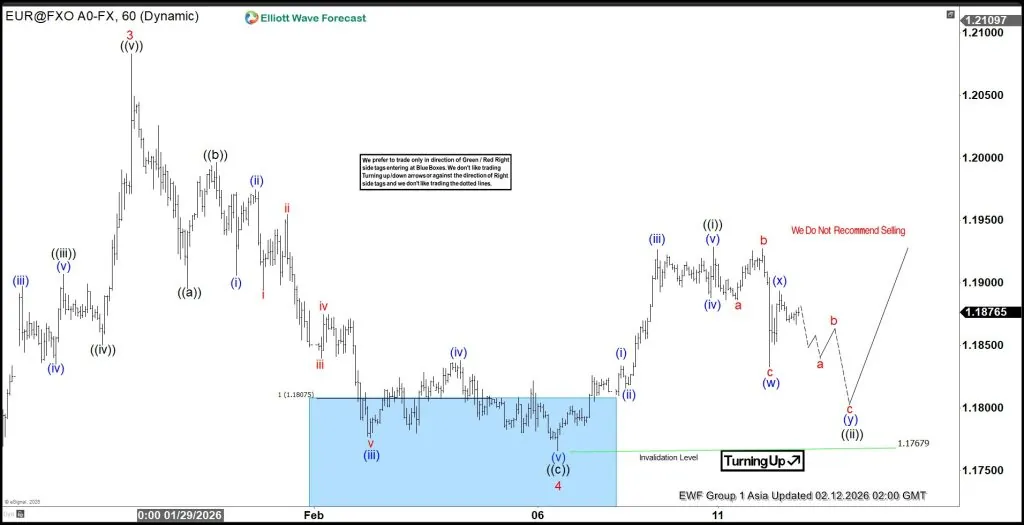

EURUSD Latest 1-Hour Elliott Wave Chart From 2.12.2026

This is the latest 1-hour Elliott wave Chart from the 2.12.2026 Asia update. In which the pair is showing a strong reaction higher taking place, right after ending the correction within the blue box area. Allowed members to create a risk-free position shortly after taking the long position at the blue box area. However, a break above $1.2082 high is needed to confirm the next extension higher. Towards $1.2158- $1.2279 ( minimum extension target) and avoid deeper correction lower.

If you are looking for real-time analysis in EURUSD along with the other forex pairs then join us with 14 day trial for the latest updates & price action.

Success in trading requires proper risk and money management as well as an understanding of Elliott Wave theory, cycle analysis, and correlation. We have developed a very good trading strategy that defines the entry.

Stop loss and take profit levels with high accuracy and allow you to take a risk-free position, shortly after taking it by protecting your wallet. If you want to learn all about it and become a professional trader. Then join our service by taking a Trial.