Sample Category Title

NZD/USD in range awaits upside breakout, as RBNZ outlook holds after job data

NZD/USD is trading steadily in range after New Zealand’s Q4 employment data delivered few surprises for policy expectations. The mixed report offered early hints of stabilization but stopped well short of forcing a rethink at the RBNZ. Interest rate is expected to remain on hold at 2.25% for most of the year.

The next policy move is still expected to be a hike rather than another cut, but timing remains highly uncertain. Whether that comes late in 2026 or slips into early 2027 will depend on how growth, inflation, and labor market slack evolve. For now, it is too early to draw firm conclusions.

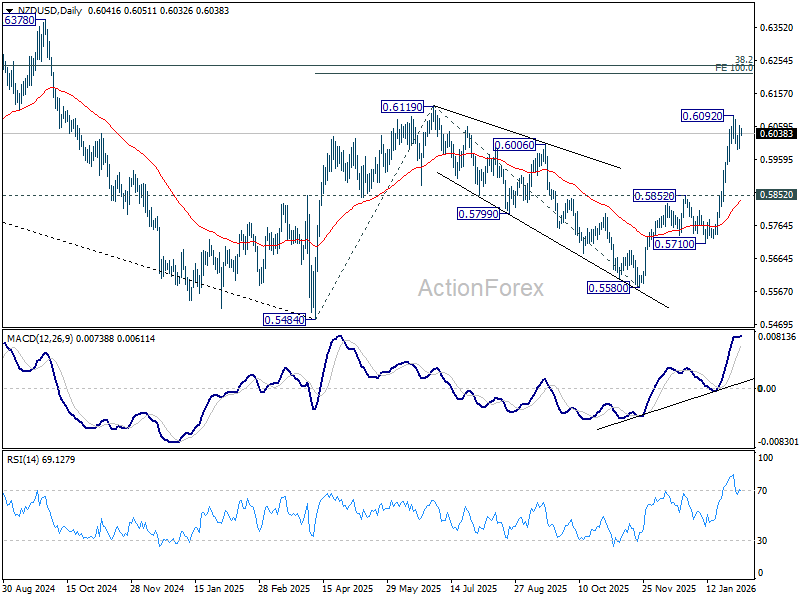

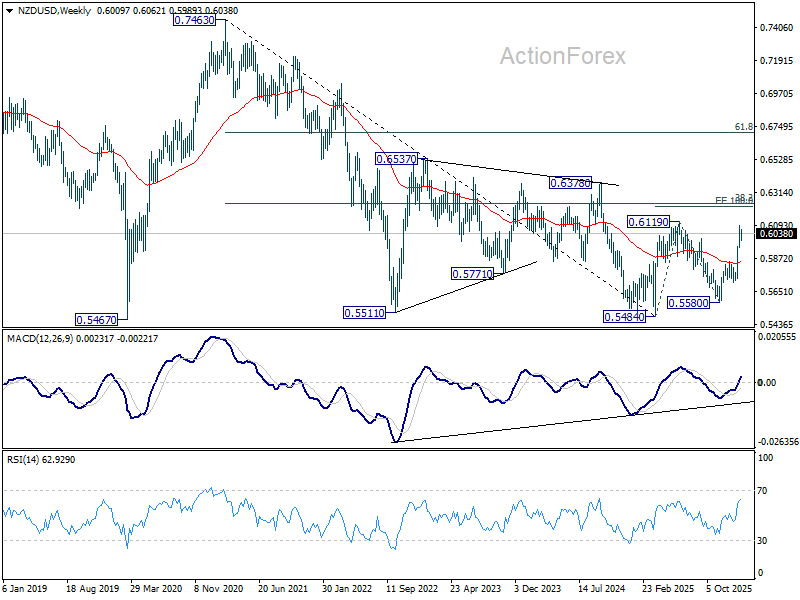

Technically, NZD/USD continues to consolidate below the 0.6092 short-term top. While a deeper pullback cannot be ruled out, downside should be contained well above 0.5852 resistance turned support. Current rise from 0.5580 is seen as the third leg of the pattern from 0.5484 (2025 low). Above 0.6092 should send NZD/USD through 0.6119 (2025 high) to 100% projection of 0.5484 to 0.6119 from 0.5580 at 0.6215.

Longer term, the 0.62 resistance area is decisive. Sitting near 38.2% retracement of 0.7463 (2021) to 0.5484 at 0.6240, it will define whether the recovery from 0.5484 evolves into a broader bullish trend reversal or stalls as a corrective rally within a dominant downtrend.

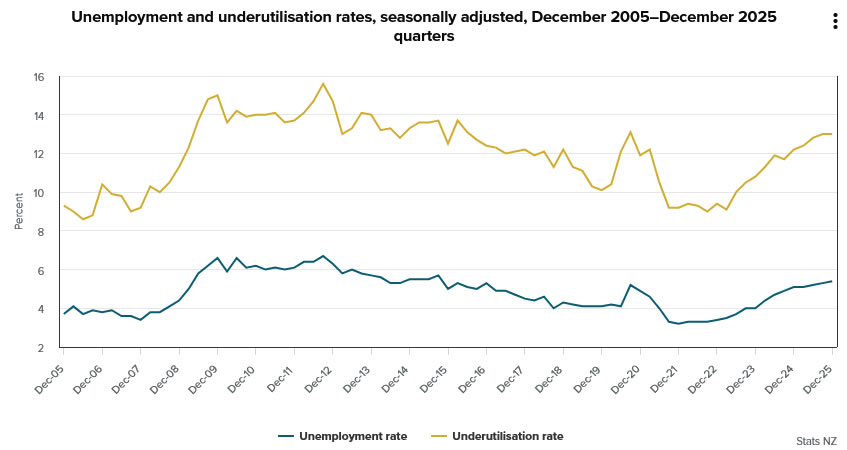

New Zealand jobs grow 0.5% in Q4, unemployment ticks to decade-high

New Zealand’s labor market delivered mixed signals in Q4. Employment rose 0.5% qoq, beating expectations for a 0.3% gain, pointing to continued job creation. Employment rate edged up to 66.7% from 66.6%, reinforcing the view that labor demand remains resilient.

At the same time, unemployment rate climbed to 5.4% from 5.3%, above expectations and the highest since the September 2015 quarter. The rise was accompanied by an increase in the labor force participation rate to 70.5% from 70.3%, suggesting that more people are entering or re-entering the job market, which is adding to slack even as hiring continues.

Wage pressures remained contained. The labor cost index rose 2.0% yoy, with private sector wages up 2.0% and public sector wages up 2.2%. The combination of steady employment growth, rising participation, and moderate wage inflation points to a labor market that is still cooling gradually.

First Impressions: NZ Labour Market Statistics, December Quarter 2025

The unemployment rate ticked up to 5.4% in the December quarter. The details were positive though, with growth in jobs and hours being outstripped by an even larger rise in participation.

- Unemployment rate: 5.4% (prev: 5.3%, Westpac: 5.3%, RBNZ: 5.3%, mkt: 5.3%)

- Employment change: +0.5% (prev: 0.0%, Westpac: +0.3%, RBNZ: +0.2%, mkt: +0.3%)

- Participation rate: 70.5% (prev: 70.3%, Westpac: 70.3%, RBNZ: 70.3%, mkt: 70.3%)

- Labour costs (private sector): +0.5% (prev: +0.4%, Westpac: +0.5%, RBNZ: +0.5%, mkt: +0.5%)

The December quarter labour market surveys showed some early signs of improvement in the jobs market, despite a further small rise in the headline unemployment rate. Wage growth measures remained unsurprisingly subdued at this stage of the cycle.

Overall, we think the results were broadly in line with the Reserve Bank’s forecasts and won’t give them much new to mull over ahead of their 18 February policy review. What that means is there is little here to hurry the RBNZ quickly towards reversing those last 75bp of OCR cuts made after August 2025. Still muted wage pressures should imply there is time to assess the strength and durability of the recovery before raising rates. We remain comfortable with our forecast of a December 2026 first rate hike.

The number of people employed rose by 0.5% for the quarter – actually more than what was suggested by the Monthly Employment Indicator, and ahead of the 0.3% rise in the working-age population. However, there was an even more significant rise in labour force participation from 70.3% to 70.5%, with the net result being an uptick in the unemployment rate. In any case, both of these ‘surprises’ are well with the margin of error for this survey, and we don’t regard them as being meaningfully different from our expectations.

Another positive indicator from the household survey was a 1% rise in hours worked for the quarter, on top of a 1.1% rise in the September quarter. We certainly wouldn’t dismiss this lightly, given that this measure has been an unusually good guide to the swings in quarterly GDP in recent times. However, there was a contrasting 0.5% fall in total hours paid in the business-oriented Quarterly Employment Survey (which had also seen a strong 1.1% rise last quarter).

Given the existing degree of slack in the labour market, wage trends unsurprisingly remained subdued. The Labour Cost Index rose by 0.4% overall for the quarter, with a 0.5% rise in the private sector and a more modest 0.3% rise in the public sector. On an annual basis the LCI rose by 2.0%, its slowest pace since March 2021.

The unadjusted analytical LCI, which includes pay increases that are related to higher productivity, rose by 0.8% for the quarter, slightly more than the 0.7% rise in the September quarter. The annual growth rate slowed from 3.4% to 3.3%, also the lowest reading since March 2021. The distribution of pay rates continues to drift towards annual increases in the 2-3% range, and away from the larger increases that were more common in previous years.

S&P 500 (SPX) Approaches Completion of Elliott Wave Diagonal Pattern

The S&P 500 (SPX) continues to advance as it works toward completing a diagonal Elliott Wave structure that began at the November 21, 2025 low. From that level, wave ((i)) pushed higher and ended at 6986.33. The market then entered wave ((ii)), which unfolded as a clear zigzag. Wave (a) declined to 6885.74, while wave (b) recovered to 6979.34. Wave (c) extended lower and finished at 6788.87, completing wave ((ii)) at a higher degree.

Following this correction, the Index resumed its upward trajectory in wave ((iii)), which progressed toward 7002.28. A pullback in wave ((iv)) later developed and concluded at 6870.8. The structure has since shifted into wave ((v)), which is advancing with an internal subdivision that aligns with an impulsive pattern at the lesser degree. From the wave ((iv)) low, wave (i) rose to 6971.09, and wave (ii) retraced to 6893.48.

The broader bullish outlook remains intact while the pivot at 6788.87 holds. As long as this level stays protected, any pullback is expected to attract buyers within a three‑ or seven‑swing sequence. This behavior supports the potential for further upside as the diagonal structure continues to mature. The overall pattern maintains its integrity and reinforces the view that the Index retains scope for additional strength in the near term.

S&P 500 (SPX) 45 minute chart

SPX Elliott Wave video:

https://www.youtube.com/watch?v=E-XoGIGBp60

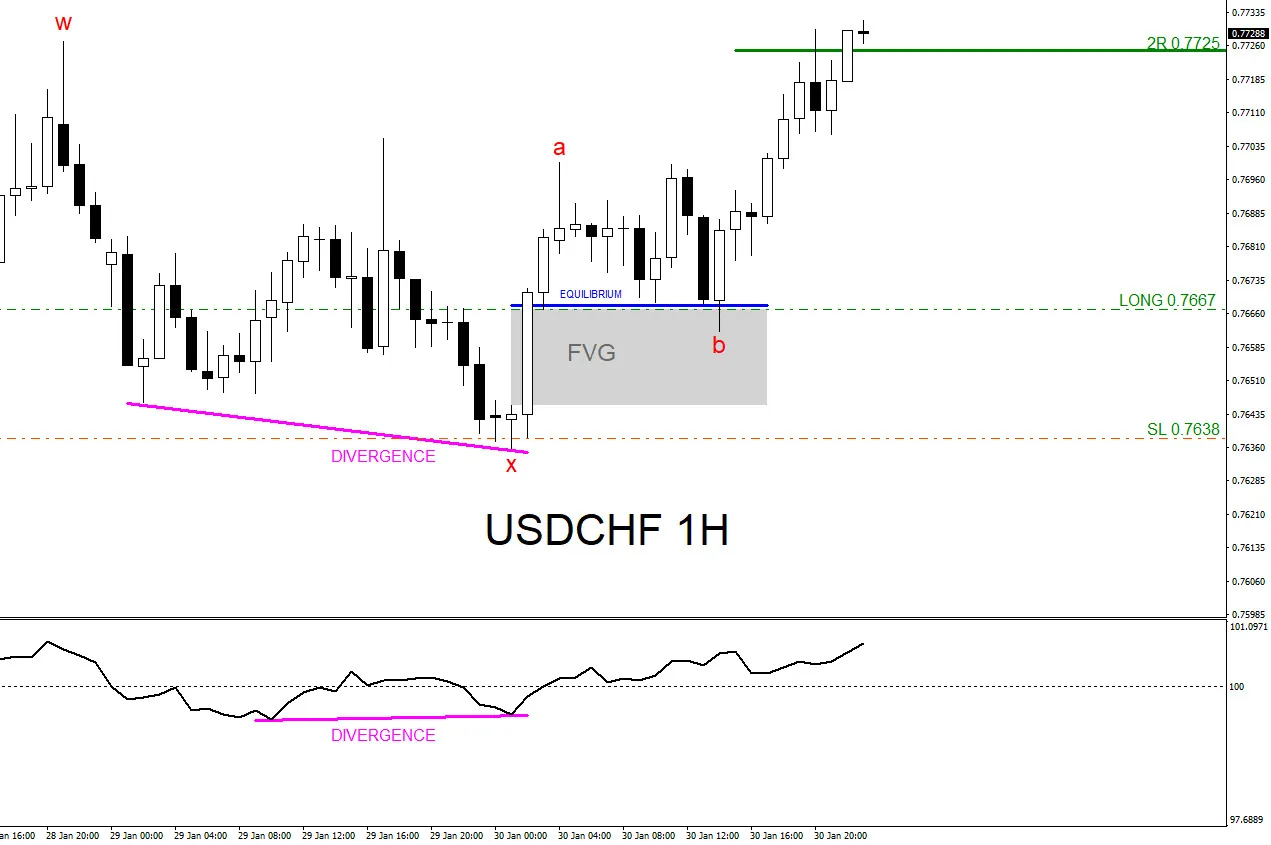

USDCHF Moves Higher as Expected and Hits Targets

On January 30 2026 our clients was expecting for USDCHF to push higher to terminate red wave c, red wave y, blue wave (iv).

The first chart below was published in our private members area and clearly shows the Elliott Wave count was calling for the red wave c push higher.

The second chart is my buy entry. When the USDCHF pair tagged the bullish FVG zone (Gray Box) I entered the buy trade at 0.7667 with a 29 pip stop loss at 0.7638 and a take profit target at the 2R 0.7725.

Added confirmation for the buy entry was the bullish divergence market pattern (Pink) which formed at the red wave x termination.

USDCHF 1 Hour Chart January 30 2026

USDCHF 1 Hour Chart January 30 2026

USDCHF moves higher and hits 2R target at 0.7725 where I closed buy position for +58 pips and a +2% profit gain. (Risking 1% on every trade)

A trader should always have multiple strategies all lined up before entering a trade. Never trade off one simple strategy. When multiple strategies all line up it allows a trader to see a clearer trade setup.

We at EWF never say we are always right. No market service provider can forecast markets with 100% accuracy. Only thing we at EWF 100%, is that we are RIGHT more than we are WRONG.

Of course, like any strategy/technique, there will be times when the strategy/technique fails so proper money/risk management should always be used on every trade.

Hope you enjoyed this article and follow me on social media for updates and questions> @AidanFX

At Elliottwave-Forecast we cover 78 instruments (Forex, Commodities, Indices, Cryptos, Stocks and ETFs) in 4 different time frames and we offer 5 Live Session Webinars everyday. We do Daily Technical Videos, Elliott Wave Trade Setup Videos and we have a 24 Hour Chat Room. Our clients are always in the loop for the next market move.

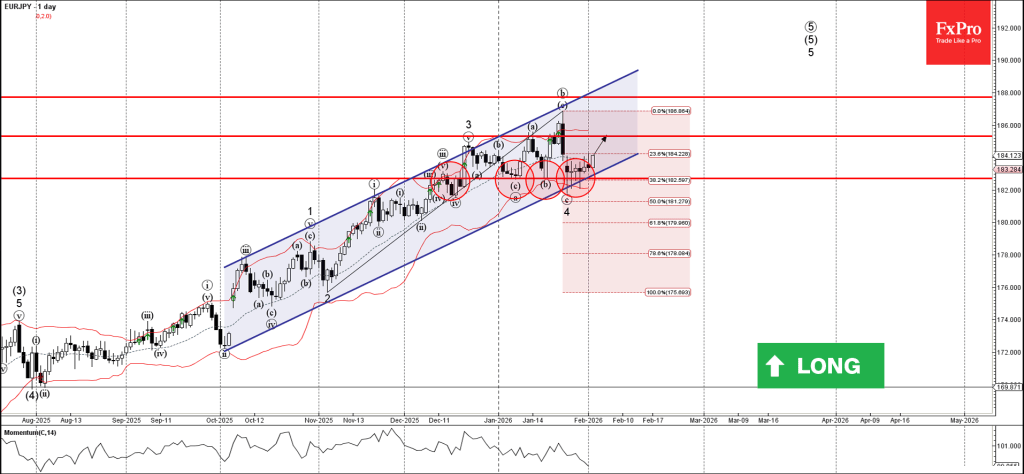

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY reversed from support area

- Likely to rise to resistance level 185.30

EURJPY currency pair recently reversed up from the support area located between the pivotal support level 182.70 (which has been reversing the pair from the start of this year) and the support trendline of the wide daily up channel from October.

The pair made multiple Japanese candlesticks reversal patterns Doji near the support level 182.70 – signalling the strength of this support level.

Given the strong daily uptrend, EURJPY currency pair can be expected to rise in the active impulse wave 5 toward the next resistance level 185.30.

Eco Data 2/4/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Employment Change Q4 | 0.50% | 0.30% | 0.00% | |

| 21:45 | NZD | Unemployment Rate Q4 | 5.40% | 5.30% | 5.30% | |

| 00:30 | JPY | Services PMI Jan F | 53.7 | 53.4 | 53.4 | |

| 01:45 | CNY | RatingDog Services PMI Jan | 52.3 | 52 | 52 | |

| 08:50 | EUR | France Services PMI Jan F | 48.4 | 47.9 | 47.9 | |

| 08:55 | EUR | Germany Services PMI Jan F | 52.4 | 53.3 | 53.3 | |

| 09:00 | EUR | Eurozone Services PMI Jan F | 51.6 | 51.9 | 51.9 | |

| 09:30 | GBP | Services PMI Jan F | 54 | 54.3 | 54.3 | |

| 10:00 | EUR | Eurozone CPI Y/Y Jan P | 1.70% | 1.70% | 1.90% | |

| 10:00 | EUR | Eurozone Core CPI Y/Y Jan P | 2.20% | 2.20% | 2.30% | |

| 10:00 | EUR | Eurozone PPI M/M Dec | -0.30% | 0.30% | 0.50% | 0.70% |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | -2.10% | -2.30% | -1.70% | -1.40% |

| 13:15 | USD | ADP Employment Change Jan | 22K | 48K | 41K | 37K |

| 14:45 | USD | Services PMI Jan F | 52.7 | 52.5 | 52.5 | |

| 15:00 | USD | ISM Services PMI Jan | 53.8 | 53.8 | 54.4 | 53.8 |

| 15:30 | USD | Crude Oil Inventories (Jan 30) | -3.5M | -2.0M | -2.3M |

| 21:45 | NZD |

| Employment Change Q4 | |

| Actual | 0.50% |

| Consensus | 0.30% |

| Previous | 0.00% |

| 21:45 | NZD |

| Unemployment Rate Q4 | |

| Actual | 5.40% |

| Consensus | 5.30% |

| Previous | 5.30% |

| 00:30 | JPY |

| Services PMI Jan F | |

| Actual | 53.7 |

| Consensus | 53.4 |

| Previous | 53.4 |

| 01:45 | CNY |

| RatingDog Services PMI Jan | |

| Actual | 52.3 |

| Consensus | 52 |

| Previous | 52 |

| 08:50 | EUR |

| France Services PMI Jan F | |

| Actual | 48.4 |

| Consensus | 47.9 |

| Previous | 47.9 |

| 08:55 | EUR |

| Germany Services PMI Jan F | |

| Actual | 52.4 |

| Consensus | 53.3 |

| Previous | 53.3 |

| 09:00 | EUR |

| Eurozone Services PMI Jan F | |

| Actual | 51.6 |

| Consensus | 51.9 |

| Previous | 51.9 |

| 09:30 | GBP |

| Services PMI Jan F | |

| Actual | 54 |

| Consensus | 54.3 |

| Previous | 54.3 |

| 10:00 | EUR |

| Eurozone CPI Y/Y Jan P | |

| Actual | 1.70% |

| Consensus | 1.70% |

| Previous | 1.90% |

| 10:00 | EUR |

| Eurozone Core CPI Y/Y Jan P | |

| Actual | 2.20% |

| Consensus | 2.20% |

| Previous | 2.30% |

| 10:00 | EUR |

| Eurozone PPI M/M Dec | |

| Actual | -0.30% |

| Consensus | 0.30% |

| Previous | 0.50% |

| Revised | 0.70% |

| 10:00 | EUR |

| Eurozone PPI Y/Y Dec | |

| Actual | -2.10% |

| Consensus | -2.30% |

| Previous | -1.70% |

| Revised | -1.40% |

| 13:15 | USD |

| ADP Employment Change Jan | |

| Actual | 22K |

| Consensus | 48K |

| Previous | 41K |

| Revised | 37K |

| 14:45 | USD |

| Services PMI Jan F | |

| Actual | 52.7 |

| Consensus | 52.5 |

| Previous | 52.5 |

| 15:00 | USD |

| ISM Services PMI Jan | |

| Actual | 53.8 |

| Consensus | 53.8 |

| Previous | 54.4 |

| Revised | 53.8 |

| 15:30 | USD |

| Crude Oil Inventories (Jan 30) | |

| Actual | -3.5M |

| Consensus | -2.0M |

| Previous | -2.3M |

WTI Oil: Double Failure at Key Support Zone

WTI oil extended pullback from new multi-month high ($66.46) in early Tuesday’s trading, following gap-lower opening at the start of the week and over 4% drop on Monday which marks the biggest daily loss since Nov 11.

Signals of de-escalation in US-Iran tensions eased supply fears and prompted strong selling, along with firmer dollar.

Although Tuesday’s fresh extension lower pointed to rising risk of deeper correction of $54.87/$66.46 recovery leg, some technical signals will be still required to verify the action.

A double attempt through key supports at $62.21/03 (200DMA/Fibo 38.2% of $54.87/$66.46) has so far been repeatedly rejected which develops signal of healthy correction before larger bulls regain control.

The notion is supported by a double bear-trap under 200DMA, multiple MA bull-crosses and positive momentum studies.

Repeated close above 200DMA to generate initial bullish signal, with extension above $64.00 zone needed to boost the structure for attempts to fill Monday’s gap and open way for retest of key barriers at $66.40/46 (tops of Sep 26/Jan 29) and confirm reversal.

Res: 63.00; 63.72; 64.00; 64.66.

Sup: 62.50; 52.21; 62.03; 61.10.

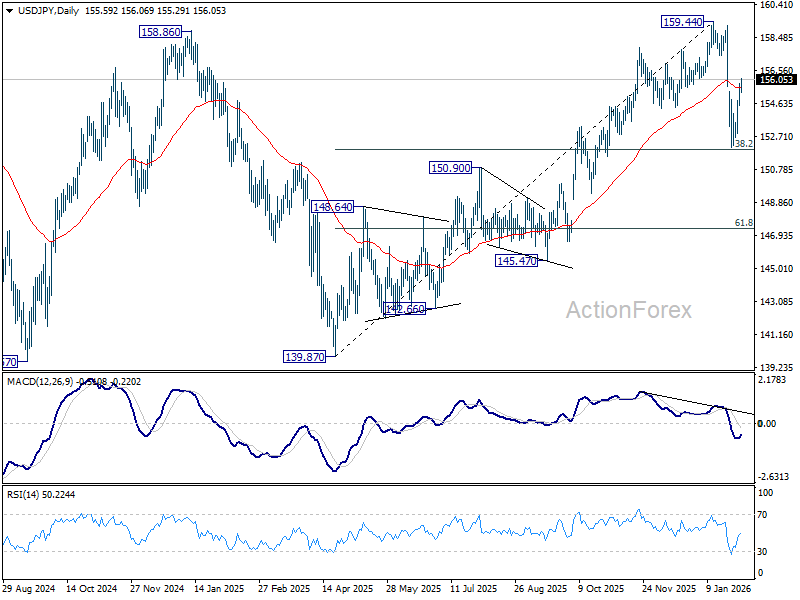

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.84; (P) 155.32; (R1) 156.08; More...

No change in USD/JPY's outlook and intraday bias stays on the upside. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Further rebound should be seen to retest 159.44 next. On the downside, below 154.53 minor support will turn intraday bias neutral first. Sustained break of 38.2% retracement of 139.87 to 159.44 at 151.96 will argue that it is reversing whole rise from 139.87.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.59) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

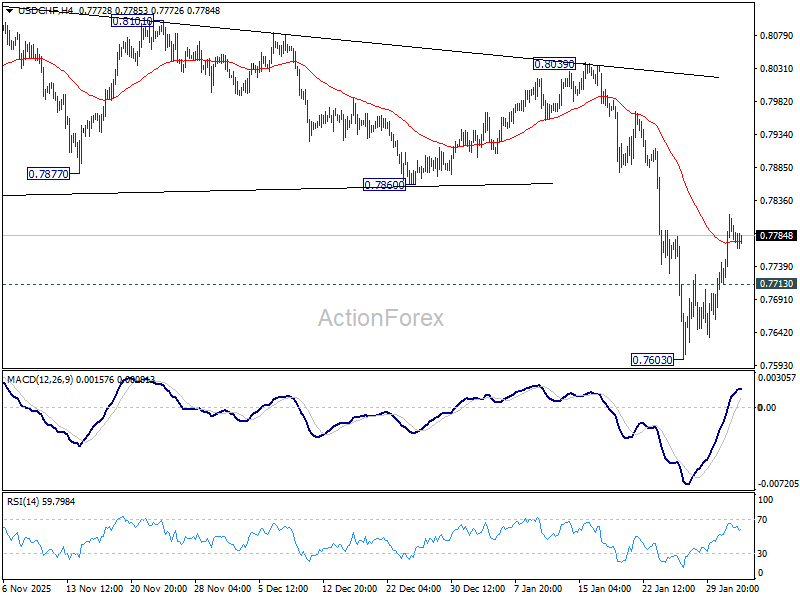

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7736; (P) 0.7777; (R1) 0.7839; More….

USD/CHF's rebound from 0.7603 short term bottom is still in progress. Intraday bias stays mildly on the upside for 55 D EMA (now at 0.7912). On the downside, below 0.7713 minor support will bring retest of 0.7603. Firm break there will resume larger down trend to 0.7382 projection level next.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8166) holds.