Sample Category Title

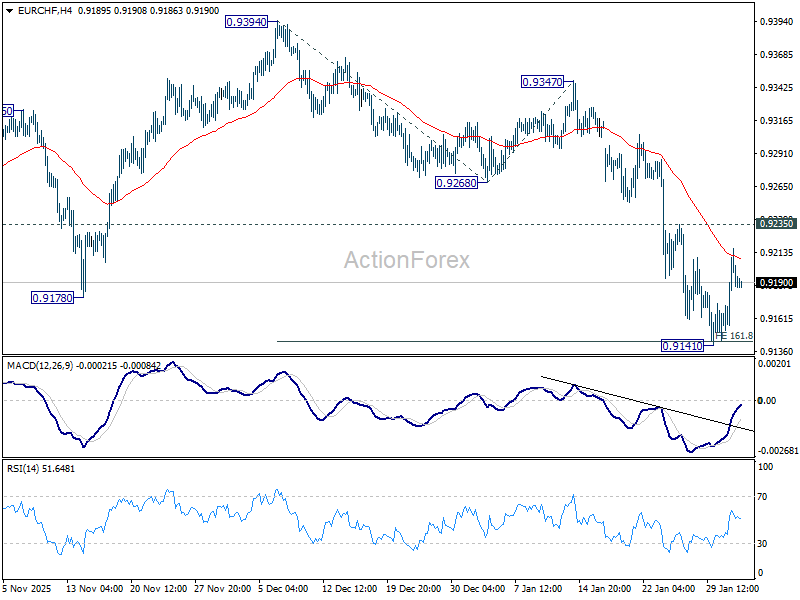

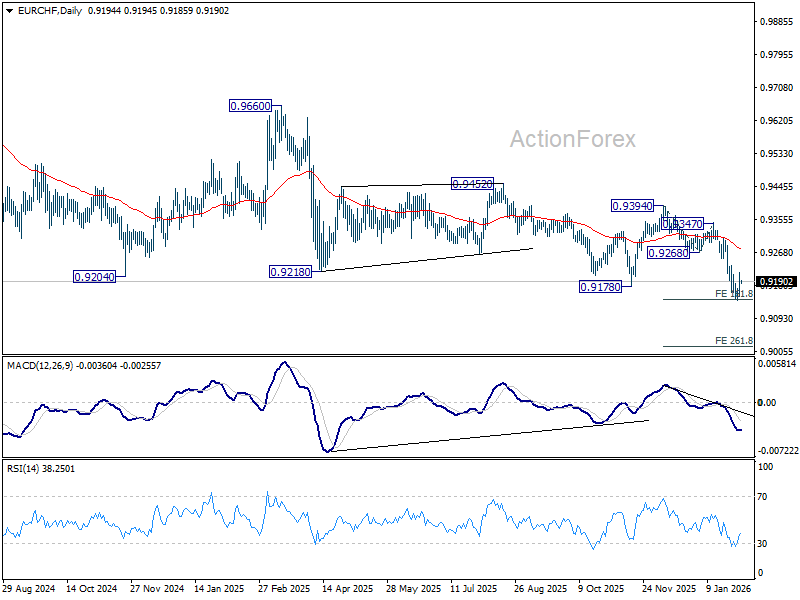

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9159; (P) 0.9188; (R1) 0.9223; More....

Intraday bias in EUR/CHF remains neutral first and more consolidations could be seen above 0.9141. Upside of recovery should be limited by 0.9235 to bring another fall. Decisive break of 0.9141 will extend larger down trend to 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143. However, firm break of 0..9235 resistance will suggest short term bottoming and bring stronger rebound to 55 D EMA (now at 0.9275).

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

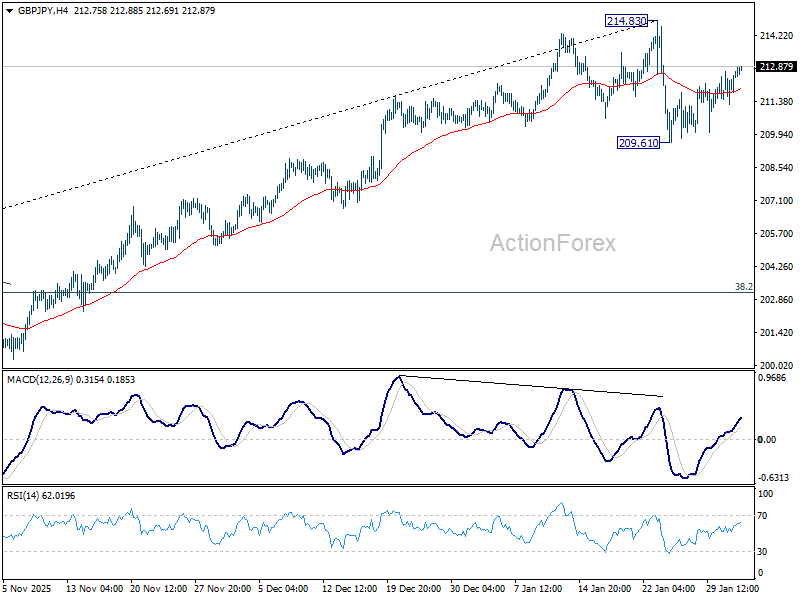

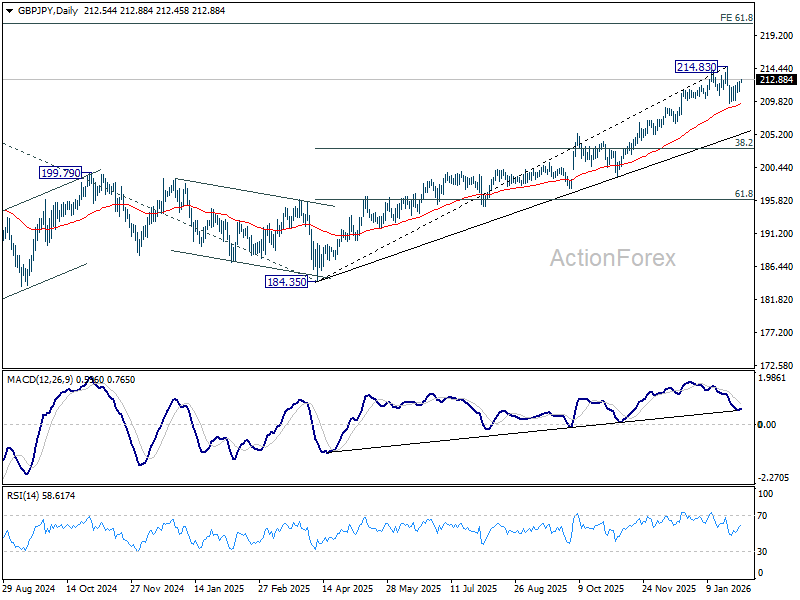

GBP/JPY Daily Outlook

Daily Pivots: (S1) 211.69; (P) 212.29; (R1) 213.28; More...

Intraday bias in GBP/JPY remains neutral and more consolidations would be seen first. Risk will stay on the downside as long as 214.83 holds, even in case of stronger recovery. Below 209.61, and sustained break of 55 D EMA (now at 209.51) will argue that it's correcting whole rise from 184.35 and target 38.2% retracement of 184.35 to 214.83 at 203.18.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

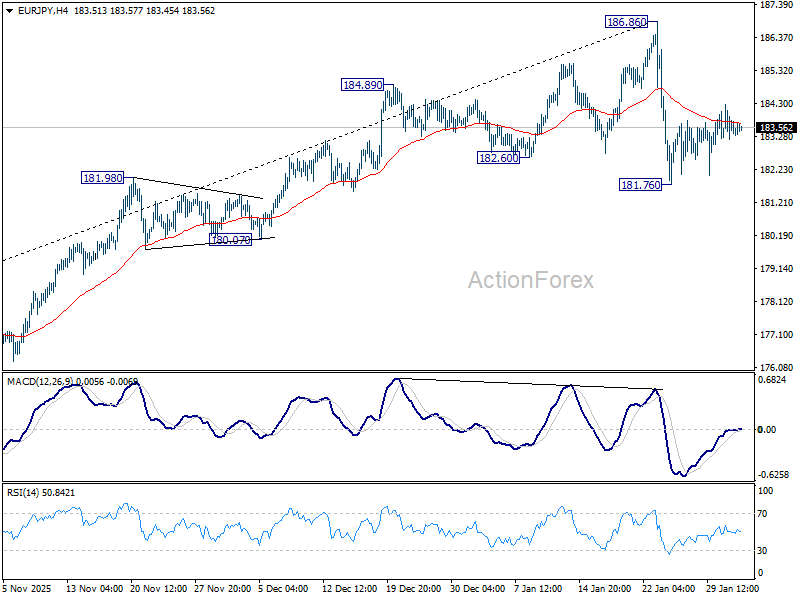

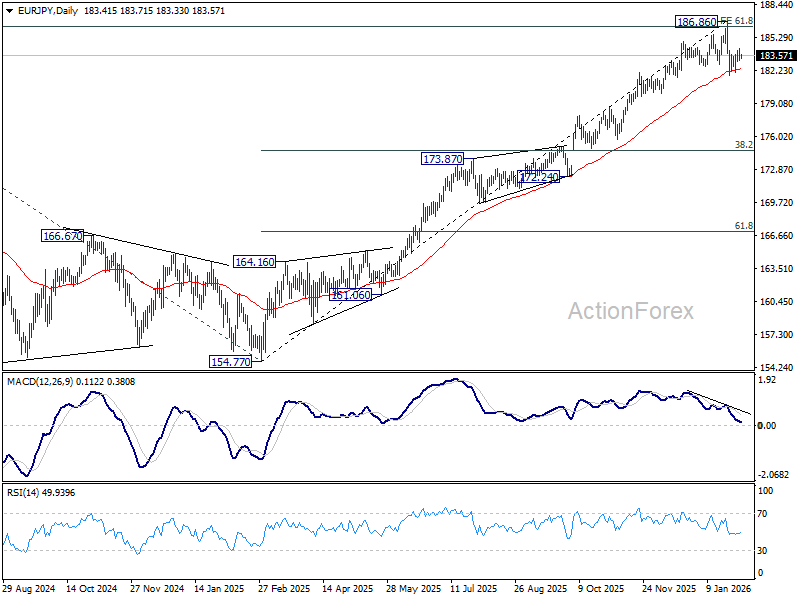

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.01; (P) 183.65; (R1) 184.10; More...

No change in EUR/JPY's outlook and intraday bias stays neutral for consolidations above 181.76. Risk remains on the downside as long as 186.86 holds, in case of strong recovery. Break of 181.76 and sustained trading below 55 D EMA (now at 182.35) should solidify the case that fall from 186.86 medium term top is correcting whole rise from 154.77. Deeper decline should then be seen to 38.2% retracement of 154.77 to 186.86 at 174.60.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and and met 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 173.32) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

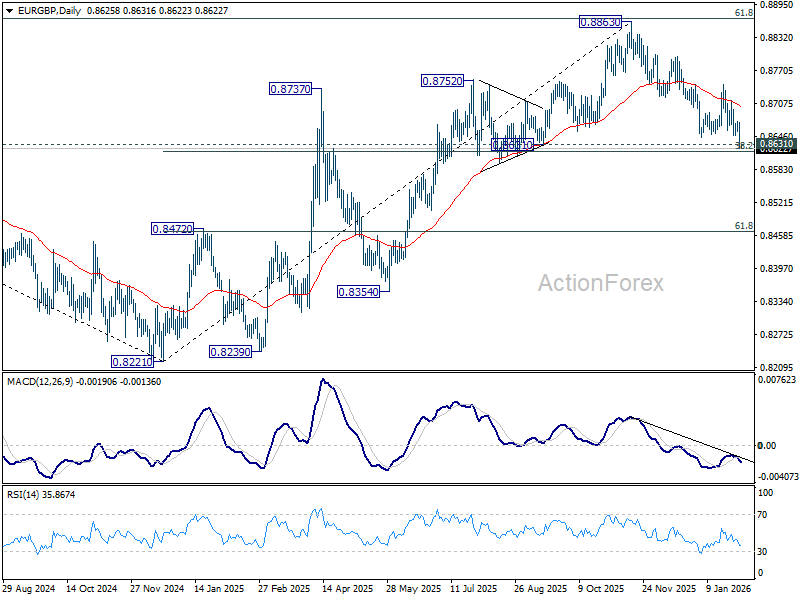

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8609; (P) 0.8641; (R1) 0.8658; More…

EUR/GBP's decline resumed by breaking through 0.8643 and intraday bias is back on the downside. Decisive break of 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618) will carry larger bearish implications. Next target is 61.8% retracement at 0.8466. On the upside, above 0.8674 resistance will turn intraday bias neutral again first.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

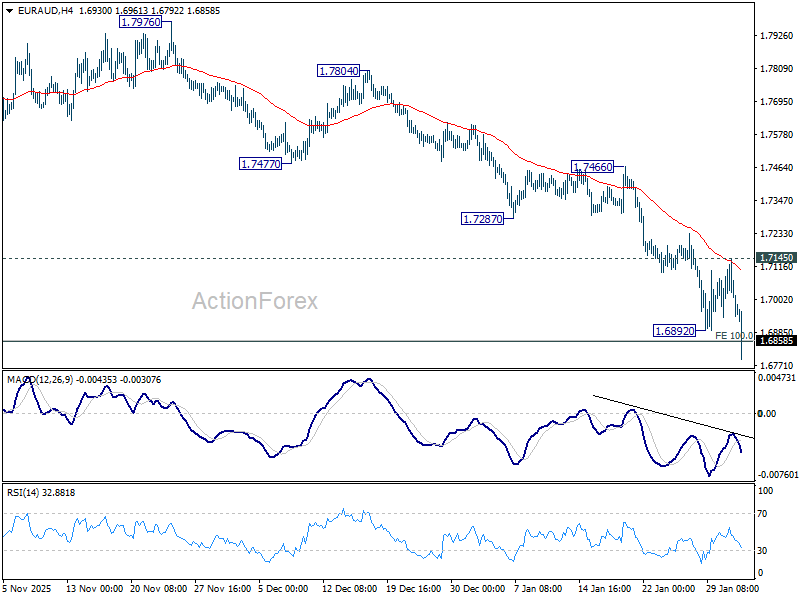

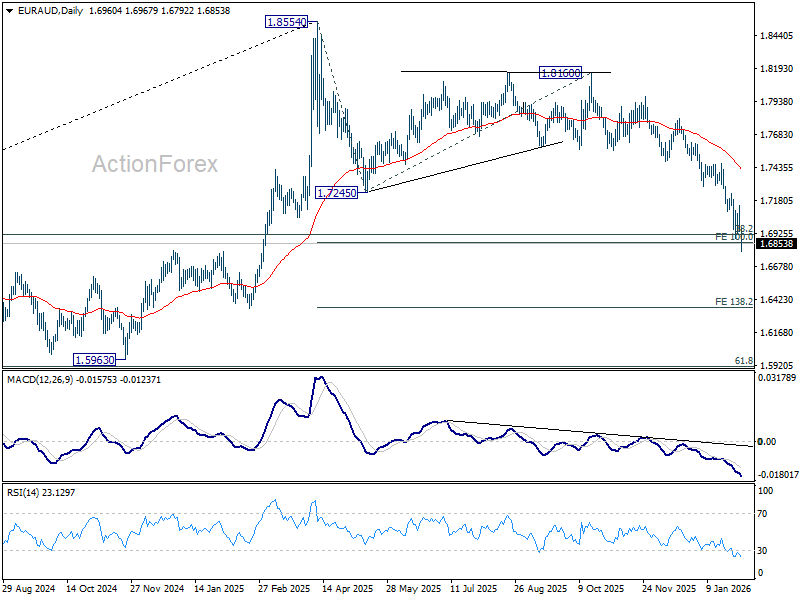

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6947; (P) 1.7016; (R1) 1.7091; More...

EUR/AUD's decline resumed by breaking through 1.6892 temporary low and intraday bias is back on the downside. Sustained trading below 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851 will pave the way to 138.2% projection at 1.6351 next. On the upside, break of 1.7145 resistance is needed to indicate short term bottoming. Otherwise, will remain bearish in case of recovery.

In the bigger picture, fall from 1.8554 medium term top is still in progress. Sustained break of 38.2% retracement of 1.4281 to 1.8554 at 1.6922 will argue that it's already reversing whole up trend from 1.4281 (2022 low). Deeper fall would be seen to 61.8% retracement at 1.5913. For now, risk will stay on the downside as long as 55 D EMA (now at 1.7418) holds even in case of strong rebound.

Risk-On Asia and Hawkish RBA Propel Aussie Higher

Australian Dollar surged broadly in Asia session, drawing fresh strength from a hawkish RBA rate hike that reinforced expectations of further tightening later this year. The move gave the Aussie an extra tailwind on top of an already constructive regional backdrop.

Risk appetite in Asia has been firm, with the latest boost to sentiment coming from a surprise breakthrough on trade. The US and India reached an agreement to immediately lower tariffs on each other’s goods. Under the deal, US tariffs on Indian goods will be cut sharply to 18% from 50%, bringing India broadly in line with Asian peers at 15–19%. In return, India agreed to halt purchases of Russian oil and reduce a range of trade barriers, according to US President Donald Trump.

Indian Prime Minister Narendra Modi also committed to significantly increase purchases of US products. Modi later confirmed the tariff reduction in a post on X, hailing the agreement as a major win for Indian exports. The announcement followed closely on the heels of India’s landmark free trade agreement with the European Union, which Modi described as the “mother of all deals.”

While the trade news supported risk currencies, Yen remained under pressure amid mixed messaging from Tokyo. Japan’s Finance Minister Satsuki Katayama today defended Prime Minister Sanae Takaichi’s recent remarks on the benefits of a weaker yen, saying they reflected standard economic theory. Katayama stressed that Takaichi was speaking in general terms, noting that while a weak Yen has downsides, it can also support corporate revenues, domestic investment, and exports. The comments added to confusion over how tolerant authorities are of further Yen depreciation.

Overall this week so far, the Aussie sits firmly at the top of the FX performance table, followed by Kiwi and Dollar. Swiss Franc trails at the bottom, with Yen and Euro also lagging. Sterling and Loonie are trading in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 3.85%. Hong Kong HSI is down -0.06%. China Shanghai SSE is up 0.44%. Singapore Strait Times is up 0.92%. Japan 10-year JGB yield is up 0.018 at 2.255. Overnight, DOW rose 1.05%. S&P 500 rose 0.54%. NASDAQ rose 0.56%. 10-year yield rose 0.034 to 4.275.

RBA delivers expected hike, forecast path points to another move

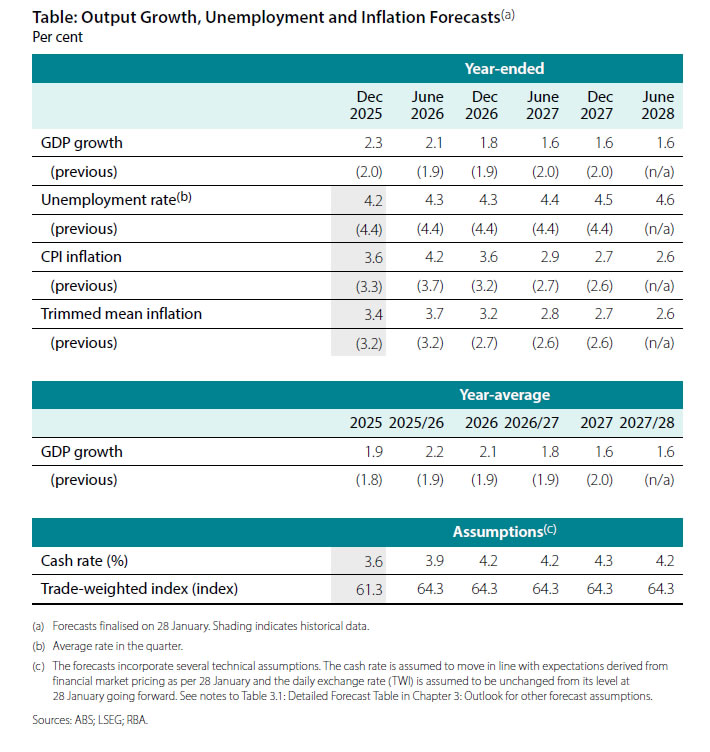

The RBA raised the cash rate by 25bps to 3.85% as widely expected, with the decision taken unanimously. While the accompanying statement avoided any explicit commitment to further tightening, the updated forecasts carried a more hawkish undertone.

Notably, the new projections are built on an assumption that the policy rate rises further to around 4.2% by the end of this year. That implicitly points to at least one additional hike being needed in the Bank’s view to contain resurging inflationary pressures.

In its statement, the RBA acknowledged that a broad range of recent data confirms inflationary pressures “picked up materially” in the second half of 2025. While part of the acceleration is judged to be temporary, the Bank highlighted that private demand is growing faster than expected, capacity pressures are higher than previously assessed, and labour market conditions remain slightly tight. Against that backdrop, the Board concluded that inflation is “likely to remain above target for some time,” justifying today’s move.

The message suggests policy is shifting from fine-tuning toward a more deliberate effort to re-anchor inflation expectations. The revised forecasts reinforce that view. CPI is now projected to peak at 4.2% in June 2026, up sharply from the previous 3.7% estimate, before easing to 3.6% by December 2026 and only gradually returning to 2.7% by end-2027. Trimmed mean inflation was also revised higher across the horizon, with the peak lifted to 3.7% in mid-2026.

Growth and labour market assumptions remain resilient. Average GDP growth for 2026 was revised up to 2.1% (from 1.9%), while the unemployment rate was nudged lower to 4.3% (down from 4.4%) next year, before edging higher to 4.5% in 2027. That profile suggests the RBA sees room to keep policy restrictive without inflicting material damage on employment, keeping the door open for further tightening if inflation fails to cool as projected.

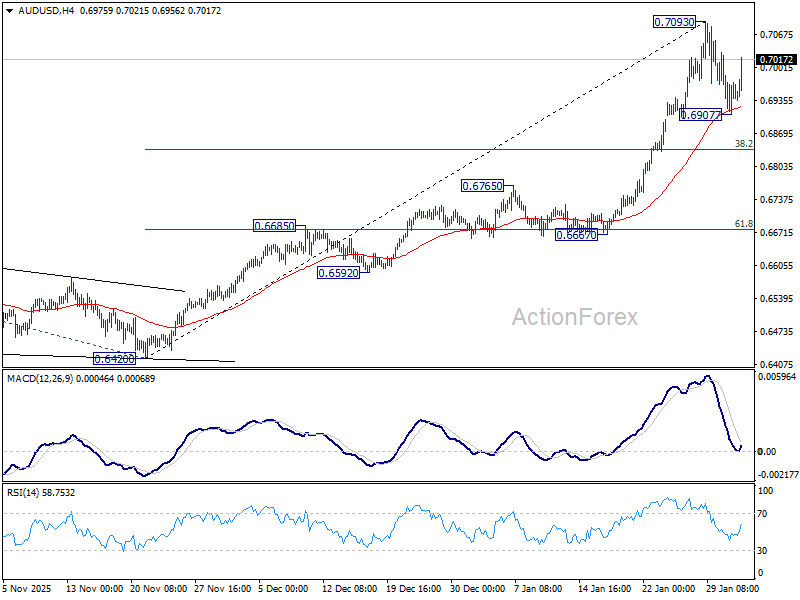

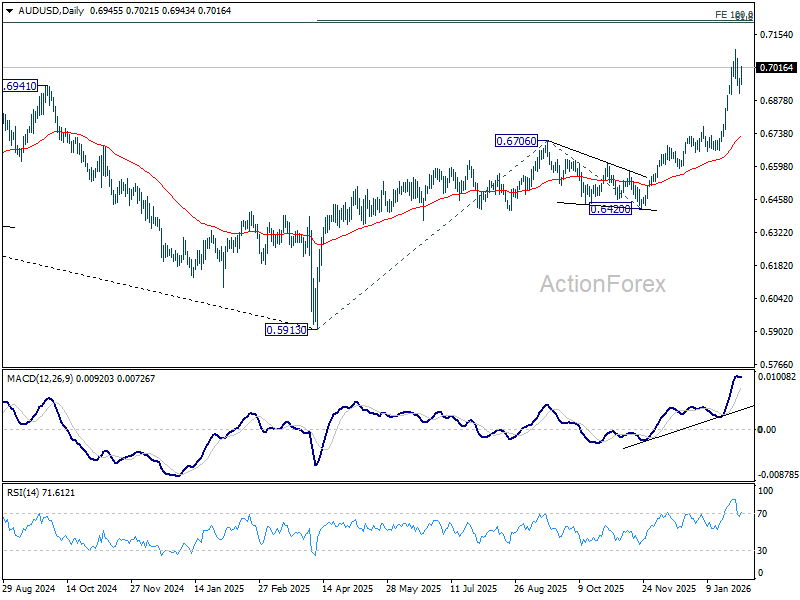

AUD/USD uptrend to resume to 0.72 after hawkish RBA hike

Aussie rallied broadly after the RBA raised the cash rate by 25bps to 3.85%, in line with expectations. While the decision itself was fully priced, the accompanying forecasts carried an implicit signal that another rate hike is likely later this year, providing fresh support to the currency.

AUD/USD quickly pushed back above the 0.7000 mark following the announcement. Technically, strong support has been established at 55 4H EMA, suggesting that the recent consolidation from the 0.7093 should remain shallow and temporary.

Decisive break above 0.7093 would confirm continuation of the broader uptrend from 0.5913 (2025 low). In this scenario, AUD/USD would be on track to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 in the next leg higher.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6947; (P) 1.7016; (R1) 1.7091; More...

EUR/AUD's decline resumed by breaking through 1.6892 temporary low and intraday bias is back on the downside. Sustained trading below 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851 will pave the way to 138.2% projection at 1.6351 next. On the upside, break of 1.7145 resistance is needed to indicate short term bottoming. Otherwise, will remain bearish in case of recovery.

In the bigger picture, fall from 1.8554 medium term top is still in progress. Sustained break of 38.2% retracement of 1.4281 to 1.8554 at 1.6922 will argue that it's already reversing whole up trend from 1.4281 (2022 low). Deeper fall would be seen to 61.8% retracement at 1.5913. For now, risk will stay on the downside as long as 55 D EMA (now at 1.7418) holds even in case of strong rebound.

AUD/USD uptrend to resume to 0.72 after hawkish RBA hike

Aussie rallied broadly after the RBA raised the cash rate by 25bps to 3.85%, in line with expectations. While the decision itself was fully priced, the accompanying forecasts carried an implicit signal that another rate hike is likely later this year, providing fresh support to the currency.

AUD/USD quickly pushed back above the 0.7000 mark following the announcement. Technically, strong support has been established at 55 4H EMA, suggesting that the recent consolidation from the 0.7093 should remain shallow and temporary.

Decisive break above 0.7093 would confirm continuation of the broader uptrend from 0.5913 (2025 low). In this scenario, AUD/USD would be on track to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 in the next leg higher.

RBA delivers expected hike, forecast path points to another move

The RBA raised the cash rate by 25bps to 3.85% as widely expected, with the decision taken unanimously. While the accompanying statement avoided any explicit commitment to further tightening, the updated forecasts carried a more hawkish undertone.

Notably, the new projections are built on an assumption that the policy rate rises further to around 4.2% by the end of this year. That implicitly points to at least one additional hike being needed in the Bank’s view to contain resurging inflationary pressures.

In its statement, the RBA acknowledged that a broad range of recent data confirms inflationary pressures “picked up materially” in the second half of 2025. While part of the acceleration is judged to be temporary, the Bank highlighted that private demand is growing faster than expected, capacity pressures are higher than previously assessed, and labour market conditions remain slightly tight. Against that backdrop, the Board concluded that inflation is “likely to remain above target for some time,” justifying today’s move.

The message suggests policy is shifting from fine-tuning toward a more deliberate effort to re-anchor inflation expectations. The revised forecasts reinforce that view. CPI is now projected to peak at 4.2% in June 2026, up sharply from the previous 3.7% estimate, before easing to 3.6% by December 2026 and only gradually returning to 2.7% by end-2027. Trimmed mean inflation was also revised higher across the horizon, with the peak lifted to 3.7% in mid-2026.

Growth and labour market assumptions remain resilient. Average GDP growth for 2026 was revised up to 2.1% (from 1.9%), while the unemployment rate was nudged lower to 4.3% (down from 4.4%) next year, before edging higher to 4.5% in 2027. That profile suggests the RBA sees room to keep policy restrictive without inflicting material damage on employment, keeping the door open for further tightening if inflation fails to cool as projected.

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 3.85 per cent.

While inflation has fallen substantially since its peak in 2022, it picked up materially in the second half of 2025. The Board has been closely monitoring the economy and judges that some of the increase in inflation reflects greater capacity pressures. As a result, the Board considers that inflation is likely to remain above target for some time.

Capacity pressures reflect, in part, the greater momentum in demand seen in recent months. Growth in private demand has strengthened substantially more than expected, driven by both household spending and investment. Activity and prices in the housing market are also continuing to pick up. Financial conditions eased over 2025 and it is uncertain whether they remain restrictive. Credit is readily available to both households and businesses and the effects of earlier interest rate reductions are yet to flow through fully to aggregate demand, prices and wages. More recently, the exchange rate, money market interest rates and government bond yields have risen following a rise in market expectations for the cash rate.

Various indicators suggest that labour market conditions remain a little tight and that they have stabilised in recent months, in line with the pick-up in momentum in economic activity. The unemployment rate has been a little lower than expected and measures of labour underutilisation remain at low rates. Growth in the Wage Price Index has eased from its peak, but broader measures of wages growth continue to be strong and growth in unit labour costs remains high.

There are uncertainties about the outlook for domestic economic activity and inflation and the extent to which monetary policy is restrictive. On the domestic side, if growth in demand is stronger than expected, and growth in the economy’s supply capacity remains limited, it is likely to add further to capacity pressures. Uncertainty in the global economy remains significant but so far there has been little or no depressing effect on the Australian economy; indeed, recent growth and trade in Australia’s major trading partners has surprised on the upside.

Decision

A wide range of data over recent months have confirmed that inflationary pressures picked up materially in the second half of 2025. While part of the pick-up in inflation is assessed to reflect temporary factors, it is evident that private demand is growing more quickly than expected, capacity pressures are greater than previously assessed and labour market conditions are a little tight.

The Board judged that inflation is likely to remain above target for some time and it was appropriate to increase the cash rate target.

The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

Today’s policy decision was unanimous.

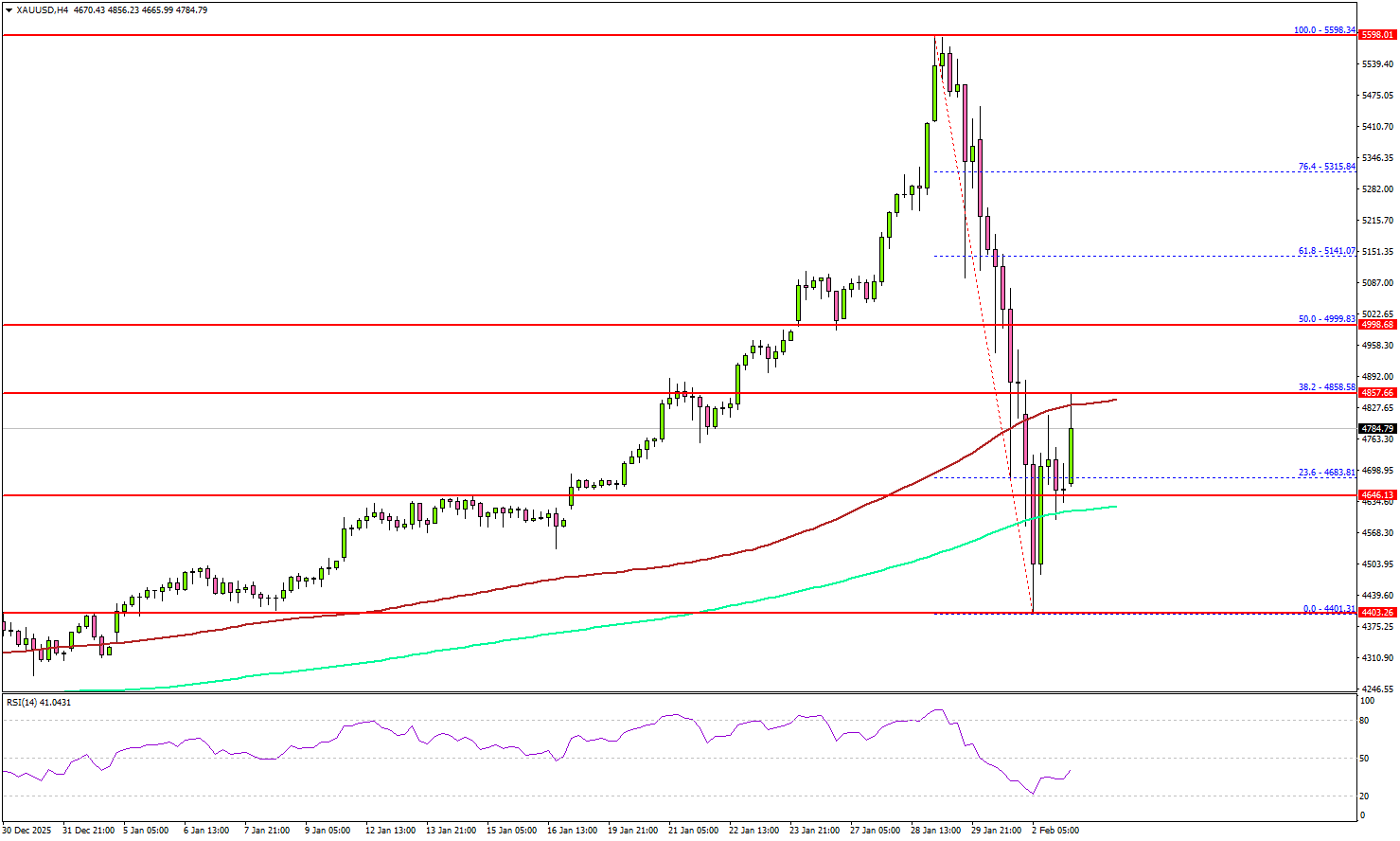

Gold Attempts Recovery As Traders Digest Flash Crash

Key Highlights

- Gold nosedived below $5,000 before it found support at $4,400.

- It could now face hurdles near $4,850 and $5,000 on the 4-hour chart.

- WTI Crude Oil prices also corrected some gains from $66.50.

- USD/JPY started a recovery wave above 153.75 and 154.50.

Gold Price Technical Analysis

Gold extended its rally to $5,598 against the US Dollar before witnessing a major decline. The price tested the $4,400 zone and recently started a recovery wave.

The 4-hour chart of XAU/USD indicates that the price traded as low as $4,401 and recently started a recovery wave above the 200 Simple Moving Average (green, 4 hours). The price climbed above the 23.6% Fib retracement level of the downward move from the $5,598 swing high to the $4,401 low.

On the upside, immediate resistance is near the $4,850 level and the 100 Simple Moving Average (red, 4 hours). The next major resistance sits near the $5,000 handle since it coincides with the 50% Fib retracement level of the downward move from the $5,598 swing high to the $4,401 low.

A clear move above $5,00 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $5,200. The main target for the bulls could be $5,320.

If there is another decline, Gold might find bids near the $4,620 level. The first major support sits at $4,550, below which the price might slide to $4,500. The main support sits at $4,400. Any more losses might call for a test of at $4,320 or even $4,200 in the coming days.

Looking at WTI Crude Oil, the price recovered above $65.00 before the bears took a stand near $66.50.

Economic Releases to Watch Today

- Fed's Barkin speech.

- Fed's Bowman speech.